Search News Results

Intergovernmental Group of Twenty-Four on International Monetary Affairs and Development: Communiqué – 2016 Spring Meetings

Communiqué of the Ministers of the Intergovernmental Group of Twenty-Four, held in Washington, D.C. on April 14, 2016

1. We, the Intergovernmental Group of Twenty-Four on International Monetary Affairs and Development, held our ninety-fifth meeting in Washington D.C. on April 14, 2016 with Mauricio Cárdenas, Minister of Finance and Public Credit of Colombia in the Chair, Abdulaziz Mohammed, Minister of Finance and Economic Cooperation of Ethiopia as First Vice-Chair; and Ravi Karunanayake, Minister of Finance of Sri Lanka as Second Vice-Chair.

2. We congratulate Ms. Christine Lagarde on her appointment for a second term as Managing Director of the IMF.

The Global Economy and the International Monetary System

3. The recovery of the global economy remains modest, with greater downside risks. Growth in advanced economies remains sluggish, while it is moderating in emerging markets and developing countries (EMDCs), which still account for the bulk of global growth. The sharp drop in commodity prices has not materialized in positive effects globally, as has been expected, as we continue to face weaker global demand, tighter financial conditions, more volatile capital flows, and heightened security challenges. These headwinds could further weaken our growth outlook and contribution to global growth.

4. In light of this global reality, managing our policy space, making our economies more resilient to support macroeconomic stability, as well as achieving higher, more balanced and inclusive growth remain our priorities. Exchange rate flexibility, where appropriate, and reserve buffers, where available, could contribute to cushioning the impact of external shocks. We will continue to strengthen our fiscal and structural reforms and our financial systems, based on country-specific priorities, to diversify our economies and enhance our growth prospects, promote employment, competition, and productivity, while implementing macroeconomic and social policies to address inequality and alleviate poverty.

5. We welcome the IMF’s ongoing work towards strengthening the International Monetary System (IMS) with efforts in three key areas: mechanisms for crisis prevention and adjustment; global cooperation on issues and policies affecting global stability, including spillover effects from systemic economies; and a large enough and more coherent Global Financial Safety Net (GFSN). We also support the IMF’s review of the GFSN, including the adequacy of the IMF resources and its lending toolkit, and look forward to concrete follow-up steps. In this regard, we reiterate our call for predictable and adequate liquidity support in times of need. We note the potential for greater and more effective cooperation between the different layers of the GFSN, especially between the Fund and regional financing arrangements (RFAs). We also call for further work from the IMF and other International Financial Institutions (IFIs) on mechanisms to support countries coping with the sharp drop in commodity prices. We welcome the inclusion of the renminbi in the SDR basket. We look forward to the discussion on possible allocation of SDRs and support further work to examine the broadening of SDR use in the IMS.

6. We support the continued reform of global financial regulation and the strengthening of the anti-money laundering and combating the financing of terrorism (AML/CFT) framework, but highlight the need to address their unintended consequences. In this regard, we call on the IMF, the World Bank and global financial regulators, to develop concrete measures to address the decline of correspondent banking, as a result of de-risking by global banks, in order to mitigate financial exclusion. This phenomenon, which could adversely impact the functioning of the financial system of affected countries, further constrains access to credit and other financial services, including remittance transfers.

7. To facilitate timely and orderly debt restructuring, we support the IMF’s continued efforts to promote the use of strengthened pari passu and collective action clauses in sovereign bond issues. We take note of the large outstanding stock of sovereign debt that does not include these provisions, and support more work to explore solutions to address potential holdout problems for such debt. At the same time, we welcome Argentina’s efforts to end a decade long dispute with holdout creditors to regain access to international capital markets.

8. We continue to call for support, including through additional non-IDA concessional financing, from IFIs for developing countries disproportionately affected by the refugee and security crises, as well as by internally displaced populations. These countries are providing a global public good by hosting those that are forcibly displaced. We welcome the MENA Concessional Financing Facility and other initiatives of the World Bank Group (WBG), and call for a mainstreaming of such instruments in supporting other middle-income countries in such fragile situations, in partnership with others. We also call for IFIs to strengthen their attention on the impact of migration, including those that occur for economic reasons.

Financing for Development

9. We reiterate the importance of the 2030 Agenda for Sustainable Development and the Addis Ababa Action Agenda. We welcome the Paris Agreement that sets out our global, shared responsibility to deliver on the climate and development agenda, while respecting the principle of common but differentiated responsibilities. The availability of concessional finance will play a key role in lowering the up-front costs of greenhouse gas emissions, climate-resilient investments as well as in mitigating the risks related to climate change. We look forward to a concrete roadmap from developed economies toward providing USD 100 billion per year by 2020 to support mitigation and adaptation in developing countries and strong advocacy by the MDBs in this regard. We also seek the urgent replenishment of the Climate Investments Funds. We continue to urge the international community to work with small middle-income countries and those in fragile situations that are vulnerable to climate change, in improving their debt sustainability, including through enhancing their access to concessional financing. We look forward to the successful outcomes of the 22nd Session of the Conference of the Parties (COP) to be held in Marrakech, Morocco later this year.

10. Multilateral Development Banks (MDBs) should emerge as a strong partner for developing countries in Disaster Risk Management (DRM) to enable them to achieve the Sendai Framework targets by 2030. We call for MDBs to increase financial support to developing countries and facilitate their access to new technologies. Overall, continuous work on DRM will prevent disasters from undermining the progress towards achieving the Sustainable Development Goals (SDGs).

11. Adequately and appropriately scaling up quality investments in sustainable infrastructure will be particularly critical to delivering the development, climate and economic growth agenda. In addition to mobilizing our domestic resources through financial deepening, we call for scaled-up support from MDBs through strengthening policy and institutional frameworks, increasing lending, and effective leveraging of private sector resources. We note the ongoing efforts by MDBs to optimize the use of their own balance sheets, while promoting dialogue with credit rating agencies to foster more appropriate methodologies in assessing the MDBs’ financial strength. We welcome the forthcoming inaugural global infrastructure forum. We call for further and productive dialogue towards ensuring the adequate capitalization of MDBs.

12. Effective international tax cooperation is an essential complement to our efforts to mobilize domestic resources. We strongly support the participation of developing countries on an equal footing in the widespread and consistent implementation of outcomes of the G20/OECD Base Erosion and Profit Shifting (BEPS) Project. We welcome the joint initiative of the IMF and the WBG on capacity building on tax administration and call for delineating concrete steps on how they can support enhancing the participation and voice of developing countries on international tax issues. Furthermore, we urge the IMF and the WBG to strengthen their support to combat illicit financing flows.

13. Concessional finance will continue to be a vital source of financing in low-income countries (LICs). We welcome the advancement of innovations under IDA18 to leverage financing flows across all sources of finance. We stress, however, that as IDA integrates non-concessional finance among its instruments, it should ensure adequate targeted concessional resources for the poorest and most vulnerable clients, and guard against burdening them with higher cost liabilities. These resources should be additional, rather than substitute for contributions from development partners in the light of ambitious global agreements on SDGs, COP21, and the Sendai Agreement. We call on the IMF to step up efforts to mobilize additional resources for the Poverty Reduction and Growth Trust (PRGT) and to allow more flexibility in accessing General Resources Account (GRA) resources by eligible LICs. More broadly, we ask for further strengthening of the IFIs’ engagement with and support for fragile and conflict affected countries, especially by enhancing institutional capacities and providing financial support towards higher resilience. We call on advanced countries to fulfill their commitments to Official Development Assistance (ODA). We look forward to increased donor contributions to IDA18.

Governance and Reform of International Financial Institutions

14. We welcome the entry into force of the 2010 Quota and Governance Reforms of the IMF that have made progress in shifting the distribution of quota shares to EMDCs, and note that there is still a long way to go in this respect. We call for the full implementation of the 2010 governance reforms, including those on Board representation. We look forward to the completion of the 15thGeneral Review of Quotas by the Annual Meetings in 2017, and to a new quota formula that further shifts quota shares to EMDCs while protecting the quota share of the poorest countries. The realignment of quotas must reflect the rapidly growing weight of EMDCs in the global economy, and this must not come at the expense of other EMDCs. We call for putting greater weight to GDP measured in Purchasing Power Parity (PPP) in determining the economic weight of countries. We express our strong and continued support for a quota-based and adequately resourced IMF. We reiterate our longstanding call for a third Chair for Sub-Saharan Africa in the IMF Executive Board, provided it does not come at the expense of other EMDCs’ Chairs.

15. We call for a World Bank’s shareholding reform process that reflects its original and overarching goal, as established in the Istanbul Principles: to enhance the voice and representation of Developing and Transition Countries for strengthening the legitimacy and effectiveness of the Bank. In this regard, we call for a World Bank’s shareholding review that meaningfully increases the voting power of developing countries and moves toward equitable voting power, while also protecting the voting power of the smallest poor countries. Economic weight should be the primary component of the new formula with as much weight on this component as possible. In addition, we ask that greater weight be given to the GDP PPP in determining the economic weight of countries in the formula. We caution against regressive outcomes that could compromise the gains from previous reforms and look forward to an agreement on the dynamic formula by the 2016 Annual Meetings and consideration of Selective Capital Increase and General Capital Increase, by the Annual Meetings of 2017. We also call upon the World Bank to strengthen the pillar of Representation in its Board of Executive Directors in the voice reform process.

16. We look forward to an implementable, simple, transparent, and predictable Environmental and Social Safeguards Framework of the World Bank that gives a greater role to the use of country systems and does not impose undue burden in terms of cost and time on borrower countries, maintaining the primacy of their development objectives. We call on the World Bank to allocate budgetary resources necessary to strengthen countries’ capacity to implement the new Framework.

17. Finally, we reiterate our call for strengthening the ongoing efforts towards greater representation by nationals from under-represented regions and countries in the form of recruitment and career progression to achieve balanced regional and gender representation, including at managerial levels, in the WBG and the IMF.

Other Matters

18. The next meeting of the G-24 Ministers is expected to take place on October 6, 2016 in Washington, D.C.

Related News

The future of food: Why healthy, safe and sustainable food is a basic necessity

“We need to look afresh at agriculture in Africa as a series of systems, and to see it not as a way of life, but a business”, said African Development Bank Acting Vice-President for Operations, Kapil Kapoor, at a World Bank Spring Meetings panel on ‘The Future of Food’ on Wednesday. But the challenges of food and agriculture are global: while 2 billion people in the world are undernourished, 2 billion are obese or overweight. The world wastes one-third of the food it produces.

The paradoxes continue: “How is it,” asked Kapoor, “that the continent with two-thirds of the world’s arable land and plentiful water resources, struggles to feed its own people – to the extent that it imports US $35 billion of food a year – and creates so little agricultural produce?” Speaking on behalf of Bank Group President Akinwumi Adesina, the former Nigerian Minister of Agriculture, he announced the imminent unveiling of a continent-wide strategy to ‘Feed Africa’, which will be shared with African and international audiences alike at the Bank’s Annual Meetings in Lusaka from May 23, 2016.

“The strategy is in part the result of new and holistic thinking among our partners in government”, he said. “Last October, in Dakar, the Bank convened a ‘Feed Africa’ conference which brought together Ministers of Agriculture, Finance and Health in an almost unprecedented move to see agriculture across all its component parts, at the nexus of health, economic growth, and a sustainable planet. The goal is nothing if not ambitious: we believe that by 2025 the continent of Africa can be a net exporter, not an importer, of food.”

Kapoor set out a number of the challenges, not least those of the different political economies of different countries in Africa, and of poorer countries which are not ready to debate the diversification of the food supply, until they have the basics of food supply guaranteed. He charted the contrasts of African food poverty and a growing African middle class with aspirations about food, as about other aspects of life. He stressed the role of partnership in transforming African agriculture. “We have found a huge matrix of players in agriculture in Africa, but little coordination. And the role of the private sector is key: every conversation we have with governments is essentially a conversation with and about the role of the private sector. It is the private sector which will bring about change.”

The event was moderated by former White House chef and now NBC TV food analyst chef Sam Kass, who in September 2015 served a meal made from food waste to Heads of Governments meeting at the UN in New York, as they discussed common approaches to the COP21 climate change summit in Paris three months later. “Food is the ultimate expression of who we are and where we are from”, he said. “We cannot ignore its cultural aspects.”

Other panelists were Juan José Freijo, Consumer Goods Forum and Global Head of Sustainability, Brambles; Bonnie McClafferty, Director, Global Alliance for Improved Nutrition; Johan Rockström, Co-Founder, EAT Initiative, and Juergen Voegele, Senior Director, Agriculture Global Practice, World Bank.

Voegele vocalised many of the challenges of the sector. “The agriculture sector is way behind the curve”, he said, “while for instance the energy sector has invested in research and debate, and found solutions, like renewable energy. Agriculture has simply not had these conversations, and when the leading agriculture research agency CGIAR has a research budget of less than US $1 billion a year, no wonder we are behind. We need an agricultural sector that is productive, resilient, and low-imprint. Every country needs to think through its own agriculture journey... but we can collectively help countries align around certain key principles and priorities.”

Related News

tralac’s Daily News Selection

The selection: Thursday, 14 April 2016

Starting today:

In Mauritius: the inaugural African Economic Platform

Announced by the Chairperson of the AU Commission, Dr Nkosazana Dlamini Zuma, during the just-concluded 26th AU Summit of Heads of State and Government, the AEP will contribute to fast track African economic transformation toward the realisation of Africa’s Agenda 2063. The participants expected to attend this first African Economic Platform will come from the public sector, led by Heads of State and Government; the African private sector, led by captains of commerce and industry, and the African higher education sector. This is a strategic approach by the African Union to bring together these three sectors to engage in discussions on cooperation and collaboration deemed to be critical for the continent’s growth and tangible economic transformation. [Concept paper]

In Lusaka: the Commonwealth's Africa trade prospects consultation

Next week:

On Tuesday, in London: hearings for the UK’s Africa Free Trade Initiative inquiry

This inquiry seeks to answer the following three main questions: i) What has been achieved in AFTi since 2011 and what lessons can be learned? ii) Is there a case for a successor to AFTi in the area of further facilitating trade and investment within Africa as a driver of growth and poverty reduction, and between African and the rest of the world, including the UK? iii) What should a future AFTi look like, what targets should it seek to achieve, and through which means and partnerships should it be delivered?

On Tuesday, in Midrand: a briefing on SADC certificates of origin and the new VAT rules

Roberto Azevêdo: 'Embracing change: forging global trade partnerships' (WTO)

Empirical evidence suggests that the deeper the RTA, the greater the potential for the development of production chains which span national borders. WTO members in the Asia-Pacific region in particular have greatly benefited from these global value chains. As production networks expand and regional and global value chains become more important, it becomes critical to more rapidly harmonize differences in legislation, rules and infrastructure, which impact international trade and investment. This appears to be what we see occurring more and more in modern RTAs and other regional networks.

Southern African Business Forum: launch of regional working groups (The Herald)

Following the launch [yesterday in Johannesburg] Gainmore Zanamwe, Regional Trade Adviser at the SADC Secretariat, said: “Both the Revised RISDP and the SADC Industrialisation Strategy call for the development of a Regional Private Sector Partnership and Collaboration Strategy and the establishment of a platform for the Public-Private Dialogue to improve the involvement of private sector in regional integration. To this end, the SADC Secretariat and Member States will be working with the regional public and private sector as they collaborate under the SABF’s six Regional Working Groups, which include Industrialisation and Regional Value Chains, Transport Corridors, Trade Facilitation, Movement of Services and Skills, Water and Energy.”

After their official launch, the SABF Working Groups begin their work in earnest, including establishing a work programme for the next year. Decisions and plans will vary from group to group, focusing on a range of activities from policy interventions and public-private co-operation geared at policy reform. Other groups may focus on the development of elements of regional infrastructure projects. The next major milestone is the 2nd Annual SABF Conference on the margins of the SADC Heads of State Summit in Swaziland, where progress reports from the six Working Groups will be presented. [SADC moves on industrialisation of region]

Botswana: Businesses ill-informed about EU trade prospects – envoy (Mmegi)

Many Botswana businesses are unaware of how to export to the European Union, a trade official said at a recent journalists’ seminar on EU cooperation. John Taylor, who is the trade officer for the EU delegation in Botswana, also said local businesses do not know how to take advantage of the EU trade benefits. “When I came here to talk about trade and interact with the trading community and administration, I was shocked. What we heard was about the wonderful opportunities with China and the US,” he said.

Kenya: Maize exports to Tanzania rise on high prices (Business Daily Africa)

Latest market data indicates that 145 tonnes of maize have been shipped to Tanzania through Isebania border in the last 30 days alone as farmers seek better prices in the regional market. Data prepared by the Regional Agricultural Trade Intelligence Network (Ratin) shows that a 90-kg bag of maize currently retails at Sh4,898 in Dar es Salaam, the highest unit price in East Africa.

International regulatory cooperation and domestic regulatory coherence: this week's tralac Newsletter

Public interest considerations behind SAB merger delay (IOL)

Public interest considerations of the planned merger between the world’s largest brewer Anheuser-Busch (AB) InBev and fellow brewing company SABMiller appear to be behind the delay in the Competition Commission’s assessment of the transaction, according to competition law analysts. AB InBev has agreed to an extension to May 5, after the commission missed Tuesday’s deadline. It had also missed its previous deadline of April 5. [Patel ‘hijacking’ cartel watchdog’s powers]

Mihe Gaomab II: ‘NACC guarding against future medical costs in Namibia' (Namibian Competition Commission)

The Commission opposed this application. NAMAF’s application was argued in the High Court on 26 November 2015. On the 18th March 2016, through a landmark judgement which solidified the precedence of the competition law on jurisdiction of all undertakings in Namibia, the High Court squashed NAMAF and the medical aid fund’s application and profoundly agreed with the Commission’s arguments by ruling that NAMAF and medical aid funds are subject to the jurisdiction of the Competition Act. This means that the Commission has regard to the ways and means of how NAMAF has conducted its modus operandi especially on how they set the medical tariffs. Following this judgment, the Commission intends to now file its application interdicting NAMAF and the Funds from engaging in the unlawful conduct and to seek further appropriate redress mechanisms.

COMESA: EOI for consultancy services for baseline study to assess industrial research and development, technology and innovation capacities (AfDB)

Specifically, the study aims at assessing the capacities, state infrastructure for industrial R&D and technology, and associated systems of innovation with a view to generate recommendations on appropriate areas of tripartite intervention to improve capacities, and strengthen Industrial R&D infrastructure and associated systems of innovation in the tripartite countries.

The Second IORA Economic and Business Conference concluded yesterday in Dubai: an Indian perspective

Migration and Development Brief 26: recent developments and outlook (World Bank)

Remittances to developing countries grew only marginally in 2015, as weak oil prices and other factors strained the earnings of international migrants and their ability to send money home to their families, says the World Bank’s latest edition of the Migration and Development Brief, released today. Officially recorded remittances to developing countries amounted to $431.6bn in 2015, an increase of 0.4% over $430bn in 2014. The growth pace in 2015 was the slowest since the global financial crisis. Global remittances, which include those to high-income countries, contracted by 1.7% to $581.6bn in 2015, from $592bn in 2014.

The estimated 1% rise in remittances to Sub-Saharan Africa in 2015 represents some recovery from the 0.2% rise in 2014. Remittances to Nigeria, accounting for around two-thirds of total remittance inflows to the region, are estimated to have declined by 0.8% to $20.7%, and remittances to South Africa are estimated to have fallen by 5.2% to $0.9bn. Regional growth in remittances in 2015 was largely driven by strong remittance growth in Kenya (8.3% to $1.6bn) and Uganda (21.1% to $1.1bn). Remittance flows to the region are projected to rise by 3.4 and 3.7% in 2016 and 2017, respectively.

Independent power projects in sub-Saharan Africa: lessons from five key countries (World Bank)

The five case study countries, namely Kenya, Nigeria, South Africa, Tanzania, and Uganda were selected because they present the largest and most diversified experience with independent power projects over the longest time period. The primary objective of this study is to evaluate the experience of IPPs in Sub-Saharan Africa and explore how they may be improved. Lessons from past experiences and a review of best practices from the region and from around the world can greatly help countries attract more and better IPPs. [The authors: Anton Eberhard, Katharine Gratwick, Elvira Morella, Pedro Antmann]

Natural resource revenues and public investment in resource-rich economies in sub-Saharan Africa (UNU-WIDER)

Using panel data for the period 1990–2013, we find in line with the scaling-up hypothesis that resource rents significantly increase public investment in SSA and that this tends to depend on the quality of political institutions. We also find evidence of a positive effect of public investment on economic growth, which also depends on the level of resource rents. Using some of the components of public investment, such as health and education expenditure, we find a negative effect of resource rents, suggesting among other things that public spending of resource rents is directed more to other infrastructure investments.

World Bank, AIIB sign first co-financing framework agreement (World Bank)

The agreement outlines the co-financing parameters of World Bank-AIIB investment projects, and paves the way for the two institutions to jointly develop projects this year. In 2016, the AIIB expects to approve about $1.2 billion in financing, with World Bank joint projects anticipated to account for a sizable share. The World Bank and the AIIB are currently discussing nearly one dozen co-financed projects in sectors that include transport, water and energy in Central Asia, South Asia and East Asia. Under the agreement, the World Bank will prepare and supervise the co-financed projects in accordance with its policies and procedures in areas like procurement, environment and social safeguards.

Quantifying the effects of trade liberalisation in Brazil: a CGE model simulation (OECD)

Brazil remains a fairly closed economy, with small trade flows relative to its share of world income. This paper explores the effects of three possible policy reforms to strengthen Brazil’s integration into global trade: a reduction in import tariffs, less local content requirements and a full zero-rating of exports in indirect taxes. A simulation analysis using the OECD Multi-Region Trade CGE model suggests that current policies are holding back exports, production and investment in Brazil. The model simulations suggest significant scope for trade policy reforms to strengthen industrial development and export competitiveness. Results also show that the expansion of investment and production would be accompanied by significant employment gains.

AfDB President strengthens alliances in South Africa

Mozambique plans to raise US$1bn a year for roads and bridges (Club of Mozambique)

André Thomashausen: 'How Mozambique subsidizes South Africa' (Club of Mozambique)

Regional experts meet towards actualisation of Dakar-Abidjan Corridor Highway (ECOWAS)

Senegal truckers tired of taking the long way around The Gambia (BBC)

On ECOWAS road transit (editorial comment, The Daily Observer)

Strong US$ affects Zim exports (The Herald)

China moves on $4 bln Ethiopian export project (Natural Gas Daily)

UNCTAD's latest Transport Newsletter

WTO: India opposes US, EU bid to hold small-group talks (The Hindu)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

NACC guarding against future medical costs in Namibia

Almost two years ago, the Commission concluded its investigations against NAMAF and 10 Medical Aid Funds in which it found that NAMAF and its fund members contravened the competition law and does price fixing of medical tariffs in Namibia.

Shortly after the Commission’s decision was published in the government Gazette, NAMAF and the Funds brought an application before Court wherein they contest the Commission’s jurisdiction on the basis that neither NAMAF, nor the Funds could satisfy the definition of an ‘undertaking’ as defined in the Competition Act.

The Commission opposed this application. NAMAF’s application was argued in the High Court on 26 November 2015. On the 18th March 2016, through a landmark judgement which solidified the precedence of the competition law on jurisdiction of all undertakings in Namibia, the High Court squashed NAMAF and the medical aid fund’s application and profoundly agreed with the Commission’s arguments by ruling that NAMAF and medical aid funds are subject to the jurisdiction of the Competition Act (see an earlier article here).

This means that the Commission has regard to the ways and means of how NAMAF has conducted its modus operandi especially on how they set the medical tariffs.

Following this judgment, the Commission intends to now file its application interdicting NAMAF and the Funds from engaging in the unlawful conduct and to seek further appropriate redress mechanisms.

It is an anecdotal fact that medical costs forms a significant consumption behaviour of both the rich and the poor. Hence the Commission will guard cautiously against any implications of the landmark judgement in Namibia.

The experience of the neighbouring country, South Africa had the Competition Commission of South Africa ruling in 2014 wherein the decision was made to have a free fall of medical tariff setting by medical aids, doctors, private medical practitioners, hospitals, clinics etc. This had the effect of the cost of the services being disproportionate and excessive and that despite the protection that medical aid schemes are meant to provide, the consumer making use of medical arrived end up significantly paying more and consumptively poorer whenever there was access to private healthcare.

This means that consumers in South Africa are increasingly paying more for the excess even in presence of the medical aid referred to as medical cover gaps. In the last few years, research shows that there have been something like over 250,000 gap cover schemes that have emerged in South Africa.

This has prompted the Competition Commission’s to do an inquiry in South Africa in 2015 to address the problem of the pricing of private healthcare in South Africa. The South African Government over the last 15 years has also taken some steps to attempt to regulate price of medicine, price of healthcare services, etc due to the vision and resilience of the Minister of Health in that country.

It is crucially important that Namibia does not fall into a “price increase trap” of higher medical costs on Namibia, as it will obviate consumer protection and put medical costs out of reach especially for the poor and the middle class.

It is the Commissions view that on a post high court judgement basis of seeking redress mechanisms that the Commission through a consultative and engaged process with Ministries of Finance and Industrialisation, Trade and SME Development and most importantly the Ministry of Health and NAMFISA to assist in setting in place certain institutions and mechanisms to control the price of medicines by regulation as, of course, medicines is a very key component of healthcare.

This would promote greater transparency, clarity, and balanced representation of all actors in the Health Sector of Namibia and set about what healthcare services actually cost and the composition of health care costs and its formation in general in the Health sector.

The Commission is assured that there will also be greater access to health care costing and healthcare provision with both the consumer, government and private practitioners having managed access to that information which allows a system that allows reasonable regulation of prices to the benefit of all of us.

And in the context of National Health Insurance which as we all know it is the government’s grand plan for universal access to healthcare services through the Social Security Commission. And for overcoming some of the costing, tariff setting and financing problems, the issue of both the public and private healthcare sectors has to be addressed on uniform and coherent basis.

The Competition Commission Aims to consult broadly to gain consumer, economic, social and political will with to regard to the regulatory dispensation and aims to engage with the private healthcare companies on a post competition law due process to ensure this is effected.

The Commission aims to fulfill the Nation's constitutional obligation that states generally that everyone has a right of access to healthcare services in Namibia because good health is fundamental to good life and contributes to fair economic, political and social justice in the country.

Mihe Gaomab II is the CEO of the Namibian Competition Commission.

This article will appear in the April 2016 issue of Consumer News Magazine, Namibia.

Related News

Independent power projects in Sub-Saharan Africa: lessons from five key countries

The track record of Sub-Saharan Africa’s power sector is dismal. Two out of three households in Sub-Saharan Africa, close to 600 million people, have no electricity connection. Most countries in the region have pitifully low access rates, including rural areas that are the world’s most underserved. In some countries, less than 5 percent of the rural population has access to electricity.

Chronic power shortages are a primary reason. The region simply does not generate enough electricity. The Republic of Korea alone generates as much electricity as all of Sub-Saharan Africa. Across the region, per capita installed generation capacity is barely one-tenth that of Latin America.

The need for large investments in power generation capacity is obvious, especially in the face of robust economic growth on the continent, which has been the key driver of electricity demand over the last decade. The International Energy Agency predicts that the demand for electricity in Sub-Saharan Africa will increase at a compound average annual growth rate of 4.6 percent, and by 2030 it will be more than double the current electricity production. The World Bank estimated in 2011 that Sub-Saharan Africa needed to add approximately 8 gigawatts (GW) of new generation capacity each year through 2015 (Eberhard and others 2011). But, in fact, over the last decade an average of only 1-2 GW has been added annually.

The cost of addressing the needs of Sub-Saharan Africa’s power sector has been estimated at US$40.8 billion a year, which is equivalent to 6.35 percent of Africa’s gross domestic product (GDP). The existing funding is far below what is needed. This large funding gap cannot be bridged by the public sector alone. Private participation is critical. Historically, most private sector financing has been channeled through independent power projects (IPPs). IPPs are defined as power projects that mainly are privately developed, constructed, operated, and owned; have a significant proportion of private finance; and have long-term power purchase agreements (PPAs) with a utility or another off-taker.

Like any other private investment, IPPs will not materialize in the absence of a suitable enabling environment. The primary objective of this study is to evaluate the experience of IPPs and see what is necessary to maximize their contribution to mitigating Sub-Saharan Africa’s electric power woes.

Investment in Power Generation in Sub-Saharan Africa: An Overview

Current Power Generation Systems in Sub-Saharan Africa

In 2012, the 48 countries of Sub-Saharan Africa had a total grid-connected power generation capacity of only 83 GW. South Africa accounts for over half of this total. The remaining Sub-Saharan African countries have a combined capacity of only 36 GW, and just 13 of these countries have power systems larger than 1 GW. Twenty-seven countries have grid-connected power systems smaller than 500 megawatts (MW), and 14 have systems smaller than 100 MW.

Across Sub-Saharan Africa (excluding South Africa, which uses mostly coal), hydropower contributes just over half the capacity. Fossil fuels, primarily natural gas and diesel or heavy fuel oil, along with some coal, make up almost all the remainder. Renewables such as biomass, geothermal, wind, and solar add about 1 percentage point.

Power Generation Capacity Additions and Investment over the Past 20 Years

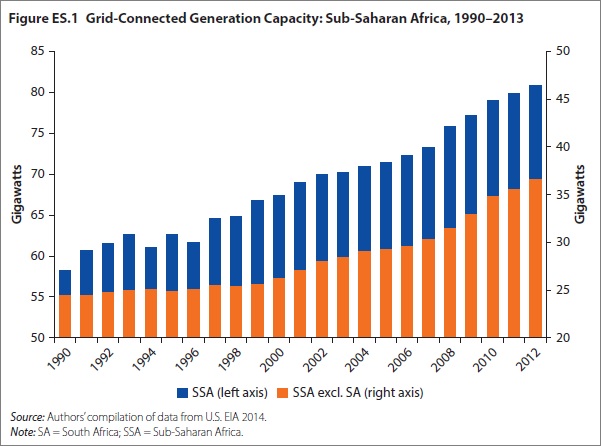

Between 1990 and 2013, only 24.85 GW of new generation capacity was added across Sub-Saharan Africa, of which South Africa accounted for 9.2 GW (figure ES.1). In the first decade of this period, 1990 to 2000, the countries of Sub-Saharan Africa other than South Africa added only 1.84 GW, and some even lost capacity. Between 2000 and 2013, investments picked up in these countries with an additional 13.8 GW installed. However, 94 percent of this increase occurred in only 15 countries, leaving dozens that added hardly any capacity at all. And as in the decade between 1990 and 2000, some actually lost capacity. Civil strife and lack of adequate system maintenance were the prevalent causes.

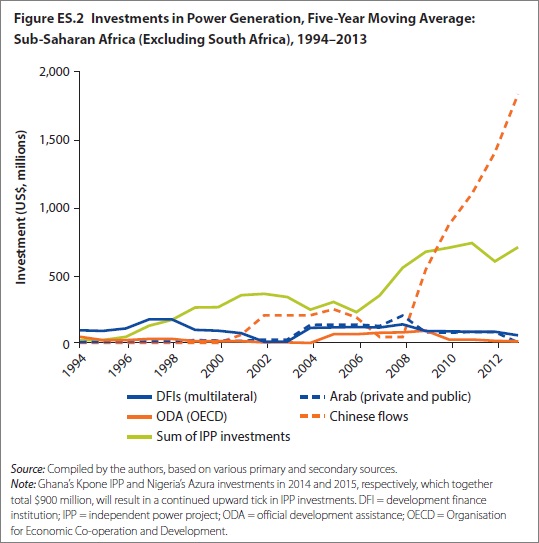

Between 1990 and 2013, investments in new power generation capacity totaled approximately $45.6 billion ($31.3 billion, excluding South Africa), or far below what is required to meet Africa’s growth and development aspirations. Although public utilities have historically been the major sources of funding for new power generation capacity, that trend is changing. Most African governments are unable to fund their power needs, and most utilities do not have investment-grade ratings and so cannot raise sufficient debt at affordable rates. Official development assistance (ODA) and development finance institutions (DFIs) have only partially filled the funding gap. ODA and concessional funding has fluctuated considerably over the past two decades and has recently been overshadowed by IPP and Chinese-supported investment. Indeed, private investments in IPPs and Chinese funding are now the fastest-growing sources of finance for Africa’s power sector (figure ES.2).

Independent Power Projects

IPPs in Sub-Saharan Africa date to 1994. Representing a minority of total generation capacity, IPPs have mainly complemented incumbent state-owned utilities. Nevertheless, IPPs are an important source of new investment in the power sector in a number of African countries.

IPPs are now present in 18 Sub-Saharan countries – all with varying degrees of sector reform and private participation. Currently, 59 projects (greater than 5 MW) are in countries other than South Africa, totaling $11.1 million in investments and 6.8 GW of installed generation capacity. Including South Africa adds 67 more IPPs, bringing the total to 126, with an overall installed capacity of 11 GW and investments of $25.6 billion.

IPPs in Sub-Saharan Africa range in size from a few megawatts to around 600 MW. The overwhelming majority of IPP capacity (82 percent) is thermal; only 18 percent is fueled by renewables. However, there is important growth in renewables. For example, three wind projects reached financial close between 2010 and 2014, and seven small hydropower projects are on the horizon. South Africa procured 3.9 GW in private power between 2012 and 2014, all of which is renewable.

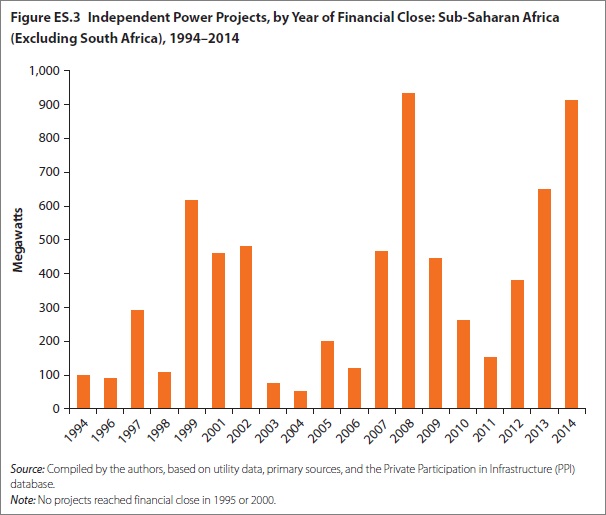

As shown in figure ES.3, there have been three major IPP investment spikes: 1999-2002, 2008, and 2011-2014. The first two spikes were due to the financial close of a small number of comparatively large projects. In 2011, IPP investments began taking off. Excluding South Africa, total IPP investment for projects in Sub-Saharan Africa between 1990 and 2013 was $8.7 billion, whereas in 2014 alone another $2.3 billion was added. Previously, IPP investments in South Africa had lagged those in other Sub-Saharan countries, but between 2012 and 2014 that country closed $14 billion in renewable energy IPPs.

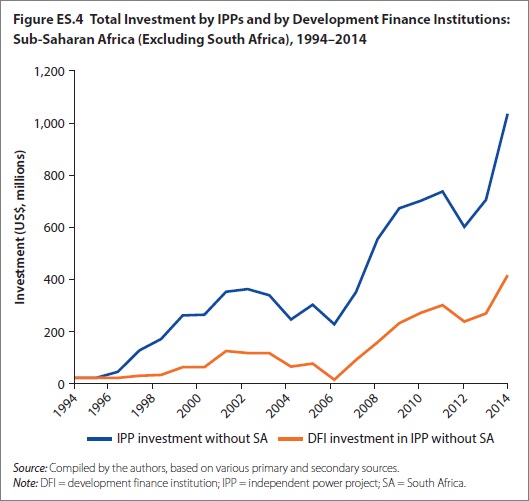

Although the conditions were varied in the countries where IPPs and other private participation took root, certain themes were common. With the exception of South Africa and Mauritius, none of the Sub-Saharan African countries with IPPs had an investment-grade rating. The possibility of a traditional project-financed IPP deal in this climate was limited. DFIs that invest in the private sector have made a significant contribution to funding IPPs (figure ES.4).

Chinese-Funded Power Generation Projects

In addition to IPPs, significant increases in generation capacity have stemmed from Chinese-funded projects. Chinese-funded generation projects can be found in 19 countries in Sub-Saharan Africa. Eight of these countries have IPPs as well as Chinese-funded projects.

Between 1990 and 2014, there were 34 such projects in Sub-Saharan Africa, totaling 7.5 GW. Chinese-funded projects far exceed IPPs in terms of total megawatts, especially for the years 2010-14, with an average size of 226 MW, in contrast to the IPP average of 98 MW. As of 2014, Chinese-funded projects exceeded IPPs in total megawatts and in total dollars invested.

The majority of Chinese-funded projects are large hydropower projects, for which Chinese engineering, procurement, and construction contractors have become renowned worldwide. The typical project structure involves a contractor plus a financing contract. The majority of these projects received funding from the China ExIm Bank (responsible for soft loans and export credit) on behalf of the Chinese government. Additional finance has been provided by other banks owned in whole or part by the Chinese government.

Conclusions

Independent power projects make a significant contribution to meeting Africa’s power needs. There is no doubt that IPPs are worth the effort. But it is not only the quantum of private investment in IPPs that is relevant; equally important are investment outcomes and, especially, the price and reliability of the electricity produced. The challenge ahead is for African countries to create the conditions to attract more and better IPPs and thus help overcome the continent’s power deficit.

Competition still poses a conundrum in Africa, which is why this study pays particular attention to unpacking the trade-offs attached to competitive procurement. When procured competitively, IPPs have generally delivered power at lower costs than directly negotiated projects, and their contracts have held up better. Despite this, unsolicited and directly negotiated deals have been the norm across Sub-Saharan Africa, accounting for over 70 percent of all IPP megawatts procured.

After 20 years of reform efforts in Africa, nowhere on the continent is full wholesale or retail competition to be found in power sectors. Countries that have attracted the most finance have a wide range of sector policies, structures, and regulatory arrangements. In 13 such destinations for IPP investments, vertically integrated, state-owned utilities predominate. The presence of a regulator is also not definitive in attracting investment. Although the countries with the most IPPs all have formally independent regulators, some countries with regulatory agencies do not have any IPPs.

There seems to be no clear relation among reforms, degree of competition, and the success of countries to attract IPPs. Thus it is reasonable to ask what are the merits of competition in this context, and what are the key reform elements that can help African countries most advantageously attract IPPs? Responses to these questions may be condensed into five main conclusions:

-

Systematic and dynamic power sector planning is crucial to identifying the generation projects that best meet a country’s power needs and define the potential space for IPPs. Sound planning means that countries are able to project future electricity demand correctly, decide on best supply (or demand management) options, and anticipate how long it would take to procure, finance, and build the required generation capacity. Planning tools must be updated regularly and new building opportunities allocated based on clear criteria. Finally, there must be an explicit link between planning and the timely initiation of the generation procurement process.

-

Competitive procurement of IPPs helps ensure that projects are implemented transparently and at the lowest cost. Two decades of experience in power procurement in Sub-Saharan Africa have amply demonstrated that a lack of competition in procuring new generation capacity has extensive drawbacks, ranging from immediate effects on project outcomes (higher prices, unraveling contracts, and so on) to more general effects on the overall governance of the electricity sector and its investment climate. IPP investment in Africa will rely on long-term contracts with off-takers where electricity demand is growing at medium or high rates. Where long-term contracts for new power are competitively bid rather than directly negotiated, there is a potential for reduced prices. Also, competitive procurement can stimulate the development of potentially bankable projects, especially renewable energy. African governments have not done enough to offer competitive tenders or auctions with clear ground rules; standardized, long-term contracts with IPPs; and reliable timelines. In the absence of these, project developers and funders have offered unsolicited bids. Designing and running competitive tenders are not trivial tasks. But if a core government team is authorized to do the work and sufficient resources are allocated for this purpose, then experienced transaction advisers can be hired to help. And the benefits of lower prices invariably justify the initial cost of running these tenders.

-

Direct negotiations and unsolicited offers are not ruled out. Indeed, sometimes they are unavoidable, but governments that engage in unsolicited proposals or directly negotiated deals must develop the capacity to properly assess the costcompetitiveness of these projects and the technical and financial capabilities of the project developers – thereby negotiating cost-competitive contracts. In addition, unsolicited bids may be opened to more scrutiny by instituting a public tender.

-

The financial viability of utilities is a critical factor in attracting IPP investments. IPP contracts should be undertaken with financially viable off-takers, whether they be utilities or large customers. Most IPPs are project-financed, and their bankability rests on secure revenue flows. Although credit enhancement and security measures can mitigate risk, a financially strong off-taker provides a sustainable basis for securing long-term contracts with IPPs. A sustained effort to better the performance of utilities must be at the center of countries’ reform agendas and also be consistently supported by development partners through financial and technical assistance.

-

Reforms, especially those improving the investment climate, remain important. Although IPP investment trends do not appear to be correlated with specific power sector institutional arrangements, the importance of reforms geared toward promoting a sound investment climate should not be discounted. Unraveling potential conflicts of interest between incumbent state-owned generators and IPPs, through unbundling generation from transmission, is in principle positive for private investment, as is more transparent contracting among state generators, IPPs, and independent transmission companies and system operators. Having a regulator in place is especially important, but the mere existence of a regulatory agency is not enough. The quality of regulation capacity is non-negotiable: the regulator must be independent and endowed with competent – and sufficient – human resources.

In conclusion, investment in Africa’s power sector IPPs is growing, but not fast enough. The region does not have sufficient power. All sources of investment need to be encouraged. For IPPs to flourish, the countries of Sub-Saharan Africa need dynamic, least-cost planning, linked to the timely initiation of the competitive procurement of new generation capacity. This must be accompanied by building an effective regulatory capacity that encourages the distribution utilities that purchase power to improve their performance and prospects for financial sustainability – and to widen access to electricity. Such efforts promise to promote economic and social development across the region.

Five Case Studies

1. Kenya’s Electric Power Promise

Kenya is among the countries in Sub-Saharan Africa with the most extensive experience in independent power projects (IPPs). Its first IPPs date back to 1996, and since then the country has closed a total of 11 projects for a total of approximately 1,065 megawatts (MW) and $2.4 billion in investment. While from a global standpoint these numbers are small, IPPs will soon represent more than one-third of Kenya’s total installed generation capacity. Most of the plants procured over the past two decades use medium-speed diesel/heavy fuel oil (MSD/HFO); some are geothermal and wind plants. And more IPPs are on the way: for example, in September 2014, a 900-1,000 MW coal plant was awarded to a consortium led by the Kenyan companies Gulf Energy and Centum Investment Company. Despite this momentum, the actual process of procuring new geothermal and wind power has become more muddled and complex with a series of procurements conducted by the publicly owned Geothermal Development Company (GDC) and directly negotiated wind projects.

What can be learned from Kenya’s IPP experience, particularly in terms of planning, procurement, and contracting? How do Kenya’s IPPs measure up to their public counterparts, and what areas might require further improvement?

2. Independent Power Projects and Power Sector Reform in Nigeria

While Nigeria has the largest population and economy on the African continent, 46 percent of its citizens live below the poverty line and less than 50 percent have access to electricity. The demand for electricity far outweighs available capacity, which is less than 5 gigawatts (GW) for a population of about 170 million (Compare this with South Africa, which has an installed capacity of 43 megawatts [MW] for a population one-third the size of Nigeria’s.) The actual generation output rate in Nigeria, meanwhile, is far below installed capacity. In fact Nigeria’s output rate per capita is among the lowest in the world, owing to poor operation and maintenance, aging generation and transmission infrastructure, fuel supply constraints, and vandalism.

Nonetheless, Nigeria has embarked on the most ambitious electricity sector reform effort of any country in Africa. Reforms were initiated in 2001 with the publication of a new power policy. The objectives of the reforms were to improve efficiency, attract private participation, and strengthen power sector performance so as to enable economic and social development. To this end, policy makers set a goal of achieving 40 GW of capacity by 2020 – a goal that now seems out of reach.

As part of the reform process, Nigeria unbundled the generation, transmission, and distribution subsectors; privatized power generation stations and distribution utilities; appointed a private management contractor to manage the transmission company; and established a bulk trader. Barring South Africa, the country also boasts the largest investment in independent power projects (IPPs) in Sub-Saharan Africa.

Since 1998, five large IPPs have been developed. Several generations of IPP transactions may be attached to distinct phases of the sector reform process. The first generation of IPPs emerged before the reforms began in earnest and included a project-financed plant. A second generation of IPPs was developed after President Olusegun Obasanjo took office in 1999 and the new power sector policy was published in subsequent years. Two stopgap projects emerged during this period, financed by international oil companies (IOCs) and with equity contributions from the Nigerian National Petroleum Corporation. After a hiatus of a number of years, and the rejuvenation of the reform process under President Goodluck Jonathan, who took office in 2010, a third generation of IPPs was developed including a predominantly Nigerian-financed IPP that intends to serve a local grid with mainly industrial demand. Today, a new power market is being established, and a fourth generation of classic, project-financed IPPs is emerging. IPP contracts have had to be designed and negotiated afresh in the new market conditions, and appropriate credit enhancement and security measures put in place to mitigate payment and termination risks.

Nigeria thus represents a fascinating case study of accelerating investment in new power capacity, in an electricity sector undergoing radical reform. Will the next generation of IPPs be successful and lead to further investment in much-needed power generation capacity? Will risks be mitigated? Will sector reforms foster financial sustainability? Will greater competition be possible in the future?

3. Investment in Power Generation in South Africa

South Africa is a latecomer in introducing private investment and independent power projects (IPPs) into its electricity sector. For nearly a century, its national electricity utility, Eskom, dominated the power market. Various attempts to introduce IPPs were half-hearted and unsuccessful. However, this has changed during the past four years.

South Africa now occupies a central position in the global debate about how best to accelerate and sustain private investment in renewable energy. In 2009, the government began exploring feed-in tariffs (FiTs) for renewable energy, but these were rejected in favor of competitive tenders. The resulting program, known as the Renewable Energy Independent Power Project Procurement Programme (REIPPPP), has successfully channeled substantial private sector expertise and investments into grid-connected renewable energy in South Africa at competitive prices.

To date, 92 projects have been awarded to the private sector, and the first projects are already online. Private sector investments of more than $19 billion have been committed for projects that total 6,327 megawatt (MW) of renewable energy. Prices of renewable energy dropped during the four bidding phases, with average solar photovoltaic (PV) tariffs decreasing by 71 percent and wind dropping by 48 percent in nominal terms. Most impressively, these achievements occurred during a four-year period, from 2011 to 2015. Additionally, there have been notable improvements in economic development that have primarily benefitted rural communities. Important lessons can be learned from this process for both South Africa and other emerging markets contemplating investments in renewable energy and other power sources.

4. Power Generation Results Now, Tanzania!

Tanzania has a vast array of conventional and renewable energy resources, and yet the country struggles to generate sufficient power to fuel growth and development. It has only 1,583 megawatts (MW) in installed generation, and imported fuel is a critical piece of its electric power generation. Network failures undermine what little power is produced. As a result, approximately 46 percent of the nation’s total power consumption is from off-grid self-generation (averaging $0.35/kilowatt-hours, kWh).

What has prevented Tanzania from harnessing its domestic resources in an economically efficient way, and what may be done differently going forward? There appear to be three key elements that directly affect Tanzania’s electricity supply industry and generation procurement. The first is a lack of coherent and up-to-date planning; the second is related to the planning and contracting nexus, including the allocation of public and private generation projects. The third element is a lack of sustained commitment to private sector investment and competitive bidding practices. The gas sector also suffers from many of the same issues, with direct implications for power production.

5. Power Generation Developments in Uganda

Uganda occupies a unique space in the history of power sector reform and investment in Africa. It was the first country to unbundle generation, transmission, and distribution into separate utilities and to offer separate, private concessions for power generation and distribution. Critics said that Uganda’s power system was too small to reap the possible benefits that might flow from competition in generation, and more focused management of transmission and distribution (T&D). The years that immediately followed the reforms seemed to bear out the critics’ views: the private distribution operator struggled to reduce losses, and there were delays in investments in large new hydropower capacity, resulting in costly dependence on short-term thermal power.

Despite ongoing challenges, Uganda’s power sector reforms are now bearing fruit. The performance of the distribution utility has improved. Losses are down, and collections, investment, and connections are up, although access rates remain low. After a torturous start, Uganda concluded the largest private hydropower investment in Africa, the Bujagali plant, built by an independent power project (IPP). Simultaneously, it has attracted a raft of smaller IPP investments, including the innovative competitive bids for small hydropower, biomass, and solar projects solicited under the global energy transfer feed-in tariff (GETFiT) program, which was developed jointly by Uganda’s Electricity Regulatory Authority (ERA) and the Kreditanstalt für Wiederaufbau (KfW, German Development Bank). After South Africa, Uganda has the largest number of IPPs in Sub-Saharan Africa and the only other competitively bid grid-connected solar photovoltaic (PV) program.

Alongside these IPP successes, Uganda has now embarked on two large Chinese-funded hydropower projects. Private investment in power is still politically contested, and IPPs are seen locally to be potentially expensive, complex, and time-consuming.

Uganda thus offers much pertinent experience and many valuable lessons in power sector reform, private sector participation, IPPs, competitive bidding, grid-connected renewable energy, and Chinese-supported projects.

Related News

DG Azevêdo: “The role of the multilateral trading system in the midst of mega-regionalism: responding to the problems of trade and investment”

Director-General Roberto Azevêdo visited Jakarta, Indonesia, on 12-13 April to discuss the implementation of recent WTO agreements and future work of the organization. During the visit DG Azevêdo met with President Joko Widodo and the Minister of Trade Thomas Lembong. He also met with a number of other government officials and representatives of the private sector.

In a roundtable discussion on 12 April with the Indonesia Chamber of Commerce and Industry and the Employers’ Association of Indonesia, the Director-General called on Indonesia to ratify the Trade Facilitation Agreement, an outcome of the Bali Ministerial Conference, as it could reduce Indonesia’s trade costs by around 13% and would create a friendlier climate for the private sector.

He also highlighted Indonesia’s important role in ensuring that negotiations in the Nairobi Ministerial Conference reached a positive outcome. Outcomes from Nairobi, he said, will help benefit farmers and exporters in Indonesia and will also be important to the country’s development strategy, which includes food security as a key element. Looking ahead, Indonesia has the opportunity to contribute to the important conversation now under way among WTO members about how to move forward the work of the WTO, DG Azevêdo said.

DG Azevêdo also met with academics and students on 13 April at a seminar organised by the Indonesian Economist Association, the Centre for Strategic and International Studies, and the Institute for Development of Economics and Finance.

“The role of the multilateral trading system in the midst of mega-regionalism: responding to the problems of trade and investment”

Remarks by Director-General Roberto Azevêdo

It is a great pleasure to be with you today – and to be back in Indonesia.

This is my first visit since the WTO’s successful Ministerial Conference in Bali in 2013.

The conference was a historic moment for the WTO.

I was told at the time that Bali is affectionately referred to as the ’Morning of the World’.

After a tough period in global trade negotiations, I expressed the hope that our time in Bali would prove to be the ’morning of the World Trade Organization’.

And that has proved to be the case.

Our Bali conference delivered the first multilateral trade agreement since the WTO was created, two decades earlier.

It proved that the WTO could negotiate important outcomes.

And it showed that the organisation could deliver results with real economic impact, which will make a real difference to people’s lives.

I will come back to the results of Bali later. But I would like to pay a sincere tribute once again to the government of Indonesia for its hospitality and leadership which made the success of the Bali conference possible.

As a result, this country will forever be associated with a vital moment in the history of the multilateral trading system.

Of course, Indonesia has always been a committed and engaged member at the WTO.

The country was one of the founding members of the organization – and remains a central player.

Indonesia is an active user of our dispute settlement mechanism, which helps countries settle their trade differences in a transparent and objective manner.

And you play an important role as the coordinator of an influential group of developing countries in the agriculture negotiations – known as the G-33.

I think this strong engagement shows two things.

First, it shows Indonesia’s confidence in the WTO, and the system of global trade rules that it embodies.

Second, it shows your belief that the WTO can help the country to improve its trading terms.

And right now, this engagement is more important than ever.

We are meeting at a time when the economic scenario is very mixed.

Last week I announced the WTO’s new trade forecasts. In 2015 global goods trade grew at 2.8%. And we expect it to remain at the same level this year. This would make 2016 the fifth consecutive year of sub 3% growth.

This is not unprecedented – we saw lower growth in the early 1980s. And we expect to come out of this pattern of low growth in the coming years, with trade growth forecast to pick up to 3.6% in 2017. But, nevertheless, it is a worrisome situation.

Of course, Indonesia has not been immune from some of the headwinds we’ve seen in recent times. Factors such as the dramatic fall in commodity prices and lower growth in China have had an impact here, as they have had in many other economies.

But I think there are reasons to be optimistic.

Indonesia has both a strong vision for the way forward in the medium term economic plan, and an extremely strong basis on which to build.

Indonesia is the largest economy in ASEAN. It is one of the most populous countries in the world – with a young, dynamic workforce. It has abundant natural resources. And it has an improving business climate – jumping 11 places in the World Bank’s 2016 rankings for the ease of doing business. This performance was in part due to reforms which improved access to credit and made it easier to pay taxes.

In a wider context, a range of reforms have helped to transform the economy – such as diversifying away from agriculture, so that manufacturing now accounts for a greater share of the country’s GDP.

Similarly, efforts on infrastructure development and to improve education and healthcare could have a very significant effect.

The government has set an ambitious trajectory, towards achieving 8% growth by 2019.

Trade can play an important role here. And I believe that some of the recent agreements struck at the WTO can help Indonesia in securing further growth, development and job creation.

The WTO provides the framework of rules by which global trade is governed.

These rules aim to avoid unilateral, discriminatory or arbitrary measures, helping to level the playing field between developed and developing countries.

In this way the WTO provides a kind of constitution for global trade – and I believe that the fundamental principles enshrined therein will remain constant.

Nevertheless, of course there are areas where the rules can be adjusted and updated to ensure that trade flows more freely, and to tackle some specific issues – particularly those faced by developing countries.

Changes to the rules come through negotiations – and with 162 members at the table it has historically proved very tough to reach consensus.

Our ministerial conference in Bali changed all that.

Members reached consensus on a range of important issues at that conference – including the Trade Facilitation Agreement.

This Agreement is about streamlining, simplifying and standardising customs procedures, thereby reducing the time and expense of moving goods across borders, and driving down the costs of trade. The impact will be very significant – greater than removing every single remaining tariff around the world.

Indonesia has already taken positive steps to facilitate trade, such as improving existing infrastructure, including Tanjung Priok port.

It used to take an average of 6.4 days for containers to leave the port after being unloaded. Improved systems have brought the time down to just over four days. This is very positive, but it is still four times longer than it takes in Singapore.

So there’s still work to do, and the Trade Facilitation Agreement can help to complement these efforts.

Studies show that when fully implemented, the Agreement could reduce Indonesia’s trade costs by around 13%.

This would have a big impact. It would lower the barriers for doing business overseas, which have often prevented companies – particularly SMEs – from accessing foreign markets.

Moreover, by further streamlining business processes, the Agreement will help to create an even friendlier climate for private sector investment.

But, in order to benefit from the Agreement, first it must be ratified. This is one immediate and very positive step that Indonesia could take. And, of course, it would be fitting for the country where the Trade Facilitation Agreement was delivered to lead the way in bringing it into force.

Since Bali, the WTO has continued to deliver – and to do so in ways which can benefit Indonesia.

Our most recent ministerial conference was held in December last year, in Nairobi.

At that meeting members took the historic decision to abolish agricultural export subsidies.

This was the biggest reform in agricultural trade rules in the last 20 years – and it fulfils a longstanding demand of developing countries.

By eliminating this trade-distorting support for exports, it will help to level the playing field in agriculture markets to the benefit of farmers and exporters here in Indonesia.

Under the decision, developed members have committed to remove such subsidies immediately, except for a handful of farm products. Developing members have the flexibility to cover marketing and transport costs for agriculture exports until the end of 2023.

Of course, there is much more to do in order to reduce distortions in the agricultural markets, but this is a significant step forward.

In Nairobi, members also pledged to negotiate in the next two years a decision on public stockholding of grains for food security purposes.

In addition, they made a commitment to negotiate a mechanism allowing developing countries to shield local farmers from import surges of food products which can harm domestic production.

As food security is a key element of Indonesia’s development strategy, the negotiations stemming from these recent decisions will be very significant.

And, as in Bali, I want to acknowledge Indonesia’s important role in ensuring that the negotiations in Nairobi reached a positive outcome.

The active engagement of Minister Tom Lembong and his resounding call for WTO ministers to summon the political will and flexibility needed to reach an agreement was instrumental to the success of the conference.

As a result of these breakthroughs, engagement in the work of the WTO is at a level today that I have not seen for a long time.

And with a great deal of effort also being put into regional trade deals, I think many are asking how the different tracks work together.

Actually, although a lot of focus has been put on regional initiatives lately, they are not a new phenomenon. They have long co-existed with the global system, and have largely acted in a positive way, reinforcing cooperation on trade.

In my view, a healthy trading system would see progress and engagement at all levels.

Our recent efforts to analyse these issues supports this conclusion. It shows that regional agreements have WTO DNA, and in the areas where they overlap with WTO rules we have found no obvious conflicts.

A bigger consideration is where such initiatives cover areas that are not currently covered by the WTO. And this puts the spotlight back on the current WTO agenda.

An important conversation is now underway among WTO members about how we should move our work forward.

It is clear that all WTO members want to deliver on the so-called Doha negotiating issues, such as domestic subsidies in agriculture, fisheries subsidies, and improved market access for agricultural produce, industrial goods and services. However, members do not agree on how to tackle these issues.

In addition, some would like to start discussing a wider range of topics, including other, non-Doha issues. Investment promotion, e-commerce, and small and medium-sized enterprises are a few of the broad areas that have been raised so far.

This is an important conversation. And despite some gaps, there are some important commonalities.

For example, there is a strong desire to keep development at the centre of our efforts and to continue making positive efforts to integrate developing countries into trading flows.

In addition, members want to achieve more – and to do it faster.

I think this is an exciting opportunity for Indonesia. You have the opportunity to shape the future of global trade talks in your interests.

I encourage you to bring your issues to the table. Clearly agriculture and food security are priorities. I have also heard a lot of discussion here in Jakarta about increasing the level of investment in the country. So there are a range of interests which you could seek to pursue.

This debate is happening now – and I urge you to stay engaged.

Your voice will be as important as ever.

I have tried to demonstrate today how important trade and the WTO are for Indonesia. But I think it’s also clear just how important Indonesia is for the WTO.

It was here in Indonesia that the WTO delivered its first major negotiating success.

And I hope that you will be at the heart of many more successes in the years to come.

Thank you for listening.

Related News

2016 African Economic Platform

The African Economic Platform will bring African leaders from public, private, philanthropic and academic sectors to engage on four (4) critical matters leading to implementable initiatives. As agreed, to ensure that the basic human rights of our peoples are at the centre of Agenda 2063, we have to ensure that rights to education, to food and nutrition, to health care, to safe water, sanitation and energy are enshrined in our respective endeavours to implement Agenda 2063.

The Continent is at a fork in the road. Notwithstanding the current challenges faced by the continent, sustained growth remains the key ingredient to unleash the potential of the continent when adequate skills are continuously harnessed and free movement of the African people becomes a real facility accessible to all. We know that development aid has helped, but will not deliver sustainable growth and transformation in Africa. The continent must continue to explore and tap into innovative and domestic finance for the effective implementation its transformation through trade and industrialisation.

A study by NEPAD and ECA (2014) shows that Africa is responsible for a significant proportion of its development finance as more than $527.3 billion comes from domestic taxes compared to $73.7 billion received in private flows and 51.4 billion in official development assistance. Supplemental revenues come from pension funds, diaspora remittances, earnings from minerals and fuels, international reserves held by reserve and central banks, liquidity in the banking sector, the growing marketplace for private equity funds and potential resource flows from securitisation of remittances.

Following the January 2016 African Union Summit, we find it appropriate to take the decisions and conversations forward in order to ensure that business and political leaders, find realistic and achievable common ground to ensure that terrorism in Africa will not find fertile ground in poverty. It is our belief that Africa has the required internal resources to finance the transformation of its people and the continent. Furthermore, that shared prosperity and well-being are achievable for ordinary Africans across the continent.

While African countries taken separately may have diverging issues, the African Economic Platform will allow for four (4) interconnected issues to anchor the programme. As a result, the time invested will result in greater collaboration on matters of common interest for effective African integration leveraging on two (2) billion Africans.

Critical issues

Four critical areas that have the potential when realised in their right mix, in each country and region, to elevate the socio-economic conditions of Africans, have been identified. We ought to leave Mauritius with the assurance that Africans will be equipped with adequate skills on the largest visa-free continent, in order to use their skills through the value chain of our natural resources making African industrialisation, the premise of greater intra-African trade. For this purpose, we agree to focus our discussions on (1) skills, (2) trade, (3) industrialisation and (4) free movement.

More specifically, the African Economic Platform aims at securing:

-

Commitment from all parties to remove policy obstacle for doing business in Africa;

-

Implementation of policies for sustained and inclusive growth;

-

Increase African awareness of continental issues in a global context; and

-

Integrate youth perspective and commitment into the #AfricaWeWant

Trade

What would it take for African countries to stop exporting the bulk of their oil, diamonds and maize to foreign countries rather than to other African countries?

Trade creates linkages that are essential to the integration agenda. Although intra-African trade is not a panacea for development, it is quite important. Small Medium Enterprises could become more competitive by creating economies of scale across their respective regions. As they grow, SMEs can strengthen product value chains and facilitate the development of technology and knowledge.

Trade incentivises and spurs infrastructure development and attracts foreign direct investment expanding intra-African trade. This is key to accelerating economic growth on the continent. Especially important for the continent’s many small, non-coastal countries that face tremendous challenges trading internationally.

Unfortunately, Africa’s current internal trade is challenged by the fact that most of its exports go to the world’s advanced economies like the US,UK and China, and most of its imports come from those same advanced economies. In this respect, the African Economic Platform ought to reflect on:

Economic diversification in order to encourage many African countries to specialise in complementary goods to exchange with each other;

Conflict as it diminishes the capacity for African states to engage in intracontinental trade. These factors lead to low levels of economic growth, destroy needed export infrastructure, and slow and reverse regional integration;