Search News Results

IMF Executive Board 2015 Article IV Consultation with Botswana

On March 16, 2016, the Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation with Botswana.

After a rapid recovery from the 2009 downturn, GDP growth is estimated to have turned slightly negative in 2015 owing to a decline in the global demand for diamonds and copper. Non-mining activities, while recording positive growth over the year, remained subdued owing to spillovers from lower mining activity, a regional drought, and electricity and water shortages. Inflation has been declining over the past few years and is now close to the lower bound of the Bank of Botswana’s objective range of 3-6 percent, reflecting a successful monetary policy, lower fuel prices, and an appreciation of the Pula against the South African Rand.

After three years of surpluses, the government balance has turned into a deficit, reflecting lower mining revenues, a decline in revenues from the South African Customs Union (SACU), and higher fiscal spending, part of which is related to the Government Stimulus Program. The deficit has been financed by drawing on previously accumulated savings and incurring a small amount of domestic debt. The external current account surplus has also been declining, but is estimated to be in positive territory. As Botswana entered the current downturn with large fiscal and foreign reserve buffers, the country is well positioned to deal with the decline in export demand.

A gradual economic recovery is projected in the next three years, based on an expected gradual increase in diamond prices and fiscal stimulus, while inflation is expected to remain within the BoB’s objective range. The 2016/17 budget submitted to Parliament in February envisages a fiscal deficit of about 4 percent of GDP as a result of lower mining and SACU revenues and higher capital expenditures. In the medium-term, the macroeconomic framework envisages fiscal consolidation based on a gradual recovery of the mining sector and expenditure rationalization (the authorities plan to contain the growth of wages and salaries and reduce transfers to state-owned enterprises).

Lastly, the external current account surplus is projected to narrow further this year, but gradually reverse to trend thereafter along an expected recovery in export prices. Botswana’s diamond endowment and its track record of good macroeconomic policy management and political stability contributed to high average economic growth and strong fiscal and balance of payments positions in recent years.

Beyond these achievements, the authorities see a need to reduce unemployment, eliminate water and electricity shortages, and improve the efficiency of government operations. In addition, given the limits of the diamond and public sector-based growth model (diamond reserves could be exhausted by 2050 and inefficiencies in the public sector), a wave of reforms is called for to foster the development of the private sector, diversify the economy, and improve the skills of the labor force.

Staff Report

Real GDP growth is estimated to have turned negative in 2015 owing to weaknesses in the global demand for diamonds and a deceleration of activity in the non-mining sector, driven mainly by spillovers from lower mining activity. Inflation has been low and is now near the lower bound of the Bank of Botswana objective range of 3-6 percent.

The economy is expected to recover gradually over the next three years, driven by a gradual pick up in global diamond prices and fiscal stimulus. The main risks to the outlook are a slowdown in economic activity in major advanced and emerging markets and delays on restoring reliability and self-sufficiency in water and electricity and in implementing other structural reforms.

The 2016/17 budget presented to Parliament in February envisages high levels of public investment and a higher fiscal deficit. The stimulus is justified in the face of a negative output gap, strong fiscal buffers, and the need to close the infrastructure gap. However, its scale may be ambitious given past difficulties in implementing infrastructure projects. The Bank of Botswana’s accommodative monetary policy stance is appropriate, although the space for further monetary easing will be constrained by the fiscal expansion. The financial sector is stable but requires continued monitoring.

In the near-term, the priorities are to increase the efficiency of public investment, reform the water and energy sectors, and improve workers’ skills and the business environment. In the medium-term, the growth strategy needs to be focused on a few areas and backed by bold reforms to mobilize domestic revenues, rationalize government spending and state-owned enterprises, implement a well-prioritized public investment program and consider adopting a sound fiscal rule, and improve education and labor market policies.

Recent Developments

The economy has entered a period of weakness connected to a decline in the global demand for diamonds which have also affected the country’s fiscal and external positions, while successful monetary and financial policies have kept inflation in check and the financial sector stable.

The economy has been slowing down, while inflation has been within the Bank of Botswana’s objective range of 3-6 percent. Following a healthy recovery after the 2009 downturn, economic growth slowed down in 2014 and is estimated to have come to a halt in 2015. Both external and domestic factors contributed to the slowdown. Mining GDP was affected by a decline in the global demand for diamonds and copper, while non-mining GDP decelerated owing to spillovers from lower mining activity, a regional drought, electricity and water shortages, and less favorable domestic credit conditions. The decline in non-mining GDP growth was cushioned by an expansionary fiscal policy. Inflation has also been in decline (the 12 month-rate of inflation was 2.7 percent in January 2016), reflecting a prudent monetary policy, lower fuel import prices, and a recent appreciation of the Pula against the South African Rand.

After three years of surpluses, the government balance has turned into deficit. The fiscal deficit for FY 2015/16 (the fiscal year runs from April 1) is estimated to be in the order of 3 percent of GDP on account of lower mineral revenues, reduced receipts from the Southern African Customs Union (SACU), higher wages and transfers to state-owned enterprises, and higher capital expenditure. The latter reflects an “Economic Stimulus Program” that began to be implemented in the second half of 2015 to counteract the economic slowdown and includes higher capital expenditures targeting the tourism, transport, and agriculture sectors. As Botswana entered the downturn with sizable fiscal savings, the deficit is being primarily financed by government deposits.

The current account surplus has declined, but foreign reserves remain high. The current account surplus is estimated to have fallen from a peak of 16 percent of GDP in 2014 to about 9 percent in 2015 on account of (i) lower prices and volumes of diamonds and copper exports; and (ii) lower SACU revenues. Despite a small decline in 2015, the stock of foreign exchange reserves remain comfortably high at US$7.5 billion (65 percent of GDP), well above the upper bound of the optimal range estimated by the Adequacy of Reserves Assessment metric (Appendix I).

Minor adjustments were made to the exchange rate framework. To better reflect trading partners’ trade weights and inflation differentials (particularly an increase in South Africa’s projected inflation), the Bank of Botswana (BoB) increased slightly the target rate of crawl of the Pula from a downward crawl of 0.16 percent in 2014 to zero in 2015 and to 0.38 in 2016, and reduced the basket weight for South Africa from 55 to 50 percent in 2015.8 The real effective exchange rate remained virtually unchanged in 2015, and the staff assessment of the real value of the Pula suggests that it is consistent with economic fundamentals (Appendix II).

Monetary policy has been eased but transmission through the credit channel has been weak. In the context of declining inflation, the BoB reduced its policy rate from 7.5 in 2014 to 6 percent in 2015. These cuts have been consistent with cyclical developments as confirmed by a standard Taylor rule. Even though the prime lending rate fell in response to policy easing, credit growth declined as commercial banks adopted a cautious approach to lending in the context of slow growth in customer deposits and increasing competition to raise funds. To further ease liquidity conditions, the Primary Reserve Requirement on Pula denominated deposits was reduced from 10 percent to 5 percent in 2015.

The financial system is stable, but some vulnerabilities remain. There are 11 banks in the system alongside several non-bank financial institutions providing a variety of modern services. Banks are well capitalized, with an average capital adequacy ratio of 21 percent and a low share of non-performing loans (4.5 percent of total gross loans). Nevertheless, asset quality deteriorated during the past year, profitability declined slightly, and funding conditions became more challenging, especially for smaller institutions. While the system remains sound, a major economic contraction could raise stability risks given lenders’ relatively large exposure to households (59 percent of total bank loans), which is mainly in the form of unsecured lending (about 65 percent of total credit to households).

Outlook and Risks

Armed with ample savings and foreign reserves, the authorities are well-positioned to weather the current slowdown. The economy is expected to recover gradually, driven by a pick up in the global demand for diamonds and fiscal stimulus, while custom receipts are expected to remain subdued. The main risks to the outlook are sluggish external demand for minerals and slow or insufficient reforms.

The baseline scenario assumes a gradual recovery in the next three years and modest growth in the longer term. The projection is based on the assumption of a measured recovery in global diamond and copper prices (Box 1). It also reflects the impact of higher government spending and investments in the energy and water infrastructure, together with gradual reforms to improve the business environment, which could bring real GDP growth towards 5 percent by 2019. Subsequently, the baseline projects annual average real GDP growth of around 4 percent based on the withdrawal of the fiscal stimulus and continued prudent macroeconomic policies and economic reforms. Inflation is projected to remain within the BoB’s objective range.

The fiscal and external positions are expected to deteriorate further in 2016 and improve thereafter. The 2016/17 budget entails a fiscal deficit of about 4 percent of GDP, the result of lower mining and SACU revenues and the continued implementation of the government’s stimulus program. Fiscal consolidation is expected over the medium-term, based on a gradual recovery of the mining sector and expenditure rationalization. On the latter, the authorities envisage containing the growth of wages and salaries and lowering transfers to state-owned enterprises, especially electricity and water. Regarding the external position, the current account surplus is projected to narrow further from 9 percent of GDP in 2015 to about 2 percent in 2016 and reverse trend thereafter, alongside a projected recovery in diamond prices and volumes (supported by a gradual pickup in global demand).

An alternative scenario entailing a stronger reform effort and prioritized public investment has a better chance to address Botswana’s challenges. Staff prepared an alternative scenario that suggests that, with accelerated reforms, a gradual and well-prioritized public investment program, and improved efficiency in the public sector, the country will be in a better position to achieve economic diversification, higher growth, and a transition to high-income status.

There are important risks to the outlook. In the near term, the main downside risks are: (i) sluggish growth in key advanced and emerging economies, that could lead to continued weakness in the demand for diamonds (and copper); (ii) unresolved economic problems in South Africa and continued depreciation of the Rand, which could lower SACU receipts and have a negative impact on regional investors’ sentiment; and (iii) delays in plans to restore reliability and self-sufficiency in the water and electricity sectors, which would have adverse impact on costs, the fiscal balance, and the business environment; as well as delays on other structural reforms (e.g. deregulation and removal of red tape).

On the upside, a faster than expected recovery in the global demand for minerals could enable a faster recovery. In the longer term, the main risks relate to insufficient or ineffective actions to improve the efficiency of public investment and foster fiscal consolidation, economic diversification, and inclusive private sector-led growth.

Box 1. Botswana: Developments in the Diamond Industry

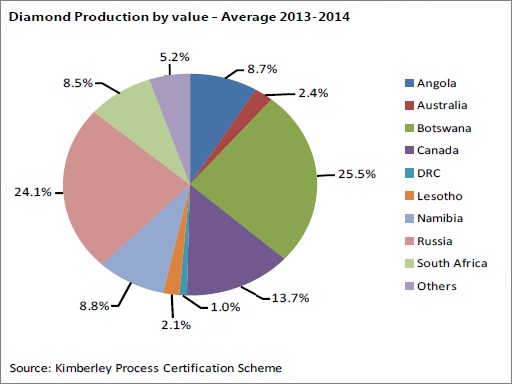

Diamond production is concentrated in two major country groups: a northern one, which includes Russia and Canada, and a Southern one that includes mainly Southern African states. There is another, less significant, group that produces diamonds of lower value and includes the Democratic Republic of Congo. The top three producing countries are Botswana, Russia, and Canada, accounting respectively for 25.5, 24.1, and 13.7 percent of world output, respectively. The rough diamond market is dominated by two companies: De Beers and ALROSA, each accounting for 34 and 25 percent of the world market. On the demand side, the U.S. represents about 40 percent of the global market for polished diamonds, followed by China/Honk Kong/Macau (15 percent), India (8 percent), the Gulf Region (8 percent), and Japan (6 percent).

The global demand for polished diamonds started to fall in the second half of 2014 prompted by a slowdown in China’s economy and signaling a reversal from a period of high growth (which had led to overly optimistic market expectations). This, together with a slowdown in other markets, led to an accumulation of inventories of polished diamonds and lower demand for rough diamonds. Between mid-2014 and September 2015, prices for polished and rough diamonds decreased by 12 and 23 percent respectively. Consequently, major producers started cutting production beginning in the second half of 2015. In Botswana, De Beers reduced production by about 20 percent in 2015 and announced further cuts for 2016. Debswana – the 50/50 joint venture between De Beers and the government of Botswana – put its Damtshaa mine on care and maintenance status and plans to scale down production at the Orapa 1 mine for the period 2016-2018.

Notwithstanding these negative developments, market observers coincide that with a careful management of supply, diamond prices may rebound as excess inventories clear, although uncertainties remain as to whether the recent decline in demand is transitory or structural (as diamonds are not a exchange traded commodity, information on prices and volumes is limited, which constrains the scope for analytical work on developments and prospects). For instance, Bain and Company (2015), expects demand to return to a long-term growth trajectory of 3-4 percent per year, relying on strong fundamentals in the US and continued growth of the middle classes in India and China. At the same time, the U.S. market is largely saturated, and while demographic changes in the faster growing countries would in principle favor increased demand for diamonds, consumer preferences in younger generations across the globe may be shifting. On the supply side, output is expected to decline by 1-2 percent per year through 2030, based on an analysis of existing and prospective volumes inferred from publicly announced plans by producers. Other factors that could affect market developments are, on the one hand, the recycling of diamonds and the emergence of synthetic stones and, on the other hand, the fact that new diamond deposits could be further underground and much more costly to extract.

Lastly, the industry faces other challenges in its value chain. Cutting and polishing firms may not be robust enough to cushion against short-term fluctuations in the retail market, given their constrained bargaining power over producers and retailers and limited access to financing. In fact, lower margins are driving weaker firms out of business, most of them in Africa (in 2015, the combined market share of cutting and polishing firms in China and India rose to 85 percent while the share of African companies declined, reflecting insufficient competitiveness of the latter).

Policy Discussions

The discussions focused on the near term policy mix to counter the economic downturn, contain fiscal risks, and preserve financial stability as well as on selected medium-term issues, namely measures to improve the efficiency of public investment, strengthen the frameworks for managing mineral revenues and the financial sector, and foster job creation and private sector-led growth.

-

Policy Mix, Fiscal Risks, and Financial Stability

As the fiscal stimulus is rolled out, additional monetary easing may not be required, but the authorities need to be cautious with public investment projects and consider reforms to mobilize revenue in order to limit fiscal risks. Financial sector risks call for continued close monitoring of the sector.

-

Enhancing the Framework for Economic and Financial Stability

Building on a good track record of fiscal soundness and macroeconomic stability, there is scope to strengthen the framework for managing mineral revenues and safeguard financial stability.

-

Diversification and Inclusive Growth

Progress with economic diversification has so far been limited and high levels of unemployment persist, with most employment creation coming from an oversized public sector. Looking ahead, well-prioritized investments in education, energy, water, and other infrastructure will be critical, supported by reforms to improve the business environment and the efficiency of the public sector.

Related News

Trading into sustainable development: Trade, market access, and the Sustainable Development Goals

The 2030 Agenda for Sustainable Development and the Sustainable Development Goals (SDGs) suggest that countries achieve sustainable development in all three dimensions, that is, economic, social and environmental, simultaneously. In this context, international trade is expected to play its role as a means of implementation for the achievement of the SDGs.

“Means of implementation” include factors that facilitate countries’ progress towards the achievement of sustainable development, such as public and private financial resources, capacity‐building, and transfer of environmentally sound technologies.

Recognizing international trade as a means for achieving socioeconomic development is not a new phenomenon. At the establishment of the United Nations Conference on Trade and Development (UNCTAD) in 1964, the international community acknowledged that:

“Economic and social progress throughout the world depends in large measure on a steady expansion in international trade. The extensive development of equitable and mutually advantageous international trade creates a good basis for the establishment of neighbourly relations between States, helps to strengthen peace and an atmosphere of mutual confidence and understanding among nations, and promotes higher living standards and more rapid economic progress in all countries of the world” (UNCTAD, 1964).

In practice, however, it remains a considerable challenge to trade policymakers to map out interlinkages between trade policy and sustainable development, let alone to ensure that trade policy outcome positively influence sustainable development. In this increasingly globalised world, achieving the SDGs as universal agenda requires policy coherence at all (national, regional and global) levels, where trade policy and its policy and institutional interfaces with all the SDGs is one part of the jigsaw.

This report examines various interactions between trade policy, with a specific focus on market access conditions, and factors that constitute the basis for achieving sustainable development. Market access conditions vis-à- vis imports are determined by a combination of border measures and “behind the border” measures, both of which add costs to the price of an imported product. By generating significant impact upon consumer welfare and the competitiveness of domestic industries, market access conditions in international trade thus are a key determinant of the effectiveness of trade as a means of implementation.

Chapter I provides an overview of the report by examining to what extent sustainable development concerns are integrated into today’s trade policymaking. The chapter first looks into how those concerns are treated in trade agreements at multilateral, regional and bilateral levels. It then discusses opportunities as well as challenges in using market access conditions to meet sustainable development objectives.

Chapter II discusses the use of tariffs for trade and development purposes, and provides comprehensive statistical information on the trade-related “indicators” for the reviewing and monitoring of the implementation of the 2030 Agenda.

Chapter III discusses how NTMs can act as an important “policy interface” within the trade-SDG nexus at home as well as that of trading partners. The majority of NTMs are domestic regulations that cater for social and environmental development objectives. The chapter discusses ways to achieve synergies between policy measures for achieving the SDGs and enhancing trade flows across countries.

Chapter IV presents recent evidence on the importance of connectivity, especially maritime connectivity, to international markets. Enhancing physical connectivity to markets is one of the most effective policy actions to complement market access improvement for both exports and imports.

This report will be discussed at the UNCTAD Briefing: Realizing trade potential to contribute to Sustainable Development, taking place on 15 April 2016 in Geneva.

Related News

84% of World Bank’s private investments in Sub-Saharan Africa go to companies using tax havens

Fifty-one of the 68 companies that were lent money by the World Bank’s private lending arm in 2015 to finance investments in sub-Saharan Africa use tax havens, Oxfam revealed on 11 April 2016.

Oxfam’s new analysis focused on the International Finance Corporation’s (IFC) investments in Sub-Saharan Africa. It shows that together these 51 companies, whose use of tax havens has no apparent link with their core business, received 84 percent of IFC investments in that region in 2015. It also reveals that the IFC has more than doubled its investments in companies that use tax havens in just five years – from $1.2billion in 2010 to $2.87billion in 2015.

The findings come ahead of the annual IMF-World Bank Spring meetings starting on Wednesday in Washington DC, and in the wake of the Panama Papers scandal which revealed how powerful individuals and companies are using tax havens to hide wealth and dodge taxes. The issue of tax havens is also expected to be high on the agenda at the UK government’s Anti-Corruption Summit in London next month.

In Oxfam’s study, the most popular haven for IFC’s corporate clients was Mauritius; 40 percent of IFC’s clients investing in Sub-Saharan Africa have links there. Mauritius is known to facilitate “round-tripping.” This is where a company shifts money offshore before returning it disguised as foreign direct investment, which attracts tax breaks and other financial incentives.

Sub-Saharan Africa is the poorest region in the world. It desperately needs corporate tax revenues to invest in public services and infrastructure. For example, the region lacks money to provide enough skilled birth attendants, clean water or mosquito nets, resulting in high rates of child mortality; one child in 12 dies before their fifth birthday.

Oxfam’s Head of Inequality, Nick Bryer, said: “It’s crazy to be giving with one hand and taking away with another – the UK government donates to the World Bank to encourage development, but by allowing investments in tax havens the World Bank’s lending arm is ultimately depriving poor countries of much-needed revenues to fight poverty and inequality.”

“The World Bank Group should not risk funding companies that are dodging taxes in Sub-Saharan Africa and across the globe. It needs to put safeguards in place to ensure that its clients can prove they are paying their fair share of tax.”

The IFC invested more than $86billion of public money in developing countries between 2010 and 2015; 18.6 percent of it spent in Sub-Saharan Africa. The IFC has a significant focus on financial markets, infrastructure, agribusiness and forestry, among other sectors.

While the IFC arguably leads the private sector with its disclosure, environmental and social standards, the public still has no access to information about where over half of the institution’s financing ends up, because it is done through opaque financial intermediaries. It also continues to face major challenges in measuring its overall development impact, and ensuring that the projects it funds do not harm local communities. This latest Oxfam research shows that the organisation also has a long way to go in ensuring that its clients are responsible tax payers.

Oxfam is calling for the IFC to develop new standards to ensure it only invests in companies that have responsible corporate tax practices. For example, companies should be transparent about their economic activities so it is clear if they are paying their fair share of tax where they do business.

The international agency is also calling on David Cameron to show strong leadership in tackling tax havens, beginning by intervening to ensure that the UK’s Overseas Territories and Crown Dependencies publish public registers revealing the true owners of companies based there, ahead of the Anti-Corruption Summit in May.

Oxfam is urging the World Bank and IMF to work with governments around the world to further reform the international tax system and help prevent tax dodging by wealthy individuals and companies, including action to end the era of tax havens. Tax dodging using tax havens is estimated to cost poor countries $100billion in lost revenues every year.

Related News

Third Africa Think Tanks Summit: Communiqué

Creating a Sustainable Future for African Think Tanks in Support of Agenda 2063 and Sustainable Development Goals

Preamble

-

We, the African think tanks, have met in Victoria Falls, Zimbabwe, on April 8-9, 2016 in the framework of the Third Africa Think Tank Summit. As we conclude our 2016 Summit on the theme “Creating a Sustainable Future for African Think Tanks in Support of Agenda 2063 and SDGs”, we would like to express our deepest and sincere appreciation to the African Capacity Building Foundation (ACBF) for organizing this Summit in partnership with the African Union Commission (AUC), the New Partnership for Africa's Development (NEPAD) and the United Nations Economic Commission for Africa (ECA).

-

We note the convergence of Agenda 2063 and Agenda 2030 and the importance of building the necessary capacity for their effective implementation. This is because despite over a decade-long history of development planning, many African countries continue to experience challenges in designing, implementing and monitoring their development planning frameworks.

-

We also note that think tanks would play a critical role in supporting the continental and global agendas through their support to evidence policy design, implementation and monitoring based on their research and analysis; their capacity development activities for state and non-state actors and through their provision of platforms for stakeholder engagement and dialogue and advocacy.

-

We therefore reiterate the need for pan African institutions including the Africa Capacity Building Foundation (ACBF), African Union Commission, UN Economic Commission for Africa (UNECA), New Partnership for Africa's Development (NEPAD), African Development Bank (AfDB) as well as African countries to involve think tanks in their decision making processes through provision of development/economic intelligence around development planning and domesticating of the Agendas. This is critical for the successful implementation of the Agendas and achieving structural transformation in the continent.

-

We note that the key challenge facing many think tanks within the continent has to do with their sustainability and the diversity of their source of funding. Therefore, the resource mobilization capacity of Africa’s think thanks needs to be strengthened.

African think tanks and the domestication of Agenda 2063 and Agenda 2030

-

We recognize that thinks tanks can and should play an important role in actively engaging and developing methodologies to guide member states in integrating Agenda 2063 and Agenda 2030 in their national planning frameworks. The AUC should provide Guidelines and toolkits that could promote standardized methods of integration of the global and regional agendas and enhance cross country comparisons of performance.

-

We reaffirm that think tanks should contribute to the analytical work around the inter-linkages across the global and African Agendas’ goals and targets and identifying the areas of convergence and divergence that need attention.

-

We reiterate that successful implementation of Agendas 2063 and 2030 must be supported by the think tanks and underpinned by evidenced-based policy-making, including evaluating the interactions between economic, social and environmental policies through policy simulations, ex-ante and ex-poste impact studies, and compiling the datasets needed for further work in this area.

-

We note that think tanks can enrich the monitoring and evaluation of both Agendas 2063 and 2030 based on their respective areas of expertise. Monitoring and evaluating progress of both Agendas will be vital in ensuring that corrective actions are taken to keep implementation on the right track.

Sustainability of think tanks: capacities, networks and partnership

-

We recognize that think tanks can fully carry out their role in supporting the implementation of Agenda 2063 and Agenda 2030 only if they have the necessary capacities and resources, and are able to effectively channel well-packaged, relevant, timely and quality outputs to policymakers.

-

We reaffirm our conviction that the sustainability of African think tanks begins with the quality of its soft, human, institutional and leadership capacities. We, therefore, undertake to work towards the strengthening of their capacities through networking, partnership and exchange programs and trainings. Moreover, we agree on having think tanks innovative use of Information and Communications Technology (ICT) in communicating their research work and reaching out to policy makers.

-

We encourage African think tanks to make more effective use of their interactions using platforms such as the Africa Think Tank Network (ATTN) and Africa Think Tank Summits.

-

We also reaffirm that the Africa Think Tank Summit should be institutionalized and organized regularly on a yearly basis to get African think tanks the opportunity to discuss their common issues together with the potential solutions, exchange knowledge, ideas and best practices, build stronger networks and partnerships, peer-learn, monitor and evaluate their impact in the delivery of the two Agendas.

-

We strongly commit ourselves to support the implementation of Agenda 2063 and Agenda 2030, while creating a sustainable future for our respective think tanks. We are also committed to collectively share best practices, enhance partnerships, networking and synergies in the spirit of pan-Africanism.

-

We welcomed the creation, on November 12, 2015, of the Africa Think Tank Network (ATTN) by ACBF. We acknowledge that the launch of the ATTN is considered as a first and important step towards the effective implementation of the recommendations of the Africa Think Tank Summits. Moreover, the establishment of the ATTN is a critical step to the isolationist tendencies within the think tanks’ community.

-

We reaffirm our conviction that the sustainability of African think tanks is ultimately the responsibility of Africans themselves. It is therefore crucial that think tanks not only serve the public sector but also private sector without neglecting other potential contributors such as international partners and civil society.

Moving forward

-

We express our profound concern that the resources allocated by donors to African think tanks are shrinking along the years. We therefore stress the need to build our individual and collective capacities towards our sustainable existence and call upon AUC, NEPAD, ACBF, UNECA and other supporters of think tanks to help in mobilizing resources towards building this essential capacity in order to sustainably and effectively contribute to the successful implementation of Agenda 2063 and Agenda 2030.

-

We call for continued support to ACBF and other supporters of think tanks to enable them create new think tanks where needed, strengthen the capacities of existing ones and ensure that platforms such as the Africa Think Tank Summits are organized and networks sustained.

-

We resolve to support ACBF to continue providing leadership in coordinating our efforts towards staying engaged and working together in order to efficiently contribute in tackling Africa’s development challenges and ensure our sustainability.

Presented on 9 April at Victoria Falls in Zimbabwe.

Related News

Trade facilitation and regional integration in Africa

On 21 July 2016, UNCTAD and Trade Mark East Africa (TMEA) will host a joint side event at UNCTAD 14. The panel will discuss linkages between trade facilitation reforms and regional integration, with a special focus on the East African Community (EAC). The following article aims at providing some initial considerations for this discussion.

This article discusses two linkages between regional integration and Trade Facilitation in Africa:

First, Trade Facilitation is increasingly important for regional integration, competitiveness and development. Intraregional trade is far lower in Africa than in most other regions and Trade Facilitation should be among the priority areas for policy action and international support.

Secondly, this article also discusses Trade Facilitation measures in view of their regional dimension. For several specific Trade Facilitation reforms, collaboration and cooperation among regional partners is helpful or even necessary. Such collaboration and cooperation itself can provide an additional impetus to further African integration.

The African continent and its Regional Economic Communities (RECs) record less intra-regional trade than most other regions of the world. According to UNCTAD data, intra-African trade amounts to only about 13.8% as compared to intra-regional trade among Latin America countries (22%), Asian countries (52%) and Europe (about 70% for the EU). One of the major factors behind this low level of trade integration is the low level of Trade Facilitation implementation. Africa has a roughly comparable size in terms of population and output as India, yet African countries are separated by 104 international borders between them. Facilitating crossborder trade is key for any further economic integration.

Trade facilitation implementation is also necessary for over-seas trade. It is particularly relevant for the participation of African countries in global value chains and trade in manufactured goods. Especially small and medium-sized enterprises (SMEs) and perishable, time sensitive and intermediate goods sectors in least developed and landlocked developing countries benefit from reduced transaction costs and times. Many Trade Facilitation reforms are in themselves positive steps towards human, enterprise and institutional development. They help small traders- often women- to enter the formal sector, make economic activities more transparent and accountable, promote good governance, generate better quality employment, strengthen IT capabilities, and generally help modernize societies by bringing benefits in terms of administrative efficiency.

Many Trade Facilitation solutions also have a regional dimension in their implementation. By requiring collaboration and cooperation among partner countries, their implementation itself can be a positive step towards further regional integration. It is thus recommended that ambitious Trade Facilitation measures are incorporated into regional integration schemes, including arrangements such as the Continental Free Trade Area for Africa (CFTA) and African Regional Economic Communities (RECs).

Facilitating regional integration and development in Africa

Most African countries are part of regional integration schemes. From the perspective of Trade Facilitation, having more Regional Trade Agreements (RTAs) can lead to a “spaghetti bowl”, requiring more certificates of origin and possibly other documents so as to benefit from preferential tariffs. Obtaining and submitting these documents, in turn, requires more paperwork and potential waiting times. To counter this potentially negative impact of RTAs it is crucial that African countries engage in ambitious Trade Facilitation reforms that contravene the possible additional paperwork.

The Action Plan for Boosting Intra-Africa Trade of the African Union specifically aims at deepening Africa’s market integration and significantly increasing intra-African Trade. To achieve this, the plan is composed of seven clusters, of which Trade Facilitation is one. Other examples of regional programmes that cover Trade Facilitation are the Common Market for Eastern and Southern Africa (COMESA) strategic medium plan, the West African Economic and Monetary Union (UEMOA) Trade Facilitation programme, and the regional indicative strategic development plan of Southern African Development Community (SADC). The Africa Trade Fund by the African Development Bank (AfDB) also specifically targets Trade Facilitation programmes in Africa’s regional organisations.

Compared to other regions, Africa records among the least favourable trade and transport facilitation indicators. The World Bank’s Doing Business 2016, for example, reports the highest documentary compliance time to export (108 hours) and to import (123 hours) for Sub-Saharan Africa. The World Bank’s Logistics Performance Index reports the lowest regional average for SubSaharan Africa. And research by UNCTAD shows that African countries have the lowest level of implementation of Trade Facilitation measures as recorded by the World Trade Organization’s category A notifications under the TFA.

The relationship between Trade Facilitation and development is dynamic. African countries with more capacities, higher trade volumes and financial resources, are in a better position to invest in reforms that make trade faster, easier and more transparent. At the same time, if Africa invests in programs that modernize Customs administrations and trade procedures, it will reap the benefits of more trade, revenue collection and institutional development. African countries that trade more will find it easier to attract financial resources to invest in Trade Facilitation as larger trade volumes help to achieve a higher rate of return on trade related investments. And those African countries that invest in Trade Facilitation will help their trade to grow further.

The regional cross-border movement of goods also requires the facilitation of its transport. This includes the border crossing of vehicles, their drivers, and containers. Transhipment of cargo at the border is costly, as is an empty return voyage if market restrictions do not allow transport companies to pick up cargo in both directions. Efficient transit requires functioning Customs guarantee schemes. Transport infrastructure needs to be planned regionally to take into account cross-border trade flows, vehicle standards, and axle loads. There needs to be mutual recognition of permits, insurances and drivers’ licences. All of the above requires regional collaboration and coordination.

Choosing the right Trade Facilitation measures for regional collaboration

It will be critical that African countries use their existing REC mechanisms to identify which Trade Facilitation measures could benefit from regional coordination or collaboration. The following six criteria are proposed for consideration in the identification process:

-

The measure itself requires or benefits from bilateral cooperation, as is the case for example for border agency cooperation (see Box 1).

-

There are similar needs for technical assistance. For example, large number of countries in the REC may have the same TFA measure notified as category C.

-

A small or weak member of a regional grouping can benefit from the experience and strength of more advanced fellow-members possibly through intra-regional technical assistance and support. Experiences gained in a regional “pilot” country can be passed on to the next country within the region.

-

Implementation could benefit from regional standards and mutual recognition. Examples here can include Customs automation and other technological solutions, as well as AEO schemes.

-

There already exist regional agreements such as common Customs codes. It can also be beneficial to pool resources for updating such regional codes.

-

On-going regional programmes exist to support broader transport and Trade Facilitation integration. Examples here may include trade hubs, TMEA, corridor programmes et al.

In order to support regional aspects of TF implementation, a regional coordinating mechanisms, such as a regional TR Committee should be considered. Hosted within an appropriate regional intergovernmental structure, the Regional Trade Facilitation Committee (RTFC) could be assigned, inter alia, the following mandates.

-

To support, coordinate and monitor the establishment of national Trade Facilitation committees (NTFCs) with the region.

-

To provide a regional platform for the exchange of experiences and expertise

-

To develop and compare KPIs to benchmark and benchmark successful TF implementation.

-

To serve as a regional platform for UNCTAD’s NTFC empowerment programme and other technical assistance projects.

Box 1: TFA Articles with a potential regional dimension

The implementation of several Articles of the WTO Trade Facilitation Agreement (TFA) may have a regional dimension. They may allow for collaboration, or they may require or benefit from working with neighbouring countries or trading partners.

Article 1 (Publication) can be implemented jointly to provide traders with a common platform. Article 1.3 (Enquiry Points) specifically, allows members to “establish or maintain common enquiry points at the regional level”.

Article 5.1 (Notifications for enhanced controls or inspections) could also help traders in neighbouring countries if implemented regionally. Under Article 5.3 (Test Procedures), a “Member may, upon request, grant an opportunity for a second test”; this second test could be undertaken in a third country, possibly under a scheme of mutual recognition of test results.

A number of Customs related measures included in Articles 7 and 10 require regional coordination if the country is member of a Customs union. Pre-arrival Processing as per Article 7.1 can benefit from regional cooperation, especially when involving land-transport. The EAC Revenue Authorities Data Exchange (RADEX), for example, provides advance information to allow Customs to process data before the goods arrive at the land-border. Article 7.6 on the Establishment and Publication of Average Release Times becomes more relevant and interesting if comparable standards and benchmarks are established on a regional level. Article 7.7 (Measures for Authorized Operators) can involve mutual recognition of authorized operators within a region. Article 10.3 encourages the use of international standards. Data models, codes, and document lay-outs should all be harmonized globally. At times, a first step can be harmonization on the regional level.

Article 8.2 (Border Agency Cooperation), specifically requests WTO Members to coordinate procedures at border crossings to facilitate cross border trade. This may include aspects such as working hours, aligned procedures and formalities, common facilities, joint controls and the establishment of one stop border post controls.

Article 11 (Freedom of Transit), as well as several other articles that make reference to transit, aim at facilitating transit trade. Their implementation would ideally take place within broader regional transit or corridor programmes that may also involve infrastructure investments, regional transport markets, or the mutual recognition of licences and certificates.

Article 12 (Customs Cooperation) provides for a wide range of possibilities for cooperation, including through technical assistance, capacity building and information exchange.

Conclusions and the way forward

The special and differential treatment (SDT) provisions included in Section II of the WTO TFA provide a unique opportunity to take Africa’s development into consideration when planning for Trade Facilitation implementation. Developing countries have the opportunity to notify specific Trade Facilitation measures as category B (to be implemented later) and C (requiring financial or technical assistance), and there is a commitment by the international community to provide financial and technical assistance towards TFA implementation.

Given the importance of Trade Facilitation for regional integration, trade competitiveness and development, Trade facilitation should be among the priority areas for policy action and support by the international community.

In addition, there is also a regional dimension in the implementation phase of Trade Facilitation reforms. For several specific Trade Facilitation measures, collaboration and cooperation among regional partners is helpful or even necessary. Such collaboration and cooperation itself can provide an additional impetus to further African integration.

This article was published in the UNCTAD Transport and Trade Facilitation Newsletter No. 69, First Quarter 2016. Updates on the UNCTAD14 side event will soon be posted on http://unctad14.org.

Related News

“Africa Feeding Africa”: New mega initiative to transform agriculture in Africa is focus of international meeting

More than 200 research and development partners and experts will meet at the International Institute of Tropical Agriculture (IITA), Ibadan, Nigeria, in a three-day workshop to discuss a new initiative known as “Africa Feeding Africa”, or the Technologies for African Agricultural Transformation (TAAT) program.

The TAAT program is a critical strategy for transforming agriculture on the continent that would ensure that Africa is able to feed itself through agriculture.

The goal of the TAAT Program includes eliminating extreme poverty, ending hunger and malnutrition, achieving food sufficiency, and turning Africa into a net food exporter as well as setting Africa in step with global commodity and agricultural value chains.

Adopting modernized, commercial agriculture is the key to transforming Africa and the livelihoods of its people, particularly the rural poor.

To carry out these objectives, the African Development Bank (AfDB), working with IITA and other partners, has identified eight priority agricultural value chains relating to rice sufficiency, cassava intensification, Sahelian food security, savannas as breadbaskets, restoring tree plantations, expanding horticulture, increasing wheat production, and expanded fish farming.

The Forum for Agricultural Research in Africa (FARA) and the CGIAR Consortium and 12 of its 15 international agricultural centers active in Africa support this initiative by the Bank and the co-sponsors to revitalize and transform agriculture through the TAAT program within the shortest possible time while restoring degraded land and maintaining or strengthening the ecosystems that underpin agriculture. The April 12-14 workshop is being organized by IITA in partnership with the Support to Agricultural Research for Development of Strategic Crops (SARD-SC) project for the African Development Bank, which is funding this mega initiative.

The identification and preparation workshop is a preliminary step to establishing and operationalizing the program. It will be attended by leading agricultural experts from Africa and beyond, development institutions, research agencies, the private sector, financial institutions, academia, and civil society. The workshop is a response to the Action Plan for Agricultural Transformation in Africa resulting from the AfDB-led high-level conference held in Dakar, Senegal, in October 2015. The major objective is to execute a bold plan to achieve rapid agricultural transformation across Africa and raise agricultural productivity.

This initiative will be led by IITA, the Forum for Agricultural Research in Africa (FARA), CGIAR, national agricultural research systems, and the Alliance for a Green Revolution in Africa (AGRA). This will involve close partnerships among AfDB, the World Bank, and major development partners to ensure increased funding for agricultural research and development along the value chains in Africa. CGIAR, FARA, The World Vegetable Center (AVRDC), Africa Harvest, and other partners will provide the technical and developmental support for the Bank’s quest of widespread agricultural transformation.

“IITA supports AfDB and partners in ensuring that TAAT is effectively set up,” said IITA Director General, Nteranya Sanginga. “The whole CGIAR system is backing this huge initiative with its research infrastructure in collaboration with FARA, AGRA, Africa Harvest, and the national partners. Everybody wants to ensure that this initiative succeeds.”

To date, about 22 African countries have been identified as potential partners with the CGIAR centers in the planning, content, and evaluation of investments in agricultural transformation. This workshop gives an opportunity for more Regional Membership Countries (RMCs) of AfDB to join in this effort.

Related News

Africa’s $30 billion rail renaissance holds ticket for trade

On a sweltering Kenyan morning on the outskirts of a national wildlife park, Chinese and local workers maneuver a massive concrete rail-bridge structure onto towering support piers. In the distance, trucks loaded with shipping containers rumble down a highway.

The bridge at Voi, northwest of the port of Mombasa, is the latest construction frontline for the initial 327 billion-shilling ($3.2 billion) stretch of an ambitious railway project to link the East African country with landlocked neighbors including Rwanda and Uganda. As a faster alternative to the trucks clogging the only road running inland to the capital, the Chinese-built and -financed standard-gauge railway, known as the SGR, has the potential to transform trade in the region.

Kenya’s rail line, the country’s biggest investment since independence in 1963, is among the most advanced of the more than $30 billion of African rail projects planned or under way. Together, they span more than 11,000 kilometers (6,835 miles), enough to connect Cape Town to Copenhagen. It’s one of the bright spots on the world’s least developed continent, where governments are wrestling with drought-induced food shortages, weakened currencies and shrinking budgets following the plunge in commodity prices.

Held Back

“Infrastructure constraints are one of the major things holding back Africa and this standard-gauge railway will make a big difference,” said Mark Bohlund, an Africa and Middle East economist with Bloomberg Intelligence.

Not all the projects will be built on time, if at all, especially with the commodity-price slump weighing on those designed to move raw materials from mines to ports. And with Chinese growth slowing, the nation’s central role in African infrastructure development may diminish. Countries including Kenya and Ethiopia are also borrowing heavily to fund projects.

Already, though, U.S. and European and companies such as General Electric Co., Alstom SA and LafargeHolcim Ltd. are poised to benefit, along with Chinese builders and African suppliers such as Transnet SOC Ltd. GE is investigating opportunities in countries including Kenya, Ethiopia and Nigeria and will have almost tripled its number of service personnel on the continent from 2015 to the end of this year.

West Africa

“The overall bed of opportunities around the region remains strong, at least 50 percent higher than it was 10 years ago,” said Thomas Konditi, GE’s head of transportation for Africa. “Those opportunities are still going to be strong for another five to 10 years.”

Besides the East African line, others on the continent include Bollore SA’s plan to develop a 2,700-kilometer West African rail corridor. The project, which has faced legal challenges from rival developers, would link Ivory Coast, Burkina Faso, Niger and Benin.

Also in West Africa, Senegal signed an agreement in December with China Railway Construction for the renovation of 645 kilometers of railroads. Projects are also planned in Tanzania, Mali and Egypt, while Ethiopia recently completed a line connecting Addis Ababa to Djibouti and has another 4,000 kilometers of projects planned.

Economic Growth

Rail infrastructure is vital to improve trade between African countries, which stood at just 13 percent of the total last year, according to the African Union.

Kenya, which moves about five percent of freight by rail, predicts the new project will add to economic growth. The government sealed agreements in March with Chinese partners to build the rest of the track up to the border with Uganda, which itself has signed construction agreements for the first phase.

Kenya’s initial stretch, from Mombasa to Nairobi, will be ready to start operating by June 2017, Kenya Railways Corp. Managing Director Atanas Maina said in an interview at the Voi bridge. The line will have daily capacity for eight freight trains in each direction, each with the ability to carry the equivalent of more than 100 containers. It’ll also run as many as two daily passenger trains each way.

Colonial Tracks

Besides the often-clotted Mombasa-Nairobi road, the only other land transportation option is the century-old railway completed by the British colonial authorities in 1901. The line operates at a leisurely pace of about 30 kilometers per hour, compared with 120 kilometers per hour for passengers and 80 kilometers per hour for freight that Kenya Railways is predicting for the SGR.

The railway design also accounts for local wildlife movements, said Kenya Railways social environmentalist James Chimera. Kenya Wildlife Service provided locations of animal-crossing corridors so elevated overpasses could allow elephants and giraffes to pass underneath safely, he said.

The Export-Import Bank of China has agreed to fund 90 percent and 85 percent respectively of the first two phases of Kenya’s project, with the government covering the rest.

Chinese History

China has a history of successful railway projects in Africa. The 1,870-kilometer Tazara railway, which linked landlocked Zambia to Tanzania’s Dar es Salaam port, was funded and built by China in the 1970s. Nigerian President Muhammadu Buhari plans to visit China to get funding for railway projects, Vice President Yemi Osinbajo said this week.

Nigeria will struggle to meet its agricultural development targets and improve fuel distribution without “robust" rail infrastructure, Osinbajo said.

Some African mine-related freight rail and port projects have been delayed because of low commodity prices and there has been evidence of a shift towards investing in passenger rail instead, said Maria Leenen, CEO at Hamburg-based transportation consultancy SCI Verkehr. The S&P GSCI index of raw materials has dropped 24 percent in the past year.

Transnet, the South African rail and port operator marketing its train equipment and expertise across the continent as well as investing in rail at home, has seen pressure on its order book from the decline in commodity prices. However, the company continues to see opportunities, according to the head of its engineering and manufacturing unit, Thamsanqa Jiyane. Contracts the company is working on include supplying wagons to Swaziland and passenger coaches to Botswana.

For some African governments, the tougher economic conditions are requiring more imagination for funding rail investments, GE’s Konditi said.

“I’m seeing more interest in creative financing – leasing – and I’ve seen more interest in letting the private sector drive some of the maintenance and service of the rail companies,” he said. “This environment is actually helping people to see things more creatively, in a very modern way.”

Demand for World Bank lending on the rise as countries face headwinds

IBRD/IDA* Support to top $150 billion between FY13 and FY16

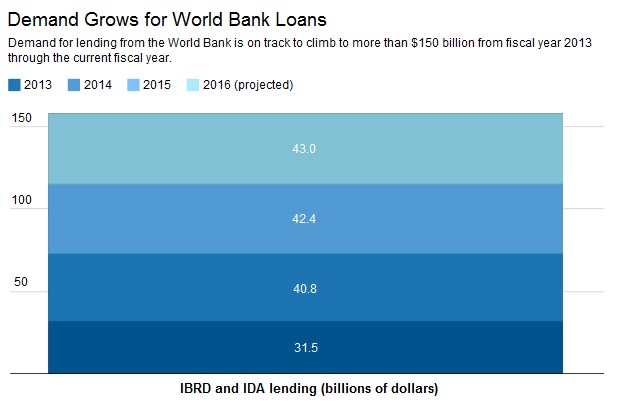

As developing countries continue to face strong economic headwinds, demand for lending from the World Bank has risen to levels never seen outside a financial crisis, and is on track to climb to more than $150 billion in support between FY13 and the current fiscal year.

“We are in a global economy where growth is expected to remain weak, so it is critically important that the World Bank play our traditional role of helping developing countries accelerate growth,” said World Bank Group President Jim Yong Kim. “We have an historic opportunity to end extreme poverty in the world by 2030 but the only way we can achieve this goal is if developing countries – from middle-income to low-income nations – get back on the path of faster growth that helps the poorest and most vulnerable.”

Global economic growth is projected at 2.9 percent in 2016, picking up at a slower pace than previously expected from an estimated 2.4 percent in 2015. However, conditions have generally deteriorated further since the start of the year.

In the face of these challenges, demand from middle-income countries for IBRD lending in our last fiscal year, FY15, was the highest it has ever been outside a financial crisis at $23.5 billion. The Bank expects that FY16 will easily eclipse that record, with lending projected to rise above $25 billion.

A decade ago, in FY06, IBRD lending was at $14 billion; demand from middle-income countries rose to $44 billion in FY10, the peak lending year of the financial crisis. When management reviewed IBRD’s financial capacity in FY10, during the crisis, it was predicted that by FY13, post-crisis lending would drop to pre-crisis levels of $15 billion, which was the average level in real terms for the decade prior to the crisis. IBRD lending hit roughly $15 billion in FY13, but the Bank expects to see demand rise at least $10 billion higher than that in our current fiscal year, FY16, to more than $25 billion. Further, thanks to a record replenishment during the last round of fundraising for the poorest countries, support from IDA, the World Bank Group’s fund for the poorest, this year is also expected to be near historic levels. And demand for non-lending advisory services, to help clients implement important policy changes, is also higher than ever.

An important portion of current lending support has been in the form of Development Policy Financing (DPF), which has backed important reforms client countries have been implementing to help diversify sources of growth and buffer against future shocks. Reforms countries are seeking to implement vary according to the client’s needs and the challenges they are facing.

“Developing country governments are feeling the pressure to find additional ways to accelerate growth, in the current downturn,” said Jan Walliser, Vice President for Equitable Growth, Finance, and Institutions. “Improving long-term growth trends now calls for a broad set of legal, regulatory, institutional, and even logistical reforms that make investing more attractive. Focusing now on structural reform is the recommendation of both mainstream economists and of G20 governments.”

The World Bank Group has longstanding experience in advising on and supporting implementation of country-driven reforms. The Bank offers a unique mix of deep country knowledge, sectoral expertise, and distilled global experience.

“The use of these types of loans are important because the Bank is basically signaling to the financial markets that a country’s reforms are technically solid, the country will follow through on these commitments, and the reforms will help and not hurt the poor and vulnerable,” Kim said. “This is highly complementary to the IMF’s stabilization efforts.”

The World Bank helps support countries’ reforms because they often help accelerate growth, and economic growth has accounted for roughly two-thirds of global poverty reduction in the last half-century. The demand for the World Bank Group’s advice and financing to support those reforms have followed cyclical patterns. Today, with weak growth, the World Bank Group is observing a sharp increase in the demand for DPFs and associated reforms throughout our continuum of clients – from upper middle-income to low-income countries including both commodity exporters and commodity importers.

“The World Bank Group is a cooperative of countries and our role is to work with our clients so that they can achieve their highest aspirations,” Kim said. “But it is now exceedingly clear that we will never end extreme poverty and boost shared prosperity if we don’t tackle global threats like pandemics, climate change and forced displacement in partnership with our member countries – one region, one country and one person at a time.”

* The World Bank’s International Development Association (IDA), established in 1960, helps the world’s poorest countries by providing grants and low to zero-interest loans for projects and programs that boost economic growth, reduce poverty, and improve poor people’s lives. IDA is one of the largest sources of assistance for the world’s 77 poorest countries, 39 of which are in Africa. Resources from IDA bring positive change to the 1.3 billion people who live in IDA countries. Since 1960, IDA has supported development work in 112 countries. Annual commitments have averaged about $19 billion over the last three years, with about 50 percent going to Africa.

Related News

tralac’s Daily News Selection

The selection: Monday, 11 April 2016

The SACU-Mercosur FTA entered into force on 1 April: a Swazi perspective (Times of Swaziland)

Textile companies of Swaziland which were hard hit by the loss of the lucrative duty free market under African Growth and Opportunity Act of the US Government, have found another preferential market that is ready for textile products. The market was opened on 1 April 2016 when the Preferential Trade Agreement between Mercosur and the Southern African Customs Union entered into force, the Times of Swaziland has reported. [Perspective from Uruguay]

India-Mercosur Preferential Trade Agreement: questions and answers (WTO)

The Committee on Trade and Development discussed, 16 March, a goods agreement between Mercosur and India, which the parties are hoping to expand so that it covers a larger share of trade. The trade agreement, which entered into force in 2009, covers over 450 tariff lines for each party according to a factual presentation prepared by the WTO Secretariat. The deal is described as the first step towards the creation of a free trade area among the parties, consisting of Argentina, Brazil, Paraguay, Uruguay and India. Venezuela, a Mercosur member, is not a party to the agreement. The representative of India said that parties to the agreement have agreed on the need to “significantly increase” the number of tariff lines so that it covers a “sizeable portion” of bilateral trade. The latest exchange of request lists to expand the deal's coverage — undertaken in 2013 — is still under review by all sides, said India and Uruguay speaking on behalf of Mercosur.

Ghana: Exports’ bleak future over govérnment's uncertainty on EPA (GhanaWeb)

Currently, the EU leaders are awaiting their ECOWAS counterparts to complete the signing of an EPA they endorsed two years after negotiations on the agreement closed. However, players in the export trade business believe the uncertainty over government’s stance with signing of the EPA before the deadline could be the final nail in the coffin. Major exporters - Pioneer Food Cannery (PFC), Cosmo Seafood Company, West African Fisheries, Golden Exotics, Volta River Estate, Jei-River Farms, Barry-Callebault, ADM and Cargill - whose main market is the European Union are therefore calling on government to sign the EPA in order not to be hit by a tariff hike of approximately 20% on their goods. It will be recollected that while negotiations for a regional EPA were still on-going, an interim agreement was initialled in December 2007 by Ghana and the EU for goods only to avoid paying these tariffs.

China seeks free trade pact with East Africa region (The East African)

Recently, China wrote to the EAC Secretary-General proposing to negotiate with the EAC partner states a comprehensive free trade agreement (EAC-China FTA). China also requested to undertake a joint feasibility study with the EAC on the proposed FTA, outgoing Secretary-General Richard Sezibera informed the Council of Ministers at a meeting in Arusha. The Council directed the Secretariat to undertake a comprehensive cost-benefit analysis on the implications of negotiating FTAs with third parties. “We are working on the directive of the Council,” EAC spokesperson Richard Owora said. He said they expect to conclude the work by June 30. However, East African Business Council executive director Lillian Awinja cautioned that free trade with China would hinder EAC industrialisation. [Made in China, counterfeited for Nigeria (The Guardian)]

COMESA Transporters and Logistics Services Industries Dialogue: recommendations (CBC)

The following are some of the key outcomes of the meeting (17-18 September, Nairobi): The meeting recognised the strength of political will that has seen the fast tracking of infrastructure corridors along Eastern and Southern Africa. The great need to form a regional sectoral workgroup to increase collaboration amongst the private sector stakeholders for development of common positions and sharing of information and best practices on trade and transport facilitation was acknowledged. Member states are requested to support the request for a Pan African Logistics Information Hub which will be a depository of documentation requited for movement of goods between countries. The facility should be accessible to all corridor users and other stakeholders, ranging from manufacturers, logistics services.

Tanzania: Govt outlines plans for infrastructure overhaul (IPPmedia)

President John Magufuli's administration has unveiled its blueprint for a radical overhaul of the country's infrastructure, including the construction of standard-gauge railway lines, multi-lane roadways, and strategic bridges that could potentially transform Tanzania into a regional transport hub. The government is figuring to finance the projects by borrowing $800 million from international financial markets, and is also considering issuing an infrastructure bond. The Ministry of Finance and Planning released the new development plan this [past] week as part of its draft 2016/17 budget proposals where the government is targeting to spend a total of 29.53 trillion/-.

Dakar-Abidjan Highway: ECOWAS ministerial

The Ministerial meeting, scheduled to take place on 14 April 2016 in Banjul, would involve member states of the Dakar-Abidjan corridor of Senegal, The Gambia, Liberia, Sierra Leone, Guinea, Guinea Bissau and Cote d’Ivoire. The Dakar-Abidjan corridor has a high level of economic importance in the region and will serve to complement the Abidjan-Lagos corridor which is part of a larger African Union project- the Trans-African Highways Network. Technical experts from the roads/infrastructure/works/transport sectors and the Justice ministries from Member states involved in this phase of the project will assess the feasibility, detailed designs, funding options as well as the appropriate legal framework which will govern the development of the highway.

ECOWAS Corridor Development and Management Strategy and Action Plan: EOI from USAID Trade and Investment Hub

The study shall: i) design an ECOWAS Corridor Development and Management Strategy, ii) draft an Action Plan for implementing the strategy over a period of 20 years, iii) through a hierarchy of corridors, identify corridors where Corridor Management Institutions (CMI) can be established, iv) advise on a regional approach to establish CMIs and propose a regional coordination mechanism for all corridors, drawing from lessons learnt in other regions and adapting implementation modalities to West Africa, v) define the viability of identified corridors and corridor projects and establish a short, medium and long-term financing plan, vi) advise how a pilot CMI can be established on selected corridors such as the Tema– Ouagadougou and Abidjan–Bamako Corridors as test cases.

Tanzania's tax paradox: 'When beer is worth more than gold' (IPPMedia)

But according to a new report by the state-run Tanzania Minerals Audit Agency, the total taxes paid by the top companies dealing in gold mining in 2015 was 355.33 billion/-; a measly sum compared to the 476bn/- paid by TBL as tax during the same year. In other words, last year the country’s top beer producer alone paid 34% more tax than the entire large-scale gold mining industry, despite the latter being one of the country’s key economic sectors. Similarly, while the total value of minerals sold by major gold mines in Tanzania last year was worth $1.63bn (3.56 trillion/-), the total tax paid by the mining firms represents less than 10% of their revenues. On the other hand, TBL said in its 2015 annual report that it posted total sales of 1.07 trillion/- last year, with the total taxes paid to the government in 2015 representing 44.5% of its revenues.

Panama Papers: statement by Thabo Mbeki, Chair of HLP on Illicit Financial Flows (UNECA)

Kenya got oil: what next? (World Bank Blogs)

And finally, on the third, implementation, two mechanisms are paramount: designing a sovereign wealth fund, following a rule-based framework to prevent political interference, and managing expectations around oil revenue-sharing at three levels: intra-county (within Turkana); inter-county (Turkana and other counties); and between Turkana and the national government. Are these arguments overly cautious? Perhaps yes, but for a good reason. The figure below provides a tale of three oil producing countries: Malaysia, Republic of Congo, and Angola. [Kenya's oil production goals keep shifting (Daily Nation)]

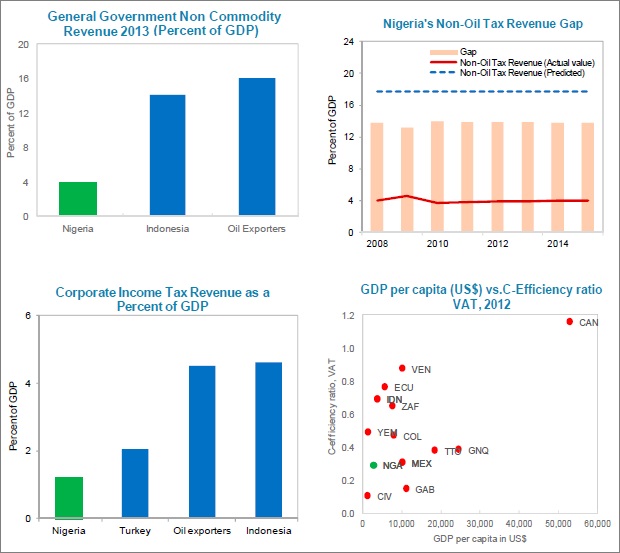

Nigeria: 2016 Article IV Consultation (IMF)

The large permanent terms-of-trade shock requires a significant macroeconomic adjustment. It is important to initiate urgently an integrated package of policies centred around: (i) a fundamental change in the nature of government; (ii) reducing external imbalances (including real exchange rate realignment); (iii) further safeguarding the resilience and improving the efficiency of the banking sector; and (iv) implementing structural reforms for inclusive growth. The policy measures envisaged in the draft 2016 budget with aggressive revenue mobilization efforts and a shift from recurrent to capital spending are in the right directions, though more is needed. Outward spillovers via regional trade channels: The foreign exchange restrictions are impacting exporters in trading partners such as South Africa, while the growth slowdown is adversely impacting growth in neighbouring countries, mainly through informal trade and rapidly growing cross-border bank channels—for example, it is estimated that a 1% reduction in Nigeria’s growth generates a 0.3% reduction in Benin’s growth. [Related: Selected Issues paper]

ECOWAS: Why and when to introduce a single currency (AfDB)

The creation of a single currency in West Africa remains a timely and relevant project, despite post Euro zone crisis uncertainties and the postponement, for the fourth consecutive time, of the introduction of a single currency in member countries of the West African Monetary Zone. To reduce the likelihood of a new postponement which could dent the credibility of this important project, the authorities should prioritize the Big Bang option in 2020, consisting in all ECOWAS member countries adopting the single currency as from 2020. West Africa’s heavyweights, namely Cote d’Ivoire, Ghana, Guinea, Nigeria and Senegal, could assume a leadership role and encourage all stakeholders to take ownership of the project. [The authors: Ferdinand Bakoup, Daniel Ndoye]

Appointment of Marcel Alain De Souza as new ECOWAS President

West Africa Trade and Investment Hub: Chief of Party opportunity (Abt)

Profiling South Africa-China’s agricultural trade relationship (AGBIZ)

Traditionally, South Africa has had a net deficit in terms of the agricultural trade balance. South Africa has imported more agricultural products from China than it exports in 13 of the last 15 years. It is only in the last two years that South Africa has attained a positive trade balance for agriculture with China. Bilateral trade in agricultural products has been relatively small in terms of share of total trade, ranging between 2% and 6% of total trade over the past decade and a half. The share of total trade has, however, averaged 3% between 2012 and 2015. The drop in South Africa’s agricultural imports from China was mainly attributed to the decline in apples (-30%), kidney beans (-70%), glucose and glucose syrup (-17%), animal feed preparations (-33%), sugar confectionary (-12%), and plain weave cotton fabrics (-17%), among others. South Africa’s agricultural exports have increased over the same period by 24% - from $295m 2012 to $366m in 2015. Driving this growth are several products, which include macadamia nuts, grapefruit, peaches, oranges, fine animal hair and grape wines, among others. [The author: Tinashe Kapuya] [FAO Food Price Index]

China goes global with development banks (Bretton Woods Project)

Two of China’s policy banks, the CDB and the C-EXIM, already hold more assets than the combined sum of the assets of the Western-backed multilateral development banks. Table 1 shows that the C-EXIM and the CDB have over $1.8 trillion in assets, whereas the Western-backed banks hold just over $700bn. That said, the CDB’s international holdings are just 30% of total assets, putting the two banks’ international assets at around $0.5 trillion. These banks provide concessional and non-concessional (in the case of the C-EXIM) finance in virtually every corner of the world. China has also pioneered a host of bilateral and regional development funds. These funds combine to add upwards of $100bn in development finance provided by the Chinese in recent years. Table 2 exhibits the major funds that we were able to confirm. [The authors: Rohini Kamal, Kevin P Gallagher]

Kebs faults international standards (Daily Nation)

Kenya on Friday sought to be included in the international standards-setting committee for electrical and electronic items. Kenya Bureau of Standards Managing Director Charles Ongwae said some finished products imported into Kenya are below par as their standards ignore local environmental conditions. The MD urged professionals in electro-technical fields to seek positions in international committee saying Kenya has representatives in four committees but is not represented in four other committees.

Kenya to get Sh6bn Chinese loan amid concern over heavy debt

BRICS Dispute Resolution Shanghai Centre: update

IFPRI's 2016 Global Food Policy Report will be launched tomorrow.

CII's Naushad Forbes: 'We will push for an outward-looking trade policy to boost global access'

US and Turkish agencies team up to target African business

Jubilee Debt Campaign: 'World’s poorest countries rocked by commodity slump, strong dollar'

Kevin Watkins: 'Africa's great opportunity for reform'

Humanitarian response in Africa: the urgency to act (UN)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

Swaziland textile companies get a lifeline

Textile companies of Swaziland which were hard hit by the loss of the lucrative duty free market under African Growth and Opportunity Act (AGOA) of the US Government, have found another preferential market that is ready for textile products.

The market was opened on April 1, 2016 when the Preferential Trade Agreement between MERCOSUR and the Southern African Customs Union (SACU) entered into force, the Times of Swaziland has reported.