Search News Results

IMF regional consultation with the West African Economic and Monetary Union

On March 21, 2016, the Executive Board of the International Monetary Fund (IMF) concluded the annual Discussion on Common Policies of Member Countries of the West African Economic and Monetary Union (WAEMU).

Background

Despite the fragile security situation in some member countries and a less favorable external environment in 2015, economic growth exceeded 6 percent for the second consecutive year, driven by ongoing infrastructure investments, solid private consumption, and favorable agricultural campaigns. Inflation has remained subdued around 1 percent in 2015, reflecting the exchange rate anchor and positive terms of trade developments. Monetary policy has remained accommodative, with the key policy rate unchanged at 2.5 percent since September 2013, and private sector credit grew by nearly 14 percent in 2015.

The overall budget deficit (including grants) increased to 4.8 percent of GDP in 2014, up from 3.3 percent in 2013, largely driven by ongoing large public investment programs to address countries’ infrastructure gaps. This deterioration increases public debt for the region to 44.7 percent of GDP in 2015 from 38.9 percent in 2014.

The drop in oil prices has lightened the energy bills for all WAEMU countries while cocoa and groundnut prices have remained buoyant, thereby improving the trade balance, notably of Cote d’Ivoire, the largest economy in the region. However, the surge of imports associated with public investment and private consumption has partly offset the impact of lower energy bills. As a result, in 2015 the region’s overall current account deficit reached 5.6 percent of regional GDP, compared with 6.1 percent in previous year, and gross international reserves rose to 5 months of imports from 4.7 months in 2014.

The medium-term growth outlook remains positive but entails significant downside risks. Growth should remain above 6 percent, owing to continued strong domestic demand, while inflation is expected to remain subdued. The overall fiscal deficit should gradually decrease while total public debt is projected to stabilize at moderate levels (about 40 percent of GDP). In the short term, security risks remain high. In the medium term, weaker trading partner growth, tighter global financial conditions, sluggish implementation of structural reforms, and difficulties delivering on the planned fiscal consolidation could weaken growth prospects.

WAEMU: Staff report on common policies of member countries

The region continues to experience strong growth in 2015, and the immediate outlook is positive. Inflation is projected to remain low, reflecting the exchange rate peg and positive terms of trade developments. However, risks are on the downside. In the short term, security risks remain high. In the medium term, weaker trading partner growth, tighter global financial conditions, sluggish structural reforms, and difficulties delivering on the planned fiscal consolidation could weaken growth prospects.

Policy recommendations

The challenge is to sustain the growth momentum while preserving internal and external stability in an uncertain global landscape.

-

Fiscal policy. Pursuing fiscal consolidation while meeting development needs will require steadfast implementation of reforms to increase domestic revenue, rationalize current spending, improve public financial management, increase public investment efficiency and further strengthen debt management.

-

Monetary policy. Macroeconomic conditions do not warrant a tightening of monetary policy. Action is needed, however, to enhance monetary transmission mechanisms. This will require improving liquidity management, deepening financial markets, and strengthening market-based operations.

-

Financial sector. The authorities should pursue the reform agenda to strengthen risk-based supervision, align prudential limits with international standards and best practices, and avoid regulatory forbearance. Financial deepening will also be critical.

-

Competitiveness, diversification, and inclusion. Strong resolve is needed to move ahead with long-awaited structural reforms to boost competitiveness and diversification, improve the business environment and enhance inclusion

Recent economic developments

Growth remains robust and inflation subdued. While average economic growth in Sub-Saharan Africa has been slower than expected, reflecting weak commodity prices and difficult financing conditions, economic activity in the WAEMU remained strong. Regional real GDP growth is estimated to have reached 6.4 percent in 2015, driven by ongoing infrastructure investments, solid private consumption, and favorable agricultural campaigns. Inflation remained subdued reflecting the exchange rate anchor and positive terms of trade developments.

The fiscal deficit widened further. The overall fiscal deficit has largely been driven by ongoing large public investment programs. It is estimated to have reached 4.6 percent of GDP in 2015 up from 3.4 percent in 2014. This deterioration brings the regional deficit more than 2 percentage points higher than the average of the last 10 years.

The current account deficit remains large in spite of lower energy prices. The drop in oil prices has lightened the energy bills for all WAEMU countries while cocoa and groundnut prices have remained buoyant, thereby improving the trade balance, notably of Cote d’Ivoire, the largest economy in the region. However, the surge of imports, associated with public investment and private consumption has partly offset the impact of lower energy bills. Thus, the region’s overall current account deficit has improved somewhat from 6.1 to 5.6 percent of regional GDP. Gross international reserves (GIR) have slightly increased, supported by a stricter implementation of the obligation to repatriate export receipts. The net foreign asset (NFA) position of commercial banks, however, has continued to deteriorate. This appears to reflect commercial bank sales of foreign currency to meet client needs, exceeding corresponding purchases from WAEMU central banks or from exporters.

The external position is sustainable but vulnerabilities remain. Model-based assessments indicate that the current account and real effective exchange rate are broadly in line with fundamentals. Regional reserve coverage, even after assuming that BCEAO reserves would be used to replenish commercial banks’ NFA drawing, remains adequate – provided the current account deficit stabilizes over the medium term – according to traditional metrics and under the zone’s monetary arrangement with France.

Outlook and Risks

The outlook remains positive. Over the projection period, growth should remain above 6 percent, owing to continued strong domestic demand and stronger agricultural production. Meanwhile, inflation is expected to remain subdued over the medium term. The overall fiscal deficit should gradually decrease while total public debt is projected to stabilize at moderate levels (about 40 percent of GDP). The current account deficit (including grants) would stabilize slightly above 6 percent of GDP over the medium term because of fiscal consolidation and rising exports. FDI and capital transfers are expected to remain the main source of external financing. Reserve coverage would remain stable.

The outlook is subject to significant downside risks.

-

The projected economic growth assumes the realization of reforms to spur private investment. In particular, growth in most WAEMU countries anticipates progress in the efficiency of infrastructure investment, reforms of the energy sector, a more inclusive financial sector, and improvements in the business climate. If structural reforms fail to materialize, growth prospects could falter.

-

Fiscal consolidation is required to maintain macroeconomic stability and thus the sustainability of the currency peg.

-

Security-related risks remain high in several countries. Islamist groups remain active in Mali and Niger with potential spillovers to neighboring countries. Beyond the immediate human toll, security issues would affect economic activity, strain budgets and undermine foreign investment to the region.

-

On the external side, a further slowdown in global growth, and/or tighter global financial conditions, could affect macro-fiscal stability, foreign direct investment, and other external flows (Box 2). Lower cocoa and groundnut prices would also adversely affect exports. Overall, external growth shocks could reduce WAEMU growth by up to 1.5 percentage point.

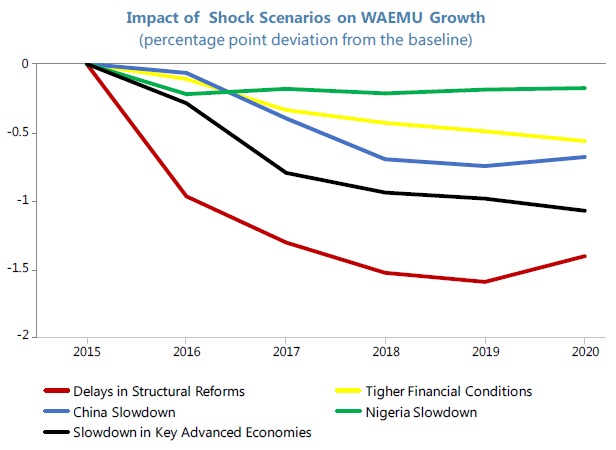

Box 2. WAEMU: Risks for the Regional Economic Outlook

We estimate the possible effects of identified domestic and external downside risks on the WAEMU outlook (See companion Selected Issues Paper). First, we simulate the impact of (i) country-specific delays in structural reforms and (ii) tighter or more volatile global conditions which would result in higher financing costs for governments and (iii) we model the impact of a growth slowdown in key advanced economies, China, and Nigeria. Results show that the materialization of these risks would reduce real aggregate WAEMU GDP growth by up to 1.5 percentage points through different channels.

-

Delays in structural reforms. For most WAEMU countries, growth projections under the baseline scenario assume the realization of growth-enhancing structural reforms including improvements in PFM, better incentives for private sector activity, higher investment efficiency etc. Country assessments of a delay in those reforms show substantially lower domestic investment growth coupled with less external financing, reflecting mainly a significant reduction in private and foreign investment due to a less favorable business climate. This scenario would result in a lower WAEMU economic growth by about 1-1.5 percentage points compared to the baseline scenario.

-

Tighter global and, therefore, regional financing conditions in 2016-17. While regional exposure to global financial markets remains limited, increased financing costs could affect the region through higher regional risks premia and availability of external and regional financing. Overall, WAEMU growth could be reduced by about 0.6 percentage points compared to the baseline scenario, owing to lower private investment.

-

Lower growth in key advanced economies. Result show that a 1-percentage point lower growth in key advanced economies would reduce WAEMU real GDP by about 0.8 percent after two years and about 1 percent at the peak after five years.

-

Lower growth in China. A slowdown in China would directly affect regional exports and investment flows. WAEMU countries could also be affected through cross-border spillovers from the Euro area and other emerging market partners. A 1-percentage point lower growth in China would lower WAEMU real GDP by about 0.5 percent in the short term. It is worth noting that the effects of a lower growth in China have increased over time, and also become more heterogeneous across all countries. Finally, lower growth, driven by a slowdown in the manufacturing sector has significant spillover effects suggesting a potential important role of China rebalancing process on the region.

-

Lower growth in Nigeria. Spillovers from Nigeria are the lowest: a 1-percentage point lower growth in Nigeria would reduce WAEMU real GDP by only 0.2 percent after 3-4 years.

Aggregate numbers hide diverse situations across countries: the impact of shocks is larger in countries with higher trade openness (Benin, Senegal, and Burkina Faso) and benefitting from higher investment levels from China (Niger and Togo). Transit and informal trade are major spillover channels of regional shocks (Benin, Togo) while regional linkages increase through rapidly growing cross-border banks.

Selected Issues Paper

Public investment efficiency in WAEMU: An empirical assessment

WAEMU countries are projected to increase public investment volumes significantly to close the region’s infrastructure gap. This gap is relatively large and has been widely identified as a growth bottleneck. The WAEMU’s infrastructure needs are substantial. In particular, WAEMU countries are lagging behind sub-Saharan African benchmark countries in electricity supply, paved road density and telecommunication infrastructure. Insufficient or inefficient infrastructure reduces the return to trade and economic activity and constrains growth prospects. To close this gap, many WAEMU countries are envisioning to significantly boosting public capital expenditure in the medium-term. On average, staff projects that public capital expenditures will increase to around 9.5 percent of GDP in 2015 to 2019, up from an average below 8 percent in 2011-14.

In addition to the infrastructure gap, however, the region’s infrastructure is also perceived as being of relatively low quality, and investment efficiency appears low. The most recent World Economic Forum’s (WEF) Global Competitiveness Indicators ranks WAEMU countries 110 out of 148 countries, behind the sub-Saharan African average and sub-Saharan African benchmark countries. The quality of electricity supply, railroads and roads scored below sub-Saharan benchmark countries’ average as well. At a comparable level of real public capital stock, WAEMU’s overall infrastructure quality is perceived as lower than that of regional peers.

There is substantial room to improve public investment efficiency in WAEMU, in particular by improving the quality of institutions. The analysis finds that WAEMU’s public investment efficiency seems weak relative to that of the best performers in SSA, using efficiency frontiers. The regression analysis suggested that stronger institutions could reduce the public investment efficiency gap in WAEMU. WAEMU countries need to evaluate the strength of their PIM practices and identify country-specific PIM institutional priorities for reform. Improving public investment efficiency, in turn, could help boost growth and speed up progress in realizing the development agenda.

Fiscal space in WAEMU

The Need for Scaling Up

WAEMU countries need to mobilize substantial financial resources to address the infrastructure gap, which has been widely identified as a growth bottleneck. Many studies find that inadequate infrastructure impedes growth. Infrastructure development was estimated to have contributed about 1 percentage point to per-capita growth in West Africa in 2001-05. For Benin, Domínguez-Torres and Foster (2011) estimate that infrastructure contributed 1.6 percent points to per capita growth; while in Senegal, Torres, Briceño-Garmendia, and Dominguez (2011) find the contribution was about 1 percent point. Also, raising the two countries’ infrastructure endowment to that of Africa’s middle-income countries could boost annual growth by 3.2 and 2.7 percentage points respectively. Recent reports also confirmed a continued infrastructure bottleneck in other WAEMU countries.

To finance the scaling up of public investment while preserving macroeconomic stability, WAEMU countries have to use their fiscal space efficiently. While WAEMU countries’ external debt levels declined owing to the heavily indebted poor countries (HIPC) multilateral debt relief initiative, leaving some scope for external borrowing, the availability of financing at attractive terms is limited. Also, some countries’ total government debt has increased considerably since those countries received the debt relief, which suggests that caution is warranted in additional borrowing.

Therefore, it is essential for the sustainable financing of scaling up infrastructure investment that the two major channels for creating fiscal space be used. These channels are increasing tax revenue and increasing the efficiency of spending.

Raising Tax Revenue

Improving tax collection remains the main channel for enlarging the fiscal space. This has been well recognized in the WAEMU, which has a convergence criterion of 20 percent for the tax-to-GDP ratio, even though several member countries have not been in compliance with this criterion for years.

The WAEMU’s relatively high indirect tax rates have not resulted in higher tax collection. Indirect tax rates in the WAEMU are higher than the average rates in sub-Saharan Africa and in low-income countries, especially for goods and services taxes and trade taxes. However, higher rates have not generated higher revenues. Roughly, the tax-to-GDP ratio has been below the sub-Saharan Africa average throughout the observation period (2000 to 2011), and just broadly in line with the low-income countries average. Looking at the trend over time, the WAEMU’s tax-to-GDP ratio improved from 11.7 percent of GDP in 2000 to 14.7 percent of GDP in 2011, driven by a broad trend in all member countries except Côte d'Ivoire, where results were affected by internal conflicts. However, the size of improvements varied considerably among the countries. For instance, Benin’s total tax revenue increased by 2.1 percent percentage points, while Togo’s total tax revenue rose by 6.6 percent percentage points.

Looking at the performance tax by tax, the improvement in the WAEMU’s tax ratio is driven by higher collection from income tax and goods and services taxes, while trade revenues are broadly flat due to limited trade liberalization.

-

Trade taxes: In contrast with sub-Saharan African and low-income countries, where weighted average tariff rates declined, reflecting trade liberalization over the last decade, the WAEMU’s tariff rates dropped only marginally and the tax-to-GDP ratio has remained broadly stable over time. In the comparator groups, sub-Saharan Africa’s drop in trade tax revenues reflects the rate decline, while it seems that low-income countries were able to offset the rate decline by efficiency measures that allowed these countries to broadly preserve the trade- tax-to-GDP ratio.

-

Personal income taxes: The WAEMU increased the tax-to-GDP ratio from about 3 to close to 4 percent of GDP, but it remained below the ratios for low-income countries and subSaharan Africa.

-

Goods and services taxes: The francophone tradition of relying more on direct than on indirect taxation is reflected in the relatively higher rates. This translates into a higher level of tax revenues than is the case in comparator countries by around 0.6 to 0.8 percent of GDP. Also, the improvement in the WAEMU countries over the observation period was most pronounced in this tax category.

WAEMU countries show considerable variation in the drivers for revenue collection by tax categories. For example, in Togo, income tax revenue declined from 2.9 percent to 2.5 percent of GDP, but goods and service tax revenue rose sharply from 2 percent to 9.2 percent of GDP. In Benin, the revenue gain was driven by higher trade tax revenue, while goods and services tax revenue declined. In Cote d’Ivoire, however, the decline in tax revenue was mainly driven by falling trade tax revenues.

Our analysis suggests that WAEMU countries are ahead of comparator countries in their total tax collection, but have room to improve income tax collection. In 2011, total tax collection in the WAEMU exceeded the potential revenue by around 6 percent and 12 percent when compared with low-income countries and sub-Saharan African countries respectively. This shows an improvement compared to 2000 when the WAEMU’s total tax collection was below potential by around 4 percent compared with both low-income and sub-Saharan African countries. The following factors explain this trend:

-

Goods and services taxes: The relative improvement between 2000 and 2011 was mainly driven by a more positive goods and services tax gap. However, higher tax rates in the WAEMU explain at least part of this positive tax potential.

-

Trade taxes: Despite the higher average tariff, our tax potential analysis indicates only a moderately positive tax gap in 2011. However, improvements of the trade tax revenue compared 2000 range from below to slightly above potential for both benchmark groups.

-

Income taxes: Revenue performance as measured by the tax gap deteriorated from around - 1½ percent to around -5½ percent compared with the gap in sub-Saharan African countries, and closed only slightly from around -3½ percent to around -2 percent with respect to the low-income country benchmark.

WAEMU countries have substantial room to improve domestic tax collection. WAEMU countries have recently initiated reforms towards trade liberalization, most notably, the introduction of a common external tariff for all Economic Community of West African States countries in January 2015. While the implementation will be gradual, it is expected that trade revenues will decline. Therefore, it is important for the WAEMU to enhance its domestic tax revenue base, in particular, income tax revenues, where both analytical approaches indicate room for improvement by around 0.8 to 2 percent of GDP.

Improving spending efficiency

Is there scope for creating fiscal space by improving the efficiency of public spending? Our analysis focused on the technical efficiency of translating public spending into the corresponding results by comparing WAEMU’s input-output performance in public spending to those of other sub-Saharan African countries with similar levels of development. In addition, to reflect WAEMU countries’ aspirations to accelerate growth, specific comparisons with the fast-growing non-resource rich sub-Saharan African countries were provided. Quantitative assessments were conducted through a nonparametric data envelopment analysis (DEA). While public spending covers many sectors, only the education and health sectors were analyzed because these are sectors in which public spending plays a major role, and consistent cross-country data are readily available. Furthermore, based on data for 2008-12, we estimated the potential budgetary savings from higher efficiency in education and health to better inform policy discussions.

Financial stability, development and inclusion in the WAEMU

Based on most recent indicators of stability, deepening and inclusion, this paper provides comparative evidence of the situation of WAEMU in several areas of financial development relative to groups of benchmark countries. A regression of the volatility of growth on financial development highlights that the volatility of growth in the WAEMU over the last decades could have been substantially lower if financial development was at the levels of Asian or African benchmark groups.

While growth of credit to the economy is robust, there are significant gaps in the financial development in the region. Credit to the economy continues to grow robustly at around 15 percent year on year and the average WAEMU country’s credit to GDP level is in line with its macroeconomic fundamentals. However, the region is facing challenges in other dimensions of financial development. On the regulatory and financial stability side, prudential standards in WAEMU are weak by international standards and not well enforced. Indicators of financial inclusion have improved recently but are lagging behind both a group of African (Ghana, Kenya, Lesotho, Rwanda, Tanzania, Uganda, and Zambia) and Asian (Bangladesh, Cambodia, India, Laos, Nepal, and Vietnam) countries with whom the WAEMU shared similar levels of development in the 1990s but which have since then experienced faster growth.

As these benchmark countries have also experienced a decline in the volatility of growth over the same horizon, the question arises in how far this observed stability has been driven by developments in the financial sector. Growth in the WAEMU has been volatile, even when excluding large movements in real GDP per capita growth in Cote d’Ivoire due to episodes of political instability. As African and Asian benchmark countries which have on average succeeded to increase financial development more strongly, have also witnessed lower volatility of growth over the last decade, the question arises to what extent further financial development in the region could mitigate these growth swings. To answer this question, this note uses the recently developed index of financial development by Sahay and others (2015), and tests for its economic and statistic significance in a panel regression, together with standard determinants of growth volatility. The results suggest that difference in financial development in the WAEMU compared to the African and Asian benchmark countries can account for 10 percent of the difference in the volatility of growth between the WAEMU and these groups in the last decades. In addition, as pointed out by Sahay and others (2015), a more developed financial sector could also boost growth itself.

Developments in Banking and Financial Stability

The WAEMU’s banking sector has been growing at a steady pace over the last few years, with variations across member countries. This growth which averaged 15 percent a year reflects the continuing development of banking activities and products and their reach in the WAEMU area. It also underscores an increasing contribution to finance the economy. While credit to the private sector remains one of the main banking activities, banks sovereign exposures appear to be on the rise reaching more than 26 percent of total assets in 2015.

Developments in Financial Access

Access to financial services has increased in most WAMU countries but remains lower than in benchmark countries. Access to financial services, as measured by the share of the population with a bank account, has increased significantly in most WAMU countries from 2011 to 2014. The share of the population with an account has more than doubled in Senegal from almost 6 to almost 12 percent, and Niger from a low level of 1½ percent to almost 3½ percent. Benin, Togo, and Mali have seen increases of more than 50 percent in these shares. Moreover not all groups of the population have benefited equally from this increase in access. Financial access gaps across gender, age, education and income remain relatively high, and have even increased in some cases. The share of the population in possession of a debit or credit card also remains multiple times lower in WAEMU countries as compared to the benchmark groups.

Developments in Microfinance

While micro-finance activities have been steadily increasing in WAEMU, they are still low relative to those of the banking sector. There were around 724 Micro-finance Institutions (MFIs) at end June 2015. Their deposits and credit activities witnessed a steady average annual increase of 12.2% and 9.9% respectively. However, the size of these activities is still very low compared to banking sector. While microfinance institutions have been a strong tool to promote financial inclusion in WAEMU, they have posed some challenges, including weak credit management, poor governance, lacking information systems and internal controls, weak application of prudential rules, and existence of some MFIs without proper licenses. In order to address these issues, WAEMU authorities have proceeded to liquidation and license revocation of many MFIs and closure of a large number of unlicensed MFIs. Some of the solutions taken by WAEMU authorities were also to regroup some small MFIs into networks, ensure a close monitoring of problematic MFIs and place some of them (13 as of June 2015) under temporary administration. Moreover, the initiatives taken by the BCEAO to establish a regional financial inclusion strategy and the creation of a credit information reporting system for MFIs are also additional tools to enhance the stability of this system and allow it to play its intended role.

Composite Measure of Financial Development

A composite measure helps rank the WAEMU’s performance in terms of financial development across several dimensions. The new broad-based index of financial development by Svirydzenka (2016) and Sahay and others (2015) helps benchmarking the WAEMU against benchmark groups according to its financial institutions and markets. The composite measure of financial inclusion suggests that the WAEMU lags behind benchmark groups with respect to the development of financial institutions and markets. While the WAEMU’s level of financial development was similar to that of other regions in the 1980s and 1990s, it was outperformed, especially by the Asian benchmark group in the 2000s and today. While there is a significant difference between the WAEMU’s performance in financial institutions compared to the Asian benchmark, the difference is even larger for the financial markets index. In particular, the financial market development appears insignificant in most WAEMU countries, except for Cote d’Ivoire. However, these low levels are comparable to the group of African benchmark countries.

Financial Development and Volatility of Growth in the WAEMU

This section tries to assess how further financial development could contribute to reduce the volatility of growth in the WAEMU. Building on Sahay and others (2015), we regress rolling standard deviations of growth (five-year period ending in current year) on the financial development index and a set of controls – initial GDP per capita (PPP), trade and financial openness, energy exports in percent of GDP, the volatility of foreign growth, gross capital inflows to the region excluding the country in question, terms of trade changes, the polity index, transition and offshore center dummies, growth of GDP per capita and the government balance. The results suggest that higher financial development is associated with lower volatility of growth and the relationship is weakening at higher levels of financial development.

Income inequality, gender inequality, and growth in the WAEMU

There is robust evidence that higher income inequality can impede growth. Lower net income inequality has been associated with faster and more sustained economic growth in both advanced and developing countries. With imperfect credit markets, income inequality prevents an efficient allocation of resources by decreasing poorer households’ ability to make investments into human and physical capital. Higher income and wealth inequality can also lead to socio-political instability and poor governance, thus discouraging investment.

The evidence that gender inequality is impeding economic growth is also growing. Gender inequality has been associated with worse growth and development outcomes. Gender gaps in economic participation restrict the pool of talent in the labor market and can yield a less efficient allocation of resources, lower productivity and hence lower GDP growth. Since women are more likely than men to invest a large proportion of their household income in the education of their children, higher economic participation levels and earnings by women translate into higher expenditure on school enrollment for children. IMF (2015) highlights reductions in gender inequality as one of the most promising avenues to boost growth in the region – together with closing gaps in infrastructure and education. It shows that decreasing income and gender inequality in sub-Saharan African countries to levels observed in the ASEAN 5 (Indonesia, Malaysia, the Philippines, Thailand and Vietnam) could increase real GDP per capita growth by about 1 percentage point on average.

This paper has shown that both lower income inequality and lower gender inequality could boost real GDP per capita growth in the WAEMU, in addition to previously identified policies. The results emphasize that gender inequality of outcomes and opportunities is very high, and policies to mitigate these inequality are particularly promising. In particular, closing gender gaps in education would not only stimulate growth from a more efficient allocation of resources, it would in addition increase total education in the region, thus boosting growth further. Lower gender inequality has also been associated with a more equal income distribution which in turn is also associated with higher growth. This note confirms previous findings that the region could benefit from boosting infrastructure and human capital and strengthening of institutions.

The following policies could help reduce income inequality and gender inequality:

-

Remove legal inequalities between men and women. For example, Namibia equalized property rights for married women and granted women the right to sign a contract, head a household, pursue a profession, open a bank account, and initiate legal proceedings without the husband’s permission in 1996. In the decade that followed, Namibia experienced a 10 percentage point increase in its female labor force participation rate. Lower gender gaps in female labor force participation, in turn, have also been associated with lower income inequality.

-

Foster education. This could not only increase productivity through a more efficient allocation of resources but in addition boost overall education levels, a pre-requisite for sustained growth.

-

Boost infrastructure, including through improving access to water and increased electrification of the region. This could not only boost growth directly but in addition free women’s time to go to school and join the labor market since girls and women are most cases the main providers of household work.

-

Reduce the regressivity of fiscal spending and taxes. In particular, replace across-the-board subsidies with well-target social transfer schemes.

-

Foster financial inclusion, including for women (see SIP on financial inclusion and stability)

In promoting policies to reduce gender and income inequality, this paper does note pose any normative judgment on countries social and religious norms but argues for a level playing field, for all agents in the economy being able to explore their economic potential – if they so choose.

Assessing risks for WAEMU economic outlook

Risks to the regional outlook are skewed to the downside. As shown in the 2016 WAEMU Staff Report on Common Policies of Member Countries, the outlook for the region is positive but with downside risks. On the domestic side, delays in implementing structural reform may lower regional growth prospects. The positive outlook of the baseline scenario assumes, indeed, timely and effective implementation of several domestic reforms such as (i) enhancing the efficiency of spending and improving the quality of public investment; (ii) creating additional fiscal space to meet development needs while safeguarding macroeconomic stability and debt sustainability; (iii) increasing financial access and inclusion while preserving financial stability; and (iv) boosting competitiveness and diversification, improving the business environment and enhancing inclusion. On the external side, the growth slowdown in China or tighter or more volatile global conditions would also affect WAEMU members. While regional exposure to global financial markets remains limited, increased financing costs could influence the region through higher regional risks premia and availability of external and regional financing. A sharper-than-expected slowdown in China would directly affect regional exports and investment, flows. WAEMU countries could also be affected by cross-border spillovers from the Euro area and other emerging market partners.

Country-specific simulations indicate that delays in structural reforms would lower WAEMU economic growth by 1-1.5 percentage points compared to the baseline scenario. The domestic risk scenario assumes a delay in key reforms at each individual country level (and at the regional) level. These reforms can be related to fiscal consolidation, improvement in public finance management, infrastructure investment, the energy sector, the financial sector, or business climate. As these reforms are already – to the certain point – integrated in the countries’ baseline projections, their delay has an immediate impact on the consolidated WAEMU economic performance. Assuming inertia in structural reforms, domestic investment growth would be lower by about 2.5-3 percentage points compared to the baseline, reflecting mainly a significant reduction in private investment due to a less favorable business climate than assumed in the baseline scenario. Domestic consumption growth is projected to be lower by about 1.2 percentage points compared to the baseline. Lower domestic demand is expected to immediately reduce imports while export growth would decline more gradually reflecting lower competitiveness of the region. The current account balance (excluding grants) is projected to improve by about 0.5 percentage point of GDP, on average. The overall fiscal balance (excluding grants) is expected to improve by about 0.6 and 0.2 percentage point of GDP in 2016 and 2017, respectively, due to lower public investment. However, with falling fiscal revenue, the overall fiscal balance would deteriorate by about 0.1 percentage point of GDP over the medium term. Delays in structural reforms would put strains on external financing; lowering substantially current transfers and official loans up to about one percentage point of GDP in favor of more short-term portfolio inflows. This scenario would result in a small cumulative reduction in WAEMU official reserves of about US$ 0.2 billion.

Simulations show that tighter global conditions in 2016-17 would affect WAEMU growth mainly through lower investment. A global financial volatility scenario assumes a reassessment by investors of underlying risks and a disorderly overshooting in the normalization of risk premia across the globe, leading to higher corporate default rates, heightened money market spreads, and depressed consumer and investor demand throughout the world. Under this scenario, lower risk appetite among investors reduces the availability of both external financing and capital inflows to the region by about one percentage point compared to the baseline. While regional exposure to global financial markets remains limited, increased financing costs impacts financing at the regional sovereign bond market. Initially, the governments are expected to maintain investment efforts and face higher debt service, which would contribute to an increase in the overall fiscal deficit. Private investment growth on the other hand is projected to slow down by about 0.5 percentage point, on average, compared to the baseline. Over the medium term, as external financing for the region is expected to resume slowly, more costly regional financing would lead to lower public investment growth by about 0.8 percentage point compared to the baseline. Overall, this scenario would reduce WAEMU growth by about 0.6 percentage points, on average.

Global and regional growth shocks will impact economic growth in WAEMU countries. We model the impact of lower growth in key economic partners of the region:

-

Lower growth in key advanced economies. Result show that a 1-percentage point lower growth in key advanced economies would reduce WAEMU real GDP by about 0.8 percent after two years and about 1 percent at the peak after five years.

-

Lower growth in China. A slowdown in China would directly affect regional exports and investment flows. WAEMU countries could also be affected through cross-border spillovers from the Euro area and other emerging market partners. A 1-percentage point lower growth in China is estimated to lower WAEMU real GDP by about 0.5 percent in the short term. It is worth noting that the effects of a lower growth in China have increased over time, and also become more heterogeneous across all countries. Finally, lower growth, driven by a slowdown in the manufacturing sector has significant spillover effects suggesting a potential important role of China rebalancing process on the region.

-

Lower growth in Nigeria. A 1-percentage point lower growth in Nigeria would reduce WAEMU real GDP by 0.2 percent after 3-4 years.

Spillover effects become more important with the strengthening of trade and financial linkages. The above results suggest that the impact of growth shocks in China and Nigeria is larger in countries with higher trade openness, less diversified export structure, and with larger investment from China. For instance, a 1-percent point lower growth in China reduces real GDP by 1.2 percent at the peak in countries with more trade openness as Benin, Senegal, and Burkina Faso compared to 0.4 percent for less open economies. The results also indicate that a lower growth in China reduces real GDP by 1.2 percent in WAEMU countries where Chinese investment has been above the regional average, such as Niger and Togo. However, spillover effects are smaller for countries with a more diversified export structure as Cote d’Ivoire and Senegal. Cross-border banking groups – with ten pan-African banks already present in the SSA region and, at least, three in the WAEMU and neighboring Nigeria – constitute another rapidly developing shock propagation channel.

Related News

Seventeenth Session of the Regional Coordination Mechanism (RCM) for Africa: Calls for a transformative path on Sustainable Development and Agenda 2063

The Seventeenth Session of the Regional Coordination Mechanism (RCM) for Africa kicked off on 2nd April 2016 at the United Nations Economic Commission for Africa (UNECA) Conference Centre in Addis Ababa, Ethiopia, amidst reiterated calls for coordination in the implementation of the African Union’s Agenda 2063 and the global Sustainable Development Goals (Agenda 2030).

RCM-Africa – a platform for the UN system to support the African Union and its member countries to implement global, and continental development goals in Africa – will play a key role in making this a reality.

The meeting was highly attended by high officials from the African Union Commission (AUC) led by the Chairperson of the AU Commission, H.E Dr. Nkosazana Dlamini Zuma; the UN Under-Secretary General and Executive Secretary of the ECA, Mr. Carlos Lopes; the Representative of the UN Deputy Secretary General, Under Secretary General and UN Special Adviser on Africa, Maged Abdelaziz; high officials from UN agencies and Systems; the African Development Bank; the NEPAD Planning and Coordinating Agency; the World Bank and the IMF; and AU Member States.

The deliberations called for strengthening of partnership, accountability, progressive monitoring and evaluation system, and transformative path to the economic development of Africa through syncing the Agenda 2063 and the Sustainable Development Goals (SDGs).

Officially opening the meeting H.E. Dr. Nkosazana Dlamini Zuma, stated that one important lesson from the Millennium Development Goals (MDGs) in Africa is that initial conditions invariably influenced the pace of progress on global development agendas. However, each region has to consider both what it has and it’s aspirations in order to meet obligations to its citizens as well as global obligations.

She indicated that, it comes as no surprise in the technical analysis of the goals of Agenda 2063 and the Sustainable Development Goals that there is over 90% convergent. The implementation of the Agenda 2063 priorities will help in meeting the sustainable development goals. “The RCM in 2015 agreed on the need for joint implementation, and this 17th RCM must therefore focus on the practicalities of this at continental level with the Regional Economic Communities (RECs),” noted the AUC Chairperson. She further acknowledged the recommendations on the reconfigured RCM clusters based on the agenda 2063 10 year Implementation Plan, on the concrete joined programs for implementation at continental as well as regional level with the sub regional mechanisms.

“The implementation of Agenda 2063 will really help us meet the Sustainable Development Goals of ending poverty, zero hunger or quality education, water, sanitation, protecting the planet, gender equality, reducing inequalities and ensuring prosperity for all,” added Dr. Dlamini Zuma. “An integrated, peaceful, prosperous Africa that is driven by its own citizens is in the interest of the whole humanity.”

Mr. Carlos in his remark said the timing of the seventeenth session of the RCM is auspicious because it is occurring in the aftermath of the adoption of the Agenda 2063 which aims to support the vision of an integrated, prosperous and peaceful Africa, driven by its own citizens representing a dynamic force in international arena. He highlighted that both Agenda 2063 and 2030 contain global and regional specific interventions that if effectively implemented, can propel the continent on a transformative path for sustainable development.

Mr. Lopes noted that, though African countries also have their own development plans and strategies, the greatest challenge policy makers’ face is how to implement these frameworks in a coherent and integrated manner. Dr. Carlos further added that in order for support to be truly effective, UN bodies have outlined works for the priority of the AU in a coordinated and coherent manner which is a fundamental role of the RCM for Africa.

He emphasized on the need to strengthen engagement with the science community which may be a necessary solution to seek answers to some of the vexing challenges posed by climate change among others, underlining the need for global partnership which can also be a solution to tackle some of the key socio-economic development challenges facing the African continent.

“There is no doubt that global partnerships can provide the impetus for tackling the key socio economic challenges currently facing Africa. Global partnerships can work for Africa if they are aligned with the strategic objectives of the continent and buttressed by a unified continental voice… We have the opportunity to model what such a partnership could be,” said ECA Executive Secretary. He added that global partnership can therefore work for Africa if they are aligned with the strategic vision of the continent and backed by a unified voice from the continent.

Speaking on behalf of UN Deputy Secretary-General Jan Eliasson, Mr. Abdelaziz, UN Special Adviser on Africa said: “What is critical for us today is what the implementation of the UN-AU partnership and the implementation of Agenda 2063 and 2030 agenda for sustainable development entail: both agendas are wide and comprehensive, together they will be therefore addressing a range of political, economic, social, and environmental challenges for Africa.”

Mr Abdelaziz recommended that RCM Africa prioritize multi stakeholder and public-private partnerships, facilitate joint work to support national efforts to domesticate and implement both Agenda 2063 and Agenda 2030, help address the perennial problem of lack of resources.

He lauded the joint commitment and efforts of the AU and UN in achieving milestones with the RCM with the view of harnessing cooperation between both institutions the United Nations and the African Union through the cluster system. Enabling joint planning and programming of a range of issues including social, economic, agriculture, peace and security, governance, Human Rights and gender free values.

“Furthermore, the RCM has improve synergy and coordination, avoiding duplication, enabling a better use of resources and facilitating joint advocacy in communication and outreach,” he noted.

Held under the theme: “Toward an integrated and coherent approach to the implementation, monitoring and evaluation of Agenda 2063 and the sustainable development goals”, the 17th Session of the Regional Coordination Mechanism for Africa deliberated on the UN-African Union partnership for the implementation of Agenda 2063 and the Sustainable Development Objectives (SDGs); the African Year of Human Rights with a particular focus on the Rights of Women; Movement, Migration, Youth and Gender Empowerment; Regional Integration, Infrastructure and Trade; and Strengthening the Regional Coordination Mechanism for Africa for an effective Implementation of Agenda 2063 and the SDGs.

The RCM meeting ended on Sunday 3rd April 2016.

Background

The United Nations General Assembly (UNGA), through its resolution 1998/46, makes the holding of regular inter-agency meetings an imperative for all regions. Accordingly, regional coordination mechanisms (RCMs) were initiated in 2002 as frameworks for consultations among agencies, programmes, organizations, funds and offices of the United Nations working at the regional level. In the case of Africa, the RCM-Africa has evolved from serving as a consultative mechanism into holding formal, annual sessions at which organizations and agencies of the United Nations system operating in Africa share information on their respective activities and agree to coordinate their strategies for programme delivery in support of the African Union programmes.

Furthermore and based on the mandate derived from UNGA resolution 57/7, the United Nations system in Africa was called to coordinate its activities through the RCM-Africa, in line with NEPAD adopted as the overarching development framework for Africa and other priorities of the African Union and its organs and regional and subregional organizations. RCM-Africa serves as a vehicle for enhancing coordination and coherence by engaging, more and more, in the joint planning and programming of United Nations activities in order to deliver as one in response to the needs and priorities of the African Union and other regional and subregional partners.

The annual RCM-Africa sessions have become a forum for assessing effectiveness of cooperation, collaboration and coordination between the United Nations and the African Union organs and other regional and subregional organizations, with the aim of enhancing the effectiveness of United Nations support for Africa’s development. It is in the spirit of past sessions that the United Nations system working in Africa have chosen for the theme of the seventeenth session of RCM-Africa to be: AU-UN Partnership for the implementation of the Agenda 2063 and Sustainable Development Goals.

Africa’s economic performance over last decade has been very robust, growing in the last two years around 4 percent which is higher than the global average of 2.5 percent. Africa has also registered remarkable progress on several socioeconomic indicators despite low initial conditions. Despite the positive performance, much more needs to be done to increase employment for the youth, reduce poverty and improve access to health and education services.

Studies in ECA show that the relatively high level of poverty is linked to the structure of most African economies. African countries are largely dependent on commodities which are exported with little or no value added and therefore not much employment is generated. That is why Africa needs to embark on commodity-based industrialization and through that create decent job opportunities, which in tend will lead to substantial reductions in poverty and the minimization of income and wealth inequalities.

Agenda 2063 and the 10-year Implementation Plan

The Agenda 2063, a plan for Africa’s structural transformation, was agreed upon by African Heads of State at the African Union Golden Jubilee Summit of May 2013. Based on the Solemn Declaration, the Summit pledged to develop and pursue a transformational Agenda through eight key areas: (a) African identity and renaissance; (b) the struggle against colonialism and the right to self-determination of people still under colonial rule; (c) an integration agenda; (d) an agenda for social and economic development; (e) an agenda for peace and security; (f) democratic governance; (g) determining Africa’s destiny; and (h) Africa’s place in the world.

The Agenda is founded on the AU vision of “an integrated, prosperous and peaceful Africa, driven by its own citizens and representing a dynamic force in the international arena.” The Agenda also builds on the AU Constitutive Act and Regional frameworks. In addition, the process takes cognizance of and reviewed national, regional and existing and past continental frameworks such as PIDA, CAADP and MIP, including the Monrovia Declaration, the Lagos Plan of Action, and the Abuja Treaty among others.

The Agenda is also anchored on the AU vision and is based on the seven aspirations derived from the wide consultations, namely:

-

A Prosperous Africa based on inclusive growth and sustainable development;

-

An Integrated Continent, Politically United, based on the ideals of Pan Africanism and the Vision of Africa’s Renaissance;

-

An Africa of Good Governance, Respect for Human Rights, Justice and the Rule of Law;

-

A Peaceful and Secure Africa;

-

An Africa with a strong Cultural Identity, Common Heritage, Values and Ethics;

-

An Africa whose development is people-driven, especially relying on the potential offered by its women and youth; and

-

Africa as a Strong, Resilient and Influential Global Player and Partner.

The aspirations reflect the desire of Africans for prosperity and well-being, for unity and integration, for a continent of free citizens and expanded horizons, with freedom from conflict and improved human security. They also project an Africa of strong identity, culture and values, as well as a strong and influential partner on the global stage making equal contribution to human progress and welfare – in short a different and better Africa. There are transitions to the aspirations and each milestone of the transition provides a step towards the attainment of the end goal of the aspirations by 2063.

The aspirations embed a strong desire to see a continent where women and the youth have guarantees of their fundamental freedoms and where they assume a leading role in the development of African societies. They are based on the conviction that Africa has the potential and capability to converge and catch up with other regions of the world and thus take her rightful place in the world community.

The Agenda 2063 is expected to be implemented in phases of ten years. The first phase of ten years has been crafted to cover the period 2013-2023 and addresses the following:

-

Sustainable inclusive economic growth.

-

Human capital development.

-

Employment creation.

-

Social protection.

-

Gender/women development and youth empowerment.

-

Good governance and capable institutions.

-

Infrastructural development.

-

Science, technology and innovation.

-

Peace and security.

-

Culture, arts and sports.

The First Ten Year Implementation Plan of Agenda 2063 (FTYIP) calls on African countries to fast track the implementation of flagship programmes identified to have immediate positive impact on growth: the integrated high-speed train network; the Great Inga Dam project; the single aviation market; the outer space programme; the Pan-African e-Network; an annual African consultative platform; the virtual university; the African passport and the free movement of persons; the Continental Free Trade Area; silencing the guns by 2020; the development of a commodity strategy; and the establishment of the continental financial institutions, including the African Central Bank by 2030.

In addition, the implementation strategy of Agenda 2063 spells out 20 goals and 34 priority areas. The goals and priorities include: poverty reduction; the expansion of education at all levels; improved maternal and child health, water and sanitation facilities; industrialization of the African economy; greater resilience to the effects of climate change and prioritized adaptation; modernized farming methods for increased production, productivity and value-addition; better and more sustainable management of natural resources, including mineral and agricultural resources; the establishment of a continental free trade and a significantly developed intra-African trade; and a well-developed infrastructure network.

Furthermore, the observance of good governance, the rule of law and human rights, and the cessation of all intercountry and intracountry conflicts on the continent are also goals to be attained by 2023. Also to be achieved are goals in the realm of culture – full engagement with the African diaspora, the development and wider use of African languages, and the growth of the creative arts and cultural industries. The greater empowerment of women and young people is also an important goal to be pursued as is the need to increase Africa’s presence and voice in global affairs.

The Sustainable Development Goals (SDGs)

The UN General Assembly has adopted sustainable development goals (SDGs). The SDGs come at a time when billions of people are living in poverty and inequalities within and among countries are on the ascendance as well as enormous disparities of opportunity, wealth and power. There is also recognition of the challenge of gender inequality, rising unemployment, particularly youth unemployment, threats to global health, conflict, violent extremism, terrorism and related humanitarian crises and forced displacement of people. Natural resource depletion and climate change, especially increases in global temperature, sea level rise, and their impact on coastal areas and low-lying coastal countries, including many least developed countries and small island developing States, are among the list of challenges that continue to reverse much of the development progress made in recent decades.

The SDGs are made up of 17 goals and 169 associated targets. The goals were globally agreed upon through an inclusive process of intergovernmental negotiations and takes account of different national realities, capacities and levels of development and respecting national policies and priorities. The targets are defined as aspirational and global, with each Government setting its own national targets guided by the global level of ambition but taking into account national circumstances. Each Government will also decide how these aspirational and global targets should be incorporated into national planning processes, policies and strategies.

Africa’s input into the development of the SDGs was through the Common African Position (CAP). The CAP, which has the same tenants of the Agenda 2063, is Africa’s consensus on the continent’s challenges, priorities and aspirations, and the strategies for dealing with them. It is the view of the African Union that the Agenda 2063 is in sync with the SDGs because most of the recommendations of the CAP were taken on board by the UNGA and therefore there is an alignment between the Agenda 2063 and the SDGs.

Need for a common approach to the implementation of the Agenda 2063 and the SDGs

African countries have committed to the implementation of the SDGs as well as the Agenda 2063. The countries also have their own development plans and strategies. It is therefore important to have a common strategy for the implementation of both framework so as to achieve the goals and targets and minimize the challenges associated with implementing both agendas.

Most of the SDGs are in congruence with the goals of Agenda 2063. For example, Goal 1 of the Agenda 2063 aims at: “A High Standard of Living, Quality of Life and Well Being for All Citizens.” The achievements of SDG 1 (end poverty in all its forms everywhere), SDG 2 (end hunger, achieve food security and improved nutrition and promote sustainable agriculture), SDG 6 (ensure availability and sustainable management of water and sanitation for all), SDG 7 (ensure access to affordable, reliable, sustainable and modern energy for all), SDG 8 (promote sustained, inclusive and sustainable economic growth, full and productive employment and decent work for all), SDG 10 (reduce inequality within and among countries), and SDG 12 (ensure sustainable consumption and production patterns) is clearly consistent in achieving Goal 1 of the Agenda 2063. The alignment between most of the goals of the Agenda 2063 and the SDGs provide an opportunity to implement both within a single framework without unduly burdening policymakers with multiple development frameworks.

Equally important is a need for better coordination to ensure effective implementation and follow-up, addressing areas of convergence as well as those unique to Africa. That is why a coherent and common framework that integrates both Agenda 2063 and the SDGs into national planning framework is needed. The SDGs attempts to respond to the global dimensions of Africa’s development challenges while Agenda 2063 responds to the regional dimension. Implementation of both will therefore require: advocacy and sensitization about the details of both frameworks; strengthened capacities to integrate in a coherent fashion, such initiatives in national planning frameworks; and research to support evidence-based policymaking.

Accompanying a common framework for the implementation of Agenda 2063 and the SDGs should be a monitoring and evaluation (M&E) tools. These tools will reinforce the culture of managing for results with regards to the implementation of the common framework. An M&E framework, by setting targets/milestones, will also ensure that all parties involved work towards achieving the development goals. It also ensures that the causes of non-performance are identified and addressed through evaluation processes.

Related News

Finding fortune at the bottom of the ocean: Africa’s Blue Economy prospects are exciting but not without challenges

Thirty-eight of Africa’s 54 states are at the coast and two-thirds of Africa’s equivalent land mass lies in its maritime zones under the sea. More than 90% of the continent’s trade is conducted by sea.

This highlights the enormous opportunity presented by water in the continent’s future, delegates at African Development Week.

The statistics supported the case for the continent and countries to develop “blue economies” to support their quest for sustainable growth and economic transformation.

The continent not only benefits from an extensive coastline, it also has some of the biggest fresh water sources in the world. The Great Lakes in central Africa contain the largest proportion of the world’s surface fresh water – 27%, a statistic that makes it a globally strategic resource.

Lake Victoria is the third largest freshwater lake in the world. By volume and depth Lake Tanganyika is the third largest. These are all strategic assets for Africa that are underutilised but represent enormous opportunity to develop new economic activity and more sustainable development.

The inherent opportunities for African in this undeveloped area led the ECA to take the vision for a Blue Economy a step forward with a new publication, Africa’s Blue Economy: A policy handbook, which was launched on 2 April at African Development Week 2016.

Leading the discussion at the launch, ECA Executive Secretary Carlos Lopes thanked Dr Nkosazana Dlamini-Zuma for her role in initiating the project and putting the blue economy in the mainstream of Agenda 2063.

In the African Union’s 2050 Africa’s Integrated Maritime Strategy (AIM) the Blue Economy is described as the “new frontier of African Renaissance”.

The African Union has indicated that the blue economy could be a major contributor to an Africa wide shipping industry.

“We have a hidden treasure under our seas which needs to be revealed and help us to transform the continent,” said Dr Lopes, adding that two-thirds of Africa’s equivalent land mass lies under the sea and large areas of these waters were part of countries’ territorial waters.

Mauritius, for example, had territorial waters that were more than a thousand times the land mass equivalent of the island.

But Africa is still facing multi-faceted challenges preventing it from fully optimising Blue Economy assets.

For example, the size of water resources makes their access, sustainable use and management, as well as preservation and conservation, a daunting challenge for most African states.

Geopolitical issues are also a challenge. The increasingly intense use of the oceans and seas in several economic sectors, combined with the impacts of climate change, has added to the pressure on the marine environment.

Rapid urbanisation is leading to increased pressure on coasts and marine resources. Other threats include: piracy and armed robbery, trafficking of people, illicit narcotics and weapons, weather issues, rising sea levels and ocean acidification, illegal and unregulated fishing, pollution and habitat destruction.

Insufficient knowledge of resources as well as related rights and obligations for African states leads to capacity gaps. A number of maritime and transnational aquatic boundaries are not formally delimited. Insufficient awareness of the applicable legal frameworks and dispute resolution mechanisms and other related capacity gaps exacerbate the problem.

The uncertainty created by undemarcated borders can lead to tension between neighbouring countries. Additionally, this uncertainty may discourage investment and leave countries reticent to move forward with cooperation or joint development activities.

This article is published in the African Development Week Roundup - Day 4 by IC Publications.

Foreword

Africa’s aquatic and marine spaces are an increasingly common topic of political discourse; its natural resources have remained largely underexploited but are now being recognized for their potential contribution to inclusive and sustainable development. This “Blue word” is more than just an economic space – it is part of Africa’s rich geographical, social, and cultural canvas.

Through a better understanding of the enormous opportunities emerging from investing and reinvesting in Africa’s aquatic and marine spaces, the balance can be tipped away from illegal harvesting, degradation, and depletion to a sustainable Blue development paradigm, serving Africa today and tomorrow. If fully exploited and well managed, Africa’s Blue Economy can constitute a major source of wealth and catapult the continent’s fortunes.

Africa’s economies continue to grow at remarkable rates, including through the exploitation of the rich endowment of land-based natural resources and commodity exports. Converting this growth into quality growth, through the generation of inclusive wealth, within environmental limits and respecting the highest social considerations, requires bold new thinking. It also involves the creation of jobs for a population on the rise.

The Blue Economy offers that opportunity. For example, the International Energy Agency estimates that ocean renewable energy has a power potential sufficient to provide up to 400% of global current energy demand. Other estimates indicate that in 2010 the total annual economic value of maritime related activities reached 1.5 trillion euro. It is forecasted that by 2020, this figure will reach 2.5 trillion euro per year. Surely, Africa needs holistic and coherent strategies to harness this potential.

All water bodies, including lakes, rivers, and underground water, in addition to seas and the coast are unique resources, yet neglected and often forgotten. The largest sectors of the current African aquatic and ocean-based economy are fisheries, aquaculture, tourism, transport, ports, coastal mining, and energy. Additionally, the Blue Economy approach emphasizes interconnectedness with other sectors, is responsive to emerging and frontier sectors, and supports important social considerations, such as gender mainstreaming, food and water security, poverty alleviation, wealth retention, and jobs creation. The Blue Economy can play a major role in Africa’s structural transformation.

The approach advocated in this Policy Handbook is premised in the sustainable use, management and conservation of aquatic and marine ecosystems and associated resources. It builds on principles of equity, low carbon footprint, resource efficiency, social inclusion and broad-based development, with the jobs agenda at the centre of it all. It is anchored on strong regional cooperation and integration, considers structural transformation as an imperative for Africa's development and advocates for a complete departure from enclave development models. Instead, through better linkages to other sectors of the economy, it situates the aquatic and marine economies as part of integrated ecosystem services based on the harvesting of living and non-living resources, benefitting both costal, island states and landlocked countries.

Biotic resources allow Africa to expand its fishing, aquaculture, mariculture sectors and foster the emergency of vibrant pharmaceutical, chemical and cosmetics industries. The extraction of mineral resources and the generation of new energy resources provide the feedstock to resource-based industrialisation and places Africa at the centre of global trade in value-added products, no longer a supplier of unprocessed raw materials. Central to this agenda, is the need to modernise Africa's maritime transport and logistics services, its port and railway infrastructure, improve its reliability and efficiency with the view to seamless link the continent's economies to national, regional and global value chains as well facilitate tourism and recreation activities, just to name a few.

Africa has salutary examples of maritime, riparian and river-based cooperation and dispute settlement. This includes examples of maritime and transnational aquatic boundary delimitation and demarcation. A collaborative approach for the development of the Blue Economy will create the foundation for the formulation of shared visions for transformation. The Blue Economy development approach is an integral part of African Agenda 2063. Building on the experience with implementing Green Economy principles for a transition to low-carbon development, we are seeing an increasing number of African member States formulating Blue Economy strategies to diversify their economic base and catalyze socioeconomic transformation.

This Policy Handbook, offers a step by step guide to help African member States to better mainstream the Blue Economy into their national development plans, strategies, policies and laws. It is a timely contribution to help the continent harness its “New Frontier”.

Related News

Africa Regional Integration Index: Report 2016

Integration Matters

Regional integration is a development priority for Africa. All Africans, not just policy makers and decision makers, have a role to play in making integration a reality for the continent.

Integration matters in Africa. It affects what people can buy; the variety of what is on offer at the local market; how easily citizens move between countries; where individuals travel for leisure or for work; how cost-effective it is to keep in touch; where people choose to study or look for a job; how to transfer money to family or get start-up capital for a business.

Regional integration is about getting things moving freely across the whole of Africa. This means getting goods to move more easily across borders; transport, energy and telecommunications to connect more people across more boundaries; people to move more freely across frontiers, and capital and production to move and grow beyond national limits.

Africa’s integration journey towards a more connected, competitive and business-friendly continent is underway and its roadmap is, in some areas, under construction. Africa’s Regional Integration Index is an action tool measuring the progress of an Africa on the move.

The Index

Measuring where Africa stands on regional integration gives an assessment of what is happening across the continent and is an important way of highlighting where the gaps are. It is a dynamic, evolving way to track integration by giving everyone access to verified, quality information to start a dialogue and take forward the next steps to integrate Africa.

Index Makeup

The Index is made up of five Dimensions, which are the key socio-economic categories that are fundamental to Africa’s integration. Sixteen Indicators (based on available data), which cut across the five Dimensions, have been used to calculate the Index. Further details are set out in Table 1.

The Index 2016 report covers Member Countries from the eight Regional Economic Communities (RECs) recognized by the African Union. The Dimensions and Indicators chosen for the Index are based on the Abuja Treaty and its operational framework.

Regional integration is cross-border and multi-dimensional. Indicators that have a cross-border interaction, and where verified, quality data is available, have been used to make up the Index. Future editions of the Index will grow in scope as more data becomes available.

Index Impacts

The Index aims to be an accessible, comprehensive, practical and results-focused regional integration tool that focuses on the policy level and on-the-ground realities.

-

Accessible: a centralized data system on regional integration will be made publicly available to inform policy decisions and drive policy reforms on priority areas.

-

Comprehensive: the 16 Indicators that make up the five Dimensions of the Index build an overview and dimensional view of Africa’s regional integration.

-

Practical: at-a-glance rankings and scores for RECs, and for countries within a REC, overall and by Dimension. Countries are classed as high performers, average performers or low performers within each REC.

-

Results-focused: comparative analysis within and among RECs takes into account the diversity in Africa’s integration process. A REC, and a country within a REC, can identify its strengths and gaps across each of the Dimensions.

RECs can be compared on overall integration scores and on scores in each of the five Dimensions. As the Index recognizes and uses the RECs as the building blocks for the African Economic Community, based on the Abuja Treaty, there are no overall country rankings.

A country’s classification within a REC shows (with a 95% confidence interval) when a country is a:

-

High performer – score is higher than average of countries

-

Average performer – score is within the average of countries

-

Low performer – score is below the average of countries

As some countries are members of more than one REC, they have multiple rankings/scores. To see the distance they have to travel overall, as well as in particular Dimensions, countries can be compared against the average scores of the top performing countries in a REC. For a REC with six or more countries, the reference is the average of the top four countries.

The Regional Economic Communities (RECs) are regional groupings of African states. The RECs have developed individually and have differing roles and structures. Generally, the purpose of the RECs is to facilitate regional economic integration between members of the individual regions and through the wider African Economic Community (AEC), which was established under the Abuja Treaty (1991). The 1980 Lagos Plan of Action for the Development of Africa and the Abuja Treaty proposed the creation of RECs as the basis for wider African integration, with a view to regional and eventual continental integration.

The AU recognizes eight RECs:

CEN-SAD – Community of Sahel-Saharan States

COMESA – Common Market for Eastern and Southern Africa

EAC – East African Community

ECCAS – Economic Community of Central African States

ECOWAS – Economic Community of West African States

IGAD – Intergovernmental Authority on Development

SADC – Southern African Development Community

UMA – Arab Maghreb Union

Roadmap for the Future

To get the dimensions of regional integration to work together will take a series of actions on the ground, led by well thought-out strategies, matching policy reforms and backed up by capacity building.

It will take political commitment and leadership as well as resources and networks to be mobilized. At the same time it will take engagement from Africa-wide organizations, regional bodies, governments, policy makers, business, civil society, researchers, development partners, the media and the public.

Measuring where Africa stands on regional integration gives an assessment of what is happening across the continent and is an important way of highlighting where the gaps are. It is a dynamic, evolving way to track integration by giving everyone access to verified, quality information to start a dialogue and take forward the next steps to integrate Africa.

The Index is part of a central database and system for collecting data on regional integration. It will capture additional data for indicators that are not part of the Index but that play a role in regional integration, from the movement of workers across borders to trade corridor costs.

It is over to the Index user to make use of the information in the rankings and scores, by drilling down to priority areas, to drive concrete change at policy and operational level.

Regional integration overall in Regional Economic Communities

Index findings are in line with progress being made on RECs’ regional integration agendas. The RECs score highly on areas that they have prioritized on regional integration to date. The different RECs’ performance on the Dimensions reinforces how progress is being made through a regional approach to integration in Africa rather than through a continent-wide approach.

Index findings

-

Average REC scores on Regional integration stand at 0.470 on a scale of 0 (low) to 1 (high). Average Regional integration scores for the eight RECs stand at below half of the scale from 0-1, showing that overall integration in the regions could significantly progress.

-

EAC is the top performing REC on Regional integration overall. EAC has higher than average scores across each Dimension of Regional integration, except for Financial and macroeconomic integration.

-

SADC and ECOWAS have higher than average REC scores on Regional integration overall. SADC has higher than average REC scores across the Dimensions of Regional infrastructure, Free movement of people and Financial and macroeconomic integration. ECOWAS has higher than average REC scores across the Dimensions of Free movement of people and Financial and macroeconomic integration.

Index: five Dimensions in Regional Economic Communities