Search News Results

Central African Economic and Monetary Community (CEMAC): Financial System Stability Assessment

This report is based on the work of a joint IMF/World Bank team that visited Brazzaville and Pointe Noire (Republic of Congo), Douala and Yaoundé (Cameroon), and Libreville (Gabon) in November 2014 and January 2015, to update the Financial Sector Assessment Program (FSAP) for the CEMAC conducted in 2006.

The short-term risk of a financial crisis appears low, but the assessment identified pockets of vulnerabilities. The financial sector is not well positioned to contribute effectively to the financing of the CEMAC economies, and it faces an intensification of risk factors related to geopolitical tensions and the fall in commodity prices.

Reform progress has been slow in addressing longstanding weaknesses, despite extensive technical assistance (TA), and the urgency for progress is heightened by recent macroeconomic developments. Firm action is required to foster the development of the financial sector while ensuring adequate oversight of risk factors. The reform agenda calls for granting greater operational autonomy to the regional financial agencies, and boosting their capacity to carry out the reform projects successfully.

Prudential regulations need to be upgraded, and regulatory forbearance should be avoided through effective enforcement. There is also considerable scope for enhancing the business climate, one of the weakest worldwide, and financial inclusion, which has been lagging behind.

CONTEXT

Macroeconomic Risks in the Financial Sector

Over the past decade, primarily as a result of high oil prices, the CEMAC achieved robust economic growth, although lower than the SSA average, but insufficient to significantly reduce poverty. Countries launched wide-ranging public infrastructure programs needed to support regional economic activity, but large fiscal expansion reduced the fiscal buffers for coping with the negative oil price shocks. The economies are poorly diversified, and non-oil GDP growth is largely sustained by public expenditure and the services sector. Poverty and unemployment remain high, in particular among young people.

A poor business climate and weak governance are hampering financial sector development and its contribution to financing investments. Corrective actions in this regard are needed to improve the growth potential and competitiveness of the CEMAC economies.

The weakness of regional integration also limits the growth potential. Although the CEMAC has a common legal system (OHADA), a common external tariff, and a common currency, numerous tariff and non-tariff barriers hinder the flow of goods, services and persons. Intra-regional trade accounts for only 2 percent of all trade. Intra-regional financial transactions are also limited, compared with the volume of international transactions. By contrast, a certain increase is noted in intra-regional payments, along with an expansion in government securities issued at the regional level.

The drop in oil prices by about 60 percent between June 2014 and January 2015 has had a large impact on the CEMAC countries’ macroeconomic performance (Box 1). Oil revenue represents over 50 percent of the Union’s fiscal outlays and more than 80 percent of exports. The sharp decline in oil revenue is expected to force some countries to reduce budgetary spending, including public investment programs. Pressures on their treasuries could also lead states to use a portion of their deposits at the BEAC and in the banking sector, which could in turn weaken the liquidity position of some financial institutions. Such pressures could also lead to problems in paying suppliers and thus to an increase in the nonperforming loans (NPLs) of financial institutions.

Box 1. BEAC Assessment of the Oil Shock Impact

According to the baseline scenario prepared by the BEAC, the oil shock impact would be as follows:

Real sector: The CEMAC is expected to record a 1.8 percent growth decline in 2015 owing to falling oil sector activity and the consequent retrenchment in capital expenditures. For 2016-17, growth is projected to recover to average about 7 percent. Inflation is expected to remain subdued at around 2.3 percent for the period 2015-17.

External sector: Over the period 2015-17, the current account deficit would deteriorate to 14.1 percent of GDP on average, and the international reserves coverage is projected to fall to an average of 3½ months of imports of goods and services.

Public sector and debt: The fiscal balance would decline to - 6.7 percent of GDP in 2015, -4.9 percent in 2016, and - 3.4 percent in 2017; financing needs should lead to a significant increase in debt.

Monetary aggregates and banking sector: The external coverage ratio would fall to 87.4 percent for the period 2015-17. However, it would plummet to 52 percent if the states’ financing requirements were only met on the domestic market. The banks’ liquidity levels should remain at comfortable levels.

Source: BEAC.

The worsening of the security situation related to the crisis in Central African Republic (CAR) and Boko Haram’s activities in the northern part of Cameroon could also affect economic activity. The expectation of higher risks could affect investment in new projects and commercial activity, with ensuing adverse effects on financial sector stability and profitability.

Structure and Performance of the Financial Sector

The CEMAC’s financial sector is dominated by commercial banks, and in some countries large microfinance institutions (MFIs); foreign banks manage about 50 percent of the total assets. The banking sector is heterogeneous, segmented, and strongly concentrated: on average, the three main banks in each country hold more than 70 percent of the assets despite the arrival of new foreign players.

Financial depth has improved somewhat since 2006. At end-2013, banking assets in the CEMAC represented 26.3 percent of the CEMAC’s GDP, compared with 15.7 percent in 2004. The ratio of private credit to GDP, at 10 percent, increased less quickly. For the most part, loans are granted for short and medium terms, and demand deposits represent the bulk of banks’ resources. The ratio of credit to deposits also increased, going from 57 percent in 2010 to 67 percent in 2013. The Cameroonian and Gabonese markets shares have declined, with Congo and Equatorial Guinea becoming larger.

Access to formal banking services is however lower than in comparable SSA countries. Credit to the private sector, as percentage of GDP has increased since the last FSAP but still remains low in a regional comparison. Financial inclusion is limited and less than 15 percent of adults are bank account holders, which is lower that the SSA average. The level of income affects access to financial services. Bank lending is preferably to customers whose wages are deposited in an account with them and large enterprises receive most of bank loans (80 percent). Surveys of potential bank users find as constraints relatively high minimum deposit requirements compared with income, the high costs of the services, and the distance from the nearest bank branch (Findex database, 2012). In addition, access to savings and to traditional bank financing are comparatively more difficult for the poor and for women in the CEMAC. The mix of all these constraints results in an extremely limited access to financial services in the CEMAC.

The bank business model shows little diversity and a limited match with developmental needs. Loans to connected parties, reflecting the ownership structure of local banks, have been the main contributor to past bank crises and remain a source of risks for locally owned banks. The banks’ overall ample liquidity and the absence of regular publication of the banks’ financial statements contribute to the limited development of the money market. Electronic banking services are beginning to be offered but are still embryonic, and the cost of electronic funds transfers is much higher than that in comparators, for example, in East Africa. The microfinance sector is relatively well developed in three countries (Cameroon, Congo, and Chad) and offers financial services to households and SMEs not using the banking system.

Financial intermediation and access to credit remain hampered by a number of structural constraints. The barriers include, in particular, inadequate functioning of the judiciary, the absence of appropriate guarantee instruments, and the lack of credit reporting. To reduce these barriers, the BEAC envisages developing a payment problem information center at the regional level, but the authorities should implement more wide-ranging reforms.

Overall, the banking sector is profitable, with wide differences across countries, and differentiation depending on the size of the institutions (the smaller banks being less profitable). After plunging in 2009, the banking sector’s profitability recovered gradually up to levels close to those noted in 2004-05. In 2013, the return on equity (ROE) averaged 19.3 percent, compared with 16.9 percent in 2005. The profitability of Cameroonian banks, on the decline between 2010 and 2012, settled in 2013. Congolese and Gabonese banks show relatively comfortable and stable profitability. A downward trend is observed for the banks in Equatorial Guinea and Chad. The political crisis in CAR led to a collapse of bank profitability. The large banks show relatively strong profitability as opposed to the small banks whose return on equity (ROE) was highly negative in 2013. Of the eleven state-owned banks, five recorded losses in 2013.

Interest and fees account for nearly the same share of revenues, which illustrates the low level of banking diversification. Cameroon is an exception: fees are relatively large, whereas the interest margin is near double the revenue from fees in CAR. The low level of operating expenses for the banks in Equatorial Guinea is also noteworthy. The evolution in the average cost of credit has been negligible: interest rate margins stood at 7.1 percent in 2013 (lower than in 2011).

Other trends in the banking landscape since the 2006 FSAP have been as follows: (i) a sharp increase in the number of state-owned banks, from 2 to 11, with others planned in several countries. In 2014, state-owned banks accounted for nearly 11 percent of banking sector assets, compared with 3.6 percent in 2005; (ii) the sector concentration: the three main banks manage 50-90 percent of bank assets, depending on the country, and two groups originating in the CEMAC own one-third of the banking assets; and (iii) the arrival or development of new players headquartered in SSA countries and the Maghreb (respectively, 13 and 9 percent of sector’s assets).

Follow-up of the 2006 FSAP

The initial 2006 CEMAC FSAP identified institutional and capacity constraints undermining the effectiveness of the regional financial agencies, including material deficiencies in the legal and judicial framework; poor quality of financial data; weak financial market infrastructure; limited institutional autonomy of the COBAC compounded by inadequate staffing; poor conformity with international standards; and weak systemic liquidity frameworks at the BEAC.

The 2006 FSAP was also followed by wide-ranging IMF and World Bank technical assistance (TA) programs in support of the actions initiated by the authorities. The technical assistance related to increasing staff bank supervisory capacity at the SG-COBAC, improving the accounting and internal control systems at the BEAC, building the BEAC’s capacity to manage systemic liquidity and the foreign exchange reserves, and assisting the member countries in public debt management. The Central African Regional Technical Assistance Center (AFRITAC) contributed to these actions in the areas of banking supervision and public debt management. The African Development Bank provided support in the area of securities markets.

Progress in addressing the findings of the 2006 FSAP was held back due to several factors, including: delays in the recruitment or appointment of professional staff at the BEAC and SG-COBAC; lengthy processes for adopting CEMAC regulations; and difficulties in building a consensus for reforms. Delays in the reform agenda at the regional level have led some member states to move forward even though a regional approach would have been preferable.

Stress Test Results

The stress tests show a high vulnerability to credit risks specific to the CEMAC (fiscal imbalances in response to the oil shock and a degradation of security), especially for the banks with main activity within the CEMAC. However, the team’s analysis, and supervision more generally, are limited by weaknesses in the quality and reliability of financial data: supervisory returns are poorly verified; capital positions may be overstated given the weak regulatory framework on lending to connected parties and the definition of regulatory capital; and the weights applied to some transactions do not always reflect the risks associated to the underlying assets.

Most notably, the stress tests show the predominance of credit risk. In the event of an extreme macroeconomic scenario leading to 15 percent of the performing loans becoming non-performing, only 58 percent of all the banks would comply with the solvency ratio (currently, 80 percent of the banks comply with the minimum level of 8 percent). Yet, immediate capital shortfalls would be contained (less than 0.50 percent of regional GDP). The vulnerability to credit risk is amplified in the event of weak sectoral credit diversification, which is generally the case for banks whose business is concentrated in the CEMAC: only 18 percent of those banks would be in compliance with the solvency ratio after the shock, compared with 65 percent and 76 percent respectively in the case of banks operating in SSA and those operating internationally.

The results of the other unitary shocks are as follows:

-

The banks are highly vulnerable in case of deposit withdrawals, due their heavy reliance on volatile sight deposits (representing close to 80 percent of their liabilities) for their funding. Following a 25 percent decline in deposits, the weighted average of the regulatory liquidity ratio would fall to 66 percent, against 138 percent before the shock. Banks in Cameroon, Gabon, and Chad are the most vulnerable, their respective ratios being 49 percent, 50 percent, and 65 percent. However, it is worth noting that the banks have large current account amounts available at the central bank which could be used to mitigate the liquidity risk.

-

Exposures to direct foreign exchange and interest rate risks are limited. The immediate impact on the bank’ balance sheets of devaluation of the CFA franc against the euro, or of a depreciation or appreciation of the CFA franc against the U.S. dollar, would be small. While lack of data prevents the assessment of a secondary effect (impact on borrower creditworthiness), the low level of borrower indebtedness denominated in foreign currency suggests limited direct vulnerability. The banks’ direct exposure to interest rate risk is also very limited: the valuation of assets and liabilities is not very sensitive to interest rate changes because of the scarcity of tradable securities in the bank’s balance sheets.

-

The largest MFIs, like the banks, are mostly exposed to credit risk. They would no longer comply with the solvency ratio following a 15 percent transition of performing loans to NPLs. However, a drop of up to 30 percent in their deposit base would not threaten their ability to comply with the liquidity ratio.

-

A recalibration of risk weights, so that they reflect better the risks associated to the underlying assets, would affect negatively the solvency of the banks.

-

BCP assessment, weighting of loans and the nature of the deductions applicable to certain categories of loans divert from prudent practices. In order to evaluate the impact of regulations aligned with Basel rules, the mission recalibrated banks’ prudential ratios. Only 69 percent of the banks would comply with the solvency ratio once risk weights are recalibrated so as to ensure a better alignment of CEMAC rules with Basel.

The results of the stress tests exercise and of the analysis of the financial statements of credit institutions point to a few measures to be considered to better align the supervisory framework of the COBAC with the specificities of the CEMAC: (i) given the banks’ widely varying risk profiles, it would be advisable to implement the Basel pillar II approach, as this would allow the COBAC to adjust capital requirements on the basis of the bank’s risk profile; (ii) given the growing role of banking groups in the CEMAC, it is important to operationalize quickly the framework for consolidated and cross-border supervision; (iii) the reduced weights applied to some assets for the calculation of the solvency ratio should be revised so that they reflect more accurately their risk profile; and (iv) large MFIs should be subject to an enhanced supervisory framework, closer to the one in place for the banks.

FINANCIAL STABILITY POLICY FRAMEWORK

Actions of the Central Bank

The pressure on countries’ public finances and on the CEMAC’s external position as a result of the current macroeconomic conjuncture call for strengthening the BEAC’s ability to manage systemic liquidity proactively. At this time, the monetary programming framework in place at the BEAC is not as flexible as it should be. Moreover, the imperfect pooling of cash balances by some states at the BEAC (in particular of the financial flows related to the oil sector) complicates systemic liquidity management by the BEAC.

These challenges emphasize the urgent need to bring to completion the reform of the monetary policy framework. The following key actions are recommended:

-

Strengthen the internal functioning of the BEAC. The strengthening of the BEAC’s internal controls and its accounting system, when completed to the satisfaction of the oversight bodies, will make it possible to return the chairmanship of the BEAC board of directors to the governor, together with the adoption of a governance structure for the BEAC which combines the three pillars of modern central banking, namely independence, transparency, and accountability. It is also critical to revisit the rules and practices for the selection and appointment of the BEAC’s top officials (national and head office directors and other senior staff), in order to ensure that appointments by the BEAC authorities are based on candidates’ professional qualifications and experience, while at the same time maintaining a balanced national representation.

-

Strengthen the systemic liquidity forecasting and management framework. The work already started at the BEAC should be completed as a matter of priority. This will involve a close coordination with the national authorities in charge of government cash flow management.

-

Initiate the reform of the monetary policy operating framework. The multiplicity of monetary policy instruments blurs the readability and transparency of the BEAC’s actions. It is therefore urgent to streamline the framework, along the lines of past recommendations made in the context of Fund technical assistance. This effort should also include actions to develop the government securities market; a regional committee under the aegis of the BEAC should be established to this effect.

-

Put in place a lender of last resort framework distinct from the monetary policy operating framework.

The current pressures on the external position of the CEMAC also reinforce the need to strengthen the BEAC’s reserve management framework, and to have its key components validated by the Ministerial Committee, including: (i) the methodology for assessing the optimal level of international reserves; (ii) the structure of the reserves portfolio; and (iii) the methodology for determining the remuneration of the deposits by CEMAC member states. Current arrangements could be amended towards an assets-liabilities approach, whereby the remuneration of the deposits would reflect the return on the assets in which they are invested. The implementation of the above principles governing the framework for foreign exchange reserves management should remain under the responsibility of the Monetary Policy Committee-MPC (e.g., actual calculation of the optimal level of reserves, of the structure of the reserves, and of the remuneration of deposits, and setting the strategic allocation of reserves).

Financial Stability Framework

The recently established financial stability framework needs to be made fully operational. While overtime a fully developed institutional framework for macroprudential policies will be useful, at this juncture the priority should be given to strengthening the microprudential supervision framework; clarifying the BEAC’s role (including establishing a lender of last resort function); adopting a mechanism for identifying banks and MFIs of systemic importance; strengthening of the framework for monitoring financial stability through the conduct of stress tests in coordination with the SG-COBAC; and undertaking analysis of the channels of contagion between the macroeconomic and financial sectors.

CRISIS MANAGEMENT AND SAFETY NETS

Crisis Management and Resolution

The recently adopted regulation for crisis management and resolution is a significant progress, but needs supporting measures. After a lengthy process, drawing on the lessons of recent banking crises (Box 2), a new regulation was adopted in 2014 by the MC. Two main points deserve the authorities’ attention:

-

The special restructuring provisions create for the resolution authorities, under CEMAC, COBAC, UMAC, and MC Regulations, far-reaching powers that have not yet been tested, and that could be challenged in court.

-

The actual implementation of the new arrangements requires supporting measures to: (i) specify the criteria for initiating special restructuring operations, and especially regarding the assessment of whether or not a bank is of systemic importance; (ii) specify the provisions aimed at safeguarding the interests of parties that believe they have incurred losses greater than those they would have suffered in the context of liquidation under ordinary law; (iii) protect the interests of the funding entities (the deposit insurance fund - FOGADAC and the states) by recognizing their preferential rights over those of other creditors; and (iv) clearly establish the obligation for the FOGADAC and the COBAC to take legal action against shareholders and executives responsible for bank failures caused by anomalous or fraudulent management actions.

Box 2. Lessons of the Recent Banking Crises

The treatment of the most recent banking failures offers a broad catalogue of the risks likely to arise in dealing with problem banks.

National authorities did not always intervene in a well coordinated manner with the COBAC.

The rescue of insolvent banks with public funds was not timely and not always based on the proven systemic importance of the banks.

The maintenance of shareholders in the capital of banks being restructured with public funds enabled them to limit their contribution to the losses, whereas the banks’ failure largely resulted from loans granted to entities in their group.

The lack of legal backing in the measures taken opened the door to judicial appeals by the shareholders, leading to the excessive lengthening of the resolution process

The legal framework should also be supplemented by mechanisms for consultation and coordination among all the authorities potentially concerned by the failure of complex financial groups with cross-border business. These additions should entrust to the COBAC a prominent, if not exclusive, role over the other authorities in the region, so as to ensure: (i) the indispensable speed in decision making; and (ii) the consistency of the options implemented by the national authorities concerned by the failure of a group operating in several jurisdictions of the region. The improvement of the current regulations should be accompanied by the formulation of clear procedures assigning to each pertinent authority, including the FOGADAC, a specific role in the selection of available options, and in the decision-making and implementation processes.

The ordinary resolution arrangements applicable to institutions that are not of systemic importance should also be reviewed. The powers assigned as regards disciplinary and restructuring matters are not established clearly enough to be legally unquestionable. The criteria for the use of those powers should be specified to ensure that interventions are gradual and match the seriousness of the given situation.

The following key measures are recommended:

-

The mandate given to the COBAC as the resolution authority should be explicitly established.

-

Financial groups operating in the CEMAC should be structured around a holding company subject to consolidated supervision and the resolution framework.

-

The objectives and priorities governing special restructuring should be more explicitly established.

-

The COBAC should require at least the systemic banks to elaborate Recovery and Resolution Plans.

-

The COBAC should immediately undertake the analysis of the legal resolution frameworks governing the foreign groups carrying out a systemic activity within the CEMAC.

DEVELOPING THE FINANCIAL SECTOR

Financing of the Economies

Financial inclusion represents a major challenge in the CEMAC. The World Bank’s 2011 Findex survey showed that only 12 percent of adults had a bank account, one half of the average noted in SSA, with great disparity within the region. The BEAC and the COBAC should put into place a management chart that can be used to measure and monitor financial inclusion in all its dimensions. It would also be helpful to undertake surveys through interviews and polls that can give a better idea of the financial capacity of households and the barriers (on the demand side) to progress as regards financial inclusion.

Customer relations and the services offered to individuals have slightly evolved. Individuals in the formal sector are a major source of deposits, but the share of credit going to them is steady (15 percent). These financing operations take the form of overdrafts and consumer loans (consistently backed by wages) whose maturity is often 3-4 years. The use of payment cards is limited; remote banking is only now being developed. The rapid growth of financial services targeting households has revealed shortcomings in the consumer protection framework that deserve further attention.

Microfinance plays a significant role in the CEMAC. Most MFIs are authorized to take deposits. The microfinance sector though remains weak, especially with an extremely high average rate of outstanding payments, at 22 percent. Excessive exposure to connected parties, barely or poorly identified, is a common issue, and the ongoing liquidation of some MFIs, triggered by severe governance problems and affecting thousands of low-income savers, has highlighted the need to strengthen the supervision and crisis management arrangements for MFIs.

Credit to SMEs is negligible and growing only slowly. While little reliable information is available, SMEs financing by the banks seems to be stagnant. The MFIs, which serve a somewhat different population of SMEs, are increasing their financing operations; rates are in the range of 9-18 percent for banks and 15-25 percent for MFIs. Leasing is a key source for the financing of capital goods in those countries where a specific legal and institutional framework has been established (Cameroon and Gabon).

The low level of term financing from domestic banks reflects concerns about risks and the size of bank balance sheets (for large projects), and the lack of long-term resources. Moderate progress has occurred since 2006 in medium- and long-term domestic bank financing. The above-mentioned problems related to the business climate as well as the sociopolitical uncertainties in some countries led the banks to focus on high-grade borrowers for whom the risks are better managed. The structure of their resources is also a constraint, as these are composed largely of demand deposits. In the absence of a reference interest rate index, fixed-rate loans expose lenders to interest-rate risk. Development institutions have been created (or are planned) to remedy these weaknesses; they should strictly adhere to the best international practices which requires considerable effort.

Housing credit is still only marginally developed in the CEMAC and remains far short of the needs. Along with exogenous constraints (limited use of the banking system, lack of affordable housing, large portion of the labor force in the informal economy), major barriers are created by the poor credit climate itself. The lack of long-term resources also explains the great prudence of the commercial banks and contributes to the rise in the cost of credit. Microfinance does not offer solutions that match the needs, despite sporadic progress. The temptation persists to replace the market by government interventions instead of tackling the causes of its inefficiency. Progress was achieved recently in land management from the legal and operating perspectives.

Improving the business climate and financial environment to facilitate access to households and SMEs to finance is essential and some reforms can be implemented quickly. The processes of registration, transfer, and notarization of property deeds should be streamlined and the associated costs and delays reduced in order to facilitate the use of real estate as collateral. Strengthening creditor rights (in particular when they have assets) and the establishment and modernization of unified collateral registries would allow SMEs to use a broader range of securities to access credit. This would also allow banks to reduce the required levels of collateral and prevent “opportunistic” defaults. The modernization of the credit information systems is also essential and can bear results quickly. The BEAC and the COBAC should monitor financial inclusion and the pricing of financial services. Regulatory measures have been taken to reduce the cost of financial services that could be complemented by a review of the value-added tax regime. Strengthening transparency, redress mechanisms, and financial education will improve consumer protection. The rules on governance and internal control of banks and MFIs regarding connected parties transactions need to be strengthened and enforced to reduce the risks of financial crises. Finally, public interventions should not be designed to replace financial institutions, but to encourage interventions by them.

Financial Infrastructures

The capital market remains embryonic and fragmented. The market includes the regional stock exchange (BVMAC), supervised by a regional body (COSUMAF), as well as a parallel mechanism in Cameroon, with a stock exchange (Douala Stock Exchange, DSX) and a supervisor (CMF). The coexistence of two separate mechanisms, regional and Cameroonian, was already highlighted in 2006. In practice, the survival of the two mechanisms depends on financial support from the public sector. The long-ongoing actions to unify the mechanisms should be completed quickly, first starting with the establishment of a unique central securities depository (CSD).

Since the 2006 FSAP, the BEAC has made good progress with the establishment of a Real Time Gross Settlement (RTGS) system, and an automated clearinghouse. Delays in establishing an efficient retail payments market (which has a negative effect on economic development and financial inclusion), will be absorbed only with a proactive approach by the BEAC. Electronic money’s potential for development is extremely significant, and the BEAC should improve the monitoring of its development in the CEMAC. The BEAC should also strengthen its oversight function, so as to be able to supervise the systems of systemic importance as well as to fulfill its mission of supervision, monitoring, and strategic encouragement of retail payments.

More reliable, detailed credit reporting is a key factor for facilitating proper risk control by financial institutions and therefore for financial inclusion. It is important to improve coordination of the multiplicity of uncoordinated regional and national initiatives, a source of redundancies that weakens the chances of success of those initiatives. The establishment of an efficient, coherent regional credit reporting system will require consensus and the participation of a wide range of public and private players, as well as a commitment from the public authorities, and in particular from the BEAC.

Anti-Money Laundering and Combating the Financing of Terrorism

The CEMAC faces significant money laundering and terrorism financing risks. In the implementation of effective AML/CFT policies, the authorities face structural and sectoral challenges that are conducive to money laundering operations: a predominance of informality and the use of cash in the economy, a small portion of the population using the banking system, unreliability of identification documents and lack of register computerization, highly porous borders, and money laundering in the real estate, banking, funds transfers, manual foreign exchange operations, and microfinance.

The Central African Anti-Money Laundering Task Force (GABAC), despite serious efforts, has not yet been recognized as a Financial Action Task Force (FATF)-style regional body (FSRB). The GABAC has made efforts to launch a program of mutual assessments, organize regular task force meetings, and prepare typology exercises on AML plans in Central Africa. The GABAC began a process of close cooperation with the FATF, with a view to obtaining FSRB status; that process is currently frozen because of delays in the GABAC’s adoption of procedures for transparent financial management.

The following actions should be undertaken as a matter of priority:

-

Complete, as soon as possible, the process of recognizing the GABAC as a FSRB, providing it with procedures for transparent financial management;

-

Put the FIUs in Congo and Equatorial Guinea into operation;

-

Set up, within each state, an effective inter-ministerial committee responsible for drafting a national AML/CFT policy defining priorities for action by each player, short and medium-term quantitative objectives, and means of action;

-

Draft, in each member state, a comprehensive and structured criminal justice policy for AML/CFT and the principal offenses, including corruption and the embezzlement of public funds, that would include the combating of money laundering in criminal proceedings.

-

Make funds transfer companies subject to a mechanism for licensing/registration and for supervision; and

-

Increase the appropriate financial, technical, and human resources of regional and national supervisors of the financial and non-financial sectors, for gradual and effective implementation of AML/CFT risk-based supervision and ensure supervisors have and use a broad range of powers to enforce AML/CFT requirements.

Related News

Ease investment terms to lure foreign firms, Kenya tells African nations

Kenya on Tuesday urged African governments to set up independent investment portals to enhance interaction with foreigners seeking to launch operations within their countries.

Kenya Investment Authority Managing Director, Dr Moses Ikiara, said its e-regulations platform received 20,600 enquiries from potential investors drawn from 100 countries.

Dr Ikiara told an international conference on Ease of Doing Business Initiative at Safari Park Hotel in Nairobi yesterday that going digital would further deepen interaction with investors leading to meaningful dialogue as compared to a one-stop-shop for all State services.

“Huduma Centre is a great initiative for Kenyans but the outside world as well as local investors need a specific portal to engage knowledgeable advisors on matters investment,” said Dr Ikiara.

Industrialisation Cabinet Secretary Adan Mohamed said Kenya moved fast to ease conditions of doing business as a prerequisite to attracting investments, accelerating economic growth, creating job opportunities and wealth.

“African governments must be ready to work together, with key partners such as the World Bank and International Finance Group, alongside local and international private sector organisations to consolidate gains made on the business reforms made in 2015,” he said.

Mr Mohamed said while economic outlook showed Africa would grow at 5.1 per cent, there is need to translate the impressive growth indicators into tangible gains that impact positively on the living standards for all citizens.

Kenya hosts ease of doing business conference

The Government of Kenya is hosting the 7th Ease of Doing Business Initiative (EDBI) Conference from May 3rd 2016 to May 6th 2016 at the Safari Park Hotel Nairobi, Kenya.

The EDBI Conference is a peer-to-peer learning event requested by African countries and supported by the World Bank Group, to facilitate knowledge sharing on Doing Business reforms. It aims at showcasing and facilitating replication of best practice, best fit in reforming, ideas, opinions and expertise on the legal and institutional framework underpinning successful business environment reforms in order to help pave the way for bigger and better business and increased investment flows in Sub Saharan Africa. More specifically, this knowledge transfer gathering offers an excellent opportunity for the participating African countries to learn from each other’s experience in implementing reforms thereby facilitating job creation by the private sector.

The theme for this year’s conference is ‘Digitizing Business – Leveraging ICT to enhance the Business Environment’. The 3-day conference will bring together over 300 delegates drawn from government, industry and business leaders as well as international investors, economists and academics from Africa.

The objectives of the EDBI 2016 are to:

-

Facilitate sharing of knowledge and experience on investment climate reforms in Africa; and

-

Improve the investment climate and increase the region’s share of investment flows and export markets, in line with the stated regional economic integration objectives of the involved Regional Economic Communities and Member States.

-

Facilitate the showcasing of best practice under one roof, encourage political buy-in and follow-through of committed reform agenda covering various sectors.

Background

The Doing Business Report is an annual report that was first published and launched in 2002 by the World Bank Group to analyze regulations that apply to an economy’s businesses during their life cycle, including start-up and operations, trading across borders, paying taxes, and resolving insolvency. The aggregate ease of doing business rankings are based on the distance to frontier scores for 10 topics and cover 189 economies.

The Doing Business findings have stimulated policy debates worldwide and enabled a growing body of research on how firm-level regulation relates to economic outcomes across economies. The key goal of Doing Business is to provide an objective basis for understanding and improving the local regulatory environment for business around the world.

By gathering and analyzing comprehensive quantitative data to compare business regulation environments across economies and over time, Doing Business encourages economies to compete towards more efficient regulation and offers measurable benchmarks for reform.

EDBI Conference

The “Ease of Doing Business Initiative” (EDBI), is grounded in the interest and need expressed by several Africa countries to learn and share information and experiences about the reforms implemented in the scope of Doing Business.

It was therefore imperative to host an Annual Conference in order to concretize these objectives, in which knowledge and experiences from various countries are presented, promoting regional collaboration in reforms based on “peer-to-peer learning”.

In August 2010, the World Bank Group, in collaboration with the Regional Multidisciplinary Centre of Excellence (RMCE) and some Governments, designed the EDBI, which has been gradually refined over the years. Mauritius, the top-ranked DB country in the Africa region for three years running, offered to host the event and to share its experience.

Following the successful pilot of this peer-to-peer learning model held in Mauritius in 2010, Rwanda, the country which improved the most in the ease of doing business in 2009/2010, hosted a second peer-to-peer workshop for Governments in Eastern and Southern Africa in March 2011. The third meeting was held in March 2012 in Gaborone, Botswana, the 2013 meeting was in Sandton, South Africa, the 2014 meeting took place in Maputo, Mozambique and the last meeting was held in Kampala, Uganda in 2015.

Related News

DG Azevêdo calls for action to provide trade finance for small businesses

Director-General Roberto Azevêdo has issued a call for action to help close the gaps in the availability of trade finance that affect the trade prospects of small and medium-sized enterprises (SMEs), particularly in Africa and Asia.

In a new WTO publication, “Trade Finance and SMEs: bridging the gaps in provision”, which examines the problem and looks into possible solutions, DG Azevêdo says that easing the supply of credit could have a big impact in helping small businesses grow and in supporting the development of the poorest countries.

The availability of trade finance is essential for a healthy trading system as up to 80 per cent of trade is financed by credit or credit insurance. But trade finance is not always available. A lack of trade finance is a significant barrier to trade. SMEs have particular challenges in accessing affordable financing. Globally, over half of trade finance requests by SMEs are rejected, against just 7 per cent for multinational companies.

SMEs in developing countries face the greatest challenges in accessing trade finance and there are some very large gaps in provision. The estimated value of unmet demand for trade finance in Africa is US$ 120 billion (one-third of the continent’s trade finance market) and US$ 700 billion in developing Asia. Bridging these gaps would unlock the trading potential of many thousands of individuals and small businesses around the world.

“Without adequate trade finance, opportunities for growth and development are missed and companies are deprived of the fuel they need to trade and expand,” said DG Azevêdo. “By working together with our partners, I believe we can further close the gaps in provision and ensure that trade finance is no longer a barrier to trade, but a springboard to growth and development.”

Various steps are already being taken to tackle this issue on a number of fronts: encouraging global financial institutions to remain engaged; encouraging regulators to emphasise the trade and development dimension; increasing the capacity of local financial institutions; and providing support measures to increase the availability of trade finance via multilateral development banks.

The report highlights a number of further steps which could be taken, including:

-

enhancing existing trade finance facilitation programmes to reduce the financing gap by US$ 50 billion

-

reducing the knowledge gap in local banking sectors for handling trade finance instruments by training at least 5,000 professionals over the next five years

-

maintaining an open dialogue with trade finance regulators to ensure that trade and development considerations are fully reflected in the implementation of regulations

-

improving monitoring of trade finance provision to identify and respond to gaps, particularly relating to any future crises.

Related News

Expert group meets in Kenya to discuss continental free trade issues

An expert group comprising representatives of Africa’s regional economic communities, the African Union Commission, the Economic Commission for Africa (ECA) and academia is meeting in Nairobi, Kenya, to discuss issues connected to the Continental Free Trade Area (CFTA). The meeting runs from 2-6 May.

The CFTA, which is expected to be in place by October 2017, will bring together fifty-four African countries with a combined population of more than one billion people and a combined gross domestic product of more than US $2.5 trillion.

With the CFTA, African leaders aim to, among other things, create a single continental market for goods and services, free movement of business persons and investments and expand intra-African trade. The CFTA is also expected to enhance competitiveness at the industry and enterprise levels

The meeting this week will focus on nine issues that can be feasibly achieved or agreed upon ahead of the October 2017 deadline. These are; trade in goods, trade in services, agriculture, fisheries provisions, industrial pillar, common investment area, trade facilitation and customs cooperation, trade remedies and competition policy and institutional arrangements for implementation.

The expert group meeting is jointly organized by the Department of Trade and Industry of the African Union Commission and the ECA’s African Trade Policy Centre.

Related News

Investment flows through offshore financial hubs declined but remain high

Investment flows to offshore financial hubs, including offshore financial centers and special purpose entities (SPEs), were increasingly volatile in 2015, according to the latest UNCTAD Global Investment Trends Monitor.

The research shows that these flows, which are excluded from UNCTAD’s foreign direct investment (FDI) statistics, declined but remain sizable. The magnitude of quarterly flows through SPEs, in terms of absolute value, rose sharply compared with 2014, reaching the levels last registered in 2012-2013.

Meanwhile, investment flows to offshore financial centers continued to retreat from their recent high of $132 billion in 2013, but remained roughly in line with the flows of previous years.

Offshore financial hubs offer low tax rates or beneficial fiscal treatment of cross-border financial transactions, extensive bilateral investment and double taxation treaty networks, and access to international financial markets, which make them attractive to companies large and small. Flows through these hubs are frequently associated with intra-firm financial operations − including the raising of capital in international markets − as well as holding activities, including of intangible assets such as brands and patents.

An in-depth analysis of FDI trends will feature in the forthcoming World Investment Report 2016, to be published in June 2016.

Highlights

-

In 2015, the volatility of investment flows to offshore financial hubs – including those to offshore financial centers and special purpose entities (SPEs) – rose significantly. These flows, which are excluded from UNCTAD’s FDI statistics, declined but remain sizable.

-

Financial flows through SPEs surged in volume during 2015. The magnitude of quarterly flows through SPEs, in terms of absolute value, rose sharply compared with 2014, reaching the levels registered in 2012-2013. Pronounced volatility, with flows swinging from large-scale net investment in the first three quarters to drastic net divestment in the last quarter, tempered the annual result, which dipped to US$221 billion.

-

Investment flows to offshore financial centres continued to retreat from its recent high of US$132 billion in 2013, but remained roughly in line with the flows of previous years. Investment to these jurisdictions, which hit an estimated US$72 billion in 2015, had risen in recent years by the growing flows from multinational enterprises (MNEs) located in developing and transition economies, sometimes in the form of investment round-tripping.

-

The proportion of investment income booked in low tax, often offshore, jurisdictions is high – and possibly growing. The disconnect between the locations of income generation and productive investment results in substantial fiscal losses, and is therefore a key concern for policy makers.

-

The persistence of financial flows routed through offshore financial mechanisms highlights the pressing need to create greater coherence among tax and investment policies at the global level. The international investment and tax policy regimes are both the object of separate reform process. Better managing their interaction would not only help to avoid conflict between the regimes but would also make them mutually supporting, with positive implications for productive cross-border investment.

Related News

tralac’s Daily News Selection

The selection: Tuesday, 3 May 2016

Featured African trade policy processes, presently underway:

In Nairobi: Ease of Doing Business Initiative 2016 conference on the theme 'Digitizing Business – leveraging ICT to enhance the business environment'

In Nairobi: ‘@UNCTAD joins @ECA_OFFICIAL/AUC/RECs and experts for 5 days of drafting #CFTA draft texts'

In Kampala: National Trade Facilitation Committee workshop on the effective implementation of the TFA within the EAC

Sub-Saharan Africa: 'Time for a policy reset' (IMF)

After a prolonged period of strong economic growth, sub-Saharan Africa is set to experience a second difficult year as the region is hit by multiple shocks, the IMF said in its latest Regional Economic Outlook for Sub-Saharan Africa. The steep decline in commodity prices and tighter financing conditions have put many large economies under severe strain, and the new report calls for a stronger policy response to counter the effect of these shocks and secure the region’s growth potential. The report shows growth fell to 3½ percent in 2015, the lowest level in 15 years. Growth this year is expected to slow further to 3 percent, well below the 6% average over the last decade, and barely above population growth. [Asia Pacific Regional Economic Outlook] [World Bank raises 2016 oil price forecast, revises down agriculture price projections]

African Regional Standards Organization: report on activities for the implementation of WTO's TBT agreement (WTO)

Understandably, one of the main challenges facing the African countries is the variation in Regulatory framework, standards, certification, testing, and inspection practices used by different countries. This makes trade between the countries difficult, contentious, and expensive. This explains the low level of intra African Trade 12% and participation in the global trade (3%). For this, ARSO, an intergovernmental body, established in 1977 with the mandate to harmonise African Standards and conformity assessment procedures in order to reduce these Technical Barriers to Trade, promote intra-African and international Trade. Currently ARSO has 36 member States. Current programmes and activities are implemented under the current strategic plan 2012-2017 and may I bring to the attention of the Committee the following ARSO programmes which aims at facilitating the implementation of the WTO TBT Agreement.

Trade and the SDGs: making ‘means of implementation’ a reality (Commonwealth)

A major factor that inhibits more effective use of the global trading system by firms in LDCs is high trade costs. Extensive evidence suggests that trade costs are much higher than prevailing tariff rates of protection. Even if account is taken of non-tariff measures (NTMs), foreign market access barriers in export markets are rarely the binding constraint on trade expansion. The post-1980 experience makes clear that autonomous reforms drive economic development. However, non-tariff barriers and services trade restrictions do not figure prominently in the SDGs and the 2030 agenda. [The author: Bernard Hoekman]

Sixteen countries now in COMESA Free Trade Area

The number of member States participating in the COMESA Free Trade Area has risen to 16 following the passage of the required law by the DRC to join the regional economic community. Two other countries are expected enlist any time soon. Describing this development as positive, Director of Trade at the COMESA Secretariat, Dr Francis Mangeni said this will boost the levels of investment and intra-regional trade for the 19 member bloc. The 16 participating countries are Burundi, Comoros, Djibouti, Democratic Republic of Congo, Egypt, Kenya, Libya, Madagascar, Malawi, Mauritius, Rwanda, Seychelles, Sudan, Uganda, Zambia and Zimbabwe.

East African Parliamentary Institute: update

EAC Speakers are optimistic that the operationalization of the East African Parliamentary Institute (EAPI) shall go the mile in building capacities for legislators, Parliamentary staff and other stakeholders in Parliamentary practice and contribute to widening and deepening integration. The operationalization is expected in the next Financial Year once the EAPI Act, 2011, is gazetted by the EAC Council of Ministers. In addition, the EAC Bureau of Speakers considered a number of key areas deemed to strengthen integration as they held a one day Forum in Arusha, on April 29th, 2016. [New EA parliamentary body to help deepen integration]

IGAD Regional Infrastructure Master Plan: AfDB appraisal mission

The key objective for IRIMP is to establish regional infrastructure development that will enhance regional physical and economic integration through trade, free movement of goods and persons and poverty reduction amongst IGAD Member States. Regional Integration has been part of Africa’s strategy for economic transformation and the RECs including IGAD, are the building blocks that will enhance continental integration. IGAD Secretariat had submitted a request to the AfDB in June 2013 to support the preparation of the IRIMP. The Bank responded positively to this request for support. IRIMP is one of the deliverables set out under “IGAD Minimum Integration Plan/Roadmap” as part of the “Roadmap towards creating a Free Trade Area (FTA) in the IGAD Region” approved by IGAD Member States in Nairobi, Kenya in 2010 and the wider “Horn of Arica Initiative’.” After three fruitful days of discussions between IGAD and AfDB the aide memoire was signed on 27 April. According to the memoire the AfDB will fund the project at a cost of about $3.8m. The project will be structured into two components:

The 2016 Africa Logistics forum: COMESA joins initiative to improve security in Africa

The 2016 Africa Logistics forum which comprises African member States is exploring possible ways of avoiding conflict in the continent. This is by enhancing capacity among members States towards improving national, regional, and multinational logistical preparedness for peace support, humanitarian and disaster management response operations in Africa. This was disclosed during the forum hosted by the African Union in collaboration with partnership with the US Africa Command (AFRICOM) and the Washington D.C-based Africa Centre for Strategic Studies (ACSS) at the Koffi Annan International Peacekeeping and Training Centre, Accra, 12–14 April, 2016. The seminar noted that some RECS had made great strides in fostering regional integration efforts and in particularly the free movement of people, and exchange of goods and services that was accompanied by infrastructural development (roads/highways, ports, airports, and rail).

South Africa: March 2016 merchandise trade statistics (SARS)

The R2.92bn surplus for March 2016 is due to exports of R96.13bn and imports of R93.22bn, improving from a revised deficit of R1.27bn in February 2016. Exports increased from February 2016 to March 2016 by R5.66bn (6.3%) and imports increased from February 2016 to March 2016 by R1.48bn (1.6%). Africa trade surplus: R16 063 million – this is a 12.4% increase in comparison to the R14 295 million surplus recorded in February 2016. Europe trade deficit: R10 639 million – this is a 58.4% increase in comparison to the R6 716 million deficit recorded in February 2016. Asia trade deficit: R10 088 million – this is a 27.3% decrease in comparison to the R13 878 million deficit recorded in February 2016.

Is it worth it? (The Economist)

In reality, though, South African firms have proved more optimistic than most about the potential of the African market. Where they have failed, it has often been because they were too sanguine about infrastructure and working of the law. In particular, they put too much faith in the power of innovative product design. “You can come up with an amazing product here, but that doesn’t help you sell it in Nigeria if you haven’t got the contacts to get it out of the port,” says Safroadu Yeboah-Amankwah, the South Africa director of McKinsey, a management consultancy.

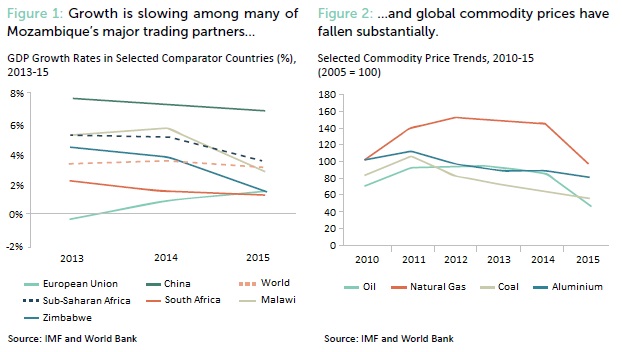

Mozambique: latest economic update (World Bank)

After several consecutive years of accelerating growth, Mozambique’s economic performance eased to its slowest pace since 2009, whilst the economy remains increasingly exposed to heightened levels of fiscal risk, according to the Mozambique Economic Update released today. Although Mozambique’s economic prospects remain sound, a robust policy response is vital to manage short term pressures and lay the ground for future growth. Mozambique has been substantially scaling-up public investment over the last few years. Financing has taken various forms. However, liabilities have accumulated at a rapid pace while the due diligence mechanisms to govern them more efficiently lagged. The report highlights the need to improve monitoring, disclosure and management of debt and fiscal risks. These efforts should be complemented by measures to improve the government’s capacity to appraise and manage public investments.

Uganda: Trade ministry takes over investment authority (Daily Monitor)

The activities of Uganda Investment Authority are now going to be overseen by the Ministry of Trade, Industry and Cooperatives, Daily Monitor has learnt. In an interview with this newspaper, Trade minister Amelia Kyambadde confirmed the development: “We think it belongs here in the Ministry of Trade. All the necessary expertise is here and it will now streamline trade and investment.”

Tanzania: How JPM fell out with TIC boss Kairuki (The Citizen)

Sacked Tanzania Investment Centre Executive Director Juliet Kairuki fell out with President John Magufuli over tax issues and an apparent arrangement through which she was reportedly earning a salary outside the established government structure, The Citizen can reveal. A brief government statement revealed yesterday that President Magufuli fired Ms Kairuki last Sunday for declining a salary offered to her since April 2013 when she was appointed. The Citizen has established, however, that a Tanzania Revenue Authority (TRA) tax bill slapped on Dangote Cement was at the centre of a heated dispute within government that may have cost Ms Kairuki the job for which she was head-hunted from South Africa by then President Jakaya Kikwete. [Vodacom’s contribution to Tanzania’s economy hits Sh4tr: study]

Eric Mboma: 'How China is building the future in sub-Saharan Africa – and why the US needs to rethink its approach' (SCMP)

While much is made of China’s expanding footprint in Asia, the reach of its global aspirations can be seen in Africa. The Democratic Republic of Congo reveals the complex dynamics of China’s interaction with the continent, and the inability of the US to balance it. The fundamental reason for this state of affairs is that American and Chinese foreign-policy priorities in sub-Saharan Africa, of which Congo is a part, diverge considerably. [The author is CEO Standard Bank Group in the DRC]

Creating optimal partnerships to tackle socio-economic problems: lessons from North Star Alliance (Knowledge@Wharton)

When it comes to tackling large-scale socio-economic problems, especially in emerging markets, several entities usually form partnerships to solve these challenges. But what is the optimal configuration of these partnerships and how should they best be coordinated for maximum effect? That is the topic of an ongoing research study led by Aline Gatignon. Gatignon and her colleagues are gathering their data from North Star Alliance, a non-profit that manages health clinics for truck drivers along African transport corridors. [Infrastructures: ces corridors africains qui valent de l'or (JeuneAfrique)]

Sustainable fisheries: international trade, trade policy and regulatory issues (UNCTAD)

In a ‘business-as-usual’ scenario, only half the amount of fish harvested in 1970 will be probably available by 2015 and only one-third by 2050. In contrast, fish consumption can be expected to expand substantially, as the global population is predicted to increase from over 7 billion presently to about 9-10 billion by 2050. These trends raise serious questions about the sustainability of the sector globally and related sector practices.

Angola-China Chamber of Commerce wants to encourage partnerships (Macau Daily Times)

Kenyan firms push for laws forcing EAC States to implement treaties (Business Daily)

Nigeria’s foreign reserves dip significantly, reverses previous gains (Vanguard)

Examining the Naira-Yuan deal (Leadership)

Foreign exchange policies of major trading partners of the United States (US Treasury)

Ethiopia: urgent action needed to help farmers produce food in main cropping season (FAO)

EU may appoint negotiator for bilateral trade pact with India (Livemint)

Seizing the moment in Asian economic diplomacy (editorial comment, East Asia Forum)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

Weakening growth in Sub-Saharan Africa calls for policy reset

After a prolonged period of strong economic growth, sub-Saharan Africa is set to experience a second difficult year as the region is hit by multiple shocks, the IMF said in its latest Regional Economic Outlook for Sub-Saharan Africa.

The steep decline in commodity prices and tighter financing conditions have put many large economies under severe strain, and the new report calls for a stronger policy response to counter the effect of these shocks and secure the region’s growth potential.

The report shows growth fell to 3½ percent in 2015, the lowest level in 15 years. Growth this year is expected to slow further to 3 percent, well below the 6 percent average over the last decade, and barely above population growth.

Hit by several shocks

The commodity price slump has hit many of the largest sub-Saharan African economies hard. While oil prices have recovered somewhat compared to the beginning of the year, they are still more than 60 percent below 2013 peak levels – a shock of unprecedented magnitude.

As a result, oil exporters such as Nigeria, Angola, and five of the six countries within the Central African Economic and Monetary Community continue to face particularly difficult economic conditions. The decline in commodity prices has also hurt non-energy commodity exporters, such as Ghana, South Africa, and Zambia.

Compounding this shock, external financing conditions for most of the region’s frontier markets have tightened substantially compared to the period until mid-2014 when they enjoyed wide access to global capital markets.

In addition, a severe drought in several southern and eastern African countries, including Ethiopia, Malawi, and Zimbabwe, is putting millions of people at risk of food insecurity.

Medium-term prospects still favorable

However, the impact of these shocks varies significantly across the region and many countries continue to register robust growth, including in per capita terms (see Chart 2).

In particular, most oil importers are faring much better with growth of 5 percent or higher in countries such as Côte d’Ivoire, Kenya, Senegal, and many low-income countries. These countries continue to benefit from infrastructure investment efforts and strong private consumption.

While the immediate outlook for many sub-Saharan African countries remains difficult, the region’s medium-term growth prospects are still favorable. The underlying domestic drivers of growth at play over the last decade generally continue to be in place. In particular, the region’s much improved business environment and favorable demographics should help bolster growth in the medium term.

Policy reset urgently needed to secure growth potential

To reap this strong potential, however, a substantial policy reset is critical in many cases, as the policy response to date has generally been insufficient.

In commodity exporting countries, where fiscal and foreign reserves are depleting rapidly and financing is constrained, the response to the shock needs to be prompt and robust to prevent a disorderly adjustment. Countries outside monetary unions should use exchange rate flexibility, as part of a wider macroeconomic policy package, to absorb the shock. As revenue from the extractive sector is likely durably reduced, many affected countries also critically need to contain fiscal deficits and build a sustainable tax base from the rest of the economy.

Given the substantially tighter external financing environment, market access countries with elevated fiscal and current account deficits will also need to recalibrate their fiscal policies to rebuild scarce buffers and mitigate vulnerabilities if external conditions worsen further.

The required measures may come at the cost of lower growth in the short-term. However, they will prevent what could otherwise be a significantly more costly disorderly adjustment. These policies would lay the ground work needed for the region to reap the substantial economic potential which still lies ahead.

In two background studies, the Regional Economic Outlook also examines the current commodity terms-of-trade shock and policy responses against past downswings, and the economic impact of progress made in financial development. The region has made strides in broadening access to financial services through the use of mobile technology, and the expansion of home-grown pan-African banks.

IMF calls for a policy reset to secure sub-Saharan Africa’s medium-term growth

After an extended period of strong economic growth, sub-Saharan Africa is set to experience a second difficult year as the region is hit by multiple shocks, the International Monetary Fund (IMF) said today.

According to its April 2016 Regional Economic Outlook for Sub-Saharan Africa, Time for a Policy Reset, growth in the region as a whole is projected to fall to 3 percent in 2016, the lowest level in some 15 years, albeit with considerable differences across the region.

While the outlook remains favorable, growth is well below the 6 percent that was customary over the last decade, and barely above population growth. “Africa needs a substantial policy reset to reap the region’s strong potential,” said Antoinette Sayeh, Director of the IMF’s African Department. “This is particularly urgent in commodity exporters and some market access countries, as the policy response to date has generally been insufficient.

The slowdown reflects the adverse impact of the commodity price slump in some of the larger economies and more recently the drought in eastern and southern Africa. The sharp decline in commodity prices, a shock of unprecedented magnitude, has put many of the largest sub-Saharan African economies under severe strain. As a result, oil exporters, such as Nigeria and Angola but also most countries of the Central African Economic and Monetary Union, continue to face particularly difficult economic conditions. Non-energy commodity exporters, such as Ghana, South Africa and Zambia, have also been hurt by the decline in commodity prices. Several southern and eastern African countries, including Ethiopia, Malawi, and Zimbabwe, are suffering from a severe drought that is putting millions of people at risk of food insecurity.

However, Ms. Sayeh stressed that the outlook remains favorable. “Many countries in the region continue to register robust growth. In particular, most oil importers are generally faring better with growth in excess of 5 percent in countries such as Côte d’Ivoire, Kenya, and Senegal, as well as in many low-income countries. In most of these countries, growth is being supported by ongoing infrastructure investment efforts and strong private consumption. The decline in oil prices has also benefitted many of these countries, though the drop in prices of other commodities that they export, and currency depreciations, have partly offset the gains. More broadly, medium-term growth prospects remain favorable, as the underlying drivers of growth at play domestically over the last decade generally continue to be in place. In particular, the much improved business environment and favorable demographics should play a supportive role in the coming decades.

“Faced with rapidly decreasing fiscal and foreign reserves and constrained financing, commodity exporters should respond to the shock promptly and robustly to prevent a disorderly adjustment. As revenue from the extractive sector is likely durably reduced, many affected countries critically need to contain fiscal deficits and build a sustainable tax base from the rest of the economy. For countries outside monetary unions, exchange rate flexibility, as part of a wider macroeconomic policy package, should also be part of the first line of defense.

“Given the substantially tighter external financing environment, market access countries in which fiscal and current account deficits have been elevated over the last few years will also need to recalibrate their fiscal policies. Such recalibration would help them to rebuild scarce buffers and mitigate vulnerabilities if external conditions worsen further.”

Related News

Mozambique Economic Update: Growth slows amid challenging global conditions and rising fiscal risks

After several consecutive years of accelerating growth, Mozambique’s economic performance eased to its slowest pace since 2009, whilst the economy remains increasingly exposed to heightened levels of fiscal risk, according to the Mozambique Economic Update released today.

Mozambique’s economy continues to face challenges of weaker commodity prices, lower demand amongst trading partners and rising U.S. interest rates, according to the inaugural edition of the Mozambique Economic Update (MEU). The already difficult headwinds are further aggravated by regional drought, falling investment levels, political instability and rising debt levels. Amid these conditions, the report predicts growth will continue to slow this year.

“Given the current environment, it’s important for Mozambique to press ahead with reforms aimed at securing macroeconomic stability whilst also maintain the longer term focus on a resilient and diversified economy,” said Mark R. Lundell, World Bank country director for Mozambique, Madagascar, Mauritius, Seychelles and Comoros. The report covers the period to March 2016.

Recent Economic Developments and Outlook

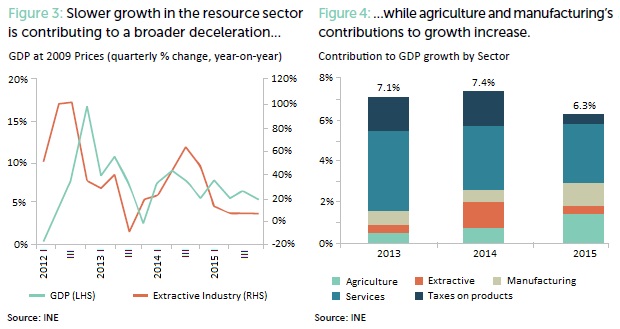

The MEU reviews recent economic developments and assesses near-term economic prospects, forecasting that growth will slow further to 5.8% in 2016, before rising above 7% in 2017. Much like other resource-rich countries, the Mozambican economy continues to face the challenges of low commodity prices and weak demand amongst trading partners, as well as regional drought. These difficult conditions are further aggravated by falling investment levels and rising public debt. In 2015, foreign direct investment fell by 24 percent, exports declined by 14 percent and growth decelerated to 6.3 percent, its slowest level since 2009.

The projected slowdown in 2016 reflects the continued decline in commodity prices for key Mozambican exports, effects of the ongoing drought on agricultural production, and further fiscal tightening, according to the report. This outlook is subject to additional downward risk if gas megaproject investments are deferred to 2017 the report says, and if rising debt levels result in sharper policy adjustment. Given the weak external position, the report notes further currency depreciation is likely and will add to inflationary pressures in 2016.

The adverse external environment is expected to persist through 2016. The report projects that a continued decline in prices for key exports, the ongoing drought and further fiscal tightening will further decelerate GDP growth to 5.8 percent in 2016, before recovering to over 7 percent in 2017. This outlook is subject to further downward risk if investment levels remain subdued and if rising debt levels lead to sharper fiscal and monetary policy adjustments.

Although short-term economic pressures are pronounced, the MEU notes that medium-term prospects for economy remain sound. Large investment flows from the gas sector are expected between 2017 and 2020. These flows will support the widening of the current account deficit and boost growth. Gas exports are expected to ramp up by 2022 and the current account deficit to shrink thereafter.

“Short-term pressures in 2016 point to the importance of rebalancing the external position, rebuilding international reserves and securing final investment decisions for the development of the Rovuma basin gas fields,” noted Shireen Mahdi, World Bank Senior Country Economist for Mozambique.

Special Focus on Fiscal Risk

The report also includes a special focus section on public investment and fiscal risk arising from public debt, guarantees, state owned enterprises and public private partnerships. Mozambique has been substantially scaling-up public investment over the last few years. Financing has taken various forms. However, liabilities have accumulated at a rapid pace while the due diligence mechanisms to govern them more efficiently lagged. The report highlights the need to improve monitoring, disclosure and management of debt and fiscal risks. These efforts should be complemented by measures to improve the government’s capacity to appraise and manage public investments.

“It will be increasingly important that the authorities ensure thorough assessment of the country’s fiscal risks and increase transparency through greater disclosure,” highlighted Lundell.

Related News

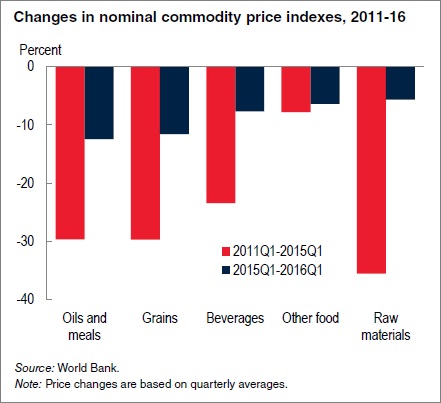

World Bank raises 2016 oil price forecast, revises down agriculture price projections

Oil prices seen rising as oversupply diminishes

Amid improving market sentiment and a weakening dollar, the World Bank is raising its 2016 forecast for crude oil prices to $41 per barrel from $37 per barrel in its latest Commodity Markets Outlook, as an oversupply in markets is expected to recede.

The crude oil market rebounded from a low of $25 per barrel in mid-January to $40 per barrel in April following production disruptions in Iraq and Nigeria and a decline in non-Organization of the Petroleum Exporting Countries production, mainly U.S. shale. A proposed production freeze by major producers failed to materialize at a meeting in mid-April.

“We expect slightly higher prices for energy commodities over the course of the year as markets rebalance after a period of oversupply,” said John Baffes, Senior Economist and lead author of the Commodities Markets Outlook. “Still, energy prices could fall further if OPEC increases production significantly and non-OPEC production does not fall as fast as expected.”

All main commodity indexes tracked by the World Bank are expected to decline in 2016 from the year before due to persistently elevated supplies, and in the case of industrial commodities – which include energy, metals, and agricultural raw materials – weak growth prospects in emerging market and developing economies.

Energy prices, including oil, natural gas and coal, are due to fall 19.3 percent in 2016 from the previous year, a more gradual drop than the 24.7 percent slide forecast in January. Non-energy commodities, such as metals and minerals, agriculture, and fertilizers, are due to decline 5.1 percent this year, a downward revision from the 3.7 percent drop forecast in January.

Metals prices are projected to fall 8.2 percent in the coming year, less than the 10.2 percent drop forecast in January, reflecting expectations of stronger demand growth by China. Agriculture prices are forecast to fall more than projected in January in what is expected to be another favorable harvest year for most grain and oilseed commodities. Agricultural commodities prices are also pulled down by lower energy costs.

Low commodity prices are undermining growth prospects for many resource-rich countries that experienced a surge in exploration, investment, and production during the commodities boom of the 2000s. Countries that have borrowed and invested heavily in anticipation of faster growth may struggle to service their debt and sustain investment when growth disappoints as a result of lower commodity prices, a special feature of the Commodity Markets Outlook says.

With oil and metals prices today 50 percent to 70 percent lower than their early 2011 peaks, natural resource development projects have already been put on hold or delayed in several emerging and developing countries.

“These project delays can adversely affect countries that can ill-afford such setbacks,” said Ayhan Kose, Director of the World Bank’s Development Prospects Group. “Greater transparency, improved government efficiency and improvements in macroeconomic frameworks could soften such disruptions. Countries may prefer to wait for prices to start rising again before launching new natural resource development initiatives.”