Search News Results

Global commitment to multilateral agreements key towards achieving sustainability, says UN Secretary-General

With billions of lives hanging in the balance, the next phase of development depended on the international community’s commitment to build on recent multilateral agreements and put the world on a sustainable path, stressed Secretary-General Ban Ki-moon as the Economic and Social Council opened its inaugural forum on financing for development follow-up on Monday, 18 April 2016.

“Now is the time for smart investments in people and the planet,” he said, calling on States, United Nations entities and other stakeholders to sustain the political momentum that had led to the adoption of the 2030 Agenda for Sustainable Development, the Addis Ababa Action Agenda on Financing for Development and the Paris Agreement on climate change in 2015.

While those agreements were triumphs of multilateralism, he said, the time for implementation was now. The Addis Agenda, in particular, provided a full range of actions to realign financial flows and policies with economic, social and environmental priorities. The global response to the 2030 Agenda must match the scope of the challenge, which meant tapping into the potential of all actors to achieve the transformation that was needed.

Opening the meeting, Oh Joon (Republic of Korea), President of the Economic and Social Council, said the launch of the forum marked a new chapter in the organ’s history. Mandated by the Addis Agenda, the Council served as a platform for policy dialogue on financing for development follow-up. Among other things, it was tasked to assess progress, identify challenges and facilitate the delivery of the means of implementation of sustainable development.

High-level speakers throughout the meeting agreed with the Secretary-General that implementation would be the true test of the international community’s commitment to achieving the targets of the 2030 Agenda. The heads of a number of United Nations departments and agencies described their contributions to those ends.

“We can all do something, wherever we have expertise,” said Christine Lagarde, Managing Director of the International Monetary Fund (IMF), who spoke via video link. Echoing calls from other speakers for concerted action that was tailored to the needs of countries and their people, she described work being done by the Fund in areas including macroeconomic policy, taxation, climate change and inclusive growth. On the latter, for example, spending on the education of young people could deliver the biggest development gains.

Helen Clark, Administrator of the United Nations Development Programme (UNDP), said that while monitoring the implementation of sustainable development commitments would be a complex exercise, the forum could support the process with adequate planning. For its part, UNDP could showcase a wide range of innovative approaches, from green financing to impact investing, and would continue to provide a platform for Member States to share their ideas, technologies and capacities.

Other speakers pointed to current global challenges, including slow economic growth and massive waves of forced migration, as hurdles to be overcome by concerted action and innovative development financing.

“We have started off on a bumpy ride” to realize the efforts of the 2030 Agenda, said Mukhisa Kituyi, Secretary-General of the United Nations Conference on Trade and Development (UNCTAD). Flows of foreign direct investment to sub-Saharan Africa had declined and there was limited positive recovery in trade. Meanwhile, official development assistance (ODA) was at a standstill, he said, calling for “repurposed” international institutions, refocused expertise and more coherent action.

As the forum began its general debate, ministers and other high-ranking officials from Governments around the globe underscored the important role of the meeting, as well as the Addis Agenda itself, in financing the next era of sustainable development. Many called for increased capacity-building and the creation of enabling environments to assist developing countries in achieving the aims of the 2030 Agenda.

Unfair trade rules were only one obstacle to sustainable development, said the representative of Uganda, speaking on behalf of the African Group. Others included inadequate resources exacerbated by illicit financial flows and unmet official development assistance commitments. Highlighting the importance of national ownership in sustainable development, he said the Group was committed to take the lead in formulating policies that would facilitate the integration of the Addis Agenda and the 2030 Agenda into its national plans and priorities.

“It doesn’t matter how much money we spend, if we spend it on the wrong things,” said Isabella Lövin, Minister for International Development Cooperation of Sweden. Countries, institutions and the private sector must work together to deliver the resources needed for climate finance, she said, adding that gender equality and the empowerment of women and girls would be necessary given the linkages between women’s economic participation and increased growth.

In the afternoon, the Forum held an interactive dialogue with intergovernmental bodies of major institutional stakeholders on the theme “Fostering policy coherence in the implementation of the Addis Ababa Action Agenda”.

Also addressing the forum this morning were Roberto Azevêdo, Director-General of the World Trade Organization (WTO); Mahmoud Mohieldin, Senior Vice-President for the 2030 Development Agenda, World Bank Group; Bambang Brodjonegoro (Indonesia), Chairman, IMF/World Bank Development Committee; Alfredo Suescum (Panama), President, Trade and Development Board, UNCTAD; Calvin McDonald, Deputy Secretary of IMF and Acting Secretary of the International Monetary and Financial Committee; Wu Hongbo, Under-Secretary-General for Economic and Social Affairs, and Chair of the Inter-Agency Task Force on Financing for Development; and Shamshad Akhtar, Under-Secretary-General and Executive Secretary of the Economic and Social Commission for Asia and the Pacific (ESCAP).

Participating in the general debate were the representatives of the European Union, Guatemala, Panama, Netherlands, Iran, Thailand (on behalf of the “Group of 77” developing countries and China), Maldives (on behalf of the Alliance of Small Island States), Honduras (on behalf of the Like-Minded Group of Supporters of Middle-Income Countries), Mexico, Denmark, Philippines, Lebanon, United Arab Emirates, Norway, Italy, Argentina, Colombia, Brazil, Sri Lanka, Indonesia and the Organisation for Economic Co-operation and Development (OECD).

Related News

State of the Africa region: The time to reform is now

During the recent State of the Africa Region, World Bank Vice President Makhtar Diop cited reforms as key to reigniting growth and helping African countries achieve structural transformation.

While growth in African countries continues to slow amid a weakened global economy, reforms can stimulate growth and help countries achieve structural transformation.

This was the message from World Bank Africa Vice President Makhtar Diop in his State of the Africa Region address during the World Bank-IMF Spring Meetings.

“Despite weak global growth, a difficult external environment facing Sub-Saharan Africa in the near-term, and low and volatile commodity prices, this worsening situation also presents us with a significant opportunity to transform Africa’s economies,” Diop said. “It has signaled an urgent need for economic diversification in Africa.”

Using data from the recently-released Africa’s Pulse, Diop led a panel discussion with a presentation highlighting challenges and opportunities for countries in the short and medium term. The panel included Louis-Paul Motazé, Cameroon’s Minister of Economy, Planning and Regional Development and Claver Gatete, Minister of Finance and Economic Planning for Rwanda.

According to the latest World Bank projections, Sub-Saharan Africa’s gross domestic product (GDP) growth slowed to an estimated 3.0% in 2015 from 4.5% in 2014. This low pace of growth was last seen in 2009 following the global financial crisis.

The fall in commodity prices represents a significant shock for the region, as fuels, ore and metals account for more than 60% of the region’s exports. The impact is seen most in oil-exporting countries, such as Nigeria, the Republic of Congo, and Equatorial Guinea. Activity also weakened significantly in non-energy mineral-exporting countries, including Botswana, Sierra Leone, South Africa and Zambia.

“In order to start tackling challenges we are facing, we have no other choice but to increase domestic resource mobilization, remove trade barriers, improve education, invest in agriculture and renewable energy,” Diop said.

There were some bright spots, mostly among oil importers, where economic activity remained robust. Côte d’Ivoire saw broad-based growth, supported by a favorable policy environment, rising investment, and increased consumer spending. Ethiopia and Rwanda continued to post solid growth, supported by public infrastructure investment, private consumption, and a growing services sector. Elsewhere, growth remained buoyant in Kenya, amid improving economic stability; Tanzania registered strong growth, underpinned by expansion in construction and services sectors.

“What helped us leap frog is the digitalization of the economy,” Gatete said. “ICT is part of almost everything in Rwanda today. It is transforming our lives, people are paying by phone and we are moving very fast in that area. We have also been improving the efficiency of tax collection and put in place policies to improve regional integration between Kenya, Uganda and Rwanda, eliminating all unnecessary costs and hurdles for transporting goods.”

With commodity prices expected to remain low for longer amid a gradual pickup in global activity, the Pulse forecasts that average growth in the region will remain subdued at 3.3% in 2016. For 2017-18, growth is projected to average 4.5%.

“In Cameroon, despite all the efforts we make, the results are still not good enough, as there are so many challenges we are facing. Security is one of them, which leaves us with less resources for other areas,” said Motazé. “That is why specialization is very important for us. For example, in education, we need to train a critical mass of students in specific areas that the country actually needs, and this, in turn, will help us transform our economy. We are determined to put in place all the right policies to help the situation, but we need all the partners to work with us in order to succeed.”

Africa’s Pulse finds that well-managed cities provide a major opportunity for much needed economic diversification. Today cities in Africa are crowded, disconnected, and costly for families and for companies, according to World Bank research. Cities must offer services, amenities, and housing for the poor and the middle class. Successful urbanization will also support Africa’s agricultural and rural transformation by effectively absorbing the labor being released by these sectors; by providing a market for agricultural produce; and by financing further transformation and commercialization.

“These are not small tasks, and they require reforms that will not be easy – they will require commitment and courage on the part of Africa’s leaders. The cushion that high commodity prices provided to many countries is now largely gone. We are here to work with you and to support you,” closed Diop.

Related News

tralac’s Daily News Selection

The selection: Monday, 18 April 2016

Today, in Gaborone: President Jacob Zuma visits Botswana, then Namibia and Swaziland, on SACU issues

Today, in Mauritius: seminar on WTO Agreement on Subsidies and Countervailing Measures

Today, in New York: Special High-Level Meeting of ECOSOC with the Bretton Woods institutions, WTO, UNCTAD

Tomorrow, in London: tralac's Trudi Hartzenberg, and others, participate in the inquiry into the UK’s Africa Free Trade initiative

On Thursday, in Geneva: Aid for eTrade consultation on a draft call for action (UNCTAD)

UNCTAD is taking the lead in exploring possibilities for launching a new global initiative called Aid for eTrade, aimed at unlocking the potential of e-commerce in developing countries. Aid for eTrade is intended to be a multi-stakeholder initiative to improve the ability of developing countries and countries with economies in transition to use and benefit from e-commerce. It will be a demand-driven mechanism in which leading development partners cooperate with the private sector to pool capabilities and resources. The goals of the initiative are as follows: [Download the draft]

The World Bank, IMF Spring Meetings concluded over the weekend. A guide to some key outcomes:

African Consultative Group Meeting: statement by Abdoulaye Bio-Tchané, Christine Lagarde (IMF)

We concurred that the decline in commodity prices is likely to be long lasting, as the causes seem structural rather than temporary—including the ongoing rebalancing of demand in China and, in the case of oil, technological innovation that has enhanced supply. We also recognized that non-economic shocks such as weather- and security-related challenges, are posing downside risks to Africa’s economic prospects.”

Related: Drought, insecurity add to commodity woes – African Ministers, AfDB Governors from Rwanda and Nigeria paint realistic – and optimistic – picture of Africa

Development Committee: communiqué (IMF)

We are encouraged by progress on the Forward Look exercise on the medium to long term future of the WBG, which aims to ensure that the Group remains a strong global development institution in an evolving development landscape; and we expect a final report by the Annual Meetings. The Board and management shall develop proposals to ensure that the WBG remains responsive to the diverse needs of all its clients; leads on global issues and knowledge; makes the “billions to trillions” agenda a reality; partners effectively with the private sector; becomes a more effective and agile development partner; and adapts its business model accordingly.

Global Infrastructure Forum: inaugural meeting

Mandated by the Addis Ababa Action Agenda on financing for development to help bridge the infrastructure gap, which is key to achieving the Sustainable Development Goals (SDGs), the Forum aims to improve alignment and coordination among the partners, while respecting the diversity of approaches, policies, and procedures among them, to facilitate the development of sustainable, accessible, and resilient infrastructure for developing countries. The Forum will be held annually, with responsibility for hosting rotating among the MDBs. [Akinwumi Adesina at the GIF: 'The future of Africa lies inside Africa']

International Monetary and Financial Committee: communiqué

We welcome the IMF’s growing engagement with small states. We welcome proposed work on other challenges facing the membership—within the IMF’s mandate and where they are macro-critical—including migration, income inequality, gender inequality, financial inclusion, corruption, climate change, and technological change, including by leveraging the expertise of other institutions. To support countries managing spillovers from non-economic sources, such as large refugee flows and global epidemics, the IMF should be prepared to contribute within its mandate, including to global initiatives. We look forward to a review of the Guidance Note on The Role of the Fund in Governance Issues. We encourage the IMF to continue helping countries to strengthen their institutions to tackle illicit financial flows.

The 2016 edition of World Development Indicators is out: three features you won’t want to miss (World Bank)

The Global Consumption and Income Project: project launch, data

African trade and regional integration updates:

Namibia: Livestock industry jittery as SA stays mum on requirements (New Era)

Almost four months after meeting all the requirements set out by South African authorities regarding new import measures on January 08, Namibia’s N$2bn per annum livestock industry remains in the dark about the future as no date has yet been announced for implementation of the prerequisites. Neither has South Africa confirmed whether the Standard Handling Procedure, as communicated with Namibia, been accepted or not, or the contents of a new official veterinary import certificate to accompany the Standard Handling Procedure been made known. What has been dubbed a cat-and-mouse-game by SA authorities since May 2013, has now resulted in an urgent livestock industry meeting to take place today regarding markets for cattle producers in the northern communal areas , which produce up to 70 percent of the lucrative weaner exports of some 180 000 animals per year.

Zim records trade surplus against SA (Fin24)

According to figures from Zimstat, Zimbabwe imported goods worth $476.1m from South Africa in the three months ended March 31 2016. This was against exports to South Africa amounting to $504.6m for the period under review. As a result, Zimbabwe has recorded a trade surplus of 5.98% against its neighbour for the first time in years. Overall, Zimbabwe's trade deficit narrowed 17.7% after imports came down 17% to $1.32bn from $1.6bn in the same comparable period last year. Exports were at $625.96m, a 12.6% drop from $716.6m last year. [In the three months to March, Singapore overtook South Africa as Zimbabwe's largest import destination]

African governments urged to invest in cashew industry (GhanaWeb)

Ms Rita Weidinge, Executive Director of African Cashew Initiative (ACI), has called on African governments to invest in the production and policy development of the cashew sector, to increase economic value and enhance private investment. She noted that it is imperative for Africa to put in place consistent and coherent strategy in the value chain by investing in research for the growth of the sector. Ms Weidinge made the call at the weekend in Accra at a consultation of African Public and technical Actors in Cashew on the theme: "Opportunities of the African cashew sector”. The workshop brought together public officials from the ministries related to the cashew sector, public Pan-African actors: African Union Commission and Regional Economic Communities.

Uganda exports 70 tonnes of ARVs to Namibia (The East African)

Quality Chemicals broke into regional markets in 2011 when its drugs were bought by Global Fund, to fight HIV/Aids, tuberculosis and malaria in Kenya. Later, the company exported drugs to Tanzania, South Sudan, Zambia, Cameroon, Comoros; Namibia is its seventh export market. Company officials told The EastAfrican that the deal was reached after six months of bilateral negotiations with Namibia’s Ministry of Health. [Uganda launches plan to promote IT exports]

Non-tariff barriers on selected goods faced by exporters from the EAC to the EU and USA (CUTS Geneva)

Based on two case studies, this study found that the main NTBs for EAC Exporters in the cut flowers and coffee sectors, facing the EU and the US, are: [The authors: Françoise Guei, Famke Schaap] [KNCCI automates issuance of Certificates of Origin]

Kenya: The makers of fake goods now cover practically every sector (Daily Nation)

In the past year alone, the Kenya Bureau of Standards (KEBS) has destroyed substandard goods valued at Sh57.7 million impounded in Nairobi and its environs. The goods have now gained a wider market. KEBS Chief Manager for Market Surveillance Raymond Michuki said the dealers in fake products are increasingly targeting far-flung towns. KEBS has launched an SMS platform to verify the authenticity of goods, where you send a brand name after a # to 20023 to verify if a product is genuine (i.e. sms SM#Brand name or permit number to 20023).

Draft Bill proposes new EAC regional retirement policy (Daily Nation)

“The draft is being handled by the Treasury and stakeholders are contributing their input and aligning it with the country’s labour laws before it is taken to the Cabinet. We want to come up with a guiding policy that could apply throughout Kenya, Uganda, Tanzania, Rwanda, Burundi and South Sudan,” said Retirement Benefits Authority chief executive Edward Odundo. Mr Odundo said a committee had also been set up by EAC member states to harmonise tax regime and retirement issues across the region.

Uganda systematic country diagnostic: boosting inclusive growth and accelerating poverty reduction (World Bank)

The report noted that Uganda’s physical and social economic progress over the last three decades represents a mixed bag of positives and negatives. While major milestones have been achieved in terms of growth, primary school enrollment and access to health services, the report notes that stakeholders still present strong concerns about inclusiveness of the growth, sustainability of progress made as well as quality of services. The SCD also notes that while there is a significant reduction of poverty from 54.6% in 2002/2003 to 19.7% in 2012/2013), there’s a wide inequality with 85% of the poor found in the North and Eastern Uganda of which two-thirds of the population is vulnerable. Recommendations from the report for prioritization include: [Download]

Mozambican researchers question weak investment in Zambezia (Club of Mozambique)

An analysis published this month by the Observatory of Rural Environment (Observatório do Meio Rural / OMR) asks why Zambezia province occupies the worst positions when it comes to economic development in the country. Although about 19% of the total population of the country live in Zambezia and about 5% in the city of Maputo, the capital receives 10% of the state budget and Zambezians only 9%.

Making trade work for Least Developed Countries: a handbook on mainstreaming trade (UNCTAD)

Least developed countries have very high trade-to-GDP ratios, reflecting the fact that they are heavily dependent on trade. Over the past few decades, they have also embarked upon significant trade reforms. LDCs account for about 12% of world population but less than 2% of world trade, indicating that they have not fully reaped the potential benefits of trade for development. A key reason for this is that these countries have low productive capacity and have not effectively integrated trade into their national development strategies and plans. The project had six LDCs as beneficiaries: Ethiopia, Lesotho, and Senegal in Africa:

South Africa: Mining Charter changes worsen division (Business Day)

Indian Ocean Dialogue adopts ‘Padang Consensus’ for enhancing cooperation (BDNews24)

AU, US Congress talks on strengthening cooperation, including trade (AU)

Africa expands trade presence in east Chinese city, Yiwu (New Era)

Financing healthcare in Africa: CABRI position paper

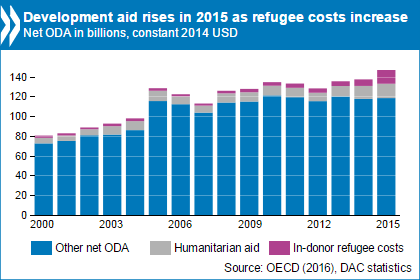

Development aid rises again in 2015, spending on refugees doubles (OECD)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

Hearings: Inquiry into the UK’s Africa Free Trade initiative

The All-Party Parliamentary Group on Trade Out of Poverty is undertaking an inquiry into the UK’s Africa Free Trade Initiative (AFTi), which was launched by the Prime Minister five years ago.

The Inquiry, taking place on Tuesday, 19 April 2016, will look at progress, potential and future development of the Africa Free Trade Initiative. This Inquiry seeks to answer the following three main questions:

-

What has been achieved in AFTi since 2011 and what lessons can be learned?

-

Is there a case for a successor to AFTi in the area of further facilitating trade and investment within Africa as a driver of growth and poverty reduction, and between African and the rest of the world, including the UK?

-

What should a future AFTi look like, what targets should it seek to achieve, and through which means and partnerships should it be delivered?

The Inquiry is led by a committee co-chaired by Lord Stephen Green, former Minister of State for Trade and Investment and Group Chairman of HSBC, and Mr. Ali Mufurki, Board Chair of TradeMark East and founder and Chairman of Infotech Investment Group. Other Committee members include Prof. Myles Wickstead, former Head of Secretariat, Commission for Africa and Ambassador Darlington Mwape, Senior Fellow at International Centre for Trade and Sustainable Development (ICTSD) and former Permanent Representative of Zambia to the WTO.

The Secretariat for the APPG-TOP, Saana Institute, will support the Inquiry committee in gathering evidence, organising hearings and preparing its Report.

» Written submissions supporting the Inquiry are available here.

About the Africa Free Trade initiative (AFTi)

The UK government launched the Africa Free Trade initiative (AFTi) in February 2011 to help African countries integrate into the global world trade system, using trade as an instrument for economic growth and poverty alleviation.

Recognised as a priority in the UK Trade and Investment for Growth Whitepaper, AFTi has brought together regional trade initiatives from across the Department for International Development (DFID), the Department for Business Innovation and Skills (BIS) and the Foreign and Commonwealth Office (FCO) to provide investment, technical assistance and political support to enhance trade in Africa. This included providing support to African countries on the design of border posts, infrastructure investment and analysis of major transport bottlenecks.

Related News

Development Committee: World Bank Group, IMF urged to help solve refugee crisis, other challenges

Government ministers from around the world confronted the refugee crisis, a slowing economy, and other global challenges at the 2016 World Bank Group-IMF Spring Meetings.

“Forced Displacement and Development” was the only item on the agenda at the Development Committee meeting on Saturday. The committee, which represents the 189 shareholder countries of the Bank Group and the IMF, urged its members to take action to support vulnerable people who have been forced to flee their homes, and encouraged the institutions to partner with humanitarian organizations to help forcibly displaced people and host communities confront the root causes of the problem.

“We will not reach our end poverty goal unless nations are secure and citizens are not confronted by conflict and violence,” said World Bank Group President Jim Yong Kim. “The tragedy of forced displacement causes a tremendous amount of human suffering, as we have seen on a daily basis with the Syrian refugee crisis.”

The meeting followed pledges on Friday by eight countries and the European Commission, who contributed to a package of more than $1 billion in support of Syrian refugees and host communities in Jordan and Lebanon, as well as reconstruction in the Middle East and North Africa.

Japan, France, the United Kingdom, the United States, Germany, Canada, the Netherlands, Norway, and the European Commission pledged contributions to the New Financing Initiative to Support the Middle East and North Africa Region, launched jointly by the World Bank Group, the United Nations, and the Islamic Development Bank Group last October.

Earlier Friday, Jordan’s Queen Rania and other high-ranking officials called for a new approach to forced displacement and a refugee crisis that has spread from the Middle East into Europe over the last year.

“We must respond to this monumental crisis with monumental solidarity,” said United Nations Secretary-General Ban Ki-moon, adding that the issue will be addressed at next month’s World Humanitarian Summit.

Countries are facing the refugee crisis and other global challenges such as climate change in an environment of slowing global growth. The Development Committee asked the Bank Group and IMF to provide developing countries with policy advice and financial support amid weak demand, tighter financial markets, softening trade, persistently low oil and commodity prices, and volatile capital flows.

Demand for lending from the Bank Group is at its highest for a non-crisis period and is on track to climb to more than $150 billion over four years.

“We’re now working urgently and in new ways with partners to find solutions to these issues that affect all of us,” Kim said, addressing the media at the beginning of the Meetings.

One of those issues is climate change. The committee welcomed the Bank Group’s Climate Change Action Plan to help developing countries add 30 gigawatts of renewable energy – enough to power 150 million homes – to the world’s energy capacity, bring early warning systems to 100 million people, and develop climate-smart agriculture investment plans for at least 40 countries – all by 2020.

The committee urged the Bank Group to work with the World Health Organization and others to help developing countries strengthen their health systems, including pandemic prevention and preparedness. It also urged the Bank Group to finish preparing its Pandemic Emergency Facility “as soon as possible and foster a new market for pandemic risk management insurance.”

On Thursday, Kim and UNICEF Executive Director Anthony Lake urged global and national leaders to step up and accelerate action and investment in nutrition and early childhood development programs as a critical foundation for equitable development and economic growth. The Bank and WHO also hosted a livestreamed event on the need to make mental health a global development priority.

The committee urged the Bank Group and IMF to step up efforts to find financing for the ambitious Sustainable Development Goals, approved in September, which are expected to require far more resources than official development aid can supply. It said the multilateral development banks should partner to “support developing countries’ efforts to meet the SDGs, while adjusting to a slower growth environment and reduced private capital flows.”

The committee said gender equality is central to the SDGs and welcomed the Bank Group’s renewed gender strategy.

A special event with U.S. First Lady Michelle Obama on Wednesday highlighted the issue in the context of equal access to education for girls. Obama urged leaders to put girls’ education at the “very top” of their agenda. Kim announced the Bank Group would invest $2.5 billion in education projects benefiting adolescent girls over the next five years.

The committee said the International Development Association, the World Bank’s fund for the poorest countries, remains an important source of financing for these countries and asked donors to show strong support for IDA’s replenishment this year.

Development Committee Communiqué

World Bank/IMF Spring Meetings 2016

-

The Development Committee met today, April 16, in Washington, D.C.

-

Global growth continues to disappoint in 2016. Substantial downside risks to growth remain, including weak demand, tighter financial markets, softening trade, persistently low oil and commodity prices, and volatile capital flows. We call on the World Bank Group (WBG) and the International Monetary Fund (IMF), within their respective mandates, to monitor these risks and vulnerabilities closely, and update the Debt Sustainability Framework for Low-Income Countries. We also call on them to provide policy advice and financial support for sustained, inclusive and diversified growth and resilience.

-

We are encouraged by progress on the Forward Look exercise on the medium to long term future of the WBG, which aims to ensure that the Group remains a strong global development institution in an evolving development landscape; and we expect a final report by the Annual Meetings. The Board and management shall develop proposals to ensure that the WBG remains responsive to the diverse needs of all its clients; leads on global issues and knowledge; makes the “billions to trillions” agenda a reality; partners effectively with the private sector; becomes a more effective and agile development partner; and adapts its business model accordingly. The Board and management should continue to consider ways to strengthen the financial position of the WBG institutions, including by optimizing the use of their existing resources, so that they are adequately resourced to accomplish the Group’s mission.

-

Fragility and conflict have displaced millions of people, significantly impacting both origin and host countries. We look forward to WBG and IMF action in this area, within their respective mandates and in partnership with humanitarian and other actors, to mitigate the vulnerabilities of forcibly displaced persons, to help host communities manage shocks, and to tackle the root causes of forced displacement. We urge the international community to take action in supporting these vulnerable populations who largely live below the poverty line. We recognize the sacrifices and generosity of host countries and the lack of adequate instruments to support them. We welcome Islamic Development Bank, UN and WBG efforts to develop the financing facility for the Middle East and North Africa and donor commitments to this initiative. We ask the WBG to explore options to develop a long term global crisis response platform. We look forward to the upcoming first World Humanitarian Summit and the Summit on Refugees at the UN General Assembly.

-

IDA remains the most important source of concessional financing for the poorest countries. We advocate for a strong IDA 18 replenishment with the support of traditional and new donors that ensures continued focus on the poorest countries. We look forward to a concrete and ambitious proposal on IDA leveraging options in the context of the replenishment.

-

In 2016, we begin the task of implementing in earnest the challenging program we committed to in the 2030 Development Agenda. In line with their comparative advantage, the IMF, MDBs, UN and WBG should partner to support developing countries’ efforts to meet the SDGs, while adjusting to a slower growth environment and reduced private capital flows. We support collaboration among MDBs on developing high quality financing for sustainable and growth-oriented infrastructure investments. The WBG and IMF should also step up efforts to implement the Addis Ababa Action Agenda on Financing for Development, in particular, crowding in the private sector and boosting domestic resource mobilization, including by tackling illicit financial flows.

-

The private sector is critical to achieve our ambitious development objectives. Inclusive job creation is central to shared prosperity. We encourage all WBG institutions to work together in support of this agenda. In particular, we call on IFC and MIGA to do more to catalyze sustainable economic growth, including by mobilizing funds and providing guarantees in the most challenging environments, and to small and medium enterprises. We also urge IFC, IBRD and IDA to help countries undertake reforms and invest in the quality infrastructure needed to establish business environments that support private investment and local entrepreneurs.

-

Achieving gender equality is central to the 2030 Agenda for Sustainable Development. We welcome the WBG’s recent adoption of the renewed gender strategy and look forward to its effective implementation.

-

The WBG should continue to deliver evidence-based development solutions at the country, regional, and global levels, including through improved country data systems, and South-South cooperation both in low- and middle-income countries. We urge the WBG and IMF to become more effective in fragile and conflict situations, through strengthened operational capacity in affected countries, better-tailored capacity development activities, incentives and enhanced security for staff, and innovative financing and resourcing.

-

We stress the need to strengthen country institutions and health systems, including enhancement of pandemic prevention and preparedness, in close collaboration with the World Health Organization and other stakeholders. We urge the WBG to finish the preparatory work on the Pandemic Emergency Facility as soon as possible and foster a new market for pandemic risk management insurance.

-

We applaud the historic Paris Agreement, which set the stage for ambitious climate action for all stakeholders. The WBG’s recent Climate Change Action Plan sets out its commitment to help operationalize, based on client demand, climate-smart policies and projects as well as to scale up technical and financial support for climate change mitigation and adaptation, consistent with UNFCCC. Small states, the poor and the vulnerable are among the most exposed to the negative impacts of climate change and natural disasters and we urge the WBG and IMF to continue to step up their support to build resilience in these countries.

-

We welcome the Progress Report on Mainstreaming Disaster Risk Management. We call on the WBG to implement actions and policies using the principles of prevention and preparedness and to continue to build capacity for disaster response guided by the Sendai Framework for Disaster Risk Reduction, in particular, in Small Island Developing States. We look forward to an update on the Progress Report in two years.

-

We encourage management and the Board to finalize the modernization of the World Bank’s Environmental and Social Framework by August 2016.

-

We welcome the interim report on the Dynamic Formula and stress the need for the planned further work aiming to reach an agreement by the 2016 Annual Meetings in line with the Shareholding Review principles and the Roadmap agreed in Lima.

-

The next meeting of the Development Committee is scheduled for October 8, 2016.

Related News

Drought, insecurity add to commodity woes – African Ministers

The dramatic decline in commodity prices combined with severe drought conditions and rising insecurity has hit many countries hard, African finance ministers said during the IMF-World Bank Spring Meetings in Washington.

Ministers from four strongly affected countries told a press briefing that weak global demand is taking a toll on growth prospects for the region, forcing significant fiscal adjustments.

Chad has lost over 60 percent of their budget revenue from the slump in oil prices, and the country’s Finance Minister, Mahamat Allamine Bourma Treye, said insecurity in the Lake Chad region caused by Boko Haram and an ISIS offshoot in the north has triggered a massive influx of refugees, putting added pressure on the country’s limited resources.

“This security situation has brought about a new problem, because we are no longer able to trade with neighboring countries. We have major agricultural production which is usually traded with Niger, but now the border is hermetically closed,” Treye said. “Thus far, assistance by the international community is very significant, but nonetheless insufficient given the tremendous challenges Chad faces.”

Climate change having an impact

Swaziland’s Finance Minister, Martin Dlamini, said the effects of climate change have caused macro-critical challenges for the country, noting that the frequency of natural disasters, such as droughts and floods, had intensified in recent years.

“Swaziland, like many other countries in southern Africa region is currently facing severe drought conditions, affecting agriculture – especially subsistence and livestock farming, disrupting water and power supply, fueling inflation and adding to fiscal pressures,” Dlamini said.

Swaziland is facing a 30 percent decline in trade revenues due to the slowdown in neighboring South Africa, also partly caused by the drought.

Burkina Faso’s Finance Minister, Rosine Sori-Coulibaly, said a shorter rainy season has forced them to control the use of water, especially for agriculture.

“We are one of the region’s biggest producers of Cotton, which provides a livelihood to 2-3 million people,” Coulibaly said, noting the country is also feeling the effects of lower cotton prices.

Reaching out for assistance

Somalia’s Finance Minister, Mohamed Aden Ibrahim, said Somalia has abundant natural resources, but the potential for its economic development largely depends on its ability to manage the country’s external debt of more than $5 billion.

“Without addressing that issue we will not have real growth in Somalia,” Ibrahim said. “For that reason, we have engaged with the IMF three years ago, and last July concluded our first country review in 26 years. Also, Somalia concluded an agreement with the Fund only one week ago that we hope will eventually make financial resources available to us.”

Ibrahim told the room of reporters that after decades of conflict, Somalia is working hard to rebuild its economy and institutions.

“I’d like to ask you today to adjust your lenses. Somalia is no longer the Somalia of 10 or 20 years ago. Somalia is moving forward, and it’s a positive story, a story of progress,” Ibrahim said, adding that he is looking forward to a peaceful and smooth presidential election later this year.

African Consultative Group Meeting: Statement by the Chairman of the African Caucus and the Managing Director of the IMF

Mr. Abdoulaye Bio-Tchané, Chairman of the African Caucus, and Ms. Christine Lagarde, Managing Director of the International Monetary Fund (IMF), co-chaired the African Consultative Group meeting on 17 April 2016 at the IMF Headquarters. They issued the following statement after the conclusion of the Group’s meeting in Washington.[1]

“We had very productive discussions on Africa’s economic prospects, highlighting the near-term policy challenges as well as the continued opportunities. Reflecting the more difficult external economic environment and, in particular, the sharp drop in commodity prices, and tighter financial conditions, growth in Africa is projected to decline to about 3 percent in 2016, the lowest level in a long while. However, there is significant variation in growth performance across countries, with low-income countries in sub-Saharan Africa continuing to grow by over 5 ½ percent.”

“We concurred that the decline in commodity prices is likely to be long lasting, as the causes seem structural rather than temporary – including the ongoing rebalancing of demand in China and, in the case of oil, technological innovation that has enhanced supply. We also recognized that non-economic shocks such as weather- and security-related challenges, are posing downside risks to Africa’s economic prospects.”

“Against this backdrop, we agreed that prompt fiscal adjustment is needed to safeguard macroeconomic stability and rebuild policy buffers across the region, especially in oil-exporting countries. We also concurred that, in pursuing these consolidation efforts, country authorities should aim at protecting priority expenditures, such as social expenditures and well-prioritized and efficient infrastructure spending, with a view to ensuring that longer term development goals remain achievable. Furthermore, we agreed that, where feasible, the exchange rate should be allowed to adjust as needed to absorb shocks and improve competitiveness, with central banks’ interventions limited to mitigating disorderly market movements.

“Beyond immediate policy reactions, we agreed on the need to reinvigorate the economic diversification agenda. Stepped-up structural reforms to improve the business environment as well as labor and financial markets and opening to trade are critical for boosting economic prospects, creating jobs, and improving living standards.”

Mr. Abdoulaye Bio-Tchané noted that “it is indispensable for African countries to adapt policies to the new environment and use all tools at their disposal – fiscal, monetary, exchange rate and structural policies to preserve hard-won macroeconomic stability, contain social impact, further strengthen our economies’ resilience to shocks, and support growth. As public investments have helped greatly in preserving positive growth in a very challenging period, it is particularly essential to not slow abruptly the economic dynamism impulse by public and private investment. In this context, African countries look to the Fund not only to continue its effective engagement with Africa, but also to adapt its instruments and financial support to the magnitude of the shocks experienced by African countries. One avenue would be to increase access to the general resources of the Fund for low-income countries. Going forward, as countries seek to achieve the Sustainable Development Goals, we agreed that it will be important for governments to maintain macroeconomic stability, strengthen institutions and the business environment, address critical infrastructure gaps, expand access to financial services in our economies, and seek to ensure that growth is both broad-based and inclusive.”

Ms. Lagarde stated that “as in the past, the IMF will remain closely engaged with its African members. Appropriate policies will be key to weathering this difficult time and to maintaining a strong foundation for sustainable growth and poverty reduction. The Fund’s support can take several forms, depending on countries’ needs: policy advice, technical assistance and capacity development, and – where appropriate and needed – financial assistance. The IMF will continue to strengthen the analytical underpinnings of its policy advice and instruments and seek to adapt to meet the evolving needs of the membership”.

[1] The African Consultative Group comprises the Fund Governors of a subset of 15 African countries belonging to the African Caucus (African finance ministers and central bank governors) and Fund management. It was formed in 2007 to enhance the IMF’s policy dialogue with the African Caucus. The Group meets at the time of the Spring Meetings, while Fund Management meets with the full membership of the African Caucus at the time of the Annual Meetings.

Related News

Spending more and better: Essential to tackling the infrastructure gap

Countries will need to spend resources better – by improving efficiency and building capacities – in order to support high-quality infrastructure projects that can achieve significant development results to meet the Sustainable Development Goals.

Increasing coordination among development institutions to support planning and development of infrastructure projects is one of the objectives of the Global Infrastructure Forum 2016. In its inaugural gathering, on Saturday, in partnership with the United Nations (UN), the Forum brought together, for the first time, the leaders of the multilateral development banks (MDBs) – African Development Bank, Asian Development Bank, Asian Infrastructure Investment Bank, European Bank for Reconstruction and Development, European Investment Bank, Inter-American Development Bank Group, Islamic Development Bank, New Development Bank, and the World Bank Group – as well as development partners and representatives of the G20, G24, and G77, to enhance multilateral collaborative mechanisms to improve infrastructure delivery globally. The Forum is organized in close partnership with the United Nations.

“We can get the most of every dollar of infrastructure capital by helping countries improve governance, local planning, preparation, and administration capacity,” said World Bank Group President Jim Yong Kim, during the opening plenary. More efficient spending should also encourage more investment from the private sector – which is seen as a key source of financing for infrastructure projects.

Addressing the world’s infrastructure challenges is critical to achieving the goals of ending extreme poverty by 2030 and ensuring prosperity for all. At least 660 million people lack access to safe drinking water while 1.2 billion people live without electricity. More than one-third of the world’s rural population is not served by an all-weather road.

“If we are to achieve our goals and leave no one behind, we must address large infrastructure gaps in developing countries,” said UN Secretary General Ban Ki-Moon, also at the opening of the event. “The forum will allow for a great range of voices to be heard. Developing countries, especially the most vulnerable, need international support to bridge their infrastructure gaps.”

Countries and development partners are expected to use the forum to jointly build on existing multilateral collaboration mechanisms and coordinate efforts with multilateral and national development banks, UN agencies, and the private sector.

The space should also help partners identify and address infrastructure and capacity gaps, as well as highlight opportunities for investment and cooperation – while ensuring investments are environmentally, socially and economically sustainable.

Unprecedented collaboration among development partners to improve infrastructure implementation

Mandated by the Addis Ababa Action Agenda on financing for development to help bridge the infrastructure gap, which is key to achieving the Sustainable Development Goals (SDGs), the Forum aims to improve alignment and coordination among the partners, while respecting the diversity of approaches, policies, and procedures among them, to facilitate the development of sustainable, accessible, and resilient infrastructure for developing countries. The Forum will be held annually, with responsibility for hosting rotating among the MDBs.

Infrastructure plays a critical role in growth, competitiveness, job creation, and poverty alleviation. Yet increasing access to basic infrastructure services remains a critical challenge in developing countries. At least 663 million people lack access to safe drinking water. By 2025, 1.8 billion people will live in areas with absolute water scarcity. Sixty percent of the world’s population lacks internet access, while 1.2 billion people in the world still live without electricity. At least one-third of the world’s rural people are not served by an all-weather road. Addressing the infrastructure gap requires a boost in investment including better leveraging of private investment, but also better governance, capacities, and improving efficiency to get more from existing spending on infrastructure.

MDBs have a strong track record of collaboration in the direct financing of projects and mobilizing private capital, as well as improving capacities and knowledge around infrastructure. Some examples include the Global Infrastructure Facility, the International Infrastructure Support System, the PPP Knowledge Lab, the PPP Days conference, Infrascope, and the PPP Certification program.

The Chairman’s Statement highlights the idea that to achieve the objectives of the Forum, the MDBs and development partners resolve to work together on strengthening project preparation, promoting financing, building on shared principles and promoting compatible and efficient approaches, and improving data and information. A session to review progress will take place during the Global Infrastructure Forum 2017.

Chairman’s Statement

Global Infrastructure Forum, April 16, 2016

Mandated by the Addis Ababa Action Agenda (para 14), as an outcome of the Third International Conference on Financing for Development, the Global Infrastructure Forum is being established by the MDBs to help bridge the infrastructure gap, as key for achieving the Sustainable Development Goals (SDGs). This will provide a forum for countries and development partners to work together by building on existing multilateral collaboration mechanisms, and to “improve alignment and coordination among established and new infrastructure initiatives, multilateral and national development banks, UN agencies, national institutions, development partners, and the private sector.” (AAAA Para 14) It will encourage a greater range of voices to be heard, particularly from developing countries, and identify and address infrastructure and capacity gaps in particular in LDCs, LLDCs, SIDS, sub-national entities in MICs, and African countries. It will highlight opportunities for investment and cooperation, and work to ensure that investments are environmentally, socially, and economically sustainable, climate-smart and climate-resilient, and in line with partner countries’ national commitments under the United Nations Framework Convention on Climate Change.

The Forum will also support the infrastructure-related agendas of the G20, G-24, G-77 and g7+ by encouraging MDBs to take joint actions to demonstrate their commitment to infrastructure investment.

We, as MDBs and development partners, by nature of our roles and our convening power to partner with both the public and private sectors, and our ability to deploy a suite of knowledge, advice, financing, and commercial and non-commercial risk mitigation, are committed to working with countries and investors to support the provision of greater access to, and better quality of, affordable infrastructure services which are environmentally, socially, and economically sustainable. We will do this through a two-pronged approach.

i) We will continue to support country-led approaches to planning, executing, supervising, and evaluating sustainable, resilient, inclusive, and well-prioritized infrastructure programs and robust infrastructure frameworks. In addition, we will continue to support the involvement of all stakeholders in planning, financing through domestic resource mobilization as well as national/international financing, and operating infrastructure services, including governments, consumers, the private sector and civil society; and

ii) We will consolidate and scale up where possible existing multilateral mechanisms to promote greater knowledge transfer, project preparation, and implementation support in the form of global and regional platforms and tools, including de-risking and risk allocation mechanisms, that have already been developed in close cooperation by MDBs, such as the Global Infrastructure Facility, the Global Infrastructure Hub, the International Infrastructure Support System, the PPP Knowledge Lab, Infrascope, the PPP Certification program, and environmental, social and governance standards.

To achieve the objectives of the Forum, we resolve the following.

Improving data and information on infrastructure

MDBs and development partners will endeavor to help client countries to achieve:

-

better planning and prioritization of infrastructure, including improved provision of data, unit costs, and information on infrastructure, where feasible;

-

more informed decisions by the public and private sectors around investment, which in the case of the public sector may imply access to support from good advisors;

-

improved accountability in asset maintenance and service delivery;

-

greater levels of disclosure and transparency; and

-

a greater voice for users and the public at large.

To help achieve this, the MDBs and development partners agree to work together with client countries to improve data acquisition and develop systematic reporting where possible, on:

-

MDB lending and advisory support to infrastructure, as well as metrics on catalyzation of private investment;

-

infrastructure spending and investment (both actual and required), asset quality, service standards, and fostering disclosure and transparency;

-

assessments that promote a sound enabling environment to attract increased investment for infrastructure; and

-

private participation in the delivery of infrastructure services and the mobilization of long-term finance from investors, both domestic and international.

Promoting compatible, efficient approaches

While recognizing differing institutional characteristics, country objectives, needs, legal/regulatory frameworks, including those related to the SDGs and UNFCCC Paris Agreement, and the diversity of priorities and strategies of the mandates of the MDBs, the latter and development partners can reduce transaction costs of building and implementing sustainable infrastructure by continuing the promotion of efficient approaches to key bottlenecks or constraints, by:

-

Promoting capacity development by policy support, and via project preparation and advisory facilities, technical assistance, and capacity building support.

-

Supporting the planning and development of infrastructure in the context of Nationally Determined Contributions to the UNFCCC.

-

Supporting, when appropriate, early stage project preparation through the International Infrastructure Support System.

-

Further developing risk management principles and mechanisms for:

-

approaches to risk allocations in different sectors and markets and associated contractual clauses; and

-

planning investment under uncertainty, to build more resilient assets, notably taking into account climate change and disaster risks.

-

-

Further developing tools for assessing:

-

fiscal implications of public investment versus public-private partnerships (PPPs);

-

risks of implementation of projects as PPPs or as a public option; and

-

approaches for improving transparency on infrastructure contracts and projects.

-

-

Strengthening the capacity of economic regulators to ensure that efficiency gains obtained throughout the lifecycle of infrastructure projects are shared fairly between service providers and users.

-

Continuing our work on developing environmental, social, and governance standards, including through the work of the Multilateral Financial Institutions working group on environmental and social standards (MFI-WGESS).

-

Continuing our coordination on climate finance methods, tools, and approaches for jointly improving the effectiveness of these resources, including for mobilizing new sources of capital for investment in low carbon and climate resilient infrastructure services.

Strengthening project preparation

MDBs and development partners agree on the need to develop sustainable infrastructure project pipelines regardless of whether they are funded publicly, privately, or in combination. MDBs and development partners will continue to support existing and planned project preparation facilities and related databases to support countries to prioritize and prepare bankable pipelines of infrastructure projects (including regional and cross-border projects), to better negotiate complex legal contracts, and to better manage projects.

Promoting financing for infrastructure

The MDBs and development partners will explore taking specific actions to:

-

Achieve higher levels of private sector participation (PSP) in infrastructure, to leverage improved results regarding reduced time from construction to operation, asset management over the long-term, and overall management delivery;

-

Promote cooperation between new and existing MDBs, with a particular focus on opening up co-financing opportunities on mutually beneficial terms;

-

Pursue new innovative approaches to collaboration, including with providers of concessional sources of climate finance, donors, private foundations, and institutional investors;

-

Foster the secondary market for infrastructure equity and debt, with MDBs supporting the development of secondary markets for equity and debt, to allow project developers to recycle their scarce capital in the secondary market into new PPPs coming to tender, and to create long term assets with a risk profile that is more attractive to institutional investors;

-

Identify opportunities to support viability gap funding arrangements to help PPP projects meet bankability and affordability criteria;

-

Further increase MDBs’ financial capacity through the use of risk sharing instruments such as political risk insurance and reinsurance, partial risk and credit guarantees, issuance of green bonds, and other such instruments to crowd in other investors;

-

Develop new tools to leverage MDB balance sheets and bring in new private sector capital, including from the insurance market and institutional investors; and

-

Further strengthen domestic financial systems in client countries to support sustainable infrastructure financing.

Future meetings of the Global Infrastructure Forum and Reporting

We expect that the Global Infrastructure Forum will be held annually, to review progress. The responsibility for hosting the Forum will rotate among the MDBs. Preparations for the Forum will continue to be carried out in an inclusive manner, in cooperation with the UN system through UN-DESA. The outcomes of the Global Infrastructure Forum will be reported to UN Member States via the Financing for Development Forum.

Related News

Making trade work for Least Developed Countries: A handbook on mainstreaming trade

Least developed countries (LDCs) have very high trade-to-GDP ratios, reflecting the fact that they are heavily dependent on trade. Over the past few decades, they have also embarked upon significant trade reforms. Although LDCs had relatively high economic growth during the past decade, unemployment, poverty, and inequality continue to be major development challenges in these countries.

LDCs account for about 12 per cent of world population but less than 2 per cent of world trade, indicating that they have not fully reaped the potential benefits of trade for development. A key reason for this is that these countries have low productive capacity and have not effectively integrated trade into their national development strategies and plans.

Against this backdrop, the United Nations Conference on Trade and Development (UNCTAD) developed a project to strengthen the capacity of trade and planning ministries of selected LDCs to develop and implement trade strategies conducive to poverty reduction. The project was funded by the UN Development Account for the period 2013–2015 and had six LDCs as beneficiaries: Ethiopia, Lesotho, and Senegal in Africa, and Bhutan, Kiribati, and Lao PDR in Asia and the Pacific. As part of the project, national workshops on the trade policymaking and trade mainstreaming experiences of the beneficiary countries were organized by UNCTAD in collaboration with the governments involved and partner organizations. Two regional workshops were also organized: one on Africa and one on Asia and the Pacific.

This handbook is the outcome of the workshops and research conducted under the project. It draws lessons from the experiences of the six countries that participated and provides fresh insights on how to design and implement an effective trade strategy in LDCs. It also provides clarity on the concept of mainstreaming trade and identifies criteria on how to measure success in this endeavour. The handbook should be useful to policymakers in developing countries, development analysts, academics, and students of development. In this regard, it is meant to be a guide to policy formulation and implementation in LDCs, with the understanding that its application will vary from country to country because of differences in economic structure, history, and social and political realities.

Development opportunities and challenges in LDCs in the new global environment

The global economic environment has changed significantly over the past few decades: real output in many least developed countries (LDCs) is growing faster than the rate of population growth; there is increasing trade in tasks and the location of production is shifting; technological innovation and progress have enhanced access to information and communication technologies in developing countries and reduced trade and transaction costs; there is greater international focus on the development needs and challenges of LDCs; and emerging economies – such as Brazil, Russia, India, China and South Africa – are beginning to play more active roles in global trade, finance, and governance than in the past.

These developments present both opportunities and challenges for LDCs in their quest for sustained growth and poverty reduction. For instance, the integration of economic activities into global production networks and global value chains (GVC) presents an opportunity for LDCs to participate in global production networks for manufacturing, where they often do not have a competitive or comparative advantage in the production of entire products, by permitting them to specialize in the production of specific tasks along the value chain for a product. But GVCs also present challenges for LDCs in the sense that they may be stuck in lower-value segments of the chain and hence not derive significant benefits from the globalization process. Similarly, the increasing role of emerging economies in global trade and finance also presents opportunities and challenges for LDCs. It has diversified export markets for LDCs and also increased the sources of development finance available to them, thereby relaxing their development financing constraints. But it has also exposed them to international competition, particularly in export markets for labour-intensive manufactures. These trade-offs underscore the fact that if LDCs are to effectively integrate into the global economy and achieve their development objectives, they and the international community will have to put in place policy measures to maximize the benefits and minimize the risks associated with the changing global economic environment.

The 2030 Agenda for Sustainable Development adopted by the international community in September 2015 is now the framework and vision guiding formulation and implementation of development policies over the next 15 years. The Sustainable Development Goals (SDGs) are more ambitious than the Millennium Development Goals (MDGs), and reflect lessons learned in the implementation of the MDGs.

One of those lessons is that an ambitious development agenda requires credible and ambitious means of implementation to enhance the likelihood of success. Trade is one of the means of implementation identified for financing the SDGs. Its vital role in the development process of LDCs has also been underscored in the Istanbul Programme of Action (IPoA) for the period 2011-2020 (Box 1). Despite this recognition of the potential role of trade in the development process, LDCs have not been able to use trade effectively in support of their development efforts, as evidenced by their very low shares of global trade, high poverty rates, and the fact that they export mostly primary commodities rather than dynamic and rapidly growing products in global trade. UNCTAD research has shown that one of the reasons for the inability of LDCs to fully harness the potential of trade for sustained growth and poverty reduction is that they have not fully and effectively integrated trade into their national development strategies. In this context, if trade is to play a positive and crucial role in the implementation of the SDGs in LDCs, efforts have to be strengthened to fully and effectively integrate trade into the national development strategies and plans of those countries.

Against this backdrop, this policy handbook provides guidelines on how LDCs could effectively integrate trade into their development strategies and plans to achieve better development outcomes from trade than has been the case to date. More specifically, the aims of the handbook are to:

-

Provide an operational and results-based definition of the concept of mainstreaming trade with a view to identifying criteria for measuring success;

-

Discuss various instruments and approaches to mainstream trade into national development strategies;

-

Examine the experiences of selected LDCs in Africa and Asia in mainstreaming trade into their development strategies and draw lessons from these varied experiences for other LDCs; and

-

Provide a framework for the design and implementation of an effective trade strategy in LDCs in the new global economic environment.

The handbook is expected to serve as a guide to LDC policymakers in the design and formulation of trade policies and their integration into national development strategies and plans. History has taught us that what works in one country may not work in another due to different political realities and institutional settings. In this regard, the handbook should not be seen as a blueprint but rather as a guide on how to mainstream trade effectively.

Box 1. The Istanbul Programme of Action for LDCs

The basic international framework that has been agreed upon to guide national development policies in LDCs and related assistance by the development community is the 2011 Istanbul Programme of Action (IPoA). The framework aims to overcome the structural challenges LDCs confront to eradicate poverty, achieve internationally agreedupon development goals, and exit from the LDC category. The IPoA lays out a vision and strategy for the sustainable development of LDCs during the 2011-2020 period with a strong focus on developing their productive capacity and the specific goal of enabling half of the LDCs to meet the criteria for graduation.

The IPoA stresses the importance of a number of key principles, including ownership, a balanced role of the state and market in the development process, genuine partnership and solidarity. It also emphasizes a results-based orientation, an integrated approach to peace and security, development and human rights, equity at all levels, and the effective participation, voice, and representation of LDCs.

Key objectives of the IPoA include strengthening productive capacity in LDCs, reducing their vulnerability to economic, natural, and environmental shocks, ensuring enhanced financial resources, and improving the quality of governance. A number of trade-related areas were identified as priorities, including productive capacity, agriculture, food security and rural development, trade, commodities, mobilizing financial resources for development and capacity-building, and good governance at all levels. Specific goals are to double the share of LDCs’ exports in global exports by 2020, commit to ensuring timely and sustainable implementation of duty-free, quota-free market access for all LDCs, and enhance the share of assistance to LDCs by the development partners for Aid for Trade.

The IPoA also puts strong emphasis on technological innovation and technology transfer to LDCs, and on ensuring mutual accountability of LDCs and their development partners for delivering on their commitments. The programme calls for the mainstreaming of its provisions into national policies and development frameworks, as well as regular reviews at the country level with the full involvement of all stakeholders. Likewise, development partners are urged to integrate the IPoA into their cooperation frameworks and monitor the delivery of their commitments.

Related News

As Uganda chooses Tanzania pipeline route, Kenya to go it alone

Uganda will take its oil to the market through Tanzania’s Tanga port, leaving Kenya to build its own pipeline to Lamu, if the positions taken at the just-ended talks in Kampala are maintained.

“We have lost the pipeline deal to Tanzania. The only deal is to go back to the drawing board to construct our own pipeline to Lamu port,” a senior Kenyan official told The EastAfrican on Friday.

The outcome of the talks was closely guarded, with the technocrats meeting in Kampala insisting that the final position would be announced during the Northern Corridor Heads of State Summit next week.

The EastAfrican, however, learned that Uganda may have already sealed a deal with Tanzania to take the Tanga route and to let oil firm Total E&P of France fund and operate the pipeline.

Last week in Kampala, Uganda held two separate meetings with Kenya and Tanzania; each consultation came up with a report. It had been agreed that the technical teams would compile the two reports and hand over a joint report to the heads of State.

However, the Ugandan team is said to have been reluctant to share the report of its consultations with Tanzania.

“Uganda is playing hardball and has refused to share the report from its discussions with Tanzania. This then leaves us nowhere,” said one of the Kenyans close to the discussions.

However, it has also emerged that the Kenyan officials participating in the Kampala talks may not have had all their facts right as they tried to address the concerns raised by Uganda over the northern route for the pipeline.

For example, Uganda had raised concerns over the location of the pipeline terminal at Lamu port – a spot that they feared was prone to Monsoon winds – as well as the financing for the pipeline.

Another source at the meeting told The EastAfrican that, although Kenya had indicated that the site at Lamu had been moved to the main port, this was not the position when teams from Uganda and Kenya toured the area recently.

“On financing, Kenya was not clear on how to finance the pipeline even though it indicated that many organisations were willing to provide funds. Uganda felt this could take long and result in delays in the export of the oil,” he said.

Meanwhile, Total reaffirmed its commitment to construct the $4 billion crude oil pipeline to Tanga.

Total is eyeing production of an estimated 6.5 billion barrels of Uganda’s crude oil by 2018.

The French oil company is UK Tullow Oil’s partner in the Ugandan oil fields and the main financier of the operations. China National Offshore Oil Companies is also a partner.

Kenya’s apparent resignation and decision to go it alone is in line with President Uhuru Kenyatta’s recent remarks that the Lamu Port – Southern Sudan – Ethiopia Transport (Lapsset) Corridor must and would proceed, even without Uganda.

“The Lapsset project will move forward whether or not Uganda opts to have its oil pass through Kenya’s Northern Corridor,” said President Kenyatta.

Heads of State summit

The Kenyan president and his Ugandan and Rwandan counterparts, Presidents Yoweri Museveni and Paul Kagame, are expected to meet on April 22 for the Northern Corridor Infrastructure Summit where the pipeline will be a key agenda item.

“Tanzania will also attend the Summit for the pipeline discussions,” said Andrew Kamau, Kenya’s principal secretary, department of petroleum, at Ministry of Energy and Petroleum.

“We expect that a harmonised report compiled by Uganda from the two meetings will be tabled for the presidents to make a decision,” Mr Kamau had earlier told The EastAfrican, adding that the outcome of the report and decision by the presidents on the pipeline would determine the next step Kenya would take on the issue.

Total has also promised to finance Uganda’s contribution of 40 per cent to the construction of the refinery in Hoima, which stands at $3.8 billion.

“Uganda is struggling to raise the funds. Total has warned Uganda that the northern route, which is 1,120km, will encounter rough land terrain because of the Rift Valley in Kenya, driving the cost of the pipeline higher and delaying it. Tanzania is flat, given the Lake Victoria Basin,” said the source.

“Total also warns that the port of Lamu has not been built and the entire Lapsset project is behind schedule. It is practically impossible for Kenya to complete construction of the port by 2018. The port of Tanga has already been built.”

Tullow’s group head of communications George Cazenove said the decision around a regional pipeline was a government-to-government issue and his company would work with whichever route the East African countries choose.

Prior to the Kampala meetings, Kenya and Ugandan officials had conducted tours to Lamu, Mombasa and Tanga ports.

According to Mr Kamau, it was established that although all the ports are sheltered, Tanga was shallow and would require extensive work of dredging, which would increase the project cost and delay potential oil export.

In addition, a load-out facility will be required at least 2.3km offshore, which is complex and expensive to build.

This is unlike the Lamu port that would require a dredge channel that is less than 300m, has pre-allocated land in Lamu industrial area for marine storage, and the port is designed to handle construction material and large maritime cargo.

The 1544km Hoima to Tanga route being favoured by Total of France will cost $5.5 billion, while a joint one with Kenya through the southern route will cost $4.4 billion: The Tullow Oil of the UK preferred northern route will cost $4.2 billion.

Kenya’s loss

Over about 25 years of standalone pipeline, Kenya is projected to lose $3.32 billion, and Uganda the $3.32 billion in revenue collection for not constructing the joint pipeline.

A joint pipeline between Kenya and Uganda would have had an initial throughput of 300,000 barrels per day (200,000 barrels for Uganda and 100,000 barrels for Kenya). This could have earned the pipeline companies $1.66 billion a year, which would be shared between the countries according to throughput.

“A regional pipeline offers greatest synergy and lowest tariff for both Kenya and Uganda,” said Mr Kamau.

If the two countries go for a standalone pipeline, Uganda will lose $300 million every year due to an increase of $4.07 in tariff per barrel, and Kenya will lose $250 million per year due to the increased tariff of $6.96 per barrel.

Kenya and Uganda had until late last year agreed to construct a pipeline from Hoima to Lokichar and to Lamu. But fears of insecurity in the region bordering Somalia and huge compensation costs for privately owned land, saw Uganda explore the option of the southern route through Tanzania to Tanga.

Related News