Search News Results

Public roads with private money: A way ahead

When you drive over potholes on downtown streets, are forced to make large detours to cross rivers lacking bridges, and finally arrive to find no cell coverage, connections between the global infrastructure investment gap and your pension fund might not be the immediate thing that comes to mind.

But it should, because:

-

Huge pools of available assets: pension funds, insurance companies, mutual funds and sovereign wealth funds sit on $100 trillion in assets. To compare: U.S. nominal GDP in the third quarter of last year was $18 trillion.

-

Huge infrastructure investment gap: between $1 to 1.5 trillion per year worldwide.

By putting to work a small portion of the privately owned $100 trillion for global infrastructure development, the positive impact on the global economy could be bigger than any other source of large-scale private investments.

In a new paper, From Global Savings Glut to Financing Infrastructure: The Advent of Investment Platforms, several economists at the IMF, in academia, and business explored the problem of how to lure badly needed private investment into meaningful infrastructure projects on a global scale.

To enhance the cooperation between public and private partners, there is a new class of facilitators like the European Investment Bank or the Asia Infrastructure Investment Bank. But how can they avoid engaging private investment in inefficient infrastructure projects, bridges to nowhere, or avoid granting too generous concession terms, like high highway tolls?

The paper makes a number of suggestions, including the creation of infrastructure securities and a global infrastructure investment platform.

Introduction

The policy debate on global infrastructure financing has reached unprecedented levels. Media coverage is dominated by discussions about the fallout from the creation of the Asian Infrastructure Investment Bank (AIIB), initiated and led by China. Controversy and debates have become heightened on account of many European and Asian countries having formally announced their commitment to join the infrastructure bank, while the US has opted to stay out and actively lobbied to discourage several countries from becoming members of the AIIB. Other so-called “infrastructure investment platforms” have been set up by development banks, though they have received considerably less international attention. The principal objective of these specialized investment platforms is to tap into the pool of both public and private long-term savings in order to channel large pools of capital into infrastructure investments. The goal of the present paper is to provide a detailed overview of these new initiatives, and to critically analyze the building blocks of the emerging global landscape for public-private co-investments in infrastructure.

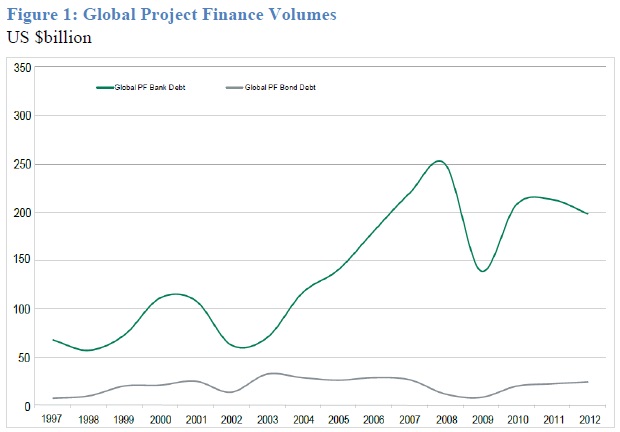

Apart from the major state-sponsored efforts in infrastructure development in China and a few other Asian countries, infrastructure development in most parts of the world has been seriously lagging over the past three decades. The initial hopes that the privatization wave of the 1980s would fuel a private-sector funded greenfield infrastructure investment boom have have fallen well short of expectations. The motivations for privatization were: i) governance; ii) incentives, and iii) budget constraints. The experience with public sector infrastructure up to the 1980s in low-income countries and advanced economies was one of large cost overruns, poor maintenance, corruption, and little positive externalities. In other words, many infrastructure projects have turned out to be white elephants. Early evidence of privatization was encouraging as it resulted in greater efficiency, better maintenance and new sources of funding, with the development of public private partnerships (PPPs). However, the most recent evidence clearly points to a relative slowdown in infrastructure development in many parts of the world (see Figure 1).

There is new hope for infrastructure development given the size of the asset under managements of long-term investors including traditional institutional investors and sovereign wealth funds in Asia and the Middle East, who are searching for longer term assets as savings vehicles. Long-term investors are relatively much better placed investing in longer term global infrastructure assets, where they are likely to face less competition, and where remarkably there is also a huge demand for funding. At a time when the world recovery from the financial crisis is still timid and public debt levels remain elevated, the provision of financing to help replace aging infrastructure in advanced economies and build brand new ones in emerging markets could contribute to reignite their economic engines.

While there are opportunities, there are also important bottlenecks including on financing and origination of infrastructure projects. Recent attempts to remove or circumvent these bottlenecks point to the need to take stock of those initiatives including investment platforms and to go further and critically discuss what the emerging landscape of private-public coinvestment in infrastructure will be. This paper aims to shed light into what that new model could be.

Related News

FAO Food Price Index steady in February, palm oil rises

First global 2016 wheat production forecast sees a modest drop from last year’s record level

The FAO Food Price Index was stable in February, as falling sugar and dairy prices offset a substantial jump in vegetable oil prices from the previous month.

Averaging 150.2 points for the month, the FAO Food Price Index was virtually unchanged from a revised 150.0 points in January and down 14.5 percent from a year ago.

FAO also issued its first forecast for the world’s 2016 wheat harvest, projecting 723 million tonnes of total production, about 10 million tonnes below last year’s record output.

The FAO Food Price Index is a trade-weighted index tracking international market prices for five key commodity groups: major cereals, vegetable oils, dairy, meat and sugar.

Diverging from February’s generally stable trend was a sharp increase in the FAO Vegetable Oil Price Index, which rose 8.0 percent from the previous month. That was led by a 13 percent surge in palm oil, which gained on reports of falling inventories and a poor production outlook in the near future. Soy oil prices also firmed as a result.

But other staple commodities more than absorbed that rise. The FAO Sugar Price Index declined 6.2 percent from January, buoyed by strong global inventories and improved crop conditions in Brazil, the world’s largest producer and exporter.

The FAO Dairy Price Index fell 2.1 percent on the month amid sluggish imports, especially by China.

Prices of the world’s staple grains were broadly stable. The FAO Cereal Price Index inched down only around half a percentage point from the previous month but was 13.7 percent lower than a year earlier. Wheat prices fell 1.5 percent, maize prices slipped only slightly, while rice prices rose modestly.

Meanwhile, the FAO Meat Price Index rose slightly, buoyed by supply constraints for beef from Australia and the U.S. as well as support for private storage of pig meat in the European Union. Poultry prices fell, reflecting lower feed costs.

Strong 2016 wheat harvests seen in China and South Asia

FAO’s latest Cereal Supply and Demand Brief forecasts a 1.4 percent drop in worldwide wheat output in 2016, due mainly to dry weather leading to reduced winter plantings in the Russian Federation and Ukraine. However, China and Pakistan are expected to sustain near-record wheat harvests, and India’s output is anticipated to recover.

FAO also trimmed its estimate of last year’s total cereal production to 2 525 million tonnes, reflecting updated wheat production estimates from India and revised output figure from the Islamic Republic of Iran.

Estimates were also lowered for last year’s world output of coarse grains and rice due to developments in Asia. Combined world cereal production in 2015 is now seen at around 1.4 percent below the record level reached in 2014.

Global cereal stocks are likely to amount to 636 million tonnes by the close of seasons ending in 2016, nearly unchanged from their already high opening levels, but down 6.2 million tonnes from the previous month’s forecast. The revision mostly reflects reduced wheat inventory forecasts for the Islamic Republic of Iran and Uzbekistan, largely resulting from adjustments to historical stock numbers of both countries.

The world cereal stock-to-use ratio, a leading indicator of global world food security, still stands at a relatively high level of 24.7 percent.

FAO now expects world trade in cereals to decline by 2.0 percent in volume terms in 2015/16 from the previous season. That mostly reflects shrinking demand for wheat and barley, more than offsetting firmer demand for rice.

Related News

Mapping global and regional value chains in SACU: Sector-level overviews

Global Value Chains and Regional Integration in SACU

Global value chains and the link to regional integration

In considering the prospects for expanding non-commodities exports, the SACU region faces a global environment that has changed markedly over the past two decades. First, trade is increasingly shifting away from high income countries and toward developing countries. Second, and perhaps most importantly, is the increasing importance of or “global production networks” or “global value chains” (GVCs). With wages rising rapidly in China and other places where GVC-oriented trade is concentrated, parts of these value chains are migrating to new global locations. Some estimates indicate that over the next generation 85 million manufacturing jobs will migrate from coastal China, and Sub-Saharan Africa is expected to be a major beneficiary. The SACU region – with its abundance of natural capital and surplus labor, along with a relatively high quality infrastructure and institutional environment – should be in a good position to attract investment and create a “Factory Southern Africa”.

Beyond assembly manufacturing that is typical of GVCs (e.g. apparel, electronics, automotive), the region should also be well-placed to compete as a location for valueaddition to agricultural and mineral commodities (“beneficiation”). Both types of investment would not only drive exports and have the potential to create significant employment, but also support upgrading by accessing global technologies and knowledge. And with growing markets across Africa, a “Factory Southern Africa” might increasingly be sustainable in the regional context.

Competing in GVCs will require scale economies that are limited in the region, and non-existent outside of South Africa. For this reason, South Africa will play a critical role as a demand engine and gateway, but it will rely on the rest of the region in order to benefit from differing sources of comparative advantage across the countries. Indeed, regional integration in the context of global value chains is likely to be the key to successful export-orientated growth in SACU. International evidence suggests that regional integration can be a driving force for growth and income convergence. In Europe, for example, the single market has facilitated private capital flows from richer to poorer countries and from low to high growth economies, resulting in faster convergence in incomes and living standards than anywhere in the world. In East Asia similarly, greater integration has led to the development of advanced regional production networks that have underpinned its spectacular growth from a poor, underdeveloped agricultural backwater to becoming the global factory today. At the heart of this integration is the linkage between trade in goods; investment in regional supply chains, technology and business relationships; and the use of efficient infrastructure services (telecom, internet, transport) to coordinate dispersed production.

The current state of global and intra-regional trade in SACU

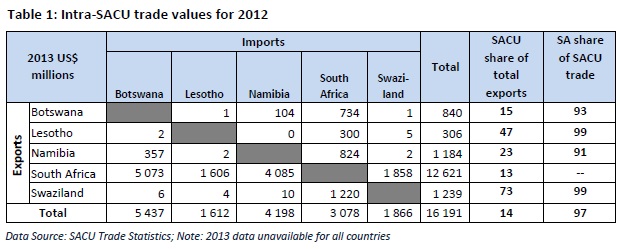

From an export perspective the region can be characterized as having two types of countries. First, Botswana, Namibia, and (to a lesser extent) South Africa rely heavily on the mining sector and the exports of raw materials, with most exports going outside the region. Second, Swaziland and Lesotho have narrow but well-developed industries that drive most export earnings: in the case of Swaziland it is sugar and (related) concentrated beverage syrups; in Lesotho it is apparels and textile. While these countries also export globally, they have a much greater reliance on regional markets. Taking exports and imports together, SACU’s value of trade within its borders equals approximately 14% of its total trade with the world, which is higher than the estimated percentage the African continent trades with itself (10% of total world trade). What is most pronounced about this regional trading landscape is the dominance of South Africa (Table 1). South Africa accounts for 97 percent of all trade in the region (which slightly ahead South Africa’s share of regional GDP) and runs a very large trade surplus with the region. The remainder of countries run extremely large intra-regional trade deficits, principally driven by bilateral imbalances with South Africa. Outside of South Africa, only Namibia and Botswana have developed bi-lateral trade of any significance, while Swaziland and Lesotho hardly feature in any regional trade outside of South Africa.

The second main point about regional trade is its product and sector nature. Here, we see that trade within SACU differs substantially in terms of sectors and products versus what member countries trade outside the region. This is unsurprising, particularly for those countries that are primarily mining and other commodity exporters. Intra-SACU is dominated by food and manufactures, with relatively small volumes of commodity trade. But while food trade is significant in agricultural raw materials appears to be relatively limited, suggesting that regional agrofood value chains may not be well developed. And while most countries export mainly manufactured goods in the region, Namibia, notably, is concentrated in food exports with very limited manufacturing exports.

Looking in more detail at the products that are traded within the region, although trade is fairly diverse, the nature of products exports from South Africa to the region differs significant from those exported from the rest of SACU to South Africa. Specifically, outside of mineral fuels (which is the largest export sector), South Africa’s exports are dominated by vehicles and machinery and equipment, along with iron and steel. The trade appears to be chiefly ‘endproduct’ sales. For example, a review of the trade data on for motor vehicles (HS 87) shows around 82 percent of trade is concentrated in end-products, with 18 percent (worth around US$ 220 million) in parts and components. The exports from the rest of SACU into South Africa is more eclectic, with soaps and detergents being the single largest category, and cocoa products, iron and steel, and plastics featuring prominently. There is some evidence of higher parts and components exports coming from SACU countries into South Africa, although this still appear to be relatively small.

The integration gap and regional industrial policy

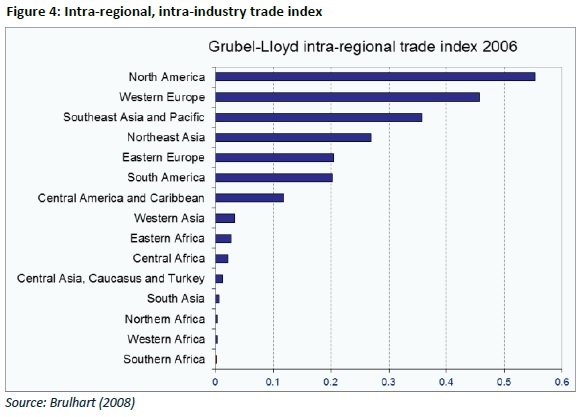

The brief overview of trade statistics outlined above gives an initial indication that integrated regional supply chains are not yet prominent in SACU. While it may be the case that some individual supply chains have developed across the regions, certainly there is no broader ‘Factory Southern Africa’. This is also true if one extends the geographical scope to encompass the wider Southern Africa (SADC) region. Indeed, Figure 4, which calculates intra-industry trade (parts and components within the same industry) within regions, shows that production chains in Southern Africa are among the least integrated in the world. This stands in stark contrast to the tightly integrated regional production networks that exist in East Asia, as well as in North America and Western Europe. This is partly explained by the emphasis on commodity exports in the region and the relatively limited complementarity of existing production structures. But even in this context, the level of regional integration of value chains is remarkably low in Southern Africa. Certainly, participating in GVCs would necessitate greater movement of parts, components, and services activities across regional borders. This underscores the importance of deeper and more effective integration arrangements that would enable value chains to operate seamlessly across the region, minimizing transaction costs and lead times. Moving even some way toward the level of integration in other parts of the world will, therefore, require significant improvements in the regional environment for cross-border trade and investment.

In this context, SACU has started work on developing a common industrial policy, which is fundamental to achieving the objectives of deeper regional integration as contained in the 2002 SACU Agreement. A SACU Task Team has been formed to oversee the development of the industrial policy framework. Central to the regional industrial policy is the development of integrated regional value chains (RVCs) that exploit of the comparative advantage of member states, and therefore not only support regional integration but more importantly productivity and competitiveness. Such RVCs may operate fully within SACU, but in most cases they are likely to be linked – upstream, downstream or both – into wider regional (African) and global value chains. It is therefore imperative that the RVCs being considered within the context of the SACU Industrial Policy function well to allow effortless integration into global value chains. And this is a two-way relationship. A recent paper by the Asian Development Bank suggests that regional economic integration within a GVC environment – through logistics, information network and connectivity improvement – can deliver substantial benefits from scale, network, coordination and agglomeration economies, with particularly strong benefits for small economies.

Objectives and Approach

While across the region there is significant interest integration of RVCs and, more broadly, integrating into GVCs, there remains limited evidence of the extent of current integration. The textile and apparel sector has been documented most. To date, however, limited information is available on value chain development across most sectors in the region. This report is intended to help address that gap by providing a broad overview of global and regional value chain participation in SACU member countries across a number of sectors. Specifically, the report provides case examples of GVC participation and the extent of SACU regional value chain development in 6 broad sectors: automotive; apparel; agro-processing; meat, livestock, and dairy; minerals; and tourism. These six broad sectors cover most of those that are being prioritized within the regional industrial policy. They also provide a balance among industries that are manufacturing-oriented and ‘traditional’ GVC industries (textiles/clothing and automotive), those linked to the agricultural sector (agroprocessing and meat, livestock, and dairy), mining, and services (tourism).

This report compiles sectoral value chain case studies that were carried out as part of parallel work, including the SACU Regional Trade and Transport Facilitation Assessment and previous report on Mapping Regional Value Chains in SACU. As the two studies were carried out for different purposes and with a different approach, the structure and focus of the outcomes are not fully consistent across sectors presented in this report. However, in all sectors, the case studies provide an overview of the structure of the value chain and interlinkages across firms in SACU, along with their positioning in wider GVCs. They also provide some discussion of the main constraints impact GVC participation and competitiveness, as well as the constraints to developing more integrated RVCs.

Related News

tralac’s Daily News Selection

The selection: Thursday, 3 March 2016

Featured tweet, @ekbensah: CFTA – The AU will be creating a dedicated website, including monitoring on #BIAT – Boosting Intra-African Trade

Featured trade policy review process: Inquiry into Africa Free Trade initiative (AFTi) – call for written evidence (SAANA)

17th Ordinary Summit of the East African Community Heads of State: communiqué

The Summit directed the council to review the East African Development Bank charter to streamline it into the EAC main structure. The Summit further directed the secretariat to develop guidelines for the creation, governance and reporting structures for all the institutions of the community. The Summit directed the council to finalize the work on the modalities required to establish a sustainable financing mechanism for the East African Community based on various options, including a hybrid of a levy and equal contribution with a commitment to increase the budget, that encompasses the principles of equity, solidarity and equality, and submit a report to the next Summit for consideration. The Summit took note of the progress and road map towards finalization of the comprehensive study on automotive industry in the EAC region; and directed the Council to expedite the process and report to the 18th Summit.

Related EAC summit updates: South Sudan becomes EAC member, but not Somalia (IPPMedia), New generation passport for East Africans unveiled (Daily Nation), Uhuru, Magufuli seek to re-set trade ties with joint road projects (The East African), Museveni: EAC will ensure region’s survival, prosperity and security (The Independent), Why East Africa wants to ban second-hand clothes (BBC), Boost for Kenyan workers as South Sudan wins EAC admission (Business Daily Africa), Uganda, Tanzania agree on Shs13 trillion southern oil pipeline deal (Daily Monitor)

Northern Corridor states move to fill capacity gaps (New Times)

Northern Corridor member states have announced steps toward human resource development and capacity building as part of efforts to end brain drain and cut costs on scholarships abroad. The plan involves devising joint scholarship programmes in infrastructural interconnectivity projects that will be conducted by 17 centres of excellence across the region. The plan was announced on Tuesday during a meeting of the human resource and capacity building cluster, whose purpose is to commission a draft framework that will facilitate offering of scholarships to fast-track provision of requisite skills at those centres.

@FrankMatsaert: Holili OSBP funded by @TradeMarkEastA – 1st impact survey shows already 24% reduction in border crossing time, more to come.

Nacala corridor signs $8m rolling stock deal; port tender delayed (Zitamar News)

SADC banking supervisors meet to bolster financial stability (Seychelles Nation)

Banking supervisors from countries of the Southern African Development Community have come together at the Eden Bleu Hotel in Seychelles for their 2016 steering and sub-committee meetings. The aim is to discuss ways to bolster financial stability with main issues of discussions being banking supervision and regulatory, anti money laundering and counter financing of terrorism. A proposed draft banking model law being worked on by SADC and its legal sub-committee, will also be deliberated on. The model law will help in bringing in those central banks together. A report will be submitted to the next central bank governors’ meeting in April for discussion.

Botswana’s mineral revenues, expenditure and savings policy (AfDB)

What can other countries learn from Botswana with regard to mineral revenue management and expenditure, especially now that the country is a mature mineral producer? In many respects the Botswana experience is a positive one with many examples of policy and practice that are relevant to other countries. Botswana has an effective and efficient mineral fiscal regime, and these revenues have been invested in social and economic development. Sufficient financial resources have been accumulated to provide effective stabilisation buffers. However, Botswana’s experience also has some distinctive characteristics that make it more difficult to replicate. These include the very high rents entailed in diamond mining, and the fact that the bulk of that mining is done by one company. The following are the main lessons that are of general relevance. [The author: Keith Jefferis] [Other reports from the African Natural Resources Centre]

The price is not always right: on the impacts of commodity prices on households (and countries) (World Bank)

We uncover similar patterns in the African data. The income commodity dependence in Africa is very high (higher than in Latin America) and varies across countries. The lower quintiles also tend to show higher commodity dependence. In Ghana, for instance, the share of income derived from commodities is 71.4 in the first quintile, and 27.1 in the top quintile. Table 2 shows that in the data, most of the dependence from commodities in Africa is related to dependence on agriculture. [The authors: Daniel Lederman, Guido Porto]

‘Beyond AGOA’ policy updates: @USEmbassySA: With AGOA issues resolved, we are focused on a broader, stronger economic partnership by expanding trade and investment between US and SA. [Chicken imports end AGOA impasse (Business Day), USTR Factsheet: Obama administration actions open South African market to US agriculture]

COMESA Business Council signs MOU with Corporate Council on Africa

The COMESA Business Council, which is an equal partner and the private sector partner of COMESA, the largest and most effective regional organization in Africa signed an MOU with the Corporate Council on Africa that launches a new partnership on trade facilitation initiatives. The partnership will be modelled on a project CCA launched in 2014 to develop joint private sector recommendations on trade facilitation in East Africa, which has been central to the White House Trade Africa Initiative. The CCA-CBC partnership provided guidance for the meeting of the COMESA TIFA in Lusaka on February 8, 2016 and is designed to help facilitate trade in the COMESA region, as well as to provide private sector support for the Trade Africa initiative. It will be implemented through the CCA Trade Africa Working Group.

Africa-Arab Partnership: pre-summit meeting update (AU)

It discussed the preparation for the 3rd Africa-Arab Ministerial Meeting on Agricultural Development and Food Security and considered the work so far done with respect to Cooperation on Migration; activities of the Africa-Arab Cultural Institute in Bamako, Mali; the outcome of the meetings of the Working Groups on Trade and Investment, and Infrastructure; the preparation for the 8th Africa-Arab Trade Fair and Disaster Response Fund.

India’s trade pacts in a changing world (LiveMint)

The Economic Survey 2015-16’s analysis of the impact of India’s free trade agreements on the economy is a valuable attempt to address a gap in the policymaking ecosystem. Its conclusion - a conditional one, for it acknowledges the need for more analysis - is unsurprising. Controlling for potential non-FTA trade growth, India’s FTAs have on the whole had significant impact, boosting trade without introducing inefficiency due to trade diversion. So far, so good. But this raises interesting questions about New Delhi’s long-standing preference for multilateral trade liberalization and the global shift to the contrary.

India's Duty Free Tariff Preference Scheme for LDCs: ITC launches business guide (ITC)

Namibia to address WTO in bid to save livestock sector (New Era)

At the meeting to be held from March 16 to 17 the delegation is set to present its case before the Sanitary and Phyto Sanitary (SPS) Committee of the WTO in a bid to mitigate the new stringent and soon-to-be-announced livestock import restrictions by South Africa. The delegation will include representatives from the Directorate of Veterinary Services, the Agricultural Trade Forum and agricultural unions, as well as the Ministry of Industrialisation, Trade and SME Development. “Namibia’s position is that the issue has to be solved bilaterally to the benefit of both countries by way of negotiations, and that should the import conditions be implemented, it has to be done on a differentiated basis over a period of time. It is hoped that South Africa will agree to such a process, seeing that the impact on the Namibian livestock exports and the meat industry could be catastrophic,” the Meat Board said yesterday.

Uganda: agricultural value chain study EOI (AfDB)

With an initial pilot programme in Uganda, the Bank’s Agricultural Value Chain Study aims to select, prioritise and conduct a detailed value chains study. The commodities selected for the study will be identified on the basis of stakeholder consultation. The study assesses the status, constraints and economic potential of the selected commodities. Based on the findings of the study, the investment opportunities for the Bank and bankable private sector projects will be identified and the policy and institutional measures that need to be implemented will be delineated. The study will also review farm-level productivity of selected commodities, input and output markets for commodity in question, land tenure, access to finance by agribusinesses, extension, etc.

Participation in regional and global value chains as a driver of structural change in Africa (World Bank)

The objective of this study will be to invigorate and deepen the discussion about structural change in Africa and the appropriate trade and industrial policies that will allow countries in Africa to drive employment growth in higher value-added activities. [Note: Extracted from 'Summary of Africa regional studies due in FY16'] [Further details: Nora Carina Dihel, Trade & Competitiveness, This email address is being protected from spambots. You need JavaScript enabled to view it.]

Mozambique: Running after the rankings – but perhaps we don’t want to change (SPEED)

Mozambique fell 5 places in the most recent last World Bank Doing Business ranking. As usual the report was followed by a flurry of activity by donor agencies and the Ministry of Industry & Commerce seeking to identify reforms which could be carried out to improve the ranking. A quick analysis of the pages of proposals (a 154 slide presentation from the World Bank alone!) presented shows that few of the ideas are new. In fact most of the recommendations have been under discussion for many years. So what conclusion can we draw from this? [The author: Carrie Davies]

South Africa: Port authority bemoans regulator’s tariff move (Business Day)

The Port Regulator of SA’s decision to grant a 0% tariff increase to the Transnet National Port Authority will reduce the authority’s revenue by more than R600m. TNPA had asked for 5.9% tariff increase, but on Wednesday the regulator announced it would not grant an increase, citing "cargo volume and market-related factors". Analysts have criticised SA’s ports charges for being among the most expensive in the world, an allegation denied by Transnet. The Port Regulator said the ports are expensive in some areas and cheaper in others.

Mombasa: Relief for traders as port cargo clearance amnesty extended (Business Daily)

Clover says will no longer invest in Nigeria (The Namibian)

South Africa's Clover Industries will no longer invest in Nigeria due to a financial crisis caused by a sharp fall in oil prices, the dairy products company said yesterday. “The current financial crisis experienced in Nigeria, which is fuelled by the low oil price, is a further cause for concern. Thus, the group has decided to withdraw from future investments in Nigeria,” Clover said in a statement. The company said it will continue to expand operations in Botswana, Namibia, Lesotho and Swaziland.

Rwanda: Cimerwa calls for control of cement imports as competition tightens (New Times)

Nigeria unveils data dissemination system on statistics (The Namibian)

Habitat III: strategising for sustainable urbanisation in Africa (Leadership)

Brian Levy: 'Keeping the lights on – workable and unworkable approaches to electricity sector reform' (World Bank Blogs)

Why “inefficiency” is needed in energy financing for Africa (World Bank Blogs)

Africa has the biggest reservoir of green growth (UNECA)

The Road to Nairobi 2016 project: connecting youth entrepreneurs (Building Bridges 2016)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

Joint Communiqué of the 17th Ordinary Summit of the East African Community Heads of State

Communiqué of the 17th Ordinary Summit of Heads of State of the East African Community

EAC: Advancing Market-Driven Integration

The East African Community Heads of State, their Excellencies president Dr. John Pombe Joseph Magufuli of the United Republic of Tanzania, President Yoweri Kaguta Museveni of the Republic of Uganda, President Paul Kagame of the Republic of Rwanda, President Uhuru Kenyatta of the Republic of Kenya, and H.E. Dr. Joseph Butore, 2nd Vice President of the Republic of Burundi, held the 17th Ordinary Summit of the East African Community Heads of State at the Ngurdoto Mountain Lodge in Arusha, Tanzania on 2nd March, 2016. H.E. Dr. Ali Mohamed Shein, President of Zanzibar, and H.E. James Wani Igga, Vice President of the Republic of South Sudan were in attendance. The Heads of State and Government met in a warm and cordial atmosphere.

The Summit received the annual report of the Council of Ministers covering the period November 2014 – November 2015 and noted the steady progress made in the implementation of the programmes of the community.

The Summit considered progress in the implementation of key outstanding decisions and other policy issues of strategic importance to the East African Community and noted that there are: – Council decisions/directives that have remained outstanding for many years; delays in ratification of protocols; and noted that there are bills enacted by the East African Legislative Assembly that have remained unassented to.

The Summit directed the secretariat to avail the partner states with a list of all protocols that have not yet been ratified to enable the partner states expeditiously ratify them and deposit the instruments of ratification with the secretary general by 30th July, 2016.

The Summit decided to assent to bills which have been submitted to partner states at least three (3) months prior to the Summit and to which Heads of State have given no objection during their ordinary Summit.

The Summit directed the partner states to implement all the outstanding decisions and report the status to the next Summit of the Heads of State.

The Summit delegated its powers of approval of reviews of the East African Community Common External Tariff and the East African Community rules of origin to the Council of Ministers in accordance with sections 3, 5 and 6 of the Summit (Delegation of Powers and Functions) Act 2007 for a further three years with effect from 2nd March 2016.

The Summit noted the proposed implementation framework for the EAC institutional review and directed the Council to proceed with the implementation of the proposed framework and give a progress report at the next Summit of the Heads of State.

The Summit directed the council to review the East African Development Bank (EADB) charter to streamline it into the EAC main structure. The Summit further directed the secretariat to develop guidelines for the creation, governance and reporting structures for all the institutions of the community.

The Summit directed the council to finalize the work on the modalities required to establish a sustainable financing mechanism for the East African Community based on various options, including a hybrid of a levy and equal contribution with a commitment to increase the budget, that encompasses the principles of equity, solidarity and equality, and submit a report to the next Summit for consideration.

The Summit received a report of the council on the negotiations for the admission of the Republic of South Sudan into the East African Community and decided to admit the Republic of South Sudan as a member of the EAC. The Summit designated the chairperson of the Summit to sign the treaty of accession with the Republic of South Sudan.

The Summit noted that the verification exercise for the admission of the Republic of Somalia into the EAC was not undertaken, as preparations with the government of the Republic of Somalia have not yet been finalized. The Summit directed the council to undertake the verification exercise and report to the 18th Summit.

The Summit received a report of the council of ministers on progress on the EAC political federation. The Summit commended the progress thus far and decided to finalise the matter at the next Summit.

The Summit took note of the progress and road map towards finalization of the comprehensive study on automative industry in the EAC region; and directed the Council to expedite the process and report to the 18th Summit.

The Summit took note of the progress made in promoting the cotton, textile, apparel and leather industries in the region and directed the partner states to ensure that all imported second hand shoes and clothes comply with sanitary requirements, in the partner states. The Summit further directed the partner states to consider banning the export of raw hides and skins outside the EAC region.

The Summit, being desirious of promoting vertically integrated industries in the textile and leather sector, directed the partner states to procure their textile and footwear requirements from within the region where quality and supply capacities are available competitively, with a view to phasing out importation of used textile and foot wear within three years. The Summit directed the partner states to sensitize all stakeholders and directed the council to provide the Summit with an annual review with a view to fast tracking the process.

The Summit endorsed and launched the EAC vision 2050. The EAC Heads of State committed themselves to implement the EAC Vision and ensure that by 2050, the EAC will have been transformed into an upper-middle income region within a secure and politically united East Africa based on the principles of inclusiveness and accountability.

Their Excellencies the EAC Heads of State launched the new international East African e-passport and directed that commencement of issuance of the EA e-passport takes effect from 1st January, 2017; and implement the phase out programme for the current East African and national passports from 1st January, 2017 to 31st December, 2018. The Heads of State further directed partner states to undertake awareness creation programmes and other continuous outreach programmes on the new international EA e- passport.

The Summit, pursuant to Article 42 (2) of the Treaty for the Establishment of the EAC, witnessed the swearing into office of Mr. Yufnalis Ndege Okubo from the Republic of Kenya as the new registrar of the East African Court of Justice.

Their Excellencies the EAC Heads of State launched the Code of Conduct to Fight Corruption in the Private Sector. The Summit commended the commitment and aspirations of the private sector to play a leading role in the integration process.

Their Excellencies the EAC Heads of State awarded certificates to the winners of the EAC Secondary Schools Essay Competition 2015.

The Summit appointed Mr. Liberat Mfumukeko from the Republic of Burundi as the new Secretary General. The appointment will take effect from 26th April, 2016. The Summit thanked the outgoing Secretary General, Amb. Dr. Richard Sezibera, for his dedicated service to the community and wished him success in his future endeavours.

The Summit renewed the contract of Mr. Charles Jackson Kinyanjui Njoroge as the deputy secretary general of the East African Community for a further three (3) years with effect from 29th June 2016.

The Summit clarified that H.E. Yoweri Kaguta Museveni is the EAC appointed mediator for the inter-Burundi dialogue. The Summit also appointed a team under H.E. Benjamin William Mkapa former president of the United Republic of Tanzania to facilitate the mediation.

The Summit decided that H.E. Dr. John Pombe Magufuli continues as the chairperson of the Summit for a period of one year.

The Summit expressed its solidarity with the people and the government of the Republic of Kenya following the attack by al-Shabaab terrorists on the Kenya defence forces’ Amisom base at el Adde in Somalia which resulted in the death of kdf soldiers. The Summit condemned the attack and reaffirmed the community’s resolve to counter terrorism and insecurity in the region.

Their Excellencies, President Yoweri Kaguta Museveni of the Republic of Uganda; President Uhuru Kenyatta of the Republic of Kenya; President Paul Kagame of the Republic of Rwanda, and; Joseph Butore, 2nd Vice President of the Republic of Burundi thanked their host, his Excellency President Dr. John Pombe Magufuli of the United Republic of Tanzania for the warm and cordial hospitality extended to them and their respective delegations during their stay in Tanzania.

Done at Arusha, this 2nd day of March, 2016.

Related News

Northern Corridor states move to fill capacity gaps

Northern Corridor member states have announced steps toward human resource development and capacity building as part of efforts to end brain drain and cut costs on scholarships abroad.

The plan involves devising joint scholarship programmes in infrastructural interconnectivity projects that will be conducted by 17 centres of excellence across the region.

The plan was announced on Tuesday during a meeting of the human resource and capacity building cluster, whose purpose is to commission a draft framework that will facilitate offering of scholarships to fast-track provision of requisite skills at those centres.

In exchange of course training from all centres at least each university is expected to enroll two students from a member state who will take post-graduate designated courses in energy, transport, tourism, information and communication technology amongst others.

University of Rwanda and America’s Carnegie Mellon University Kigali branch being the only accepted centres of excellence in the field are expected to enroll students specialising in geographic information systems and other chosen courses.

According to officials, member states agreed to a mutual programme of boosting capacity building mostly in engineering.

The engineers will be expected to work in ongoing corridor projects such as railways, oil pipelines, submarine cables and optic fiber network connection.

Although no exact amount of loss incurred nor how much the region might save should they train its own citizens, the Common Area of High Education was expected to be endorsed by Heads of State at the 17th summit in Arusha.

According to Dr Celestin Ntivuguruzwa, the permanent secretary at the Ministry of Education, all member countries under their respective ministries of education, labour, energy and ICT seek to promote regional education training that will cut spending on foreign expatriates.

“In our region, you have heard projects to extract petrol, mining industry, improvement of aviation services but we are still hampered by lack of capacity, we end up hiring expatriates instead,” Ntivuguruzwa said.

In common area of high education, experts have advocated for a comprehensive, harmonisation, evaluation and accreditation of course units which in the future will produce skilled personnel to compete with highly qualified foreign job seekers.

“For Rwanda as a country that relies on its citizens as the prime resources of which 70 per cent of them are youth, we need to make use of such forces by providing facilities that will help these people compete on available regional and other markets,” he added.

However, ambitious member states seeking to narrow down the skills gap are faced with high constant demand and budgetary constraints which is pushing them to source alternative funds in a drive to reduce brain drain.

Speaking to The New Times, Samuel Wanyonyi, coordinator of the project and deputy director of Kenyan Technical Education and Vocational Training, said member states will set up a fund to mobilise alternative budget besides state contributions.

“Having to go to the World Bank to look for money to train our people abroad is not necessary, we need that money here, it must be the role of our government to fund these initiatives on top of other sources,” he said.

“We will need to identify how many people we need for example in the standard gauge railway project and other projects, who will come from Kenya, Uganda, Rwanda or Southern Sudan and then we jointly invest in those people instead of others.”

Related News

Botswana’s mineral revenues, expenditure and savings policy

The African Natural Resources Center (ANRC) has commissioned a series of case studies to bridge the knowledge gap in natural resources project-driven SME development, supply chain based domestic linkages, extractives revenue management, public-private partnerships and fiscal policy formulation. This case study examines the experience of a resources-dependent country’s approaches to mining revenue management.

In the natural resources sector, national governments perform a central role by acting as stewards in resources development. This requires a balance of policy, legal and institutional considerations. It also requires governments to consider the needs of various stakeholders. In the extractives sector, the importance of protecting inter-generational benefits is a particular challenge given the finite nature of resources. This places an extra burden on policymakers to increase the value obtained from extractives while giving investors a fair return.

Additionally, to increase development outcomes, governments must make informed choices while meeting public expectations to benefit more from extractives projects. A particular challenge facing both investors and governments is to ensure that the impact of extractives projects is felt as early as possible. Another is to ensure that countries begin to enjoy the benefits despite the time lag between project commissioning, production and payment of taxes.

Equally important is the need to stabilize the project environment such that, regardless of the project life cycle, commodity market conditions and level of profitability, projects continue to have a positive effect on human development. The answer in part lies in delinking revenue from human development strategies by assisting governments with other options for delivering tangible benefits.

Other important challanges facing countries include:

-

Striking a balance between the impact on local and national economies;

-

Making the correct trade-off between fiscal and non-fiscal benefits;

-

Integrating projects into national economies to ensure local content while capitalizing on the global outreach of multinational corporation supply chains and related economies of scale;

-

Ensuring that public-private partnerships increase human impact, promote small and medium enterprises (SMEs) and deliver social welfare services directly to those affected by extractives projects;

-

Securing inter-generational value by investing revenue in productive assets.

Many resource-rich countries need to generate concrete solutions and knowledge to overcome these challenges they face and build their own capacity. In view of this the African Natural Resources Center (ANRC) has commissioned this series of case studies to benchmark best practices. Ultimately, through these studies, we want to offer countries practical solutions and a coherent policy foundation with which to improve development outcomes through natural resources projects.

Mineral Revenues, Expenditure and Savings Policy in Botswana

Introduction

In many African countries, the exploitation of natural resources is a major driver of economic growth, exports, fiscal revenues and development. Although many countries in the continent are well-endowed with both renewable and non-renewable natural resources, it is by no means assured that these endowments will automatically translate into broad-based social and economic development. Resource-based economies face particular challenges, arising from price and market volatility, the fiscal challenges of capturing resource rents, macroeconomic impacts of real exchange rate appreciation and governance challenges that often result in planning failures and corruption. Mineral resources are also finite and therefore raise issues of intergenerational fairness – how the proceeds of mineral exploitation should be shared between current and future generations. Several resource-based economies have managed to avoid some or most of these problems, and their policy choices and institutional design might provide useful insights for other countries. Botswana is one such economy. It is often cited as an example of a country that has avoided the adverse impacts of the “resource curse” through appropriate policy and governance choices.

The mining sector continues to be the backbone of Botswana’s economy, despite efforts to diversify. Mining is, by some measures, the largest contributor to gross domestic product (GDP), generates the majority of export earnings and makes a major contribution to government revenues. The use of mineral revenues is, therefore, of critical importance for sustainable development. Botswana has received widespread praise for the way in which it has managed mineral revenues and invested them in education, health care and other forms of assets. In some respects, it has managed to avoid what is commonly known in the literature as the “mineral curse” and “Dutch Disease” through appropriate macroeconomic, exchange rate and fiscal policies, as well as institutional design.

It is important, however, that past success should not lead to complacency. It is also critical to recognize that policy changes may be required in response to changing circumstances, both domestically and internationally. As this report will show, the peak of the contribution of minerals to the Botswana government’s revenues appears to have passed, and the fiscal importance of minerals is likely to decline in future. At the same time, some Dutch Disease and resource curse characteristics can be observed, such as high unemployment, high-income inequality, slow growth of non-mining exports and questionable public spending decisions.

Related News

Why “inefficiency” is needed in energy financing for Africa

One of the most important findings noted at the Africa launch of the World Bank’s Progress Toward Sustainable Energy: Global Tracking Framework 2015 (GTF) report for the Sustainable Energy for All initiative, is that despite recent trends to increase investment in the energy sector, we still need to double the number of new connections to modern energy services per year to reach universal access to energy by 2030.

Universalizing access to clean, modern energy services is at the heart of our ability to deliver on the new globally agreed sustainable development goals and climate agreements. Knowing this, the panel of experts discussing the findings of the report at the Africa Energy Indaba was asked a key question by Anita Marangoly George, Senior Director of the Bank’s Energy and Extractives Global Practice – did we think achieving the universal access goal was possible in just a decade and a half?

The answer from every panelist was – yes, achieving universal access by 2030 will be possible, but not by relying only on the 20th century method of expanding traditional electricity grids.

We agreed that emerging decentralized technologies and business models are the only way to quickly universalize energy access to the 600 million Africans who currently lack it. While the quickest technologies that can be deployed, so-called solar home systems, offer lower levels of power than a grid, it has been shown that the majority of human development benefits from access to energy actually occur at a very low level of consumption per capita. This means that there are important arguments not to use a “grid or nothing” approach that would take decades, which we do not have, to deploy.

The problem is not that we lack the technology or the methods, but rather that key development support institutions such as the World Bank and other development financiers are much better set up to support a small number of large infrastructure projects than they are to assist 7,000-20,000 thousand local energy enterprises needed to quickly universalize energy access via these lower-powered technologies.

Important movements such as the Power for All campaign of energy access-focused businesses and civil society, the U.S. government’s Power Africa partnership, and the UK government’s Energy Africa campaign are all working to create opportunities for such businesses to emerge and be supported, but one thing is agreed by all – the key is finance, and before real progress on universalizing energy access can be made, development banks, foundations and other concessional sources of finance must become major players in the energy access space.

So what are we waiting for?

Well we first of all need to utilize the practical and analytical tools we already have to build energy access markets, because it is clear that energy projects are not enough. The world needs functioning markets for energy access services but we’re still mostly focusing on individual projects. This needs to change.

We simultaneously need to develop incentives within development financiers to fund smaller projects – perhaps that would be to build and support more project aggregators such as SunFunder or perhaps it is to build a fund for to support energy training institutions to ensure money already promised to energy access will be spent on companies that can deliver, because the 7,000-20,000 companies do not exist yet and will need trained workers to undertake this massive task.

The takeaway is that a huge proportion of big, efficient infrastructure finance needs to be replaced with more complicated, expensive, exploratory, support to lots of small players. This may seem inefficient at first, but will deliver the jobs and human development benefits that Africa’s large infrastructure investments of decades past have largely missed.

On this human development point, one last message is this: while we now have agreement that the GTF was necessary because measuring access simply via the number of new connections is inadequate, we still measure the success of businesses funded to deliver access largely on this same inadequate metric.

When looking at future investments in energy access, donors should consider supporting more holistic enterprises that explicitly aim to deliver not only connections and kilowatts, but community jobs, community services and productive technologies. These services will directly impact communities’ ability to pay for more energy and more services, which in turn, improves companies’ bottom lines and banks’ balance sheets. Win-win-win.

For governments serious about development but also serious about value for money, we need to be looking at these and other energy nexus issues more holistically. In the era of SDGs and a new climate agreement, we need to be thinking about how we can use small “inefficient”, investments to deliver big, efficient results.

Related News

Uhuru, Magufuli seek to re-set trade ties with joint road projects

Tanzania and Kenya are targeting joint infrastructure projects to help boost trade flow across their common border amid thawing relations between Dar es Salaam and other partners of the East Africa Community (EAC).

President Uhuru Kenyatta and his Tanzania counterpart John Magufuli said on Wednesday they would Thursday launch the construction of the Arusha-Tengeru dual carriage way and a bypass road in Tengeru as part efforts to smoothen the flow of cargo.

The road is part of the Arusha-Holili-Taveta-Voi road that links northern Tanzania with Taveta, on the Kenyan side.

“We want to take our friendship and relations to higher levels by implementing projects that impact positively on the lives of our people,” the Heads of State said in a joint statement following a meeting on the sidelines of a regional summit in Arusha.

Kenya last week opened its first one-stop border post with Tanzania at Holili in a bid to cut the time taken to clear goods between the two nations and increase volumes of transhipment cargo through the Mombasa port.

The $12 million facility at the Taveta-Holili crossing is intended to reduce by a third the time trucks take to cross the border and will also cut the distance between Mombasa and Bujumbura by 400 kilometres.

The one-stop-border post is first to be commissioned among the total 15 border facilities under construction across the EAC bloc and South Sudan.

“I and my friend and brother President Magufuli have similar visions for our countries. We are targeting development projects that grow the economy and eradicate poverty,” said President Kenyatta.

Tanzania’s latest commitment to joint infrastructure projects with Kenya and coming in the wake of a joint oil pipeline deal with Uganda on Monday could help clear its latest “lone-ranger” image among other EAC partners on key integration issues such as trade and infrastructure development.

The fallout between Tanzania and Kenya, Rwanda and Uganda was fuelled by the formation of a “coalition of the willing” by the three states to push for faster integration within the EAC.

At a meeting in Mombasa in August 2013 regional leaders including Mr Kenyatta, Yoweri Museveni (Uganda) and Paul Kagame (Rwanda) discussed key proposals to deepen integration without the input of Tanzania.

The meeting was followed later by another in Entebbe, Uganda in what most analysts read as a resolve by Kenya, Uganda and Rwanda to ditch the laborious consensus model of the EAC, in favour of one where there is a “leading tendency” by a willing few.

The meetings drew anger from former Tanzania President Jakaya Kikwete who alleged a scheme to isolate Tanzania from the EAC bloc.

Dr Magufuli on Wednesday however said Tanzania was committed to EAC integration and pledged to work with other members of the bloc.

Related News

Namibia to address WTO in bid to save livestock sector

The eyes of the agricultural world will be on a high-powered Namibian delegation from all sectors of the local livestock and meat industry when it addresses the World Trade Organisation (WTO) in Geneva.

At the meeting to be held from March 16 to 17 the delegation is set to present its case before the Sanitary and Phyto Sanitary (SPS) Committee of the WTO in a bid to mitigate the new stringent and soon-to-be-announced livestock import restrictions by South Africa.

The delegation will include representatives from the Directorate of Veterinary Services, the Agricultural Trade Forum and agricultural unions, as well as the Ministry of Industrialisation, Trade and SME Development.

General manager of the Meat Board Paul Strydom confirmed that the Meat Board, in cooperation with the Directorate Veterinary Services, the Agriculture Trade Forum, agricultural unions and the Directorate of Planning, is currently finalising preparations to state Namibia’s case in light of South Africa’s expected new requirements that would make Namibian livestock exports to that country virtually impossible.

“Namibia’s position is that the issue has to be solved bilaterally to the benefit of both countries by way of negotiations, and that should the import conditions be implemented, it has to be done on a differentiated basis over a period of time. It is hoped that South Africa will agree to such a process, seeing that the impact on the Namibian livestock exports and the meat industry could be catastrophic,” the Meat Board said yesterday.

Stakeholders in Namibia’s N$2.5 billion per annum livestock export industry are on the edges of their seats after the last round of negotiations in January regarding the South African authorities’ intent to introduce new animal health requirements for Namibia which, if implemented, could bring the local livestock industry to its knees.

As coordinator of the negotiations, the Meat Board met the deadline of January 8 to answer South Africa on the various issues on which the neighbouring country is basing its proposed new livestock imports from Namibia.

“We’ve not received any feedback to date, but expect an announcement by the SA authorities any day now,” Strydom said.

It is expected South Africa will adopt the new restrictions within the next few days, following which the regulations will be implemented six months later.

Namibia is now preparing to address the SPS Committee to acquire some breathing space before the implementation and to activate its own Master Plan after the Livestock Producers Association (LPO) of Namibia and the Namibian Agricultural Union last week officially requested President Hage Geingob to intervene to help save the industry.

Namibia currently exports some 180 000 weaners, 90 000 sheep and 250 000 goats per year to South Africa and the N$2 billion plus industry is the livelihood of many, especially small-scale and communal farmers.

The Namibian delegation – which is yet to be named – will put forward the strongest case possible to avoid such a catastrophe, as some 75 percent of communal farmers depend on livestock exports to SA for their livelihood.

LPO chairperson Mecki Schneider has described the requirements as “trade restrictions requested by the SA Red Meat Producers Organisation (RPO), because they have no system in place to control the flow of animals to and from South Africa”.

It turns out the revised regulations have not changed from the previous publication, on which the Namibian industry has already commented extensively. These stringent regulations were imposed overnight in May 2013 and devastated the local livestock export industry, resulting in losses amounting to billions of dollars.

The Meat Board has since 2013 been putting short-, medium- and long-term strategies in place in case of a scenario, such as the one unfolding now.

These measures include the transformation of the Namibian weaner industry to an oxen production system.

Related News

SADC banking supervisors meet to bolster financial stability

Banking supervisors from countries of the Southern African Development Community (SADC) have come together at the Eden Bleu Hotel in Seychelles for their 2016 steering and sub-committee meetings.

The aim is to discuss ways to bolster financial stability with main issues of discussions being banking supervision and regulatories, anti money laundering and counter financing of terrorism.

These are mainly financial inclusion, financial stability, harmonising laws, regulations, standards and procedures.

A proposed draft banking model law being worked on by SADC and its legal sub-committee, will also be deliberated on. The model law will help in bringing in those central banks together. So when for example there is an intra-regional trade, it can ease cross-border banking transactions between respective states of the region.

The meetings are being hosted by the Central Bank of Seychelles (CBS) in collaboration with SADC itself.

The Financial Intelligence Unit (FIU) is also taking part.

SADC technical subcommittees meeting is an annual event hosted alternately by member countries. Last year’s subcommittee meeting of banking supervisors was held in Windhoek, Namibia in February.

Addressing the gathering, the first deputy Governor of the Central Bank of Seychelles, Christophe Edmond, said with the introduction of new regulatory and supervisory requirements, brought in by the international standards set ups such as the bank of international settlements and the financial task force, the issue of harmonisation of regulatory and supervising laws in the region is of particular importance.

“This sub-committee meeting is but one of many occasions where we can come together to discuss the way forward, to achieve the objective of the central banks as we look first inside our regional block to foster the right foundation that will enable the establishment of a sound banking system across our borders,” he said.

He added that SADC continues to monitor the progress made by compiling information to ensure the block is moving in the right direction as it seeks to implement the necessary standards and regulations.

A report will be submitted to the next central bank governors’ meeting in April for discussion.

Related News

tralac’s Daily News Selection

The selection: Wednesday, 2 March 2016

Today's 17th Ordinary EAC Heads of State Summit: updates

Open session proceedings can be followed live

The EABC Code of Conduct and Code of Ethics will be launched today at the summit after which it can be downloaded from the EABC website. Recommendations from yesterday's Business Summit will also be presented to the EA Heads of State Summit.

Graft killing growth in EA, leaders say (The Citizen)

"As Tanzania's envoy abroad in the past, I have seen how many potential investors skipped the country in favour of other countries. They could not withstand corrupt practices among our officials", he told business leaders from the EAC partner states. Dr Mahiga, who is the current chairperson of the EAC Council of Ministers, urged political leaders in the region to provide the necessary inputs for the private sector which he described as engine of development. He called on the EAC partner states to avoid creating parallels in their transport networks and instead inter-connect the northern, central and southern corridors. The minister assured business leaders that Tanzania was no longer an obstacle to the free flow of business in the region and that to date it has removed all but three inspection centres for goods along the highway to land-locked Rwanda, Burundi and Uganda from Dar es Salaam.

Related: Jackson Kiraka: 'Why EA needs JPM’s forceful presence' (The Citizen), EAC leaders to consider banning used vehicles, clothes (Daily Nation), President Magufuli congratulates Museveni as the two leaders discuss EAC trade (Daily Monitor)

Featured tweets from the #EABusinessSummit:

@ealawsociety: @EA_Bunge seeks to develop new legislation to anchor implementation of Common Market Protocol

@InvestEAfrica: There are 30 different laws that touch on illicit trade in Kenya; Kenya needed to consolidate the diverse laws to better enable enforcement; Much as transit time/cost have gone down - there is concern that cost savings are not being passed on to consumers

Mombasa port traffic up 7.5% in 2015 (Africa Report)

"Although this performance falls short of our target of 1.1 million TEUs for last year, it is a manifestation that the port traffic is growing at a fast rate," Muturi said. Imports totalled 22.68 million tonnes, an increase of 9.2% from the 20.77 million tonnes handled in 2014. Exports also increased by 5% to 3.53 million tonnes from 3.37 million tonnes in 2014. But the volume of goods headed to neighbouring countries decreased by 28.4%, from 731,912 tonnes in 2014 to 523,993 in 2015, a trend Muturi attributed to the introduction of a new cargo-clearing system.

Presentation from the 8th Containers Conference in Port Sudan: Challenges in infrastructures of transit transport corridors within East Africa (by Ms Nozipho Mdawe, Secretary General, Port Management Association of Eastern & Southern Port Management Association of Eastern & Southern Africa)

SGR tunnels on Nairobi-Malaba line to cost taxpayers Sh63bn (Business Daily)

The cost of building underground tunnels in the second phase of the Standard Gauge Railway from Nairobi to Malaba has been put at over Sh63 billion, a sixth of the Sh427 billion cost of Mombasa-Nairobi section. Transport Cabinet Secretary James Macharia says the section will have more than 20 tunnels that will have to cut through the Rift Valley escarpments, making the design work more expensive because it will have to achieve a certain gradient to connect to the next section.

Launching today, in Addis: Africa-China Dialogue Platform (FOCAC)

According to Oxfam, its new "Africa-China Dialogue Platform" will be launched on Wednesday in Ethiopia's capital Addis Ababa, aiming to encourage and facilitate a constructive engagement and dialogue of citizens, policy makers, researchers and other stakeholders on the growing partnership between Africa and China. In line with the launch of the platform, a day-long expert seminar will discuss issues on Africa-China engagement and partnership with a specific focus on foreign direct investment and sustainable agriculture.

EU-SA trade issues: notes from the Agbiz-Tutwa roundtable

EU Ambassador to Croatia, Dr Paul Vandoren, shared his views and experience within the EU context. He noted that South Africa and the European Union are very different, most notably in terms of economic development. However, it would be a shameful waste not to look at the EU for any useful lessons that might be applied in the South African context. More than this it would be short-sighted not to hear out the concern of EU investors holding a staggering €41.8 billion worth of investments in South Africa.

SA-US trade deal reaches beyond AGOA (IOL)

The key areas to improve utilisation of AGOA as a way of enhancing the Africa-US trade and investment relations include, among others: (1) increased US investments to assist with creating productive capacity in the continent; (2) increased US investment in infrastructure; (3) capacity building to meet the US standards; and (4) the expansion of the product coverage under AGOA to include products of export interest to African countries. In order to improve the trade and investment environment between South Africa and US, the two countries have the Tifa platform to discuss issues of interest, such as those relating to policy issues and market access. The next Tifa meeting is expected to be hosted in South Africa later this year. [The author, Mzwandile Masina, is SA's Deputy Minister of Trade and Industry]

Trouble in SA’s farming sector as drought bites (IOL)

In the preliminary estimates of real gross domestic product released by Stats SA yesterday, the contribution of the farming sector to the economy shrank by 8.4% in 2015. This is the largest annual fall in agriculture production since 1995. In the report, the country’s economy grew by 1.3% in 2015, down from 1.5% in 2014 and 2.2% in 2013. [Download the Stats SA report] [Western Cape agricultural sector update]

Mozambique: poultry value chain analysis EOI (AfDB)

The general goal of this study is to provide a detailed analysis of the poultry value chain (VC) in Zambeze and Niassa provinces in Mozambique. The overall objective is to analyse the constraints and propose measures to increase production and create more and better jobs in the poultry sector. The VC analysis must provide and interpret current quantitative and qualitative information on the overall structure and competitive position of the VC, in order to assess the strategic challenges and opportunities for job creation and competitiveness upgrading among firms. [Reposting: Development of the animal feed to poultry value chain across Botswana, South Africa, and Zimbabwe]

Mozambique: China to lead development of $6bn gas pipeline (Zitamar)

A $6bn, 2,600km pipeline to take gas from the Rovuma Basin to South Africa is set to be developed by a consortium including a group of unnamed Mozambican private investors in partnership with South African energy firm Sacoil and led by China Petroleum Pipeline Bureau (CPP), according to an announcement made yesterday. CPP will carry out the requisite pre-investment studies, Sacoil said, and finance them up to the bankable feasibility stage. CPP will also be responsible for procuring debt financing equal to 70% of the total project cost, or $4.2bn, from Chinese financial institutions.

Zimbabwe: Govt puts import controls on medicines (The Herald)

In an effort to boost the local pharmaceutical industry, Government has put import controls on 23 pharmaceutical medicines. The industry, which employs over 1000 people is made up of about nine companies but operations have been constrained by the current economic conditions and the influx of imported drugs some of which are smuggled into the country. The sector has also been struggling to breakthrough in regional markets as some of the countries have stringent licensing conditions, which subsequently make the products uncompetitive.

Tanzania: Government calls for conducive environment for local businesses (IPPMedia)

Prof Mkenda said the government has now started taking measures to reduce unnecessary procedures being taken by various people especially those seeking services from government departments. “We have started with the Business Registration and Licencing Agency (BRELA) where most of the activities there are conducted under one window,” he said. He said the government was looking at how institutions like TBS, TFDA or TIRDO could provide services to customers without interruptions. “We want our people to be served under one umbrella organisation that would reduce unnecessary delays and costs,” he said. [Tanzania: Boosting youth employment prospects (IDRC)]

Kenya: Low demand knocks Kenya's business confidence (Daily Nation)

The Business Sentiment Indicator, a measure of the level of confidence businesses have in the economy, prepared by Standard Chartered Bank fell to 57 in February, the lowest since August 2015. It was 63.9 in January. Export orders fell 14.4% in February to 51, the lowest since November last year. While future expectations also fell, majority of those polled indicated that firms expect future export orders to improve from the current levels.

Japan to set up an Embassy in Mauritius (Government of Mauritius)

Ambassador Ryuhei Hosoya, expressed the interest of Japan to become both an active and strategic partner of cooperation for Mauritius in various fields especially with regard to the Blue economy and other potential areas as outlined in the Vision 2030. According to him, the strategic position of Mauritius as a gateway to Africa will not only boost trade and investment between Japan and Mauritius but also on the international front and in the region as a whole. He further underlined that Japanese firms are already operating in Mauritius and that more investments should be encouraged between the two countries.

Is the illegal trade in Congolese minerals financing terror? (ISS)

The Institute for Security Studies is currently conducting a research project that tracks illicit financial flows related to resource extraction in the DRC. Our studies have found that where multinationals were once the major players, terror groups are now increasingly joining the criminal networks that extort minerals from the eastern part of the country. This underscores the need for urgent and drastic measures to improve natural resource governance, both in the DRC and the broader region.

Fraser Institute Annual Survey of Mining Companies, 2015

Uganda: Social accountability is vital for building trust in post-election Uganda (The Independent)

Development projects that pay greater attention to social accountability can improve citizen-state relations and trust in Uganda and other fragile countries, according to new research by peacebuilding organisation, International Alert. The report, titled Making social accountability work: Promoting peaceful development in Uganda, evaluates two large-scale development projects undertaken in Uganda and has been published following the recent elections in the country that have been undermined by widespread unrest and allegations of corruption. The report states that development projects which build in transparency and accountability components can nurture more constructive government-community relations - vital for closing historical divides between citizens and state that fuelled the civil war in Uganda, and helping people feel they can influence change. [Download]

2016 Forum on Fragility, Conflict and Violence: updates

Mr Eliasson noted that political rivalries, international interference – known as proxy wars – economic volatility and inequalities, weak governance, human rights violations and a growth in violent extremism, feed conflict. “Between 2007 and 2014, civil wars almost tripled. Wars have recently grown in intensity and scale, becoming more deadly, more protracted, more complex and less amenable to settlement. There is a glaring disrespect and disregard of international humanitarian law,” he stated. [Remarks by World Bank Group President] [Development for Peace: new blog site (World Bank)] [African Legal Support Facility receives $22m from the AfDB]

Rapid urbanization and climate change puts strain on Durban’s environment: new report (World Bank)

G20 Data Gaps Initiative II: meeting the policy challenge (IMF)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.