Search News Results

EALA set to pass Omnibus Law on Integration

The East African Legislative Assembly has proposed enactment of an omnibus law to harmonise national laws appertaining to the Community and to institute an administration law for the Common Market Protocol.

The Assembly is of the view such a move shall cure, existing challenges of harmonisation of Partner State laws appertaining to the Community. At the same time, the Assembly wants the Council of Ministers to direct the Sectoral Council on Legal and Judicial Affairs to hold regular meetings and to prioritize harmonisation of laws for EAC in order facilitate integration within the set time frames.

In order to meaningfully facilitate co-operation in legal and judicial affairs as provided for under Article 126 of the Treaty, EALA urges EAC Council of Ministers to expedite implementation of the entire Article which obliges Partner States to harmonise legal training and certification; encourage standardisation of judgments of courts within the Community as well as in establishing common syllabus for the training of lawyers.

Late on Wednesday, EALA approved the Report of the Committee on Legal Rules and Privileges on the oversight activity on the harmonisation of national laws in the EAC context. The Report presented to the House by Hon. Dora Byamukama on behalf of the Chair of the Committee, Hon. Peter Mathuki, follows an oversight activity carried out by the Committee in February 22-26, 2016.

Chapter 24 of the Treaty provides for co-operation in Legal and Judicial Affairs. Specifically, Article 126 (2) (b) of the Treaty provides that “Partner States shall through their appropriate national institutions take all necessary steps to harmonise all their national laws appertaining to the Community”.

In line with that Treaty provision, EAC Partner States established a sub-committee on the approximation of national laws in the EAC context.

During the oversight activity, the Committee was informed that Partner States are at different stages of implementation of the directives of the Council of Ministers on harmonisation on national laws. It further observed that Partner States were slow when it comes to amending laws to comply with the directive of the Council of Ministers pertaining to harmonisation of national laws. Further on, the criteria used and timelines for harmonisation of laws is also unclear.

The Committee cites a number of challenges including frequent changes in the membership of the Task Force, conflicting commitments of members of the Task Force as well as different legal systems. In addition, the slow pace in the implementation of the harmonisation agenda at national level and the lack of monitoring mechanisms to ensure Partner States comply with the adopted approximation proposals are also cited.

During debate time, Hon. Judith Pareno said the activity of harmonising and approximating laws was a Treaty matter and said it was important for the Community to have a system of the laws to harmonise. Hon. Shyrose Bhanji remarked that slow implementation of harmonising laws was retrogressive for integration. She asked the House to request the Council of Ministers to share with the Assembly a matrix showing progress of implementation.

“We also need a special strategy to popularise the laws passed by the Assembly to the citizens,” Hon. Bhanji said. Hon. Martin Ngoga called for a rethink of strategy in the way the Community undertakes its mandate as it advances the objectives of integration. Harmonisation of laws is just one of the ways but there are a number of things we need to do with reference to Article 126.

“Why are we not publishing East Africa Law Journals? There are over 600 laws that we need to harmonise to make EAC realise the Common Market and we must move faster,” he said. The legislator said EALA must take the lead.

“It is the Assembly’s role to make laws and we should not take back the matter to Partner States,” he said. “We must reassess our mode of work,” he added.

Hon. Susan Nakawuki remarked that it was key for the harmonisation of immigration laws to be speedily undertaken. “One of the key issues we need to address is that of the yellow fever certificates and I request the Council of Ministers to inform us of the position of the Community on the matter,” Hon. Nakawuki said.

Chairperson of the Legal Rules and Privileges Committee, Hon. Peter Mathuki urged the Ministers of EAC to be in attendance during the Plenary Sitting. “The continuous absence of EAC Ministers may be another reason for the slow implementation of activities of integration,” Hon. Mathuki said. The legislator also said bureaucracies needed to be reduced.

The 3rd Deputy Prime Minister and Minister for EAC in the Republic of Uganda, Rt Hon. Kirunda Kivejinja remarked that progress on the pillars of integration were notable while, the Deputy Minister for Foreign Affairs, East African, Regional and International Co-operation, Hon. Dr Susan Kolimba remarked that the Council of Ministers was committed to ensuring issues brought to fore by Members are adequately addressed.

Also rising up to support the report were Hon. Joseph Kiangoi, Hon. Abdullah Mwinyi and Hon. Valerie Nyirahabineza.

Related News

Mobile money: Lessons for West Africa

The mobile money financial services industry is now expanding rapidly in the West African sub-region after its phenomenal growth in East Africa. Experiences of East and Southern African countries confirm that mobile money presents a unique opportunity to encourage and enhance financial inclusion, formalise the informal sector, and tap into the domestic savings in rural areas, with a potential to raise economic growth.

At the same time, central banks also recognise that principles governing the sector must be carefully and deliberately managed in order to protect customers while at the same time not creating additional barriers to entry or costly operations for mobile money operators that might stifle the industry and limit its potential.

Much can be learned about this regulatory balance between policies encouraging both growth of the sector as well as consumer protection from case studies, mainly in East and Southern Africa, of countries that are years ahead of West Africa in terms of the widespread introduction of mobile money in the marketplace. In some cases such as Kenya, relaxed regulatory regimes have led to a flowering of mobile money, with its deep penetration and improved economic outcomes through access to financial services for the poorest. On the other hand, strict regulations in some countries have hampered the ability of mobile money operators to enter the market and sustain operations at a low cost, limiting the degree of financial inclusion achieved through mobile money.

Recognising that Sierra Leone and the West African region in general is 5-10 years behind countries like Kenya in this sector, the experience of these countries over the past decade (rather than their current situation) can inform the regulatory and macroeconomic challenges West Africa is facing now and will face in the coming years as the mobile money sector grows. Lessons and evidence from case studies in East and Southern Africa can provide options to answer some of the pressing questions facing the Bank of Sierra Leone and other central banks in the West African region. West African countries can also look to diversity within the region to identify best practices and opportunities for regional collaboration.

Sub-regional Workshop on Mobile Money in West Africa

March 14th-16th, 2016, Bank of Sierra Leone Recreational Complex, Freetown, Sierra Leone

This workshop – jointly organised and supported by the Bank of Sierra Leone (BSL) and the International Growth Centre (IGC) offices in Sierra Leone, Liberia, and Ghana – aimed to achieve this experience sharing and learning across sub-Saharan Africa. The workshop brought together government and private sector representatives from Gambia, Ghana, Guinea, Liberia, Nigeria, and Sierra Leone, and builds on previous SSA meetings over the past two years in Mozambique and Senegal. Through this workshop, BSL hopes they and other central banks in the region can take the next step towards advancing their new guidelines as well as look at new areas such as credit services through mobile money. Key emerging policy areas were identified for workshop sessions to address, and the IGC identified relevant economic questions that can be addressed by the SSA experience.

The workshop addressed the following topics:

-

Research Results: Much research has been done on the implications of mobile money, particularly in terms of facilitating financial inclusion, including: spreading risk and consumption, and the importance of credit and savings to achieve this (Billy Jack); implications for monetary policy (Sebastian Walker & Chris Adam); impact on inflation and productivity (Janine Aron); and uses of big data generated through mobile money for informing policy. The workshop will review these and other areas.

-

Policy/Regulation: The growth of mobile money presents challenges for the formulation and reform of policies that encourage its use for improving financial inclusion, while ensuring customer protection through appropriate market and financial regulations, without distorting financial markets. The different choices of East African countries – such as Kenya with low regulation and high inclusion leading to higher development impacts as research suggests, and Mozambique with more regulation and less inclusion – can help illustrate the implications and policy trade-offs.

-

Programmes: The potential uses of mobile money, such as for salary payments to government workers, payments for public services or taxes, and regulation of informal workers through mobile money salary payments, are opportunities for improving service delivery and promoting the wider development agenda of these countries. The landscape for mobile money in the coming years will be shaped by policy decisions on the nature and scope of its use. At this early stage in its evolution, the experience of countries in East and Southern Africa can help participating countries outline recommendations on various programme areas and define relationships among the banking, telecom, and non-banking financial services sectors to prepare for the optimal use of the instrument.

-

Country priorities for policy: The following areas have been identified as key questions facing central banks in the region, which the workshop proposed to address at country sessions:

-

Lending and credit for mobile money providers

-

Earning interest on a mobile money account/trust account for non-bank led operators

-

Partnerships with telecoms regulators, and cooperation between banks and telecoms

-

Regional considerations and cooperation

-

Customer protection & empowerment through financial literacy

-

Regulations governing agent networks

-

Capital requirements for mobile providers

-

Taxation on transactions and on salary payments for the informal sector

-

International remittances

Presentations from the workshop are available to download below.

Related News

Does trade reduce poverty? A view from Africa

Although trade liberalization is being actively promoted as a key component in development strategies, theoretically, the impact of trade openness on poverty reduction is ambiguous.

On the one hand, a more liberalized trade regime is argued to change relative factor prices in favor of the more abundant factor. If poverty and relative low income stem from abundance of labor, greater trade openness should lead to higher labor prices and a decrease in poverty. However, should the re-allocation of factors be hampered, the expected benefits from freer trade may not materialize. The theoretical ambiguity on the effects of openness is reflected in the available empirical evidence.

This paper examines how the effect of trade openness on poverty may depend on complementary reforms that help a country take advantage of international competition. Using a non-linear regression specification that interacts a proxy of trade openness with proxies of various country structural specificities and a panel of 30 African countries over the period 1981-2010, we find that trade openness tends to reduce poverty in countries where financial sectors are deep, education levels high and institutions strong.

Introduction

Most economists accept that, in the long run, open economies fair better in aggregate than do closed ones, and that relatively open policies contribute significantly to development. Many commentators fear, however, that in the shorter run, one of the steps towards openness – trade liberalization – harms the poorer actors in the economy, and that even in the longer run successful open regimes may leave some people behind in poverty. Africa remains the poorest continent of the world. Yet, at the same time, African countries have experienced significant improvements in trade liberalization. It seems that the large gains expected from opening up to international economic forces have, to date, been limited in Africa, especially for poor people.

While the traditional trade theory predicts welfare gains from openness at the country level through specialization, investment in innovation, productivity improvement, or a better resource allocation, the theoretical impact of trade on the poor remains uncertain. Besides, empirical results do not converge on this point and it seems that developing countries are not equally able to make use of the opportunities arising out of increased access to markets in the developed world.

The contribution of this paper lies in providing new cross-country empirical evidence focused on Africa on how the poverty reduction effect of greater trade openness depends on a variety of structural characteristics, including some that are subject to reform. Using a panel of African countries over the period 1981-2010 and testing for non-linearities in the trade-poverty relationship, this paper explores the empirical link between trade openness and poverty. Its results uncover an interesting pattern of reform complementarity: trade openness tends to reduce poverty in countries as their financial sector grows deeper, their education level higher and their institutions stronger.

Our concern is with poverty, not inequality. Since trade liberalization tends to increase the opportunities for economic activity, it can very easily widen income inequality while at the same time reduce poverty. Consequently, statements about its effects on inequality cannot be translated directly into statements about its impact on absolute poverty. There may be sound positive and normative reasons for interest in inequality, but they are not the concerns of this paper.

Related News

tralac’s Daily News Selection

The selection: Thursday, 17 March 2016

Starting today, in Lilongwe, the 22nd Meeting of the Intergovernmental Committee of Experts. The theme: ‘Financing the SADC Industrialization Strategy and Roadmap’.

Launching today, in Luanda: the Angola-China Chamber of Commerce

Today, in Cape Town: a briefing on the post-Nairobi work programme, by Minister Rob Davies and WTO DG Roberto Azevedo

Roberto Azevêdo: 'WTO’s record boosts its hand in talks' (Business Day)

Members have decided to reflect on how these differences might be overcome and how we might move the WTO agenda forward. The good news is that all members support the notion that we need to continue work on the Doha issues — agriculture, manufactured goods, services and fishery subsidies among them. And all members have again committed to maintaining development at the very heart of the WTO’s work. This is an opportunity to ensure that the future path of global trade talks serves SA’s development goals. I am visiting SA this week to discuss these issues.[Roberto Azevêdo: 'WTO is delivering for Lesotho' (WTO)]

Illegal fishing hurting continent’s fisheries (The EastAfrican)

The United Nations Food and Agriculture Organisation estimates the global marine fishing industry produces some 67 million tonnes of fish annually worth between $100 billion and $200 billion. Africa’s coastal waters produce only 4.6 million tonnes of fish annually, valued at $4.9 billion. However, 52% of the fish stock is fully exploited, 8% is depleted, 19% overexploited while 1% is recovering from depletion, data from both the FAO and the AU-IBAR shows. Key to the near collapse of the continent’s fisheries is the illegal, unregulated and unreported fishing, which costs the continent billions of dollars in lost revenue. The World Bank’s Africa Programme for Fisheries reports that some 11-26 million tonnes of sea food is caught illegally every year, worth between $10 billion and $23.5 billion. The West African coast is said to be the most affected by illegal fishing, with 40% of total catches falling in that category. [Improving Africa's maritime policies (ISS)]

Breaking out of enclaves: leveraging opportunities from regional integration in Africa to promote resource-driven diversification (CCSI)

This report explores the relationships between extractive resources, regional integration, and economic diversification. It looks at how regional approaches can increase the local employment and production effects of extractive resources projects. It discusses the regulatory, institutional, and political economy barriers facing African policymakers in achieving regional cooperation. The analysis makes frequent reference to three case studies of efforts to create trans-boundary transport corridors, including the Nacala corridor in southern Africa, proposals for the exploitation of iron ore in Guinea and Liberia, and the LAPSSET corridor in East Africa to ship oil and gas from South Sudan to ports on the Indian Ocean. [Download] [The authors: Gözde Isik, Kennedy O. Opalo, Perrine Toledano]

Corridors, clusters, and spatial development initiatives in African agriculture: workshop report (ECDPM)

The workshop brought together some of the key institutions and researchers that are active on this topic both from within and outside the CGIAR, with the objectives of understanding the current state of thinking in research and policy circles, and to help define how best the ISPC might contribute through its strategic study on corridors and spatial development initiatives in African Agriculture.

Kenya, Uganda, Rwanda to start joint electronic cargo tracking in June (Business Daily)

“By June 2016, goods moving along the northern corridor (Mombasa-Kigali) will be monitored in real time, curbing dumping, theft and other vices,” Uganda Revenue Authority said in an update. Kenya and Uganda have successfully piloted the ECTS while Rwanda has commenced trials and targets to fully adopt the system by mid this year. South Sudan is also expected to come on board soon following in the wake of its recent admission as the sixth member of the East African Community (EAC). “The southern corridor (Dar-es-Salaam-Bujumbura) is expected to be monitored by a similar system,” said URA's Mr Kateshumbwa. [How ICT-driven concept can boost Africa’s trade ranking (Leadership)]

Mining investment and governance review (World Bank)

By June 2016, MInGov will have completed and published assessments of nine countries using a consistent, measurable, comparable and actionable methodology. These country assessments will include seven in Africa, one in Latin America and one in Asia. Through the collection and analysis of a unique and comprehensive dataset, the Mining Investment and Governance Review (MInGov) presents an objective assessment of the mining sector of several countries. It offers actionable avenues for reform, supports transparency, and informs investment decision-making and debate among interested stakeholders. [From resource curse to rent curse in the MENA region (AfDB)]

ZimTrade calls for trade balance with SA (The Herald)

Zimtrade said yesterday South Africa must increase access to its markets by Zimbabwean companies to improve trade between the two neighbouring countries. Zimtrade chief executive Sithembile Pilime told participants at the Zimbabwe-South Africa trade and investment conference that this should be done to realise a fair trade balance. At present, the trade balance is heavily skewed in South Africa’s favour. In 2012 South Africa enacted the Preferential Procurement Policy Framework Act which stipulates that 75% of procurement should be local in an effort to protect South African manufacturers. The measure by South Africa, which is Zimbabwe’s largest trading partner, has severely impacted on local firms which are struggling to recover from a decade long economic meltdown.

Related: South Africa minister urges Zim businesses to use rands (NewsDay), SA pumps R20bn into Zimbabwe (Chronicle)

Zimbabwe expecting IMF loan in 3rd quarter (The Herald), SADC endorses candidature of Zimbabwean minister for UNWTO post (StarAfrica), Zimbabwe facing worst malnutrition rates in 15 years (UNICEF)

Banning ‘mitumba’ will certainly not revive the local textile industry (Daily Nation)

The textile industry in Kenya failed because it did not adapt to changing circumstances. Serious questions beg answers. For example, why do the export processing zones in Kenya produce high quality clothing for export under the African Growth and Opportunity Act framework only? If East Africa was to give similar tax exemptions for local clothing sold locally, would the benefit of job creation be greater than the foregone tax? Why do khanga (leso) factories in Morogoro, Tanzania, continue to survive despite the onslaught from mitumba and China? Why does the leading shoe producer in Kenya import shoes from India and brand them for local sale?

Ghana: Govt to restrict cement imports from Nigeria, China (Daily Trust)

Africa's leading cement manufacturer, Dangote Company and other cement importers are in for tougher times in Ghana, following plans by government to restrict cement imports into the country. To this end, the Minister of Trade and Industry, Dr. Ekwow Spio-Garbrah, has proposed to the parliament, the enactment of an Act "to propose a ceiling on the annual importation of cement into Ghana." Ghana has a production capacity of about 9 million metric tonnes per year, while national consumption is below 6 million; thus leaving an excess of about 3 million metric tonnes per annum. [We can’t let China destroy Nigeria’s economy - President of Manufacturing Association (CNBCAfrica)]

Portugal exports less to Angola in 2015 (MacauHub)

Portuguese financial newspaper Diário Económico cited figures from the National Statistics Institute to show that Portuguese exports to Angola fell by 45% year on year in January 2016. Although there have been political problems and devaluation of the currency in Mozambique, 2015 was not a bad year, and Portuguese exports increased from 318 million euros to 356 million euros, or almost 12% more.

Consumer market outlook in Africa ‘still positive’ (Business Day)

Despite the decline in growth, Africa’s long-term outlook as a consumer market remains positive, says an inaugural report on retail and consumer businesses by professional services network PwC. The report, released on Tuesday, analysed 10 African economies offering appealing opportunities for retail and consumer businesses looking to expand in Angola, Cameroon, Ethiopia, Ghana, Cote d’Ivoire, Kenya, Nigeria, South Africa, Tanzania and Zambia.

Ethiopia: South African companies keen to invest (Ethiopian Herald)

Opening the Ethio-South African Business Forum organized by the Ministry of Foreign Affairs jointly with the Addis Ababa Chamber of Commerce and Sectoral Associations and the Embassy of the Republic of South Africa here yesterday, Industry State Minister Dr. Mebrahtu Meles said that the nation has already created enabling business environment which attracts foreign investment and the variety of agro-ecological zones, abundant natural resources and labor could be utilized as an input for wealth creation.

Magufuli orders ban on any more dubious power deals (IPPMedia)

Eddie B. Mugarura: 'The EAC bureaucracy vs the people' (New Times)

Timely SA-Saudi trade boost for local economy (Cape Times)

SA trade and investment mission to Brazil (dti)

Business leaders, UN Member States and civil society agree: gender equality critical to economic development (UN Global Compact)

Liner shipping: is there a way for more competition? (UNCTAD)

Kenya: Mobile payments up 21% in 2015 (Daily Nation)

Transport companies promise not to ‘knowingly facilitate’ illegal wildlife trade (Container Management)

Nigeria: UNIDO officially opens an investment and technology promotion office

The top 8 active researchers in developing countries according to RePEc (World Bank Blogs)

Imposing, aggressive and unwilling to listen: how South Africans are perceived in Africa (Daily Maverick)

South Africa: Department of Home Affairs overview of 2015 asylum trends (PMG)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

DG Azevêdo: WTO is delivering for Lesotho

WTO Director-General Roberto Azevêdo visited Maseru, Lesotho, on 16 March 2016 to discuss the implementation of recent WTO agreements and how the organization can keep on supporting growth and development in Lesotho in the years ahead.

He met with His Majesty King Letsie III, as well as the Deputy Prime Minister Mothetjoa Metsing, the Minister of Trade and Industry Joshua Setipa, and the Minister of Foreign Affairs Tlohang Sekhamane.

The Director-General said:

“Helping Least Developed Countries (LDCs) like Lesotho to compete and benefit from trade is a central part of our work. In recent years, the WTO has taken further steps in that direction, negotiating new trade deals which can help Lesotho’s economic development.

“For example, the WTO’s Trade Facilitation Agreement will help a more diverse group of companies to export by reducing the time, cost and bureaucracy involved in moving goods across borders. For a landlocked country like Lesotho, this diversification could be particularly important. It is very encouraging that Lesotho has ratified this Agreement, and is now laying the foundations for these benefits to become a reality.

“Further important outcomes were agreed at our Ministerial Conference in Nairobi last December. WTO members delivered a set of decisions which can facilitate opportunities for LDCs’ export of goods and services. In addition WTO members agreed to eliminate agricultural export subsidies. This will help to level the playing field in agriculture markets to the benefit of farmers and exporters in Lesotho and other LDCs. In fact, these negotiations were chaired by Lesotho’s Minister of Trade and Industry, Joshua Setipa, whose able leadership was a big factor in this success.

“Lesotho is a small country geographically, but it has a big voice in the WTO. I look forward to continuing to build our partnership in the years ahead.”

During the visit the Director-General also visited a project which benefits from the support of a WTO-sponsored initiative, the Enhanced Integrated Framework. The project aims to build Lesotho’s capacity to produce and market high value fresh fruit and vegetables.

Related News

Economic emergence is the new target for African countries, but how can it be achieved?

As African countries work towards the goal of achieving economic emergence, Daouda Sembene points out that the key challenge is developing a concrete action plan to shape reform.

While embracing the new Sustainable Development Goals last September in New York, a number of sub-Saharan African leaders were reminded of the painful reality that only their region failed to meet the Millennium Development Goal (MDG) of halving the proportion of people living in extreme poverty by 2015.[1]

As African leaders are increasingly shifting their focus now on achieving economic emergence, away from primarily reducing poverty, they may have to draw lessons from their experience with poverty reduction strategies (PRS) to make sure that the new emergence-inspired era will ultimately enjoy a better fate.

Assuredly, there is a strong sense that emergence plans embody clear indications about what policy and reform agendas need to be implemented. Most emergence strategies in sub-Saharan Africa describe clearly what the government intends to do.

Typically, these are underpinned by broadly similar pillars across the region, including the need to boost strong and inclusive growth, strengthen governance and the rule of law, create jobs, promote private sector development, deepen the financial sector, improve competitiveness, and diversify the economy.

However, while emergence strategies provide an answer to the “what to do” question, they generally miss the “how to do it” question, particularly when it comes to addressing political economy impediments to sustained reforms.

Many candidates for emergence usually fail to spell out in a clear and comprehensive manner specific action plans that can deliver their government’s vision. Besides their other policy documents rarely fill out this gap and when they do, they tend to remain silent about how to overcome existing political economy constraints to reforms.

Yet, this is one of the shortcomings of the PRS approach that must be addressed for emergence to become a reality. Indeed, it is well-known that political economy considerations, notably those related to rent-seeking activities, tend to impede reform implementation. For instance, the literature offers extensive evidence that in sub-Saharan Africa competitive clientelism undermines the quality of policymaking and blocks the conditions for economic transformation and better governance.[2]

While the literature may offer useful guidance, no learning experience could potentially be as effective and rewarding for policymakers as a policy dialogue with peers from countries that coped successfully with such challenges.

That is partly the reason why Senegalese officials, in close partnership with the IMF staff, adopted in the recent past a promising peer-to-peer learning initiative, with a view to implementing their Government’s Plan for economic emergence. This involved crossing over the Atlantic and Pacific oceans, reaching out to peers to draw together lessons from our countries’ respective reform experience.

The latest exercise took place in January 2016 when a delegation of Senegalese officials, accompanied by representatives from the academia, civil society, and the central bank headed to Washington to participate in a book workshop attended by peers from Mauritius, Morocco, and Seychelles, in addition to IMF and World Bank staff. The event provided participants with a platform for exchanging ideas and experience about advancing reform agendas in the face of political economic constraints.

It is expected that the workshop will also be the birthplace of an upcoming publication that will eventually provide Senegal and other countries in similar circumstances with additional insights about how best to shape their reform efforts.

Preliminary indications suggest that peer-learning activities are associated with significant payoffs. It has catalysed reform efforts, offered new insights about reform success, and produced new ways of dealing with old issues, notably related to the political economy of reforms and economic competitiveness.

Therefore, peer-learning bodes well for reform implementation in the country and must be pursued.

Dr Daouda Sembene is a Senior Advisor to Senegal’s Minister of Economy, Finance, and Planning. He is a member of the Boards of Governors of the World Bank and the International Monetary Fund, as Alternate Governor for Senegal.

The views expressed in this blog post are those of the author and do not necessarily reflect those of the Government of Senegal, Africa at LSE blog or the London School of Economics and Political Science.

Daouda Sembene will be speaking at LSE on Thursday 17 March alongside Ali Mansoor and Salifou Issoufou at the event The Political Economy of Change: the Case of Senegal.

[1] According to the MDGs Report released last year by the United Nations, all developing regions had met the target by 2011 except sub-Saharan Africa. Ultimately, the rate of extreme poverty in this region was only projected to be cut by just over a third, from 57 percent in 1990 to 41 percent in 2015.

[2] See Africa Power and Politics Programme et al. (2012). The Political economy of Development in Africa: A joint statement from five research programmes.

Related News

Why regional integration is so important for resource-driven diversification in Africa

Natural resources management, particularly in the extractives industry, can make a meaningful contribution to a country’s economic growth when it leads to linkages to the broader economy. To maximize the economic benefits of extractives, the sector needs to broaden its use of non-mining goods and services and policymakers need to ensure that the sectors infrastructure needs are closely aligned with those of the country’s development plans.

In Africa, especially, mining and other companies that handle natural resources traditionally provide their own power, railways, roads, and services to run their operations. This “enclave” approach to infrastructure development is not always aligned with national infrastructure development plans.

In a continent facing massive infrastructure needs, African countries can thus miss out on opportunities to promote the shared use of infrastructure and to strengthen the linkages between extractive resources and the broader economy. Non-mining businesses like farms or food traders in sparsely populated or remote areas, for example, would benefit from shared infrastructure, since railways, roads and electricity are all needed to bring goods to markets.

Regional integration is often seen as less relevant for resource-rich countries, since demand for commodities typically comes from the global market rather than from regional demand. Regional integration in Africa, however, can play a vital role in diversifying economies away from dependence on the export of just a few mineral products; in delivering food and energy security; in generating jobs for the increasing number of young people; and in alleviating poverty and delivering shared prosperity.

The relationship between resources, regional integration and diversification is twofold.

First: Since resource deposits don’t always fit neatly inside the borders of individual countries and tend to span multiple borders (including landlocked countries), trans-boundary mining transport will need to be built to extract and transport the resources. That often has implications for regional integration. Global experience shows that the development of such infrastructure requires strong cooperation and coordination among all parties involved, along with a legal and regulatory environment that allows for the shared use along that infrastructure. Designing and building such infrastructure and a regulatory environment in a multi-country context is, however, very complex: It involves a wide range of political-economy issues that need to be addressed.

Second: Extractives can help diversify economies through linkages to the broader economy. Regional value chains in minerals and metals, for example, will create demand for services and goods that feed in to that value chain. Regional integration is essential here as well, since goods, services and people need to be able to flow seamlessly across borders to reduce costs and to help firms become competitive enough to link to these value chains. The deeper integration of regional markets through the elimination of non-tariff barriers can reduce trade and operating costs. It can also ease the constraints faced by many firms in gaining access not only to demand for their products but also to the essential services and skills that they need as to boost productivity and diversify into higher-value-added areas.

Deepening regional integration among African economies, therefore, provides both opportunities and challenges to the sound management of extractive resources and translating wealth from these resources in to diversified economies and equitable growth. Our recent report, “Breaking out of Enclaves Leveraging Opportunities from Regional Integration in Africa to Promote Resource-Driven Diversification” explores this nexus of extractive resources, regional integration, and economic diversification.

The report looks at how regional approaches can increase the local employment and production effects of extractive-resources projects and discusses some of the regulatory, institutional, and political economy barriers facing African policymakers in achieving regional cooperation.

The analysis is based on three case studies of efforts to create trans-boundary transport corridors anchored by extractive resources: The cases include the extraction of coal in the Nacala corridor in southern Africa; proposals for the exploitation of iron ore in Guinea and Liberia; and the LAPSSET corridor in East Africa that aims to ship oil and gas from South Sudan to ports on the Indian Ocean. These case studies encompass three different sub-regions that vary in their level of regional integration. They are assessed through a framework that organizes the most important policy questions and leads to a number of concrete recommendations for national and regional policymakers.

Through our research and the recommendations provided in the report, we show that regional integration is still relevant for Africa’s resource-rich countries – and that it is more crucial than ever before for diversifying countries’ economies as the global commodity supercycle comes to an end.

Related News

Illegal fishing hurting continent’s fisheries

The best net is the one that catches the most fish, said Kofi Nyamegbe, in a low and steady voice as he stared into the ocean, where lots of fishing boats dotted the horizon.

“We say that all the time but it doesn’t mean anything anymore. There are many boats here, but the nets return empty most of the time,” said Nyamegbe.

Nyamegbe is among some 25,000 people who reside in the fishing village of Moree, on Ghana’s Cape Coast, about 120 kilometres from the capital Accra. He has been fishing for the past eight years, but the nets no longer return enough fish to sustain his family.

Ghana’s coastline is about 500km long, providing employment to at least 10 per cent of the population of about 27 million people.

“That translates into so many boats, all competing for the few fish,” said Farnyi Kweigya, Moree’s chief fisherman.

The exact amount of fish caught in Ghanaian waters is unknown, but the African Union Inter Bureau for Animal Resources (AU-IBAR) says Ghana is among the highest fish consuming countries on the continent, with a per capita consumption of 26 kilogrammes per person per year, against a global average of 10-19 kilogrammes.

The East African region has some of the lowest consumption rates, estimated at just 3 kilogrammes per person, per year.

“In Kenya, we eat 3.5 kilogrammes per person, which is ridiculously low,” said Prof Micheni Ntiba, the Principal Secretary in the State Department of Fisheries in the Ministry of Agriculture.

In the 1998/99 fishing season, Ghana had its highest fish harvest of 200,000 tonnes. Today, the catches barely hit 10 per cent of that figure.

“It means that our fish stocks are collapsing,” said Kofi Agbogah, a fisheries conservationist.

The United Nations Food and Agriculture Organisation (FAO) estimates the global marine fishing industry produces some 67 million tonnes of fish annually worth between $100 billion and $200 billion.

Africa’s coastal waters produce only 4.6 million tonnes of fish annually, valued at $4.9 billion. However, 52 per cent of the fish stock is fully exploited, 8 per cent is depleted, 19 per cent overexploited while 1 per cent is recovering from depletion, data from both the FAO and the AU-IBAR shows.

Key to the near collapse of the continent’s fisheries is the illegal, unregulated and unreported fishing, which costs the continent billions of dollars in lost revenue.

The World Bank’s Africa Programme for Fisheries reports that some 11-26 million tonnes of sea food is caught illegally every year, worth between $10 billion and $23.5 billion.

The West African coast is said to be the most affected by illegal fishing, with 40 per cent of total catches falling in that category.

In East Africa, Kenya’s coast has become quite vulnerable in recent years to illegal fishing, especially with regard to tuna fish. The government reports that the country loses at least $118 million annually due to illegal fishing and fish poaching.

“The worst thing is that we don’t have the capacity to sufficiently patrol our waters and protect our fish,” said Prof Ntiba.

Tuna is one of the most illegally caught fish in the world, estimated at seven million tonnes globally, with a value of $10 billion, data shows.

Kenya’s territorial waters lie within the South West Indian Ocean, the richest tuna belt, with the fishing season running from May to July.

“The demand for tuna is high, mostly in Europe and Asia,” said Prof Ntiba.

Although Africa often cries foul over illegal fishing, a number of conservationists believe that governments are abetting illegal activities, because when an unauthorised vessel is arrested off the African coast, it is quickly freed without any charges, as was the case recently in Nigeria.

Then there is Somalia, which has Africa’s longest coastline, extending some 3,300 kilometres where Illegal, unreported, and unregulated (IUU) fishing is exacerbated by the fact that there are no structures.

Somali factor

“It is difficult to say exactly how much fish is lost in Somalia due to the lack of structures to keep track of the numbers,” said Richard Trenchard, the FAO country representative for Somalia.

“The potential of the ocean to the Somali economy is $400 million annually. With a coastline that long, Somalia has a rich marine resource base, but they have serious challenges with overfishing.”

Illegal, unreported and unregulated fishing is carried out mostly by Chinese and European Union vessels, according to a report published in May last year by Greenpeace Africa, an organisation that advocates for environmental protection.

Kenya has licensed nearly 40 purse seiners in the past four years to fish in its waters. Of these, 14 are Spanish and 13 are French. In 2014 – the last year complete data is available – 35 foreign purse seiners took annual licences. Twenty five of these were from the European Union.

Kenya requires reporting – specifying the cargo on board, time and entry or exit position – as a condition of a licence for foreign vessels operating in its territorial waters.

The reporting is done at the State Department of Fisheries via the Director of Fisheries whenever entering and leaving Kenya’s exclusive economic zone (EEZ) – a sea zone prescribed by the UN Convention on the Law of the Sea.

Kenya also requires licensed foreign vessels to submit weekly catch data reports, but there are concerns that the reporting is not done accurately, purposefully concealing any illegal activities in its waters.

“I think where Kenya and a few other African countries go wrong is in reporting; fisheries officers are required to get on board those foreign vessels for a specific period of time to observe what they are doing,” said Edward Kimakwa, the fisheries programmes officer with WWF Kenya.

“Many countries fail to put their officers on board, which means then it becomes hard to verify if what is reported is true.”

Tanzania has licensed between 18 and 38 purse seiners to fish annually in their EEZ in the past six years. Of these 14 are Spanish and 13 French. In 2014, 33 foreign purse seiners took annual licences. Most licences are issued annually.

Payment of these licences is done per tonne of fish caught. In Kenya’s case, payment of royalties is stipulated in the Fisheries Act, but the method is not specified which is seen as loophole through which revenue leaks.

Between 2012 and 2014, though, purse seiners were charged $50,000 for a licence, a fee that has been reduced to $30,000. Kenya says the reduction is intended to make the country competitive in the light of the piracy threats in the Indian Ocean waters.

“This fee is low. But a Fisheries Management Bill before parliament proposes higher fees,” said Prof Ntiba.

Remedies

So what countries are doing to save their fish stock?

A number of African governments have made strides towards saving their fishing industries. Before 2,000, the Ghanaian fisheries department for example, was only interested in ensuring that the fishermen caught the most fish, hence the phrase “The best net is the one that catches the most fish.” But this brought more problems due to overfishing.

Last year, the Ministry of Food and Agriculture started registering the fishermen. But because most of them are small scale, it is difficult to track them down. Through the village chief fishermen, the government also conducts training on sustainable fishing practices.

There was also a plan to regulate the kind of nets the fishermen use so that the wrong species of fish are not caught, but the plan was shelved, because the fishing gear is linked to tribes and cultural practices, and therefore outlawing one gear would disadvantage an entire community.

In Southern Africa, the government is working with the fishermen because they know who the illegal fishers are.

“They are the eyes and ears in waters and it has worked excellently,” said FAO’s Mr Trenchard.

In Kenya, the government is constructing a monitoring control and surveillance Centre in Mombasa. This centre is expected to be operational by the end of the year. The country is also acquiring an off shore patrol vessel that will enable better tracking of illegal vessels in Kenyan waters.

“Kenya is also training its fisheries officers in offshore monitoring so that when the centre is up and running, the officers know exactly what to do,” said Mr Trenchard.

Last year, the Fisheries Management and Development Bill, which seeks stiff penalties for vessels caught fishing illegally in Kenya’s EEZ was formulated. The Bill is currently before parliament. Also, a Tuna Fisheries Development Management Strategy was launched in 2014, to enable Kenya exploit its stocks.

The only tuna fish processing plant in East and Southern Africa was in Mombasa and it shut down in June last year due to idle capacity.

Tanzania, on the other hand, has amended the Tanzania Deep Sea Fishing Authority Regulations in line with the Maputo Declaration, which not only enables it keep better track of its fish, but also better manage its stocks.

In the case of Somalia, it ratified the 2009 FAO International Port State Measures Agreement in November last year, which compels countries to eliminate, deter and prevent IUU, said Mr Trenchard.

Only 21 countries have ratified the agreement. Most African countries are yet to do so.

For Kenya, if the Fisheries Bill becomes law, it will enable the country to ratify and domesticate the provisions of the agreement.

Fish importing countries such as those in the European Union have laws that blacklist countries that fail to take action on illegal, unregulated and unreported fishing.

The EU is among the world’s biggest importers of fish and also among the biggest owners of distant water fishing vessels, with at least 15,000 registered to fish in such waters. It uses a card system – yellow and green – to decide whether a country should be blacklisted.

Ghana for instance, exports 128 million euros worth of fish to the EU every year, but in November 2013, it was yellow carded for failing to take sufficient action against IUU. Within two years, Ghana strengthened its legal framework and set punitive measures against IUU. In October last year, it received a green card and is back to exporting to the EU.

Prof Ntiba said African governments have the political will to strengthen the fishing industry.

“Look at the East African Community for instance. We have made great strides on the Lake Victoria region by working together. Each country is not only reviewing its fisheries laws but we are developing an EAC strategy that will see us work on fisheries as a block,” he said.

“Even at the AU level, ministers responsible for fisheries have held several meetings and are working on a continental strategy that will ensure that we collaborate in patrolling our waters, such that a vessel that breaks the law in one part of Africa does not run to and hide in another part of the continent,” he added.

According to WWF-Kenya’s Mr Kimakwa African countries need to learn from each other in order to strengthen the industry.

“Take Namibia for example which is using air surveillance systems. It is a small country yet it is winning the war on illegal fishing,” he said.

With fish being a big player in the global economy, the World Trade Organisation issued a ministerial statement on fisheries last year to scrap fishing subsidies, because they contribute to the over-exploitation of fish resources.

The ministerial was signed by 29 countries in the least developed regions of the world.

Related News

How ICT-driven concept can boost Africa’s trade ranking

African countries must join others around the world in adopting the National Single Window Environment, an ICT-based concept, to eliminate the bureaucracy posing a challenge to trade processing in the region, the managing director of West Blue Consulting, Valentina Mintah has said.

Speaking at a workshop on single window organised for Nigerian and Ghanaian journalists at the Royal Senchi Resort, Akosombo, Ghana, she declared excessive bureaucracy as the most severe constraint to trade processing in Africa.

Mintah said there was plenty of room for improvement for Africa countries if only they could adopt the single window concept in trade processing, noting that Swaziland ranks 1st in Africa and 30th in the world out of 189 countries on the World Bank trading across border index, with Zimbabwe ranking 100, Ghana 171 and Nigeria 182.

If African countries and stakeholders, according to her, could join forces and pursue the goals of the national single window, a concept developed by the United Nations Economic Commission for Europe (UNECE) in 2005, to simplify, harmonise and standardise international trade procedures and associated information flows between trade and government and within government itself, it would be relatively easy to create a solid foundation which will enable the continent achieve the 50 percent better, faster and cheaper trade across border indicators.

The single window, according to the UN Centre for Trade Facilitation and Electronic Business (UN/CEFACT), is “a facility that allows parties involved in trade and transport to lodge standardized information and documents with a single entry point to fulfil all import, export and transit related regulatory requirements.”

Mintah, who is the lead consultant in the implementation of the Nigeria’s single window concept, said “so matter how much is done as individual institutions and countries in addressing these bottlenecks, it cannot be compared with the positive and timely impact that can be achieved with the joined up efforts of all stakeholders.”

Speaking further, the expert who now presently leads the implementation of the Ghana single window concept, added “that African importers and exporters remain uncompetitive in the global business arena is largely attributable in part, to the number of days it takes to complete import and export processing and their attendant costs.

“The collaboration of sister countries, Ghana and Nigeria on trade facilitation activities will bring about further gains in our quest for increased inter African trade, with the realisation of efficient processes and movement of goods.”

The single window concept she said, helped countries to transition from a culture of delays and high costs of doing business to a culture of faster, simpler, automated and predictable means of processing imports, exports and transit trade.

According to her, many countries around the world are currently focusing on implementing major trade facilitation reforms to enhance their competitiveness and increase their participation in global economy, pointing out that Africa should not be left out.

Since its inception in 2005, single window has been implemented in over 70 countries and the concept is now seen by the World Bank and many other development agencies as a key tool to enhance the trade and economic competitiveness of a country.

Mintah equally defined a single window as “an organic concept focusing on the way we do business both within government and between government and business, ensuring the maximum integration, harmonization and standardization of the process, procedures and related information flows within the international trade environment. She said it was essentially driven by the principle of a partnership between trade and government for economic development and prosperity of a country.

She described the single window as not just an IT software to be procured but a concept that must be organically implemented according to individual country’s needs, adding that in implementing the single window, countries should not stand still at any point, but should see continuous innovation as key to the success of the concept.

“You can’t stand still in this environment, everybody is innovating and competition is high… so many elements come into play in this environment,” Mintah stated, adding what Nigeria had done were only some of the ingredients needed for the full meal to be cooked.

Related News

Liner shipping: Is there a way for more competition?

With around 80 per cent of global trade by volume and over 70 per cent of global trade by value carried by sea, and with these shares being even higher in the case of most developing countries, maritime transport, including liner shipping, remains highly important for international trade and the global economy.

To ensure stability in the sector, in various jurisdictions around the world, liner shipping conferences – arrangements among ocean carriers allowing for freight rate fixing – have been exempted from the application of competition laws over the years. Many of these jurisdictions confer exemptions, under similar conditions also to consortia and strategic alliances – arrangements among ocean carriers that do not involve freight rate fixing.

This paper aims to provide an overview of recent and potential developments related to competition and cooperation in liner shipping.

A number of reviews and studies conducted over the last decades by organizations and individual countries have suggested that liner shipping may not be unique, as its cost structure does not differ substantially from that of other industries, or at least not sufficiently to justify that it needs to be protected from competition, by being exempted from competition laws.

As a result, such exceptions have gradually come under review and have narrowed in scope, giving more space to pro-competition, non-ratemaking agreements.

Therefore countries are encouraged to establish appropriate and harmonized regulatory systems to support and monitor such agreements.

Carriers may continue to collaborate to achieve operational improvements, while the competition authorities ensure that the competition in the market is sufficient and shippers benefit from eventual cost savings. At the same time, enhancing cooperation between national competition agencies, sharing of information among them, and other relevant measures shall be encouraged.

Introduction

Although the content and practice of competition laws, including those applicable to liner shipping, vary in different countries, their purpose is “to control or eliminate restrictive agreements or arrangements among enterprises, or mergers and acquisitions or abuse of dominant positions of market power, which limit access to markets or otherwise unduly restrain competition, adversely affecting domestic or international trade or economic development”.

Throughout its history, liner shipping, the business of offering regular time scheduled ocean shipping services in international trade, has enjoyed exemptions from the effect of certain competition rules and, as a result, conferences among oceans carriers, allowing for freight rate fixing, have been permitted. The main reason for this practice has been the belief that it was justified by the specific economic problems faced by liner shipping as compared to other industries. These include unusually high fixed costs, very large initial capital investment, other large non-cargo costs, overcapacity, etc. As a result, it was argued that without collective freight rate fixing, open and unrestrained competition would lead to “destructive” competition, instability of prices and undesirable oligopoly.

Following discussion in many countries and regional organizations as to whether exemptions from competition rules, historically enjoyed by liner conferences, are still justified, there has been a tendency during the last decade towards review and narrowing of the scope of such exemptions. In addition, there appears to have been a shift of emphasis among shipping lines away from the traditional liner conferences, and towards the establishment of alliances and other forms of efficiency-enhancing operational types of agreements. In these circumstances, carriers continue to collaborate to achieve operational improvements, while the competition authorities ensure that there remains sufficient competition in the market so that eventual cost savings are passed on to the shippers.

This paper will briefly examine the rationale behind the exemptions from the effects of competition laws that have been historically granted to liner shipping cooperative arrangements, the legitimacy and continued justification for such exemptions, as well as applicable instruments, negotiations, and relevant legislative developments. It will continue with a brief description of the recent global alliances among major shipping lines, related considerations, potential legal uncertainties and the way forward.

Related News

Business leaders, UN Member States and civil society agree: Gender equality critical to economic development

The UN Global Compact and UN Women organize the Women’s Empowerment Principles Annual Event

Recognizing gender equality as a fundamental human right, central to driving the global economy and achieving the recently adopted Sustainable Development Goals (SDGs), business leaders joined UN Member States and civil society organizations at the Women’s Empowerment Principles (WEPs) Annual Event. The event focused on the multiplier effect of empowering women and girls in advancing all development issues and the enormous opportunity for business to lead on promoting gender equality.

In the keynote address, His Excellency Mr. Luis Guillermo Solís Rivera, President of Costa Rica urged: “The time is right. International consensus has been reached, at Beijing+20 and in Agenda 2030, about the importance of women’s empowerment in the global sustainability agenda.” He emphasized that “a society that puts gender equality at its forefront not only grows economically but becomes more human.”

UN Secretary-General Ban Ki-moon explained, “We cannot achieve our Sustainable Development Goals without securing the full and equal rights of half of the world’s population, in law and in practice.” He noted that “when companies invest in women, they see a range of benefits and a return on investment. It is clear that gender equality is a business issue.”

The Women’s Empowerment Principles – a partnership initiative of the UN Global Compact and UN Women – provide companies with an integrated and proven approach to unlocking the power of women in business and society. It is the largest business-led gender equality initiative in the world endorsed by more than 1,100 CEOs from 80 countries. Held in conjunction with the 60th Commission on the Status of Women, this year’s annual event spotlighted companies that are implementing the WEPs to achieve the SDGs, step up action, and find innovative ways to partner and advance gender equality.

Phumzile Mlambo-Ngcuka, Executive Director of UN Women, stressed the importance of partnerships and collaboration with business to achieve gender equality, stating: “The engagement and commitment of the private sector to gender equality are essential to reaching the Agenda 2030 goals and aspirations. Gender equality and sustainability must be integral to every business plan and strategy.”

Lise Kingo, Executive Director of the UN Global Compact told participants, “We have not reached the tipping point on gender equality. It’s time that we have honest conversations about what is really holding women back. We need to end bias, both overt and unconscious. We must recognize that gender equality is not just a women’s issue – it’s a men’s issue, a family issue, a community issue and a business issue.”

To help accelerate progress, the development of a new gap analysis tool was announced by the Inter-American Development Bank, the UN Global Compact and UN Women, along with supporting partners from business and government. The tool will assist companies in identifying gaps in gender equality and scale up implementation of the Women’s Empowerment Principles.

Five CEOs Recognized for Leadership on Gender Equality

Since 2013, the Annual Event has included the presentation of the Women’s Empowerment Principles CEO Leadership Awards, acknowledging business leaders for championing gender equality and implementing the principles, in particular Principle One which urges CEOs to lead by example.

Conferring the awards, Joseph Keefe, Co-chair of the WEPs Leadership Group and President and Chief Executive Officer of Pax World Funds said: “The WEPs are an effective tool to advance women in business and society. The WEPs CEO Leaderships Awards bring to life concrete actions and measurable impacts that are changing workplaces, marketplaces and communities. As a previous Awards recipient, I know that this prestigious award gives companies encouragement to press forward with this important work.”

The 2016 WEPs CEO Leadership Award recipients are:

-

Jean-Paul Agon, Group Chairman and Chief Executive Officer, L’Oréal (France) – Benchmarking for Change WEPs CEO Leadership Award

-

Federico Bernaldo de Quiros, Chief Executive Officer, Toks Restaurantes (Mexico) – Community Engagement WEPs CEO Leadership Award

-

Lance Hockridge, Chief Executive Officer, Aurizon (Australia) – Cultural Change for Empowerment WEPs CEO Leadership Award

-

Michael Landel, Chief Executive Officer, Sodexo (France) and Janet Awad, Regional Chair of Latin America and Country President, Sodexo Chile (Chile) – 7 Principles WEPs CEO Leadership Award

-

David Sproul, Senior Partner and Chief Executive, Deloitte UK (United Kingdom) – Business Case for Action WEPs CEO Leadership Award

About the Women’s Empowerment Principles

Launched in 2010 the Women’s Empowerment Principles – Equality Means Business has grown to become the largest business-led gender equality initiative in the world endorsed by more than 1,100 CEOs from 80 countries. The Principles highlight that empowering women to participate fully in economic life across all sectors and throughout all levels of economic activity is essential to build strong economies; establish more stable and just societies; achieve internationally agreed goals for development, sustainability, and human rights; improve quality of life for women, men, families and communities; and propel business’ operations and goals.

Related News

Transport sector joins fight against wildlife crime

The global fight against wildlife crime received another major boost with the signing of a declaration at Buckingham Palace in London committing the leaders of the global transportation industry to take concrete steps to tackle wildlife trafficking.

Leaders of 40 airlines, shipping firms, port operators, customs agencies, intergovernmental organisations and conservation charities from around the world signed the historic Declaration of the United for Wildlife International Taskforce on the Transportation of Illegal Wildlife Products at the palace.

“The poaching crisis is bringing violence, death, and corruption to many vulnerable communities and threatens to rob future generations of their livelihoods,” said the Duke of Cambridge. “But this crisis can be stopped. By implementing these commitments, the signatories of the Buckingham Palace Declaration can secure a game changer in the race against extinction. I thank them for their commitment and I invite any other company in the industry to sign up to Declaration and play their part in the fight against the poaching crisis.”

The Buckingham Palace Declaration is the result of a year’s worth of meetings, research, and coalition building by the United for Wildlife Transport Taskforce, convened by The Duke of Cambridge and chaired by Lord Hague of Richmond.

Transport representatives on the Taskforce include companies and organisations based in China, USA, UAE, Kenya, the UK and Denmark.

“The Buckingham Palace Declaration is a major achievement as the transport sector has a key role in tackling this destructive trade. This landmark agreement sets out clear actions the transport industry can take to stop criminals from exploiting their legal transit routes,” said Glyn Davies, Conservation Director, WWF-UK.

“We applaud the 40 companies that have already signed this landmark agreement and encourage other companies to sign up too. Together we can stop this devastating trade.”

The Declaration commits signatories to eleven steps that will raise standards across the transportation industry to prevent traffickers from exploiting weaknesses as they seek to covertly move their products from killing field to marketplace.

The commitments focus on information sharing, staff training, technological improvements, and resource sharing across companies and organisations worldwide. They will also see the world's leading transportation firms assisting those in poorer nations who are in need of expertise and new systems.

“WWF is proud to be part of this dynamic United for Wildlife Taskforce and looks forward to continuing to work with the signatories in tackling this devastating trade in the parts of threatened animals,” added Davies. “Now we have the Declaration, efforts must focus on implementing the much needed actions to help end this illegal trade. Only by making it harder for criminals can we stop the trade.”

The work of the United for Wildlife Transport Taskforce has been strongly supported not only by the transport sector but a number of intergovernmental agencies including the World Customs Organisation, the United Nations Development Programme and importantly CITES – the world's regulatory instrument on trade in endangered species.

“I want to thank everyone who has been part of this unprecedented initiative and I ask them all to sustain the momentum we have established over the past 15 months,” said Lord Hague. “It is nearly too late to save our rhinos, elephants, tigers, and other iconic species, but it is not quite too late. It will require our combined efforts, resolve, and intensified determination and that is what this Declaration is about.”

The commitments in the Buckingham Palace Declaration include:

-

Developing information sharing systems for the transport industry to receive credible information about high risk routes and methods of transportation;

-

Supporting a secure system for passing information about suspected illegal wildlife trade from the transport sector to relevant customs and law enforcement authorities; and

-

Notifying relevant law enforcement authorities of cargoes suspected of containing illegal wildlife and their products and, where able, refuse to accept or ship such cargoes.

Related News

tralac’s Daily News Selection

The selection: Wednesday, 16 March 2016

African Transformation Forum: closing address by President Kagame

Africa Pension Funds Network: update (AfDB)

Discussions about the WAEMU are often limited to questions about the degree of overvaluation of the real effective exchange rate and the level of remuneration of the central bank’s foreign exchange reserves. These are valid questions, especially as they relate to competitiveness and the opportunity cost of leaving foreign exchange reserves at the French Treasury. But they are not the only ones. In this note, we explore a number of other questions to provide a greater insight on the nature of regional economic communities in Africa. [The authors: Amadou Sy, Mariama Sow]

EALA passes key report on governance and project performance issues in EAC institutions

The objectives of the assessment were to assess whether governance and management systems of the institutions are good enough to guarantee performance and proper discharge of duties. It further sought to establish the implementation of the Assembly’s recommendations, strengthen governance and management systems of EAC Institutions and to establish extent to which the said institutions apply modern governance and management of applied technologies.

SADC Council of Ministers: briefing (SADC)

On the Tripartite Free Trade Area, Council urged member states to expedite conclusion of outstanding Phase 1 negotiation issues, which include rules of origin, trade remedies, and finalization of tariff negotiations in order to fully operationalize the Tripartite Free Trade area and endorsed the proposal by the Tripartite Task Force to convene a Tripartite Council of Ministers, preceded by the Sectoral Ministerial Committee meeting on 9-14 May 2016 to facilitate unlocking of all outstanding Phase 1 issues; and directed the Secretariat as current chair and coordinator of the Tripartite Task Force to facilitate the legal scrubbing of all completed Annexes before the proposed Sectoral Ministerial Committee; and mobilization of resources for Phase 2 TFTA issues.

Enhancing India’s engagement with the Southern African Development Community (Export-Import Bank of India)

During the last ten years, India’s total trade with the SADC countries has witnessed over eight-fold increase from $3.7bn in 2004 to $29.6bn in 2014. While India’s total exports to SADC has risen from $1.6bn in 2004 to $15bn in 2014, depicting a nine-fold rise during the period, India’s total imports from SADC have also risen, although at a slower pace, from $2bn to $14.6bn, showing a seven-fold rise. India’s trade balance with SADC turned into a surplus of $0.4bn in 2014, after witnessing a deficit for six consecutive years.

The increasing importance of India as SADC’s trading partner can be assesses from the fact that India accounts for a respectable 7.4% of SADC’s global imports in 2014, which was significant improvement compared to 2.1% recorded in 2004. Further, India accounts for around 7% of SADC’s total exports, up from 3.3% in 2004, depicting the rising importance of India in SADC’s trade configuration. The importance of the SADC region can also be gauged from the fact that the region accounted for 4.7% of India’s global exports in 2014, up from 2.2% recorded in 2004. India’s imports from SADC region, as a percentage share of India’s global imports, accounted for 3.2% in 2014. The period also witnesses a rise in the importance of SADC in India’s global trade configuration. [Download]

India-Africa trade relations: the way ahead (Economic Times)

While the two-way trade and investment ties have deepened, the future potential is much higher. With the changing architecture of global trade agreements, the focus is shifting towards creating value-chain and investment-led trade. The Indian private sector can leverage available institutional mechanisms to further deepen its trade and economic footprint in African nations. The second important instrument is the EXIM Bank/Government of India's Lines of Credit (LoC). Undoubtedly, LOCs have helped Indian companies enter the African market as well as expand their footprint in the continent. This is evident from the fact that LOCs to African countries constitute 60 per cent of all LOCs. However, there is still a gap between LOC commitments and actual disbursement, which needs to be bridged. [The author, Chandrajit Banerjee, is the Director General of the Confederation of Indian Industry]

India’s exports contract for 15th month on tepid demand (Livemint)

The trade deficit narrowed further from its previous month’s low, data released by the commerce ministry showed. Exports shrank 5.66% in February and imports contracted 5.03%, leaving a trade deficit of $6.5 billion. Only eight out of the 30 import items reported growth in February, compared with 10 in January. Among the major items, the import of coal (-16.85%), petroleum (-21.9%), chemicals (-1.05%), iron and steel (-12.46%), transport equipment (-7.9%) and gold (-29.5%) contracted, while the import of precious stones (41.2%) and machinery (50.2%) shot up. Shipments of 14 out of the 30 top export items grew in February, against 13 in the previous month. Among the major items, export of gems and jewellery (11.2%), pharmaceuticals (8.8%) and chemicals (4.5%) increased, while export of engineering goods (-11.2%), readymade garments (-0.72%) and petroleum products (-28.3%) fell.

UNCTAD Investment Policy Monitor: latest edition

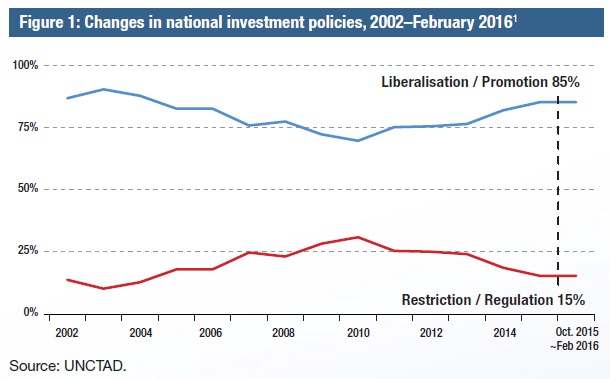

The Monitor finds that 25 countries took 41 investment policy measures between October 2015 and February 2016. The share of liberalization and promotion measures was 85% - broadly in line with last year's average. These policy measures show a continued move towards improving entry conditions, reducing restrictions and facilitating foreign investment. In terms of policy types, measures related to "entry/establishment" were predominant. UNCTAD found that countries concluded ten new international investment agreements, bringing the total number of IIAs to over 3280 at the end of February 2016. The new treaties are five bilateral investment treaties and five "other IIAs", including the Trans-Pacific Partnership. At least six IIAs entered into force.

Chinese presence in real estate in South Africa and Mauritius (CCS)

Preliminary statistics from research centres, and media and public discourses highlight South Africa and Mauritius as two of the most popular destinations of Chinese real estate investment. This paper investigates the substantiality of these hypotheses and assesses the impact Chinese real estate activities have on the socio-economic environment of the respective two countries. It also provides policy propositions that would ease these prospective challenges to the two societies. [Africa-China relations: Lagos conference (Yale)]

Botswana: new trade portal makes import, export easier, cheaper (World Bank)

The Botswana Trade Portal is a web-based database system, which makes all cross-border trade regulatory information available at a stroke of a key. The information includes all laws, prohibitions, restrictions, technical standards, the entire commodity classification and tariffs, all procedures for license and permit application and clearance, copies of all forms as well as plain language instructions. The trade portal also enables traders to see, in response to a single query, all the obligations they need to comply with to import or export a specific good.

Namibia: the Annual Trade Statistics Bulletin 2015 is available for download

South Africa: Reserve Bank Quarterly Economic Review is posted

South Africa: MPs question viability of Congo hydro project (Business Day)

MPs on Tuesday questioned the country’s substantial investment in the Grand Inga hydroelectric scheme, citing political instability in the Democratic Republic of Congo. SA is poised to pump more than R64bn into the ambitious scheme to transmit about 2,500MW from the DRC to a power station in Limpopo.

Closer look at South African pork market shows opportunities (National Hog Farmer)

According to USDA estimates, South Africa is the world’s 20th largest pork producer at 245,000 mt per year. South Africa imported about 38,500 mt of pork in 2015, valued at $81.8 million, with Germany, Canada and Spain being the primary suppliers. This was an increase of 55% in volume and 36% in value from 2014, though still down slightly from the peak volume level of 2011 (41,371 mt) and the peak value level of 2012 ($98 million). With US pork re-entering the South African market after a significant absence, displacing existing suppliers will present a challenge — especially considering the access limitations that remain in effect. However, US pork has achieved success in markets with similar import restrictions — Australia, for example, is currently the seventh-largest destination for US pork.

Zambia: value chain, jobs diagnostics project launched (World Bank)