Search News Results

Putting trade and investment at the center of the G20

It might not have made the leading global headlines but, three weeks ago, there was a significant new development in global governance of trade and foreign investment. In Beijing, China convened the first meeting of a new working group in the G20 to pursue initiatives in these areas: the G20 Trade and Investment Working Group (TIWG). Over two days, officials from G20 members and invited governments, along with the World Bank Group and other international organizations, discussed the future direction of trade and investment in the G20.

This is a promising step. There is no doubt that the G20 can have an impact in this area. The G20 accounts for three-quarters of world trade; half of global inward Foreign Direct Investment (FDI) and two-thirds of global outward FDI; and 80 percent of global output. Actions taken by the G20 also have a clear impact on developing countries outside the G20, with around 70 percent of non-G20 developing-country imports coming from the G20 countries, and around 80 percent of those countries’ exports directed to the G20. However, the G20 has yet to deliver its full potential on trade and investment.

In the wake of the financial crisis and the elevation of the G20 to a leaders-level forum, the group emphasized immediate post-crisis recovery, as well as such pressing issues as financial regulation and macroeconomic stability. Attention has since shifted to the need to restore growth in a still-weak global economy, defining the achievement of “strong, sustainable and balanced growth” as a key priority for the G20.

Despite efforts by different chairs of the G20 to raise the profile of trade and investment in this context, discussions have generally produced generic statements, such as the exhortation to complete the WTO Doha Round. The results of this approach have been mixed, to say the least. There have, however, been positive exceptions. In particular, the pledge on protectionism made at the G20 Summit in 2008 was followed by the decision to give some power to international organizations to monitor trade and investment policies by G20 members. The G20 has helped prevent a major surge in protectionism, which damaged growth prospects during previous times of economic crisis. Nevertheless, the protectionism focus has been a “defensive” act aimed at preserving existing openness, rather than looking in a more positive sense toward the ways that trade and investment policy actions can contribute to much-needed global growth.

The working mechanisms for trade and investment in the G20 have been partly responsible. Other issues in the G20 – notably the Framework Working Group, which oversees the growth agenda – have a clearer structure, defined targets, and mechanisms for monitoring and evaluation, backed by analytical input from international organizations. Reforming the way the G20 operates on trade and investment will present challenges, but the approach of the Chinese presidency has been that an enhanced structure is needed if the group seeks to exert its role of political leadership and policy direction in these areas.

Although discussions are continuing, the working group that met three weeks ago in Beijing covered a lot of ground, from the mechanics of discussing trade and investment in the G20, to the future of the multilateral trading system, to investment policy, to global value chains, to reducing trade costs. G20 members themselves drive the process, but the World Bank Group and other international organizations have an important role to play, providing independent analysis of potential policy options, as well as data and expertise to support monitoring and evaluation. For example, in the area of trade costs, we maintain a database along with UNESCAP that tracks the evolution of trade costs since 1990, as well as a number of indicators on logistics performance, trading across borders, temporary trade barriers, services trade restrictiveness and other determinants of trade costs. This wealth of information could have a valuable role in helping the G20 shape its action on trade costs.

The establishment of the Trade and Investment Working Group was a good first step in putting these policy areas at the center of the G20 agenda. We at the World Bank Group will be doing what we can to support this effort – and to ensure that it has the greatest possible impact on the global economy and the prospects of developing countries.

Related News

New Bank report finds skills, infrastructure and business landscape key to achieve shared prosperity in Mauritius

The rise in income inequality combined with lagging shared prosperity indicators have adverse impacts on relative poverty in Mauritius, says a World Bank report launched on 18 February. The report, titled ‘Inclusiveness of Growth and Shared Prosperity’, analyses Mauritius’s growth pattern of the past decades as well as existing opportunities to accelerate progress toward achieving inclusive growth and shared prosperity.

“We believe Mauritius has what it takes to achieve its ambition of becoming a high income country with the implementation of the right set of reforms,” said Mark Lundell, World Bank Country Director for Mauritius, Mozambique, Madagascar, Seychelles, and Comoros. “Reaching high-income status will imply a careful review of the country’s economic model. This includes the ability to improve the labor force skills set, develop infrastructure, and further improve the business environment to attract FDI and generate domestic investment.”

The nature of the economic changes of the 2000s associated with the deterioration of the traditional primary sectors led to an increase in income inequality, which impacted negatively on shared-prosperity indicators in the country. Furthermore, incomes of the bottom 40 percentile of the population deteriorated in relative terms. The report concludes that economic growth and declining inequality are equally important for the reduction and possible eradication of poverty in Mauritius.

“Inclusiveness of growth remains the main challenge for the current growth pattern in Mauritius,” said Victor Sulla, World Bank Senior Economist and main author. “Micro-simulation analysis suggests that reducing and eventually eradicating poverty in Mauritius will depend on a two-fold combination of policies: first, lower unemployment and increased productivity, and second, improved targeting and efficiency in social protection.”

Policies designed to upgrade infrastructure, support research and development and innovation, advance public-sector efficiency, and further improve business environment are deemed key to boost productivity. The report suggests that the labor market needs to foster flexibility and reward higher productivity. Besides, skills mismatch grew by 30 percent during the years 2000s, signaling an urgent need for policies to support high-tech and services-oriented sectors. Educational reforms are therefore needed to provide people with the appropriate and relevant skills needed in today’s Mauritius.

The report further suggests the need for public-sector reforms to improve accountability at all levels and improve planning, procurement, and management processes across the system. Efficient country-level monitoring and evaluation systems could be developed to further support evidence-based policymaking. Reforms in public enterprises also have the potential to create fiscal space for productive spending.

» Download: Mauritius: Inclusiveness of Growth and Shared Prosperity (PDF, 8.07 MB)

Related News

Africa far from sustainable energy for all, but showing signs of progress

Energy underpins every aspect of economic development. The world acknowledged that by adopting a dedicated UN Sustainable Development Goal (SDG 7) that aims to ensure access to affordable, reliable, modern and sustainable energy for all by 2030. Africa lies at the heart of that objective.

Although it has long been the least electrified continent, Africa is showing signs of significant change. At the continent’s annual Energy Indaba event, the World Bank shared the most recent evidence of Africa’s progress towards SDG7 and stimulated a discussion about Africa’s prospects for meeting the new global targets.

As of 2012, about 35% of Africans had access to electricity, up from 32% in 2010, according to the “Progress Toward Sustainable Energy: Global Tracking Framework 2015” report. In fact, in as many as 19 African countries less than one in five people had access to electricity in 2012.

Some countries are making meaningful progress. Ethiopia, Nigeria and South Africa were among the fastest moving countries globally in terms of expanding electrification from 2010-2012. Countries like Mali, Rwanda and the Democratic Republic of Congo expanded electrification more rapidly than their own populations are growing, and bold targets and electrification programs have been adopted in countries like Kenya and Rwanda.

Yet overall expansion of electrification in Africa has barely kept pace with population growth in the same period, in sharp contrast to South Asia where electrification grew four times as fast as population. In order to reach SDG7, Africa will need to electrify over 60 million people each year, more than double its current performance of 24 million.

“What this shows is that universal access by 2030 may not be achievable using conventional approaches, yet still remains within reach as long as we focus on providing basic – but meaningful – forms of access,” said Aaron Leopold, Global Energy Advocate with Practical Action. “The evidence shows that many of the human development impacts of electrification are achievable with relatively modest amounts of electricity consumption.”

Depending on the tier or service package provided, the cost of reaching universal access to energy can vary from US$1 billion a year for a simple solar lighting and phone charging solution to $37 billion a year for high-end, round-the-clock grid electricity; an intermediate tier that supports a number of basic appliances would run to $8 billion per year. So countries must also determine what level of access makes sense to try and achieve by 2030, and how that could differ for urban, peri-urban and rural areas.

In contrast, Africa has barely advanced on clean cooking in recent years. The absolute number of Africans cooking with solid fuels such as firewood and dung actually increased from 708 million to 747 million, showing that expansion of access to clean cooking fuels did not keep up with the overall growth in population. In fact, Africa will need to ensure that 71 million people each year gain access to clean cooking fuels, which is more than 14 times its most recent performance.

“Unlike electricity, expanding access to clean cooking does not appear to have been such a priority for policy-makers,” said Anita Marangoly George, Senior Director of the World Bank’s Energy and Extractives Global Practice. “This is worrisome given the heavy health burden carried by women and children inhaling smoke from traditional cooking practices.”

Africa’s reliance on traditional uses of biomass – both by households and enterprises – is one of the reasons why it derives as much as 70% of its energy consumption from renewable sources; more than any other continent in the world. And even though Africa is only beginning to tap its vast hydro, geothermal, wind and solar resources, it already gets 9% of its energy – and 21% of its electricity – from these modern renewables, putting it ahead of Asia in this regard.

The inefficiency of traditional uses of biomass also explains why Africa comes out as one of the most energy intensive regions of the world, despite its very low levels of per capita energy consumption. In fact, Africa needs twice as much energy as Europe to produce a single dollar of GDP. Yet progress is not insignificant, annual energy savings made from 2010-2012, are equivalent to what Ethiopia uses each year. About half of these savings were made by South Africa alone, and greatest advances on energy efficiency came from the transportation sector.

In fact, an estimated $50-80 billion is required each year to reach all of the Sustainable Energy for All (SE4All) objectives in Africa. And private investment is crucial to making that happen. By far the largest price tag is for renewable energy investments at $36 billion a year. Energy efficiency would cost about $12 billion a year and the remainder for energy access.

“What we need is for stakeholders – governments, civil society, energy suppliers and consumers – to work towards achieving sustainable energy for all,” said Anita Marangoly George. “Ending energy poverty by 2030 is something that we can achieve.”

The SE4All Global Tracking Framework is produced jointly by the World Bank’s Energy and Extractives Global Practice, the World Bank’s Energy Sector Management Assistance Program (ESMAP) and the International Energy Agency, and is supported by 20 other partner organizations and agencies.

Related News

Break the chain of desperation that leads to emergencies and humanitarian disasters, IFAD President tells development leaders in Rome

Against a backdrop of new reports that show the number of refugees entering Europe has continued to skyrocket, senior government officials attending the final day of the International Fund for Agricultural Development’s 39th Governing Council, renewed their commitment to invest in smallholder agriculture and reduce poverty in developing countries.

Recognizing that rural development plays a fundamental role in stabilizing communities and reducing migration and conflict, IFAD President Kanayo F. Nwanze told leaders that “by working together to deliver on the Sustainable Development Goals (SDGs) – starting with zero poverty and zero hunger – we can break the chain of desperation” that leads to emergencies and humanitarian disaster.

Urgent calls for action in support of increased investment in smallholder agricultural to ensure food security, climate change adaptation, equitable prosperity and ultimately to remove the root causes that lead to conflict and migration, were shared throughout the two-day conference, held annually in Rome for senior government officials representing IFAD’s 176 member states.

Sergio Mattarella, the President of the Italian Republic, pledged that Italy will continue to play a key role in the eradication of hunger and poverty – conditions he described as “insidious”.

Mattarella brought attention to the increasing number of refugees fleeing the conflict in Syria and called on leaders of all nations to get involved. “Saving human lives and reaching out to those fleeing war or misery is a moral duty, a duty for any society that defines itself as free, democratic and truly respectful of human rights,” he said.

Dr Mohamed Ibrahim, globally recognized entrepreneur and founder of the Mo Ibrahim Foundation, delivered this year’s IFAD Lecture. Ibrahim took African governments to task for not living up to their commitments to invest in agriculture and rural development. He said it is essential that they create opportunities for young people in agriculture so that they are able to resist the dangerous call of extremism.

“No jobs, no hope,” he said, adding that Africa has more hungry, malnourished people than anywhere else in the world. “We are by far the least productive region in the agriculture sector but because we have more uncultivated, arable land than anywhere else, it presents opportunities.”

A private-sector panel which included Sunny Verghese, Cofounder and Group CEO of Olam International, highlighted the need for bold initiatives to better link smallholder farmers to markets. Panel participants emphasized that everyone – government, the private sector, financing institutions such as IFAD, small- and medium-sized enterprises and smallholders farmers – have a role to play.

A second panel discussion, facilitated IFAD Associate Vice President Périn Saint Ange, focussed on innovative agricultural solutions to many of the global challenges discussed over the two days, including IFAD investments in farming technologies, approaches to empower women and youth, and the use of new technology to enhance rural development project design and management.

In a one-on-one conversation ahead of the panel, Dr Ismahane Elouafi, Director General of the International Centre for Biosaline Agriculture, said that the world is at a crossroad in terms of its overuse of natural resources, and that the Middle East and North Africa region already has some of the highest water scarcity in the world.

“Climate change impacts the poor and marginalized most of all,” she said. “We have huge challenges ahead, and we need to act now.”

Among the outcomes from the Farmers’ Forum, a two-day meeting held in conjunction with IFAD’s Governing Council, organizers announced a plan to make the platform for dialogue more inclusive, inviting pastoralists and livestock breeders to take part, and more decentralized creating stronger links to smallholders and family farmers on the ground.

IFAD invests in rural people, empowering them to reduce poverty, increase food security, improve nutrition and strengthen resilience. Since 1978, we have provided US$17.6 billion in grants and low-interest loans to projects that have reached about 459 million people. IFAD is an international financial institution and a specialized United Nations agency based in Rome – the UN’s food and agriculture hub.

Related News

Better enforcement of anticorruption laws needed to clean up business in Mozambique

Minimal enforcement of anti-corruption laws coupled with the private sector’s lack of exposure to international anti-corruption norms allows corruption to thrive in Mozambique’s business sector, according to a new study from Transparency International and its chapter in Mozambique, the Center for Public Integrity.

The new report, which will help set a Business Integrity Country Agenda (BICA) for Mozambique, is part of an effort by the Centre for Public Integrity and Transparency International to reduce corruption in Mozambique’s private sector. The initiative comprises an assessment of business integrity in the country, resulting in the BICA Assessment Report and then translation of the assessment’s key findings into a working agenda for reform.

“The only way we can clean up the business environment is through collective action,” said Adriano Nuvunga, the Director of the Centre for Public Integrity. “This new programme will be used for the first time ever in Mozambique. It is based on the idea that the government, the business sector and civil society working together can be far more effective in promoting business integrity than actions by individuals or stakeholder groups acting alone.”

In the public sector, the results show that Mozambique has signed and ratified the main international and regional anti-corruption conventions: the United Nations Convention Against Corruption (UNCAC), the African Union Convention on Preventing and Combating Corruption and the Southern Africa Development Community (SADC) Protocol Against Corruption, and has made a considerable effort to incorporate these instruments into its legal framework.

But enforcement is problematic because of a low capacity to implement anti-corruption laws and poor incentives to promote clean business dealings. Public sector thematic areas related to business integrity cover issues such as bribing public officials, commercial bribery, money laundering, economic competition, accounting and audit, undue influence, public tendering, and tax administration. In most of these areas the country has a legal framework in line with international standards.

Unlike the public sector, in the business sector in Mozambique local enterprises do not have the same exposure, stimulus and ability to adopt policies and practices in line with international standards. Some factors that have played a role in fostering poor standards of business integrity, include the concentration of exports and the few opportunities for linkages with multinationals and megaprojects in a few enterprises; a weak market with limited business-to-business relations; and weak enforcement of integrity standards in the public sector in Mozambique.

In this context, relatively few companies operate in an environment that creates positive incentives for good management standards and the promotion of business integrity. However, there is growing awareness that corruption harms business. In this regard, business associations are adopting business integrity codes of conduct, although still with low adherence by companies. Moreover in August 2015, in the context of the dialogue between the government and private sector, both parties agreed to include anti-corruption measures in the set of actions to be implemented by the business sector, which includes responsibility for monitoring and reporting on the progress by the latter.

Historically, civil society in Mozambique has played the role of oversight and watchdog in relation to the public sector. The research found that civil society – together with the media – is a key player in promoting business ethics. It can be instrumental to preventing, reducing and responding to corruption in the business sector providing broad societal checks and balances.

The assessment is based on evidence gathered from multiple sources: legislation, official documents, studies, primary data, stakeholders and interviews with experts. The process included the selection of a National Advisory Group (NAG), comprising representatives of all the stakeholder groups and donors, who were responsible for validating the research findings and presenting recommendations on collective action.

» Download: Business Integrity Country Agenda (BICA) Assessment Report: Mozambique | Executive summary (PDF, 6.85 MB)

Related News

1st Meeting of the Continental Free Trade Area Negotiating Forum (CFTA-NF)

The 1st Meeting of the Continental Free Trade Area Negotiating Forum is scheduled to take place from Monday 22 to Saturday 27 February 2016 at the AU Headquarters in Addis-Ababa, Ethiopia.

The main objective of the meeting is to consider all the post launch preparatory issues and essential process issues and technical documents that will enable the efficient conduct of the negotiations. Specifically, the Meeting will undertake the following:

-

Discuss studies that have been conducted on the establishment of the CFTA;

-

Identify capacity needs for the CFTA negotiations;

-

Consider and adopt the Rules of Procedure for the CFTA Negotiating Forum;

-

Consider technical issues to advance the preparations for the negotiations;

-

Consider the establishment of various Technical Working Groups in specific areas

The meeting shall be attended by all the Member States of the African Union. The meeting will also be attended by Trade Officials from the following RECs and institutions; AMU (Arab Maghreb Union), CEN-SAD, COMESA, EAC, ECCAS, ECOWAS, IGAD, SADC, UNECA (United Nations Economic Commission for Africa) and the AfDB (African Development Bank).

The meeting will be preceded by a two-day capacity building and information sharing workshop (22-23 February 2016) where the AUC will introduce a capacity needs assessment and share findings and conclusions from a select number of studies that have been conducted on the establishment of the CFTA.

Background

The 25th Ordinary Session of the Assembly of Heads of State and Government of the African Union which was held in Johannesburg, South Africa in June 2015 launched the negotiations for the establishment of the Continental Free Trade Area (CFTA). The launch of the negotiations marked a major milestone in the implementation of the Summit decision to establish a continental free trade area by 2017. The objective of the CFTA negotiations is to conclude a comprehensive and mutually beneficial trade agreement among the Member States of the African Union.

In launching the CFTA negotiations, the Summit adopted the following documents; The objectives and principles of Negotiating the CFTA; The indicative Roadmap for the Negotiation and establishment of the CFTA; The Terms of Reference for the CFTA Negotiating Forum (CFTA-NF); The institutional arrangements for the CFTA negotiations; and The Declaration on the Launch of the negotiations for the establishment of the CFTA. The Roadmap identifies phases in the negotiations for the CFTA, the post launch preparatory phase, the negotiations phase, finalisation of the CFTA Agreement and launch of the Continental Free Trade Area and the domestication of the CFTA agreement by Member States.

The CFTA Negotiating Forum was established by the Assembly and is composed of Officials from the African Union Member States and Regional Economic Communities that are recognised by the African Union. It has the responsibility of conducting trade negotiations at the technical level and it reports to the Committee of Senior Trade Officials on its negotiation activities. The CFTA Negotiating Forum also has the responsibility of preparing quarterly reports on progress made in the negotiations highlighting areas requiring higher level intervention to the Committee of Senior Officials, Ministers of Trade, the High Level African Trade Committee and the Assembly.

The Continental Free Trade Area is an Agenda 2063 flagship project of the African Union.

Related News

Kenya eyes crude exports in 2017 via trucks and railway

Kenya is considering moving its crude oil to Mombasa by road and railway as President Uhuru Kenyatta’s administration races to hit export markets before the General Election set for August next year.

The Energy ministry has offered Rift Valley Railways (RVR) the contract to move the oil over a distance of more than 800km, from Eldoret to the Kipevu-based Kenya Petroleum Refineries (KPR) from as early as February next year.

By choosing trucks and train, Mr Kenyatta’s administration appears determined to sidestep bureaucracy involved in constructing a joint pipeline with Uganda in an effort to beat its tight timelines.

“We are quite ambitious but we know we will be able to pull this off in the next 12-16-month window,” said the head of Presidential Delivery Unit Nzioka Waita.

“And as we speak, work has been done to improve the road network from Lokichar to Lodwar and from Lodwar to Kapenguria to increase the shoulder size to allow trucks which carry crude oil to convey it to Kitale and subsequently to Eldoret,” Mr Nzioka said in a presentation made during the Governors’ Summit last week.

The upgrade of the 213km road from Lokichar to Kitale has been top of the government’s agenda as it looks to facilitate the quick transport of crude to an export terminal in Mombasa.

Kenyan officials also appear to be keen on sidestepping the long process of constructing a joint crude oil refinery under discussion with Rwanda, South Sudan and Uganda.

The joint projects were supposed to be built in public-private partnership model.

South Sudan is embroiled in civil strife since 2013 while Uganda has in recent months been preoccupied with political campaigns that culminated into Thursday’s election.

Uganda, which aims to start crude production by 2018, recently signed an agreement with Tanzania to explore the possibility of building a crude oil pipeline between the two countries.

Although Uganda had agreed to the Kenyan route, it said Nairobi had to guarantee security for the pipeline, along with financing and cheaper fees than alternatives.

Settling for a route through Tanzania could slow some projects in Kenya, which are planned to run alongside the pipeline on the land corridor in the North of the country to Lamu, where Kenya wants to build a new port to serve the region.

“We are now trying to refurbish Kipevu plant – which has only been bringing petroleum in – to take petroleum out,” said Mr Nzioka.

“At the Kipevu plant, they’ll do what they call first line refinery and then take that into the export market.”

British firm Tullow Oil Plc, working jointly with Africa Oil Corporation, have discovered an approximately one billion barrels of crude oil in the South Lokichar basin.

The prospects for export have appeared bleak lately as crude prices tumble in the global market.

The crude oil prices have dropped from $73 per barrel at the beginning of last year to a ten-year low of $27 this year. Tullow has since indicated its plan to roll out production next year.

The firm has also dismissed concern over low prices saying it can export at prices as low as $25 per barrel.

Mr Nzioka however said Kenya has not pulled out of its regional commitment.

He said: “We are looking at all options of whether to move this oil through our regional engagement with the government of Uganda or to move on our own even as we look at building the pipeline from Hoima, Lokichar though to Lamu.”

Related News

DG Azevêdo: WTO can help Senegal achieve its development goals

WTO Director-General Roberto Azevêdo ended his official trip to West Africa on 18 February 2016 with a visit to Dakar, Senegal. He met with President Macky Sall to discuss how the WTO can help the country achieve its development objectives. He also met with the Minister of Trade, Informal Sector, Consumption, Promotion of Local Products and SMEs, Alioune Sarr, and a number of other high-level government representatives.

During his visit to Senegal, the Director-General also held meetings with the Ministry of Economy and Finance and Planning and the Ministry of Foreign Affairs, students at the Groupe École Supérieure de Commerce de Dakar, as well as the singer, musician and former minister Youssou Ndour. In addition, the Director-General spoke at the Cheick Anta Diop University about Senegal’s participation in the global trading system, the results of the WTO's recent Nairobi Ministerial Conference, and the future work of the organization.

The Director-General’s full speech is available below.

Cheick Anta Diop University, Dakar, Senegal

Remarks by Director-General Roberto Azevêdo

It is a great pleasure to be here in Senegal – especially as this is my first visit to the country.

I am also very pleased to address you today at this prestigious institution that was awarded a Chair under the WTO Chairs Programme. This programme aims to enhance knowledge and understanding of the international trading system among academics and decision-makers in developing countries. The Cheikh Anta Diop University is one of the few institutions in the world to have been selected to participate in this programme.

This is my first time back in Africa since the WTO’s successful Ministerial Conference in Nairobi two months ago.

The Conference put a spotlight on Africa.

In Nairobi, WTO Members adopted decisions that will support the growth and development of Senegal, Africa and the world.

Following on from this success, we must ensure that Africa remains in the spotlight. We need to deliver other agreements that support your development objectives.

I would like to formally thank the Government of Senegal for its support throughout the process leading up to the Nairobi Conference.

Senegal is one of the founding Members of the WTO, and acceded to the General Agreement on Tariffs and Trade, the WTO’s predecessor, in 1963.

For more than 50 years, the country has participated actively and constructively in the multilateral trading system.

Senegal works alongside other least developed country – or LDC – Members of the WTO to help define the work programme and tackle the specific obstacles faced by LDCs.

The LDCs form a powerful group within the WTO and their development is an absolute priority for the Organization.

This level of priority is clear from the flexibilities and special provisions included in WTO Agreements and Decisions.

And it is also clear from the substantive support that is available to LDCs to help them strengthen their trading capacity.

I would like to build on this to further your integration into the trading system.

And I think that the results obtained in Nairobi show that this commitment is shared by the entire Membership.

Nairobi outcomes

Let me explain in a bit more detail what was delivered in Nairobi.

The Nairobi Package contains a set of Ministerial Decisions on agriculture and issues concerning LDCs.

Regarding agriculture, the decision on export competition is particularly important. It is the most significant reform in international trade rules on agriculture since the creation of the WTO.

It will eliminate agricultural export subsidies and ensure that Members do not resort to such measures in the future.

Eliminating subsidies is, in fact, one element of the UN’s new Sustainable Development Goals – and we delivered the decision barely three months after the goals were agreed!

It will certainly have a positive impact in terms of improving the global trading environment by tackling the enormous trade-distorting potential of these subsidies.

Farmers in the developing world should not have to compete with the treasuries of developed countries.

The decision will help to level out the playing field in agriculture markets, to the benefit of developing countries and LDCs. And this is very significant for Senegal, where agricultural products account for more than 30% of exports.

The decision will also help to limit similar distorting effects associated with export credits, State trading enterprises, and food aid.

Members also undertook to negotiate steps to improve food security and to develop a Special Safeguard Mechanism to help deal with import surges of food products, which can harm domestic food production.

So it is important that we follow up on these commitments.

And as I mentioned before, an important package of decisions was adopted to support the integration of LDCs into the global economy.

These decisions most notably include significant provisions on preferential rules of origin for goods from LDCs and preferential treatment for LDC services providers.

Significant steps were also taken regarding cotton, so as to open up foreign markets for the most vulnerable producers and end cotton export subsidies.

In short, these decisions will provide LDCs with additional opportunities to export their goods and services to developed and developing countries.

In Nairobi, Members also launched the second phase of the Enhanced Integrated Framework, a programme focused exclusively on LDC capacity-building.

I think it is therefore fair to say that Nairobi delivered successful outcomes – outcomes that significantly boost growth and development.

Other achievements

These results build on our successful Ministerial Conference in Bali, where Members delivered a number of important outcomes, including the Trade Facilitation Agreement.

This Agreement will make a real difference on the ground. It aims to streamline, standardize and simplify border processes around the world, thereby cutting trade costs.

It is estimated that this will boost global trade by $1 trillion a year – with almost three-quarters of this increase accruing to developing economies.

Those that make the biggest reforms will likely reap the biggest gains.

It is encouraging to see that Senegal views trade facilitation as a priority and that it has made significant reforms in this area. Since 2006, import and export times have almost halved. This is a significant achievement. Senegal is also striving to improve its business environment and is moving up in the international rankings.

According to the World Bank’s Doing Business report 2013-2014, Senegal was one of the economies that had most improved their business climate, a trend that continued in 2015.

The Trade Facilitation Agreement will do much to help Senegal in its efforts. It will help cut trade costs, speeding up the flow of goods and improving the country’s ability to trade, both regionally and globally.

A recent WTO report noted that full implementation of the Agreement could reduce trade costs by an average of 14.5%, which would favour diversification. The report also found that the Agreement would help LDCs to increase the number of new products exported by as much as 35%, and increase their access to foreign markets by 60%.

But in order to benefit from the Agreement, it must first be ratified. Many African countries have already taken this step and I would encourage Senegal to do the same. The Agreement does not impose a rigid programme of reforms – on the contrary, it gives you the flexibility to implement its provisions according to your specific needs and capacities, and provides practical support to help with implementation.

On all these issues, the WTO is here to help. If more information or support is needed then we stand ready to help and will do all we can.

Post-Nairobi

So, in my view, our experiences in recent years show that the WTO is capable of delivering concrete outcomes. We are becoming accustomed to success.

However, we must also recognize that the WTO’s slow progress over many years has left its mark, with many countries entering into other trade initiatives, such as regional or bilateral agreements.

Senegal itself is party to a number of initiatives of this type, such as the Economic Community of West African States (ECOWAS). And this is certainly very positive. Steps taken to improve trade and integration at regional level can be very important for trade promotion, and yet effective global trade cooperation remains essential.

Cooperating in the field of trade will enable us to function well at all levels. Topics such as fisheries subsidies – fisheries being vital for Senegal’s economy – can only be addressed effectively at multilateral level, via the WTO.

We must therefore continue delivering outcomes at that level.

In Nairobi, Ministers started a frank conversation on the future of the Organization – and on how it can do more, and faster.

But there is currently no consensus on how to move forward.

All Members do, however, want to deliver on outstanding Doha issues, such as agriculture (particularly domestic subsidies) and market access for industrial goods and services, but they do not agree on precisely how these issues should be tackled.

What’s more, some Members would like to start discussing issues that do not form part of the Doha Agenda.

This conversation has already begun, in Geneva and in capitals all over the world.

And despite some differences, there are significant commonalities. For example, there is a strong desire to maintain development at the centre of our efforts. It is also clear that Members want to continue making positive efforts to better integrate LDCs into trading flows.

So I think we need to build on these common elements – and learn from our recent successes – in order to make as full a contribution as we can. This conversation is an opportunity to make sure that the future work of the WTO delivers for you.

We can take actions that will help you deliver on your development goals, by diversifying the economy and encouraging more businesses to trade.

Small and medium-sized enterprises are an important part of your countries’ economies, and we can take further steps to help them integrate into trading flows.

These are just a few examples. The point is that you have an opportunity to shape the future of global trade discussions in your interests. I want to help you seize that opportunity.

Conclusion

The challenge we face is by no means small.

The WTO has delivered important results for Senegal. Now we need to follow our agreements through and implement them in full.

We are entering a potentially very exciting period as regards the world trading agenda. And Senegal’s voice in this debate will, of course, continue to be as important as always.

I would be interested to hear your views today and I count on your participation in the weeks and months to come.

Thank you.

Related News

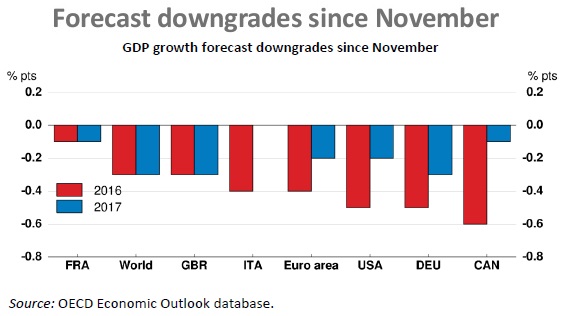

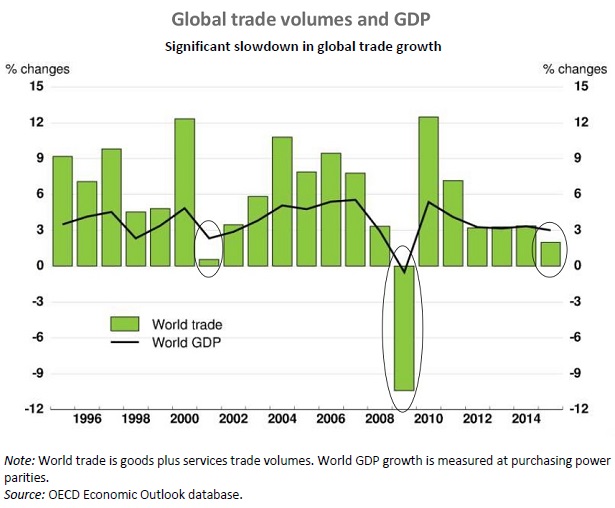

Elusive global growth outlook requires urgent policy response

Achieving strong growth in the global economy remains elusive, with only a modest recovery in advanced economies and slower activity in emerging markets, according to the OECD’s latest Interim Economic Outlook.

The world economy is likely to expand no faster in 2016 than in 2015, its slowest pace in five years. Trade and investment are weak. Sluggish demand is leading to low inflation and inadequate wage and employment growth.

The downgrade in the global outlook since the previous Economic Outlook in November 2015 is broadly based, spread across both advanced and major emerging economies, with the largest impacts expected in the United States, the euro area and economies reliant on commodity exports, like Brazil and Canada.

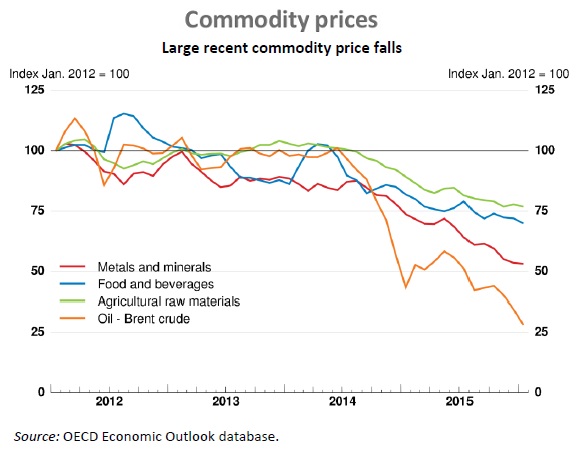

Financial instability risks are substantial, as demonstrated by recent falls in equity and bond prices worldwide, and increasing vulnerability of some emerging economies to volatile capital flows and the effects of high domestic debt.

“Global growth prospects have practically flat-lined, recent data have disappointed and indicators point to slower growth in major economies, despite the boost from low oil prices and low interest rates,” said OECD Chief Economist Catherine L. Mann. “Given the significant downside risks posed by financial sector volatility and emerging market debt, a stronger collective policy approach is urgently needed, focusing on a greater use of fiscal and pro-growth structural policies, to strengthen growth and reduce financial risks.”

The OECD projects that the global economy will grow by 3 percent this year and 3.3 percent in 2017, which is well below long-run averages of around 3¾ percent. This is also lower than would be expected during a recovery phase for advanced economies, and given the pace of growth that could be achieved by emerging economies in convergence mode.

The US will grow by 2 percent this year and by 2.2 percent in 2017, while the UK is projected to grow at 2.1 percent in 2016 and 2 percent in 2017. Canadian growth is projected at 1.4 percent this year and 2.2 percent in 2017, while Japan is projected to grow by 0.8 percent in 2016 and 0.6 percent in 2017.

The euro area is projected to grow at a 1.4 percent rate in 2016 and a 1.7 percent pace in 2017. Germany is forecast to grow by 1.3 percent in 2016 and 1.7 percent in 2017, France by 1.2 percent in 2016 and 1.5 percent in 2017, while Italy will see a 1 percent rate in 2016 and 1.4 percent rate in 2017.

With China expected to continue rebalancing its economy from manufacturing to services, growth is forecast at 6.5 percent in 2016 and 6.2 percent in 2017. India will continue to grow robustly, by 7.4 percent in 2016 and 7.3 percent in 2017. By contrast, Brazil’s economy is experiencing a deep recession and is expected to shrink by 4 percent this year and only to begin to emerge from the downturn next year.

The OECD says monetary policies should remain highly accommodative in advanced economies, until inflation has shown clear signs of moving durably towards official targets. In emerging market economies, monetary support should be provided where possible, taking into account inflation developments and capital market responses.

The Outlook suggests that a stronger fiscal policy response, combined with renewed structural reforms, is needed to support growth and provide a more favourable environment for productivity-enhancing innovation and change, particularly in Europe.

“With governments in many countries currently able to borrow for long periods at very low interest rates, there is room for fiscal expansion to strengthen demand in a manner consistent with fiscal sustainability,” Ms Mann said. “The focus should be on policies with strong short-run benefits and that also contribute to long-term growth. A commitment to raising public investment would boost demand and help support future growth,” Ms Mann said.

Related News

tralac’s Daily News selection

The selection: Thursday, 18 February 2016

Important trade and regional integration policy pointers:

From the African Union’s Trade and Industry department: the 1st meeting of the CFTA Negotiating Forum will be held from 22-27 February in Addis Ababa

From the AfDB - two EOIs:

Intra-African investment and regional financial integration

The African Development Bank has unveiled a landmark initiative (The High 5s, within the context of the Bank’s Ten-Year Strategy) to accelerate Africa's development over the next 10 years. Under this initiative, the High-Five priority areas of focus in Africa - to light up and power Africa, feed Africa, integrate Africa, industrialize Africa, and improve the quality of life for the people of Africa - form a blueprint for African countries to embark on a course of sustainable transformation. The objective of this assignment is to assist the Task Manager and the team on the intra-African investment and regional financial integration initiatives: participate in the drafting of the Approach to Regional Financial and Investment Integration in the SADC region; participate in the drafting of the joint Regional Integration Policy Paper on Regional Financial Integration in North Africa; participate in the drafting of the joint Regional Integration Policy Paper on Regional Financial Integration in Central Africa.

ECOWAS: developing a common policy on migration

As part of the efforts at deepening integration, in 1979 ECOWAS ratified the Protocol on Free Movement of Persons and subsequently waived visa requirements and adopted a common passport to enhance movement of community citizens. In spite of the progress that ECOWAS have made in the area of migration, the Community still faces a number of challenges, including the pursuit of conflicting objectives by member states and weak implementation of the Protocol on Free Movement, especially the rights of residence and establishment – due in part to the absence of strong regulatory framework on migration. The ECOWAS Commission has recognised that a key way of overcoming these obstacles is the drafting of a common policy on migration. The objective of this assignment is to deliver technical assistance to the ECOWAS Commission that will contribute to achieving the following:

South Africa: African trade and regional integration update by Minister Patel (ANC)

To support jobs through regional integration, we are focusing on markets on the continent. Last year for the first time other African countries became our single biggest regional market, overtaking Asia. We exported R303bn worth of goods to other African countries. These supported roughly 250 000 South African jobs. For example, half of the trucks we export, go to the rest of Africa and 60% of fruit juice exports is to our own continent. We will now work on deeper regional integration by private and public sector co-investment in other parts of the continent and support for a big infrastructure push in the continent, covering key projects such as the North South corridor that links the continent by road and rail; the big water and energy projects such as the Lesotho Highlands Water Project and working on Grand Inga with the DRC.

Namibia to address WTO in bid to save livestock industry (New Era)

Namibia is to send a high-powered delegation from all sectors of the livestock and meat industry to Geneva to present its case before the Sanitary and Phyto-Sanitary (SPS) Committee of the World Trade Organisation from March 16 to 17, in a bid to oppose soon-to-be-announced livestock import restrictions by South Africa. It is expected that South Africa will adopt the new restrictions before the end of February, after which the regulations will be implemented six months later. Namibia is now preparing to address the SPS Committee to acquire some breathing space before the implementation and to activate its own Master Plan after the Livestock Producers Association of Namibia and the Namibian Agricultural Union last week officially requested President Hage Geingob to intervene and save the industry.

Botswana, South Africa, Zimbabwe: development of the animal feed to poultry value chain (UNU-WIDER)

The cross-country investments being made by large poultry companies in the region indicate that a degree of regional integration is being fostered by firms in the region, largely in the absence of agreements between neighbouring states and in spite of barriers to trade that have been put in place. However, the predominance of large firms in the value chain also raises important questions about the strategies lead firms are pursuing, including vertical integration and agreements, and the implications for the development of local and regional agro-processing capabilities. Two important aspects of industrialization in the poultry value chain—upgrading of feed and breeds, and co-ordinated investments across the region—have been led by large firms. [The authors: Phumzile Ncube, Simon Roberts, Tatenda Zengeni]

Egypt: Prime for investment, COMESA countries must be more than export market (Daily News)

Exchange between Egypt and COMESA countries in 2014 amounted to about $2.7bn. Egyptian exported goods worth over $2bn including plastic products, ceramics, and electrical appliances. Egypt also imported tea, coffee, copper, and livestock worth about $700m from COMESA member countries in 2014. Egyptian exports to COMESA countries accounted for about 8% of its total exports in 2014. Although the percentage is not large, it is expected to increase in the upcoming years, especially as COMESA markets absorb significant proportions of Egyptian exports. For instance, COMESA markets receive about 25% of Egypt’s exports of ceramic products, 10% of plastic products, 35% of sugar production, 20% of fruit and vegetable exports, 25% of cement and paper exports, 18% of dairy exports, and 15% of medicine and glass exports. Various engineering products have an export percentage that ranges from 8% to 25%. These are impressive proportions that must be preserved and increased.

Related: Egyptian banks unconcerned with Africa (Daily News), Egyptian tech companies to expand in Africa to develop governmental services (Daily News)

UK seeks to revive Kenya exports with Sh74bn kitty (Business Daily)

Britain has set up a Sh74 billion fund to provide credit lines to local firms that buy goods from the European state in a bid to revive its dwindling exports to Kenya. The UK’s Trade envoy to Kenya, Lord Clive Hollick - who is expected in the country on Wednesday for a three-day visit - is set to unveil the fund that also provides cover against risks incurred by British firms while exporting goods to Kenya. In recent years, the country has been losing out to China, India and Japan with official data showing the value of imports from the UK to Kenya dipping to Sh40.1 billion in the first 11 months of last year, compared to Sh41.3 billion a year earlier and Sh45.7 billion in 2013.

Nigeria: These charts show the decline of investor confidence in Africa’s largest economy (Quartz)

The Capital Importation report tracks the total inflow of capital into the country under three main investment types: Foreign direct investment , portfolio investment and other investments, including currency deposits and loans. In 2015, total capital imported into Nigeria stood at $9.6bn, the lowest recorded total since 2011. It represents a 53% drop from the $20.7bn recorded in 2014.

Committee on Technical Barriers to Trade: 2015 annual review (WTO)

The WTO Committee on Technical Barriers to Trade (the Committee) will conduct its Twenty-First Annual Review of the Implementation and Operation of the WTO Agreement on Technical Barriers to Trade (the TBT Agreement) under Article 15.3 at its next meeting on 9-10 March 2016. This document contains information on developments in the Committee relating to the implementation and operation of the TBT Agreement from 1 January to 31 December 2015.

Extract: In terms of the Committee's review of measures, during the year, notifications decreased by 12% compared to the previous year (to a total of 1,989 notifications). Nevertheless, the trend since 2015 has been an upward one driven increasingly by developing Members. In 2015, developing Members continued to submit significantly more new notifications than developed Members - also the number of notifications from LDCs increased during the year. In total, 86 specific trade concerns were discussed in 2015, the second highest number since 1995. [Download]

German development cooperation with SADC: newsletter

Highlight: 13 April, Johannesburg - launch of Southern African Business Forum Working Groups to improve cooperation between private sector and SADC to accelerate Regional Economic Integration around selected topics and barriers to trade. Johannesburg

Five proposals for SADC health innovations (SAIIA)

Social cohesion in Eastern Africa (UNECA)

The report examines social cohesion using data from a wide variety of sources, including national statistics institutes and international organisations. But it also investigates qualitative data, including opinion surveys and questionnaires to gain a deeper appreciation of the perspectives of citizens in the region. This results in some surprising findings.

Extract: This final point merits some further discussion. Regional solutions to the problems associated with a lack of social cohesion will be constrained by the availability of resources at the regional level. Presently, for instance, the annual budget of the EAC Secretariat, at around $140 million, is miniscule compared to the scale of challenges and the size of the regional economy (approximately $134 billion in 2014). Thus far, despite all the good work, it is probably fair to say that regional organizations such as the EAC do not impact directly enough on the lives of their citizens. At least, that seems to be people’s perceptions at present. A recent opinion poll carried out by Afrobarometer (2015) revealed that less than one in five of the citizens in Burundi, Kenya or the United Republic of Tanzania enthusiastically felt that the regional body was having a positive impact on their lives. [Download]

Financing mechanism top agenda of next EAC summit (New Times)

“Top on the agenda is the consideration of reports by the EAC Council of Ministers on: the negotiations on the admission of the Republic of South Sudan into the Community; sustainable financing mechanisms for the EAC; and the EAC Institutional Review,” reads an EAC statement. For the past few years, EAC leaders have been mulling how to find the best sustainable financing mechanisms for bloc’s activities. A directive by the Summit in November 2013 tasked the Council, the bloc’s policy organ, to present a report on alternative financing mechanisms, including the option of one per cent of imports from outside EAC, as one of the ways the bloc could reduce overreliance on donor aid. “The ministers for finance are going to meet early next week and they will advise accordingly on what would be a final solution,” said Innocent Safari, the permanent secretary at the Ministry of East African Community Affairs.

Demand for iron ore levelled off in 2015 (UNCTAD)

The UNCTAD Iron Ore Market Report 2015, covering developments in the iron ore market in 2014 and providing an overview for 2015–2016, shows that slowing growth in worldwide steel production meant that the market for iron ore, the primary raw material of steel, entered a new phase with slower growth, lower prices and squeezed margins for mining companies. The report notes that world crude steel production in 2015 reached an estimated 1,763 million tonnes, a decrease of 2.9%, while the iron ore production reached 1,948 million tonnes, down 6% on 2014. The effect on the iron ore market was that, after a long period of rapid growth, demand levelled off and prices returned to levels not seen since 2002. The price of iron ore began 2015 at $71.26 per dry metric tonne but fell 39% by the end of the year. A reorientation of China’s economic strategy brought growth in the use of steel almost to a halt, and signs of demand picking up in other parts of the world were not enough to offset China's slowdown.

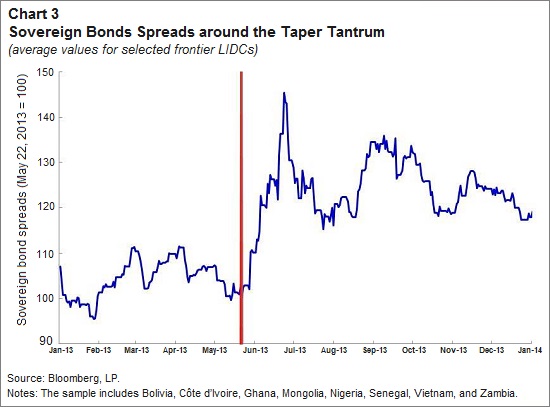

The change in demand for debt: the new landscape in low-income countries (IMF)

Sovereign bonds issued by low-income countries amounted to $4bn in 2013 and to $8bn in 2014, thanks in part to issuances by Côte d’Ivoire, Ethiopia, Ghana, Kenya, Senegal, Vietnam, and Zambia. In 2015, with weaker global conditions and falling commodity prices, the number of issuances declined and those who issued new bonds had to pay significantly higher yields.

Ghana: National commodity exchange will be a game-changer (Asoko Insight)

US-ASEAN: Sunnylands Declaration (White House)

Narendra Modi’s Rs8 trillion Make-in-India haul masks challenges to come (Livemint)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

New report on Social Cohesion in Eastern Africa

Poverty, inequality, migration and political unrest have all threatened social cohesion in Eastern Africa, as well as many other threats. Yet the region has proved remarkably resilient to these challenges, finds a new report launched the Economic Commission for Africa.

The report examines social cohesion using data from a wide variety of sources, including national statistics institutes and international organisations. But it also investigates qualitative data, including opinion surveys and questionnaires to gain a deeper appreciation of the perspectives of citizens in the region.

This results in some surprising findings. For example, the official estimate of how many people are living in poverty is different in many countries from the number of people who view themselves to be living in poverty. Understanding perceptions, the report argues, is essential for understanding the state of social cohesion.

The enormous economic and social progress made in Eastern Africa over the last 10 to 15 years is discussed in the report, as well as a number of rising challenges. These include some of the fastest rates of urbanisation in the world, high levels of gender-based violence in some countries and alcohol abuse in certain regions.

A regional approach needs to be taken to many of these issues, argues an author of the report, Ms Emelang Leteane, ECA Social Affairs Officer, speaking at the 20th Intergovernmental Committee of Experts meeting in Nairobi. “Some threats to social cohesion do not respect national borders. These threats demand a regional response,” said Ms Leteane.

The report makes other recommendations as well, including the creation of a fund managed by the East African Community that would be used to reduce spatial inequalities and strengthen social cohesion in the region.

Social Cohesion in Eastern Africa

Executive summary

This report provides an overview of the state of social cohesion in Eastern Africa.[1] The term “social cohesion” is used to refer to a situation where a group of people interact in a way that advances the interests of all those involved. They act as a community. It is a multidimensional concept involving a number of elements, including trust, equity, beliefs, acceptance of diversity, perceptions of fairness and respect. Accordingly, this report does not purport to provide a comprehensive assessment of the state of social cohesion in Eastern Africa. Instead, using a combination of qualitative and quantitative data from a wide range of sources, the report presents a broad “social audit” of the state of social cohesion and development in the region.

The primary finding is that social cohesion in Eastern Africa has shown resilience in the face of numerous challenges since the beginning of the twenty-first century. Nearly all countries have notably improved their Human Development Index since 1990, with some countries achieving particularly rapid progress in education and health indicators. The report also shows that there has been promising improvements in poverty reduction, with Ethiopia, Uganda and Rwanda achieving the fastest progress.

Despite this positive picture, the report highlights a number of outstanding challenges for social cohesion. An estimated 237 million people from East African are still living in poverty. Beyond open conflict in South Sudan and Somalia, parts of the region are still afflicted by low-intensity conflicts and social disorder. The capacity of law and order institutions to manage such tensions is often stretched. A number of communities in the region are still faced with sporadic humanitarian crises while others remain vulnerable to natural disasters. The report also highlights both the weak performance of the labour market and rising inequality as significant threats to greater social cohesion.

Demographic pressures are putting a strain on scarce resources, which further tests cohesion. While it is one of the least urbanized regions in the world, Eastern Africa is also one of the fastest urbanizing. The resulting social pressures are leading to some worrying trends. For instance, levels of substance abuse are high. Alcohol abuse is nearly double the African average in five countries across the region. In six countries for which there is data, between one third and one half of all women report that they have suffered gender-based violence.

Persistent problems in the efficiency of service delivery can compound social malaise, undermining the quality of education and health provision. These inefficiencies convey a perception that governments could do more. For instance, in a recent Afrobarometer poll (Afrobarometer, 2015) (Burundi, Kenya, Madagascar, Uganda and the United Republic of Tanzania), a majority of the respondents felt that their government’s efforts to improve the living standards of the poor, create jobs and reduce inequality were insufficient.

Despite these threats to social cohesion, there are many signs of resilience. Trust provides a foundation for building cohesive societies, and some countries in the region display exceptionally high levels of trust. Contrary to popular perception, our social audit also reveals notable resilience to divisions along ethnic, religious and cultural lines. For example, the United Republic of Tanzania has attempted to overcome these differences by adopting Kiswahili as a national language. Rwanda has improved service delivery through the rolling out of Imihigo – a home-grown governance arrangement based on a traditional form of performance contract.

The report concludes by observing that while there is a lot of information available pertinent to the state of social development and cohesion, much of it is currently scattered. Monitoring both qualitative and quantitative indicators more closely (perhaps through a regular regional report under the aegis of bodies such as the East African Community or the Intergovernmental Authority on Development) is recommended. The forthcoming African Social Development Index by the Economic Commission for Africa (ECA), which has a particular focus on sub-national inequities, is an example of a useful tool for monitoring cohesion.

Finally, the report shows how a lack of social cohesion can rapidly endanger regional stability. Yet the focus of most regional integration programmes in Eastern Africa has been the advancement of physical and economic integration, with trade and market access being high in the priority list. Because of the trans-frontier nature of many social problems, increasingly the challenges need to be tackled at the regional level. In this context, the report argues in favour of establishing a “regional solidarity fund” to tackle social inequalities and inequities head-on.

Over the past decade and a half, Eastern Africa has emphatically demonstrated that it is capable of achieving great things in terms of improving some dimensions of social cohesion. It now needs to extend that progress to other areas to create a more cohesive and prosperous future.

[1] The Eastern Africa region is defined as including 14 countries: Burundi, the Comoros, the Democratic Republic of the Congo, Djibouti, Eritrea, Ethiopia, Kenya, Madagascar, Rwanda, Seychelles, Somalia, South Sudan, Uganda and United Republic of Tanzania.

Related News

Financing mechanism top agenda of next EAC summit

The forthcoming 17th Ordinary East African Community (EAC) Heads of State Summit, scheduled February 29 in Arusha, Tanzania, will discuss the best sustainable financing mechanism for the bloc, among other things.

The summit will be preceded by a weeklong meeting of the EAC Council of Ministers that will take place at the EAC Headquarters in Arusha from February 22.

“Top on the agenda is the consideration of reports by the EAC Council of Ministers on: the negotiations on the admission of the Republic of South Sudan into the Community; sustainable financing mechanisms for the EAC; and the EAC Institutional Review,” reads an EAC statement.

For the past few years, EAC leaders have been mulling how to find the best sustainable financing mechanisms for bloc’s activities.

A directive by the Summit in November 2013 tasked the Council, the bloc’s policy organ, to present a report on alternative financing mechanisms, including the option of one per cent of imports from outside EAC, as one of the ways the bloc could reduce overreliance on donor aid.

“The ministers for finance are going to meet early next week and they will advise accordingly on what would be a final solution,” said Innocent Safari, the permanent secretary at the Ministry of East African Community Affairs.

Partner states seem to have taken too long to agree on a sustainable financing mechanism for the bloc.

Under the 2014/15 Budget passed by the East African Legislative Assembly (EALA), for example, out of the total budget of $124 million, partner states contributed $41.9 million, while $73.2 million came from donors.

Imposing a one per cent levy on all imports to the region would generate $310 million for the Community every year. This amounts to nearly three times the annual bloc’s budget and, as such solve for good, the irksome cash crunch often experienced by the EAC Secretariat.

EALA’s Dr James Ndahiro, an economist, in a past interview with The New Times, said a financing model whereby each partner state contributes one percent of its import revenue is the best option.

The 17th summit will also consider Council reports on: the Model, Structure and Action Plan of the EAC Political Federation; Implementation of the Framework for Harmonised EAC Roaming Charges.

Modalities for promotion of motor vehicle assembly in the region and reduction of the importation of used vehicles from outside the Community; and the promotion of the textile and leather industries in the region, and stopping importation of used clothes, shoes and other leather products from outside the region.

South Sudan, Somalia bid

South Sudan’s bid to join the Community suffered a setback following the mid December 2013 new break out of a civil war pitting forces loyal to previously sacked – and now reinstated – Vice-President Riek Machar against those supporting President Salva Kiir Mayardit.

The country seceded from Sudan in 2011 but the ensuing political unrest between government forces and Machar’s rebellion dampened its restoration.

Kiir has recently appointed Machar as vice president in a move to restore peace and resolve the country’s deepening economic crisis but it remains to be seen whether the lull will be sustainable.

After it became the world’s newest country almost five years ago, South Sudan’s public debt reportedly skyrocketed from zero to $4.2 billion.

Apart from South Sudan, the Summit is also expected to deliberate on a report by the Council on the verification exercise for the admission of the Republic of Somalia into the EAC.

The troubled Horn of Africa nation submitted its request in 2012 but it continues to be bogged down by the war against the al-Qaeda-linked al-Shabaab terrorists.

To become an EAC member, an applicant country’s government must – among other things – adopt policies that harmonise economically and politically with those of the bloc’s partner states.

Bloc’s e-Passport

While in Arusha, the EAC Heads of State are also expected to launch the new International East African e-Passport (electronic passport), yet another significant milestone towards achieving the integration agenda, during their meeting.

EAC’s senior official in-charge of communication, Owora Richard Othieno, disclosed that people in the region will from March be able to access the e-Passports that will help ease their movement in the trading bloc.

The e-Passport was scheduled for launch last November but it was postponed to allow more time to airbrush pending issues on the document.

Among others, the EAC Institutional Review is critical especially as the Council in April 2009 directed the Secretariat to undertake a comprehensive study and propose institutional reforms to boost efficiency in executing an expanded mandate.

Meanwhile, Tanzania’s President John Magufuli is scheduled to hand over the EAC chair to another leader who will be decided by the Heads of State.

It was supposed to be Burundi’s Pierre Nkurunziza’s turn to take over Chair but the latter has reportedly turned it down for the time being.

Related News

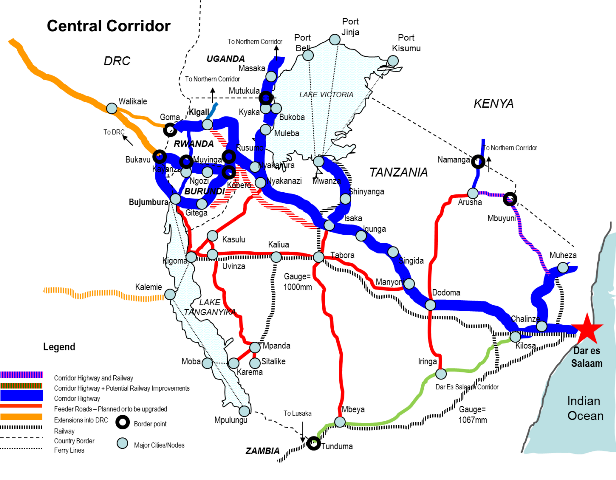

Ministers agree on fast-tracking Central Corridor railway line project

Infrastructure projects undertaken by the Central Corridor states, including the railway line, will be fast-tracked, ministers for infrastructure from Rwanda, Tanzania and Burundi resolved over the weekend.

The ministers have subsequently approved the plan to fast-track the Dar es Salaam-Isaka-Kigali/Keza-Musongati railway project along the corridor, Rwanda’s Minister for Infrastructure James Musoni has said.

Musoni added that the partner states also signed an agreement as commitment to meet construction, operation and maintenance requirements.

This was during an Inter-State ministerial meeting to discuss ways on how to implement the projects in Mwanza, Tanzania last week.

The meeting was also attended by Prof Makame M. Mbararwa, Tanzania’s Minister for Works, Transport and Communications, and Jean Bosco Ntunzwenimana, Burundi’s Minister for Transport, Public Works and Equipment.

Musoni, who led the Rwandan delegation, said the partner states also agreed to adopt a common legal framework and operational manual to allow seamless operations.

They will also set up an implementation unit under the Central Corridor Transit Transport Facilitation Agency to oversee the project.

The Central Corridor member states have for almost 10 years been working to improve the route to make it more competitive in the region. The railway line is one of the key projects member states are banking on to help reduce the cost of doing business along the corridor.

Experts say railway transport is the only way partner states can significantly reduce transport costs and make the corridor attractive to the private sector.

The main line, from Dar es Salaam to Isaka, is already in place. So far, the Central Corridor member states and development partners, including the World Bank and African Development Bank, have committed to rehabilitate the existing railway line. They are also working on the Dar es Salaam-Isaka-Musoganti project.

The ICM followed the 10th Executive Board Meeting of the Central Corridor were the Board Memebers (Permanent Secretaries of the Ministries incharge of Transport and representatives from Private Sectors) surveyed the Routes from Bujumhura, Kigali and Dar es Salaam and got a chance to visit Isaka Dry Port in Isaka Kahama before sat for the Board Meeting. Previously, Isaka Dry Port had been operating as a Dry Port for Central Corridor Countries where Cargo were moved by Train to Isaka and the shifted to Trucks.

The Central Corridor Secretariat also Donated two Landcruisers to Tanzania Police Forces for patrolling along the Central Corridor. This will help to increase Security along the Route on Tanzania Side.

Related News

Twenty-first annual review of the implementation and operation of the WTO Agreement on Technical Barriers to Trade

The WTO Committee on Technical Barriers to Trade will conduct its Twenty First Annual Review of the Implementation and Operation of the WTO Agreement on Technical Barriers to Trade (the TBT Agreement) under Article 15.3 at its next meeting on 9-10 March 2016. This document contains information on developments in the Committee relating to the implementation and operation of the TBT Agreement from 1 January to 31 December 2015.

In 2015, the Committee completed its Seventh Triennial Review. The Report includes a set of recommendations covering, among other things: good regulatory practices, regulatory cooperation between Members, conformity assessment procedures, standards and transparency. The reports also sets out a work programme of thematic sessions aimed at strengthening information exchange in the various cross-cutting areas covered by the TBT Agreement.

In terms of the Committee’s review of measures, during the year, notifications decreased by 12% compared to the previous year (to a total of 1,989 notifications). Nevertheless, the trend since 2015 has been an upward one driven increasingly by developing Members.

In 2015, developing Members continued to submit significantly more new notifications than developed Members – also the number of notifications from LDCs increased during the year.

In total, 86 specific trade concerns (STCs) were discussed in 2015, the second highest number since 1995. A much lower proportion of these, however, were notified to the Committee: only 49% of the STCs discussed had been notified (well below the long-run average of 68%).

On technical assistance (TA), the Secretariat delivered 18 TA events specifically targeted to the TBT Agreement and an additional 19 TBT modules were delivered as part of various other WTO TA activities.

Finally, ad hoc observer status was granted to the African Organization for Standardisation (ARSO) and the Intergovernmental Authority on Development (IGAD).

Review of TBT Measures

Notifications of technical regulations and conformity assessment procedures

Trends in new notifications and follow-up (addenda, corrigenda, revision)

In 2015, Members submitted 1,438 new notifications of technical regulations and conformity assessment procedures. In addition, 27 revisions, 476 addenda and 47 corrigenda to notifications were also submitted (Chart 1). In total, 1,988 TBT notifications were submitted in 2015 by 73 Members. While 2014 marked the year with most notifications in a single year since 1995, the number of notifications decreased by 12% in 2015. Nevertheless, 2015 was still the year with the fourth most notifications overall since 1995. Since 2007, Members have submitted more than 1,000 new notifications annually with that figure increasing to 1,500 since 2012. Since the entry into force of the Agreement and up to 31 December 2015, a total 25,390 notifications have been submitted by 128 Members. The number of notifying Members increased by 2 in 2015 as Suriname and Yemen notified for the first time.

Over the last decade there has been a marked growth in the use of addenda and corrigenda, with a record 675 notified in 2014. In 2015, this number decreased to 523 notified addenda and corrigenda. The US (1,200), Brazil (533), Ecuador (529), Colombia (323) and the EU (307) have notified the most addenda and corrigenda since 1995.

The overall relation between new notifications, addenda and corrigenda, and revisions is illustrated in Chart 2. The Committee adopted a recommendation on “Coherent Use of Notification Formats” in 2014 which provides Members with guidance on when to use different formats. It is recommended that Members use: new notifications “to notify the draft text of a proposed technical regulation or conformity assessment procedure”; addenda “to notify additional information related to a notification or the text of a notified measure”; corrigenda “to correct minor administrative or clerical errors (which do not entail any changes to the meaning of the content)”; and revisions “to indicate that the notified measure has been substantially re-drafted prior to adoption or entry into force.”

While the number of revisions has also grown, this format is used infrequently. China (31), Brazil (20), Canada (16), South Africa (14) the Dominican Republic (10) and Korea (9) have notified most revisions since 1995.

Members’ engagement in notifications

2014 showed a new trend indicating more notifications from Members that had been historically less active. This partly continued in 2015 as observed over the period 1995-2014 In 2015, for example, the US again led by numbers of new notifications (283) followed by Ecuador (126) (Member which notified most in 2014) and Brazil (115). China was more active in 2015 than in 2014, submitting 106 notifications compared to 49 in 2014. Uganda submitted 100 notifications in 2015.

Three consecutive years of significant notification activity has placed Ecuador (126 in 2015; 420 in 2014; 103 in 2013) among the ten Members that have notified most measures over the period of 1995-2015. Korea has dropped out of the “top ten” category following Japan with a total number of 765 notifications in 2015.