Search News Results

South Africa Merchandise Trade Statistics for February 2016

The South African Revenue Service (SARS) has released trade statistics for February 2016 that recorded a trade deficit of R1.07 billion. This figure includes trade data with Botswana, Lesotho, Namibia and Swaziland (BLNS).

Including trade data with Botswana, Lesotho, Namibia and Swaziland (BLNS)

The R1.07 billion deficit for February 2016 is due to exports of R90.68 billion and imports of R91.75 billion, improving from a revised deficit of R17.96 billion in January 2016. Exports increased from January 2016 to February 2016 by R19.29 billion (27.0%) and imports increased from January 2016 to February 2016 by R2.39 billion (2.7%).

On a year-on-year basis, the R1.07 billion deficit is an 85.8% decrease on the deficit recorded in February 2015 of R7.53 billion. Exports of R90.68 billion are 16.5% more than the exports recorded in February 2015 of R77.82 billion. Imports of R91.75 billion are 7.5% more than the imports recorded in February 2015 of R85.35 billion.

The cumulative deficit for 2016 of R19.03 billion is 38.5% less than the deficit for the comparable period in 2015 of R30.96 billion.

The month of January 2016 trade balance deficit was revised upwards by R0.09 billion from the previous month’s preliminary deficit of R17.87 billion to a revised deficit of R17.96 billion.

Trade highlights by category

The month-on-month export movements (R’ million):

| Section: | Including BLNS: | |

| Vehicle & Transport Equipment | + R6 596 | + 109.1% |

| Precious Metals & Stones | + R5 908 | + 51.9% |

| Machinery & Electronics | + R1 962 | + 28.1% |

| Vegetable Products | + R1 279 | + 34.8% |

| Mineral Products | - R1 373 | - 8.2% |

The month-on-month import movements (R’ million):

| Section: | Including BLNS: | |

| Vehicle & Transport Equipment | + R 1 671 | + 19.1% |

| Equipment Components | + R 939 | + 13.3% |

| Textiles | + R 898 | + 24.1% |

| Vegetable Products | + R 677 | + 28.5% |

| Machinery & Electronics | - R1 668 | - 6.9% |

| Mineral Products (Including Crude Oil) | - R 620 | - 5.7% |

Trade highlights by world zone

The world zone results from January 2016 to February 2016 are given below.

Africa:

Trade surplus: R14 320 million – this is a 21.4% increase in comparison to the R11 798 million surplus recorded in January 2016.

America:

Trade deficit: R2 606 million – this is a 27.1% decrease in comparison to the R3 573 million deficit recorded in January 2016.

Asia:

Trade deficit: R13 365 million – this is a 24.1% decrease in comparison to the R17 620 million deficit recorded in January 2016.

Europe:

Trade deficit: R7 060 million – this is a 44.6% decrease in comparison to the R12 752 million deficit recorded in January 2016.

Oceania:

Trade surplus: R 517 million – this is an improvement in comparison to the R 285 million deficit recorded in January 2016.

Excluding trade data with Botswana, Lesotho, Namibia and Swaziland (BLNS)

The trade data excluding BLNS for February 2016 recorded a trade deficit of R9.21 billion, with exports of R79.39 billion and imports of R88.60 billion. Exports increased from January 2016 to February 2016 by R18.15 billion (29.6%) and imports increased from January 2016 to February 2016 by R1.82 billion (2.1%).

The cumulative deficit for 2016 is R34.76 billion compared to R46.38 billion in 2015.

Trade highlights by category

The month-on-month export movements (R’ million):

| Section: | Excluding BLNS: | |

| Vehicles & Transport Equipment | + R6 204 | + 120.9% |

| Precious Metals & Stones | + R5 665 | + 53.7% |

| Machinery & Electronics | + R1 618 | + 28.6% |

| Prepared Foodstuff | + R1 442 | + 80.3% |

| Vegetable Products | + R1 253 | + 40.3% |

The month-on-month import movements (R’ million):

| Section: | Excluding BLNS: | |

| Vehicles & Transport Equipment | + R1 657 | + 19.1% |

| Equipment Components | + R 939 | + 13.3% |

| Textiles | + R 788 | + 23.2% |

| Vegetable Products | + R 690 | + 29.7% |

| Machinery & Electronics | - R1 730 | - 7.3% |

Trade highlights by world zone

The world zone results for Africa excluding BLNS from January 2016 to February 2016 are given below.

Africa:

Trade surplus: R6 173 million – this is a 46.3% increase in comparison to the R4 218 million surplus recorded in January 2016.

Botswana, Lesotho, Namibia and Swaziland (Only)

Trade statistics with the BLNS for February 2016 recorded a trade surplus of R8.15 billion, with exports of R11.29 billion and imports of R3.14 billion. Exports increased from January 2016 to February 2016 by R1.14 billion (11.2%) and imports increased from January 2016 to February 2016 by R0.57 billion (22.1%).

The cumulative surplus for 2016 is R15.73 billion compared to R15.42 billion in 2015.

Trade Highlights by Category

The month-on-month export movements (R’ million):

| Section: | BLNS: | |

| Vehicles & Transport Equipment | + R 392 | + 42.8% |

| Machinery & Electronics | + R 343 | + 26.2% |

| Precious Metals & Stones | + R 244 | + 29.3% |

| Prepared Foodstuff | - R 343 | - 25.5% |

| Mineral Products | - R 298 | - 16.1% |

The month-on-month import movements (R’ million):

| Section: | BLNS: | |

| Chemical Products | + R 122 | + 22.4% |

| Precious Metals & Stones | + R 115 | + 31.0% |

| Textiles | + R 110 | + 33.3% |

| Live Animals | + R 67 | + 41.9% |

| Machinery & Electronics | + R 62 | + 23.6% |

Related News

The importance of investing in built-to-last infrastructure

The Global Infrastructure Forum being organized by multilateral development banks (MDBs) next month in Washington, D.C. comes at an opportune time. The adoption of the Sustainable Development Goals and the Paris Agreement on climate action have generated valuable political momentum to set the world on a path toward better and more sustainable development outcomes.

Infrastructure is at the core of this agenda. It is a major driver of economic growth and inclusive development. It is also key to tackling climate change. Done badly, it is a major part of the problem; infrastructure currently accounts for around 60 percent of the world’s greenhouse gas (GHG) emissions. Done right, it is a major part of the solution; sustainable infrastructure mitigates GHG emissions and builds resilience to climate change.

Globally, investment needed in infrastructure over the next 15 years is estimated at more than $90 trillion. On an annual basis, infrastructure investment will have to more than double from $2.5-3 trillion currently to more than $6 trillion. As much as three-quarters of the new investment will need to take place in the developing world, particularly middle-income economies. The estimated investment needs over the next 15 years are almost twice the value of the entire infrastructure stock today. This presents a big challenge, but also an opportunity to remake our physical environment in a better way.

The world needs to build more infrastructure but build it to last in the new climate economy. There is a great danger of locking in high-carbon, polluting, and unsustainable pathways if the new infrastructure is built in much the same way as before. But if the new investments are designed to factor in climate risks, they can not only bridge the infrastructure gap to support growth and development but also protect the climate. This means investing in renewable energy, cleaner transport, efficient and resilient water systems, and smarter cities.

Delivering sustainable infrastructure at scale will require strong public policy leadership and active private-sector engagement, including important transformations in the way infrastructure investments are developed and financed. Specific actions must be tailored to individual country circumstances. However, the main elements of the agenda can broadly be captured under four “I”s: investment, incentives, institutions, and innovation.

Boosting investment in infrastructure to more than twice current levels will require substantial increases in public sector’s own investment and policies to catalyze a major scale-up of private investment. The generally negative trend in public investment rates over the past couple of decades, which exacerbated infrastructure gaps, must be reversed. Given the scale of the needs, and fiscal constraints in many countries, more than half of the new investment will have to come from the private sector. Policy risks and costs of doing business must be reduced to attract more private investment.

Market incentives must be reformed to orient new investment towards sustainable infrastructure. Removal of fossil-fuel subsidies and implementation of carbon pricing are crucial. The current low petroleum prices provide an opportunity to jumpstart reform. Pricing reform is also needed in sectors beyond energy, such as water. Getting prices right and reforming regulation to correct incentive distortions put markets to work in support of public policy goals.

The quality and impact of higher investment will depend greatly on the strength of public institutions. Especially important are capacities to develop strong pipelines of sustainable projects and improve institutional frameworks for public-private partnerships. As much as 70 percent of total investment in sustainable infrastructure will be connected with urban areas. So institutional and fiscal strengthening of cities merits particular attention.

Technological innovation expands possibilities by providing new and more efficient technologies for low-carbon, climate-resilient infrastructure. Fiscal and financial innovation will be important in capturing those possibilities. Investment in research and development, notably in renewable energy technologies, should be boosted. Mobilizing financing for sustainable infrastructure at scale will require enhancing and creatively utilizing fiscal space, and leveraging private finance and lowering its cost through innovations in financial instruments and use of development capital. Carbon taxation can raise substantial revenue as well as improve tax structure. Globally, assets under management by banks and institutional investors amount to more than $120 trillion but only about 5 percent of those are invested in infrastructure. Innovations to promote infrastructure as an asset class and tap these large pools of savings will have a high payoff.

The foregoing public policy agenda is primarily the responsibility of national governments. But there is an important role for international cooperation through collective actions and technical and financial support. For emerging and developing economies, MDBs in particular will be a key partner in building capacities and mobilizing financing. The scale of the sustainable infrastructure challenge will require enhancements in the capabilities of these institutions. The Global Infrastructure Forum provides an important opportunity for the MDBs and their development partners to translate the current favorable political momentum into a more concrete action agenda to step up sustainable infrastructure development. It must not be missed.

Zia Qureshi is currently a Nonresident Senior Fellow in the Global Economy and Development program. Formerly, he was a Director in the Development Economics Department of the World Bank.

Related News

Trade turbulence

China’s transition to a new growth path is contributing to trade volatility today and will shape trade opportunities tomorrow

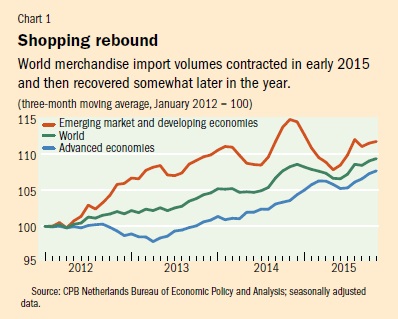

Global trade has been a puzzle lately. In the 2000s, and especially after the Great Recession, trade growth has been persistently sluggish relative to GDP. And 2015 appears to have added a new dimension: volatility. Available data indicate that global trade contracted sharply in the first half of the year before beginning to grow again, albeit slowly.

In a previous article (“Slow Trade,” in the December 2014 F&D), we examined the cyclical and structural factors behind the global trade slowdown: weak demand, maturing value chains, and slower trade liberalization than in the 1990s. These forces are all still at work and contributed to the weak growth of world trade in 2015.

The trade fluctuations in 2015 may reflect turbulence as China adjusts to a new, slower growth path that is less dependent on investment and industrial production. China’s transition has strikingly different implications for countries depending on their main exports. Some of these effects are temporary; others are more structural. Manufacturers (especially in east Asia) suffered significant declines in export quantities but are now recovering; commodity producers were hurt primarily by lower export prices, which persist; and services exporters have benefited in a way that could presage future opportunities.

A most peculiar year

After a period of low but fairly consistent trade growth, preliminary data for 2015 show a sudden contraction in trade volume of about 3 percent quarter over quarter in the first half of the year (see Chart 1). In the third quarter of 2015, growth appears to be positive again but weaker than in the second half of 2014. The contraction and partial rebound were concentrated in emerging market economies.

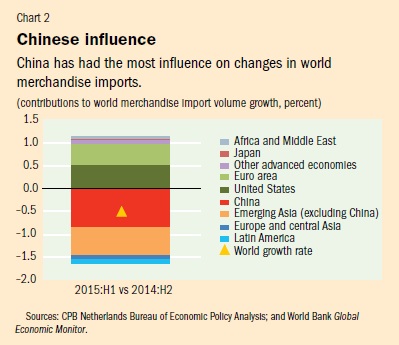

Emerging Asia, which accounts for more than a quarter of world trade, seems to have been the epicenter of the 2015 trade downturn and incipient rebound. According to preliminary figures, in the first half of 2015 emerging Asia’s imports dropped by 10 percent, accounting for nearly 90 percent of the contraction in world import volumes. China alone saw a contraction in import volumes of 15 percent and was responsible for more than half of the contraction in world imports (see Chart 2). The reversal of these trends in the region in the third quarter is contributing to the rebound that we observe in world trade, although trade growth in 2015 was still weaker than in 2014. Developments in other regions also matter. In particular, lower imports from crisis-stricken commodity exporters such as Brazil and Russia – in part reflecting lower demand in China, as discussed below – have contributed to falling global imports.

Napoleon’s prophecy

Napoleon is reputed to have said, “When China wakes, the world will shake.” Indeed, short-term macroeconomic fluctuations as China’s economy shifts from investment and manufacturing to consumption and services are affecting the pattern of production and trade in east Asia and beyond. These changes are manifested in manufacturing, commodities, and services trade.

On the production side, the slowdown in GDP has been concentrated in the industrial sector, which depends more on imported inputs than do other sectors of the economy; imported inputs make up 11.5 percent of total inputs in the industrial sector and only about 6 percent in other sectors. On the demand side, the slowdown is more significant in investment, which has greater, though declining, import intensity than other components of total demand. The import intensity of China’s investment is more than 50 percent higher than that of its consumption. Investment-related imports account for almost 60 percent of China’s total imports, and for 11 percent of the world’s investment-related imports (second only to the United States).

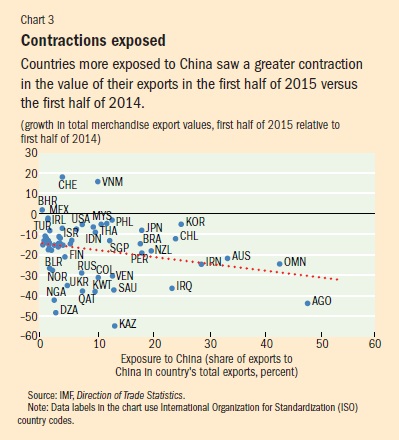

The contraction in China’s imports was distributed across all the regions of the world. Countries more exposed to China, as measured by that country’s share in their total exports, tended to see a greater contraction in the value of their exports in the first half of 2015 than in the corresponding period in 2014 (see Chart 3). Bilateral trade data for the third quarter are not yet available. A 1 percent higher exposure to China meant a 0.3 percent greater contraction in the growth of value of a country’s exports. The reduction in value of exports was attributable to lower prices and lower quantities, varying across regions depending on the composition of their exports. The slower growth in imports from large commodity exporters, such as those in the Middle East and sub-Saharan Africa, reflects the recent drop in prices; the sizable contraction in imports from emerging Asia, especially in the first quarter of 2015, resulted largely from lower quantities.

Magnifying chains

The impact on manufacturing was most visible in east Asia, which experienced a regional trade collapse. China is an important ultimate destination for the value-added exports of other Asian countries. Data available for five countries in east and south Asia indicate that about 50 percent of gross exports of these countries to China constitute value added that is ultimately absorbed in China, and therefore fully dependent on Chinese demand. Another 20 percent of regional exports are reexported by China and consumed in third countries, and therefore not dependent on China’s demand. The remainder constitutes foreign value added in a particular country’s gross exports to China, which originates elsewhere in the region and beyond.

The impact of macroeconomic changes in China may have been magnified by changes in the composition of economic activity. Production shifted away from sectors that are associated with global value chains – that is, from industrial production to services and, within industrial production, from capital goods (equipment and machinery) to consumption goods. Given the extensive network of supply chains in east Asia, this magnification effect likely affected intraregional trade flows more than interregional trade.

In the longer term, the recovery of global trade will, on one hand, be limited by diminished growth in demand in China; on the other hand, it will be boosted by the relocation of production away from China toward other lower-cost economies. Rebalancing from investment to consumption is likely to create opportunities for exporters of final goods and may also eventually boost upstream intermediate and capital goods sectors that are now adversely affected.

Nominal troubles and real opportunities

Commodity exporters saw no decline in export volumes. Exporters in Africa, the Middle East, eastern Europe and central Asia, and Latin America did experience lower trade values, but that was largely because of falling commodity prices – that is, a nominal rather than a real contraction. This evidence suggests primarily a price response to expectations of diminished demand for commodities and enhanced supply in sectors like oil and gas. Nevertheless, deterioration in the terms of trade for commodity producers has hurt real incomes for that group and contributed to recessions in countries such as Brazil and Russia, leading to a further contraction in commodity exporters’ import volumes.

Africa and the Middle East are emblematic of these nominal troubles. Having experienced the deepest plunge in export values since mid-2014, Africa and the Middle East contributed significantly to the recent decline in world trade values. Mostly a nominal phenomenon driven by changing prices, the downturn in oil and commodity exports also reflects sluggish volume growth in recent years. China and other emerging Asian economies together account for more than half of the decline in export values of Africa and the Middle East.

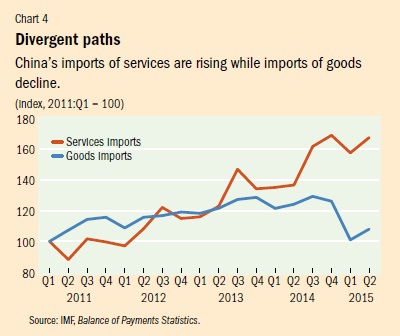

The rebalancing of the economy from investment to consumption is also shifting China’s demand from goods to services. Some of this demand is being served by cross-border imports and consumption abroad – whose growth is already visible. Available data indeed show the different dynamics of goods and services imports in recent years, with slowing imports of goods and rising imports of services, especially travel (see Chart 4). The latter may reflect consumption abroad of services ranging from tourism to education and health. But it is also possible that these data capture other short-term factors such as disguised or illegal capital outflows.

Services imports are growing, but trade in goods still dominates. The net effect is influenced largely by the decline in imports of goods, because services were a relatively small share of total imports of China in 2014. But the share of services has grown – from about 15 percent at the beginning of 2011 to close to 22 percent in the first half of 2015.

Mind the transition

Looking ahead, the rebalancing of the Chinese economy will unquestionably influence trends in world trade. But how the transition is managed will affect how much global trade fluctuates in the coming years.

Diminished growth in China, as well as the national shift in emphasis from investment to consumption, is affecting manufacturing and commodity exporters. The changing composition of demand is likely to favor exporters of consumption goods and eventually of upstream intermediate and capital goods used in their production. In the longer term, rising wages in China may also encourage industrial production and exports in lower-cost economies, and in turn enhance demand for commodities. Finally, the rebalancing is also shifting China’s demand from goods to services, and these imports may grow even faster if services markets continue to open up.

Cristina Constantinescu is an Economist and Michele Ruta is a Lead Economist, both in the Trade & Competitiveness Global Practice of the World Bank, and Aaditya Mattoo is Research Manager, Trade and International Integration, at the World Bank.

This article is based on a World Bank report by the authors, “Global Trade Watch: Spillovers from China’s Rebalancing.”

Related News

tralac’s Daily News Selection

The selection: Wednesday, 30 March 2016

Featured alerts, commentary:

South Africa’s February 2016 trade data will be released tomorrow. Bloomberg consensus sees a compression of the deficit to -R4.3bn.

The Commonwealth Trade Expert Group is meeting in Delhi, discussing 'Revitalising global trade and multilateralism'

Joshua P Meltzer: 'New trade deals challenge Africa to step on to the global stage' (The Guardian)

Rwanda: Trade deficit grows in first two months of 2016 (New Times)

According to a statement from the central bank yesterday, the country’s trade deficit widened to $297.2m (about Rwf232.4bn) largely due to an increase in formal imports that rose by about 7.2%, as well as a 9.7% decrease in the value of Rwanda’s exports. The international trade developments were among the focus of discussions during yesterday’s quarterly financial stability committee and monetary policy committee meetings chaired by the National Bank of Rwanda governor, John Rwangombwa.

South Africa: Poultry crowd rubs salt in own wounds (Business Day)

The South African Poultry Association is trying to get the South African International Trade Administration Commission to institute an agricultural safeguard on EU chicken. An agricultural safeguard is not dissimilar in effect to the antidumping duty that is no longer imposed on US bone-in chicken, except that it operates in three-year cycles. The association is essentially looking to institute protectionist action in the form of a 37% import tariff on EU bone-in chicken. [The author, David Wolpert, is CEO of the Association of Meat Importers and Exporters SA] [Call for steps against duty-free European chicken] [AGOA sword will keep hanging above SA]

Kenya's tea sector: value chain capacity assessment project launch (ACBF)

The assessment will undertake a comprehensive review of capacity assets, needs and options for strengthening capacity of key targeted institutions responsible in the value-chain of the tea product. The review will also identify structural and institutional factors including agents that can influence change resulting from a capacity development investment to improve the performance of the product. These factors will include the conduciveness of the socio-political environment, efficiency of prevailing policy instruments, effectiveness of organizational arrangements, as well as technical skills and knowledge. The assessment is expected to be finalized by the end of May 2016. [Further details: KIPPRA]

Recent papers published by the COMESA Monetary Institute:

Challenges of dollarization in COMESA: Governors noted the following recommendations from the study [extract] : i) Successful de-dollarization requires implementation of an appropriate mix of sound macroeconomic policies, market-based incentives, and micro-prudential measures including: ii) There is need for countries to avoid policies that may lead to stagflation and severe macroeconomic disruptions which precipitates the need for dollarization.

Enhancing the effectiveness of fiscal policy for domestic resource mobilization in the COMESA region: In the COMESA region, as elsewhere, fiscal policy can and should be used effectively to foster growth, reduce short term fluctuations of economic activity and maintain economies close to their potential growth paths. The necessity to carry out these tasks is emphasized by the following conclusions [extract]: i) Domestic revenue to GDP ratios remain low for most member countries (figure 2) attributed to among others low per capita income and growth, institutional problems and weak governance. Addressing these challenges provides a case for fiscal policy in domestic resource mobilization. [COMESA Committee of Governors of Central Banks: meeting report, 19 November 2015]

AfDB President rounds up Asian tour in Beijing with firm commitments for support (AfDB)

Most of the cooperation commitments discussed at the meetings will be concretized at the Bank’s 2016 Annual Meetings in Lusaka, Zambia. The Bank’s staff involved in Japan, Korea and China will be very activate in the coming days refreshing MOUs and writing the terms of new cooperation agreements, a member of the delegation said.

African Institute for Economic Development and Planning: progress report (UNECA)

Now that the strategic framework has been defined globally, time has come for an contextualized action in 2016, to translate these agenda into national, subregional and regional objectives. IDEP will therefore reorganize itself in order to adapt its offer to a changing environment and - as previously - pursue its support to member States in setting up training programmes in full compliance with the requirements of their transformative agenda.

Training of trade counsellors from IGAD livestock exporting countries to GCC countries (IGAD)

The IGAD Centre for Pastoral Areas and Livestock Development, in collaboration with FAO SFE, organized the training of trade counselors in Addis Ababa, 21-24 March. The activity was funded by an Italian-funded project. The limited exports has partly been due to limited coordination between the trade counsellors, exporters and chief veterinary officers. The gap has been in terms of real time market information and dissemination on import requirements as well as commodity prices and limited promotional and linkage efforts. The workshop made the following recommendations: [Zuma consolidates ties in the Gulf region (IOL)]

Nigeria: trade diplomacy, foreign policy perspectives (Daily Trust)

Q to Minister of Foreign Affairs, Geoffrey Onyeama: After one year, what should Nigerians expect from the ministry? 'We are faced with severe economic challenges. What can we, as a ministry, do? We decided on economic diplomacy as the framework in which we want to operate. We have identified two areas. First, we are looking at a strategy of targeting a number of African countries to have with them an agreement for the free movement of business people within Africa in order to enlarge the economic space for Nigerian businessmen. The second is to develop a matchmaking data base where Nigerian business persons can upload information about themselves, businesses and what they want to sell to the world and this would be accessible through our 119 foreign missions.'

Nigeria's promise turns to peril as investors head for the exits (Bloomberg)

Nigeria’s appeal has faded as the price of oil, source of 90% of export earnings, has crashed. Growth slumped to 2.8% last year, the slowest since 1999, and will decelerate to 2% in 2016, according to Morgan Stanley. In dollar terms, the economy in 2019 will still be 17% smaller than its 2014 peak of $542bn. Only two years ago, McKinsey & Co. said Nigeria had the potential to grow 7.1% annually until 2030 and build a $1.6trn economy. [Nigerian lawmakers want wireless giant MTN's fine doubled to eye-popping $10bn (M&G Africa)]

Total readies Shs13 trillion for oil pipeline development (Daily Monitor)

French oil major Total S.A has said it will finance the development of the $4b (Shs13 trillion) crude oil export pipeline from Uganda’s Albertine Graben to Tanzania’s Tanga port at the Indian Ocean. Mr Javier Rielo, the Total East Africa vice president, on Monday, assured Tanzanian President John Magufuli that “the company will begin construction of the pipeline project to transport oil from Uganda to Tanga as soon as possible, for funds to implement the project exist.”

Is the WTO a World Tax Organization? A primer for WTO rules for policy makers (IMF)

This paper examines the extent to which World Trade Organization rules impinge on policy makers’ freedom to formulate tax policies. It provides an overview of both the economic rationale for WTO rules concerning taxation and the provisions of the main WTO agreements concerning border taxes and internal taxes (direct as well as indirect). It also points out some tax anomalies and inconsistencies in these rules, and how the rules have evolved as a consequence of the interpretation of the WTO agreements by its Dispute Settlement Body and the latter’s rulings in connection with several disputes over taxes affecting trade. [The author: Michael Daly]

International regulatory co-operation: the role of international organisations (OECD)

In order to strengthen the information base on this topic and shed light on the contribution of IOs to IRC, the OECD carried out in 2015 a survey covering the governance, operational modalities and tools of IOs, as well as their rule-making disciplines and assessment of implementation and impacts. For most IOs, the main benefits provided by their IRC activities come from increased transparency of regulatory frameworks, knowledge flow and peer learning through exchange of information. Secondly, they promote efficiency gains and reduction of regulatory burdens through the sharing of tasks and increased coherence across regulatory requirements. The economic benefits, such as reducing regulatory burden or fostering economies of scale, come last.

Local nexus and jurisdictional thresholds in merger control (OECD)

Background paper by the Secretariat: Three years later, this paper seeks to provide a detailed overview of merger control thresholds and local nexus criteria in various countries, and to compare them with international recommendations on the topic. The paper is structured as follows: chapter 2 will provide some background on the topic of merger control thresholds and local nexus criteria; chapter 3 will describe the various types of notification thresholds and local nexus criteria adopted in different countries; chapter 4 will compare current practices to international guidelines, and identify the main developments since the Recommendation was adopted in 2005; and, finally, chapter 5 will summarise and analyse the main findings. [Annex to the Background Paper]

Related: Best practice roundtables on competition policy: June 2016, OECD, Public interest considerations in merger control: background paper

Over-The-Top (OTT) Services and regulation (tralac)

A close connection is developing between the rules of international trade on market access, domestic regulation and network neutrality. This is increasingly subject to trade negotiations. However, a comprehensive classification of the different facets of OTT services is yet to be developed. [The author: JB Cronje]

Going beyond goods: measuring services for export competiveness (World Bank)

Many governments are interested in how services support their country’s exports and economy at large. Answers to such questions are typically left unanswered because systematic data is not readily available on how services contribute to exports across developing countries and sectors. The Export of Value Added Database was developed to fulfill this need. What sets the EVA Database apart is the wide coverage of developing countries: over 70 of the economies included are low- and middle-income.

Egypt, World Bank sign $5m grant to ease regulatory environment for investors (World Bank)

Asian Development Outlook 2016 (ADB)

Growth is slowing across much of developing Asia as a result of the continued weak recovery in major industrial economies and softer growth prospects for the People’s Republic of China (PRC). This will combine to push growth in developing Asia for 2015 and 2016 below previous projections, says a new Asian Development Bank report. In its new Asian Development Outlook (ADO) 2016, ADB forecasts GDP growth of 5.7% in 2016 and 2017 for the region. In 2015, GDP growth was 5.9%. ADO is ADB’s flagship annual economic publication. [Downloads]

Related, regional perspectives: The benefits of regional electricity cooperation and trade: lessons from South Asia (World Bank), ADB, JICA establish $1.5bn fund to invest in private infrastructure (ADB), With RCEP commitment, India marks big shift in trade policy (Livemint), Roberto Azevêdo speech: 'Brazil in the global trading system: achievements and future challenges' (WTO), DG Azevêdo welcomes Brazil’s ratification of WTO trade facilitation deal (WTO)

Swaziland has to borrow $422.1m - official (StarAfrica)

Challenges for EAC to phase out 'Caguwa' by 2019 (New Times)

Mozambique/Swaziland: new bridge to boost trade (StarAfrica)

Tanzania: Ruvu gas find could be worth up to $11bn (IPPMedia)

East Africa: 'Chambers can issue Certificates of Origin' (editorial comment, East Africa Business Week)

Oil prices and the global economy: it’s complicated (IMF)

London Stock Exchange launches Africa Advisory Group to boost African capital market development

GREAT Insights: Partnerships with business for development (ECDPM)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

tralac in the news ~ African countries should diversify exports to adapt to changes in China

The ongoing changes in China’s economy may be an opportunity for African countries that now mainly export raw materials and oil, to adapt and diversify exports and move up the value chain, according to analysts.

China, Africa’s main trading partner, has registered an economic slowdown and the authorities want the “engine” of growth in the coming years to be domestic consumption rather than investment, which will affect external demand, particularly in sub-Saharan Africa, according to an analysis by the Trade Law Centre for Southern Africa (tralac).

“As Chinese domestic demand changes from investment goods for domestic consumption and, implicitly, to services, exporters of food and services can gain from the change,” said the March analysis of the China Africa Trading Relationship.

This will offset the impact of reduced demand for African imports and the fall in commodity prices, which will have a negative impact on global prices of such goods, affecting the terms of trade.

“It is therefore imperative for African countries to diversify exports and move up the value chain,” says the document.

Angola, for which oil is the main export and the basis of its economy, is among the countries where efforts to diversify exports are most visible, following the fall in revenue related to the oil price drop since mid 2014.

The increase of Chinese trade with Africa – to USD221.5 billion in 2014, more than 20 times that recorded in 2001 – was driven “by the large bill on oil imports, mainly from Angola,” the Trade and Law Center said.

Figures from UN Comtrade (United Nations Commodity Trade Statistics Database) for 2014 put Angola as the second largest source of Chinese imports in Africa, with 27 percent of the total, behind South Africa (39 percent), and 5th largest destination for exports with 6 percent.

After the last Forum on China-Africa Cooperation (Johannesburg, 4-5 December 2015), economist Mark Bohlund in an article for Bloomberg Intelligence, noted that the slowdown in China would be another “jolt” for African countries.

The fall in oil prices, he argues, is more of a result of increased production in the United States than a reduction of imports by China – whose economy continues to grow, from a higher base.

The drop in investment levels, he said, mainly reflects the devaluation of some mining assets and “investment financed by debt is much more important for Africa than FDI and should continue to grow as China expands the scope of projects financed in Africa.”

“Chinese investment in infrastructure in sub-Saharan Africa is more likely to increase than decrease,” taking into account the Chinese central bank’s transfers to the Export Import Bank of China ($45 billion) and the China Development Bank ($48 billion) in July 2015 to finance the New Silk Road strategy, said Bohlund.

The Chinese authorities have been arguing that even in the current context of slowdown, Africa investment and will continue and even become more important.

Li Yifan, the Chinese Ambassador to Ethiopia told the Reuters news agency on 15 March that African countries may even be “the ideal place” for business investment of companies that “have driven the expansion of Chinese infrastructure in the last 30 years,” at a time when the domestic economy is slowing and they are increasingly looking to foreign markets.

“Despite all the doubts, I can share that in China the relevant government departments, development banks, and insurance companies are addressing their African partners to make this great plan a reality,” said Li.

» Read the China Africa Trading Relationship, March 2016 update

Related News

Is the WTO a World Tax Organization? A primer for WTO rules for policy makers

This paper examines the extent to which World Trade Organization (WTO) rules impinge on policymakers’ freedom to formulate tax policies. It provides an overview of both the economic rationale for WTO rules concerning taxation and the provisions of the main WTO agreements concerning border taxes and internal taxes (direct as well as indirect).

It also points out some tax anomalies and inconsistencies in these rules, and how the rules have evolved as a consequence of the interpretation of the WTO agreements by its Dispute Settlement Body and the latter’s rulings in connection with several disputes over taxes affecting trade.

As WTO Members will undoubtedly want to avoid having their tax policies successfully challenged in the WTO, the paper provides some guidance concerning the design of tax policy.

Introduction

Despite more than six decades of multilateral trade liberalization unleashed by the General Agreement on Tariffs and Trade (GATT) in 1947, protectionist policies persist in many international goods markets. Perhaps the greatest challenge regarding the design of multilateral trade rules is the concern that trade liberalization commitments with respect to one policy instrument, such as tariffs, may be vitiated by other protectionist instruments unconstrained by such rules. Consequently, multilateral trade and other agreements must address a wide range of potentially protective measures, including tax measures other than tariffs.

Tariffs and other indirect taxes, whether levied at the border or internally, have long been subject to the binding multilateral rules embodied in the GATT. However, in recognition of the fact that tax measures can be used as substitutes for other types of protection and government assistance or regulation, direct as well as indirect taxes have come under increased scrutiny at the World Trade Organization (WTO). This recognition is reflected in several of the agreements negotiated under the Uruguay Round, notably those concerning subsidies and trade-related investment measures (TRIMs). These agreements reflect the realization by national governments that multilateral rules need to play an increasingly important role in regulating the use of tax as well as non-tax measures, especially where these measures affect the international movement of goods, services, capital, technology and persons.

As a consequence of these agreements, the range of tax measures challenged by WTO Members has widened considerably beyond the more traditional trade taxes. Since 1995, taxation has been the cause of over 40 of the 500 disputes that have been initiated with Members’ requests for consultations submitted to the WTO’s Dispute Settlement Body (DSB), which is now arguably the world’s most prolific international dispute resolution system. Roughly half of these disputes have resulted in the establishment of panels and consequent rulings by the DSB. The DSB’s rulings against Indonesia’s National Car Programme and especially against the United States concerning the latter’s Foreign Sales Corporation (FSC) scheme, which, at the time, led to the largest retaliation award ever authorized in a dispute at the WTO, are particularly noteworthy. These rulings confirmed, if there were ever any doubt, that, generally speaking, direct as well as indirect taxes (including, of course, not only tariffs), are subject to WTO rules, notwithstanding efforts by tax authorities to secure specific exemptions for certain direct tax measures in these agreements. The FSC ruling also reconfirmed the traditional distinction under multilateral trade rules between direct and indirect taxes, especially with respect to how such taxes should be treated under the border tax adjustment and subsidy rules of the WTO. It would not be surprising if other WTO-inconsistent tax measures were identified in the future, leading to further disputes among WTO Members. WTO rules can therefore be expected to continue to be an important factor in shaping tax policies, as Members will undoubtedly want to avoid having their tax policies successfully challenged in the WTO.

This paper provides an overview of the extent to which taxation is subject to WTO rules, which embody the fundamental principles of non-discrimination, predictability and transparency. Section II provides a synopsis of the possible economic rationale for these principles (and thus the main provisions of the GATT/WTO agreements), which can be ignored by readers already familiar with the basic theory of trade policy instruments. Section III focuses attention on the basic rules of the GATT/WTO agreements as well as several other provisions that are especially relevant for tax policymakers. Section IV examines how these rules have been interpreted by the DSB in a few selected cases concerning tax measures. Section V contains some concluding remarks. The Annex provides some guidelines concerning WTO rules for tax policymakers.

Economic Rationale for WTO Rules

Before providing an overview of the extent to which GATT/WTO rules encompass taxation, this section considers the possible economic rationale for the main rules and their underlying principles, namely non-discrimination, predictability and transparency. The broad aim of these rules is to regulate, if not remove, distortions to trade. These distortions contribute to economic inefficiency, by, for example, reducing consumer choice, raising prices to consumers, including downstream processors, and disrupting global supply chains, thus impeding economic development. Attention here is focused mainly on the GATT because the fundamental principles and consequent obligations embodied in this agreement form the basis for the other WTO agreements, such as the General Agreement on Trade in Services (GATS). In some respects, however, WTO tax rules appear to be anomalous or, indeed, inconsistent with economic theory concerning trade taxation.

Notwithstanding the considerable progress made in dismantling barriers to trade as a result of multilateral negotiations under the auspices of the GATT/WTO, protectionist policy measures are still widely used by WTO Members for various reasons, compelling or not. These may include: shifting the terms-of-trade in a country’s favour; protection of specific domestic “infant” industries; correction of “market failure”; conservation of natural resources; assistance to downstream processing of such resources; food security; or as a counterbalance to domestic or other countries’ trade distortions (in accordance with the theory of Second Best). In some mainly developing countries, they are also still an important source of tax revenues. Among the various protectionist measures available concerning trade in goods are tariffs (non-discriminatory or discriminatory), quantitative restrictions (quotas), voluntary export restraints, export taxes, discriminatory tax policies, and subsidies, including tax incentives. Some of these (and other measures) may have similar or equivalent economic effects, particularly concerning their deadweight efficiency losses, while others can have very different effects. There may also be inherent similarities or differences concerning their transparency, predictability, susceptibility to rent-seeking, ease of administration, etc.

The rest of this section provides an analysis of these non-tariff measures in comparison with a tariff, irrespective of whether government intervention to restrain trade makes economic sense or not. It also highlights some well-known instances of economic equivalence as regards different measures. At the same time, it identifies protectionist tax policy measures that do the least damage. After all, damage limitation is often a major challenge for tax, if not other, policymakers. In doing so, it is shown that, by and large, WTO rules do encourage “efficient protection,” particularly as far as goods markets are concerned (Sykes, 2001). A comparison of tax measures suggests that non-discriminatory tariffs and domestic subsidies, including those in the form of tax relief, tend to involve relatively “efficient protection” and that these measures are less constrained by WTO rules. More damaging forms of protection are, to a large degree, discouraged, if not prohibited.

This material was prepared at the request of the IMF; Mr. Daly is a member of a panel of fiscal experts advising the IMF’s Fiscal Affairs Department. The analysis and policy considerations expressed in this publication are those of a member of the author and do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

Related News

Oil prices and the global economy: It’s complicated

Oil prices have been persistently low for well over a year and a half now, but as the April 2016 World Economic Outlook will document, the widely anticipated “shot in the arm” for the global economy has yet to materialize. We argue that, paradoxically, global benefits from low prices will likely appear only after prices have recovered somewhat, and advanced economies have made more progress surmounting the current low interest rate environment.

Since June 2014 oil prices have dropped about 65 percent in U.S. dollar terms (about $70) as growth has progressively slowed across a broad range of countries. Even taking into account the 20 percent dollar appreciation during this period (in nominal effective terms), the decline in oil prices in local currency has been on average over $60. This outcome has puzzled many observers including us at the Fund, who had believed that oil-price declines would be a net plus for the world economy, obviously hurting exporters but delivering more-than-offsetting gains to importers. The key assumption behind that belief is a specific difference in saving behavior between oil importers and oil exporters: consumers in oil importing regions such as Europe have a higher marginal propensity to consume out of income than those in exporters such as Saudi Arabia.

World equity markets have clearly not subscribed to this theory. Over the past six months or more, equity markets have tended to fall when oil prices fall – not what we would expect if lower oil prices help the world economy on balance. Indeed, since August 2015 the simple correlation between equity and oil prices has not only been positive (Chart 1), it has doubled in comparison to an earlier period starting in August 2014 (though not to an unprecedented level).

Past episodes of sharp changes in oil prices have tended to have visible countercyclical effects – for example, slower world growth after big increases. Is this time different? Several factors affect the relation between oil prices and growth, but we will argue that a big difference from previous episodes is that many advanced economies have nominal interest rates at or near zero.

Supply versus demand

One obvious problem in predicting the effects of oil-price movements is that a fall in the world price can result either from an increase in global supply or a decrease in global demand. But in the latter case, we would expect to see exactly the same pattern as in recent quarters – falling prices accompanied by slowing global growth, with lower oil prices cushioning, but likely not reversing, the growth slowdown.

Slowing demand is no doubt part of the story, but the evidence suggests that increased supply is at least as important. More generally, oil supply has been strong owing to record high output from members of the Organization of the Petroleum Exporting Countries (OPEC) including, now, exports from Iran, as well as from some non-OPEC countries. In addition, the U.S. supply of shale oil initially proved surprisingly resilient in the face of lower prices. Chart 2 shows how OPEC output has recently continued to grow as prices have fallen, unlike in some previous cycles.

Moreover, even in the United States, a net oil importer where demand has been fairly strong, cheap oil seems not to have given a substantial fillip to growth. Econometric and other studies suggest that only part of the recent decline in oil is due to slowing demand – somewhere between a half and a third – with the balance accounted for by increasing supply.

So there remains a puzzle: where in the world can the positive effects of lower oil prices be seen?

To address this question, the forthcoming April 2016 World Economic Outlook compares 2015 domestic demand growth in oil importers and oil exporters to what we expected in April 2015 – after the first substantial decline in oil prices. The lion’s share of the downward revision for global demand comes from oil exporters – despite their relatively small share of global GDP (about 12 percent). But domestic demand in oil importers was also no better than we had forecast, despite a fall in oil prices that was bigger than anticipated.

Understanding why the naked eye cannot detect positive spending effects requires a closer look at the composition of demand in oil exporters and importers.

Domestic demand in oil exporters

In 2015, domestic demand in oil exporters was indeed much weaker than we had forecast a year before. This negative surprise reflected both weaker consumption and especially weaker investment. Rich oil exporters can draw on their reserves or sovereign wealth funds, and most of them have, but they have also been cutting government spending sharply. Poorer countries, of course, have much lower borrowing capacity, and risk crises if foreign debt levels get too high. Most have sharply lower current account surpluses or higher deficits, and their sovereign spreads have risen. In these countries domestic spending can fall sharply, in a nonlinear fashion – sometimes through the impact of large exchange rate depreciations that make imported goods more expensive. Public investment has fallen especially fast – most capital goods are imported, and when fiscal adjustment is needed, capital spending is typically the first item to be cut. And of course, factors unrelated to oil prices have also being weighing on economic activity in a number of oil exporters – ranging from domestic strife in Iraq, Libya, and Yemen to sanctions in Russia.

Of course, low oil prices make exploration and extraction activities less profitable in the private sector, leading to lower capital expenditures there as well. According to Rystad Energy, the fall in global capital expenditure in the oil and gas sector amounted to about $215 billion between 2014 and 2015 – about 1.2 percent of global fixed capital formation (or just below 0.3 percent of global GDP). Even some oil importers have been hit hard, notably the United States, which accounts for a significant part of the global drop in energy-related investment.

Domestic demand in oil importers

Advanced oil importing economies have indeed seen some positive effects on consumption – for instance, in the euro area – but the impact has been somewhat less than anticipated. And investment growth has fallen short of expectations – also reflecting the unexpectedly large decline in U.S. energy-related investment mentioned above. The situation for oil importers in the emerging and developing world is varied. These countries typically have more limited pass-through from international to domestic fuel prices compared with advanced economies; some have reduced fuel subsidies. True, governments’ improved fiscal positions should eventually result in lower taxes or increased public spending, but the process could take time and is subject to various frictions and leakages. Overall, domestic demand growth for these oil importers was broadly in line with expectations – despite difficult macroeconomic conditions in a few countries that are exporters of other commodities.

Surprising macroeconomics at the zero interest-rate bound

There is another factor potentially impeding a pickup of demand in oil importers.

Compared with previous price cycles, falling oil prices this time coincide with a period of slow economic growth – so slow that the major central banks have little or no capacity to lower their monetary policy interest rates further to support growth and combat deflationary pressures.

Why does this matter? In the 1970s and 1980s, a large economics literature, summarized by Michael Bruno and Jeffrey Sachs more than three decades ago, showed how oil-supply-driven price increases lead to stagflation – a combination of higher inflation and slower growth. Stagflation is a direct result of higher costs for producers who use energy, costs that lead them to reduce output, shed labor, and raise prices to cover higher costs.

Even though oil is a less important production input than it was three decades ago, that reasoning should work in reverse when oil prices fall, leading to lower production costs, more hiring, and reduced inflation. But this channel causes a problem when central banks cannot lower interest rates. Because the policy interest rate cannot fall further, the decline in inflation (actual and expected) owing to lower production costs raises the real rate of interest, compressing demand and very possibly stifling any increase in output and employment. Indeed, those aggregates may both actually fall. Something like this may be going on at the present time in some economies. Chart 3 is suggestive of a depressing effect of low expected oil prices on expected inflation: it shows the strong recent direct relationship between U.S. oil futures prices and a market-based measure of long-term inflation expectations.

Being near the zero bound also can imply a “perverse” response to higher oil prices. When central banks are battling deflation pressures, they are unlikely to raise policy interest rates aggressively to counter an uptick in inflation. As a result, oil price increases, symmetrically, can be expansionary by lowering the real interest rate.

Of course, it would be wrong to conclude that central banks can enhance the benefits of current low oil prices by raising their policy interest rates. On the contrary, all else equal, that action would harm growth by raising real interest rates. Our claim is simply that when an oil importer’s macroeconomic conditions warrant a very low central bank interest rate, a fall in oil prices could move the real interest rate in a way that runs counter to the positive income effect.

The way forward

Persistently low oil prices complicate the conduct of monetary policy, risking further inroads by unanchored inflation expectations. What is more, the current episode of historically low oil prices could ignite a variety of dislocations including corporate and sovereign defaults, dislocations that can feed back into already jittery financial markets. The possibility of such negative feedback loops makes demand support by the global community – along with a range of country-specific structural and financial-sector reforms – all the more urgent.

Related News

Crude pipeline confusion strains Kenya-Tanzania ties

A rift between Kenya and Tanzania could widen following Uganda’s indecisive position on the $4 billion crude oil pipeline.

A week before the meeting between Uganda’s President Yoweri Museveni and President Uhuru Kenyatta, energy officials from Uganda held parallel meetings on the matter with Tanzanians and Kenyans.

Kenya and Uganda officials held a week-long meeting at Laico Regency, Nairobi, under the Northern Corridor Integration Projects while Tanzanian energy officials met with their Ugandan counterparts in Kampala.

The two parallel meetings were held before the presidential meeting to ascertain the level of preparedness by either Tanzania or Kenya on the crude oil pipeline.

Kenyan and Ugandan officials led by President Museveni and Kenyatta then met at Kenya’s State House Monday last week to finalise the talks.

Frances’ Total, UK’s Tullow Oil and China’s CNOOC were part of the meeting, sending strong signals for the Hoima-Lokichar-Lamu route.

“President Uhuru Kenyatta today held fruitful discussions with Uganda’s President Yoweri Museveni on the regional East Africa crude oil pipeline,” said a statement signed by Energy minister Charles Keter and his Uganda’s counterpart Irene Muloni.

Tanzania’s President John Pombe Magufuli, however, was not pleased with the proceedings of the Kenya-Uganda meeting. He demonstrated his frustration last week Wednesday by holding diplomatic passports of Kenyan energy officials, denying them entry into the Port of Tanga.

The team was on a tour to the Tanga Port acting on the presidential order to have all three ports – Tanga, Mombasa and Lamu – compared technically to inform in the final decision making.

Mr Keter and Petroleum PS Andrew Kamau, his Energy counterpart, Mr Joseph Njoroge and The Lamu Port Southern Sudan-Ethiopia Transport (Lapsset) corridor CEO Sylvester Kasuku are the Kenyan crew denied entry into Tanga.

Passport

“We had earlier made officials communications to Tanzanian foreign affairs of our visit and were granted access,” said an official privy to the ordeal.

“Things changed when we were received at the airport by government officials. Passports were submitted for clearance and took too long to come back. President Magufuli had given orders not to allow us in though our Ugandan counterparts went through.”

“We are basically captives here. They have refused to give us back our passports for about one hour. They have also refused us entry into the Port of Tanga,” PS Kamau had earlier told the Smart Company in a telephone interview.

Tanzania Petroleum Development Corporation (TPDC) Executive Director James Mataragio, also recently announced that France had set aside $4 billion to begin construction of the Tanga pipeline by August and have it completed in two years.

“It is anticipated that over 200,000 tonnes of bare pipes, materials and equipment such as pipe insulation, pump, bulk heating and trace heating stations will be imported through Tanga port,” Mr Mataragio is quoted by Tanzania’s publication The Citizen.

Talks on the pipeline taking the Kenyan route are back on track and could be sealed soon, causing a blow to Tanzania.

Kenya together with Uganda is currently on a quest to settle on the least cost option for a regional integrated pipeline. Next week, the two countries will travel through Lamu to compare the infrastructure, terrain and elevations on the route with the Eldoret-Mombasa route and the Uganda-Tanga route. Tanzania officials have been invited for the tour.

Museveni and Kenyatta will thereafter in early April meet at the Northern Corridor Integration Projects Summit in Kampala with the view of settling on the prolonged $4billion crude oil pipeline route.

Ongoing discussions could thwart a deal mooted in October to have the crude oil pipeline constructed through Tanga. Uganda is bound to Tanzania by a MoU initiating a study on the Tanga route.

Further, this could worsen the shaky relationship between Tanzania and Kenya both in terms of trade and project relations. Tanzania-Kenya trade has not been at its peak with the former being accused of putting non-trade barriers on Kenyans including delay of work permits.

Data by the Kenya National Bureau of Statistics (KNBS) in February states that Tanzania cut its imports from Kenya last year by Sh8 billion to Sh25.3 billion, signaling the worsening relationship between the two countries.

Uganda on the other hand is the largest buyer of Kenyan goods with imports standing at Sh60 billion by February. While Tanzania has not embraced the integration spirit in infrastructure projects along the Northern Corridor (where crude oil pipeline is a major project) Uganda is part of the bloc which consists of five members.

Related News

New trade deals challenge Africa to step on to the global stage

Without growing its economy, Africa risks being left behind, unable to create the jobs it needs to reduce poverty

Africa needs to grow its economy in order to reduce poverty and create jobs for the millions who will be entering the workforce. In the development community, this statement has become almost trite.

But is it the whole truth? After decades of underperformance, Africa had economic growth rates of 5.8% from 2004 to 2014, democracy is now the norm rather than the exception, and corruption is being tackled as the rule-of-law has been strengthened in several countries.

By 2030 sub-Saharan Africa could be adding more working-age people to the global labour force than the rest of the world combined. If jobs can be created, then this demographic transition alone could raise GDP per capita by a further 50% by 2050.

Still, many challenges threaten to reverse this progress. Responding to them will require Africa to diversify its economy and better integrate into the global economy. And this will mean bringing Africa into the new systems of international trade that are being negotiated.

Over the last 18 months many of the key drivers of Africa’s growth have changed. Commodity prices have collapsed, contracting government budgets and export income. China – Africa’s largest trading partner – is slowing, perhaps by a lot. And the easy monetary policy in the US, which drove cheap capital into investments in Africa, is at an end. As a result, GDP in Africa in 2015 slowed to around 4.5% – not bad considering the anaemic growth in most of the world, but significantly lower than Africa needs.

To reduce poverty further and create jobs, Africa will need to become more globally engaged.

As has been seen with the remarkable growth in Asia over the last 30 years, trade openness supports export-orientated manufacturing sectors, which absorb large numbers of low-skilled labourers. There are also opportunities for Africa to expand agriculture exports, a sector responsible for 65% (pdf) of jobs in sub-Saharan Africa, half of which are held by women.

Yet international trade is an area where Africa underperforms.

For instance, in 2014 the share of global exports from sub-Saharan Africa was less than 2%. And this poor performance was despite African business having preferential market access into the United States and the European Union.

Sub-Saharan Africa is also poorly integrated into global supply chains where businesses can contribute inputs into the creation of final products. More than half of world trade is now in intermediate goods. And plugging into these global networks avoids having to develop entire industries from scratch.

But there are also new rules.

While Africa needs to become part of the global economy, the rules of engagement are changing in ways that could further marginalise Africa. This is primarily the result of a US-led push to develop new high-standard trade and investment agreements – the most significant of these being the Trans-Pacific Partnership agreement concluded last October. In addition, the US and the EU are negotiating a bilateral trade deal and there are other large trade negotiations centred in Asia.

No country in Africa is a part of these new trade agreements; yet they will significantly affect Africa’s ability to participate in the global economy. As tariffs come down, the value to African businesses of tariff-free access to the US market will be reduced. These agreements also include new rules on labour and environment standards that African businesses are likely to find difficult to meet, further affecting participation in global supply chains.

At the same time, no progress is being achieved on completing the global trade negotiations at the World Trade Organisation. This means that there is currently no large global trade negotiation where Africa’s views are being considered.

The risk is that Africa will find it increasingly difficult to compete globally, confining the continent to a shrinking share of international trade and diminishing its attractiveness as a destination for investment, undermining growth, and job prospects.

These challenges underscore the need for leaders, businesses, and civil society in Africa, and globally, to ensure that Africa is not left behind. Progress here could be the difference between a prosperous Africa and a slowly declining, less stable continent, with global repercussions.

Joshua P Meltzer is a senior fellow in global economy and development at the Brookings Institution

Related News

21st Meeting of the COMESA Committee of Governors of Central Banks: Challenges of dollarization in COMESA

The 21st Meeting of the COMESA Committee of Governors of Central Banks was held from 18-19 November 2015 in Lusaka, Zambia. Governors reviewed the activities that were undertaken by COMESA Monetary Institute (CMI) and the COMESA Clearing House for enhancing monetary cooperation in the region and endorsed a 2016 Work Plan for the two COMESA institutions.

The Secretary General of COMESA, in his statement, emphasized that monetary cooperation programmes at the regional level are building blocks for achievement of continental integration. He, therefore, proposed to make monetary cooperation as a Tripartite (COMESA, EAC and SADC) agenda for speeding up continental integration which is currently being pursued by the Association of African Central Banks (AACB). This he said will avoid duplication of efforts due to overlapping membership. He also emphasized the importance of the region’s involvement in supranational and global value chains as well as international production aimed at high value products that can access global markets.

He pointed out that industrialization can diversify the region’s dependence on commodity trade and emphasized the importance of collective thoughts to come up with a good industrialization policy for the region. He underscored the importance of prudent fiscal policies and financial intermediation for making the region a zone of macroeconomic stability and enhancing integration. He stated that the speedy implementation of the Regional Payment and Settlement System (REPSS) will significantly contribute to the expansion of intra-COMESA trade. He, therefore, urged all member Central Banks to expeditiously use REPSS for payment for their intra-COMESA transactions.

Report of the 13th Meeting of the Monetary and Exchange Rates Policies Sub-Committee

The Effects of Fiscal Policy on the Conduct and Transmission Mechanism of Monetary Policy

Governors were informed that research papers were prepared by experts from Central Banks of Burundi, Egypt, Kenya, Malawi, Mauritius, Rwanda, Swaziland, Sudan, Uganda, Zambia and Zimbabwe. The papers focused on the following:

-

Key features of the operational framework for fiscal and monetary policy and interaction between fiscal and monetary policies;

-

Theoretical and empirical literature on the different channels through which fiscal policy can affect monetary policy;

-

Trends in fiscal performance including trends on dependence on foreign borrowing and grants;

-

Review of existing legal and institutional development which are necessary in order to avoid fiscal dominance and to ensure effective coordination of monetary and fiscal policies;

-

Challenges facing the existing fiscal policy regime;

-

Empirical analysis of the channels in which fiscal policy affects monetary policy; and

-

Recommendations.

Governors noted the following salient features of the research papers:

Key features of Fiscal and Monetary Policies in COMESA member countries in recent years

Governors were informed that the following are key features of fiscal policy in selected countries:

-

Many countries introduced Public Finance Management System (PFM). PFMs require that the budget is comprehensive by including all financial operations of the Government. Thus both the current and capital budget should be included under one budget and aid and debt, as well as other off-budget items (including contingent) must be captured in the budget. Such a comprehensive sweep of the budget would facilitate coordinating fiscal policies within a macroeconomic policy framework and enable assessment of the sustainability of fiscal policies over the short and medium term. Having a robust PFM by member countries is one of the requirements of the COMESA Multilateral Fiscal Surveillance Framework.

-

Many Member countries are making significant progress in preparing their budgetary policies within a comprehensive medium term financial management framework, comprising a set of four separate frameworks: A Medium Term Fiscal Framework (MTFF), a Medium Term Budget Framework (MTBF) and Medium Term Expenditure Framework (MTEF). The COMESA Multilateral Fiscal Surveillance Framework is based on the availability of all the four components of the Medium Term Financial Management Framework. However, their development in member countries is constrained due to insufficient availability of data, and capacity for data analysis which could only be built from the medium to long run.

-

The institutions and laws governing fiscal policy are enshrined in legislation and often derived from constitution.

-

All countries have legal systems that define functions and responsibilities of the Ministry of Finance in the country’s debt management process. This also specifies the limit of indebtedness and guarantees that the country can undertake. This strengthens fiscal discipline in the country and ensures that the country remain on a prudent fiscal path.

-

Many member countries undertook the following tax reforms:

-

Significant attempt has been made by most member countries to reduce reliance on the taxation of international trade and to shift the tax system toward domestic transactions and sources of income.

-

VAT was introduced in almost all member countries. Tax reforms have also been instrumental in shifting excises from a specific to an advalorem valuation basis.

-

Almost all countries have simplified and improved the equity and efficiency of their personal income taxes by scaling down the highest marginal rates, reducing the number of rates, and reducing exemptions and deductions.

-

Tax administration in almost all countries has improved through better training and salaries and conditions of service for revenue collection personnel. Special emphasis was placed on providing adequate trained manpower and other infrastructural facilities to enable the attainment of revenue potential.

-

-

Some countries use countercyclical interventions when the economy is below or above potential growth path. Countercyclical expenditures involves increasing public spending when the economy is growing below its long run potential, and decreasing it when output rises close to potential and is threatening to cause resource scarcities that provoke inflationary pressures.

Governors observed that the following are key features of monetary policy in selected member countries:

-

The overriding objective of monetary policy for most central banks is price stability. Other objectives pursued by many central banks in the region in recent years include financial stability and economic growth.

-

Most COMESA member countries removed exchange controls and adopted a more flexible exchange regime.

-

Most countries moved from direct to indirect monetary management. This includes establishment of open market operations for monetary policy purposes and to improve liquidity management. Some countries introduced framework for repurchase and reverse repurchase transactions. In some countries for example Mauritius, Key Repo Rate (KPR) acts as a policy rate to signal its monetary policy stance.

-

Many countries still use base money or reserve money as operational target in the conduct of monetary policy while broad money has been used as the intermediate target with inflation being the ultimate target.

-

Many countries are embarking on modernizing their monetary policy framework with the ultimate objective of adopting an inflation targeting monetary policy framework. Some countries have introduced policy rates. The motivations for modernizing the monetary policy regime are to enhance market participants understanding of the monetary policy stance and to strengthen the monetary policy transmission channel, particularly the interest rate channel.

-

Some countries like Mauritius, Kenya and Swaziland are making remarkable attempts on inflation targeting approach in the conduct of monetary policy.

-

Most central banks have Monetary Policy Committees with diverse membership.

Governors also noted that the following are direct and indirect channels through which fiscal policy affects monetary policy in selected countries:

-

Fiscal policy influences demand pressures and thus impacts inflation, via both direct spending by government and changes to private disposable income (through taxation and the benefit system). In particular, through the monetization of the fiscal deficits, fiscal policy undermines monetary policy as it fuels inflationary pressures. Even in the absence of monetization by the central bank, higher deficits may cause inflation, as the government’s borrowing requirements will increase the net credit demands, drive up interest rates and crowds out private investment. The resulting reduction in economic growth would lead to a decrease in the amount of goods available for a given level of cash balances, causing higher price levels;

-

Fiscal policy affects monetary policy directly through indirect taxes. If governments resort to substantial increases in indirect taxes-sales taxes, value added tax – this would have a direct impact on prices through the wage-price spiral;

-

Perceptions and expectations of huge budget deficits, and resulting large borrowing requirements are likely to trigger a lack of confidence in the economic prospects, posing risks to financial system stability;

-

On the external side, there are risks of too much dependence on foreign funding of domestic debt, arising from unsustainable fiscal deficit. This may result in exchange rate and/or balance of payment crisis which are worrisome to central banks;

-

Fiscal policy affects monetary policy through both domestic and public debt depending on its sustainability. If market participants perceive the growth in domestic/public debt as unsustainable, the credibility of the overall policy mix is reduced and interest rates will rise. Also, adverse shocks to external indebtedness tend to shift the long run interest rate spreads. Wider interest rates spreads lead to higher yields on government bonds and to higher commercial interest rates.

Challenges for Implementation of Fiscal and Monetary Policies

Governors observed that the following are some of the challenges for fiscal policy implementation in selected COMESA member countries:

-

Low level of private savings partly because of low income levels due to high levels of poverty.

-

A sizeable portion of most developing economies is non-monetized, rendering fiscal measures of the government ineffective and self-defeating.

-

External shocks on commodity prices such as oil, copper price shocks and external debt in most member countries affect the stance of fiscal policy.

-

In a number of countries, fiscal policy effectiveness is hindered by the difficulty to generate direct tax revenues; the inefficient collecting schemes of taxes; low rates of taxes on property; and a decline in taxes on international trade due to tariff reductions, trade agreements, and discretionary exemptions.

-