Search News Results

Trade, finance and development: Overview of challenges and opportunities

Sustainable development is the Holy Grail of the international community, and the potential roles played by trade and finance lie at the heart of the search effort. The extremely robust positive correlation between various measures of trade and financial development on the one hand, and economic growth, on the other, is the bread and butter of thriving sub-disciplines within economics (international trade and the finance and growth literature, respectively). Evidence concerning the direction of the causal relationships is, however, less than compelling.

For example, there is increasing evidence (and the 2008 crisis may be a manifestation of this) that countries can have financial sectors that are “too large.” As such, one needs to be extremely cautious in formulating policy recommendations that rest on putative causal relationships that have not been rigorously established. Moreover, the link between trade and finance on the one hand, and various measures of development (as opposed to a narrow focus on economic growth), on the other, has attracted much less attention.

To some extent, this is because of the proliferation of measures of development: it suffices to think of the vast array of Millennium Development Goals (MDGs) or Sustainable Development Goals (SDGs). An implicit assumption is that economic growth will necessarily translate into improvements in these indicators: this is not, of course, the case. In addition, it is already difficult to establish the causal determinants of economic growth: doing so for a plethora of other development indicators increases the challenge by several orders of magnitude.

Geography and institutions

During the past twenty years, our understanding of the determinants of economic growth has been profoundly shaped by a vast corpus of cross-country empirical literature. This work was initially driven by the construction of internationally comparable measures both of economic growth and development (such as the Penn World Tables or the World Bank’s Word Development Indicators) and of country characteristics. Though it is something of an oversimplification, this literature has given rise to two broadly defined schools of thought concerning the key fetters to economic development and growth.

On the one hand, the “geography” school, often associated with Jeffrey Sachs, holds that a country’s development performance is to a large extent determined by its geographical location. For example, it is argued that a country’s level of gross domestic product (GDP) per capita is, ceteris paribus, an increasing function of its distance to the equator; similarly, landlocked countries are believed to have both a lower level and a lower rate of growth GDP per capita. There are many causal pathways that can explain geographically driven income and growth effects, including the higher burden of disease under subtropical climates or the infrastructure needed to overcome geographic isolation from world markets for landlocked countries. In a traditional growth accounting framework, both of these examples underscore the fact that geographical fetters to development affect total factor productivity (TFP), the overall efficiency with which factors of production, such as labour and capital (both human and physical), are transformed into output; the productivity of single factors of production (such as labour); and the amounts of the factors themselves that are used.

On the other hand, the “institutional” school of thought, often associated with the work of Daron Acemoglu and his collaborators, has emphasised the importance of a country’s institutional environment, where institutions are understood in their economic (and not political) sense in terms of social structures, such as the rule of law or the protection of property rights that allow economic activity to develop. As with geography, institutional factors can affect the productivity of single factors, TFP, and factor use.

One of the most important empirical regularities established by the institutional school is that there is a causal relationship linking national economic institutions (as usually measured by protection against expropriation risk) to income per capita. Moreover, a second important empirical regularity is that geography affects per capita income through its impact on institutions: once economic institutions are appropriately taken into account, geography arguably no longer has an independent impact on income levels.

A simple diagram, based on empirical results similar to those of one of the most influential recent papers in economics (Acemoglu, Johnson, and Robinson, 2001) will render this mechanism more explicit: geography affects economic institutions, but has no direct effect on growth; economic institutions, in turn, determine economic growth. The effect of geography on economic growth is therefore mediated through national economic institutions. There is a final arrow linking economic growth to development in a broader sense.

Where do trade and finance fit into this picture? In order to organize our thoughts, let us divide the impact of trade and finance on economic growth (leaving development per se out of the picture for the time being) into two components.

Where do trade and finance fit into this picture? In order to organize our thoughts, let us divide the impact of trade and finance on economic growth (leaving development per se out of the picture for the time being) into two components.

First, there are direct effects: trade and finance, through well-established mechanisms, may enhance growth performance. Though the causal evidence at the macro level is often weak (the finance and growth or aid effectiveness literatures are cases in point), there is a corpus of microeconomic evidence that points to productivity enhancing causal effects of trade and finance. These effects are added in the following picture.

Second, there are indirect effects, which operate through either geography or economic institutions. “Geographic” effects of trade and finance include trading arrangements (such as preferences), which effectively compensate for geographical disadvantages, or financing options – such as official development assistance (ODA) or public-private partnerships (PPPs) devoted to infrastructure projects – which overturn geographic fetters, such as being landlocked. “Institutional” effects of trade and finance have been explored less. While, to take but two examples, the corruption-enhancing effects of ODA have been well documented, as has the positive impact of openness on many national bureaucracies, there are undoubtedly many other mechanisms that could, and should, be explored.

Growth versus development

Finally, there remains the vexing question of the link of all of this (as noted at the outset) with broader measures of sustainable development. Here (and I am willing to be corrected on this), the existing literature is not of much help. In an effort to wrestle a broader development indicator into the above conceptual straightjacket, I appended, as a very rough thought exercise, a third equation to the Acemoglu, Johnson, and Robinson (2001) empirical framework. The scalar measure of development that I added was the classic child anthropometrics indicator of stunting (the proportion of children in a country whose height is one standard deviation below where it should be if they were in good health).

I chose this synthetic indicator for two reasons. First, because half a century of empirical evidence has taught us that it is determined by four factors: income (and therefore economic growth); access to clean water and basic healthcare; maternal education and female empowerment. Second, this indicator is culturally neutral: in different societies, economic and social success may be measured by a bewildering number of indicators, ranging from income, to land ownership, to livestock; but the bottom line is that all inhabitants of this planet care about the welfare of their children, which also adds an intertemporal perspective to things. A remarkable empirical regularity emerges: while income per capita is (unsurprisingly) a statistically significant determinant of stunting (more precisely, a 1 percent increase in per capita GDP is associated with a 5 percent fall in the prevalence of stunting), neither geography nor institutions appear to play a role. While this regularity is merely suggestive, it does offer the hope that the above conceptual framework may be of some use in pinpointing the roles that can be played by trade and finance in enhancing development in general, and not merely economic growth.

Jean-Louis Arcand is Professor and Director of the Centre for Finance and Development at the Graduate Institute Geneva.

Implemented jointly by ICTSD and the World Economic Forum, the E15Initiative convenes world-class experts and institutions to generate strategic analysis and recommendations for government, business, and civil society geared towards strengthening the global trade and investment system for sustainable development.

Related News

To de-link or not to de-link? A contribution to the current debate in Namibia

There have been calls recently from some commentators to re-consider the one-to-one peg of the Namibia dollar to the South African rand, because of the rand’s strong depreciation over the past year. It is interesting to note that these calls are usually made, when the rand is under pressure, not when it is appreciating against major currencies.

Before evaluating the merits of such calls a brief review of the rand’s performance vis-à-vis major currencies such as the US dollar (USD) and some emerging market currencies such as the currencies of the BRIC countries (Brazil, Russia, India, China) is necessary.

The South African rand (ZAR) showed periods of appreciation and depreciation against the USD, the British pound (GBP) and the Euro (EUR) over the past 10 years. In addition, the performance against these three currencies has not always been alike. During 2005 the ZAR appreciated by between 1.3 per cent and 2 per cent against these currencies, but lost value in the following three years in particular against the Euro.

Compared to 2005 the ZAR depreciated by the end of 2008 against the Euro by more than 50 per cent, but only by some 30 per cent against the USD and GBP. Some of the losses were reversed in the following two years, when the ZAR appreciated by between 11 per cent (USD) and 25 per cent (GBP) as at the end of 2010 compared to 2008.

In 2011, the South African currency moved sideways, appreciated slightly again vis-à-vis the USD, but lost slightly against the two European currencies. Since 2012 the ZAR started losing ground, but still appreciated slightly against the EUR in 2015 when comparing the average value of the currency in 2015 to 2014.

The fact that the performance of the ZAR against these three currencies differed in magnitude and sometimes even in direction suggests that the performance has not only been influenced by internal, domestic factors, but by external factors as well. This is further corroborated when comparing the value of the ZAR against the Japanese yen.

The direction and degree of change often differed substantially compared to the rand’s performance against the other three currencies.

Furthermore, the rand showed a mixed performance vis-à-vis the BRIC currencies. Since the Chinese yuan’s value was guided by the USD, the ZAR depreciated over the past two years, but slightly less compared to the USD.

It also lost value (8 and 12 per cent) against the Indian rupee in 2014 and 2015 respectively. On the other hand, the rand appreciated strongly against the Russian rouble by 6 per cent and 27 per cent over the same period and gained last year against the Brazilian real 16 per cent.

Although the weaknesses of the latter two currencies can to a large extent be attributed to domestic factors (drop in energy prices and economic sanctions in the case of Russia; economic challenges and political uncertainty in the case of Brazil), global factors play a crucial role in the performance of in particular emerging markets currencies.

There was the time of the USD80 billion per month bond-buying programme of the US Federal Reserve Bank that flushed the markets with liquidity and resulted in the depreciation of the USD and the appreciation of among others emerging market currencies such as the ZAR.

The expectation that the Federal Reserve Bank will increase the policy interest rates in the US changed financial investors’ sentiments and coupled with uncertainties about the direction of the Chinese economy and globally weak commodity prices resulted in increased risk aversion and the search for safe havens. Contrary to trends in the past, it was no longer gold that played the role of a safe haven, but currencies such as the USD, which resulted in the depreciation of emerging market currencies in general and not only the ZAR.

On the other hand, not only emerging markets but also countries such as Denmark used monetary policy to gain competitive advantages. Talk of a currency war made the rounds. China devalued the Chinese yuan in the second half of 2015, which triggered currency adjustments in other countries such as Kazakhstan, Turkey and Vietnam.

Countries devalued their currencies in order for their goods and services to become more competitive on the world market. Kazakhstan for instance de-linked the Kazakh tenge from the USD in August 2015 and the currency’s value dropped by more than 20 per cent. Currently, Saudi Arabia and Hong Kong consider de-linking their currencies from the USD for the same competitiveness reasons. While quite a number of countries took or are taking steps to devalue their currencies other countries have faced economic challenges owed to the appreciation of their currencies, notably Switzerland and the USA.

Switzerland terminated the cap of the value of the Swiss franc against the Euro in January 2015, which resulted in a steep appreciation of the Swiss franc and a loss of competitiveness of Swiss exporters and subsequently a lower economic growth rate. The strength of the US dollar is one of the reasons for a downward revision of economic growth expectations for 2016 from 2.8 per cent to 2.6 per cent by the International Monetary Fund (IMF) in January 2016.

These monetary policy responses indicate that the appreciation or depreciation of a currency is not ‘good’ or ‘bad’ per se. The depreciation of a currency is a monetary tool to among others gain competitive advantages since domestic goods and services become less expensive not only on the international market but also on the domestic market compared to goods and services from countries which currency appreciated. The depreciation of a currency is therefore been used as an industrial policy instrument.

The flip side of the coin is however, that imports become more expensive, including imports that are used in the production of exportable goods. In countries with a narrow industrial base, such as Namibia, that rely on the importation of most consumer goods and coupled with an arid climate depend on the importation of most of the foodstuff, increasing import prices can finally lower the population’s standard of living unless they are compensated for the rising costs of living by increasing salaries, wages and or social transfers.

South Africa’s currency was however hit harder recently than some other emerging markets’ currencies, because of a combination of the external factors mentioned above and domestic factors such as policy uncertainty, structural issues, widening budget and current account deficits, downgrading by sovereign rating agencies, and low growth prospects. For instance, the IMF changed its economic growth estimates for South Africa for 2016 drastically from 3.7 per cent in January 2015 to just 0.7 per cent in January 2016. There is also a risk that South Africa faces a further downgrading that markets might already factor in. These factors contributed to the strong depreciation of the ZAR in recent weeks and by implication of the Namibia dollar, the Lesotho loti and the Swazi lilangeni.

Even if Namibia does not face all the same domestic factors that contributed to the devaluation of the South African rand, the country will still be exposed to the external factors.

Given the narrow industrial and export base of Namibia, the economy and by implication the currency is more vulnerable to external shocks in one or more of the dominant sectors, such as diamond or uranium mining or the fishing sector, than a more diversified economy such as the South African. Angola (reliance on oil) and Zambia (copper) serve as examples.

It could therefore well be that a de-linked Namibia dollar would be weaker than the South African rand, which would result in a declining standard of living in Namibia since imported goods and services become more expensive.

In addition, since most of Namibia’s imports are sourced from or through South Africa, prices would be more volatile in Namibia because of additional exchange rate fluctuations. On the other hand, the South African market is important for some of Namibia’s industries, such as the beverage and meat industries.

If a de-linked Namibia dollar appreciates against the South African rand, Namibia’s exports to South Africa become less competitiveness and exporters risk losing market shares.

Last but not least, de-linking the Namibia dollar from the South African rand would imply that we abandon our regional integration ambitions of a monetary union that is still on the agenda even though no new time lines for achieving it have been agreed upon.

Addressing the domestic factors in earnest that contributed to the depreciation will support the recovery of the ZAR and hence the Namibia dollar as soon as investor sentiments change again and emerging markets are not viewed as risks but as opportunities.

Klaus Schade works as economic policy analyst and consultant in Namibia

Related News

tralac’s Daily News selection

The selection: Wednesday, 3 February 2016

Some conference dates to diarise:

2016 Mining Indaba (Cape Town, 7-11 February)

EAC’s Council of Ministers (Arusha, 22 February) and Heads of State summit (Arusha, 29 February)

Taking stock of IIA reform (Geneva, 16 March)

AfDB Annual Meetings (Lusaka, 23-27 May)

TICAD VI (Nairobi, 27-28 August)

Second Southern African Business Forum (August 2016)

China-Mauritius relations 'have gone beyond the scope of bilateral relations' (FMPRC)

Foreign Minister Wang Yi said China-Mauritius relations are of increasing strategic significance and have gone beyond the scope of bilateral relations. Looking into the future, China’s cooperation ideas are as followsThe unique geographic and regional advantages of Mauritius should be fully leveraged to gradually build the country into a gateway for China’s investment in Africa and a hub for China’s connectivity cooperation with Africa. Both sides could explore the feasibility of jointly establishing a financial service centre for cooperation with Africa and a training platform for Africa and the feasibility to promote Mauritius’s aviation connection with all other African countries. Second is to expand China-Mauritius cooperation eastward to the Indian Ocean with a focus on enhancing mutually beneficial cooperation in maritime economy. China views Mauritius as a natural extension along the Maritime Silk Road and will explore effective ways with Mauritius for jointly building the 21st Century Maritime Silk Road based on an open attitude and the principle of voluntariness.

China and Mozambique sign visa waiver agreement (Macauhub)

Navigating the new normal: China and global resource governance (Chatham House)

The report considers the costs and benefits of a more active role for China in global resources governance. It recognizes that different commodities face different challenges and require different governance frameworks, and that different regions require context-specific responses. The report also considers the risks of more limited engagement of China and other new actors, which could mean declining relevance for existing processes and institutions that govern resource production, trade and consumption, and a diminished capacity to tackle longer-term challenges like climate change.

Carlos Lopes: 'Conflict grows out of inequality and exclusion' (UNECA)

Results show that the economic performance of conflict areas is on average 10% below that of conflict-free areas in most GDP performance categories. A study estimated a loss of 284 billion USD (in constant 2000 rates) for 23 African countries, from 1990 to 2005. This figure represented then an average annual loss of 15% of their GDP. Regression analysis indicates a loss of about 2.2% GDP growth due to conflict. The interrelated nature of African economies also means that the costs of war within a sub-region generally result in economic costs for neighbouring countries. These include production losses through loss of opportunities deriving from migration, trade losses, increased costs of security and policing and the costs of supporting refugees.

Sandra Uwera: 'Intra-regional trade key to Africa's industrial growth, competitiveness' (New Times)

So the Kigali meeting was crucial as we wanted to collect views of the private sector in the COMESA trade bloc on the rules of origin regime to ensure a balanced framework. We have so far made head way on a number of issues, including agreeing to put in place simple and predictable rules that will facilitate intra-regional trade. We have agreed that rules of origin should be administered in a consistent, uniform, impartial, transparent and reasonable manner to promote industrialisation in the region. We are also aware of the fact that when rules of origin are not flexible, the cost of compliance exceeds benefits accruing from market access, a reason why some exporters do not comply with the rules. As a result, exporters will trade with companies in countries with favoured rules, this means low intra-regional trade, and slow pace of industrial growth in the region. Member states still don’t understand the benefits of creating a more harmonised regional market. We need to look at the bigger picture of creating more than $1 trillion in GDP simply because we decided to trade among ourselves. [The author is CEO, COMESA Business Council and SG of the Tripartite Private Sector platform]

Phyllis Wakiaga: 'Africa's future lies in free movement of goods, people' (Capital FM)

Over the last decade, Kenya exports average Sh2 billion while imports averages Sh313 million between 2004 and 2014 making Nigeria a significant trading partner for Kenya. The two countries have committed to double their trade and investment levels in five years. In 2014, Kenya’s share of world exports was 0.03%, 33.5% of these exports are from the manufacturing sector. On the other hand, the countries share of world imports is 0.10% pointing to the growing trade imbalance with surging imports. Africa share of global trade is 2% which is still low. There therefore an enormous potential to enhance Kenya’s with the rest of Africa particularly in growing the manufacturing sector with a view to enhance exports of value added products. [The author is the CEO, Kenya Association of Manufacturers]

New PS promises to address Kenya's trade balance (Daily Nation)

Newly appointed Permanent Secretary Chris Kiptoo says he will deliver a trade policy to address the imbalance in Kenya exports against imports. Mr Kiptoo said he will come up with a new set of rules on taxes, subsidies, import and exports in the next four months to boost Kenyan trade. The former TradeMark East Africa Kenya Country Director said he will also spearhead the development of an export strategy to boost Kenya’s capacity to produce for the global market.

Kenya: Govt told to involve MPs before signing trade pacts (Daily Nation)

In a report, the Kenya Human Rights Commission said Parliament was best suited to deliberate on such matters which could see Kenyan food industries edged out by multinationals whose contracted farmers enjoy huge subsidies in their respective countries. “The full implementation of Economic Partnership Agreements, may shift consumption away from local products, to EU goods. This may in turn lead to a decline in production and employment in large-scale industries,” it said. The report follows completion of a study entitled, ‘Impact of EU trade agreement EAC-EU EPA on Kenya’s Agriculture’, where KHRC called for establishment of a monitoring mechanism incase the agreement is ratified to track negative effects.

South Africa: AGOA compromises raise questions about goals (Business Day)

This is interesting because AGOA has evolved from what many regarded as an aid or economic access programme into an instrument for the creation of markets for US goods. This is not objectively bad from the perspective of the US. But it does raise important questions about long-term industrial trade and industrial policy as implemented today by the government. It has to be asked, in defending the benefits under AGOA, whether the government is making short-term choices rather than thinking long-term about developing domestic industry over time. [The author, Xhanti Payi, is head of research at Nascence Advisory and Research]

South Africa: Lucky Cement drops court challenge (IOL)

Pakistan cement producer Lucky Cement has decided against reviving its South African court challenge to the imposition by the International Trade Administration Commission of anti-dumping duties on Portland cement imports from Pakistan. The company said it had instead decided to put its faith in the Pakistan government’s approach to the World Trade Organisation (WTO) to challenge and revoke the anti-dumping duties.

Port of Maputo handles less cargo in 2015 (Macauhub)

The cargo handled at the port of Maputo in 2015 – 15.6 million tons – represented a contraction of 19.17% compared to 19.3 million tons processed in 2014, said Tuesday in Maputo the port’s management company. The Maputo Port Development Corporation explained the slump with the difficult conditions experienced in international markets, following a sharp decline in commodity prices compared to previous years. The largest declines in tonnage were seen in loading of coal and magnetite, as well as in the car terminal and sugar, the MPDC said in a statement.

Mozambique: Private credit bureau legislation (SPEED)

In 2016 the Bank of Mozambique presented regulations to the law for discussion. The report below analyses those regulations and provides recommendations.

The impact of foreign direct investment on productivity and growth in SADC (UCT)

This thesis focuses on the impact of foreign direct investment on productivity and growth in the Southern African Development Community (SADC), which is dealt with in three related studies. The first study undertakes an investigation of the existence and nature of technology and productivity spillovers from foreign direct investment to domestic firms in the region, while the second investigates the role of the spatial density of economic activities in speeding up the productivity externalities and impact of foreign direct investment in FDI host countries. In the last study, we investigate the role of intra-regional bilateral foreign direct investment between South Africa and countries in SADC in influencing growth and income convergence in the region. [The author: Nicholas Masiyandima]

Nairobi grabs top FDI destination slot, leaves behind Joburg (Daily Nation)

Nairobi edged out Johannesburg to become the top destination of foreign direct investment in Africa in 2015 reflecting improving investor confidence in Kenya. A report by an investment monitoring platform, FDI Markets also shows that FDI flows into Kenya rose 37% in 2015 compared to 2014 adding that Kenya also attracted 12.6% of FDI inflows into Africa, second only to South Africa’s 17.1%. "This is further compounded by Nairobi attracting the most FDI on the continent at city level in 2015, beating Johannesburg, which has held this accolade since 2010," notes the report.

6 initiatives tackling African electrification (Devex)

A host of alliances and initiatives have been set up to address the energy deficit challenge. They bring together a range of institutions from business, government and civil society under a common objective of reducing poverty and promoting inclusive growth by meeting basic energy needs. To give a sense of the scope of the challenge and the range of actors involved, Devex has pulled together a shortlist of projects and initiatives that are dedicated to addressing energy shortages in Africa.

Investment facilitation: an Action Menu (UNCTAD)

The Action Menu proposed here for discussion is based on UNCTAD’s Investment Policy Framework and rich experiences and practices of investment promotion and facilitation efforts worldwide over the past decades. The Action Menu proposes 10 action lines with a series of options for investment policymakers to adapt and adopt for national and international policy needs: the package includes actions that countries can choose to implement unilaterally, and options that can guide international collaboration or that can be incorporated in international investment agreements. The Action Menu should be read in the broader context of UNCTAD’s Investment Policy Framework for Sustainable Development.

Record number of Investor-State Arbitrations filed in 2015 (UNCTAD)

The Enhanced Data Dissemination Initiative 2: update after Ghana conference (IMF)

Botswana: Strategy for the development of statistics (AfDB)

India: Commerce minister holds consultation with Export Promotion Councils (Business Standard)

'Indian likely to become CFO of AIIB’ (The Hindu)

US Delegation to the African Union Summit: press briefing (State Department)

Closing 2016 Youth Forum, senior UN official says young people key to new sustainability agenda (UN)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

Zimbabwe Economic Update: Changing growth patterns, improving health outcomes

The World Bank presents the first edition of the Zimbabwe Economic Update (ZEU). The objective of the ZEU is, first, to provide a World Bank perspective on Zimbabwe’s recent economic developments, and second, to profile recent progress in a key sector or a key issue in detail. In this edition, we discuss the ongoing progress in improving health outcomes and review some of the policies and practices the sector has adopted in response to its challenges.

Over the last five years, Zimbabwe has made significant progress in stabilizing and revitalizing its economy. The economy grew at an average of six percent annually, while inflation has been kept low. A steady, albeit gradual, sequence of economic and institutional reforms is gaining momentum, and is reflected in the World Bank’s annual Country Policy and Institutional Assessment (CPIA). With strong Government commitment, steadfast household investments and substantial donor support, considerable progress has also been made towards regaining Zimbabwe’s past performance in social outcomes, particularly in health and education. The authorities are now implementing a number of reforms to strengthen the financial sector, in particular, and to improve the business environment, in general.

Yet significant challenges remain. The economic boom that followed the introduction of the multi-currency system in 2009 appears to have run its course and the economy is facing significant headwinds. The Country was adversely affected by a drought in 2015, and is starting to experience the effects of El Nino this year, in particular on agriculture, energy and water supply. Industry remains subdued due to a challenging policy environment, shifting terms of trade and infrastructure weaknesses. The services sector, however, continues to grow, building on Zimbabwe’s skilled labor force.

A high public debt overhang still constrains and raises the cost of capital for investment. Successfully addressing the arrears to mulitlateral and bilateral partners would enable relations with external creditors to be normalized. This would strengthen investor confidence and increase private financial flows, as well as allow partners to fully support Zimbabwe's development and to help protect the poor.

To raise growth, Zimbabwe will have to correct key macroeconomic imbalances in particular, the high current account deficit, which will require real improvements in investment, productivity and adjustments in public spending. Indeed, without substantial improvements in the allocation and efficiency of public spending, the poor will bear the brunt of the headwinds ahead.

Executive Summary

Recent Developments

Trend economic growth is now around 2-3 percent per annum following the end of the dollarization boom in 2012. Prices have stabilized, and the turbulence of the 2000s is giving way to a restructured Zimbabwean economy. Agricultural production now represents a broadly constant share of total output, while the service sector is experiencing dynamic growth. However, the manufacturing and mining sectors are struggling to cope with rising capital costs, a difficult business climate and a decline in external competitiveness. As a result, there has been a shift in economic activity from industry to services.

A poor growth and worsening external environment contributed to a deceleration in 2015 and growth is projected to remain at 1.5 percent in 2016. The GDP growth rate slowed from 3.8 percent in 2014 to 1.5 percent in 2015 and 2016, due largely to the impact of an ongoing drought, which is taking a heavy toll on agriculture production. The depreciation of the South African rand against the US dollar has weakened Zimbabwe’s competitiveness vis-à-vis its main trading partner. Exchange-rate dynamics are having an especially negative impact on the mining and manufacturing sectors, which already face considerable challenges in attracting investment. The mining sector is experiencing a structural transition as the commodity super-cycle ends. Growth in the service sector particularly finance, insurance and construction has accelerated.

Weather-related shocks to the agricultural sector have had an especially negative impact on the poor. Over 90 percent of Zimbabwe’s extremely poor live in rural areas. Of these households, the overwhelming majority depend directly or indirectly on agriculture. The drop in agricultural output in 2015 is estimated to have temporarily increased the poverty rate by about 1.5 percentage points, marginally reversing the substantial gains in poverty alleviation that were achieved during the stabilization period. Projections for a poor harvest in early 2016 suggest that poverty may increase further this year.

Low export prices and high production costs are contributing to a persistent deficit in the external accounts. Despite narrowing somewhat in recent years, Zimbabwe’s current account deficit remains much larger than those of comparable countries in the region, and exports currently amount to just over half of imports. A decline in global prices for gold, platinum and other mineral commodities, coupled with unresolved supply-side constraints, has reduced the value of mining exports. Zimbabwe has also benefited from lower oil prices, butrising import volumes largely offset the impact on import values. Remittances gradually increased during 2010-2015 and are estimated to have reached almost 7 percent of Gross National Income (GNI) in 2015. The deficit is primarily financed by capital inflows, especially foreign borrowing, but unfavorable terms contribute to making this model unsustainable over time.

Growth has been largely driven by consumption, while both public and private investment has fallen substantially since 2011. Aggregate consumption exceeds GDP and has made a disproportionally large contribution to economic growth during 2010-15. Public sector investment is constrained by severely limited fiscal space for non-wage expenditures and scarce external borrowing opportunities. Investment fell to an estimated 13 percent of GDP in 2015, as a high cost structure and a difficult business climate continued to erode firm competitiveness. Capital inflows, including external borrowing and asset sales are sustaining consumption growth, but this is untenable over the long-term.

The domestic financial sector is slowly recovering from a post-dollarization credit boom and interest rates remain elevated. The Central Bank has stabilized the financial sector, a recent growth of broad money looks robust and bank lending has become market-driven. But still only blue-chip borrowers are able to access financing at competitive rates. The authorities are taking measures to update Zimbabwe’s credit infrastructure, strengthen oversight and restore the regulatory framework.

Zimbabwe is experiencing a deflationary trend in response to these macroeconomic imbalances. The multicurrency regime, adopted in 2009, limits monetary policy instruments available to the authorities but also provides a level of fiscal and economic restraint. As competitive pressures increased, the consumer price index fell -2.5 percent, year-on-year, at end-2015. Declining prices should help to restore competitiveness over time, but should be accompanied by efforts to raise productivity at all levels of the economy.

The Government has maintained a tight fiscal stance in recent years and the primary deficit remains small and manageable. Fiscal revenue represented over 25 percent of GDP from 2011 to 2015, but the public sector wage bill accounts for more than three-quarters of total spending during recent years. A tight fiscal envelope has encouraged the authorities to adopt innovative financial management strategies in the health sector, improving health outcomes and generating important lessons for other sectors.

Outlook and Challenges

Zimbabwe’s economic outlook is subdued, and growth is projected to remain at 1.5 percent in 2016 as El Nino related weather conditions depress agricultural output, but growth is expected to revert to trend growth of 2-3 percent in 2017-18. However, these projections are subject to upside and downside risks, both of which are intensified by the economy’s dependence on a limited range of key sectors. Unfavorable weather conditions compounded by the 'ElNino' weather, power shortages,insufficient liquidity in agricultural markets and limited access to agricultural credit will continue to threaten agricultural production over the projection period. Meanwhile, a further decline in global commodity prices, an economic shock in South Africa, or the further depreciation in the South African Rand against the US dollar could put Zimbabwe’s recovery at serious risk. Finally, Zimbabwe’s current account deficit is equal to over 17 percent of GDP, while the investment rate is 13 percent and the GDP growth is 1.5 percent; this situation is unsustainable.

Zimbabwe has enormous potential for inclusive growth, but it will be a complex challenge to ensure that recovery is truly broad-based and not regressive. As a country, Zimbabwe's education expenditures relative to GDP are among the highest in Sub-Saharan Africa and the Country has an impressive human capital base. Following the economic disruptions of the 2000s, income distribution is more equitable than at any time in the country’s recent history. But the price of this redistribution, and the new downside risks facing the economy have a disproportionately negative impact on middle and low-income households. The authorities have demonstrated a credible commitment to broad-based growth, but without correcting key imbalances in both private sector and public sector service delivery, the recovery could take place in a way that is regressive and could compromise Zimbabwe’s path toward a fair distribution of the gains from further economic growth.

Clearing external debt arrears is important to Zimbabwe’s medium-term growth trajectory. The total public and publicly guaranteed external debt was estimated to be US$7.1 billion (51 percent of GDP) as at September 2015, with external arrears occupying a large share at US$5.6 billion (79 percent of total external debt). The public debt burden has had a deleterious impact on the cost of capital and the economy. It has limited Zimbabwe’s access to financing for development and raised the cost to the private sector of accessing international capital markets. The authorities have recognized that clearing the arrears would allow for a resumption of longer term and concessional development financing both for investment and for buffering the impact of current shocks on the poor and vulnerable. To this end, the Government has presented a strategy to clear Zimbabwe’s arrears to multilateral institutions in 2016 using own resources and loans, at a meeting with its international creditors during the 2015 annual World Bank – IMF meetings. If successful, this strategy will go a long way to lifting Zimbabwe’s medium-term growth outlook.

Related News

Conflict grows out of inequality and exclusion

For a while Africans enthusiasm with the good economic performance of the continent has had a contagious lazy effect in many minds. It was as if the road to a new continental status was a given, even though we were all too busy approving many frameworks and strategies, centered on the need for real structural transformation. Unfortunately the time for a wake-up call is passed.

A combination of renewed conflict, drop on commodities demand and prices, including oil, high currency volatility, rising interest rates, choking of key economic locomotives and another devastating visit of our hated El Niño, are dominating yet again the African story line. Let us get the story straight.

The fundamentals for Africa’s economic prospects are there and intact. Africa continues to register the highest growth within a global slump, our international reserves took a beaten, but this is to be put in contrast with still internationally low debt levels, public deficits are still under control, and steady increase in investments from many , although not all, sources. Recent Summits with India and China, the two demographically equivalents, demonstrated trust in the future. Infra-structure projects have mostly not been affected by the downturn, from a new Suez Canal, to the largest ever dam in Ethiopia or world size solar farms in three countries. As far as the economy is concerned the news are actually better than most could afford. So, where are then the key factors that shift the mainstream narrative back to the past?

Squarely it is a combination of two factors: fragility perception and lack of deeper structural transformation, seen as the need to combine higher agricultural productivity, adding value to natural resources, modernized services associated with urban and youth bulges, powered by strong industrialization. African Agenda 2063 approved by the continent’s leaders is all about that.

If Africa is going to sustain a different narrative it has to be based in real changes. It is therefore opportune to focus on the part of the continental narrative less strategically assessed by Africans themselves: the causes of conflicts.

Between the early hours of April 11th and the late afternoon of May 14th 1994, fifty thousand Rwandese where killed with machetes by their neighbors in the Nyamata Hill. This was a very small part of what is now considered the largest genocide since World War II. A genocide that took the lives of hundreds of thousands of Rwandese. This shocking reality requires for us to understand why was this possible? One participant in the brutal killings said: “Rule number one was to kill. Rule number two, didn’t exist.”[1]

Is it possible to recognize amongst those we call terrorists, be it Al Shabbab, Boko Haram or those who perpetrate the carnages in Central African Republic or South Sudan, a similar rule book? Killing without remorse? Doing it like a job, better than planting or surviving in the periphery, and then have a good drink and laugh at the panic provoked and media attention. How can this happen? How can this continue to happen?

Huge differences in the distribution and exercise of political and economic power result in violent conflicts, in absence or failure of a political mechanism to address inequality. Inequality between groups rather than individuals is probably the foremost cause of conflict in Africa. It exists on three mutually reinforcing levels: economic, social and political. Relatively deprived groups seek or are persuaded by their leaders to seek redress. Privileged groups may also be motivated to fight to protect privileges. Horizontal inequalities are most likely to lead to conflict where they are substantial, consistent, and increasing over time. Exclusion, the extreme manifestation of inequality, is a major factor igniting conflicts. Of particular attention is the exclusion of youth. Uneducated and unemployed youth is a common characteristic to countries experienced conflicts. This marginalized and excluded fraction of the population has been more prominent in the conflict as combatants and least visible during peace.

Very often the richest regions in minerals, oil and gas and which contribute most of national revenue are the poorest in terms of social development and general wellbeing. The collapse of State institutions translated by its inability and ineffectiveness to provide basic services or security has proven to be an important trigger to conflicts. Social stability is based on a hypothetical social contract between citizens and government. People accept state authority so long as the state delivers services and provides reasonable economic conditions. With economic stagnation, decline, or worsening state services, the social contract breaks down, and violence is likely to occur. The collapse of infrastructure completes the erosion of state authority. The combination of a breakdown of institutions and physical infrastructure coupled with the use of ethnic violence creates the conditions in which violence becomes self-sustaining. Evidence suggests a higher incidence of conflict among countries with low per capita incomes, life expectancy, and meagre economic opportunities.

Of the 54 African states only 8 have not experienced armed or violent conflict since independence.

War confers benefits on individuals as well as costs which can motivate people to fight. Young uneducated men, in particular, may gain employment as soldiers. War also generates opportunities to loot, profiteer from shortages and from aid, trade arms, and carry out illicit production and trade in oil, drugs, diamonds, timber, and other commodities. Where alternative opportunities are few, because of low incomes and poor employment, and the possibilities of enrichment by war are considerable, the incidence and duration of wars are likely to be greater. This “greed hypothesis” has its base in rational choice economics. Very often, political leaders deliberately “rework historical memories” to engender or strengthen cultural identities in the competition for power and resources and justify the recourse to violence because of economic interest.

Environmental stress can be a serious catalyst for violence too, especially when people seek alternatives to desperate situations, while resource riches give strong motivation to particular groups to gain control over such resources. This reality is maximized by illegal trade and financial transactions that are depriving the continent of over fifty to sixty billion USD every year.

Results show that the economic performance of conflict areas is on average 10% below that of conflict-free areas in most GDP performance categories. A study estimated a loss of 284 billion USD (in constant 2000 rates) for 23 African countries, from 1990 to 2005. This figure represented then an average annual loss of 15% of their GDP. Regression analysis indicates a loss of about 2.2% GDP growth due to conflict. The interrelated nature of African economies also means that the costs of war within a sub-region generally result in economic costs for neighboring countries. These include production losses through loss of opportunities deriving from migration, trade losses, increased costs of security and policing and the costs of supporting refugees.

In Niger’s real GDP growth reduced to 3.6% in 2013 after expanding by 11.1% in 2012. In Mali, the series of events triggered by the 2012 outbreak of conflict and insecurity led to falls in government resources and expenditures by at least 30%. In DRC internal investment as a percentage of GDP dropped from 31.6% in 1997 to 17.7% in 1998; and reached its lowest level of 2% in 2000. Libya oil output has shrunk to less than 400,000 barrels per day (bpd), from about 1.7 million bpd before the outbreak of conflict. As a result, GDP contracted by an estimated 24% in 2014. The government accounts are expected to post a deficit of about 80 % of GDP in 2015, with the current account deficit exceeding 60% of GDP.

The message is clear. African priorities either deal upfront with the causes of conflict, or everybody will pay the price for the fragility perception. It is true that countries in Europe, Asia or the Americas were stabilized after prolonged wars that were fomented by the same ingredients of exclusion. They evolved to create better institutions, regulated markets and stabilized security. But it is also true that when it happened there, there was no universal telephony coverage or global media. A continent with more conflicts and affected people than Africa right now, continues to be associated with progress and change. I am talking about Asia. If Africa wants to follow suit there is a need for boldness, a common security framework and squarely accept the challenges of exclusion and managing diversity. That is the only way on deals with die hard perceptions.

Rule number one -to kill- with no rule number two, is still mobilizing far too many in the continent. We need Africa to focus on the “why”, and not allow this pervasive virus mentality to rotten past decade and a half achievements.

The why in fact can take inspiration from a virus’s metaphor. Any virus is basically a micro infectious agent that replicates only inside the living cells of other organisms. Viruses can infect all types of life forms. Even if they are not inside an infected cell or in the process of infecting a cell, viruses exist in the form of independent particles. Virus spread in many different ways, but they do have a pattern. It is known that virus can come from far away.

The good news is that viral infections in humans provoke an immune response that usually eliminates the infecting virus. Immune responses can also be produced by vaccines, which confer an artificially acquired immunity to the specific viral infection.

Africa either has strong immunity to deal with these terror groups viral effects, because of the strength of its institutions and capabilities, or has to develop, fast, a vaccine that will rid us of its damage. Such a vaccine could be labeled “antidote to exclusion”.

This article is based on a speech delivered by Carlos Lopes at the 26th African Union Executive Council, 25 January 2016, Addis Ababa.

[1] Reference to Jean Hatzfeld, Une saison de machettes, Seuil, 2003.

Related News

Launch of the 2015 Global Go To Think Tank report

The Economic Commission for Africa joins hundreds of think tanks and civil society actors around the world in a series of annual coordinated events as part of a program organized by the Think Tanks and Civil Societies Programs at the University of Pennsylvania (TTCSP).

The events are intended to highlight the important role think tanks play in government and civil societies around the world. This year’s theme is “Why Think Tanks Matter to Policymakers and the Public.”

This year’s Go To Think Tank Index Launch marks the ninth annual event organized by the TTCSP to acknowledge the important contributions of think tanks worldwide. TTCSP’s initial effort to produce a global ranking of the world’s leading think tanks in 2006 was in response to a series of requests from donors, government officials, journalists, and scholars who wanted the TTCSP to identify the leading think tanks in the world.

Since its inception, the objective for the Global Go To Think Tank Index report has been to gain a better understanding of the role think tanks play in governments and civil societies and help enhance the quality, capacity, and performance of think tanks around the world.

The global launches are taking place in 75-80 countries, including one at the Economic Commission for Africa's Conference Centre, on 5th February 2016.

About the Think Tanks and Civil Societies Program

The Think Tanks and Civil Societies (TTCSP) at the Lauder Institute of the University of Pennsylvania conducts research on the role policy institutes play in governments and in civil societies around the world. Often referred to as the “think tanks’ think tank,” TTCSP examines the evolving role and character of public policy research organizations.

Over the last 20 years, the Think Tanks and Civil Societies Program has laid the foundation for a global initiative that will help bridge the gap between knowledge and policy in critical policy areas such as international peace and security, globalization and governance, international economics, environment, information and society, poverty alleviation, and health.

This international collaborative effort is designed to establish regional and international networks of policy institutes and communities that will improve policy making as well as strengthen democratic institutions and civil societies around the world.

» Download the Go To Think Tank Index.

Related News

Commissioner Acyl articulates the dire need for Africa’s structural transformation in line with the Agenda 2063

The Commissioner for Trade and Industry of the African Union Commission (AUC) held a press briefing on 27 January 2016 on the margins of the 26th African Union Summit of Heads of State and Government, under the theme: “The African Union’s Trade and Industry Agenda as a catalyst for Africa’s Development”.

H.E. Mrs. Fatima Haram Acyl highlighted the Department of Trade and Industry’s initiatives within the context of the Agenda 2063 and expressed the urgent need for Africa to industrialize.

According to the Commissioner for Trade and Industry, Africa faces an imperative for structural transformation. H.E. Mrs Fatima Haram Acyl observed that we need to address the paradox of a rich continent with poor citizens. Therefore urgent steps must be taken to create sustainable jobs that will improve the well-being of the people of Africa, especially women and youth.

The Commissioner for Trade and Industry also pointed out that African Union’s trade and Industry agenda is looking to support the continent’s structural transformation agenda, in line with Agenda 2063 and underscored that the fall of the commodities prices have reinforced the imperative of diversifying away from commodities based economies.

“I want to highlight two critical initiatives that are central to ensuring that the AU’s trade and Industry agenda will play a catalytic role in the continent’s transformation agenda. These are initiatives related to the Africa Mining Vision as well as the Boosting Intra-African Trade and fast tracking the Continental Free Trade Area,” she said.

Commissioner Acyl mentioned that the Africa Mining Vision provides a framework for providing technical assistance currently provided through the 5 year African Minerals Development Center (AMDC) project involving AUC, UNECA, AfDB, UNDP and other partners in a manner that ensures ownership by African governments of these interventions.

The Commissioner also announced the AUC has been mandated to develop a Continental Commodities Strategy that will address the issues of commodity pricing and commodity based industrialization more broadly, building on the experiences of the past decades. “The strategy reviews the state of play of agriculture, mining and energy commodities in Africa and identifies and articulates areas of national, regional and continental policy and will be finalized this year,” she echoed.

With regards to the Boosting Intra-African Trade and the negotiations of the Continental Free Trade Area (CFTA), Commissioner Acyl indicated that the establishment of the CFTA, will create a single market for goods and services in Africa for over a billion people and a GDP of over 3 trillion dollars provides a good reason to invest and partner in Africa. The CFTA, she said, could increase intra-African trade by as much as $35 billion per year, or 52 percent above the baseline, by 2022 especially with the implementation of the WTO Trade Facilitation Agreement.

She thanked Member States and development partners for their technical and financial support during the preparatory phase and indicated that all efforts have been made to facilitate negotiations for 54 countries. She concluded by announcing that the first negotiating session of the CFTA negotiations will take place in February in Addis Abba, Ethiopia.

Related News

IMF reforms policy for exceptional access lending

The IMF has approved an important reform to the institution’s policy on lending to countries that request large-scale financing.

The broad objectives of the reform – which includes the removal of the “systemic exemption” that was created in 2010 – is to help promote more efficient resolution of sovereign debt problems and avoid unnecessary costs for the member, its creditors, and the overall system.

“This latest reform to our lending framework is actually part of a broader reform agenda aimed at more efficiently resolving sovereign debt crises where they occur, as well as to prevent their occurrence in the first place,” said Sean Hagan, the IMF’s General Counsel.

“The reform is carefully designed to preserve the IMF’s ability to continue to provide financing to assist members in resolving their balance of payments problems, including in the presence of contagion risks,” said Hugh Bredenkamp, Deputy Director of the Strategy, Policy and Review Department of the IMF.

Evolution of the “exceptional access” framework

In the late 1990s and early 2000s, the IMF provided financing to a number of its members that were experiencing capital account crises which, on several occasions, involved “exceptional access” to IMF resources – that is, financing amounts that exceeded normal IMF lending limits. The requirements in place at the time to justify these large-scale lending programs were “exceptional circumstances,” and these were not clearly defined. This left the IMF vulnerable to pressure to provide large amounts of funding even when prospects for program success were not as strong as should have been for the level of risk the IMF was assuming.

To address these concerns, the IMF established a comprehensive exceptional access policy framework in 2002. Under this framework, the IMF could only provide large-scale financing in capital account crisis if all of four conditions were met, one of which was that there is a “high probability” that the member country’s debt is sustainable. This is the second exceptional access criterion.

The other three exceptional access “criteria” (as they are known as) relate to a member experiencing exceptionally large balance of payments needs; the member having prospects for gaining/regaining access to private capital markets; and the member having the institutional and political capacity and commitment to implement a IMF-supported program.

With respect to the second criterion on debt sustainability, if the high probability bar was met, the IMF could lend without requiring any debt operation. If, however, the bar was not met, a sufficiently deep debt restructuring was typically needed to restore debt sustainability with high probability before the IMF could lend. There was no middle ground between providing financing and requiring a deep debt reduction. Accordingly, for members whose debt was “sustainable but not with high probability,” the debt reduction operation could constitute an unnecessarily drastic measure.

This underlying rigidity in the 2002 exceptional access framework was tested in 2010, in the context of the first IMF-supported program for Greece. Because the IMF did not assess Greece’s debt to be sustainable with high probability, the framework required an upfront debt reduction. However, there were serious concerns at the time that this could lead to severe contagion both in the Eurozone and beyond. Thus, at the time, the IMF created a “systemic exemption” for cases where there were significant uncertainties around debt sustainability. In such cases, the exemption allowed large-scale financing to go ahead without a debt reduction operation if there was a high risk of systemic international spillovers (see figure).

Shortcomings revealed

While the systemic exemption was a step towards greater flexibility, it had several shortcomings, which revealed themselves over time.

-

First, the exemption did not prove reliable in mitigating contagion. And this is understandable. Insofar as it left market concerns about underlying debt vulnerabilities unresolved, the exemption was unlikely to instill market confidence in the program and thereby limit contagion.

-

Second, by replacing maturing private sector claims with official claims, it increased “subordination risk” for private creditors – that is, the risk that private claims would rank lower than official claims in the case of an eventual default – making it more difficult for the country to regain market access.

-

Third, for the two reasons above, the systemic exemption entailed substantial costs and risks for the member country and the IMF. In particular, it delayed the restoration of debt sustainability, impaired the prospects of success for the country’s economic policy program, and eroded safeguards for IMF resources.

-

Finally, the exemption had the potential to aggravate “moral hazard” in the international financial system, i.e., the tendency of creditors to overlend to a sovereign at interest rates that do not fully reflect the sovereign’s risky debt situation, since they believe they are likely to be bailed out in the event of a sovereign debt crisis.

A reformed, more calibrated, but appropriately flexible framework

The reformed policy, developed by IMF staff in a series of papers in 2013, 2014 and 2015, seeks to improve the existing framework in two important ways.

First, it removes the systemic exemption, for the reasons noted above.

Second, it gives the IMF appropriate flexibility to make its financing conditional on a broader range of debt operations, including the less disruptive option of a “debt reprofiling” – that is, a short extension of maturities falling due during the program, with normally no reduction in principal or coupons.

The reformed policy – like the old one – prescribes that when debt is clearly sustainable (let us call it the “green” zone), the IMF will continue to use its catalytic role and provide financing support to the member without requiring any debt operation. When debt is clearly unsustainable (the “red” zone), a prompt and definitive debt restructuring will continue to be required to restore debt sustainability with “high probability”.

However, for countries where debt is assessed to be sustainable but not with a high probability (i.e. the “gray” zone), the new policy allows the IMF to grant exceptional access without requiring debt reduction upfront, as long as the member also receives financing from other creditors (official or private) during the program. This financing should be on a scale and terms that (i) helps improve the member’s debt sustainability prospects, without necessarily bringing debt sustainability to the green zone at the outset; and (ii) provides sufficient safeguards for IMF resources.

The new policy does not automatically presume that a reprofiling or any other particular option would be implemented at the outset when debt is in the gray zone. Instead, the choice of the most appropriate option, from a range of options that could meet the two conditions noted above, would depend on the member’s specific circumstances.

In situations where the member retains market access, or where the volume of private claims falling due during the program is small, sufficient private exposure could be maintained without the need for a restructuring of their claims.

In situations where the member has lost market access and private claims falling due during the program would constitute a significant drain on available resources, a reprofiling of existing claims would typically be appropriate. This could allow a somewhat less stringent adjustment path while also reducing the required amount of financing from the IMF. Although a reprofiling is a form of debt restructuring, it will likely be less costly to the debtor, the creditors, and the system than a definitive debt restructuring.

Where a reprofiling is undertaken, the scope of debt to be reprofiled would be determined on a case-by-case basis, recognizing that it would not be advisable to reprofile a particular category of debt if the costs for the member of doing so – including risks to domestic financial stability – outweighed the potential benefits. For instance, short-term debt instruments (by original maturity), trade credits, and local currency-denominated debt have typically not been included in most past restructurings.

Under the new policy, financing from official bilateral creditors, where necessary, could be provided either through an extension of maturities on existing claims and/or in the form of new financing commitments.

The new policy would also allow the IMF to deal with rare “tail-event” cases where even a reprofiling is considered untenable because of contagion risks so severe that they cannot be managed with normal defensive policy measures. In these rare cases, the IMF could still provide large-scale financing without a debt operation, but would require that its official partners also provide financing on terms sufficiently favorable to backstop debt sustainability and safeguard IMF resources.

This could be done through assurances that the terms of the financing provided by other official creditors could be modified in the future if needed (say in the event of downside risks materializing). If official partners could not provide such assurances (or if the member’s debt was deemed unsustainable at the outset), the terms of official financing would have to be sufficiently favorable to bring debt to the green zone.

In essence, all these options illustrate appropriate flexibility that the new framework embodies (see figure above).

In addition to the improvements to the second exceptional access criterion, the reformed policy also modified the third, or “market access”, criterion. The Board confirmed that the third criterion, which requires a member to have prospects for gaining/regaining market access remains binding even when there are open-ended commitments of official support for the post-program period. It also clarified that the timeframe within which a member is expected to gain/regain market access has to be consistent with the start of repayment of its obligations to the IMF, not just when the last one is due, as could have been implied by the old formulation of the criterion.

Putting it all together

The above reform is a central component of a four-pronged work program on sovereign debt crisis resolution endorsed by the IMF’s Executive Board in 2013. The reforms follow a series of Board discussions and consultations with stakeholders over the last three years. Before this latest reform to the exceptional access policy, the IMF had already completed two of the four components:

-

In October 2014, the Executive Board endorsed key features of enhanced collective action clauses in international sovereign bond contracts to reduce their vulnerability to holdout creditors in case of a debt restructuring. Many members now include clauses consistent with these key features in new international debt issuances.

-

In December 2015, the Board approved the reform of the IMF’s policy on non-toleration of arrears to official bilateral creditors, which allows the IMF to lend in the presence of arrears to official bilateral creditors under carefully circumscribed circumstances.

Later this year, the IMF will consider the final component of the sovereign debt restructuring work program, which intends to discuss, inter alia, issues related to debtor-creditor engagement, including the IMF’s lending-into-arrears policy for private creditors.

Together, these four workstreams will help facilitate the resolution of sovereign debt crises, thus benefiting the international financial system as a whole.

Related News

Investment Facilitation: An Action Menu

Preliminary draft for peer review, based on UNCTAD’s Investment Policy Framework for Sustainable Development

Mobilizing investment and maximizing its positive contribution to growth and sustainable development is a priority for most countries. Concerted efforts are required to boost cross-border investment, within the context of an overall policy framework aimed at maximizing the benefits of such investment for host countries and minimizing any negative side effects.

Numerous initiatives aimed at stimulating investment exist that try directly to affect the risk-return ratio for investors. Such initiatives may try to lower risks by providing guarantees, by sharing risks or by offering certain protections. Or they may try to increase potential investor returns through incentives.

In the most common international instruments for investment promotion, relatively little attention is being paid to ground-level obstacles to investment, such as a lack of transparency on legal or administrative requirements faced by investors, lack of stability and predictability in the operating environment, and other factors causing high costs of doing business.

Addressing such barriers to investment could provide a real boost to both cross-border and domestic investment, complementing direct stimulus instruments (guarantees, incentives), and reinforcing trade facilitation efforts – given that 80% of trade is driven by the international production networks dependent on investments from multinational firms.

Investment facilitation initiatives could, in fact, mirror many elements common in trade facilitation. They could include improvements in transparency and information available to investors; they could work towards efficient and effective administrative procedures for investors; they could enhance the consistency and predictability of the policy environment for investors through consultation procedures; they could increase accountability and effectiveness of government officials and mitigate investment disputes through ombudspersons; they could include cross-border coordination and collaboration initiatives such as regional investment compacts or links between outward and inward investment promotion agencies; and they could include technical cooperation and other specific support mechanisms for investment.

The Action Menu proposed here for discussion is based on UNCTAD’s Investment Policy Framework and rich experiences and practices of investment promotion and facilitation efforts worldwide over the past decades.

The Action Menu proposes 10 action lines with a series of options for investment policymakers to adapt and adopt for national and international policy needs: the package includes actions that countries can choose to implement unilaterally, and options that can guide international collaboration or that can be incorporated in international investment agreements. The Action Menu should be read in the broader context of UNCTAD’s Investment Policy Framework for Sustainable Development.

The proposed Action Menu is preliminary research and does not represent the official views of UNCTAD member States or the UNCTAD Secretariat. Comments and ideas will be invaluable to the further development of the Action Menu.

This Discussion Note is made available on UNCTAD's Investment Policy Hub to facilitate online feedback and discussion as an integral part of the Investment Policy Blog. Readers are invited to submit comments via email to Mr. James Zhan, Director of the Investment and Enterprise Division at This email address is being protected from spambots. You need JavaScript enabled to view it..

Related News

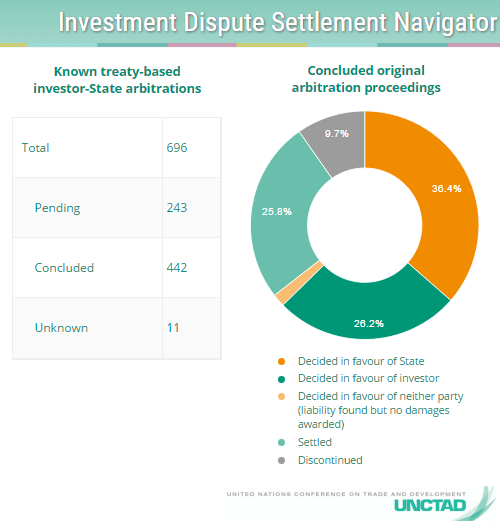

Record number of Investor-State Arbitrations filed in 2015

UNCTAD has updated its recently launched Investment Dispute Settlement Navigator. The ISDS Navigator is now up to date as of 1 January 2016.

The update reveals that the number of investor-State dispute settlement (ISDS) cases filed in 2015 reached a record high of 70. Spain was by far the most frequent respondent in 2015, with 15 claims brought against it. The Russian Federation is second on this list with 7 cases.

As of 1 January 2016, the total number of publicly known arbitrations against host countries pursuant to international investment agreements (IIAs) has reached nearly 700.

In the coming weeks, UNCTAD will publish its annual IIA Issues Note on “Recent Developments in ISDS”, providing a more detailed analysis of the newly filed cases as well as an overview of the key decisions issued by arbitral tribunals over the course of 2015.

The Investment Dispute Settlement Navigator is the world’s most comprehensive ISDS database. Each of the 696 case entries contains information on: legal basis (applicable treaty); countries involved; short summary of the dispute; economic sector and subsector; amounts claimed and awarded; breaches of IIA provisions alleged and found; arbitrators serving on the tribunal; status/outcome of the arbitral proceedings; decisions issued by tribunals and other items (to the extent the information is publicly available).

Any additional information or clarifications on specific cases as well as suggestions for improving the ISDS Navigator would be welcome (to submit information, use the “Report new developments” button).

Related News

UNCTAD Expert Meeting: Taking stock of IIA Reform

Multi-year Expert Meeting on Investment, Innovation and Entrepreneurship for Productive Capacity-building and Sustainable Development, fourth session

The meeting will discuss policy perspectives of the issues under discussion in the Multi-Year Expert Group on Investment, Innovation and Entrepreneurship for Productive Capacity-Building and Sustainable Development.

The meeting will take stock of developments in bilateral, regional, and multilateral investment policy, with a specific focus on the reform efforts related to the regime of international investment agreements.

Further, the meeting will consider several lessons on science, technology and innovation policy identified by UNCTAD, particularly in the context of its policy advice and capacity-building work, and it will provide an update on entrepreneurship policies and their relation to the achievement of the Sustainable Development Goals.

This will enable a discussion on the UNCTAD Investment Policy Framework for Sustainable Development, the Entrepreneurship Policy Framework and the Science, Technology and Innovation Policy Framework.

The meeting will also serve as a preparatory step towards UNCTAD intergovernmental activities in 2016, in particular those of the Investment, Enterprise and Development Commission.

Investment, innovation and entrepreneurship and productive capacity-building for sustainable development

The topic for the fourth session of the Multi-year Expert Meeting on Investment, Innovation and Entrepreneurship for Productive Capacity-building and Sustainable Development was decided at the fifty-sixth executive session of the Trade and Development Board, in 2012, as follows: “The fourth session of the expert meeting will bring together the findings of the three preceding meetings, with a view towards refining UNCTAD’s Investment Policy Framework for Sustainable Development, the Entrepreneurship Policy Framework and the Science, Technology and Innovation Policy Framework.”

This last session is thus intended to summarize the work of the multi-year expert meeting from the policy perspective, bringing to a close the cycle of work undertaken on the subject matter. The timing of the fourth session suggests that it will also serve as a preparatory step towards the fourteenth session of the United Nations Conference on Trade and Development (UNCTAD XIV), in particular the deliberations under sub-theme 2 of promoting sustained, inclusive and sustainable economic growth through trade, investment, finance and technology to achieve prosperity for all.

Investment is essential to build productive capacities and ensure sustainable development. New generations of investment policies have emerged that place inclusive growth and sustainable development at the heart of efforts to attract and benefit from investment. This prompted UNCTAD to update its Investment Policy Framework for Sustainable Development. Following guidance from member States, specific attention is being given to how to address investment policy challenges at the regional and international levels. In particular, and in light of the pressing need for systematic reform of the global regime of international investment agreements, it is necessary to take stock of efforts and bring that reform in line with today’s sustainable development imperative.