Search News Results

Keeping the world below 2 degrees is a $12.1 trillion investment opportunity, BNEF report says

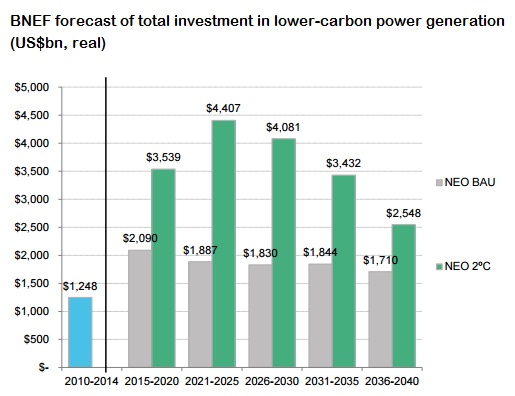

Keeping the world below the 2 degrees Celsius pathway presents a US$12.1 trillion investment opportunity over the next 25 years, a new analysis states.

The report Mapping the Gap: The Road From Paris, presented by Bloomberg New Energy Finance (BNEF) at the 2016 Investor Summit on Climate Risk hosted by Ceres, shows the opportunities and challenges of filling the ‘gap’ between the business-as-usual (BAU) investment in renewable energy and what is needed to avoid the worst effects of climate change.

At the Summit, the UN Secretary-General Ban Ki-moon called investors to at least double their investments in clean energy by 2020, adding that “we must begin the shift away from fossil fuels immediately.”

Earlier in January, another BNEF report showed how global clean investment attracted a record US$329 billion last year – about six times the amount invested in 2004.

Just a month ago, countries signed at COP21 in Paris a historic agreement to tackle climate disruption and keep global warming well below 2 degrees Celsius, compared to the pre-industrial era. However, the report by BNEF shows that to achieve this goal, investment in new renewable power generation must increase 75% above the BAU trajectory.

In fact, if governments and business leaders take no additional steps to what they have planned today, the investment opportunity for tackling climate change is US$6.9 trillion, or US$277 billion per year.

The ‘gap’ between this scenario and what is needed to keep the world safe is US$5.2 trillion, or US$208 billion per year. To put the numbers in perspective, authors point out this is far less than the US$454 billion per year that people in the US ask every year to get their auto loans.

Nevertheless, “there still remains much to be done,” says Mark Kenber, CEO, The Climate Group, in a recent blog. “While the leaders in the investment, corporate and sub-national communities have demonstrated that bold climate action brings economic benefits, the task now is to ensure those in the mainstream follow this leadership.”

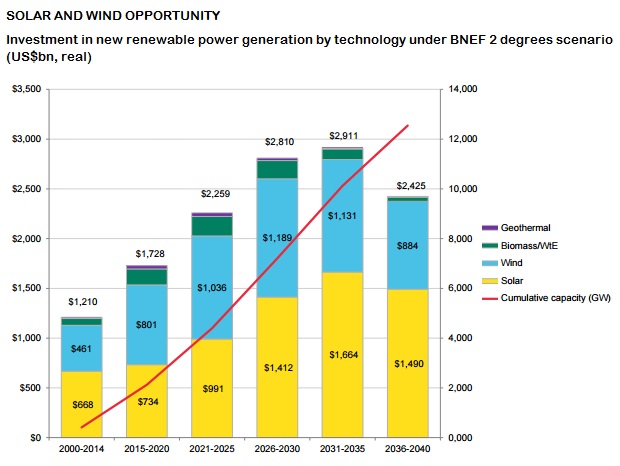

To reach this point, renewable investment must scale up quickly in the next 15 years, grasping opportunities already available today to reach 12,500 gigawatts globally by 2040.

Under this scenario, which excludes large hydropower investment, wind and solar have the lion’s share growing 46% and 43% respectively in the first decade – thanks in particular to their increasingly lowering prices and off-grid potential.

In fact, the report forecasts that the cost per unit of clean energy is due to decline consistently through the full 25 years analyzed, from an average of US$1.74/megawatt (MW) in the 2015-2020 period to $1.03/MW by the 2036-2040 period.

Policies and solutions

To scale up the opportunities offered from the 2 degrees pathway, many policies have proven to be successful. One of these solutions is putting a price on carbon, such as the system created in 2014 by Québec and California – governments that are part of The Climate Group’s States & Regions Alliance – that created the first cross-border market in North America.

Also Ontario, another valuable member of the States & Regions Alliance, last year launched a ‘cap-and-trade’ system to curb its emissions, aiming to link it to the system set up by Québec and California.

Other solutions envisaged by the report are tax incentives, to accelerate investments on clean power plants and manufacturing facilities, and feed-in tariffs to spur a widespread adoption of renewables among customers and businesses.

“Clean energy financing is poised to ‘grow up’ to more fully resemble other, better established infrastructure sectors,” conclude the authors of the report, “such as transportation or real estate, from a financial structure perspective.

“These new finance vehicles will present massive new opportunities for capital deployment. Policy makers need to ‘mind the gap’ to ensure that investment grows at the speed and scale required.”

Related News

USTR Public Hearing: Trade and Investment in Africa – Jim Kolbe Testimony

Washington, D.C., 28 January 2016

Mr. Ambassador, Mr. Chairman, Members of the Committee:

It is a great pleasure to appear today for this public hearing on the topic of trade and investment opportunities in Africa. The subject is very timely. Africa, at long last, is getting some of the attention it deserves from economists, policy makers and – most importantly – from the commercial and investment sectors in the developed world.

Six of the ten fastest growing economies in the world are to be found in Africa. The explosion of technology in communications, while occurring world-wide has been more pronounced and rapid in Africa than any other part of the globe. More people in the past decade have emerged from poverty and into the middle class in Africa than any other continent or country with the exception of China. Trade among members of the new Tripartite Free Trade Area (TFTA) has increased from $2.3 billion annually in 1994 to $36 billion in 2014 – a twelve fold increase in twenty years.

And yet, the potential for development on the African continent remains largely unrealized. Seventy percent of Africa has either inadequate or no electric power. Africa’s trade total accounts for only 3% of all world trade. Within the African continent, intra-regional trade has increased from 7% to 25% during the last twenty years, but remains substantially below that of Europe at 70% or Asia at 50%. Breaking this figure down further, we find that 14% of all imports in Africa come from other countries on the continent, while just 10% of exports go to continental neighbors. In short, we find that Africa’s trade is a woefully small share of the world’s trade, and that most of it finds its way to and from Europe and Asia – not to other African countries.

A major step toward improving African trade and investment took place this past year with the ten year extension of AGOA – the African Growth and Opportunities Act. After seemingly countless starts and stops and short term extensions – too short to be useful in making long term investment decisions – the preference act was both extended for a meaningful period and the coverage significantly expanded. The European Union had already expanded their preferences. These dual actions will help spur significant investment in Africa with a commensurate increase in two way trade.

Within Africa, an even more encouraging development has been the Tripartite Free Trade Area, or TFTA. TFTA is a planned free trade area that would integrate the members of three regional economic communities – the Common Market for Eastern and Southern Africa (COMESA), the East African Community (EAC) and the Southern African Development Community, known as SADC. The TFTA, when fully implemented, would link 26 countries from Egypt in the north to South Africa at the southern tip of the continent. Its objective in the first place would be the elimination of tariffs and non-essential barriers to trade. Promotion of trade in services would follow more gradually. Other objectives would go beyond trade as that term might be narrowly defined, to include investment promotion and free movement of business persons between countries.

While this represents a hopeful development, especially since it is internally generated and not resulting from intervention by the developed countries of Europe or the United States, it also highlights the need for more internally generated reforms. Set alongside the small amount of intra-continental trade previously referred to, it suggests that far more can be done by African countries themselves.

The hard truth is that there is a growing disillusionment in Congress and in the business community for preference programs, a sentiment not altogether unwarranted. AGOA may represent a major opening for trade an investment on the African continent, but there has to be a reciprocal showing from the other side. The quality of governance matters – tackling corruption, a competitive procurement process, transparency, an independent judiciary and adherence to the rule of law, the quality of the work force – these all matter to a business thinking of making a major investment in Africa.

This brings me to the main point of my remarks. As important as preference programs may be, as helpful as foreign assistance can be in bringing about infrastructure developments, I am convinced that the most important objective of our assistance program in Africa must be the facilitation of internal reforms. A simple thing such as developing a uniform Letter of Credit can greatly facilitate trade. Reforms that focus on internet access, enforcement and arbitration of contracts, simplifying customs forms and regulations, and reducing petty corruption are likely to do more for trade and development than all our trade preference programs or infrastructure development.

I remember a visit to Tanzania a few years ago and learning about the difficulties in exporting fresh cut flowers from Tanzania to Europe. Because they lacked adequate air cargo facilities in Tanzania, much of the product crossed the border to Kenya for shipping from the Nairobi airport. But because of the endless paperwork and inadequate staffing, Tanzanian exporters were experiencing on average a 24 hour additional shipping time to cross the border into Kenya. Translated into remaining freshness once the flowers reached their end market, the result was a significant increase in spoilage.

Congress and the administration are to be congratulated on the extension of AGOA – the longest period of continuous preferences since AGOA was first adopted. Now we should turn our attention to the details of making it work. The impetus will have to come from the African country themselves. But we can help if we re-focus our assistance from promoting more preference programs to assisting African countries in removing the regulatory and non-tariff barriers which constitute the biggest impediment to trade and investment on the continent.

Thank you Mr. Chairman.

Related News

Report on the SADC Standardization, Quality Assurance, Accreditation and Metrology (SQAM) Programme

This document contains information provided by SADC at the Technical Barriers to Trade (TBT) Committee meeting of 4-6 November 2015 under Agenda Item 4 (Update by Observers).

Elimination of TBTs in the SADC region is addressed under the framework known as the TBT Annex to the SADC Protocol on Trade. The Trade and Industry, Finance and Investment Directorate is a custodian of this framework and it supports the SADC Free Trade Area.

There are four International Cooperating Partners / International Development Partners (ICP / IDPs) supporting the developmental aspects of the SQAM programme on TBT components at a regional level. These are the European Union, GIZ, PTB, and the Southern Africa Trade and Investment Hub / USAID. Support for national quality infrastructure projects is obtained from UNIDO and is Member State driven.

For SADC Member States, the SQAM Programme has been actively engaged on assisting Member States to have available at least a basic technical infrastructure and in further building capacity as required by the TBT Annex to the SADC Protocol on Trade. The SADC SQAM Programme follows a strategic proactive and developmental approach to continually strengthen the quality infrastructure available in the region in the quest to reduce and eliminate TBTs. Main activities include:

-

Raising awareness for relevant stakeholders in SADC Member States on the importance and benefits of SQAM;

-

Organizing and convening SADC Annual Quality Awards at regional level;

-

Facilitating accreditation of Conformity Assessment Bodies (CABs);

-

Facilitating training for Lead and Technical Assessors for SADC Accreditation Services (SADCAS);

-

Operationalizing the SADC Technical Barriers to Trade Stakeholder’s Committee;

-

Facilitating the identification of Technical Regulations hindering trade; and

-

Coordinating the harmonization of standards, measurement systems and conformity assessment procedures, for harmonization of technical regulations.

Progress on the implementation of the activities is summarized below.

Promotion campaign of the SADC Annual Quality Awards

SADC Annual Quality Awards serve as a platform for private sector engagement on quality of goods and services. The objective of the awards is to recognise enterprises that are implementing quality management principles for competitiveness and market access. In the last year, four Member States organized their national quality competitions with a total of fourteen entries received from three Member States, covering categories on Organisation of the year, Product of the year, Service of the year, Exporter of the year, for both large and small and medium enterprises and Individual Award.

Out of the fourteen entries that were considered, four received awards, representing Mozambique, Namibia and Zimbabwe. Etosha Fishing Corporation, a large enterprise from Namibia was awarded as SADC Organisation of the year and Exporter of the year, Nutriconsult LDA a small and medium enterprise from Mozambique was awarded for SADC Service of the year, and Schweppes Zimbabwe, a large enterprise was awarded for SADC Product of the year.

SADC Annual Quality Awards contribute to increased awareness of the importance on a quality culture and use of international standards for product competitiveness and in trade. SADC Member States continue to give support and engage departments and institutions to continue to organize the National competitions and encourage private and public sector institutions to participate.

Preparation of Conformity Assessment Bodies (CBAs) for accreditation

The strategic long term plan for SADC SQAM Programme on CABs is to encourage CABs to pursue accreditation in order for their test certificates to be recognized the world over by their trading partners. The strategy is to assist CABs prepare for accreditation in way that will address seeming delays due to fundamental systems and processes not being in order for accreditation. While accreditation bodies can point out non-conformances they are not able to assist such bodies to carry out corrective actions before assessments. The idea is to assist these bodies to prepare well in order to avoid delays before accreditation.

The development of the strategy to assist CABs prepare for accreditation commenced in the 4th quarter of 2014/2015 financial year, and was expected to be finalised in the 2nd quarter of 2015/2016. So far a data collection exercise on challenges being faced by laboratories and certification bodies in their attempts to become accredited is underway. Inspection bodies will also be engaged following which the draft strategy will be developed. The strategy document was expected to be finalized by the end of March 2016. While we await the completion of the strategy, in March 2014, 23 representatives from CABs were trained on conducting vertical assessments of their own facilities.

During the 2015/16 financial year the same group will be trained on method validation in preparation for accreditation. Method validation was identified as a constraint during the vertical assessment training. Whilst a start has only just been made in training laboratory representatives in preparation for accreditation, during awareness workshops, enterprises are being encouraged to use existing accredited CABs for their conformity assessment needs which should encourage existing non-accredited CABs to seek accreditation. The conclusion of the CAB Strategy is expected to assist in getting non-accredited CABs ready to apply for accreditation.

Training for lead and technical assessors

In the quest to qualify and register lead and technical assessors for the SADC Accreditation Service (SADCAS), 22 candidate Assessors who were trained on ISO/IEC 17025:2005 (ISO standard for testing and calibration bodies) earlier in 2014, received additional training in March 2015, on Technical Assessing Techniques based on ISO/IEC ISO 17025:2005 to determine their competency levels for accreditation assessments, a prerequisite for registration with SADCAS. Thirteen (13) of these trainee assessors have been recommended for mentoring. As part of mentoring, the trainees will be expected to conduct assessments in various Conformity Assessment Bodies (CABs) in the region under supervision by SADCAS Qualified Assessors.

Further training of Lead and Technical Assessors on ISO/IEC 17020 (Inspection Bodies), ISO 15189 (Medical Testing Laboratories), and the mentoring of Lead and Technical Assessors on ISO/IEC 17020 (Inspection bodies), ISO 15189 (Medical Testing Laboratories), ISO/IEC 17025 (Testing Laboratories) will be carried out in January 2016. The overall output of the training programme over the next two years is not only to have assessors trained but also to qualify and register them in the accordance with the ILAC/IAF requirements for international recognition.

SADCAS peer evaluation for international recognition

In May-June 2015, SADCAS underwent a peer evaluation on the Testing Laboratory Accreditation Programme (TLAP) and Calibration Laboratory Accreditation Programme (CLAP). The evaluation team confirmed that the overall system of SADCAS meets African Accreditation Cooperation (AFRAC) and International Laboratory Accreditation Cooperation (ILAC) requirements. In particular the team highlighted that SADCAS operates its TLAP and CLAP substantially in accordance with the requirements of ISO/IEC 17011:2004 and IAF/ILAC-A5:11/2013. Laboratories accredited by SADCAS have been assessed against and found to comply with the requirements of ISO/IEC 17025: 2005. SADCAS adopts and substantially implements the applicable AFRAC and ILAC policies and guidelines. The team further noted that the full time SADCAS staff is skilled and technically qualified for the functions they perform, and that the organization has a satisfactory foundation of accreditation experience. SADCAS has access to a sufficient number of well qualified, experienced and competent assessors and experts and that SADCAS has a well-established accreditation process which is applied consistently to the accreditation of its testing and calibration laboratories.

The team submitted a recommendation to the AFRAC MRA Committee and the ILAC AMC in October 2015. SADCAS achieved signatory status of its Testing and Calibration Laboratories Accreditation Programs in the AFRAC MRA as decided by the AFRAC MRA Council on 8 October 2015. The ILAC decision will be made on 4 November 2015.

Training of conformity assessments bodies in the mining sector

The effort to train testing laboratories management and staff on ISO/IEC 17025, the appropriate standard for testing laboratories, from both the private and public sector covering exploration, research and quality control in the mining and mineral processing sector in order to prepare them for accreditation is ongoing. This programme is expected to contribute to the strengthening of industrial capacities in the mining and minerals processing sector and enhance the competitiveness and integration into the world markets. The training is being conducted by SADCAS with funding via the SADC PTB Implementation Agreement.

Operationalization of the SADC Technical Barriers to Trade Stakeholders Committee

The SADC Technical Barriers to Trade Stakeholders Committee (SADCTBTSC), an arm of the SADC SQAM Programme on private sector engagement, held a workshop in 26-27 August 2015. A work plan for the next year was developed. The work plan among others includes; continued awareness raising efforts for stakeholders, technical assistance for SMEs to obtain product and system certification, technical assistance with training on labelling and packaging and Good Manufacturing Practice.

Stakeholders also requested for further roll out of the conformity assessment toolkit which had been developed by the SADC Cooperation on Accreditation (SADCA) and released in Kinshasa, DRC, in March 2015. The toolkit was developed to assist new conformity assessment bodies (CAB’s) to understand what is required to prepare for accreditation from an accreditation body. The toolkit explains the terminology that is used and describes the whole accreditation process. It also gives tips on how to prepare a management system.

Identification and harmonization of technical regulations hindering trade

On harmonization of technical regulations hindering trade, data gathering to identify technical regulations (TR) that are hindering trade and require harmonization. The questionnaire was administered at national level by national experts. A consolidated report from four Member States was considered on the 3-4 August 2015 during the meeting of the SADCTRLC workshop. The report identifies a total of fifteen (15) technical regulations that require harmonisation. This includes among others, biosafety regulations, second hand car regulations, importation of medicine, Standard Import Inspection Regulation, pre-packaged labelling regulations and Kimberly Process Regulations. While this list is not conclusive, texts of this regulations will be analysed further to determine their level of hindrance.

In order to guide Member States in the development of technical regulations by observing Good Regulatory Practice, Risk and Impact Assessment Guidelines have been developed. The guidelines will assist regulators and legislators in taking practical evidence based decisions regarding the need for introducing, amending or withdrawing technical regulations governing the import, manufacture and sale of products. Member States representatives will be trained on these guidelines in November 2015.

Development and implementation of an e-marking scheme for regulated pre-packed products in the SADC region

SADC Cooperation in Legal Metrology will be developing and implementing a legal metrology e-marking scheme for pre-packed products originating from any country in the SADC region, mutually recognized in all Member States, for ease of regulation, consumer protection and reduction of Technical Barriers to Trade (TBTs). The initial beneficiary of the project will be the Namibia Standards Institute (NSI). Key problems to be addressed include; capacity building of the LMA, Awareness and capacity building of industry role players, Gazetting of SADCMEL documents as legal metrology technical regulations for Namibia, development / adoption and implementation of Namibian Standard on e-marking, Inspections and auditing of packers and Accreditation by SADCAS of the NSI’s inspection services. The pilot phase of this effort covers only Namibia and the roll out to other Member States will follow once the pilot phase is completed.

The SADC region has a fairly developed legal metrology infrastructure, supported by Legal Metrology Authorities (LMAs), significantly supported by Governments. The responsibilities of the LMAs, among others, are to regulate pre-packed goods offered for sale. The SADC Cooperation in Legal Metrology (SADCMEL) has developed harmonised documents (SADCMEL documents 1 and SADCMEL Document 4) for the regulation of the labelling and permissible tolerances of pre-packed goods. The level of implementation of these harmonised documents has been varied across the region.

In spite of existing legal metrology harmonised documents whose implementation is meant to eliminate Technical Barriers to Trade (TBTs), prepacked products are still found to be noncompliant as they are being traded across the borders, prompting the responsible LMAs to ‘lock out’ such products. Those products that may comply to the harmonised SADCMEL documents, that are not easily identifiable as such, are subjected to unnecessary inspections by the recipient LMA, thereby posing as a technical barrier to trade, and hindrance to trade facilitation.

The majority of SADC Member States do not have the capacity to develop and implement a credible scheme that will ensure that, if implemented properly, products that comply with legal metrology legislation are easily identified and allowed entry easy into the marketplace of another economy. The National Regulator for Compulsory Specifications (NRCS) of South Africa is the only legal metrology authority in SADC that is implementing a successful e-marking scheme based on compliance with a South African Standard (SANS 1841). Products originating from South Africa easily find their way into the SADC regional marketplace.

Coordinating the harmonization of standards, measurement systems and conformity assessment procedures, for harmonization of technical regulations

Botswana, Mauritius, Namibia, Seychelles, Zambia and Zimbabwe have their facilities accredited under the scopes of Temperature and Mass. These facilities are being assisted in profiling their Calibration and Measurement Capabilities (CMCs) to the ultimate submission to the Key Comparison database (KCDB). A training workshop was held to train staff from these National Metrology Institutes (NMIs) in the preparation of Calibration and Measurement Capability (CMC) submissions, in the fields of Mass and Temperature, for publication in the BIPM Key Comparison Database (KCDB).

The International Committee for Weights and Measures Mutual Recognition Arrangement (CIPM MRA) is the framework through which National Metrology Institutes (NMIs) demonstrate the international equivalence of their measurement standards and the calibration and measurement certificates they issue. The outcomes of the Arrangement are the internationally recognized (peer-reviewed and approved) Calibration and Measurement Capabilities (CMCs) of the participating institutes. Approved CMCs and supporting technical data are publicly available from the CIPM MRA database (the KCDB).

Joint UNIDO-SADC Expert Group Meeting on “Quality infrastructure projects and initiatives in SADC: An outlook for cooperation”

In order to identify areas of cooperation and coordination and to learn from best practices, a joint UNIDO-SADC facilitated workshop on Quality Infrastructure projects and initiatives in the SADC region was organised in Gaborone, Botswana on 28 to 29 April 2015, Gaborone, Botswana. The workshop was attended by project beneficiary representatives from SADC Member States, representatives of International Development Partners and project executing agencies. Twenty two (22) delegates attended the meeting representing the SADC Member States, the SADC Secretariat, SADCAS, PTB, SATH and UNIDO. Representatives from the EU-funded ACP-TBT project were unable to attend due to prior engagements. However, information pertaining to current projects in this latter project was made available. Following a series of presentations made on the objectives and progress of each of the projects/programmes pertaining to quality infrastructure in SADC, gaps were identified and possible solutions suggested for the current projects on the development of Quality Infrastructure.

This is summarized in the table below and These possible solutions will be used to feed in to upcoming programmes.

Table 1: Gaps identified and possible solutions

| Identified Gaps | Possible Solutions |

| Accreditation | |

|

The importance of SADCAS and its services needs to be emphasized in Member States |

Optimization of accreditation services available |

|

Promote SADCAS as a cost effective, viable multi-economy solution to the region’s accreditation needs |

|

|

There is need for SADC Member States to support SADCAS |

|

|

Awareness Raising |

|

|

Consumer and policy makers education is still lacking |

Consumer education should be included in awareness creation activities |

|

Support projects must emphasize on consumer awareness |

|

|

Targeted awareness for policy makers also required |

|

| Capacity building | |

|

Lack of national Quality Infrastructure Experts at national level |

Organise exchange programmes or working visits to other National Standards and QI institutions to share experience and assist in building each other’s capacity in the region |

| Leverage partnerships for training | |

|

Make better use of regional and local expertise and experiences in the region for project implementation |

|

| Conformity Assessment Bodies (CABs) | |

| CABs still need to be assisted with readiness for accreditation |

Support the operationalization of the Regional and National Laboratory Associations |

| Accreditation of CABs is a priority and needs to be advanced |

Coaching of CABs in the key development sectors as identified in the SADC Industrialization Strategy and Roadmap. There is need for capacity building of Inspection Services |

| Coordination and Governance | |

| No project design without participation of beneficiaries |

Projects must be better coordinated for optimal utilization of limited resources |

|

Technical Assistance projects must be designed to meet beneficiary needs and not technical partner dictates |

|

|

There should be consultation with regional level project implementers prior to finalization of national level project plans |

|

| Align national projects to regional agenda | |

| Duplication of efforts exists in some areas |

SADC Secretariat should take the lead in coordination efforts. An activity matrix should be developed and managed by SADC Secretariat, e.g. put on the SADC Website |

|

Develop mechanisms to ensure avoidance of duplication |

|

|

Cooperation in Monitoring and evaluation using common set of indicators |

|

|

Projects must take into account existing structures and promote and strengthen them, e.g. SADCAS |

|

|

Align current and future projects to the SADC Industrialization Strategy and Roadmap |

|

|

Difference in development of Quality Infrastructure in Member states should indicate to development partners where to focus their support |

|

| Weak continuity of national projects |

UNIDO to consider how Member States without QI projects/programmes can be assisted |

|

QI is a very big area, focus interventions on limited aspects so as to achieve better results |

|

|

Mechanisms to ensure continuity and sustainability of projects and programmes |

|

| Information Sharing Platform | |

| No formal mechanism in place for information sharing about project activities taking place in the region |

Continue to organize information sharing platforms such as this one in a more sustainable manner: e.g. reports can be presented at SADC SQAM structures annual meetings |

| Common challenges in the implementation of Quality Infrastructure instruments |

UNIDO should give direct feedback to National Standards Bodies on key challenges faced during project implementation |

|

Resolutions made during annual SQAM meetings not made available to current project coordinators |

The national TBTEG representative to be encouraged to share this information with executing agencies |

| Private Sector Engagement | |

| Stakeholder engagement and consultation needs to be emphasized |

Project design stage must take on board all stakeholders including the private sector |

| More direct assistance to the private sector | |

|

Develop a harmonized approach to private sector engagement |

|

|

Harmonization of curriculum development on QI and QA |

|

|

Direct assistance towards private sector institutions for quicker results |

|

|

QI development currently does not speak to value chains in priority sectors |

Link projects to private sector needs and value chains |

| More structured assistance to SME needs | |

|

SME must be assisted with product development in order to produce high quality |

|

|

Support of development of QI must go in parallel with support to enterprises and consumer s to utilize the QI Services |

|

| Standardization | |

| Private standards continue to create challenges for producers | Deal with the issue of private standards |

| There is a disconnect between QI institutions and Regulatory Agencies which needs to be bridged |

Solicit support for harmonization of Technical regulations |

|

Develop mechanisms to bridge the gap between QI and regulatory agencies |

|

|

Guidelines for Quality Policy development in the region |

|

| SADC Annual Quality Awards | |

| Limited of participation in SADC Annual Quality Awards |

Support for national and regional quality award competitions |

|

Member States to consider including National Quality Awards competitions as part of their project outputs |

|

|

Involve the Private sector in running National Quality Awards competitions |

|

|

Include a category specifically supportive of women in business in the national and regional quality awards |

|

| Technical Regulations | |

| Lack of support for quality infrastructure related to the development |

In addition to the current scope of projects, propose new scope to include administration and enforcement of technical regulations |

Related News

tralac’s Daily News selection

The selection: Monday, 1 February 2016

Today, in Gaborone: Botswana's 2016 Budget Speech. Twitter updates: @BWGovernment

Today, in Addis: the US-Africa Business Summit. Twitter updates: #AfricaBizSummit

Featured quote from the AU Summit: ‘Africa must not remain a continent in transition’, Macky Sall, Senegal's President & Chair NEPAD orientation committee

NEPAD Heads of State and Government meeting: input by AfDB's President Akinwumi Adesina, Zimbabwe’s President Mugabe

North-South Corridor: update by President Zuma (SABC)

‘This year we intend to undertake the following, with particular reference to the North-South corridor and international financing investment conference where we will open up the North-South corridor, fast tracked projects for investment and take off. A North-South corridor road show will be led by heads of state and ministers. A head of state gathering of the eight North-South corridors states will finalise the North-South corridor operational mechanisms.’

Note: the full set of outcomes from the Summit can be expected in about a week.

CFTA: Experts to review draft free trade agreement (UNECA)

The meeting (2-3 February, Abidjan) is expected to generate: a proposed outline of the continental free trade agreement, a detailed plan and timeline for the development of a draft agreement, terms of reference for the preparation of sections of a draft agreement and an agreed division of responsibilities for preparing sections of a draft agreement.

Political economy analyses of the African Union and regional economic communities in Africa (ECDPM)

From July 2014 until December 2015, ECDPM and theIDLgroup partnered to produce a study on the drivers and obstacles to regional cooperation and integration in Africa on behalf of the Swedish Embassy in Nairobi. The final report and the AU and the five REC case studies are now available for download. Key findings: The findings of the studies are organised according to ten key statements, discussed in greater detail in the remainder of this synthesis report. These statements - and some of the illustrative findings - are as follows:

EABC calls for changes in regional NTBs Bill (The East African)

The regional business community has criticised the EAC Elimination of Non-Tariff Barriers to Trade Bill 2015, saying it needs extensive changes in order to be effective. The East African Business Council has pointed out that elimination of NTBs is strictly dependent on the political will of the concerned parties, with no consequence for non-elimination and no restitution for aggrieved parties. To address this, EABC trade economist Adrian Njau proposes that the NTBs Act be taken back to the East African Legislative Assembly for amendment. Mr Njau argues that the Bill should provide for an alternative dispute resolution mechanism, arbitration by the trade remedies committee and the ability to petition the East African Court of Justice.

Updates from the RECs:

IGAD Council of Ministers: communique

Ministerial Meeting of the Peace and Security Framework on the DRC and the Great Lakes Region: communique

SADC: Regional agro-processing stakeholders training in SPS and food safety standards

Southern African Development Community Accreditation Services: Pretoria training session

A reminder, from @rsezibera: the EAC continues to invite comments on its 2050 vision document

Conference on Small Middle-Income Countries in Sub-Saharan Africa: statement by Min Zhu, Governor Linah Mohohlo

Participants concluded that...: 'In particular, countries should focus on investment projects that generate wide benefits to other sectors of the economy in priority areas (e.g., energy infrastructure) and rationalizing regulations that hinder the development of the private sector, while adopting a “smart” growth strategy that could take advantage of and/or adequately address global megatrends in technology, climate change, and demographics.' [Note: The keynote presentation by Min Zhu, IMF Deputy Managing Director, has a range of interesting graphics for the 7 focus countries. Other conference presentations can be downloaded here]

Powering Africa Summit (USAID)

The Power Africa Roadmap outlines how it will add 30,000 MW by maximizing value from existing transactions, advancing new opportunities for deal flow, and increasing the efficiency of existing generation. It also highlights how Power Africa will add 60 million connections by scaling up grid roll-out programs and intensifying its Beyond the Grid efforts. Also launched, the Power Africa Tracking Tool (PATT) allows for easy, real-time tracking of transactions across the continent. The PATT provides previously unavailable data that will increase transparency and drive the competitiveness of African markets. [Elumelu urges US Congress to pass the Electrify Africa Act (Naija247)]

Africa on the threshold of connected future – Kagame (New Times)

President Paul Kagame has said that the African continent is in the process of having a connected future with the ongoing efforts of pooling efforts and resources. The President made the remarks, yesterday, while chairing the third Smart Africa board meeting on the sidelines of the African Union summit in Addis Ababa, Ethiopia. The meeting was attended by Presidents Macky Sall of Senegal, Ibrahim Boubakar Keita of Mali, Uhuru Kenyatta of Kenya, Ali Bongo Ondimba of Gabon, Rock Marc Kabore of Burkina Faso and Edward Ssekandi, vice-president of Uganda.

South Africa: trade statistics for December 2015 (SARS)

The R8.22 billion surplus is a 4.4% increase on the surplus recorded in December 2014 of R7.88bn. Exports of R88.77bn are 0.3% more than the exports recorded in December 2014 of R88.47bn. Imports of R80.55bn are 0.1% less than the imports recorded in December 2014 of R80.59bn. The cumulative deficit for 2015 of R48.63bn is 40.9% less than the deficit for the comparable period in 2014 of R82.27bn. The month of November 2015 trade balance surplus was revised downwards by R1.09bn from the previous month’s preliminary surplus of R1.77bn to a revised surplus of R0.68 billion.Africa trade surplus is R13 810 million – a 17.3% decrease. [Surprise trade surplus buoys the rand (IOL)]

Dianna Games: 'New Abuja route signals Nigeria is still an important partner' (Business Day)

SAA flies seven times a week to Lagos and the three remaining slots are being used for the Abuja flights. The new route forms part of SAA’s turnaround strategy, and there are early signs of success. The first return flight from Abuja to Johannesburg last week had a load factor of 67%. Airline executives believe the route will be profitable in a reasonably short time. There are many reasons why.

Lesotho: IMF concludes 2015 Article IV Consultation (IMF)

The rebound in SACU revenues contributed to Lesotho’s recovery from a severe fiscal crisis and supported the rebuilding of fiscal and external buffers, with official international reserves reaching 6.3 months of imports by end-March 2015. However, SACU revenues have fallen once again. After slipping to R6.6bn (about 26% of GDP) this year, Lesotho’s allocation will drop sharply to R4.5bn (about 16% of GDP) in 2016/17, with much of this decline expected to be long-lasting.

Botswana: Trade portal to improve cross-border trade (Daily News)

The trade portal also has an objective of making it easier for traders and investors to understand, navigate and comply with regulatory requirements associated with exporting and importing. This web-based tool was intended to helping Botswana to fully comply with its international obligations at the World Trade Organisation level.

Zimbabwe: Cross-border traders find new ways to evade duty (The Zimbabwe Independent)

A loquacious middle-aged woman immediately assumed the role of group leader and started collecting R20 or US$2 from every passenger on the bus before she handed it to the conductor who in turn gave the money to the Zimra officials before the bus was allowed to proceed. Such has become the norm on Zimbabwe’s highways as thousands of cross-border traders under-declare duty daily, prejudicing Treasury billions of dollars in potential revenues every year. Tax evasion by cross boarder traders heightened after government cut travelers rebate from US$300 to US$200 late 2015.

Zimbabwe, SA sign transport infrastructure MoU (The Chronicle)

The country’s transport sector is poised for major pickings after Government signed a Memorandum of Understanding for infrastructure development with South Africa on Friday to ease movement of traffic between the two countries. The MoU is a bilateral agreement on transport and development related matters which seeks make movement easier for people of the two countries by decongesting Beitbridge Border Post. Dr Gumbo said the MoU would allow the two countries to share expertise, infrastructure development and services as well as promote investments, industry and trade co-operation on equitable terms. [Govt installs CCTVs at Beitbridge Border Post (The Herald)]

Mauritius leads investment flows into Zimbabwe (The Herald)

According to the latest statistics (2009-2015) from the Zimbabwe Investment Authority, Mauritius is the largest source of investment flows accounting for $4,56bn while the British Virgin Islands is on sixth at $760,54m. China is the second largest source country at $2,81bn with the most significant amount of $1,09bn coming through in 2011. Other top source countries include South Africa at $1,54bn, US at $1,6bn, and Nigeria at $1,45bn. The bulk of the Nigerian investment were approved in 2015 for the Dangote Group whose strategist was in the country last week.

Angola chairs economic committee of African group in Brazil (Angola Press)

The Economic Committee of the African Ambassadors Group in Brazil, chaired by Angola, represented by ambassador Nelson Cosme, expressed its satisfaction at the mechanisms created by the Brazilian Government, through the APIEX Services ((Agency for Investment and Export Promotion) and BNDES (National Bank for Economic and Social Development), to facilitate trade and investment with African countries.

KRA widens port probe to stem tax leakage (Daily Nation)

Kenya Revenue Authority has launched investigations into operations of Container Freight Stations to stem tax evasion. KRA Commissioner General John Njiraini stated that the ongoing investigations are part of a wider campaign to enforce customs regulations and seal revenue leakages. The announcement comes after KRA confiscated 40 containers of contraband goods at Compact Freight Systems in Miritini Mombasa, last week.

Results-based budgeting comes to Zimbabwe (World Bank)

Nigeria seeks $3.5bn in loans from World Bank and AfDB (Bloomberg)

Malaysia’s long race to competitiveness (World Bank Blogs)

'World SME Forum': a global platform to support SME development, bridging Turkey B20 and China B20 (World Bank Blogs)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

Conference on Small Middle-Income Countries in Sub-Saharan Africa: Joint Statement

The Governor of the Bank of Botswana, Ms. Linah Mohohlo, and the Deputy Managing Director of the International Monetary Fund, Mr. Min Zhu, hosted on 29 January 2016 in Gaborone, Botswana, a regional conference entitled “Small Middle-Income Countries in Sub-Saharan Africa – Raising the Bar”.[1]

Delegates included senior officials from a number of countries representatives of the private sector, academia, the Executive Board of the IMF and IMF staff. At the end of the conference, the following statement was issued:

“We had a very productive set of discussions on the economic outlook and policy challenges facing small middle-income countries (SMICs) in sub-Saharan Africa. This group of countries has made significant progress in terms of maintaining macroeconomic stability and sustaining high growth over the past two decades. However, a number of challenges have recently emerged and, beyond the importance of maintaining their hard earned gains in terms of economic stability, there is scope to rethink their growth strategies and move forward with bold complementary reforms that could facilitate their transition to high-income status.

“For countries that depend heavily on commodity exports, the near-term environment has deteriorated as both global demand and prices have declined. And while some countries have previously built savings that can help them cushion the slowdown, other countries have seen their fiscal positions deteriorate rapidly at a time when external financing conditions have tightened. Notably, the slowdown of the South African economy could also adversely affect the countries in the region.

“Participants concluded that, beyond following prudent policies that will help preserve economic stability (a precondition for growth), SMICs should not lose sight of the need to build resilience, adopt more inclusive policies, and foster economic diversification. To this end, reforms should be comprehensive, yet carefully prioritized to unlock these countries’ productivity growth. In particular, countries should focus on investment projects that generate wide benefits to other sectors of the economy in priority areas (e.g., energy infrastructure) and rationalizing regulations that hinder the development of the private sector, while adopting a “smart” growth strategy that could take advantage of and/or adequately address global megatrends in technology, climate change, and demographics.

“Participants also agreed that, for countries to succeed, growth will have to be inclusive in terms of job creation and, in a number of cases, ensure policies that protect the most vulnerable segments of society. This will likely require courageous reforms to reduce skills mismatches in the labor force through cost-effective training programs, adopting reforms that can lower the cost of doing business and facilitate the hiring of highly-skilled workers, and enhancing the composition and efficiency of government spending.”

Ms. Mohohlo noted that: “This conference has touched on various policy challenges that SMICs have in common – on the one hand ensuring economic stability and sustaining growth while promoting inclusion and social equity, and on the other hand recalibrating the growth strategy to facilitate the transition to high-income status. We had an excellent opportunity to discuss the lessons and prospects of policies being implemented in several SMICs as well as on other countries that successfully tackled their developmental challenges and have now well-functioning and developed markets. The wide forum in which the conference took place and the related peer-to-peer learning strengthened the dialogue among SMICs and offered novel views on how to tackle these countries’ challenges.”

In closing, Mr. Zhu said: “The IMF remains closely engaged with SMICs in Sub-Saharan Africa through policy dialogue, technical assistance, and analytical work. The conference has also served as the launch of the book Africa on the Move: Unlocking the Potential of Small-Middle Income Countries, authored by IMF staff in collaboration with officials from SMICs in the region. Looking ahead, our teams will continue to collaborate closely with country authorities as they strengthen the analytical underpinnings of their policies and rethink their growth strategies. We look forward to continuing this dialogue at the time of the IMF Spring Meetings in April.”

1 The Small Middle-Income Countries in Sub-Saharan Africa comprise Botswana, Cabo Verde, Lesotho, Mauritius, Namibia, Seychelles and Swaziland.

Small Middle Income Countries: Raising the Bar

Remarks by the Deputy Managing Director Min Zhu, International Monetary Fund

On behalf of the International Monetary Fund, I would like to welcome you all to the 2016 High Level Conference for Small Middle Income Countries in sub-Saharan African, Raising the Bar.

This conference also coincides with the launch of the book “Africa on the move: Unlocking the potential of small middle-income states,” the result of a collaboration between IMF staff and officials from member countries.

I wish to express my gratitude to the Government of Botswana for its warm hospitality and to the Bank of Botswana for co-hosting this conference. I am looking forward to interesting discussions from today’s panelists and all of you on how this group of middle-income countries can overcome current challenges and move to the next stage of development.

Today I would like to talk about three issues:

-

The changing global economic landscape

-

The successes and challenges for small middle-income countries

-

How countries could rethink their growth strategies, and the possible policies that could help them graduate to the next stage of development and avoid the so-called middle-income trap.

Together, these issues form the nucleus that will shape how small middle-income countries graduate to their next level of development. Let me start with the global picture.

The changing global economic landscape

The global economic crisis left us with a bigger scar than initially anticipated that we are still struggling to overcome: lower output and potential output, investment, and trade. Going forward, potential global growth has also moderated, including in emerging markets.

In addition, commodity prices have declined in what could be a protracted period of depressed prices. This puts pressure on those countries whose exports are mainly commodities, worsening their balance of payments and fiscal positions. The effect of the decline in export prices on the terms of trade has been at least partly compensated by lower fuel import prices.

All this is taking place as U.S. interest rates begin to rise and financial markets are experiencing heightened volatility. The increase in financing costs and volatility raises the issue of fiscal sustainability. Setbacks in domestic economic management can deteriorate both access to and pricing of external funding, yielding a potentially significant adverse shock to fiscal and external positions, and to debt dynamics. This suggests that some of the factors that supported high growth in the region – strong external demand and high commodity prices, coupled with low cost access to financing – are no longer as conducive.

Let me now turn to three megatrends that affect us all: climate change, technology, and demographics.

Climate change, while a global phenomenon, will affect countries in a variety of ways. Countries in sub-Saharan Africa are among the most vulnerable to climate change. It increases the uncertainty associated with natural disasters as the incidence of droughts, floods and cyclones is likely to increase. Mauritius is among the most vulnerable countries in the world to cyclones. All islands are vulnerable to rising sea levels. Swaziland is vulnerable to droughts. The poor are most at risk from climate change, including disruptions to the supply of food. This highlights the importance of economic resilience and measures to fight against the impact of climate change.

Innovations and changes in technology impact all aspects of our lives. Countries will have to change the way they have traditionally done things. This forces them to integrate differently into the “global village”. The impact will be both creative and destructive. For example, financial technology will affect payments, deposits and lending, financial markets, investment management, and capital raising and insurance.

Demographics potentially are on Africa’s side. While the rest of the world is aging, Sub-Saharan Africa could become the main source of growth for the global labor force. This will provide both challenges and opportunities. Sub-Saharan Africa’s population, slightly over 800 million in 2010, is projected to more than quadruple to 3.7 billion by 2100. The region is expected to account for most of the projected 2 billion increase in the global labor force this century. This requires special emphasis on building human capital and support for job creation to mitigate the social risks associated with high unemployment. By putting in place many of the reforms we are discussing today, countries can be well placed to benefit from a “demographic dividend.”

Small middle-income countries have a much narrower window of opportunity since they are at a somewhat more advanced stage of their demographic and income transitions. Mauritius and the Seychelles are even facing an aging population and need to prepare for the associated growth and fiscal challenges. If countries are able to harness the demographic dividend, small middle-income countries will have new markets next door, with trade reducing the constraints associated with smallness and location.

Successes and challenges

Small middle-income countries represent a successful group that have experienced solid growth over the past 20 years and sustained increases in per capita GDP. Their incomes have converged to advanced and emerging economy levels, but have not progressed as quickly as desired, reflecting a moderation of growth in some cases.

Growth has moderated in a few countries in 2014-15; some of it can be attributed to global conditions, but domestic constraints may also be playing a role.

We see the following main challenges countries face at home: how to diversify economies; job creation; infrastructure; developing the human resources necessary for economies to grow; and making growth inclusive.

First, countries need to accelerate their progress in diversifying exports and put in place policies to ensure that growth is broad-based. There inevitably are more risks when you have all your eggs in one basket. An economy is more resilient if the growth comes from a variety of economic drivers and the quality of growth is higher. In small middle-income countries, the service sectors have grown fast, but the main economic driver in most countries has been government expansion.

The second key challenge is job creation. Unemployment is high in several countries and the recent rise in youth unemployment is a big concern. There is also the issue of under-employment arising from large informal sectors with low productivity levels.

What are the causes of unemployment? In some cases they are structural and are caused by a lack of diversification and a country’s inability to move up the global value chain. Also a mismatch of skills – between those available and those the economy needs – can prevail, which is often caused by a lack of education and job training.

The difficulties in dealing with the problem and the political and social pressures it creates often lead to short-term solutions that are unsustainable or undesirable in the longer term. Unemployment exacerbates pressure on governments as an “employer of last resort.” This inflates the public sector wage bill and crowds out other priority spending.

The third challenge is the infrastructure gap, which is a major issue throughout Sub-Saharan Africa. Infrastructure gaps affect countries’ connections to the rest of the world, and limits their competitiveness. Countries should add infrastructure, but also make better use of what is available. There is also significant scope to improve the efficiency of investment, as higher levels of spending do not necessarily translate into improved public infrastructure. The slowdown in public investment in most small middle-income countries contributes to stagnant or declining capital stocks in several cases.

With many countries facing binding budget constraints and significant investment needs, the importance of increasing the efficiency of existing infrastructure is more important than ever. This requires well-prioritized projects, with sound cost-benefit analysis and carefully weighted financing options, including public-private partnerships.

Fourth, while various dimensions of human development indices have shown improvements over the years, challenges remain in many of your countries. Life expectancy has been converging to advanced and emerging market levels in several countries, thanks to better health care, but further progress is needed in others. While primary education is near 100 percent in most countries, in most cases there is room for progress in secondary and university education.

We see similar patterns when we look at the evolution of other human development indicators. So there is plenty of room left to build human capital, especially considering its importance in helping to deal with high levels of youth unemployment in many countries.

Fifth is inclusive growth, which is one of the key challenges many nations face in the 21st century. While poverty rates have fallen over time among small middle-income countries in Sub-Saharan Africa, efforts are still needed to ensure convergence in this area. Also, inequality remains unacceptably high in several countries. If unchanged, this will lead to social pressures and hurt growth.

Policies for growth and development: the next level

I now want to turn to how countries can best deal with all these domestic and external challenges, adapt to the new global environment and move to the next level of development.

Reform needs vary according to the stage of economic development: what got you from low-income to middle-income will not necessarily take you to the next level.

Countries that have graduated from middle-income status to advanced economy status have some features in common:

-

More effective governments, which is not necessarily positively correlated with government size

-

Private sector participation, facilitated by the right policies, including investor protection and adequate credit availability

-

More inclusive growth that leads to lower poverty and unemployment.

The earlier growth model for small middle-income countries based on factor accumulation that allowed them to graduate from low- to middle-income status may no longer be well suited, especially considering the megatrends I mentioned earlier. To deal with these headwinds and recapture the earlier growth momentum over the medium-term will require governments to rethink the possible sources of growth, along with new policies. Crucially, countries need to implement previously delayed structural reforms to enhance their competitiveness and resilience.

Reforms

In many cases, the reform priorities are country-specific and consistent with their stage of development. We have identified five areas of common interest: policies to reduce government debt and deficits; private sector development; inclusive growth; job creation; and strengthening pubic financial management.

Given multiple reform needs, countries need to prioritize and sequence reforms to maximize pay-offs. The pace of reform appears to matter for productivity growth as much as the type of reform. Similarly, there appear to be benefits in implementing certain reforms simultaneously or in “waves.” For instance, there are synergies between labor market and product market reforms.

Also, governments need to diversify growth from government-led to private sector-led. This requires addressing the high cost of doing business and creating an enabling environment for the private sector.

I want to leave you with the sense that progress and advancement are within reach. This will require policymakers to adapt and change to new circumstances while also sticking to their goals. And it will be a lot of work.

In the face of a changing and uncertain world, small middle-income countries have to carve out their own path to take their development to the next level, and the IMF will be there to assist our member countries achieve this goal.

Thank you.

Related News

Political economy analyses of the African Union and regional economic communities in Africa

Why a political economy study of regional organisations in Africa?

Regional cooperation and regional integration are deemed vital to tackle development challenges that cannot be solved at the national level. In Africa, many such challenges affect poor people’s lives in areas ranging from human security and mobility to rural livelihoods, trade, infrastructure, food security, environment and climate change.

Regional cooperation and integration have long been high on the agenda of African countries, regions and regional organisations to address these issues. Burgeoning regional policies, strategies and protocols have been matched by widening ambitions and mandates in most regional organisations, often supported by donor-financed expansions in budgets, staff and programmes.

Yet policy-makers, member state representatives and non-state actors frequently express frustration with the gap between commitments and what takes place on the ground. The Chairperson of the African Union Commission (AUC), Nkosazana Zuma, herself has said: “I don’t think Africa is short of policies. We have to implement, that is where the problem is”.

The challenge is to understand the underlying political and economic factors that really drive and hinder progress on regional integration.

Synthesis Report

This report synthesises political economy studies on six African regional organisations. The studies cover the following sectors or policy areas for each regional organisation:

- AU – Peace and security, infrastructure, food security, climate change, gender

- COMESA – Trade, energy, gender

- EAC – Trade, transport and infrastructure, gender

- ECOWAS – Peace and security, food security, gender

- IGAD – Peace and security, transport and infrastructure, trade

- SADC – Gender, industrialisation, energy, conservation

Each study answers the following related questions: What are the actors and factors affecting the policy agenda of the regional organisation? And what are the drivers and blockers of implementation?

The studies use a ‘five-lens’ approach to systematise information on: the role of structural or foundational factors; the role of institutional factors, including both formal and informal ‘rules of the game’; the power and interests of different ‘actors’ and groups operating within these institutions; the sectoral characteristics that affect political economy considerations; and external factors and influences, not least donor finance.

The approach aims to uncover why the dynamics around each of the regional organisations unfold as they do, rather than judging how they ought to be according to ‘best practice’ or model trajectories. By systematically examining the different actors and factors that affect the way these six regional organisations work, the studies aim to increase understanding of what shapes incentives and therefore what is technically and politically feasible in a particular policy area and regional context.

Ten key findings

The findings of the studies are organised according to ten key statements, discussed in greater detail in the synthesis report. These statements – and some of the illustrative findings – are as follows:

1. Structural and foundational factors continue to shape the environment in which African regional organisations set and implement their agendas. Eight out of nineteen COMESA member states are landlocked, creating an underlying need for regional integration, while four of the nineteen are island states. This geographical diversity is a basic challenge to finding a common regional agenda. The emergence of the EAC Northern Corridor countries, dubbed the ‘coalition of the willing’, largely reflects Rwandan and Ugandan political interest in overcoming their landlockedness, that aligns with Kenyan business ambitions. Physical factors also impact on IGAD, with a strong logic for regional cooperation emanating from the common physical challenges of arid and semi-arid lands and three landlocked member states.

But these ‘push factors’ are largely offset by long-running tensions and conflicts stemming from colonial experiences. Their effects are clearly evidenced in all RECs. In West Africa, there is a variety of different administrative, bureaucratic and linguistic traditions resulting in the co-existence of a Francophone and an Anglophone REC with partly overlapping and/or competing mandates, for example in the area of peace and security. Low levels of economic complementarity also hinder greater integration.

2. While regional organisations adopt the institutional forms to foster regional integration, these institutions often do not serve their stated functions. All studies highlight a gap between the multiple institutional forms of regional organisations and the functions they fulfill. In fact, many of the key functions of planning, budgeting, monitoring transparency and accountability are weakly developed and not mutually reinforcing. This leads to inflated policy agendas with limited mechanisms to encourage implementation.

Most regional organisations discussed have planned and prepared protocols for free trade arrangements and customs unions, none of which are functioning as they should on paper, with little cost or sanction for non-implementation. More broadly still, despite complex decision-making organisational forms in most RECs, decisions are driven primarily by summits of Heads of State.

Peace and security in the AU, ECOWAS, and IGAD is an area where regional institutions do seem to fulfill clear functions. Another case is SADC’s contributions to Transfrontier Conservation Areas (TFCAs) in Southern Africa. In both cases there were pressures for performance by powerful stakeholders in member states or – as with TFCAs – by cross-country coalitions around solving problems of common interest.

3. Member states face incentives to signal their support for regional policies and programmes even when implementation is not a domestic priority. There are numerous incentives, logics, and reasons for national leaders to signal their support for regional agendas without necessarily acting on it. One striking case relates to gender, with strong rhetorical support by national leaders at the level of AU and RECs; sometimes backed by donor support that arguably incentivises such signalling rather than action. In practice, the plethora of policy commitments to promoting gender equality have difficulty gaining traction over other national priority areas, particularly given limited costs to noncompliance by member states with regional decisions.

4. Implementation of regional initiatives takes place when in line with key ‘national interests’ as defined by the ruling elites. This may be the most influential of the findings in terms of its impact on other findings. The importance of national interests is part of the explanation for overlapping REC memberships: Kenyan membership of the EAC, COMESA and IGAD (currently) reflects Kenyan economic ambitions for EAC and COMESA, while interest in IGAD is seen to be more around security and dryland related issues.

One corollary of the dominance of national interests is the easier alignment of interests among smaller groups of countries. This is the case for the EAC sub-regional group of EAC Northern Corridor countries. It also emerges by comparing the Eastern Africa Power Pool (EAPP) under COMESA and the Southern African Power Pool (SAPP) under SADC. The importance of national interests partially explains greater progress on peace and security than trade in IGAD, for example. The ECOWAS study highlights the substantial differences in national interests between rice, seen as a key crop for national food sovereignty, and livestock, considered as part of regional value chains.

5. Much of the success or failure of regional processes depends on the ‘national interests’ of regional hegemons. By definition, hegemons are better able to instrumentalise regional dynamics for their own interests, or to block those that undermine their position. Progress in the EAPP as well as in IGAD regional policies are both affected by where Ethiopia sees its interest. This also goes for South Africa’s roles in SADC – as the cases of regional industrialisation and the regional energy market prove – as well as Nigeria’s role in ECOWAS on peace and security.

6. Individual personalities and leadership within regional organisations tend to shape – and can be decisive for – the implementation of regional agendas. Across AU and RECs, decision power lies largely in the hands of Heads of State, implying a concentration of influence in those individuals and in their relations with one another. The transition itself from the Organisation of African Union to the African Union was driven by powerful and visionary presidents working together to establish more effective pan-African institutions. Technical staff or bureaucratic leaders can also be instrumental in strengthening the functions of regional organisations, as was the case with the Southern African Power Pool, or was demonstrated by the AU Commission and the IGAD Secretariat in their trust and partnership building with donors.

7. The diversity of power and interests of non-state actors affects how business and civil society organisations engage at national and regional levels on regional processes. Non-state actors are involved in numerous regional processes. There are, however, but a few examples of effective civil society engagement with regional organisations. The Peace Parks Foundation played a strong brokerage role in launching Transfrontier Conservation Areas and in working with SADC. The SADC Gender Protocol emerged from the eponymous Alliance that lobbied for the rights of informal cross-border female traders. Despite the formal space for non-state actors to engage in policy dialogue with regional organisations, there is limited uptake by the latter, except in sectors such as peace and security where a few specialised non-governmental organisations cooperate in functional ways with regional organisations.

Looking at the private sector, Burkina Faso’s strong performance in implementing the regional CAADP in rice is largely down to the alignment of political concerns about food sovereignty and rice producer interests. Beyond these examples, the interests of civil society and the private sector have been too diverse and their voices little heard in regional policy debates.

8. The interests and incentives associated with regional cooperation on different sector or policy areas (security, infrastructure, energy, gender etc.) differ markedly according to the nature and characteristics of the sector, affecting implementation in these areas. This is particularly apparent in IGAD, ECOWAS and the AU where peace and security have more traction than other policy areas. The analysis suggests that this relates to the strong political appeal to national leaders to prevent or resolve violent conflicts and minimise negative cross-border externalities or spillovers from conflicts. There are visible costs to inaction and to instability for which national leaders may have to pay the price if left unresolved.

Integration around the trade, energy and gender agendas are far more aspirational, with ‘hoped for’ benefits in the future – and less politically salient features for ruling elites to solve immediately. The political economy features of the subsector of rice in ECOWAS are entirely different from those of livestock: in the rice sub-sector political incentives prioritise national level self-sufficiency, while the livestock subsector depends on extensive production chain and mobility of cattle across borders from North to South, creating entirely different political incentives for national and regional stakeholders.

9. The quantity and quality of donor support to regional organisations present opportunities but also challenges in terms of reducing the implementation gap. All regional organisations except ECOWAS depend heavily on donor funding. ECOWAS mobilises a substantial part of its regional budget through a common levy on imported goods. Donors have funded a range of important regional activities, not least those related to peace and security in all regions of Africa. Yet the combination of a strong donor dependency and poorly managed aid raise the risk of donors driving rather than supporting reforms.

Poorly managed and targeted aid is partly to blame for incentivising empty signalling of reforms by regional organisations, agenda inflation, reduced ownership, and missed opportunities to strengthen institutional functions that are pivotal for the governance of regional organisations.

10. Critical junctures such as natural disasters and political and other crises can trigger progress but also block regional organisations and dynamics. The initial relative success of the SAPP can be traced to a fortuitous combination of conditions in the mid-nineties related to drought, post-apartheid dynamics and surplus production by South Africa’s state-owned monopoly producer of electricity. The movement on the ECOWAS regional agriculture policy was triggered by the 2008 food price crisis. The IGAD study highlights the important role the Arab Spring played in changing Egyptian interests, with implications for the EAPP and IGAD.

Implications

One implication of these findings is that the vision of regional integration as a linear path is just that, a vision. This highlights the need for policy-makers to ‘think and work politically’ or ‘do development differently’; to build flexibility and adaptability into reforms and interventions or, in other words, to “plan for sailboats, not trains”.

Related News

Paris Agreement ‘decisive turning point’ on climate change, says new UN senior adviser

Less than two months after 196 parties to the United Nations Framework Convention on Climate Change (UNFCCC) adopted the Paris Agreement, the global community is already seeing signs of it being a decisive turning point, according to a senior UN official dealing with climate issues.

A month and a half since 196 parties to the United Nations Framework Convention on Climate Change (UNFCCC) adopted the Paris Agreement, the global community is already seeing signs of it being a decisive turning point, according to a senior UN official dealing with climate issues.

“Much has been happening since Paris – the World Meteorological Organization (WMO) confirmed that 2015 was the hottest year on record, not just by a little but by a lot,” Janos Pasztor, who was today appointed as Senior Adviser to the Secretary-General on Climate Change, told reporters at a briefing in New York.

For the past year, Mr. Pasztor had been leading the UN's climate change efforts as Assistant Secretary-General on Climate Change, working towards last December's 21st United Nations climate change conference (COP21).

Recalling that UN Secretary-General Ban Ki-moon has invited world leaders to a signing ceremony on 22 April – which coincides with International Mother Earth Day – the climate advisor noted that it will be the first day the Agreement is open for formal signatures.

He said Mr. Ban is urging countries to quickly ratify the agreement so it can enter into force as soon as possible, adding that the event will also be an opportunity to discuss efforts to implement national climate plans, known as INDCs, and to generally “maintain the momentum of the action agenda.”

Meanwhile, he underlined the Secretary-General's recent call for a doubling of investments in clean energy by 2020, which he said was greeted “very positively” by many investors.

“The pdf Paris Agreement (505 KB) sent a clear message to markets and investors that it's time to get serious about climate change. We're now seeing evidence that the signal has been received loud and clear,” Mr. Pasztor stressed.

Meanwhile, in a statement issued by the UN Spokesperson's Office, Mr. Ban expressed his deep gratitude for Mr. Pasztor's “dedicated service and leadership” over the past quarter of a century with the world body on the key global challenges of climate change, energy and sustainability.

“In his new role as Senior Adviser to the Secretary-General on Climate Change, Mr. Pasztor will support efforts of the Secretary-General to mobilize world leaders and all sectors of society to implement the landmark Paris Agreement,” the statement indicated.

Bringing the Paris Agreement into Force