Search News Results

SA losing out in Francophone Africa

South African companies are hardly represented in Francophone Africa, despite the significant opportunities present in these countries.

During the Co-invest in Francophone Africa Forum held in Johannesburg this week, Khanyisile Kweyama, Business Unity SA CEO, said infrastructure was the biggest challenge being faced in Francophone Africa.

In the Democratic Republic of Congo, it took days to get equipment to its final destination, Kweyama said. “And language is also a barrier.”

George Sebulela, Black Business Council chair, said there was a limited South African presence in Francophone Africa because of the French dominance in these countries.

“Political stability is also a key challenge in Ivory Coast,” Sebulela added.

The private sector in Francophone Africa was weak, countries were dependent on donors for funding and the cost of doing business in these countries was high, Sebulela said.

There was poor corporate governance and the perception of a high level of corruption. A key issue was the ability to get funding, said Sebulela.

Yunus Hoosen, acting head of investment promotion at the department of trade and industry, said a key issue for Africa was a lack of infrastructure. For instance, to access Francophone African countries, you often needed to fly via France.

“South Africa is a strong investor in sub-Saharan Africa, while France is strong in Francophone Africa,” Hoosen said.

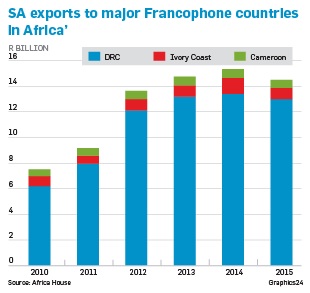

Duncan Bonnett, an Africa House director, said the major countries within Francophone Africa included the Democratic Republic of Congo, Cameroon and Ivory Coast.

All three countries have economies of similar size. The Democratic Republic of Congo’s gross domestic product (GDP) is valued at $41 billion (R615 billion), Ivory Coast’s at $35 billion and Cameroon’s is at $30 billion.

All three countries also have high growth rates. The Ivory Coast is forecast to grow by 11% this year; the Democratic Republic of Congo, Africa’s largest copper producer, is set to expand by 7%; and Cameroon, where MTN has a presence, is expected to grow at 6%.

Last year, the three countries’ total imports were $25 billion.

South Africa is the Democratic Republic of Congo’s largest source of imports at 20%. On the other hand, it makes up only 1% each of Cameroon and the Ivory Coast’s imports.

“Cameroon and Ivory Coast offer excellent opportunities... and are gateways to broader regions,” Bonnett said.

Last year, South Africa exported more than R14 billion of exports to the three countries. In Cameroon, South African wines now feature on hotel menus, Bonnett said.

A key issue raised by South African companies operating in Francophone Africa was logistical.

“But South African companies that have made the effort in these countries are slowly succeeding,” he said.

If a company wanted to make a long-term investment in Francophone Africa, it needed to speak French and understand the nuances of Francophone Africa.

Josue Tandoum Waffo, JM Capital Africa CEO, said there were opportunities for South African companies in Cameroon if they did their homework properly and chose their local partners carefully.

Cameroon’s natural resources include petroleum, bauxite, iron ore, timber, hydropower, fish, rubber, diamonds and gold. Infrastructure was by far the largest strategic opportunity in the country, he said.

In 2014, Standard Bank indicated its intention to expand into Francophone Africa by opening an office in Abidjan. “Save for a few South African companies such as MTN, SAA and Tiger Brands, South Africa is largely absent from central Africa,” Waffo said.

Alassane Ndiaye, Rayon Investments managing partner, said Ivory Coast wanted to grow its economy to $50 billion by 2020 and was projected to grow by between 8% and 10% over the next four years.

Ivory Coast, the world’s largest producer of cocoa beans and cashew nuts, was one of the world’s fastest-growing economies, he added. In 2015, it grew by 8.2%.

The country was also a major player in coffee, and in palm oil production. The government of Ivory Coast would like to increase the processing of local raw materials from 30% to 50% by 2020.

Ivory Coast was forecast to receive $20 billion worth of foreign direct investment over the coming years, Ndiaye said.

“South Africa can be a lot more active in Ivory Coast... South African companies have not ventured into Ivory Coast agriculture at all,” Ndiaye said.

Infrastructure development was a key driver of Ivory Coast’s economy, with massive investments over the past five years, especially in highways, bridges and ports. South African companies, such as AngloGold Ashanti, were exploring for gold in the country.

A key risk for Ivory Coast was that it was a fragile “post conflict” state, Ndiaye said.

“The main country risk is the national security situation, which has improved significantly over the past five years, but there is still sporadic unrest like soldiers’ strikes, road banditry and ethnic clashes over agricultural land ownership,” he added.

Another risk in the country was corruption, Ndiaye said.

Related News

Four lessons from Brexit and EU fallout for East African Community

Now that the immediate turmoil of Britain’s exit vote from the European Union has somewhat subsided, it is a good time to ask what lessons that vote holds for the East African Community. Four stand out.

-

One, a community must be based on values shared by all.

-

Two, a community won’t endure if it is not built on the consent of the people.

-

Three, integration is fragile and it takes but the opportunism of a few leaders in a member state to wreck it.

-

Four, the youth must be given voice in integration; if not, the future – complete with its uncertainties and challenges – will be shaped by those with the least stake in it, the old.

The first, second and fourth are lessons for the Community as a whole and the third, though a lesson for all, is particularly important for Kenya, which has ruined the EAC once before. Let’s flesh out each one of these lessons.

For the most part, the United Kingdom has never been one with core EU values. Rather, the UK prides itself in its exceptionalism and pursues a foreign policy that is defined more by what the country is against rather than what it stands for.

Little wonder then that Anglo-European relations have often been characterised by mutual antipathy. Britain, in the words of its former Prime Minister Harold Macmillan, is “insular” with “very special, very original, habits and traditions.” That insularity contrasts sharply with Europe’s self-conscious cosmopolitanism. And so, even though the UK is Europe’s second largest economy, Europe sees it as a difficult partner.

In economics, this ‘nation of shop-keepers’ – as Napoleon Bonaparte famously called it – is often too pro-market for Europe. In diplomacy, it pivots too often and too strongly towards the US. In Union affairs, it is a miserly penny-pincher and a veto-wielding curmudgeon, constantly complaining and slowing down important aspects of greater European cohesion, by refusing to join the Euro and the Schengen area, for instance.

Many Europeans are not surprised by the UK’s exit vote. The UK has always been deeply eurosceptic. Euro-barometer, a Public Opinion Research Service of the European Commission, has surveyed public opinion in Europe since 1973, asking nationals of member states whether the Union was a good thing; a bad thing or neither a good nor a bad thing.

Just before the Brexit vote, Danish Broadcasting Company DBR summarised forty years of these surveys and concluded that Britain was consistently the most eurosceptic country of all the large European economies.

Kenya’s attitude is insufferable

Many East Africans will recognise Kenya’s stance in Britain’s European “exceptionalism.” Although Kenya is the region’s largest economy – and boasts its most educated population – it is strangely disconnected from the Community.

The intelligentsia in Rwanda, Uganda and Tanzania closely follow Kenyan politics. It is not an interest reciprocated by the Kenyan intelligentsia, which is strangely incurious and embarrassingly ignorant about its neighbours. Yet visitors to Kenya remark on its worldly and globally oriented elite.

The disinterest in fellow community members arises not from an innate provincialism but from a deeper malaise: Kenya is in but not of East Africa. Its regional ambitions are rather modest: a market for its goods and expansion room for its companies. A few Kenyans may even go to school in Uganda, in the main, the movement is the other way. Kenya has nothing to learn from her community neighbours, it is rather a tutor to them.

We have learnt from Brexit that this mindset won’t do. And if we occasionally detect a flash of xenophobia towards Kenya in Tanzania and, to a small extent, in Rwanda, it is because Kenya’s attitude, like that of Britain in the EU, is insufferable.

The Community’s future lies in a convergence of values. That, in turn, depends on deepening cultural exchange and building common standards in education. The EAC has taken baby steps towards aligning professional standards and practices but without more, this is woefully inadequate.

Integration must work for majority

The second lesson from Brexit is that integration must work for the majority of the people or it does not work at all. The British ruling elite misread the public mood, missing out the national feeling on hot button issues like immigration and identity.

In a pre-Brexit survey by Prof Paul Whiteley of the University of Essex and Prof Harold Clarke, of the University of Texas, 52 per cent of the respondents thought that Britain could best control immigration outside the EU. Only three per cent thought immigration controls would be worse once Britain left the EU.

How could the elite be so wrong? Part of the answer lies in popular perceptions that the EU itself is in fact an elite project. Whiteley and Clarke’s survey reported that 64 per cent of graduates would vote to remain in Europe while only 25 per cent of those without formal qualifications would.

Comparable numbers showed up amongst the professional classes as against the unskilled. The jury is unanimous: those with higher education and globally marketable skills want a borderless world; those without want immigration barriers raised higher.

Would it be any different in the EAC? Would the Community survive a popular vote? Unlikely. A majority of the population lives far from the Community’s borders. With the exception of Rwanda and Burundi, both small countries with large populations close to international borders, few East Africans have crossed an international border and fewer still will cross one in their life.

At best, most East Africans are indifferent to their neighbours and, at worst, hostile to them as ‘foreigners.’ Consider a country like Malawi in contrast: 23 of its 28 districts have an international border. This means that the average Malawian will cross an international border many times in her life.

Thousands of Malawians live or have married from Mozambique, Tanzania, Zambia and even further afield from South Africa, Zimbabwe, Botswana and Namibia. Would Malawians vote to expel Mozambicans and Zambians from their country? Unlikely.

So far East Africa’s big idea is the push for political integration: one or two of current presidents are even thought to harbour ambitions of retiring to a future regional presidency. But there is a warning from Brexit here too: a headlong rush to political union without proper democratisation of regional institutions will be seen as elite-bargaining and, almost certainly, will unleash angry nationalism in member states. That would permanently damage the EAC.

Dangers of political opportunism

The third lesson is a warning about the dangers of political opportunism. The crisis unleashed by Brexit is of David Cameron’s making. Under pressure from Nigel Farage’s xenophobic United Kingdom Independence Party, UKIP, the eurosceptic wing of the British Conservative Party lurched further to the right, becoming even more virulently anti-Europe, at least in its rhetoric.

There were two reasons for this: it was partly to outflank UKIP and beat back Nigel Farage’s inroads into the Conservative’s constituencies and partly to mobilise the burgeoning anti-immigration sentiment amongst conservative voters, many of whom were especially angry about the influx of cheap labour from places like Poland.

In 2013, faced with hardening anti-Europe sentiment, a split in his party and with an eye on the 2015 election, David Cameron made an opportunistic and craven deal with the eurosceptics. In exchange for their support, he would offer them an “IN” or “OUT” referendum on the UK’s membership in the EU. His cynical deal won him the 2015 election but it has just cost him his career.

Here, too, are important lessons for the EAC. In a fit of hubris in 2013, Kenya, Uganda and Rwanda decided that Tanzania was a crimp on faster integration. They argued that it was time for ‘multi-speed EAC,’ code for the idea that Community members need not integrate at the same speed.

Laggards could take their time and the nimble, while the christened “the coalition of the willing” should be free to accelerate their own integration.

In quick succession Kenya, Uganda and Rwanda announced a series of huge infrastructure deals that excluded Tanzania but also included non-members, Ethiopia and South Sudan. The first of these was the ambitious Lamu Port – Southern Sudan-Ethiopia Transport (Lapsset) corridor project. The second project would be a new standard gauge railway linking the port of Mombasa to Kigali through Uganda.

President Jakaya Kikwete complained that this “coalition of the willing” was a claw-back on EAC integration but was ignored. Tanzania then said that under these conditions, everything – including exit of the EAC – was back on the table.

Kenyan leaders must remember that when the Community failed before, in 1977, it is they who engineered it. If they detect a certain hesitation or distrust from other EAC members, they should appreciate that neighbours, especially Tanzania, has only now begun to rebuild trust.

Youth exclusion

The final lesson speaks both to the nature of regional democracy and the role of the youth in it. Brexit was a revolt of the old: Britain left the EU because the old – who had the least stake in the future of Europe and need not live with the consequences of exit – lost faith in the future that Europe held out.

Among 18-24-year-olds, 75 per cent voted for Europe. Given that voter turnout increased with age and that Britain has an aging population, the youth sold their future short by staying away and letting their fathers and grandfathers shape a future they won’t have to live with.

Given the margin of the Brexit victory – 52 per cent to 48 per cent – it is almost certain that the ‘remain’ voters would have won if young voters had turned out in larger numbers.

It is a sobering thought: East Africa, unlike Britain, has a young population: on average, between 25 to 30 per cent of the population of the Community is between 15 and 30 years old. Like Britain though, the youth have not been turning out to vote and so, they are leaving decisions that shape the future to those who have the least stake in it.

In these lessons lies a grim message: The EAC should look to Brexit and see that a lack of common values; a growing democratic deficit; self-serving nationalism and political opportunism coupled with youth exclusion will eventually sap and ultimately destroy regional integration.

Pausing to gloat rather than learn from Britain’s woes is exactly the kind of complacency the EAC does not need right now.

Wachira Maina is a constitutional lawyer.

Related News

Netanyahu heads for Africa to find deals, mark Entebbe rescue

Prime Minister Benjamin Netanyahu will try this week to generate new business in Africa for Israeli companies while making an emotional journey to Uganda, where his brother died 40 years ago in the daring Entebbe hostage rescue.

Netanyahu left Monday on a five-day tour that also includes Kenya, Ethiopia and Rwanda in the first trip by an Israeli prime minister to sub-Saharan Africa in 29 years. With a delegation of 70 business executives, the African excursion is part of the Israeli leader’s effort to cultivate growth markets while economies languish in the country’s biggest trade partners, the U.S. and European Union.

“This has very important implications for diversifying our international alliances and international relations and expanding our powers to Asia, Russia, Latin America, and of course now, the African continent,” Netanyahu told cabinet members on Sunday. Before departing Monday, he called the trip “historic” and added, “Israel is coming back to Africa, big time.”

While Netanyahu touts Israeli technology, particularly in the fields of anti-terrorism, desalination and solar energy, he also has a clear diplomatic agenda. The prime minister is pushing for open political support from African countries that have largely sided with Arab nations on resolutions critical of Israel in the United Nations and African Union. He made the point directly in February to visiting Kenyan President Uhuru Kenyatta.

Military Allies

“Many of these countries can be said to be military allies of Israel because they also have the threat of radical Islam and terrorist attacks,” said Emmanuel Navon, a political scientist at Tel Aviv University. “They are very fond of Israeli military technology and anti-terrorist expertise but that doesn’t mean at the UN in terms of votes, we’ll reap any benefits.”

Last July, Kenya and Ethiopia both abstained in a UN Human Rights Council vote condemning Israel for alleged war crimes in the Gaza Strip.

Israel has a long history of ties with African nations built on export of arms and agricultural products while importing oil, diamonds and other natural resources.

Companies sending executives with Netanyahu include Elbit Systems Ltd., the country’s biggest publicly traded defense contractor; Netafim Ltd., which makes irrigation systems; Magal Security Systems Ltd., a specialist in perimeter security at airports; Israel Chemicals Ltd., a fertilizer producer; and dronemaker Aeronautics Ltd.

Entebbe Ceremony

The prime minister will attend two gatherings for his business delegation and potential local partners in Kenya and Ethiopia. He said last week that Israel is allocating about $13 million to strengthen economic ties with the four African countries, including training programs in health and security techniques and the signing of an agreement on space satellite technology in Ethiopia.

Netanyahu’s first stop will be a ceremony Monday at Entebbe airport marking the hostage rescue on July 4, 1976.

The prime minister’s older brother, Yonatan Netanyahu, led the commando rescue of about 100 passengers and crew members on an Air France flight seized by Palestinian and German hijackers. The Ugandan president at the time, Idi Amin, openly supported the hijackers demanding the release of Palestinian militants in Israeli prisons and prisoners in other countries.

About 100 commandos landed at the airport at night after flying 2,500 miles from Israel, bringing along a black Mercedes similar to the one the Ugandan leader used to try to fool troops guarding the airport. Bursting into the terminal, the Israelis killed the hijackers along with 45 Ugandan soldiers. Yonatan Netanyahu, the only Israeli commando killed, has become a symbol of bravery in his country. The prime minister refers to his brother’s death as a painful turning point that projected him into politics.

Related News

tralac’s Daily News Selection

The selection: Friday, 1 July 2016

SADC finance and economy ministers in Gaborone for peer review meetings (Channel Africa)

Trade, industry, finance and investment ministers from SADC have started a series of regional development peer review meetings which will run from 28 June to 8 July. "The Committee of Ministers of Trade meeting will take place on 5 July 2016. The Ministerial Task Force on Regional Economic Integration comprising, Ministers responsible for Finance, Trade and Infrastructure will meet on 6 July, while the Ministers of Finance and Investment and the Peer Review Panel will be from the 7-8 July" said Botswana Finance and Development minister Kenneth Mathambo.

South Africa: 2016 merchandise trade statistics (SARS)

The R18.73bn trade balance surplus for May 2016 is due to exports of R104.68bn and imports of R85.95bn. Exports for the year-to-date of R451.62bn are 10.2% more than the exports of R409.98bn recorded in January to May 2015. Imports for the year-to-date of R452.28bn are 3.4% more than the imports recorded in January to May 2015 of R437.56bn. The cumulative deficit for 2016 of R0.65bn is 97.6% less than the deficit for the comparable period in 2015 of R27.58bn.

The impact of Brexit: presentation by SA National Treasury (pdf, AgBiz)

Regarding total trade (i.e. both imports and exports), the UK ranked 6th largest trading partner. In 2015, SA exported R41.6bn worth of products into the UK and imported R35bn with a R6.6bn trade balance in favour of SA. Critical to negotiate trade and investment treaties sooner rather than later: SA is largest African trading partner but Africa is a very small part of the UK trade.

Gerhard Erasmus: ‘Some implications of Brexit for Southern African trade relations’ (tralac)

This Trade Brief discusses the trade implications of Brexit for the SADC EPA and will mention some of the related predicaments which the UK now faces. This episode serves as a lesson too of the costs involved in undoing well integrated regional integration arrangements. Southern African governments should ensure that their needs and the continuation of certainty in reciprocal market access arrangements will get the urgent attention which they merit. This will be a difficult task but these are matters which cannot be left to decisions of Her Majesty’s Government alone. We need well thought-through responses and diplomatic initiatives of our own. Technical issues need to be clarified in order to support such initiatives. [J. Peter Pham: 'Africa and Brexit: not all bad news' (Atlantic Council)]

Kenya: Q1 GDP, Balance of Payments report (pdf, KNBS)

In the first quarter of 2016, international merchandise trade balance improved by 25.4% to a deficit of KSh 167,251 million. Domestic export earnings increased by 13.4% to KSh 130,650 million in the quarter under review boosted by growth in earnings from horticulture and tea exports. Overall balance of payments improved to a surplus of KSh 26,318 million from a deficit of KSh 17,063 million in the corresponding quarter of 2015 as shown in Table 5. The current account balance improved by 30.1% from a deficit of KSh 101,539 million in the first quarter of 2015 to a deficit of KSh 71,018 million in the quarter under review. The narrowing of the current account deficit could be explained by the decline in import expenditure and a considerable increase in the value of exports. Cross border services receipts declined by 7.1% while payments increased by 9.0% translating into a surplus of KSh 14,265 million in international trade in services during the first quarter of 2016. Remittances from the diaspora continued to grow in the first quarter of 2016, increasing by 28.4% to KSh 42,777 million from KSh 33,328 million in the first quarter of 2015.

Nigeria-India trade hits $16bn (The Sun)

The trade volume between the Federal Republic of Nigeria and India has hit $16bn, the Indian High Commissioner-designate to Nigeria, B.N. Reddy has revealed. The Indian envoy who spoke in Abuja during the launch of the India-Nigeria Business Promotion Council, said as biggest trading partners in Africa, both countries must share experiences and assist each other in areas of interests. Former Education Minister, Oby Ezekwuesili who also spoke, bemoaned the trade imbalance between Africa and India. She called for its review, while urging the Federal Government to create an enabling environment so that investors can come into the country. “India’s trade with Africa is about $300 billion. Out of that, Africa accounts for about $32 billion,” she added.

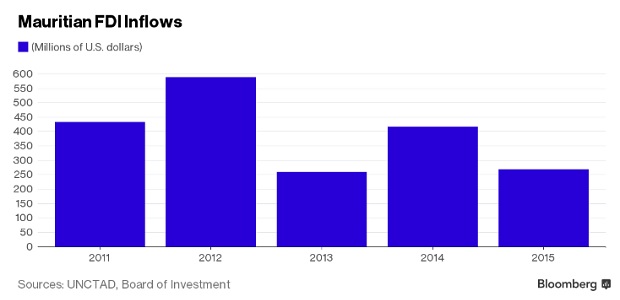

Mauritius expects 46% jump in foreign investment in 2016 (Bloomberg)

Mauritius's government expects foreign direct investment to increase as much as 46% this year, even as the United Kingdom’s decision to leave the European Union may curb inflows to the Indian Ocean island nation. Foreign investors are expected to commit 14 billion rupees ($395 million) by the end of 2016, compared with 9.6 billion rupees last year, Board of Investment Chief Executive Officer Ken Poonoosamy said in a phone interview Tuesday from the capital, Port Louis.

Mozambique’s foreign investment slumps 35% in first quarter – Finmin (Club of Mozambique)

Investors brought in $650m in the first three months compared with $1bn a year ago, Finance Minister Adriano Maleiane told members of the ruling Mozambique Liberation Front, or Frelimo, on Wednesday in the capital, Maputo. “Foreign direct investment used to be an important source of foreign exchange, but it’s falling,” Maleaine said. [Minister Tonela appoints 12 new names for Industry and Trade]

Zimbabwe: Cargo stuck as importers struggle for permits (The Herald)

Commercial cargo has been stuck at Beitbridge Border Post for the past seven days as importers struggle to get permits to ship goods that are restricted from Open General Import Licence under Statutory Instrument (SI) number 64 of 2016. The SI tightens screws on the import of basic commodities including food items, building material, furniture, toiletries and cooking oil among other things. Several trucks are stuck on the South African side since the Zimbabwe side has no adequate space to accommodate them. The Herald is reliably informed that the Zimbabwe Revenue Authority has resorted to requesting for a surety of $2 000 from importers.

Zimbabwe: Police roadblocks threat to ease of doing business (The Herald)

National Assembly Speaker Advocate Jacob Mudenda yesterday said there was need for the police to reduce the number of roadblocks as recently pronounced by national police spokesperson Senior Assistant Commissioner Charity Charamba. “We have debated in Parliament and said there is no law that says there should be X number of roadblocks on the road,” he said. “Tourists driving from Beitbridge to here, Victoria Falls, on average must go through 20 roadblocks, why? They have been checked at the border for whatever imagined misdemeanours they might have and they came through Customs and Immigration.”

Tazara: Sh94 billion debt casts dark shadow over Tazara revival (The Citizen)

Outstanding payments amounting to Sh94 billion could stand in the way of plans to revamp the Tanzania-Zambia Railways Authority, The Citizen has learnt. Documents seen by The Citizen show that Chinese investors interested in taking over Tazara want the debt cleared before meaningful investments can be made. This includes delayed payments to suppliers, unpaid pensions for retirees, salary arrears and contributions that have not been remitted to pension funds.

Tanzania: Govt suspends TBS boss (The Citizen)

Tanzania Bureau of Standards Director General Joseph Masikitiko was dramatically suspended yesterday, with the government saying the move was aimed at paving the way for an investigation into unspecified matters. The suspension was announced by the Industry, Trade and Investment Permanent Secretary, Prof Adolf Mkenda, in a statement sent to newsrooms last night. Also suspended alongside Mr Masikitiko was TBS Finance, Planning and Administration Manager Emmanuel Ntely. The communication was issued a few hours after Industry, Trade and Investment minister Charles Mwijage made an unannounced visit to TBS offices in Ubungo, Dar es Salaam.

Akinwumi Adesina: opening speech at 2nd negotiations meeting of the African Development Fund (AfDB)

The Industrialise Africa strategy has just been sent to the Board for approval, and the Integrate Africa strategy will also follow. I am very pleased that in Lusaka we set up a Special Panel – led by former UN Secretary-General Kofi Annan and former German President Horst Köhler, and including other global development luminaries from the public and private sector – which will help us as we roll out the High 5s.

Competitive manufacturing sector can solve issues in SA (IOL)

South Africa is not de-industrialising, but manufacturing is changing. The manufacturing sector is today 15% bigger than it was 10 years ago, 51% bigger than 20 years ago, and 64% bigger than 30 years ago. However, employment numbers have declined alarmingly: 14% fewer people are employed today than in 2005, 23% fewer than in 1995 and 27% fewer than 1984. Confusion arises when the size and share of the economy is mentioned in the same breath. Manufacturing constitutes a diminishing share of the economy simply because other sectors, primarily services, have been growing faster over the same period. According to the SA Reserve Bank, manufacturing’s contribution to the economy has declined from 19.7% in 1995 to 13.7% last year. [The author, Henk Langenhoven, is chief economist of the Steel and Engineering Industries Federation of Southern Africa]

South Africa: Green Paper on International Migration (pdf, Dept of Home Affairs)

Given the policy shortcomings of the current White Paper and much of the legislation based on it, this Green Paper argues that South Africans need to adopt a paradigm that sees international migration as enabling their own development and that of their country and region. In the new paradigm, South Africans would see themselves as responsible citizens of SA, Africa and the world and support efficient, secure and humane approaches to managing international migration. The current paradigm exposes SA to many kinds of risk in a volatile world and by default strengthens colonial patterns of labour, production and trade. It also serves to perpetuate irregular migration, which in turn leads to unacceptable levels of corruption, human rights abuse and national security risks. The current draft of the Green Paper raises issues that require policy interventions in seven broad policy areas. Some of the policy areas are more fully developed than others. [Speech by Home Affairs Minister Malusi Gigaba]

Alan Hirsch: 'Institute will equip future leaders to beat inequality' (Business Day)

Finally, Africa’s growth has not been equal. The income and wealth gaps between countries — as well as the gaps within many countries — are growing. Southern Africa tends to have the most inequality within countries. SA, Namibia, and Botswana are among some of the most unequal countries in the world, and Angola and Zambia are not far off. The average Gini coefficient for Africa is 0.43, which is significantly greater than the coefficient for the rest of the developing world at 0.39. On average, the top 20% of earners in Africa have an income that is more than 10 times that of the bottom 20%. Recently, the London School of Economics established the International Inequalities Institute to identify and support innovative interdisciplinary research and teaching that addresses inequalities, and to create a structure that was agile and flexible enough to accommodate this vision over generations. With generous funding from Atlantic Philanthropies, the Atlantic Fellowship Programme has just been announced, based at the institute. UCT is a collaborating partner.

Alan Roe: 'Like it or not, poor countries are increasingly dependent on mining and oil and gas' (UNU-WIDER)

The UNU-WIDER project on managing natural resources seeks to examine how poor and middle-income countries can best use their natural resource wealth to promote development. It is well understood that minerals, metals, oil or gas (collectively known as ‘extractives’) have for some years been significant in the economies of low- and middle-income countries. What perhaps is less well known is:

Malaysia Economic Monitor: leveraging trade agreements (World Bank)

Sahel and West Africa Club: newsletter, 21-27 June

Innovation prize for Africa 2016: keynote address by President Ian Khama (Mmegi)

World Bank's annual classification of nations by GNI per capita

Asean-5 Cluster Report: evolution of monetary policy frameworks (IMF)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

New meeting in Abidjan for ADF-14: Financing the development of a winning Africa

This week sees the opening of the 2nd meeting for the fourteenth replenishment of the African Development Fund (ADF-14) under the aegis of African Development Bank President Akinwumi Adesina, following the first replenishment meeting in March.

The gathering, held behind closed doors on June 30 and July 1, will be attended by the Deputies – representatives of donor countries to the Fund – as well as those of the governments of regional member countries, the AfDB Group and observers from peer institutions, all under the coordination of Richard Manning, Senior Research Fellow at the Blavatnik School of Government at Oxford University.

The African Development Fund (ADF) is one of the three distinct entities that make up the African Development Bank Group, along with the AfDB itself and the Nigeria Trust Fund (NTF). It is, above all else, its financial award section, that is, the heart of the sources of the AfDB Group’s funding. These sources enabling the Group to continue to financially assist those of its 54 regional member countries who need help most. To date, the ADF has 38 countries in receipt of support[1] and 29 donor countries.

ADF-13, drawing to its end, is intended with ADF-14 to mobilize resources to be used for funding awarded in the three-year period 2017-2019.

A delicate situation

Nevertheless, this resource mobilization process, a sort of “call for funds” to donors, is taking place at a difficult moment when the global economic and financial situation is far from positive and official development assistance is being cut. Donor countries are having to address the headwinds of the current international situation and stronger budgetary constraints while at the same time recipient countries, the most vulnerable, are seeing their needs growing and becoming more pressing, only sharpened by domestic and external economic pressures. This means that conduct of ADF-14 is a delicate matter, particularly in view of the ambitions of the new Sustainable Development Goals (SDGs) adopted in mid-2015 after the great Addis Ababa international conference on financing for development held in July of the same year, the global climate deal reached at COP21 and the High Five priorities the Bank has subsequently set itself to accelerate the development of the continent.

ADF-14: Focus on the High 5s to finance inclusive development

The majority of people living in ADF countries live in extreme poverty, on less than US$ 1.90 a day. On average, only 25% of them have access to electricity – and even less than that in 19 of the 38 ADF countries. Average electricity consumption in these countries is less than 200 kW/h per year, in comparison with the 12,954 kW/h used in the United States or the 6,520 kW/h in Europe. In ADF countries, energy shortages are estimated to cost between 2% and 4% in annual growth, on top of their consequences for employment, health, education, security and so on. This situation is intended to be tackled by the first of the AfDB’s High 5s: Light up and power Africa. With ADF-14, AfDB is planning to invest nearly US $2.9 billion in energy in ADF countries between early 2017 and late 2019 in order to install up to 4,600 MW of capacity – enough to connect 23.6 million Africans to the power grid.

According to estimates, nearly 158 million people suffer from undernutrition (particularly leading to delayed growth) in ADF countries. And this is despite enormous agricultural potential. Agriculture is a sector that is still too inefficient, as emphasized in the second of the Bank’s High 5 priorities: Feed Africa. AfDB invested US $4.3 billion in ADF countries in agricultural and agribusiness projects between 2006 and 2014 and this ADF-14 will make it possible to further invest up to US $2.1 billion by the end of 2019, given the Bank’s planned projects in this sector (the creation of agricultural development clusters and infrastructure in rural areas, water management and improved irrigation, capacity building, technology transfer, etc.) This will lead – among other benefits – to improved agricultural production, growing incomes for rural populations, reduced poverty and lower import bills.

The countries of the continent, and particularly ADF countries, need to diversify and strengthen their economic frameworks and thereby develop their private sectors. As of now, Africa’s only has a 1.5% share of the global value chain and only 19% of its exports are in manufactured goods. In several ADF countries, industrial GDP is only US $100 per capita.

Industrialise Africa is, therefore, the third of the Bank’s High 5. However, given the profile of the ADF countries and especially the most vulnerable of them, the role of the ADF is even more crucial in this area: in granting concessional funding, the ADF provides viable budget resources to the public sector while supporting the financing of the private sector through a range of risk mitigation instruments, guarantee products and mixed funding mechanisms intended to attract other finance to fill the funding gap. For ADF-14, operations targeting the industrialization of the ADF countries amount to more than US $1.7 billion. The Bank is also planning for ADF-14 to particularly strengthen support for the development of the private sector by increasing allocations to the credit enhancement facility for the private sector, which provides guarantees for non-sovereign operations conducted by countries eligible for ADF.

Integrate Africa is the fourth of the Bank’s High 5 and its justification can be found in these figures: at 15%, regional trade in Africa is the weakest in the world and this lack of integration is estimated to cost the continent between 1% and 1.5% in GDP every year. ADF countries are among the most fragmented and isolated markets. The African Development Fund, therefore, has a budget dedicated to regional integration whose investments are targeted at the elimination of non-tariff barriers that impede trade, material infrastructure (roads, rail, transport corridors), and cross-border water management, in addition to building the capacities of Regional Economic Communities (RECs), harmonizing investment codes, quality standards and certifications, overhauling the visa regime to facilitate free movement of people, the implementation of trade facilitation agreements made under the aegis of the WTO, and more. ADF-14 already has regional integration projects in the pipeline to a value of US $2.7 billion. Among other benefits of ADF-14, 73 million people will have better access to transportation by the end of 2019.

Although the ADF countries have had somewhat higher growth rates over the past decade, their poverty rates also remain high, as do inequality between men and women and between rural and urban areas. In some vulnerable ADF countries, youth unemployment is at 50%. In these countries, nearly 333 million people lack access to clean, safe water and some 772 million do not have sanitation facilities worthy of the name. To foster inclusive development in this context there is, therefore, a need to create jobs (made all the more acute by the challenges of population growth) and to promote entrepreneurship, provide economic opportunities to meet the expectations of the people and curb migration, to strengthen health systems using lessons learned from the recent Ebola crisis and to build capacities for resource optimization in social spending, to develop safety nets and, lastly, to increase access to clean water and sanitation services. And these are precisely the objectives of the fifth of the Bank’s High 5 priorities: Improving the quality of life for the people of Africa.

Under ADF-14, the Bank is, therefore, planning to invest around US $1.9 billion in the ADF countries, through which 9.5 million school textbooks and teaching materials will be produced, 5,000 health workers will be trained and 17 million people will receive better access to health services. The Bank’s new Jobs for Youth in Africa initiative (JfYA) is also intended to create 17.5 million jobs in ADF countries and provide 50 million young Africans with economic and professional skills by 2050.

US $45 billion invested over 40 years

At their first meeting, held in March 2016, the plenipotentiaries agreed that the ADF was “anchored in the Ten Year Strategy of the Bank“ and that the accent would be on the five key priorities, the High 5s, that the Bank has set itself. Three innovative financing instruments were endorsed: donors’ concessional loans, bridge loans and buyback mechanisms. This was also the case for the new model for development and service provision that the AfDB Group has begun deploying to accelerate the pace of Africa’s transformation and to promote a results culture.

Debate at this second meeting will centre on implementation of the AfDB’s High 5s, the framework for measuring the AfDB Group’s results by 2025, the role of ADF-14 in specific support for fragile states and for the development of the private sector, the proposed new financial instruments, the ADF liquidity policy and the ADF-14 funding and resource allocation framework.

A third and final meeting to be held in late November 2016 will conclude the ADF-14 replenishment process. Forty-two years after the very first replenishment of ADF resources in 1974, ADF-14 is not only maintaining but developing its ambitions. ADF-13, agreed in September 2013 and devoted to financing the Fund’s activities for the period 2014-2016, achieved the equivalent of US $7.3 billion.

The cumulative investments of the Fund on the African continent over its 40 years of existence amount to approximately US $45 billion.

[1] Eligibility for ADF is determined by a country’s gross national income per capita (GNI per capita) and its solvency.

Related News

South Africa Merchandise Trade Statistics for May 2016

South Africa’s trade balance swings to record surplus as commodities boost exports

South Africa in May recorded its biggest monthly trade surplus since the revenue service introduced a revised series in 2010 to incorporate trade with neighbouring states, as firmer commodity prices boosted exports.

The data points to a narrowing in South Africa’s longstanding current account deficit, which widened to 5 percent of GDP in the first quarter of the year, and has traditionally been a source of vulnerability for the rand.

Exports rose 14 percent to 104.68 billion rand on a month-on-month basis, while imports were down 6.6 percent to 85.95 billion rand, the South African Revenue Service said in a statement.

This resulted in a bigger-than-expected trade surplus of 18.73 billion rand ($1.3 billion) for May, compared with a revised 127 million rand shortfall in April.

Analysts polled by Reuters had expected a trade surplus of 3.1 billion rand.

The rand, which was down 0.4 percent on the day against the dollar just before release of the data, turned firmer, and was trading 0.64 percent stronger at 14.6900 by 1336 GMT.

“This (trade) performance bodes in favour of our current forecast for SA’s current account deficit to narrow back towards 4.0 percent of GDP in Q2,” BNP Paribas Securities economist Jeffrey Schultz said.

He however warned of risks to the trade outlook later in the year from possible wage strikes in the auto, platinum and steel and engineering sectors, as well as increased concerns over the global economy after Britain voted to leave the European Union last week.

The South African Revenue Service (SARS) has released trade statistics for May 2016 that recorded a trade surplus of R18.73 billion. This figure includes trade data with Botswana, Lesotho, Namibia and Swaziland (BLNS).

Including trade data with Botswana, Lesotho, Namibia and Swaziland (BLNS)

The R18.73 billion trade balance surplus for May 2016 is due to exports of R104.68 billion and imports of R85.95 billion. Exports for the year-to-date of R451.62 billion are 10.2% more than the exports of R409.98 billion recorded in January to May 2015. Imports for the year-to-date of R452.28 billion are 3.4% more than the imports recorded in January to May 2015 of R437.56 billion. The cumulative deficit for 2016 of R0.65 billion is 97.6% less than the deficit for the comparable period in 2015 of R27.58 billion.

April 2016’s trade balance was revised downwards by R0.56 billion from the previous month’s preliminary surplus of R0.43 billion to a revised deficit of R0.13 billion. Exports increased from April 2016 to May 2016 by R12.82 billion (14.0%) and imports decreased from April 2016 to May 2016 by R6.04 billion (6.6%).

On a year-on-year basis, the R18.73 billion surplus is an improvement from the surplus recorded in May 2015 of R4.44 billion. Exports of R104.68 billion are 18.5% more than the exports recorded in May 2015 of R88.31 billion. Imports of R85.95 billion are 2.5% more than the imports recorded in May 2015 of R83.87 billion.

Trade highlights by category

The month-on-month export movements (R’ million):

| Section: | Including BLNS: | |

| Precious Metals & Stones | + R8 141 | + 49.1% |

| Mineral Products | + R1 695 | + 10.4% |

| Vegetable Products | + R1 263 | + 27.4% |

| Base Metals | + R 711 | + 6.3% |

| Chemical Products | + R 525 | + 10.4% |

The year-to-date export movements (R’ million):

| Section: | Including BLNS: | |

| Precious Metals & Stones | + R12 348 | + 16.3% |

| Vehicles & Transport Equipment | + R9 373 | + 18.8% |

| Vegetable Products | + R5 441 | + 29.4% |

| Base Metals | + R5 098 | + 9.9% |

| Machinery & Electronics | + R4 762 | + 12.4% |

The month-on-month import movements (R’ million):

| Section: | Including BLNS: | |

| Machinery & Electronics | - R2 803 | - 11.7% |

| Mineral Products | - R1 812 | - 14.5% |

| Original Equipment Components | - R 862 | - 10.2% |

| Animal/Vegetable Fats | - R 453 | - 43.0% |

| Precious Metals & Stones | - R 380 | - 34.8% |

The year-to-date import movements (R’ million):

| Section: | Including BLNS: | |

| Machinery & Electronics | + R8 648 | + 8.1% |

| Original Equipment Components | + R6 102 | + 18.3% |

| Vegetable Product | + R4 611 | + 49.8% |

| Vehicles & Transport Equipment | - R3 176 | - 6.7% |

| Mineral Products | - R21 415 | - 27.3% |

Trade highlights by world zone

The world zone results from April 2016 (Revised) to May 2016 are given below.

Africa:

Trade surplus: R15 733 million – this is a 0.7% decrease in comparison to the R15 847 million surplus recorded in April 2016.

America:

Trade deficit: R 977 million – this is a 55.7% decrease in comparison to the R2 204 million deficit recorded in April 2016.

Asia:

Trade deficit: R5 472 million – this is a 61.0% decrease in comparison to the R14 028 million deficit recorded in April 2016.

Europe:

Trade deficit: R1 087 million – this is a 87.0% decrease in comparison to the R8 391 million deficit recorded in April 2016.

Oceania:

Trade surplus: R 71 million – this is a 68.8% decrease in comparison to the R 228 million surplus recorded in April 2016.

Excluding trade data with Botswana, Lesotho, Namibia and Swaziland (BLNS)

The trade data excluding BLNS for May 2016 recorded a trade surplus of R10.70 billion, with exports of R93.95 billion and imports of R83.25 billion.

Exports increased from April 2016 to May 2016 by R14.03 billion (17.6%) and imports decreased from April 2016 to May 2016 by R6.36 billion (7.1%).

The cumulative deficit for 2016 is R42.62 billion compared to R69.71 billion in 2015.

Trade highlights by category

The month-on-month export movements (R’ million):

| Section: | Excluding BLNS: | |

| Precious Metals & Stones | + R8 695 | + 54.5% |

| Mineral Products | + R2 040 | + 14.2% |

| Vegetable Products | + R1 300 | + 32.7% |

| Base Metals | + R 693 | + 6.6% |

| Chemical Products | + R 520 | + 12.7% |

The month-on-month import movements (R’ million):

| Section: | Excluding BLNS: | |

| Machinery & Electronics | - R2 780 | - 11.7% |

| Mineral Products | - R1 817 | - 14.6% |

| Original Equipment Components | - R 862 | - 10.2% |

| Animal/Vegetable Fats | - R 457 | - 43.5% |

| Precious Metals & Stones | - R 627 | - 58.5% |

Trade highlights by world zone

The world zone results for Africa excluding BLNS from April 2016 (Revised) to May 2016 are given below.

Africa:

Trade surplus: R7 711 million – this is a 22.5% increase in comparison to the R6 295 million surplus recorded in April 2016.

Botswana, Lesotho, Namibia and Swaziland (Only)

Trade statistics with the BLNS for May 2016 recorded a trade surplus of R8.02 billion. The R8.02 billion surplus for May 2016 is as a result of exports of R10.73 billion and imports of R2.71 billion.

Exports decreased from April 2016 to May 2016 by R1.21 billion (10.1%) and imports increased from April 2016 to May 2016 by R0.32 billion (13.4%).

The cumulative surplus for 2016 is R41.97 billion compared to R42.13 billion in 2015.

Trade highlights by category

The month-on-month export movements (R’ million):

| Section: | BLNS: | |

| Precious Metals & Stones | - R 554 | - 91.0% |

| Mineral Products | - R 345 | - 17.0% |

| Machinery & Electronics | - R 146 | - 8.0% |

| Vehicles & Transport Equipment | - R 107 | - 7.7% |

| Prepared Foodstuff | + R 91 | + 9.3% |

The month-on-month import movements (R’ million):

| Section: | BLNS: | |

| Precious Metals & Stones | + R 247 | + 1164.3% |

| Chemical Products | + R 133 | + 28.6% |

| Vehicles & Transport Equipment | - R 18 | - 39.3% |

| Machinery & Electronics | - R 23 | - 7.7% |

| Textiles | - R 32 | - 7.9% |

Related News

Lesotho’s new Partnership Framework supports improved public sector, private sector job creation

The World Bank Group Board of Executive Directors on 30 June 2016 endorsed a five-year Country Partnership Framework (CPF) for Lesotho, expected to deliver US $154 million over 2016 to 2020 to projects in support of the Mountain Kingdom’s efforts to improve public sector efficiency and effectiveness and promote private sector job creation.

The World Bank Group CPF is aligned with the goals of the Lesotho Vision 2020 and the National Strategic Development Plan 2012 to 2017. The framework outlines proposed investment projects, technical assistance and analytical and advisory services that are aimed at assisting the Government of Lesotho in tackling its priority challenges in line with the World Bank Group’s twin goals of ending extreme poverty and promoting shared prosperity by fostering the income growth of the bottom 40% in every country.

“Through this framework, we will support the Government of Lesotho in its transition to a new growth model driven by private sector investment which will require a reduction in the size of the public sector and improved public sector effectiveness,” said Guangzhe Chen, World Bank Country Director for Lesotho. “We will assist the Government of Lesotho to create space for the private sector to become an engine of growth and employment, in a challenging economic environment with very high unemployment.”

Lesotho’s public expenditure is above 60% of its gross domestic product (GDP) driven largely by a wage bill which is among the highest in the world at 23.1% of GDP. Along with a domestic private sector which is dependent on the state and non-tradable sectors, and several mutually reinforcing volatile events in the last 18-months such as the global commodity price slump rand the severe drought in Lesotho have exacerbated the country’s economic situation.

The proposed program of engagement seeks to achieve results in two strategic focus areas. Firstly, improving efficiency and effectiveness of the public sector through support aimed at helping the Government of Lesotho to improve public sector and fiscal management; improve equity of the social protection system; improve basic education outcomes; and improve health outcomes.

Secondly, promoting private sector job creation through support aimed at improving the business environment and diversifying the economy; improving smallholder agricultural productivity; increasing transport connectivity to facilitate private sector growth; and increasing water and renewable energy supply for industry, agriculture and export opportunities.

“Our partnership with Lesotho strives to help improve the business environment for the private sector, which is critical for job creation,” said Saleem Karimjee, IFC Country Manager. “Building a dynamic and competitive private sector through a sustained effort to diversify the economy is key to private sector growth.”

The CPF was shaped by a series of consultations with key stakeholders including government, development partners and civil society organizations and the private sector. It recognizes the importance of collaborating with other development partners, and elaborates plans to continue to increase efforts to promote communication and transparency between development partners and the government.

The two focus areas include eight strategic objectives expected to lead to strong development results. These priorities emerged from the Lesotho Systematic Country Diagnostic, an evidence based and comprehensive assessment carried out by the World Bank Group on the country’s key challenges, the South Africa Custom’s Union revenue crisis and the severe drought, as well as the Lesotho’s own strategic objectives. These eight priorities are:

-

Improving public sector and fiscal management – to achieve a capital budget that is fully derived from the public investment plan, and elimination of irregular HR and payroll cases in the civil service and non-eligible beneficiaries from the Old Age Pension.

-

Improving equity of the social assistance system – to increase the percentage of households receiving an expanded Child Grant Program that are in the poorest forty percent of the population.

-

Improving Basic Education Outcomes – to reduce drop-out rates in the 300 lowest performing primary and junior secondary schools most of which are located in mountainous and hard to reach poor rural areas.

-

Improving health outcomes – to increase average Health Facility Quality – to improve contract management of the Queen Mamohato Memorial Hospital, and improve TB treatment success rate nationwide for new and relapse TB cases.

-

Improving the business environment reform and diversifying the economy – to increase progress in the investment climate reform agenda and increase the number of domestic enterprises registered and operating in the non-textile sectors.

-

Improving smallholder and MSME agricultural productivity – to increase the household commercialization level in select districts.

-

Increasing transport connectivity to facilitate private sector growth – to improve transport connectivity for local agricultural markets and tourist sites and create jobs through road construction and maintenance jobs, and

-

Increasing water and renewable energy supply for industry, agriculture and export opportunities – to ensure that bulk water supply works are underway or completed in priority water demand zones, i.e. those with significant industrial, commercial and/or agriculture water demand, identify new viable renewable energy generation projects and complete a feasibility study of the hydropower component of Phase II of the highlands water project.

In addition to financial and technical assistance support, the WBG will also provide advisory services and analytics focusing on understanding the links between jobs, education, growth and competiveness, Under the CPF, the WBG will also undertake a poverty and inequality analysis, private sector diagnostic and, jointly with the government, a review of public expenditure. It will also support financial inclusion and strengthening the pension and insurance sectors, and analyze the impacts of the demographic dividend for Lesotho.

* The World Bank’s International Development Association (IDA), established in 1960, helps the world’s poorest countries by providing grants and low to zero-interest loans for projects and programs that boost economic growth, reduce poverty, and improve poor people’s lives. IDA is one of the largest sources of assistance for the world’s 77 poorest countries, 39 of which are in Africa. Resources from IDA bring positive change to the 1.3 billion people who live in IDA countries. Since 1960, IDA has supported development work in 112 countries. Annual commitments have averaged about $19 billion over the last three years, with about 50 percent going to Africa.

Related News

SADC finance and economy ministers in Gaborone for peer review meetings

Trade, industry, finance and investment ministers from the Southern Africa Development Community (SADC) have started a series of regional development peer review meetings which will run from June 28 to July 8.

In a statement, Botswana’s Ministry of Finance and Development Planning said the meetings, which are also set to review progress made on regional economic integration, will be held at the Gaborone International Convention Centre (GICC).

“The meetings will also comprise the SADC Peer Review Panel, which is constituted by regional Ministers of Finance and Central Bank Governors. The meetings will be attended by Senior Officials from the respective Ministries, as well as the officials from the Bank of Botswana.

“The Committee of Ministers of Trade meeting will take place on the 5th July 2016. The Ministerial Task Force on Regional Economic Integration comprising, Ministers responsible for Finance, Trade and Infrastructure will meet on the 6th July 2016, while the Ministers of Finance and Investment and the Peer Review Panel will be from the 7th to 8th July 2016,” said Botswana Finance and Development minister Kenneth Mathambo.

Further, the ministry said the meetings would provide input for regional integration topics set to be discussed at the next SADC Council of Ministers meeting, which is due to be held in Mbabane, Swaziland, in August.

Related News

Mauritius expects 46% leap in foreign investment this year

Mauritius’s government expects foreign direct investment to increase as much as 46 percent this year, even as the United Kingdom’s decision to leave the European Union may curb inflows to the Indian Ocean island nation.

Foreign investors are expected to commit 14 billion rupees ($395 million) by the end of 2016, compared with 9.6 billion rupees last year, Board of Investment Chief Executive Officer Ken Poonoosamy said in a phone interview Tuesday from the capital, Port Louis. The country received 3 billion rupees in the first quarter, Bank of Mauritius data shows. FDI slumped last year from 18.5 billion rupees in 2014, when the $12 billion economy saw several hotel acquisition deals, according to the BoI.

“With uncertainties like Brexit, we need to be very cautious in terms of figures,” Poonoosamy said. The board has some visibility “on projects that have been already been secured,” he said, without elaborating.

The U.K. is the third-biggest source of FDI flows into Mauritius, accounting for about 9 percent of the total, according to a U.S. State Department report. The country is the easiest place in Africa to do business, according to the World Bank, while the African Development Bank ranks it as the most competitive economy in sub-Saharan Africa. The sugar- and textile-exporting nation is targeting becoming a high-income country, which is defined as an economy with a gross national income per capita above $12,735, by 2025. It’s currently $700, according to the World Bank.

Real estate attracts the largest share of FDI in Mauritius, with 80 percent of the amount received in the first quarter of this year invested in the sector. In 2015, 84 percent was plowed into similar projects. The Integrated Resort Scheme and Residential Estate Scheme introduced in 2002 facilitates the acquisition of resort and residential property by non-citizens on the island. International buyers can become Mauritian residents once they acquire a luxury property with a minimum investment of $500,000.

The government has introduced a Property Development Scheme, which will require future developments to contribute social amenities and facilities that benefit the community.

The sugar- and textile-exporting island nation that attracts about 1 million tourists every year projects earning 55 billion rupees from foreigners who will visit this year, compared with 50.2 billion rupees in 2015.

“We are aware of the concentration of FDI in real estate and the BoI is doing everything possible to make sure there is diversification and that we attract investment in other sectors, mainly in manufacturing,” Poonoosamy said, adding that there are several plans by investors to build factories.

Related News

Agriculture powers Kenyan economy to 5.9pc quarter one growth

The economy recorded the highest first quarter growth in five years, helped by good weather, improved security and continued investment in public infrastructure, according to newly released data.

The Kenya National Bureau of Statistics (KNBS) on Thursday said the economy expanded by 5.9 per cent in the first three months of the year compared to five per cent in the same period last year.

The growth – second only to the 7.6 per cent that was recorded in the first quarter of 2011 – is attributed to growth in all segments of the economy.

The KNBS data shows that agriculture, which accounted for 34 per cent of the total production expanded by 4.8 per cent in the first quarter compared to 2.9 per cent in the previous period.

“Agriculture showed marked improvement in the first quarter, mainly buoyed by considerable growth in value addition for key crops such as tea and horticultural crops,” the KNBS said in a statement

Agriculture employs up to 80 per cent of Kenyan workers in rural areas, feeds majority of citizens and provides raw material for agro-based industry.

The economy has also gained from improved security that has encouraged Kenyans to engage in local tourism and buoyed source markets to lift travel bans.

“The most notable improvement was the rebound in accommodation and food services at 12.1 per cent compared to a contraction of 11.4 per cent during the same quarter in 2015,” the KNBS said.

While accommodation and food services accounted for a paltry one per cent of the first quarter production, improved security may have had a multiplier effect as tourist arrivals grew significantly.

The number of international visitors increased 16.8 per cent to stand at 206,978 between January and March compared to a similar period of 2015, much to the relief of hoteliers.

The hoteliers had earlier cut jobs, slashed pay and closed shop in the wake of 2014 travel alerts issued by American and European governments in response to the then frequent terrorist attacks.

“We are optimistic, things are looking up,” said Mohamed Hersi, the chief executive of Heritage Hotels.

The January-March boom extends to electricity generation, transport and mining segments which also recorded significant growth in the first quarter.

The KNBS data shows electricity generation grew by 8.3 per cent in the first quarter of 2016 from 2,235.43 Kwh in the first quarter of 2015 to 2,241.18 Kwh.

The rainfall-linked hydro production expanded by 26.5 while the capital-intensive geothermal generation grew by 4.4 per cent.

Over the same period, diesel-fired power production declined by 17.5 per cent during the period. The KNBS said: “The decline was mainly due to favourable weather conditions experienced during the quarter that necessitated the scaling down of the more expensive thermal generation in favour of hydro and geothermal generation.”

Sectors such as construction, manufacturing and finance however registered slowed growths in the first quarter.

The construction industry – mainly driven by implementation of government’s flagship projects – expanded by 9.9 per cent which was a slowdown when measured against an expansion of 12.6 per cent in a similar period of 2015.

Similarly, the manufacturing defied drop in international oil prices when it registered a slow growth of 3.6 per cent in the first quarter of 2016 compared to 4.1 per cent in 2015.

“The growth of the sector was partly supported by production of beer and stout but dampened by production of soft drinks as well as wheat and maize flour,” KNBS said.

Other segments that pulled down manufacturing activities are the textiles and clothing which declined by 22.0 and 8.8 per cent, respectively, in the first quarter as well as assembly of motor vehicles which dropped by 35.3 per cent.

Related News

tralac’s Daily News Selection

The selection: Thursday, 30 June 2016

Later today: the release of South Africa’s May 2016 trade statistics. The ‘Bloomberg consensus’ is for another trade surplus in May, at R4.1bn, from R0.4bn in April. Standard Bank, however, expects a trade balance of R10.1bn.

Today, in Abidjan: the launch of the ACBF’s 2017-2021 Strategic Plan, Pledging Conference

The ACBF’s new five-year strategy will focus on four ambitious and mutually supportive strategic pillars. Strategic Pillar 1 - Enabling effective delivery of continental development priorities: this pillar targets the capacity development of pan-African institutions - the African Union, NEPAD Agency, and African Peer Review Mechanism - and of regional economic communities to increase their delivery capacities. The expected result by 2021 is increasing the delivery capacities of institutions leading Africa’s transformational agenda. To support these institutions, ACBF will achieve three intermediate results: i) improve its provision of integrated capacity development advisory services to pan-African institutions and RECs, ii) support pan-African institutions and RECs in prioritizing capacity development in their intervention strategies, iii) increase the effectiveness of pan-African institutions and RECs in implementing the continental transformation agenda. [Strategy synopsis, pdf]

Beyond AGOA: the 2016 Biennial Report on the implementation of the African Growth and Opportunity Act (USTR)

The US Trade Representative presented to Congress (Wednesday) a comprehensive report on implementation of the African Growth and Opportunity Act – the cornerstone of the US trade and investment relationship with sub-Saharan Africa. The report is statutorily mandated by Congress under the Trade Preferences Extension Act of 2015 to be submitted one year following the enactment of the Act, and biennially thereafter. Even as the United States works with African partners to maximize AGOA utilization, we are examining ways to enhance the US-Africa trade relationship beyond AGOA. Some countries – including Kenya and Mauritius – have expressed an interest in establishing more mature, long term trade relationships with the United States, including by entering into free trade agreements. The issue of a US-Africa trade relationship that expands beyond AGOA will be a focus of the AGOA Forum in September 2016 and our engagement with sub-Saharan African trading partners going forward. Table of contents (pdf):

Chapter I: The US - Sub-Saharan Africa trade and investment relationships

Chapter II: Country reports

Chapter III: Status of regional integration

Chapter IV: Status of trade capacity building assistance to Sub-Saharan Africa

Chapter V: Potential Free Trade Agreements with Sub-Saharan Africa

USTR report on impact of trade preferences on poverty and hunger

The report’s major conclusions (include): i) Economic research and available data also suggest that preferences are only one element in the larger set of trade policies that help promote development. Addressing supply-side constraints including slow and expensive port transits, costly telecommunications, the time and expense of managing overly complicated trade paperwork, inefficient internal transport and logistics bottlenecks, and other challenges is essential to success in trade, and tariff preferences cannot substitute for policy reforms in these other areas; ii) Preferences are of crucial importance to a number of least-developed countries which do not as yet have the capacity to negotiate and implement comprehensive FTAs.

IGAD, USAID sign agreement to strengthen collaboration on regional development (IGAD)

The activities supported by USAID are in the categories of Agriculture, Natural Resources and Environment; Economic Cooperation, Integration and Social Development; Peace and Security and Corporate Development Services within the IGAD region for the promotion of sustainable economic growth and resilience as well as improvement of management of risks in transcended borders in the IGAD region. The $17m is to strengthen the collaboration relationship and partnership between the two organizations, to outline a common understanding of how the U.S government supports IGAD priorities and to implement programs that will contribute to common goals of USAID and IGAD over the next 5 years. Ms Karen Freeman (USAID Mission Director of Kenya and East Africa) acknowledged the efforts that IGAD has made for some of the region‘s most remote regions to access trade, adding that this has not only promoted prosperity in those regions, but has also delivered better livelihoods to their communities thus putting IGAD in the forefront as a model for Integration as a partner and driver towards the achievements of USAID’s strategy in Africa.

East Africa Business Council in new push for countries to sign EPAs (New Times)

Further delay in signing the Economic Partnership Agreement will hamper East African Community partner states’ export to the European Union market, the East African Business Council (EABC) chief executive, Lilian Awinja, has said. EAC partner states earlier proposed that EPA signing ceremony be held in the first week of August, but the apex body of business associations of the private sector and corporates from EAC countries now recommends July 18, as an apt moment to take advantage of the EU Commissioner for Trade, who will be in Nairobi attending an upcoming United Nations Conference on Trade and Development conference. The EABC expectations are that all EAC partner states’ Ministers of Trade will also attend the conference in Nairobi in July and, therefore, be able to sign the EAC-EU-EPA on the same date to project the region as a functional Customs Union.

Improving the trading environment across the EAC: institutionalising the TIR initiative (Commonwealth)

Through the Export Promotion Council of Kenya, the Government of Kenya requested technical assistance from the Commonwealth Secretariat to develop a strategic action plan to institutionalise the Convention on International Transport of Goods Under Cover of TIR Carnets (TIR Convention), an international transit system. TIR appears to be feasible in Kenya and would also be beneficial to the region if implemented. Transit times and border procedures for exports out of the region via the coastal ports would be reduced thereby lowering costs and increasing export competitiveness. Institutionalising the TIR initiative in Kenya will likely prompt neighbouring countries, particularly EAC and Northern Corridor Member States, to also consider ratification. It is anticipated that the EAC Secretariat will recognise the advantages of the system for exports through transit countries to African continental and global destinations. [The analyst, Sujeevan Perera, is an adviser in the Trade Division, Commonwealth Secretariat]

Electronic SPS certification conference: presentations (Standards and Trade Development Facility, WTO)

The seminar, 28 June, i) reviewed existing international SPS and electronic data exchange standards and considered outstanding standard-setting gaps; ii) reviewed relevant initiatives aiming to streamline the automation of trade procedures and facilitate implementation of paperless trade to identify synergies and good practice; and iii) presented countries’ experiences in the area of exchange of electronic SPS certificates, shared lessons learned, discussed challenges faced and considered capacity building needs for developing countries. [Profiled presentation (pdf): 'Lessons learned from implementation of electronic phytosanitary certification in Kenya']

Geneva Ministerial Declaration: fifth meeting of trade ministers of Landlocked Developing Countries

We urge those LLDCs, which have not done so, to ratify the Multilateral Agreement on the establishment of the International Think Tank for the LLDCs in order to bring the Think Tank to full operation, and invite the Office of the High Representative and relevant organizations of the United Nations system, Member States, including development partners, and relevant international and regional organizations to support the think tank, as it will play an important role in enhancing the analytical capability of LLDCs and provide home-grown research to cater for our specific needs.

South Africa: Understanding the poultry trade (IOL)

Not many countries are involved in poultry trade and not all that many are the recipients of that trade. This is not truly a global production problem, but it is very much a problem for all the developing world markets as most trade is directed at these developing markets. As I will explain below, this impacts the existing industries in those countries and inhibits the establishment and growth of local poultry industries. [Kevin Lovell is chief executive of the SA Poultry Association] [Biosecurity key to ASF control in South Africa]

Uganda-Tanzania oil pipeline project now to begin 2017 (IPPMedia)

TPDC managing director Dr James Mataragio told The Guardian in an exclusive interview on Monday that prerequisite technical and commercial agreements for the $4bn project are in the process of being prepared and everything should be ready by December this year. The much-awaited pipeline project to be implemented by TPDC will enable Uganda to start exporting its sizeable reserves of crude oil via the port of Tanga in Tanzania by 2020. According to Mataragio, two particular documents - the “host government agreement” and “inter-governmental agreement” - will outline the roles of both countries in relation to the project. The pipeline company (PipeCo), whose registration is expected to be completed by the end of the year, will comprise the two governments (Uganda and Tanzania) and the three international oil companies with stakes in the project - Total SA (France), Tullow Oil (UK), and Cnooc Ltd (China – as the main shareholders, he explained. [Uganda to secure Shs8 trillion loan for Malaba-Kampala SGR route]

President Kenyatta wraps up his visit to Botswana (Daily Nation)

President Uhuru Kenyatta has wrapped up his three day State visit to Botswana where he pushed for a review of regulations that limited business and employment opportunities between Kenya and the southern African country. Top on the agenda during the talks was a review of immigration rules that made the obtaining of work permits restrictive. President Khama agreed to review the rules so that Kenyans can continue accessing employment and work opportunities in the country. Kenya and Botswana have agreed to collaborate to develop Kenya’s mining sector where the southern African country’s experience will help.

Botswana: Diamond sales fall again in June (Mmegi)

De Beers yesterday reported that the June sight sales fell for the second consecutive time to $560 million, which the miner regards as a typically slower period of the year. Although the decline in fifth sight sale represented a second straight downward trend, diamond sales this year are still significantly higher than in 2015, a development that would be a boost for Botswana.

Rail the key to unlock growth in Africa (Business Day)

We need to build on that proven maintenance capacity by devising innovative ways to control the value chain. This is where African governments need to make use of regulation. Supply chain industrialisation and growth must be the area of focus; policies must maximise local value-add, and spillovers from foreign direct investment, as well as tackle the fickleness of original equipment manufacturers. The nexus between global industrial networks and African economic growth must not be lost due to inability to control the supply chain of rail investments. [The author, Bongani Mankewu, is CEO of the Rail Road Association of SA]

Innovation in electronic payment adoption: the case of small retailers (WEF/World Bank)