Search News Results

UK firms could get trade boost with rapidly developing African nations thanks to Brexit

Brexit could be the ideal time for UK companies to begin trading with Africa, particularly Ethiopia, and opportunities should be seized upon, according to experts.

Free of the European Union (EU) framework, post-Britain Brexit is set to give Africa a fresh opportunity to negotiate future trade and cultural deals from a position of strength.

Speaking to Express.co.uk, African social and political commentator, Levi Kabwato, said: “A weak pound is good for Africa as it strengthens its negotiation power at the table, that is a good thing.

“Also the UK can get into direct agreements with countries of its choice without having to engage within the EU framework. So it’s a win-win situation for both.”

This comes as more British companies are choosing to invest in Ethiopia, which also boasts the cheapest electricity in the world. The Ethiopian Embassy has named Diageo, Unilever, Heineken and Tesco as some of the companies investing in the prosperous African country.

UK leather company, Pittards, has been trading in Ethiopia for a century and has invested there for 11 years as the sheep in the African nation are well-suited to make gloves for them.

The company’s CEO, Reg Hankey, said: “With a weaker pound, we can capitalise on it and we can export more. We have five factories in Ethiopia employing 1,700 people and hope to employ 5,000 people in five years.

“We hope that many other retailers see Ethiopia as a potential supply source. The fact that Brexit has happened is making everyone consider what is going on and thinking about changing their supply chains. The uncertainty makes companies look at what else there is.

“There is opportunity in Africa and retailers should consider it.”

Mr Hankey said that there is a time advantage to trade with Africa compared with other places as the continent has a similar time zone to the UK and English is widely spoken.

The Ethiopian Embassy has cited the country as a good place to invest as the economy is growing, the population is the second biggest in Africa, the health system has improved, corruption levels are low and there is a growing middle class.

Press officer at the embassy, Gail Warden, added: “People are realising that there are real investment opportunities there.”

Foreign Secretary Philip Hammond visited Ethiopia weeks before the monumental Brexit vote to discuss ways of strengthening economic ties.

Head of G10 Research at Standard Advisory London, Steve Barrow, has said that any trade deals with Africa would be re-negotiated on the same terms following Brexit.

He said: “They’re not going to be whacking big tariffs on imported Kenyan roses, for example.”

Although Mr Kabwato said that aid initiatives will suffer following Brexit, he said: “Less aid is a good thing for Africa, it will force us to become more innovative and less dependent.”

Karen Taylor, the CEO of the Business Council for Africa, which supports 400 businesses in Africa, said: “Here at the Business Council for Africa, we are working closely with our partners in the UK Government, Europe and the private sector to ensure that building and deepening business relationships with Africa remains a priority in the post-referendum environment, irrespective of whether these relationships are developed on a bilateral or multilateral basis.

“We expect that there will be a period of uncertainty whilst the UK’s political leadership begins to address the enormous task ahead both at home and abroad. We are encouraged by the ongoing support being provided to UK businesses in Africa by our embassies, High Commissions and Prime Minister’s Trade Envoys.

“We very much hope that this support will continue over the coming months and years ahead.”

In recent years, Ethiopia has attracted investment from France for wind power, Iceland for Geothermal power and Italy for Hydroelectrics.

A spokesman for the Foreign and Commonwealth Office said: “While the nature of the UK’s relationship with the EU is still to be determined, we will want the strongest possible economic links with key partners across the world.

“Ethiopia remains a very valuable partner for the UK and we hope that this relationship will continue to go from strength to strength. Our trade and investment relationship is already well established; we currently have around 200 British companies operating in Ethiopia and the UK is the largest foreign investor in the country’s food and beverage industry.”

Related News

New report finds that stronger bridge between science and policies is needed to achieve sustainable development goals

Understanding of the scientific basis for action will be needed to achieve the ambitious and transformative goals of the 2030 Sustainable Development Agenda, according to a new report issued by the United Nations on 12 July 2016 during the High-level Political Forum on Sustainable Development.

According to the Global Sustainable Development Report 2016, key elements of the 2030 Agenda – such as what it will take to ensure that no one will be left behind – have yet to be thoroughly scientifically researched. The Report finds that the new Agenda requires asking different questions, many that have not yet been answered by the research.

The Report, an assessment of a broad array of scientific literature pertaining to the sustainable development agenda, was prepared by the UN Department of Economic and Social Affairs and draws on the technical expertise of 245 scientist and experts.

But the Report concluded that “if no one is to be left behind in 2030, the notion of inclusiveness cannot be treated as an afterthought. Rather, it should be an integral part of institution design and functioning; of research and development, and of infrastructure planning and development, to mention only topics covered in this report.”

UN Under-Secretary-General for Economic Wu Hongbo said the GSDR “underscores the importance of preserving a window for the interaction between science and policy at the High Level Political Forum.” He added, “This was one of the ground breaking innovations from Rio+20. Science is needed more than ever to inform the implementation of the ambitious new Agenda. In turn, science needs to be responsive to the questions that this new Agenda puts forward. There is need for dialogue, and the HLPF should remain a central platform for such dialogue.

“To ensure that no one is left behind, the Report found that it is necessary to determine who exactly is being left behind – often thought of as people affected by poverty, a lack of inclusiveness, discrimination and inequality. It is important to take into account the dynamic nature of deprivation and inequality; in this respect, preventive policies are critical to ensure that new people or groups do not fall behind at the same time as others escape poverty and deprivation.”

According to the Report, whether particular strategies succeed in reaching those left behind depend on many factors, from country-specific circumstances, to their design, targeting methods and practical implementation. Examples of interventions reviewed for the report that aim to reach the furthest behind first include targeting those suffering the most from stunting, area-based interventions targeting the poorest locations, and strategies to provide shelter for homeless people.

The Report also explores an extensive amount of scientific research on the interlinkages between infrastructure, inequality and resilience, finding possible links between infrastructure and inequality, as well as on how people’s resilience is affected separately by infrastructure resilience and by inequality.

“As in any nexus, harnessing synergies and addressing trade-offs is critical for policy-making. The research reviewed for the report emphasizes that a focus on both efficiency and equity is needed to harness the synergies between infrastructure, inequality and resilience.”

Other issues that the Report investigated include the role of technology for the achievement of the Sustainable Development Goals, which is essential for achieving the Goals, and the need for inclusive institutions for sustainable development.

Related News

Ecobank names SSA investment winners

Ecobank Research has identified the top 5 destinations in Sub-Saharan Africa which, despite market volatility and the fall in commodity prices, provide good opportunities for investment.

Côte d’Ivoire, Kenya, Ghana, Senegal and Ethiopia top the list.

“Our priority was to select countries that have a good track record. You can have a country that has 15% growth one year – but it might be just because of a single mining project – and then three years down the line, it’s in a mess again,” Edward George, the bank’s head of group research, tells GTR.

When selecting the top-performing countries, the first step was to exclude what George calls the “bad boys” of Africa (Nigeria, South Africa and Angola). “There has been way too much negative press out there about Africa – certainly in the first half of this year. And if you look at these three countries, you would believe that. They’re all suffering dramatic slowing in growth in response to slumping oil and metals prices, as well as some local factors,” he explains.

As such, although these countries represent the three biggest economies in Africa, they have been omitted from the list of top investment destinations. “I’m not suggesting you totally discount these three countries. But if you want to start – or increase – your investment in Africa at this precise moment, we would not recommend South Africa, Nigeria and Angola as your top priorities,” he adds.

Country profiles on these – and all Sub-Saharan nations – are included in the recently-launched fourth edition of Ecobank’s Middle Africa (FICC) Guidebook 2016.

The guidebook is intended as a reference tool for investors interested in doing business in Africa. “The problem with information about Sub-Saharan Africa is that it’s very fragmented, and as a pan-African bank, we wanted to demonstrate the depth and spread of our local knowledge,” says George.

“The guidebook has two primary uses: first, it provides an overview of the region, what the key economies are, what you need to understand about the key sectors; and second there is a detailed country-by-country guide of 41 markets in Sub-Saharan Africa,” he explains.

Côte d’Ivoire and Kenya

George identifies Côte d’Ivoire and Kenya as his top picks for investment in the region because of their political stability and domination of intra-regional trade flows.

“The more intra-regional trade countries engage in, the more they spread their economic relationships, and the less susceptible they are to sudden swings in a particular commodity or market,” he says, lauding the two countries’ diversity of commodities and services: Côte d’Ivoire is the world’s largest producer and grinder of cocoa and West Africa’s leading exporter of palm oil, rubber and cashew nuts, while Kenya is Africa’s largest exporter of horticultural goods, tea and coffee, and is a major processing hub for food and palm oil products. “They have not been negatively affected, as has Nigeria for example, by the slump in oil prices,” George explains.

What’s more, over 40% of Côte d’Ivoire and Kenya’s trade flows are with other African countries – almost three times the average for African countries for intra-regional trade. “However you’re investing in these countries, you’re doing so in markets which are growing strongly: they have the rule of law, strong government, and a vast array of different means of making money. There’s a lot of opportunity,” says George.

The following factors assisted Ecobank Research in its decision-making process for the remaining three countries:

Ghana: economy has turned a corner, but there is still work to do

“Since the start of the IMF programme Ghana has made significant progress with controlling public spending, curbing inflation and stabilising the currency. After the oil-fuelled boom gave way to economic slump, real GDP growth has started to regain pace amidst an improving investment environment.”

Senegal: under the radar

“Senegal’s real GDP growth, while not stellar, has been gathering pace since 2012. The CFA Franc’s peg to the Euro has kept inflation low, while the fiscal deficit is improving.

“Senegal is a major intra-regional trader, with its port at Dakar acting as an entry point for goods and services going into and out of the Sahel.”

Ethiopia: the long-term play

“Although Ethiopia’s annual growth rate has fallen from over 10% to around 6% now, CAGR remained at over 20% in 2011-15, around double the rate of Kenya & Tanzania.

“Ethiopia has one of the highest rates of investment of any country in Africa.

“It is Africa’s largest producer and consumer of coffee, as well as being the region’s largest wheat producer.

“Ethiopia and Kenya are Africa’s two largest exporters of vegetables, cut flowers and live plants to world markets.

“The government has strong control over all sectors of the economy, but is opening up new sectors to investment.”

» Download: Middle Africa FICC Guidebook 2016: Fixed Income, Currency and Commodities – SADC (PDF, 7.11 MB)

Related News

tralac’s Daily News Selection

The selection: Tuesday, 12 July 2016

The SADC Heads of State and Government Summit will take place in Swaziland, 30-31 August. The theme: ‘Resource mobilization for investment in sustainable energy infrastructure for an inclusive SADC’

AU Kigali Summit: 32nd Ordinary Session of the PRC opens, documentation

Dr Celestin Monga has been appointed as the AfDB’s Chief Economist and Vice President, Economic Governance and Knowledge Management

Featured interactive chart: The world’s youngest populations are in Africa (World Bank)

Structural transformation in Africa: a historical view (World Bank)

Focusing on African economies, the paper presents a country-by-country historical analysis of structural change over the past four decades. Given the varied patterns and trends in structural change across African countries, it is difficult to characterize structural change from a single, continent-wide perspective. Some countries saw an early transition of labour out of agriculture, with manufacturing absorbing this labour in the decades prior to the 1990s, while another group of countries saw a later transition out of agriculture, where the services sector played a large role in labour reallocations in the 1990s and 2000s. Finally, the paper provides a country-by-country structural transformation scorecard to assess patterns of structural change in jobs and growth. [The authors: Maria Enache, Ejaz Ghani, Stephen O’Connell]

G20 Trade Ministers’ Statement, Annexures (Ministry of Commerce, China)

To help address the global trade slowdown, we agree to improve global trade governance and remain committed to an open global economy, and will further work towards trade liberalization and facilitation. We endorse the G20 Strategy for Global Trade Growth (Annex II). Under the strategy, we will lead by example to lower trade costs, harness trade and investment policy coherence, boost trade in services, enhance trade finance, promote e-commerce development, and address trade and development. We recognize that these activities, by promoting trade opening and integration and supporting measures for economic diversification and industrial upgrading will contribute to global prosperity and sustainable development. [G20 Guiding Principles for global investment policy making]

Civil Society 20 China 2016: communiqué

We, representatives from 54 countries and regions attending the Civil Society 20 (C20) China 2016, gathered in Qingdao, China on 5-6 July for candid and in-depth discussions on the theme of "Poverty eradication, green development, and innovation: role of civil society". We share the view that, the world economy currently remains sluggish and growth lackluster; major economies lack sufficient coordination in policies and develop on different tracks; in some countries, inequality and imbalance in all their forms are increasingly prominent as unemployment rates remain high.

Investment Climate Statements for 2016 (Bureau of Economic and Business Affairs, US State Department)

The Investment Climate Statements include examples of countries and economies expanding openness to foreign investment and investor protections, as well as challenges and barriers that may exist. Topics covered for each country and economy include: openness to investment, legal and regulatory systems, dispute resolution, intellectual property rights, transparency, performance requirements, the role of state-owned enterprises, responsible business conduct, and corruption, among others. The Investment Climate Statements and related surveys of our posts highlight a variety of policies and practices that can negatively impact the environment for cross-border investment, including: rules on market access or operation and capacity and governance issues. [Uganda: Misty politics hampers trade – US (Daily Monitor]

Daniel Mminele: 'The role of BRICS in the global economy' (SA Reserve Bank)

This (topic) may have been a much easier topic a few years ago when the successes of the BRICS economies far overshadowed their weaknesses. As the challenges facing the BRICS economies have mounted, there are now many question marks over the economic power of the BRICS grouping and the ability to realistically challenge and change the global economic order to one which is more representative and fair. Indeed, BRICS is not alone in the many challenges that it faces. Both advanced and emerging economies have slowed with each facing their own set of dynamics adversely impacting growth and which inter alia require bold actions in the implementation of much needed structural reforms.[The author is Deputy Governor at the SARB. Speech delivered to the Bundesbank Regional Office] [What's going on in Europe? A view from the Deutsche Bundesbank]

Starting tomorrow, in Dakar: ECOWAS workshop on WTO’s Dispute Settlement System

ECOWAS, in line with its vision of regional economic integration, will hold a workshop, 13-15 July, in collaboration with DFID’s Trade Advocacy Fund and GIZ on identifying and resolving trade concerns that affect Member States in the context of the WTO legal system. The workshop will also introduce the Advisory Centre on WTO Law, which provides legal support to Developing and Least Developed countries in defending their legal interests in the WTO legal system.

COMESA launches virtual trade facilitation system in DR Congo

COMESA has launched the COMESA Virtual Trade Facilitation System in the DRC. The launch was conducted on the Matadi-Kinshasa Corridor which has traffic volumes of more than 1000 trucks in a month. CVTFS is an electronic system developed by COMESA not only for monitoring consignments along different transport corridors but also for integrating other COMESA trade facilitation instruments on one online platform. It constitutes a Single Regional Window that connects all Customs Offices in a transit corridor from the office of Customs, at the commencement of a journey, to the Customs office of destination. As a Single Regional Window, all customs administrations in different countries are able in real time to monitor the movement of trucks and cargo. “I look forward to the eventual rolling out of the CVFTS in the Lubumbashi to Dar es Salaam Corridor, the Central Corridor and Northern Corridor” said Director General of Excise Duty and Customs, Mr Deo Magera.

SADC: Failure to implement hampers regional integration (Mmegi)

Botswana's Investment, Trade and Industry minister, Vincent Seretse, has expressed concern at the failure by some SADC member states to implement the 15-point action matrix, saying it hampers deeper regional integration. The 15-point action matrix focuses on the review of rules of origin, completion of tariff phase downs, removal of non-tariff barriers, and facilitation or development of a mechanism to assist those member states that are not yet in the Free Trade Area to participate therein. According to Seretse, the need to finalise the trade in services negotiations has become paramount in view of SADC’s efforts to industrialise as a region. “We all know that access to cheaper services inputs is a key factor in building competitiveness of our industrial sector,” he said.

Mozambique: Providing information about trade and transport fees (SPEED)

The assignment objective was to develop communication content to enhance knowledge and information on due trade and transport related fees in Mozambique, for incoming trucks and commercial vehicles at the border port. The goal was to support the enforcement of good practice in cross-border trade in the country, curb petty corruption and reduce instances for small extortions on the main trading routes. This is expected to contribute to improve cross border trade. [Various campaign downloads, report]

Swaziland leads in cross-border trade facilitation (COMESA)

Swaziland has been named top in Africa in the management and facilitation of the Cross Border Trade, dubbed the Big Bang. It is currently ranked number 30 in the world. This is according to the World Bank, Investor Road Map rating on trading across borders. This was revealed during the 2nd Steering Committee meeting for the Automated System for Customs Data (ASYCUDA) that took place at the Royal Swazi Sun Hotel, in Ezulwini, Swaziland on 4th July 2016. The meeting brought together members of the steering committee drawn from the Swaziland Revenue Authority, the Ministries in charge of Commerce and International Trade, Finance and Economic planning.

Zimbabwe digs in heels over imports (IOL)

The country’s industry minister, Mike Bimha, however, said yesterday that the import restrictions would be reviewed, although at the moment “there is no room for reversing” the new measures. “It will take long to evaluate the impact of the new measures; we still have to give time to roll out. The private sector has been calling for this for a long time and how can you have a rethink when you have come up with a policy that supports your industry,” Bimha said. But Zimbabwe has softened on the new regulations. [SA Investment and Trade Initiative to Zimbabwe, 7-11 November]

Uganda: Trade minister outlines her 2021 Agenda (EA Business Week)

The newly reappointed Minister of Trade, Industry and Cooperatives, Amelia Kyambadde has clearly set out the agenda and areas of focus for her ministry in the period 2016-2021. Kyambadde said going forward, the priority for MTIC will include among others, expeditious completion of bills, policies and strategies under development such as Uganda Export Strategy enforcement, evaluating performance of Agencies. [Middle-income status not attainable with current growth, says NPA boss (Daily Monitor)]

SADC’s Regional appeal for humanitarian and recovery support (SADC)

The SADC Chairperson, Lt. General Dr Seretse Khama Ian Khama, President of Botswana will this month declare a Regional Disaster and launch a Regional Appeal for Humanitarian and Recovery Support (pdf) amounting to US$2.7bn. The Appeal will be a formal request to the international community to provide assistance to affected Member States. Five Member States, Lesotho, Malawi, Namibia, Swaziland and Zimbabwe have already declared national drought emergencies. South Africa has declared a drought emergency in 8 of the country's 9 provinces, while Mozambique declared a 90-day institutional red alert for some southern and central areas. [Various downloads available]

Farm input subsidy programmes: a benefit for, or the betrayal of, SADC’s small-scale farmers? (pdf, African Centre for Biodiversity)

This paper reviews the farm input subsidy programmes within countries belonging to SADC, to ascertain whether input subsidies have benefited small-scale farmers, have increased food security at the household and national levels, and have improved the incomes of small-scale farmers.

South Africa: Labour market dynamics and inequality (IMF)

Next we examine the role of unemployment in explaining the high levels of inequality in South Africa, using data from the third wave of the National Income Dynamics Study (NIDS) conducted in 2012. Our analysis (pdf) suggests that reducing unemployment by 10 percentage points would lead to a fall in the Gini coefficient from 0.665 to 0.645. This may appear small, but to achieve a similar reduction in Gini solely through fiscal transfers would require an increase in transfers by about 40% (equivalent to 3.3% of GDP in 2012 or about 11.1% of government expenditure). Therefore, without progress on reducing unemployment, reduction in inequality may be difficult to achieve through fiscal transfers alone. [The athors: Rahul Anand, Siddharth Kothari, Naresh Kumar]

Botswana: Services sector anchors economic rebound (Mmegi)

The domestic economy grew by 2.8% in the first quarter of 2016, with growth in the services sector outweighing the continued decline in mining activity. Data released by Statistics Botswana shows that the growth in Real GDP was attributed to real value added of trade, hotels and restaurants, finance and business services and transport and communications, which increased by 5.8, 5.2 and 4.6% respectively. “All other industries recorded positive growth with the exception of agriculture and mining which decreased by 3.1 and 5.6 percent respectively during the quarter under review,” said SB.

Launched: LPI's 30 percent campaign for women’s land ownership (UNECA)

On the eve of the Kigali 27th African Union Summit, the Land Policy Initiative - an initiative of the AUC, ECA and the AfDB - launched a campaign aiming at documented allocation of 30% of land to African Women by 2025. According to Ms Joan Kagwanja, Chief of Land Policy Initiative (LPI), African women have a significant role in agriculture where they contribute more than 60 percent of their labour towards food production, yet a complex set of circumstances constrain their access to and control of land under both customary and statutory realms of land governance and management.

Nepad's Ibrahim Assane Mayaki: 'The condition of women in Africa reveals the sorry state of the human condition on the continent' (WorldPost)

ECOWAS Commission workshop on climate change

Strengthening fish trade information system in Africa: AU-IBAR communique

Enhancing trade and food security in CILSS member states (FAO)

The trampling of African elephants: a matter of East, Central and North Africa versus SADC (Southern Times)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

G20 Trade Ministers’ Meeting Statement – Shanghai, July 2016

The Group of 20 (G20) Meeting of Trade Ministers concluded in Shanghai, China on 10 July 2016. Ministers endorsed the central role of the WTO in global trade governance and reiterated their support in further strengthening its functioning. Along with the G20 Trade Ministers’ Statement, the G20 Strategy for Global Trade Growth and G20 Guiding Principles for Global Investment Policymaking were also endorsed.

G20 Trade Ministers’ Statement

1. We, the trade ministers of the G20, met on 9-10 July 2016 in Shanghai, China under the chairmanship of H.E. Mr. Gao Hucheng, Minister of Commerce of the People’s Republic of China.

2. The global recovery continues, but it remains uneven and falls short of our ambition for strong, sustainable and balanced growth. Downside risks and vulnerabilities persist. We agree that we need to do more to achieve our common objectives for global growth, stability, and shared prosperity. Trade and investment should continue to be important engines of global economic growth and development, generating employment, encouraging innovation and contributing to welfare and inclusive growth.

3. G20 members agree to provide political leadership by acting with determination to promote inclusive, robust and sustainable trade and investment growth, which is integral to achieving our ambition of 2 per cent additional growth by 2018 set by G20 Leaders in Brisbane in 2014.

4. More broadly, we resolve to step up our efforts to better communicate the benefits of trade and investment openness and cooperation to a wider public, recognizing their important contribution to global prosperity and development. We welcome the continuing inputs from relevant international organizations, which have provided strong analytical support to members, and from the B20 and T20.

Strengthening G20 trade and investment mechanism

5. In Antalya, G20 Leaders reaffirmed their strong commitment to better coordinate efforts to reinforce trade and investment, asked Trade Ministers to meet on a regular basis, and agreed on a supporting working group. We welcome the establishment of the G20 Trade and Investment Working Group (TIWG), and endorse its Terms of Reference (Annex I). We encourage officials to make good use of the TIWG to better support Trade Ministers Meetings and to further strengthen G20 trade and investment cooperation.

Promoting global trade growth

6. According to the WTO statistics, global trade growth has slowed significantly since 2008, from an average of over 7 per cent per annum between 1990 and 2008, to less than 3 per cent between 2009 and 2015. 2015 marked the fourth consecutive year with global trade growth below 3 per cent.

7. To help address the global trade slowdown, we agree to improve global trade governance and remain committed to an open global economy, and will further work towards trade liberalization and facilitation. We endorse the G20 Strategy for Global Trade Growth (Annex II). Under the strategy, we will lead by example to lower trade costs, harness trade and investment policy coherence, boost trade in services, enhance trade finance, promote e-commerce development, and address trade and development. We recognize that these activities, by promoting trade opening and integration and supporting measures for economic diversification and industrial upgrading will contribute to global prosperity and sustainable development.

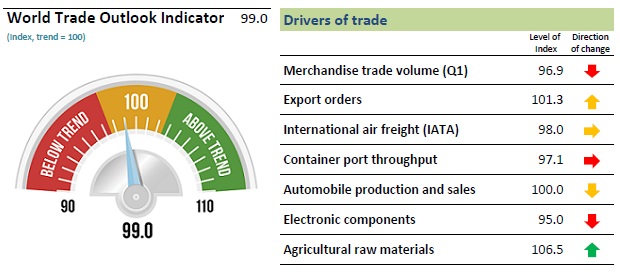

8. We welcome the World Trade Outlook Indicator released by the WTO for the first time at the G20 Trade Ministers Meeting. This can serve as an important leading indicator to help guide the recovery and growth of global trade.

9. The G20 welcomes further joint work by the WTO, World Bank and OECD, in collaboration with other relevant international organisations, within their existing mandates and resources, to measure trade costs and assess the determinants and impacts of those costs, to help improve economic trade modelling and strengthen the evidence base on the link between structural measures, trade, investment and GDP.

10. We recognize that the structural problems, including excess capacity in some industries, exacerbated by a weak global economic recovery and depressed market demand, have caused a negative impact on trade and workers. We recognize that excess capacity in steel and other industries is a global issue which requires collective responses. We also recognize that subsidies and other types of support from governments or government-sponsored institutions can cause market distortions and contribute to global excess capacity and therefore require attention. We commit to enhance communication and cooperation, and take effective steps to address the challenges so as to enhance market function and encourage adjustment. The G20 steelmaking economies will participate in the global community’s actions to address global excess capacity, including by participating in the OECD Steel Committee meeting scheduled for September 8-9, 2016 and discussing the feasibility of forming a Global Forum as a cooperative platform for dialogue and information sharing on global capacity developments and on policies and support measures taken by governments.

Supporting the multilateral trading system

11. We reaffirm the central role of the WTO in today’s global economy. The WTO provides the multilateral framework of rules governing international trade relations, an essential mechanism for preventing and resolving trade disputes, and a forum for addressing trade related issues that impact all WTO members. We remain committed to a rules-based, transparent, non-discriminatory, open and inclusive multilateral trading system and are determined to work together to further strengthen the WTO.

12. We note with concern that despite the G20’s repeated pledges, the stock of restrictive measures affecting trade in goods and services has continued to rise, with about three quarters of the measures recorded since 2008 still in place, and the number of new trade-restrictive measures imposed by G20 economies affecting both goods and services has reached the highest monthly average registered since the WTO began its monitoring exercise in 2009. In response, we recommit to our existing pledge for both standstill and rollback of protectionist measures, and to extend it until the end of 2018. We also commit to improve the track record of notifications related to standstill and rollback efforts, including making better use of existing WTO bodies. We ask the WTO, OECD and UNCTAD to continue, within their respective mandates, their regular reporting on restrictive measures affecting trade in goods and services, and investment.

13. We note the important role that bilateral and regional trade agreements (RTAs) can play in liberalizing trade and in the development of trade rules, while recognizing the need to ensure that they are consistent with the WTO rules and provisions and contribute to a stronger multilateral trading system. We encourage future RTAs by G20 members to be open to accession and include provisions for review and expansion. We appreciate the factual overview of RTAs developments given by the WTO Director-General. We will work with other WTO members towards the transformation of the provisional Transparency Mechanism on RTAs into a permanent one and commit to lead by example in fully fulfilling related notification obligations.

14. In Antalya, Leaders emphasized the importance of the prompt ratification and implementation of the TFA. In the current climate of continuing moderate economic and trade growth, G20 leadership in implementing the TFA could make a significant contribution to lowering trade costs and freeing up world trade. We therefore commit to ratify the TFA by the end of this year and call on other WTO members to do the same. We reaffirm our commitments to providing resources to Trade Facilitation assistance mechanisms designed to help least-developed countries and developing countries most in need in implementing the TFA.

15. Building on the WTO’s successful Bali and Nairobi Ministerial Conferences, we commit to implement rapidly the Bali and Nairobi outcomes. To guide and shape the WTO’s post-Nairobi work, with development at its center, and acknowledging that provisions for special and differential treatment will remain integral, we reaffirm our strong commitment to advance negotiations on the remaining DDA issues as a matter of priority, including all three pillars of agriculture (i.e., market access, domestic support and export competition), non-agricultural market access, services, development, TRIPS and rules We agree to work with all WTO members to set the direction together towards achieving positive outcomes at MC11 and beyond in a balanced, inclusive and transparent way with a sense of urgency and solidarity. We also note that a range of issues, such as those addressed in various RTAs and by the B20, may be of common interest and importance to today's global economy, and thus may be legitimate issues for discussions in the WTO, without prejudice to respective positions relating to possible negotiations in the future. Any decision to launch negotiations multilaterally on such issues would need to be agreed by all Members.

16. G20 members recognize that WTO consistent plurilateral trade agreements with broad participation can play an important role in complementing global liberalization initiatives. In this regard, we note the Information Technology Agreement and its Expansion Agreement, and negotiations on the Trade in Services Agreement and the Environmental Goods Agreement (EGA). WTO members who share the objectives of participants in such plurilateral agreements and negotiations should be encouraged to join. In particular, we note the confirmation by all G20 participants in the expanded Information Technology Agreement of their commitment to implement it without further delay. G20 EGA participants recognize the substantial progress made to date in the negotiations on an Environmental Goods Agreement, and aim to conclude, using best efforts, an ambitious, future-oriented EGA that seeks to eliminate tariffs on a broad range of environmental goods by an EGA Ministerial meeting to be held by the end of 2016, having achieved a landing zone by the G-20 Summit in September in Hangzhou, after finding effective ways to address the core concerns of participants.

Promoting global investment policy cooperation and coordination

17. Global investment is an engine of economic growth and sustainable development. It should contribute to building productive capacity, facilitate wider dissemination of technology, creation of employment and, including through Global Value Chains (GVCs), help to connect economies to world trade. Today, however, global investment flows remain well below pre-crisis peak levels. Policy attention and cooperation is required to put investment growth back on track. We welcome efforts to promote and facilitate international investment to boost economic growth and sustainable development, and agree to take actions in this regard, including promoting investment in Low Income Countries (LICs). This in turn should support a recovery of trade growth. We commit to maintaining a supportive business environment for investors, and agree to collectively play a proactive and catalytic role in this regard.

18. We value discussions on investment promotion and facilitation, and encourage UNCTAD, the World Bank, the OECD and the WTO to advance this work within their respective mandates and work programmes, which could be useful for future consideration by the G20.

19. With the objective of fostering an open, transparent and conducive global policy environment for investment, we endorse the G20 Guiding Principles for Global Investment Policymaking (Annex III). These principles will help promote coherence in national and international policymaking and provide greater predictability and certainty for business to support their investment decisions.

20. We are committed to ensuring that trade, investment and other public policies, at both national and global levels, remain coherent, complementary and mutually reinforcing. We welcome further research and analytical work in UNCTAD, WTO, OECD and the World Bank, in consultation with the IMF, within their existing mandates and resources, to identify ways and means to enhance coherence and complementarity between trade and investment regimes. In this context, we take note of the B20’s recommendation for the WTO Working Group on the Relationship between Trade and Investment to resume its work.

Promoting inclusive and coordinated global value chains

21. We recognize that GVCs, encompassing regional value chains (RVCs), have become an important feature of the global economy, and are important drivers of world trade. We support policies that allow firms of all sizes, including SMEs, in countries of all levels of economic development to participate in and take full advantage of GVCs. In particular, we support policies that encourage greater participation and value addition by business in developing countries, particularly in LICs, in GVCs. We will continue to promote responsible business conduct.

22. G20 members will continue their efforts to enhance capacity building to promote inclusive and coordinated global value chains, and will continue to seek to develop and implement initiatives to assist developing countries, particularly LICs, and SMEs in the areas that matter most to GVCs. Such initiatives could include appropriate infrastructure, technology support, access to credit, supply chain connectivity, agriculture, innovation and e-commerce, skills training and responsible business conduct. Additionally, G20 members with capacity to do so will continue to: assist developing countries’ and SMEs’ ability to adopt and comply with relevant national and international standards, technical regulations, and conformity assessment procedures; facilitate developing country and SME access to information on trade and investment opportunities, including via increased utilization of information technologies; and provide further information that would help them participate in GVCs and move up the value-chain. We welcome further work, within their mandates and resources, by the ITC, OECD, World Bank and other relevant international organizations in this regard.

Toward the Hangzhou Summit

23. In a continuing environment of low global economic growth, the role of the G20 in strengthening trade and investment remains vital. We recommend that G20 Leaders consider these important issues further at the Hangzhou Summit and we look forward to our leaders’ instructions on ways to further intensify G20 efforts on trade and investment. We believe firmly that pursuing robust international trade and investment growth can play a vital part in achieving strong, sustainable and balanced growth.

Annexes

-

Terms of Reference of the G20 Trade and Investment Working Group

-

G20 Strategy for Global Trade Growth

-

G20 Guiding Principles for Global Investment Policymaking

Related News

32nd Ordinary Session of the PRC opens with a call for solidarity, pan-Africanism, self-reliance and independence for a united Africa

The Permanent Representatives Committee (PRC) of the African Union officially opened on 10 July 2016 at the Kigali Convention Center in Rwanda in the presence of H.E Dr Nkosazana Dlamini Zuma, Chairperson of the African Union Commission, H.E Mr. Erastus Mwencha, Deputy Chairperson of the AUC, the AUC Commissioners, the Representatives of the host Government, the UNECA, Heads of AU Organs and Missions abroad, AUC Directors and Officials, the Media and invited guests.

Holding under the theme “2016: African Year of Human Rights with a particular focus on the Rights of Women”, the 32nd Ordinary Session of the PRC opened with a call by H.E. Dr. Nkosazana Dlamini Zuma for solidarity and self-reliance so as to “build an African Union of people”.

The AUC Chairperson expressed satisfaction for the good working relationship between the PRC and the Commission and hoped that such cooperation will lead the continent to “The Africa We Want”. She further urged the Ambassadors to continue to work very closely with the AU Commission for the implementation of the development agenda for the continent.

While welcoming the delegates, the AUC Chairperson also expressed appreciation to the Government and people of Rwanda for the warm welcome extended to her and her delegation and for the good arrangements put in place to ensure a successful organization of the meetings.

“It is always a pleasure to visit the city and to witness the changes, to see how progress is being made in transforming the lives of the African people. We thank the President, the Government of Rwanda and the People for their legendary hospitality and impeccable organization of this Summit.”

The Chairperson further stressed on the symbolic importance for hosting a summit with particular focus on the rights of women in Rwanda, a country which she said, has done everything to make sure that women are treated as equal citizens, where men and women work side by side to ensure the progress of the country and of the continent.

“This Summit is an important milestone in our Union, as it will mark the end of the term of this Commission and the election of a new leadership,” noted Dr. Dlamini Zuma.

She highlighted that the Summit will provide an opportunity to reflect on the journey undertaken by the AUC leadership during the past four years of their mandate, and the role they have played in their respective functions towards taking forward the mission and the vision of the African Union with the view to build an integrated, peaceful and prosperous Africa, driven by its own people and playing a dynamic role in the world arena.

AUC Chairperson reiterated that the continental Organisation has abided by its mission which are informed by the core Pan African values that define the Union: unity, cooperation, solidarity and self-reliance as well as thinking and acting Pan African.

“The issue of unity and cooperation remains critical for all the programmes and initiatives of Agenda 2063,” underlined Dr. Dlamini Zuma. She added that, it would be difficult for Africa to move forward on the transport corridors that connect countries; on the regional energy pools that must power industries and homes; on free movement of people; on regional value chains in beneficiation and manufacturing, without cooperation amongst countries and with the Regional Economic Communities (RECs).

According to the AUC Chairperson, the Permanent Representative of Member States in Addis Ababa are in a unique position, as they are based in the capital of Africa, Addis Ababa where the Commission is headquartered, to advocate for that balance between the national interests and the continental common good. Moreover, the Agenda 2063 programmes and priorities also require a great amount of solidarity, to support initiatives.

H.E. Cherif Mahamat Zene, Chairperson of the PRC and Ambassador of the Republic of Chad to Ethiopia expressed his profound gratitude to the Government and people of Rwanda for their hospitality and for accepting to host the 27th AU Summit. He congratulated the Rwandan government for the progress made through national reconciliation after the 1994 genocide experience.

Amb. Cherif highlighted that the PRC meeting will consider issues related to the activities of the AU Commission including the AU budget for 2017. He commended the PRC Sub-Committee on Administrative, Budgetary and Financial Matters and the Staff of the AUC for preparing the budget in a bid to promote and enhance the efficiency of the Institution. The PRC Chairperson also mentioned that the meeting is expected to deliberate on the reports presented by the Representatives of AU Organs among others.

Amb. Cherif appealed to members of the PRC to be precise and prioritize the discussions to give more consideration to the most important items on the agenda so as to finalise the PRC report to be submitted to the Executive Council scheduled for the 13-14 July 2016 for their consideration and adoption. He called on his peers to reflect further on ways to strengthen the collaboration between the PRC and the Commission urging them to be realistic and action driven so that they can produce a constructive document that will further monitor progress by the Member States.

Representing the host Government at the opening ceremony, Amb. Jeannine Kambanda, Permanent Secretary, Rwanda Ministry of Foreign Affairs and Cooperation, warmly welcomed all the delegates to Rwanda for the 27th AU Summit. She indicated that this Summit is a memorable for Rwandans, and that the people and Government of Rwanda are honored and thankful to the AUC for co-organising this important event.

Amb. Kambanda underlined that this summit will help to further popularize the Africa Agenda 2063 to be assimilated by the people of Rwanda and beyond, therefore creating awareness on AU activities. She reaffirmed the commitment of the Government of Rwandan to enhance integration within the continent as stipulated in Agenda 2063. She concluded by wishing the delegates a fruitful deliberation.

The PRC opening ceremony was marked by a minute of silence in memory of the loss of the Director and Ag. Director of the AUC Strategic Policy Planning, Monitoring and Evaluation and Resource Mobilization (SPPMERM).

Unity and market liberalization will spur African economic growth – Chairperson Dlamini Zuma

Opening up the market for Africa, liberalization of the economies and facilitating free movement of people across the continent are among the identified factors that will drive continent’s economic growth and development.

H.E Dr. Nkosazana Dlamini Zuma the Chairperson of the African Union Commission while addressing the 32nd Ordinary Session of the Permanent Representatives Committee (PRC) of the African Union observed that it was imperative for countries to cooperate and open up the market.

“The world is moving towards mega trading blocks, that all exclude us, and the Doha development round of negotiations have failed to even start. Unless we unite to form our African common market, the little bit of preferential trade we have at the moment, will be further eroded,” she said while addressing the session as the African Union summit kicked off at the level of the PRC in Rwanda.

The AUC Chairperson mentioned that business operators, farmers, and entrepreneurs are still hungry of the free market and this has created a negative impact on the continent’s economic growth since competing at international market is still a challenge.

“If we continue building momentum on the continental free movement of people and on the Continental Free Trade Area it will create better conditions for our traders, farmers, business, entrepreneurs and innovators to invest trade with each other and build Pan African companies and brand,” she further noted.

The AUC Chairperson’s opinion comes in as a strong backing to the yet to be launched African Union (AU) Passport that will create a favorable condition for free movement of African people within the continent.

This flagship project, first agreed upon in 2014, falls squarely within the framework of Africa’s Agenda 2063 and has the specific aim of facilitating free movement of persons, goods, and services around the continent – in order to foster intra-Africa trade, integration, and socio-economic development.

Rwanda continues to be on the forefront of facilitating the movement of people across the continent. In fact, Rwanda has taken a lead in ensuring easing Intra-Africa travel by relaxing visa restrictions. The travelers access the travel visas at the entry point and this has led the country to be on the right track to achieve the dream of visa-free travel for African citizens within their own continent by 2020.

Amb. Jeannine Kambanda, Permanent Secretary, Ministry of Foreign Affairs and Cooperation while giving her opening remarks, mentioned that Summit ponders a huge opportunity to popularize the African Union and its agenda 2063 among member states.

She observed that, by the time the AU Summit ends on 18th July, the understanding of the majority of Rwandans about the African Union will completely be different adding that they will have a deeper knowledge of the African Union and its member states.

Amb Kambanda observed that it was vital for African countries to embark on women empowerment and working together as a tool to foster African democratization.

“I, therefore, stand before you as one of the many proud Rwandan women today who have been given the opportunity to serve their country in a leadership capacity. Thanks to the Leadership of President Paul Kagame for putting woman rights at the center in all we do in Rwanda,” she said.

She added: “Human Rights, especially the Rights of women will remain central as we implement Africa’s Agenda 2063 and that is why I believe you choose this theme.”

Related News

Reserve Bank addresses Germany on future of BRICS

Deputy Governor of the South African Reserve Bank Daniel Mminele said there were many questions that needed to be answered about the future of BRICS as an economic bloc.

Speaking to delegates at the Bundesbank Regional Office in Dusseldorf this week, Mminele explained that the BRICS relationship had become significantly more complicated than it was when the bloc was first established.

When BRICS first became a reality, the economies of the five countries involved were all thriving, to one degree or the other. However, they have since encountered considerable turbulence, which has created a bout of uncertainty.

Mminele does not think it is all doom and gloom though.

“The role of BRICS in the global economy. Admittedly, this may have been a much easier topic a few years ago when the successes of the BRICS economies far overshadowed their weaknesses,” said Mminele.

“As the challenges facing the BRICS economies have mounted, there are now many question marks over the economic power of the BRICS grouping and the ability to realistically challenge and change the global economic order to one which is more representative and fair,” added Mminele.

He highlighted the fact that BRICS was not the only economic bloc which had encountered considerable difficulty during the past 12 to 18 months. The developments in the European Union, for example, have been well documented this year.

“Indeed, BRICS is not alone in the many challenges that it faces. Both advanced and emerging economies have slowed with each facing their own set of dynamics adversely impacting growth and which inter alia require bold actions in the implementation of much needed structural reforms.

“It seems appropriate to be delivering this speech in the heart of Europe, a region which has vast trade linkages with the BRICS economies and where the economic influences are strong.

“I would imagine that developments in Europe and the many challenges that this region has been confronted with lately, have occupied more of your attention than BRICS matters have.

“European developments have certainly occupied the attention of policymakers in BRICS countries since, as we all know, we live in a highly interconnected and interdependent world with significant spill-overs across countries,” added Mminele.

The reality is that, while BRICS does have its own agenda at this juncture, it simply cannot ignore the agenda of Europe and the United Kingdom; such is the nature of the global community we live in.

“South Africa takes a keen interest in Europe, given large trade linkages and therefore significant implications for our economic prospects. The relationship between South Africa and Germany in particular, has been a long and fruitful one and certainly the contribution to South Africa’s development has not been insignificant,” he said.

The automobile sector is probably the most important for both countries.

“Approximately 600 German companies have operations in South Africa, employing over 90,000 workers. Such a presence contributes significantly to employment and skills-building, and no doubt, towards technological advancement in South Africa,” Mminele added.

On the future of BRICS itself, there are many questions that need to be answered, which will have significant implications for both regions and both economies.

“Increased globalization has meant that BRICS has become an important source of global growth and political influence. BRICS economies have grown rapidly with their share of global GDP rising from 11 per cent in 1990 to almost 30 per cent in 2014. BRICS account for over 40 per cent of the world population, hold over US$4 trillion in reserves and account for over 17 per cent of global trade,” he said.

“Financial markets in the BRICS countries have similarly expanded in a rapid manner. For example, in the 20 years until 2010, Brazil’s market capitalization increased from a very low 4 per cent of GDP to 74 per cent, India from 12 per cent to 93 per cent, Russia and China from almost zero to 70 per cent and 81 per cent, respectively. In South Africa, market capitalization has more than doubled from 123 per cent to 278 per cent. According to S&P Global Market Intelligence global bank rankings, banks from these five countries figured among the top 100 banks in the world, with the top 4 banks headquartered in China.

“It therefore comes as no surprise then that these economies became the new engines of global demand. Having been victims of the global financial crisis, and suffering the impact of large and volatile capital flows and what Mohamed El Erian has referred to as “tourist dollars”, the BRICS countries were propelled into a common objective of reforming the international financial and monetary system, with a strong desire to build a more just, and balanced international order that reflects the dynamics of today’s global economy and serves the interests of all in a fair manner. To this end, the five countries in the BRICS community play an important role in the G20, in shaping global economic policy and promoting financial stability.”

“The role of BRICS in the global economy”

Extracts from the address by Deputy Governor Daniel Mminele, 7 July 2016

BRICS and South Africa

The BRIC countries, as the grouping was initially known, admitted South Africa as a member to the club in December 2010. There were many criticisms levelled towards the inclusion of South Africa in this grouping, with the perception that South Africa’s economic size was just too small for it to have any benefits for the BRIC. However, if one considers the country’s large mineral resources; very well developed, deep and sophisticated financial markets; strong institutions and robust and expanding infrastructure programme, then surely South Africa’s presence in this grouping is not misplaced. In addition to South Africa being the only African member of the G20, its inclusion into the BRIC group provides it with a more representative structure and further emphasises the BRIC countries commitment to strengthening their presence and engagement in Africa. 2 Indeed, within the Sub-Saharan Africa (SSA) region, South Africa is the second largest economy, accounting for 21 per cent of SSA GDP. SSA is an important export market, and there are significant financial linkages in terms of foreign direct investment and a strong presence of South African firms in the South African Development Community.

South Africa’s trade with BRIC countries has expanded in recent years, as exports to BRIC countries grew from R20 billion in 2005 (EUR1 billion), to R154 billion (EUR9 billion) in 2013 (although this has since slowed to R147 billion (EUR8.5 billion) in 2015). Imports have similarly increased from R48 billion (EUR2.8 billion) in 2005 to R277 billion (EUR16 billion) in 2015.4 Much of the exports are destined for China, which accounts for 64 per cent of South Africa’s exports to BRIC, followed by India accounting for close to 30 per cent. The bulk of exports to BRIC countries consist of mineral products, although the percentage of mineral products in total exports in China, for example, has declined from levels of close to 80 per cent to 60 per cent in 2015. This most likely reflects to some extent the slowdown in China. In terms of imports from BRIC countries, China accounts for 72 per cent of South Africa’s imports from BRIC, followed by India with approximately 20 per cent. Most of the imports from China relate to machinery products and in India’s case, mineral products. Thus, while trade with BRIC countries has expanded, there has been a slowdown in export growth more recently, with a consequent increase in the trade deficit with BRIC countries.

BRICS in the global context

Increased globalisation has meant that BRICS has become an important source of global growth and political influence. BRICS economies have grown rapidly with their share of global GDP rising from 11 per cent in 1990 to almost 30 per cent in 2014. BRICS account for over 40 per cent of the world population, hold over US$4 trillion in reserves and account for over 17 per cent of global trade. Financial markets in the BRICS countries have similarly expanded in a rapid manner. For example, in the 20 years until 2010, Brazil’s market capitalisation increased from a very low 4 per cent of GDP to 74 per cent, India from 12 per cent to 93 per cent, Russia and China from almost zero to 70 per cent and 81 per cent, respectively. In South Africa, market capitalisation has more than doubled from 123 per cent to 278 per cent. According to S&P Global Market Intelligence global bank rankings, banks from these five countries figured among the top 100 banks in the world, with the top 4 banks headquartered in China.

It therefore comes as no surprise then that these economies became the new engines of global demand. Having been victims of the global financial crisis, and suffering the impact of large and volatile capital flows and what Mohamed El Erian has referred to as “tourist dollars”, the BRICS countries were propelled into a common objective of reforming the international financial and monetary system, with a strong desire to build a more just, and balanced international order that reflects the dynamics of today’s global economy and serves the interests of all in a fair manner. To this end, the five countries in the BRICS community play an important role in the G20, in shaping global economic policy and promoting financial stability.

The future role of BRICS

Following an impressive performance in the aftermath of the global financial crisis, BRICS countries have recently started to slow. In this respect, there seems to be an awful lot of doom and gloom bandied about the BRICS in some quarters. Some have referred to the BRICS bubble bursting, others have noted that BRICS “instead of propelling the global economy into calmer waters, now risk capsizing it” and others question “why the mighty BRICS nations have broken?”

This slowdown has been reflected in a number of areas. Exports from BRICS to developed markets and investments into their respective economies have declined, while the collective contribution to global growth has fallen from a peak of nearly 50 per cent in 2013 to around 36 per cent in 2015. Real GDP growth of BRICS, which was over 8 per cent in 2010 declined to just over 4 per cent in 2015. In addition, the local currencies of BRICS, with the exception of China, has experienced varied levels of volatility following the onset of the global economic crisis.

As Christine Lagarde noted in a recent speech there have been three particular challenges confronting the global economy and also the BRICS countries. First is China’s growth transition and the rebalancing of its economy from industry to services, from exports to domestic markets, and from investment to consumption. In the short run, this will lead to slower growth with spill over effects through trade and lower demand for commodities. Global trade, which fell to 20 per cent below its precrisis trend, was driven by sluggish growth in advanced economies, and the maturation of global value chains which has further reduced the elasticity of trade flows to economic activity and exchange rate changes. Furthermore, higher capital requirements and tightened financial regulations have reduced banks’ willingness to extend trade finance, and the pace of trade liberalization slowed. Secondly, declining commodity prices has placed many commodity-exporting emerging economies under severe stress with very large currency depreciations in some cases and has set back growth in commodity-exporting BRICS. Third, asynchronous monetary policies has contributed to an appreciation of the U.S. dollar, putting considerable strain on emerging market currencies. Meanwhile, net capital flows to BRICS have undergone significant bouts of volatility, which have weighed on investment growth.

Until 2013, the slowdown was predominantly driven by external factors, however, the role of domestic factors has increased in the past two years and have come to the forefront as the predominant forces behind slowing growth in BRICS. This reflects declining potential growth, compounded by a deterioration in fiscal positions of BRICS and political dynamics which have dented confidence and increased pressure.

The question then is, does BRICS still matter and should it occupy so much of our attention? BRICS account for about two-thirds of emerging market GDP. The World Bank has estimated that in the event that growth in BRICS economies fell one percentage point below expectations, this would knock 0.8 percentage points off growth in other emerging markets over a period of two years and reduce global growth by 0.4 percentage points. The effects of a BRICS slowdown on other emerging markets and the global economy are significantly worse if one assumes that financial sector turbulence will also accompany the slowdown.8 These effects are a result of unintended knock-on effects, in the form of financial, trade and economic spill-overs. In this context, the BRICS are at an important juncture and the question is how does BRICS emerge from the current dismal conjuncture? It should be noted that the slowdown of BRICS hampers the scope for a speedy recovery of the world economy given the much greater weight of BRICS in the global economy.

As we have heard time and again, a combination of proactive countercyclical policies and structural reforms are needed to reinvigorate domestic economies and economic growth. While the recipe for success are of course not the same for all, the ingredients for success are mostly the same and include inter alia encouraging greater private sector investment, labour market reforms, stronger protection for intellectual property rights, and addressing infrastructure bottlenecks, amongst others. Given the sheer size, vast resources and youthful populations of the BRICS countries, the potential of this grouping for both domestic and global outcomes is beyond question. Indeed, recessions in Brazil and Russia and slower growth in South Africa are expected to bottom out this year, while China may experience only a modest slowdown and India continues to expand at a robust pace.

Conclusion

Let me then conclude by saying that the challenging times we face as the BRICS are by no means unique to us. Indeed, the entire global economy is at a difficult juncture at present. While we may have emerged from the global financial crisis, the recovery has by no means been as robust as one would have liked.

The challenges we face need to be tackled decisively and provide us with the opportunities to implement meaningful reforms, which ultimately can lead to strong, sustainable and balanced growth. Such efforts are well underway. What has been broken can certainly be fixed, and I have no doubt that the BRICS, along with the rest of the global economy, through better co-ordination and collaboration will emerge stronger.

Related News

Increase people’s purchasing power to attract more foreign investors, experts say

Encouraging Rwandans to consume locally-produced goods as well as putting in place strategies that boost people’s purchasing power are crucial in attracting more foreign investors into the country.

According to Tatsuya Narahara, the director for Africa, Middle East and Asia at Mayekawa, a Japanese firm that manufactures construction and mining equipment, increasing local consumption is an essential ingredient that serves as an incentive to woo investors in any given country.

He, however, said boosting local consumption requires investing in the sectors that would help increase the per capita income and purchasing power. Rwanda has for the past two years been encouraging consumption of locally-produced goods under the Made-in-Rwanda campaign.

The initiative aims to help reduce the trade deficit and boost the local manufacturing sector, particularly the small-and-medium enterprises (SMEs).

It also seeks to enhance quality, standards, branding and packaging of local products. The country seeks to raise the per capita income to $1,240 by 2020, up from $644.

Narahara said increasing people’s purchasing power will assure investors of a ready market.

He pointed out that Mayekawa is targeting to increase its presence in Africa, and considers Rwanda as best option.

“We are looking at Africa as a potential market and are ready to work with local investors to expand our presence on the continent,” Narahara said.

He noted that the decision for many investors to commit to the continent is informed by market availability.

According to Japanese experts, low demand and low purchase power on the continent scare away investors, noting that increase in local consumption is what largely developed Japan after the Second World War and trade embargo.

“Therefore, what countries like Rwanda are doing in regard to encouraging local consumption is critical for economic sustainability of the continent as it will attract more investments to Africa,” Narahara said in an interview with The New Times in Osaka, Japan.

According to Yuuichi Itou, the general manager of Komatsu Limited, which produces refrigerators and air conditioners, low purchasing power partly explains the minimal foreign direct investments in Africa.

“Therefore, by championing consumption of locally-make products, Rwanda is helping create a bigger market that will attract more investors to the country,” he said.

Meanwhile, at the sixth Tokyo International Conference on Africa Development in Nairobi, Kenya, scheduled to open on August 27, Rwanda will be looking to market its investment potential to more than 300 Japanese firms expected to attend the summit.

The summit, which will be co-hosted by JICA and the African Union, is expected to bring together over 6,000 trade experts, investors and policy-makers from across Africa, Japan and elsewhere to deliberate on strategies to promote industrial development for sustainable growth.

Many of the investors, according to Noria Maruyama, the director general in charge of African affairs at the Japanese Ministry of Foreign Affairs, will be seeking investment opportunities in countries like Rwanda to widen their presence in Africa.

JICA global chief tips Africa on sustainable industrial development

Africa will host the sixth Tokyo International Conference on Africa Development (TICADVI) in Nairobi, Kenya on August 27, the first such meeting to be held in Africa. The summit will be co-hosted by JICA and the African Union, and is expected to bring together over 6,000 trade experts, investors and policy-makers from Africa, Japan and elsewhere to deliberate on strategies to promote industrial development for sustainable growth.

Prof Shinichi Kitaoka, the global president of the Japan International Cooperation Agency (JICA), discussed the opportunities the TICAD initiative offers to Africa, and what Africa can do to achieve sustainable and inclusive growth with The News Times’ Peterson Tumwebaze in Tokyo, Japan last week:

Africa will host the Tokyo International Conference on Africa Development (TICAD) for the first time. What is the contribution of the initiative toward Africa’s development?

Through the TICAD initiative, we hope to strengthen and foster trade relations with Africa as one of the efforts to support development on the continent. Remember, the world’s stability partly depends on the economic strength of this continent.

Many African countries have sustained high growth rates for a decade, weathering the global financial crisis of 2008 that wrecked havoc on many economies, including the US and Europe. Yet, despite this performance, Africa still faces various economic challenges affecting its growth potential.

The continent, therefore, needs to accelerate the pace of poverty reduction, narrow income gaps, create more jobs, especially for the youth, as well as build infrastructure, and promote intra-regional trade. Reliance on commodity price booms for growth has also emerged as one of the main challenges facing many African countries. Therefore, to address these development challenges, the continent should promote strategies that ensure transformation and build economic resilience.

Therefore, the sixth Tokyo International Conference on Africa Development (TICADVI) in Nairobi, Kenya next month will be seeking ways, including pursuit of industrial development that will help transform and strengthen the resilience of African economies. We are encouraged by the international community’s recognition of the pivotal role industrial development and trade can play in Africa’s development agenda, especially under the Sustainable Development Goals (SDGs) framework.

These targets will enable the continent to achieve inclusive and sustainable industrialisation by 2030 as envisaged under Goal 9 (Build resilient infrastructure, promote inclusive and sustainable industrialisation and foster innovation).

How can Africa achieve these industrialisation targets?

First of all, there is need to increase efforts geared at poverty reduction and narrowing income inequality, particularly by increasing labour productivity. This, however, calls for reallocation of labour and capital from subsistence agriculture and informal service sectors to more productive sectors, like manufacturing.

The second aspect is to create more jobs, especially for the youth. Africa needs to meet growing demand for youth employment. In fact, the IMF estimates that 18 million new jobs need to be created every year in Africa between 2010 and 2035. There are few sectors, besides labour intensive manufacturing, that are capable of absorbing such large numbers of workers.

Thirdly, the continent needs to mitigate the impact of external economic shocks, such as sharp declines in commodity prices, like oil and metals.

The mining sector has been the main driver of Africa’s economic growth over the last decade, but falling commodity prices over the past year have affected growth. Such challenges can be addressed by emphasising economic diversification, as well as promotion of value addition in agriculture, and manufacturing sectors. Therefore, industrialisation will play a big role in helping African countries address these challenges. African policymakers and development partners can pick a leaf from the Asian Tigers’ journey to become industrial powers. Otherwise, TICADVI will be held on African soil is a clear indication of our commitment to fostering development in Africa. Toward TICADVI and beyond, JICA and partners will remain dedicated to working with Africa to turn the continent’s long-term development vision into reality.

TICAD was launched, what is your assessment of the initiative’s performance so far?

Japan launched TICAD in 1993 to promote political dialogue between Africa and development partners through mobilisation of resources for the continent’s development initiatives. Japan was the first country to start dialogue with African countries after the cold war to strengthen economic and bilateral relationships. It was not until we launched TICAD that America and the European countries started similar dialogue with Africa.

At the 5th Tokyo International Conference on African Development in Yokohama in 2013, the Japanese government committed to supporting Africa through stronger public-private partnerships.

Prime Minister Shinzo Abe also announced the African Business Education Initiative for the Youth, a five-year strategic plan to give 1,000 African youths opportunities to study at Japanese universities, and do internships at Japanese enterprises to foster sustainable industrial development on the continent.

The TICADV targeted increasing private sector investments and private capital flow to Africa which has also encouraged more investors to invest in Africa. We hope to continue supporting Africa on its development and industrialisation journey.

Related News

Structural transformation in Africa: a historical view

This paper presents evidence suggesting that the relationship between income and economic structure is shifting over time, with countries across the income distribution uniformly increasing the share of labor in service sectors and an increasingly less stark relationship between manufacturing intensity and gross value added per capita.

The paper then assesses historical patterns of productivity convergence at a more detailed sector disaggregation than has been previously available. The analysis finds suggestive evidence that, at least in recent decades, convergent pressures in services industries are stronger than in manufacturing. Focusing on African economies, the paper presents a country-by-country historical analysis of structural change over the past four decades.

Given the varied patterns and trends in structural change across African countries, it is difficult to characterize structural change from a single, continent-wide perspective. Some countries saw an early transition of labor out of agriculture, with manufacturing absorbing this labor in the decades prior to the 1990s, while another group of countries saw a later transition out of agriculture, where the services sector played a large role in labor reallocations in the 1990s and 2000s.

Finally, the paper provides a country-by-country structural transformation scorecard to assess patterns of structural change in jobs and growth.

Introduction