Search News Results

Scoping report: Improving the perspective for regional trade and investment in West Africa

The key to food security, economic development and stability in the region

Increasing international concern about instability, population pressure, migration and chronic food insecurity in West Africa and growing awareness of the potential of enhanced intraregional trade and investment to contribute to sustainable and inclusive economic development, has prompted a number of development partners including The Netherlands to increase their efforts to support West African integration and cooperation.

Support for regional integration and cooperation in West Africa by The Netherlands fits well within its policy framework for Aid, Trade and Investment and aligns with key Dutch policy objectives to promote sustainable and inclusive economic development and to enhance food security. Furthermore, there is increased interest of Dutch businesses to invest in and trade with West Africa and growing recognition of the opportunities for Dutch businesses, knowledge institutes and civil society to contribute to sustainable economic development in West Africa.

In order for support to regional integration and cooperation in West Africa to be effective and calibrated to the specific needs of the region, there is a need to build a more comprehensive understanding of the diverse and complex regional dynamics and to gain insight into the opportunities and challenges to regional integration in West Africa.

Commissioned by the Food & Business Knowledge Platform, the overall objective of the study underlying this scoping report was to contribute to a more contextualized comprehensive picture of The Netherlands’ government's ongoing cooperation with West Africa and the perspective in terms of policy options for strengthening its effectiveness and coherence by giving more emphasis to the promotion of intraregional trade and investment.

The study has been carried out by a consortium of knowledge institutes comprised of the African Studies Centre Leiden (ASCL), the Agro-economic Research Institute of Wageningen University and Research (LEI-WUR) and the European Centre for Development Policy Management (ECDPM).

In addition to this scoping report, the scoping study has also resulted in an annotated bibliography based on an inventory of literature on regional integration in West Africa, prepared by the Library, Documentation and Information Department of the African Studies Centre Leiden.

Related News

Transport and ICT projects financed by the AfDB in 2015 to create thousands of jobs, increase mobility and improve the lives of millions

The impacts arising from investments made by the African Development Bank Group in 2015 will collectively improve mobility of at least 1.2 million users of public transport, result in employment generation of about 200,000 jobs in the ITC sector and benefit almost 18 million people from improvements in road infrastructure.

These are the findings of the AfDB’s 2015 Annual Report on Transport and Information and communications technology (ICT) released July 1, 2016.

“The expected impacts over the next few years in integrating Africa, boosting agriculture, and facilitating industrialization will be tremendous,” noted Amadou Oumarou, AfDB Director for the Transport and ICT Infrastructure.

The report sharply highlights the Bank’s continued support for the development of efficient transportation and telecommunication infrastructure to promote regional integration, support agriculture development, and facilitate the industrialization of Africa. The publication underscores the Bank’s multi-faceted financing and advisory services in support of Africa’s development.

According to the report, the contribution of transport and ICT as enablers of economic development cannot be overstated. Efficient transport and ICT systems minimize transaction costs, transit times and uncertainties and can facilitate the participation of African countries in agriculture and manufacturing value chains. In addition, transport contribute to improving livelihoods and inclusiveness by providing access to social services and job opportunities. Similarly, investment in ICT support spinoffs in information access, innovation, skills, and job creation.

During the course of 2015, the Bank invested in a total of 17 transport and ICT operations for a value of US $2 billion. Lending was 50% above target mainly due to increased access by African Development Fund (ADF) countries to African Development Bank financing instruments and greater leverage of co-financing facilities such as the Africa Growing Together Fund (AGTF). Roads and highway corridors represented the largest share of the lending. However, the portfolio is gradually being diversified with increased share of investments in other transport modes particularly urban transport, aviation and ports which collectively accounted for at least 30% of total lending.

Investments in regional transport infrastructure continued to feature strongly in the Bank lending, with regional highways linking Brazzaville (Congo) and Yaoundé (Cameroon), and Bamako (Mali) and the port of San Pedro (Côte d’Ivoire) as typical examples of cross-border corridors to promote regional integration and intra-African trade. Additional support to regional integration included the financing of the Central Africa Fiber Optic backbone project and a US $12-million grant to support the Economic Community of Central African States and the Economic Community of West African States to improve regional air transport safety and security in West and Central Africa.

The financing of the Bus Rapid Transit Project in Tanzania re-affirmed the Bank’s involvement in developing sustainable cities and improving the quality of life of people. The project will not only reduce urban congestion and increase mobility and accessibility for city-dwellers but also promote green growth and improve quality of health resulting from reduced emissions.

The US $127 million lending provided for the Nador West Med Port Project in Morocco and the $140-million Sharm El-Sheikh Airport Development project in Egypt strongly signalled Bank’s support for the continent’s industrialisation. The investments are expected to support growth of efficient global value chains and promote competiveness of the countries’ economies.

In support of agriculture, investments in the Tanzania Transport Support Program and Project to Rehabilitate the National Road N°2 and facilitate access to Morphil Island in Senegal aim to provide a catalytic effect in unlocking the agriculture potential of the regions. The road improvements will support efficient movement of agriculture commodities and contribute to reduced post-harvest losses.

The year’s impressive lending added to the Bank’s growing active transport and ICT project portfolio. There are currently 114 transport and ICT projects under implementation in 44 countries valued at more than US $11 billion.

» Download: Transport and ICT Annual Report 2015 (PDF, 4.9 MB)

Related News

EA loses $2bn in generous tax incentives to investors every year

Kenya, Uganda, Tanzania and Rwanda are losing about $2 billion in revenue every year to foreign investors through generous tax incentives.

Tax Justice Network-Africa and ActionAid International figures show Kenya loses $1.1 billion, Tanzania $790 million, Uganda 370 million and Rwanda $176 million in unnecessary tax holidays, capital gains tax allowances and royalty exemptions.

On its part, Burundi lost $52 million to firms or officials who were given tax exemptions to import goods to build infrastructure and instead sold the materials.

TJN-A and ActionAid said policymakers in the region have spoken about revising tax policies but questions abound on how these tax incentives will be revised, costed and phased out, and the government’s resources and expertise to carry out the exercise.

The report by TJN-A and ActionAid titled “Still racing towards the bottom? Corporate tax incentives in East Africa,” reveals tax incentives are fuelling competition for investors and derailing harmonisation of policies, thereby undermining integration.

“Though there have been improvements in recent years in addressing the issue, governments continue to give away domestic resources in tax incentives,” said ActionAid Tanzania’s country director Yaekob Metena.

The report said the real cost of incentives remains hidden in all five EAC countries as there are neither mechanisms nor demands for accountability to reveal the huge revenue losses happening.

Mr Metena said there is a need for a shift in policy as political, financial national and institutional authorities admit tax incentives harmful to revenue mobilisation need to be revised if not altogether eliminated.

Reduce tax incentives

To their credit, East African governments have pledged steps to reduce tax incentives relating to value added tax by increasing tax collection and providing vital extra revenue that can be spent on providing critical services.

“Many leaders are promising to take measures but there is a need for tangible actions to be taken towards that end,” said TJN-A deputy executive director Jason Braganza.

He said the region must improve harmonisation of its tax legislation by ratifying the East African Code of Conduct on Harmful Tax Competition and implementing it at national levels. The code includes the recommendations of the African Union High Level Panel on Illicit Financial Flows, adopted at the AU Summit in January 2015.

The region has to grapple with tax treaties and special economic zones. At the national level, new legislation like VAT laws and tax administration seeks to redress numerous incentives.

Related News

South Africa seeks end to Zimbabwe’s ban on product imports

South African Trade and Industry Minister Rob Davies wants Zimbabwe to reverse a decision to ban imports of goods from the continent’s most-industrialized economy.

“The minister is engaging through SADC structures and in his capacity with his counterparts,” Sidwell Medupe, a spokesman for the department, said by phone on Monday, referring to the Southern African Development Community. “Engagements are still at an early stage. We hope that an amicable solution will be found.”

In June, Zimbabwe announced a ban on imports of many goods, saying the steps are needed to develop local industries. Products banned include cosmetics, cereals, cheese, canned goods and furniture.

South Africa is one of the biggest investors in Zimbabwe and companies including Impala Platinum Holdings Ltd. and Nedbank Group Ltd. own units there. South Africa’s exports to Zimbabwe amounted to 24.8 billion rand ($1.7 billion) in 2014, while imports stood at 2 billion rand, President Jacob Zuma’s office said in a statement last year.

Statement

South African government engages Zimbabwe on the latest trade restrictive measures

The Department of Trade & Industry (the dti) notes with concern the range of trade restrictive measures that the government of Zimbabwe has introduced. These measures include import bans, surcharges, increases in import duties, requirements for import permits and other forms of restrictions that have negative implications on intra-regional trade.

The position of the government of Zimbabwe is that these trade restrictions are necessary to support the development of local industries and to relieve the pressure of economic sanctions, which have led to balance of payments challenges.

The recent ban of imports or requirement for import permits in a number of products such as cosmetics, cereals, coffee creamer, mayonnaise, cheese, canned fruits and vegetables, second hand tyres, iron and steel products, furniture and woven cotton fabrics June 2016 by Zimbabwe is in addition to these previously instituted measures. The adverse impact on South African exporters cannot be underestimated and the dti continues to be responsive to affected exporters and to make representations to the government of Zimbabwe.

At the recent meeting of the Southern Africa Development Community (SADC) Committee of Trade Ministers South Africa and Zimbabwe were requested to report to SADC on the implications of these measures for the coherence of the SADC Trade Protocol.

On behalf of the South African government, Minister of Trade and Industry, Dr Rob Davies has been engaging the Zimbabwean government bilaterally and through the SADC structures to find an amicable solution that is in accordance with Zimbabwe’s obligations of the SADC Protocol on Trade, while at the same time being sensitive to Zimbabwe’s industrial development and balance of payments challenges.

Issued by the Department of Trade and Industry

Related News

tralac’s Daily News Selection

The selection: Friday, 8 July 2016

#UNCTAD14 takes place in Nairobi, 17-22 July: online document repository.

Profiled UNCTAD14 uploads (pdfs): Impact of cotton GVC on Africa and farm gate activities: contribution from the Government of Kenya, Sustainable transportation for the 2030 Agenda: boosting the arteries of global trade

Profiled tweets: @DrTaxs: 7 July: Committee of Ministers of Finance approves an Agreement to operationalize the SADC Development Fund; @martinslabber: SA's trade with the Philippines up 19% between 2015 and 12 months to April 2016. Now at US$241mn.

‘Modi in Africa’ updates: @IndianDiplomacy: Here's the link to the Press Statement of PM @narendramodi during his Mozambique visit. [Commentaries: Gopalkrishna Gandhi: 'What we must learn from Africa' (The Hindu), ASSOCHAM: Investment and capacity building agreements imperative to fructify unity b/w India & Africa, Shannon Ebrahim: 'Modi a wizard of foreign policy' (IOL), Nic Dawes: 'Modi's first visit to South Africa comes as old friendship fades' (Hindustan Times)]

South Africa: 2016 Article IV Consultation report (pdf, IMF)

Box 1 ‘Spillovers from global transitions’: This box explores spillovers from the ongoing global transitions - China’s rebalancing, lower commodity prices, and tighter global financial conditions - on South Africa. The results suggest China’s growth matters more for South Africa than U.S.’ and Europe’s growth, with commodity prices and financing conditions the main transmission channels. The impact of commodity prices is amplified by inter-sectoral linkages. Tighter global financial conditions have a significant impact on South Africa, mainly though bond yields and equity prices. China absorbs 10% of South African exports, the most of any country. More importantly, it plays a key role in determining global demand for South Africa’s commodity exports, which account for 34% of total goods exports (51% including manufactured commodities), and commodities imports including oil, which account for 16% of total goods imports.

Box 2 ‘Outward spillovers to Sub-Saharan Africa’: Past research suggests that, apart from its immediate neighbors, South Africa has limited spillovers to the rest of Africa, but these are likely to have increased. Several studies have shown that South Africa’s growth has limited spillovers on SSA, once global growth is controlled for. However, SSA’s share in South Africa’s imports has more than doubled over the last decade. South African companies in retail, banking, and telecommunications have established large networks in several sub-Saharan African countries. South Africa now represents an important export destination and source of FDI, especially for neighboring countries. South African firms have many subsidiaries in SSA, which could dampen their profitability going forward. About 75% of African subsidiaries are in services, trade, and financial sectors. The 10 firms with the highest number of subsidiaries are some of the top listed companies. While African subsidiaries have contributed to South African corporates’ high profitability in the past decade, the deteriorating performance of SSA could adversely affect profitability.

Article IV companion paper: The impact of China's growth slowdown and lower commodity prices on South Africa (pdf, IMF)

This paper estimates the impact of China’s growth slowdown and the recent large decline in commodity prices on South Africa. It seeks to identify the key channels through which a shock to China’s economy is transmitted to South Africa, as well as the propagation of this shock within the economy.

National Treasury response to IMF analysis (pdf)

National Treasury forecast is more positive compared to the IMF. We recognise, as articulated in the IMF report, that a comprehensive package of structural reforms is necessary to increase growth, create jobs and lower income inequality. An IMF/G20 guiding framework for structural reforms recommends that emerging market economies should focus on fiscal reforms, business regulations, labour market, infrastructure, banking/capital markets and product market regulations. South Africa’s structural reforms implementation package is anchored by the Nine-Point Plan, which entails:

Mozambique sees growth slowing, austerity measures needed (Club of Mozambique)

Mozambique, reeling from a sovereign debt crisis, sees 2016 economic growth slowing to 4.5% from initial forecasts of 7% and needs to bring in austerity measures in an amended budget, Finance Minister Adriano Maleiane said on Thursday. “This means that revenue that we should have will also go down,” the minister told journalists after an extraordinary meeting of the Council of Ministers which approved an amended budget which will be put before parliament on Monday. [Carlos Lopes: Mozambique needs “rapid and spectacular” measures to solve debt problem]

Ethiopia Public Expenditure Review (World Bank, GoE)

“Ethiopia’s investments in key sectors have had a positive impact on poverty reduction, now the key is for the country to develop a more effective budget allocation in order to maximize the returns on investment,” said Carolyn Turk, World Bank Country Director for Ethiopia, Sudan and South Sudan. According to the report, Ethiopia’s investment in infrastructure has increased the country’s road network five-fold, reaching 100,000km in 2015. Investment in education has also helped to increase net primary enrollment from 77.5% in 2006 to 92.6% in 2015, according to the report, and education has been extended from 10 million to more than 23 million students in the past decade. Through smart investments in the health sector and only an additional $5 in per capita health spending, the GoE reduced child mortality by more than half from 72 to 31 per 1,000 between 2005 and 2015. This is a record, as no other country has achieved such results for the same level of spending, the report notes.

Kenya: Trade deficit narrows as car imports drop Sh21bn (Business Daily)

Reduced demand for vehicles and lower fuel prices cut Kenya’s trade deficit 21.4% in the first four months of the year, helping ease pressure on the shilling. Data from the Kenya National Bureau of Statistics shows that in the first four months of this year, the trade deficit stood at Sh246bn compared to Sh314bn in a similar period last year.

Middle Africa FICC Guidebook 2016: fixed income, currency and commodities (pdf, Ecobank)

However, the medium to long term outlook appears good; African governments are likely to accelerate their ambitious investment plans as risks to the global economy subside over the medium- to long-term. Meanwhile, most Middle African banking sectors remain largely insulated from global financial strains due to limited financial integration of Middle Africa’s banking sector into the global system (bar the trade channel). However, improvements in portfolio quality, liquidity, and revenues would be welcome. The overall positive scenario for Middle Africa in 2016 is beset by numerous risks. External factors continue to pose the largest threats to the region as a whole, but domestic risks are more significant in some countries. Although nearly all countries grew in 2015, some were adversely affected by weakness in the eurozone. Currency pegs to the euro and/or strong trade links to Europe highlight some of the direct links that will remain a major concern for the continent in 2016. Moreover, weak global growth is likely to moderate growth in Middle Africa’s export sector, which in turn could increase pressure on some currencies following relatively strong depreciation in 2015. Some of the more specific risks facing Middle Africa include:

Catalysing impact investing in East Africa: recommendations for development of the services market (FSG)

Based on consultations with over 80 stakeholders in Kenya, Tanzania, Uganda, and Rwanda, the report proposes a market-responsive intervention that helps to scale access to capital raising and associated capacity building services for enterprises. To achieve this, the report recommends the creation of a donor-funded ‘Facility’ to help service providers reach deeper into the pool of enterprises that need support, and to develop a more vibrant impact investing market overall.

G20 trade: Davies to attend G20 in China (IOL)

South Africa’s Minister of Trade and Industry Rob Davies has left for Shanghai, China, to attend the G20 Trade Ministers meeting to be held over the weekend, the dti said on Thursday. A G20 Trade and Investment Working Group (TIWG) was establish this year following a decision by the G20 leaders to better coordinate efforts to reinforce trade and investment. The Trade Ministers will consider the outcomes and recommendations from the TIWG. [G20 an opportunity to promote NZ’s trade agenda]

South Africa: Watchdog probes Transnet for excessive pricing and preferential treatment (Business Day)

The Competition Commission is investigating Transnet for "excessive pricing" in port charges and the preferential treatment of some clients to the exclusion of others. SA’s port charges are excessive by global standards and have long been identified as an impediment to business. Port regulator Mahesh Fakir said the charges being probed by the commission were those levied by Transnet Port Terminals — the operator of the ports — and were not regulated. Tariffs charged by Transnet’s National Port Authority, which owned and managed the eight commercial ports in the country, were determined by the regulator and have been regulated since 2009.

Isabelle Ramdoo: ‘Can local content policies provide a transformative solution for Africa?’ (AfDB)

Implemented in a smart way and in partnership with mining companies, LCPs are thus a powerful tool to stimulate the creation of upstream linkages by capitalising on companies’ own procurement needs as well as labour requirements. Similarly, using LCPs to foster downstream linkages are critical to develop industrial activities: the case of cement in Nigeria is a case in point. It is estimated that 90% of resource-rich countries apply one form of local content policy or another and that 40 and 80% of the revenue created in extractive sector (oil, gas, mining) is spent on the procurement of goods and services. In Ghana for instance, it is reported that 80% of procurement expenditure stays in the country. Although the definition of ‘local’ and ‘content’ is not universally agreed, the scope of procuring domestically nonetheless represents a unique opportunity to supply the extractive sector.

Boosting the power sector in Sub-Saharan Africa: China’s involvement (IEA)

This report analyses China’s engagement in the sub-Saharan Africa power sector, including the key drivers underlying Chinese investments. An overview of Chinese projects (generation, transmission and distribution) during the 2010-20 period is provided in this first-ever consolidated effort to map them. The report identifies the key Chinese stakeholders and assesses their impact on policies affecting energy access, economic development and financing modalities. Two case studies examine Chinese investment at the country level in Ghana and Ethiopia.

Transfer pricing and tax base erosion in Africa: NRGI report, case studies from Zambia, Tanzania, Sierra Leone, Ghana, Guinea

'Beyond AGOA': These new [USTR] reports reveal some promising steps on trade with Africa (ONE)

Trade performance of Asian Landlocked Developing Economies: state of play and the way forward (ESCAP)

Aid for trade and the Trade Facilitation Agreement: what they can do for LDCs (FERDI)

Yesterday’s UNSC briefings on African governance issues: AU Mission in Somalia, briefing on DRC

Land dynamics in Africa: what is the potential for expansion? (pdf, Agbiz)

Global Food Security Act of 2016: Gayle Smith commentary (USAID)

India continues to lead China in pharma exports (Livemint)

Govt aims to make India design hub, new national policy likely (Livemint)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

South Africa: Latest IMF outlook shows urgent need for policy reforms

South Africa faces significant challenges and needs decisive action to revive growth, the IMF said in its latest annual assessment of the country’s economy.

South Africa has made considerable economic and social progress since its first democratic election in 1994, but many citizens have not sufficiently benefited from the improvements. The report shows income inequality and unemployment remain among the highest in the world, and growth has waned in recent years.

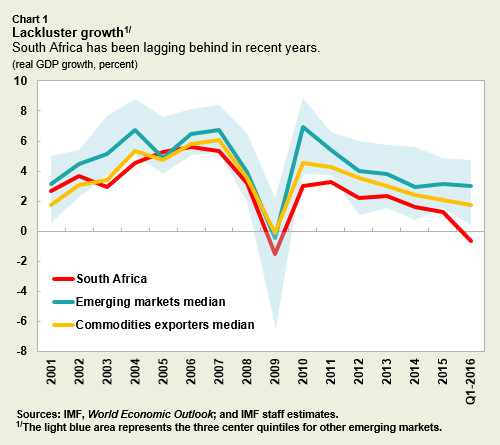

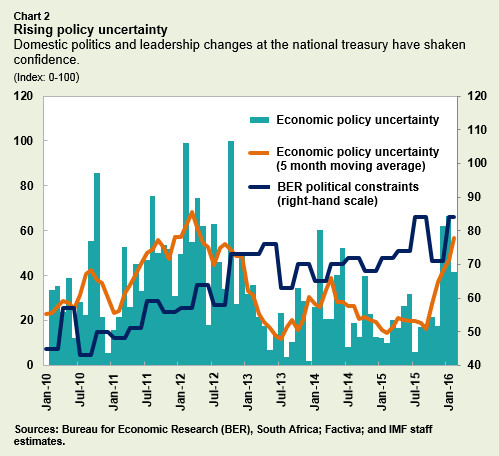

In 2015, South Africa was hit by a number of economic shocks. China’s slowdown and rebalancing, weak commodity prices, and U.S. monetary policy normalization all weighed on growth (Chart 1). On the domestic front, leadership changes at the National Treasury last December and other political developments shook confidence, heightened governance concerns, and increased policy uncertainty. A severe drought in the region also significantly reduced agricultural output.

And while electricity supply has improved, growth continues to be held back by deep-rooted structural problems such as poor education outcomes, and product and labor markets that are out of reach for too many people.

The report shows growth slowed to 1.3 percent in 2015, the lowest since the global financial crisis and below most emerging market economies and commodity producers. The IMF projects 2016 growth at 0.1 percent, which would mean a second year of falling per capita incomes. A muted recovery is expected from 2017, approaching 2-2½ percent in the outer years as shocks dissipate and more power plants are completed; with these projections, unemployment will likely rise over the medium term.

Risks of further deterioration

Downside risks dominate and stem mainly from China, heightened global financial volatility, and domestic politics and policies that may reduce confidence (Chart 2).

Shocks could be amplified by linkages between capital flows, the sovereign, and the financial sector, especially if combined with sovereign credit rating downgrades to speculative grade. The United Kingdom’s recent decision to leave the European Union (EU) has further increased risks, as there are extensive financial linkages between the United Kingdom and South Africa and sizable trade linkages with the EU as a whole.

The report notes, however, that the authorities are making progress in the recent dialogue between government, businesses, and labor, which could catalyze reform implementation and invigorate growth.

Urgent need for more reforms

Besides addressing infrastructure bottlenecks, the report said structural reforms should be a priority in order to boost growth and jobs. Greater competition, labor market policies and industrial relations that work for a greater portion of the population, better quality of government services – especially in education – and improved governance and efficiency in state-owned enterprises would all help increase growth.

Job creation, especially in small- and medium-sized enterprises that are more labor-intensive and hire a relatively high share of low-skilled workers, is the best way to ensure a sustainable reduction in unemployment and inequality. Advancing these reforms will require building trust among stakeholders, ideally via a social bargain.

To generate reform momentum, the report suggests government should implement a focused set of tangible measures with a priority on boosting private sector employment. Clarifying the regulatory environment in the mining sector and reforming state-owned enterprises, for example, would reduce policy uncertainty and increase confidence and trust even in the short term.

Elevated vulnerabilities

Sources of resilience include strong institutions and policy frameworks, the flexible exchange rate regime, strong private corporate balance sheets, a high share of rand-denominated external debt, well-capitalized banks, and the large domestic institutional investor base.

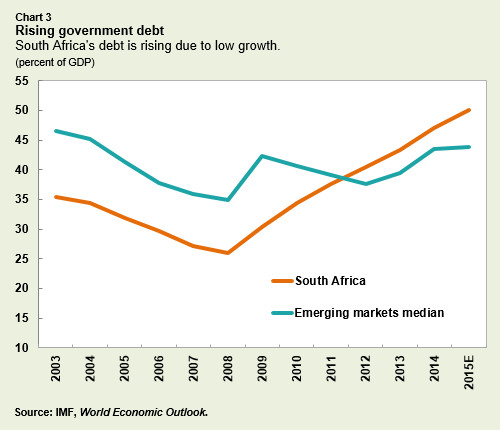

Nevertheless, vulnerabilities remain elevated. The current account deficit, though it has started adjusting, remains among the highest in emerging markets. Rising government debt, due to a large extent to low growth, and financially-weak state-owned enterprises have increased fiscal vulnerabilities, and sovereign downgrades could trigger capital outflows (Chart 3).

Limited macroeconomic policy space

The 2016 budget envisaged significant deficit reduction this year and next to stabilize debt. However, the budget targets could be challenging to achieve if IMF staff’s less-optimistic growth projections materialize. The report suggests that any additional fiscal consolidation needs to be carefully designed to minimize the negative growth impact and protect the poor. State-owned enterprise reforms are also essential to limit fiscal risks, as well as to support growth. Greater private participation and effective regulators could help improve state-owned enterprise performance and free up resources for investment.

Making a strong push on structural reforms is the absolute, urgent priority to put the South African economy on a path to improving living standards and create jobs, the report said.

Context: Confluence of shocks on top of existing structural challenges and vulnerabilities

The global transitions – China’s slowdown and rebalancing, weak commodity prices, and the U.S. monetary policy normalization – are taking a heavy toll on South Africa. China’s key role in the world economy and South Africa’s high reliance on mining exports result in significant spillovers from China’s transitions and the commodity price fall, despite the country being an oil importer (Box 1). China’s growth now matters more for South Africa than the E.U.’s and the U.S.’s growth.

Commodities are the main channel, closely followed by global financing conditions likely capturing confidence effects. The commodity channel is also likely operating via Sub-Saharan Africa (SSA) – now absorbing 30 percent of South Africa’s exports and a major destination of South African corporates’ large expansion abroad – and is reducing corporate profitability and incomes across the economy. In addition, South Africa’s financing conditions are closely tied to those in the United States, though the two economies are moving in opposite directions. Outward spillovers to South Africa’s immediate neighbors will be significant. Spillovers to the rest of SSA are rising but remain muted (Box 2).

Box 1. Spillovers from Global Transitions

Spillovers from China and lower commodity prices

Rising trade linkages and reliance on commodities have increased spillovers from China. China absorbs 10 percent of South African exports, the most of any country. More importantly, it plays a key role in determining global demand for South Africa’s commodity exports, which account for 34 percent of total goods exports (51 percent including manufactured commodities), and commodities imports including oil, which account for 16 percent of total goods imports.

Staff analysis suggests China’s growth now matters more for South Africa than that of the U.S. and the E.U. Using quarterly data from 2000, a VAR suggests that a one percentage point decline in China’s real GDP growth would lower South Africa’s growth by 0.3 percentage point (q/q sa annualized) after one quarter. This is smaller than the impact of a shock to the U.S. and the E.U. growth, and broadly consistent with estimates found in previous studies, including the World Bank’s June 2015 Global Economic Perspectives. However, the impact of a shock to China’s growth rises to 1 percentage point in the postcrisis sample, significantly exceeding the impact of shocks originating in the U.S. and the E.U. Though data limitations preclude a full analysis, the impact of a decline in China’s secondary sector could be even greater.

Commodity prices and global financial conditions are the main transmission channels. A decomposition following Swiston and Bayoumi (2008) suggests the decline in South Africa’s export commodity prices following a shock to China’s growth has a large and persistent impact. Financial spillovers (proxied by U.S. financial conditions), which likely capture global confidence effects, are also important. Spillovers through trade are small and positive, suggesting the impact of exchange rate depreciation on competitiveness outweighs the fall in global demand. Declining import commodity prices (mainly oil) provide a partial offset.

The impact of lower commodity prices is amplified by sectoral interlinkages. An analysis of input-output tables in South Africa suggests linkages between the commodity sector and the rest of the economy are significant. A sectoral structural VAR identified using multipliers from the input-output table suggests a 10 percentage point decline in export commodity prices would reduce real GDP growth by nearly 0.2 percentage points (q/q sa annualized) after two quarters, with most of the impact coming from downstream (e.g., construction) and upstream (e.g., transport) sectors including manufactured commodities. A Swiston and Bayoumi decomposition suggests that the main transmission channels are changes in corporate profitability and employment in the non-mining sector.

A shock to China’s growth worsens South Africa’s external and fiscal balances, but the impact on inflation is ambiguous. Mineral export growth declined to -7 percent in 2015 from an average of 19 percent in 2011-13 on lower demand and prices. The lower oil import bill is a partial offset, and the terms of trade are expected to remain negative over the next few years.3 Fiscal revenues are affected mainly through growth, with corporate income tax growth down from an average of 10 percent between FY11/12-FY13/14 to an estimated 2.2 percent in FY15/16. Lower oil prices are fully passed through to retail prices, with petrol prices in early-2015 27 percent below their 2014 peak. However, this effect has been partly offset by depreciation. Anecdotal evidence points to a significant deflationary impact from overcapacity in China, which South Africa has partly offset through increasing tariffs by 10 percent on some steel imports (within the WTO bound rates). The overall impact on inflation in South Africa is therefore ambiguous.

Spillovers from tighter global financial conditions

High external financing needs and a large share of bond and equities held by foreign investors make South Africa vulnerable to spillovers from tighter global financial conditions. Almost half of South Africa’s portfolio liabilities are held by U.S. investors. Estimates in Caceres et al. (2016) suggest a 100bps increase in the U.S. policy rate would increase South African long-term rates by 73bps after one year, above the EM average, but short-term rates are not significantly affected. 4 South Africa-specific estimates underlying the 2014 Spillover Report suggest a 0.2 percent decline in growth after one year following a 100bps rise in U.S. bond yields, with most of the spillovers coming from a 79bps increase in long-term bond yields and declining equity prices. Simulations using a broader set of countries in the 2015 Spillover Report and in Buitron and Vesperoni (2016) suggest that an unexpected tightening of monetary conditions that pushes up U.S. bond yields by 100 bps would spill over to bond yields in EMs and non-systemic advanced countries, result in capital outflows, and lower industrial production growth by 3½ percent per annum after one year. Most EMs would also experience significant exchange rate depreciation, though South Africa is relatively shielded from negative balance sheet effects given low corporate leverage and limited FX mismatches.

Box 2. Outward Spillovers to Sub-Saharan Africa

Past research suggests that, apart from its immediate neighbors, South Africa has limited spillovers to the rest of Africa, but these are likely to have increased. Several studies have shown that South Africa’s growth has limited spillovers on SSA, once global growth is controlled for. However, SSA’s share in South Africa’s imports has more than doubled over the last decade. South African companies in retail, banking, and telecommunications have established large networks in several sub-Saharan African countries. South Africa now represents an important export destination and source of FDI, especially for neighboring countries.

Other countries of the Southern African Customs Union (SACU) will be the most affected by South Africa’s slowdown. Besides the growth impact, SACU countries rely heavily on South Africa in their shared customs receipts, as South Africa accounts for about 85 percent of total SACU imports. With imports having declined in 2015 and low growth expected going forward, combined with the lags built in the SACU revenue formula, this vital source of revenue will decline markedly.

South African firms have many subsidiaries in SSA, which could dampen their profitability going forward. About 75 percent of African subsidiaries are in services, trade, and financial sectors. The 10 firms with the highest number of subsidiaries are some of the top listed companies. While African subsidiaries have contributed to South African corporates’ high profitability in the past decade, the deteriorating performance of SSA could adversely affect profitability.

Selected Issues Paper

The impact of China’s growth slowdown and lower commodity prices on South Africa

This paper estimates the impact of China’s growth slowdown and the recent large decline in commodity prices on South Africa. It seeks to identify the key channels through which a shock to China’s economy is transmitted to South Africa, as well as the propagation of this shock within the economy. Our findings suggest that China’s growth slowdown is likely to have a significant impact on South Africa’s economy, with commodity prices and global financial conditions the main transmission channels. Sectoral interlinkages are found to play an important amplifying effect, notably through employment, corporate profitability, and wealth effects.

Increasing trade linkages have made China the most important single-country destination for South African exports. China now absorbs 10 percent of South African exports compared to around 2½ percent in the mid-2000s. This trend reflects not only rapid growth in China and the associated rise in China’s demand for commodities, but also weak demand from the Euro Area whose share of South Africa’s exports has declined to 15 percent from more than 20 percent over the same period. Sub-Sarahan Africa (SSA) remains the most important regional destination for South African exports

China’s impact on the South African economy is magnified by China’s role in the global economy and commodity markets.

-

China accounts for around 17 percent of global output in PPP terms compared to 16 percent for the US. In terms of imports, China accounted for approximately 16 percent of the world total compared to 14 percent for the U.S.

-

More than 60 percent of the world’s traded iron ore – South Africa’s main mineral export – is absorbed by China. China also plays a large role in other commodities that South Africa exports including coal, gold, and platinum. As a result, China plays a key role in determining global demand and prices of South Africa’s main commodity exports, which now account for 34 percent of total goods exports (51 percent when manufactured commodities are included). China is also one of the world’s largest oil importers, and therefore plays an important role in setting the price of South Africa’s oil imports (though supply factors have been key for prices), which account for around 16 percent of total goods imports.

Capital flows into South Africa from China are modest, but financial spillovers are increasing. Both direct investment and portfolio flows from China are increasing, but remain modest relative to capital flows from the UK and the US. However, as noted in the April 2016 Global Financial Stability Report, financial conditions in China are now increasingly affecting global financial conditions, mainly through equity and FX markets.

China’s growth has been found to have large spillover effects on South Africa, transmitted mainly through commodity prices and global financial conditions, and amplified by sectoral interlinkages. The analysis in this paper suggests that rising trade and financial linkages with China, as well as China’s large role in the global economy and commodity markets, has increased the impact of a growth slowdown in China, which now exceeds that of a growth slowdown in the U.S. and the E.U. Commodity prices and tighter global financial conditions are the main international transmission channels. Domestically, the impact of a fall in commodity export prices is amplified by linkages between the mining and non-mining sectors, and is transmitted to the economy through large falls in mining sector employment, corporate profitability, and wealth effects.

Macro-financial linkages: capital flows, sovereign ratings, and the financial sector nexus

This paper discusses key macro-financial linkages and related risks in the South African economy focusing on downside scenarios that are not part of the baseline. South Africa’s high reliance on external finance, with banks intermediating a larger share of capital flows in recent years, exposes it to the risk of capital flow shocks. Low growth, rising interest rates, and fiscal risks could generate negative feedback loops among lower capital flows, heightened sovereign risk, and a weaker financial sector. The confluence of these factors could raise financial institutions’ funding and credit costs, and widen the fiscal deficit given the high reliance of tax revenues on the financial sector.

While so far the financial sector has not hampered growth, a weaker financial sector could reduce lending, and in turn lower growth. Sovereign rating downgrades are a possible trigger of capital outflows. A downgrade of the sovereign foreign currency (FX) debt to speculative grade seems to be mostly priced in and is likely to have a limited impact on the sovereign given the low level of government FX debt. A potential downgrade of the local currency (LC) sovereign debt rating to speculative grade is not in staff’s baseline, as the latter is currently two to three notches above non-investment grade. If it were to happen, however, it could trigger sizable capital outflows and generate some of the feedback loops described above, given large non-resident holdings of government debt, about a fifth of which are estimated to require investment grade rating. The floating exchange rate regime and South Africa’s deep capital markets are likely to mitigate such shocks.

Related News

Ethiopia’s investments in health, education and social protection yield positive results

Ethiopia’s investments in health, education, social protection, and infrastructure have had a positive impact on economic development and promoting shared prosperity in the country, says the 2015 Ethiopia Public Expenditure Review, a new World Bank Group report released on 6 July 2016.

The report, which evaluated the effectiveness of public finances, states that the country is moving in the right direction, despite rising economic pressure. The positive steps taken by the Government of Ethiopia (GoE) over the past decade to reorient expenditure from recurrent to capital, the decentralization of resources from federal to regional governments, and the focus on infrastructure have led to broad-based growth.

By leveraging external resources to boost spending in pro-poor sectors, the GoE has created the largest social safety net program in Africa benefiting 8 million people. The country has also achieved remarkable health and education outcomes using cost effective approaches. However, the report points out the urgent need to ensure equity in access to services to address major differences at household level.

For example, neo-natal mortality reduced significantly for wealthier populations, but increased for the poorest. Out-of-pocket spending accounts for about one-third of health expenditure, which is high compared to other low-income countries and undermines access for low income households. In education, while the poorest children are enrolling in primary school, they are increasingly dropping out at higher levels. Only 1% access technical and vocational training and 2% higher education.

“Ethiopia’s investments in key sectors have had a positive impact on poverty reduction, now the key is for the country to develop a more effective budget allocation in order to maximize the returns on investment,” said Carolyn Turk, World Bank Country Director for Ethiopia, Sudan and South Sudan.

According to the report, Ethiopia’s investment in infrastructure has increased the country’s road network five-fold, reaching 100,000km in 2015. Investment in education has also helped to increase net primary enrollment from 77.5% in 2006 to 92.6% in 2015, according to the report, and education has been extended from 10 million to more than 23 million students in the past decade.

Through smart investments in the health sector and only an additional $5 in per capita health spending, the GoE reduced child mortality by more than half from 72 to 31 per 1,000 between 2005 and 2015. This is a record, as no other country has achieved such results for the same level of spending, the report notes.

In addition, more people now have access to improved water and sanitation services than ever before, according to the report. By leveraging external resources to boost spending in pro-poor sectors, the GoE has created the largest social safety net program in Africa benefiting 8 million people.

Despite the progress, Ethiopia’s poverty challenges remain deep-rooted and require sustained efforts. In order to ensure that new investments translate into enhanced service coverage and delivery, the report underscores the importance of supplementing the current public investment-led strategy with increased budgetary provisions for operations and maintenance. This is especially essential in key sectors such as transport and communication, education, health as well as water and sanitation.

Notwithstanding the progress in critical aspects of human development, as Ethiopia strives to become a middle income country by 2025, it needs to address several challenges including:

-

The declining share of recurrent spending for operations and maintenance, especially in the transport and communication, education, health and water and sanitation sectors because improvements in service delivery cannot be achieved without adequate budgetary provision.

-

Enhancing revenue mobilization: Significant effort will be required to improve revenue mobilization to match operation & maintenance needs for ongoing investments

-

Equity in access: targeting the bottom 40%: Positive results have been achieved in the health and education sector however there are important differences in access to services at household level that require urgent attention.

Beyond service coverage the report underscores the need to increase technical and allocative efficiency, said Jane Kiringai, World Bank senior economist and lead author of the report.

“If we look at the health sector, more than half of current health spending is on primary care, the most cost-effective level of health care however, in some regions investments in the sector have exceeded the standard norms, creating idle capacity and undermining technical efficiency,” she said. “So more needs to be done to improve efficiency as the average number of outpatient visits per health worker per day which varies currently between two and nine and the average inpatient case per health worker per day is only one.”

While spending on primary education remained stable, secondary education increased, TVET share declined slightly and higher education is now the biggest sub-sector by spending. Higher education accounts for almost 80% of the education capital budget, taken up mostly by the construction of universities. On the supply side, classroom shortage and high pupil teacher ratio remain binding constraints to technical efficiency of primary schools in about a quarter of all districts.

The report also pointed out the need to increase efficiency and coverage of social protection programs, through consolidation of existing programs (food aid, workfare and targeted cash transfers) along with reforms and elimination of inefficient and regressive general subsidies.

As Ethiopia lays the foundation to become a middle income country, and the changing global environment implies declining external assistance, the report suggests that Ethiopia needs to focus on domestic revenue mobilization to support this transition. This will help create the much-needed fiscal space to increase funding for operations and maintenance and support fiscal sustainability. At 12% of gross domestic product (GDP), the country’s tax ratio is low compared to peer countries. According to the report more efficient tax administration stimulated by tax reforms, improved capacity and quality of tax administration as well as expanded tax bases could be a major sources of additional revenue. This will address the funding gap for future investments.

“Domestic resource mobilization will lay the foundation for Ethiopia’s journey to middle income status,” said Kiringai.

The Ethiopia Public Expenditure Review is produced by the World Bank Group in collaboration with the Government of Ethiopia. The policy note is intended to make a contribution toward how the government and development agencies design and implement their policies and programs.

Related News

Aid for Trade and the Trade Facilitation Agreement: What they can do for LDCs

The Aid for Trade (AFT) initiative, launched in 2005 to help developing and especially the Least Developed (LDCs) countries integrate the rules of the World Trade System adopted in the Uruguay Round turned out to be more about mobilizing support for the stalled Doha Round negotiations.

A decade later, a broadened AFT agenda has eluded effective evaluation. The recently concluded Trade Facilitation Agreement (TFA) provides an ideal opportunity to narrow the scope of AFT activities to heed the call for “managing for Development results” (MfDR).

The paper reviews the evidence on trade costs distinguishing between Least Developed Countries (LDCs) and Landlocked LDCS (LLDCs). The paper also includes new estimates of time in transit for international parcel data that is measured relatively accurately.

New estimates provide support for allocating a greater share of AFT funds towards LDCs and particularly towards LLDCs, both groups showing higher trade costs than comparators and less progress in reducing trade costs since 1995. On average, time in customs for imports and exports are also significantly higher for both groups than for their respective comparators. LDCs and LLDCs have systematically lower scores for the components in the new OECD Trade Facilitation Indicator (TFI). These new estimates suggest that a successful implementation of the TFA, defined as moving halfway towards the frontier value of the TFI for the respective country grouping could reduce trade costs for imports of LDCs by 2.5% and by 4.5% for LLDCs.

Even though there is more to trade costs than customs management, monitoring implementation of the TFA would be part of the IPoA and a stepping stone towards the concrete trade performance targets that have lacked in AFT activities so far.

Aid-for-Trade: Where do we stand?

The role of foreign aid in developing countries’ strategies has gone through stages. In the early days of independence in the 1960s, when enthusiasm about the liberation from the colonial powers was strong, much hope was placed on foreign aid which would provide the necessary ingredient to reach Rostovian ‘take-off’ growth. As countries were then following a state-led industrialization strategy behind high trade barriers, this period could be described as one of ‘aid but not trade’ as pessimism about the prospects of developing countries’ exports was great. As evidence of resource misallocation and corruption appeared, deception set in, and the pendulum shifted towards what one could describe as ‘trade but not aid’ as it was becoming increasingly evident that, apart from East Asia, the disappointing industrialization performance was largely due to countries’ own trade policies rather barriers to access in export markets that were falling. Once trade barriers – especially tariffs – were slashed across developing, aid entered a third phase as, once more, performance was not improving as much as expected – especially among the Least Developed Countries (LDCs), ushering in the current phase of ‘Aid For Trade’ (AFT).

The AFT initiative launched in 2005 was part of the MDGs (goal 8 ‘developing a global partnership for development’) with as objectives, a rules-based, open, multilateral trading system, improved market-access including duty-free, quota-free (DFQF) market access for LDCs, and above all to reduce poverty by half in 2015 relative to 1990 level, a target that has been reached in most countries. Now that the Sustainable Development Goals (SDGs) have been adopted by the UN General Assembly in September 2015, the main trade performance objective is a doubling of the global share of LDC exports by 2020 (already part of the Istanbul Program of Action (IPoA)). Now that WTO members have endorsed the TFA agreement signed in Bali in 2013, what is the role of AFT? In Melo and Wagner (2015), we focused on the trade-enhancing and poverty-reducing effects of AFT that were an objective of the MDGs. Here we focus on the benefits from a successful application of the TFA: a move towards results-based AFT and an evaluation of the benefits from reduced trade costs with a focus on LDCs and Land-locked Least Developed Countries (LLDCs).

At around $40 billion disbursed a year, AFT is about 30% of Official Development Assistance (ODA) financial flows to developing countries (remittance flows are more than the combined ODA and FDI flows) and what is entered as Trade Facilitation in the OECD’s Credit Reporting System (CRS) only accounts for about one percent of AFT disbursements.

In the haste to garner support for the stalling negotiations at the Doha round, the objective to raise funds rapidly took precedence over the more fundamental objectives of providing assistance, financial and technical, to help developing countries, particularly LDCs, to build the needed supply-side capacity to ‘implement and benefit from WTO agreements’ they had signed up to in the Marrakech agreement under the ‘Single Undertaking’. In the end, beyond winning the argument on mainstreaming trade in national development strategies, the biennial OECD-WTO AFT reviews turned out more about expanding the agenda than about conducting an evaluation of the effectiveness of AFT. This led to the criticism that to facilitate evaluation, the scope of AFT activities should be considerably reduced.

The many evaluations of the AFT initiative have reached the conclusion that the objective of arresting the decline in the share of AFT in ODA disbursements has been met and that trade has been mainstreamed in national development strategies. However, trying to isolate the effects of AFT from other financial flows is like looking for a needle in a haystack. This is why the attempts at detecting the effects of AFT, especially when it comes to aggregate outcomes like export growth and GDP growth have encountered attribution difficulties so that biennial OECD-WTO evaluations have focused on the rationale for AFT.

The scope of the reviews evolved with two ‘landmarks’: the adoption of a ‘results chain’ approach (i.e. a shift towards management based disbursement of ODA along the lines suggested by the Development Assistance Committee at the OECD) at the third biennial review in 2011 and the fifth biennial review of June 2015 on “Reducing Trade Costs for inclusive Sustainable Growth” in the wake of the TFA. Now, the TFA presents the opportunity for AFT to move beyond the narrow focus on accountability (was the road built?) towards a management framework that can track better the results of AFT interventions. Equally important, the TFA provides the focal point needed for narrowing the scope of AFT. Implementing the TFA commitments should therefore be targeted towards countries with the highest trade cost that would benefit the most. The evidence discussed here suggests that a shift in trade facilitation disbursements towards LDCs and LL-LDC would provide the highest returns for AFT funds.

Successful implementation of the TFA would reduce uncertainty related to trade, streamline market access procedures and would provide greater transparency at customs, all factors leading to lower transaction costs. Higher trade volumes would then be an engine of growth and poverty reduction.

» See also the tralac Trade Brief by Henry Kibet Mutai: The WTO’s Aid for Trade Initiative at 10: An Overview | December 2015

Related News

Mozambique sees growth slowing, austerity measures needed – finance minister

Mozambique, reeling from a sovereign debt crisis, sees 2016 economic growth slowing to 4.5 percent from initial forecasts of 7 percent and needs to bring in austerity measures in an amended budget, Finance Minister Adriano Maleiane said on Thursday.

“This means that revenue that we should have will also go down,” the minister told journalists after an extraordinary meeting of the Council Of Ministers which approved an amended budget which will be put before parliament on Monday.

The new government forecast is in line with a recent one by the International Monetary Fund, which in April said the southern African nation had borrowed more than $1 billion previously undisclosed, throwing into doubt its ability to meet mounting debt obligations.

Mozambique, one of the world’s poorest countries which has huge untapped gas reserves, has been thrown into economic turmoil by revelations of financial malfeasance.

These include an $850 million Eurobond issued in 2013 to finance a tuna-fishing fleet. Subsequently, it emerged that $500 million of the cash was actually spent on defence equipment and has since been re-allocated to the defence budget.

Under its austerity plan, the government aims to reduce spending on goods and services by 40 percent, saving overall 24 billion meticais ($370 million) out of a budget of 243 billion meticais.

Related News

New IEA report maps Chinese investments in Africa’s power sector

Massive investments still needed to achieve universal energy access in sub-Saharan Africa

Chinese companies are playing an increasingly significant role in the development of the power sector in sub-Saharan Africa, and accounted for 30% of new capacity additions in the region over the last five years, according to a new study published by the International Energy Agency.

This publication, Boosting the Power Sector in Sub-Saharan Africa: China’s Involvement, is part of the IEA Partner Country series and offers the first pan-regional overview of the involvement of Chinese companies in the region’s electricity supply system.

The African continent faces major electrification challenges. More than 635 million people live without electricity in sub-Saharan Africa. As part of a strategy to expand international investments and gain access to foreign markets, the People’s Republic of China and its state-owned companies have invested substantially in Africa in recent years.

The new IEA report provides a comprehensive analysis of these projects, which include investments of around $13 billion between 2010 and 2015 from China. These projects are financed largely through public lending from China.

“African countries have relied heavily on China to support the expansion of their electricity systems, to enable growth and improve living standards,” said Paul Simons, the IEA’s Deputy Executive Director.

Greenfield power projects contracted to Chinese companies have become widespread in the region. Over half of all projects are based on renewable energy, mainly hydropower.

Training of local technicians is essential to maintain efficiency and performance of newly built plants, In 2014, a special report from the IEA’s World Energy Outlook on sub-Saharan Africa showed that the lack of energy access and the shortage of electricity supply were severe constraints to better living conditions and hampered economic growth. In line with its policy to open its doors to emerging economies and become a global hub for clean energy technologies, the IEA is dedicated to supporting Africa’s electricity sector development.

Related News

tralac’s Daily News Selection

The selection: Thursday, 7 July 2016

Inquiry into UK’s Africa Free Trade initiative: extension to deal with Brexit issues (APPG)

We are now extending the Inquiry to incorporate the potential implications for UK-Africa trade relations from the UK leaving the European Union (Brexit). Specifically, a second Inquiry Hearing will be held in Parliament on Tuesday 12th July. In addition, the timeline for submission of Written Evidence has now been extended to 31st July 2016. The Inquiry Committee will then seek to present and publish its Final Report in September 2016, when a new UK Prime Minister and ministerial team will be in post. The following questions are being used to guide the Inquiry’s taking of evidence in relation to Brexit:

Trade policies: How would the existing trade arrangements (both non-reciprocal trade preference arrangements and reciprocal trade preference arrangements such as the Economic Partnership Agreements) between the UK and African countries look immediately after Brexit? What steps would need to be taken by the UK Government to ensure Africa’s exports to the UK were not interrupted upon the UK’s withdrawal from the EU? What are the potential risks and opportunities for UK-Africa trade relations arising from Brexit?

Aid-for-trade: Should the UK’s aid-for-trade programmes evolve to reflect the new trading relationships between the UK and African countries post-Brexit? Does Brexit potentially open up new channels through which the UK can use trade and investment as a vehicle to reduce poverty in Africa?

Inclusive trade: Are there specific potential implications from Brexit for small-scale traders and farmers in Africa? If so, are there ways for the UK government to ensure that post-Brexit trade policies would be pro-poor and equitable for men and women in Africa?

Less aid money, less influence: Brexit’s likely hit to the UK’s development role (The Guardian)

The first signs of the Department for International Development’s immediate priorities may come in the outcomes of the bilateral and multilateral spending reviews, which Greening told parliament should be released “in the early summer”. An EU spokesperson said it was too early to speculate on how Brexit would affect Britain’s role in the international aid community. “That will be addressed in due course, once negotiations with the UK begin on its withdrawal agreement as well as on the agreement concerning its future relationship with the EU. For the time being, nothing changes.”

Botswana: Diamonds safe from Brexit (Daily News)

The divorce between the UK and European Union, called Brexit, would not have an impact on diamond market. Head of Operations at Diamond Trading Company Botswana Mr Joseph Ikotlhaeng said major market for Botswana diamonds are the United States of America, Japan, India and China. Mr Ikotlhaeng said the USA represents 40% of the world market while Belgium is the only important European market.

The President’s Advisory Council on Doing Business in Africa: Rwanda/Nigeria trip recommendations report (USTR)

Over four days in Nigeria and Rwanda, we focused on key issues for African development and areas of interest from the American business community. Throughout the trip, we also focused on access to capital, skills training, and the importance of women’s participation in the labor force and entrepreneurship. On the basis of these conversations, and our continued consideration of African economic trends, this report contains recommendations in five areas:

‘Modi in Africa’ – selected updates on trade and investment issues:

India has had trade relations with Africa from first century CE (Indian Express)

PM Modi has touched down at the Mozambique airport, kickstarting his four-nation tour of the African continent. In the next five days, as he visits South Africa, Tanzania and Kenya, the agenda on his mind would be to enhance trade and maritime cooperation along with increasing collaboration in matters of energy and food security.

India takes its contract farming model to Mozambique (Hindustan Times), Modi keen to forge new ties with SA (IOL), India-Africa ties: pitching higher (Gateway House), Can PM make India an alternative for China? (First Post)

BRICS Bank: Maasdorp on BRICS bank's 'openness' (Devex)

The New Development Bank - a financial institution founded by the so-called BRICS emerging economies, Brazil, Russia, India, China and South Africa - will open its membership to other countries in the next few years, the bank’s vice president and chief financial officer told Devex in an exclusive interview. The opening of membership, likely to happen in the next three years or earlier, will also see the shareholding of the five member countries of the $100bn institution significantly reduced. That could help placate some critics, who have argued that the Shanghai-based bank is a dedicated political and economic tool of the five countries currently involved. The bank has so far approved around $811m in loans.

The GIBS Dynamic Market Index 2016 (pdf, GIBS)

The GIBS DMI 2016 is a global study of six enabling ‘pillars’ of market dynamism across 144 countries measured between 2007 and 2014. The GIBS DMI is a toolkit that measures which countries have undergone change and improvement (or deterioration) in six enabling pillars (comprising institutions and society measures). The six pillars include:

SADC member states urged to establish more joint investments on energy, water (Daily Mail)

The workshop, 20-21 June, held under the theme: “Accelerating energy delivery and access to water resources in the SADC region – a collective approach”, facilitated exchange of ideas and proposed recommendations towards the energy and water crisis in the region. After deliberations, the workshop recommended, inter alia: (i) The SADC Secretariat should as a matter of urgency initiate a study on transferring water from the water-rich basins to the water stressed parts of the region expeditiously, through inter/intra basin transfers. (ii) Member States must be encouraged to embark on intensive energy and water demand side management strategies which combine the use of high efficiency technologies, methodologies and better awareness creation as a matter of urgency. (iii) Member States who are not connected in the Southern African Power Pool (SAPP) transmission network must be encouraged to get connected to accelerate the respective on-going interconnector projects to enable them to benefit from trading among the Member States. Though SAPP was established more than 20 years ago, three mainland SADC Member States are still not connected.

Energy-water nexus in Southern Africa: background paper to support dialogue in the region (World Bank)

The value of this paper is in bringing together the latest knowledge work and other key information relevant for energy-water nexus dialogue in Southern Africa. This information has been derived from a number of fragmented sources, and an effort has been made to present the information in a logical framework, in one document that can help initiate discussions in the region. The issues and implications that surround the energy-water nexus are numerous. For the five focus countries - South Africa, Lesotho, Botswana, Namibia, and Swaziland - the paper considers national water sector priorities, energy sector priorities, the extent of coordination between the two, and how these priorities fit into a broader agenda of regional coordination.

SADC Transfrontier Conservation Areas Network: update (Daily News)

In an effort to complement the region’s ongoing efforts to address natural resources management challenges, the SADC Transfrontier Conservation Areas (TFCA) Network held a three-day symposium in Gaborone from 3-5 July. Officiating at the symposium, the permanent secretary in the Ministry of Environment, Wildlife and Tourism, Mr Elias Magosi said biodiversity loss as characterised by dramatic wildlife declines in some key hotspots around the world, was now considered a grand challenge on par with climate change, food security, energy security and public health, among others. For this reason, he said “embracing TFCAs will go a long way towards also addressing these grand challenges.”

Regional MPs discuss security in Great Lakes region: FP-ICGLR update (New Times)

Parliamentary leaders meeting in Kigali for a two-day 14th Ordinary Session of the Executive Committee of the Forum of Parliaments in member states of the International Conference on the Great Lakes Region (FP-ICGLR) have made regional security and political situation a focus of their discussions. At the sessions which kicked off yesterday at the Rwandan Parliament, members of the committee gave presentations and debated on the security and political situation in ICGLR member countries, especially focusing on Burundi, eastern Democratic Republic of Congo, the Central African Republic, and South Soudan.

The institutionalisation of mediation support within the ECOWAS Commission (ACCORD)

The PPB identifies the uniqueness of ECOWAS’s experiences in interventions in the 1990s, and the subsequent importance accorded to preventive diplomacy and mediation as a key factor that informed the decision to establish a mediation support structure – in contrast to using an ad hoc arrangement to backstop its mediation efforts in the past. This new arrangement, the PPB argues, will ensure that mistakes such as the marginalisation of ECOWAS in mediation processes in the region, the disconnect between the ECOWAS Commission and its appointed mediators, facilitators and special envoys, are remedied.

ECOWAS Regional Center for Disease Control: update (TODAY)

Nigeria's Minister of Health, Prof Isaac Adewole, has flagged off the ECOWAS Regional Center for Disease Control with a view of increasing the surveillance and information system for early detection, strengthening of laboratory capacity, preparedness and emergency response and retention of trained healthcare workforce in West Africa. The Director General of the West African Health Organisation, Dr. Crespin Xavier, said that the governing council has difficult task of supervising the activities of the centre in strict compliance with ECOWAS rules and regulations. [Regional Disease Surveillance Systems Enhancement (REDISSE) Project update (World Bank)]

Failure to prepare for and adapt to the 'new normal' of increasing climate-linked emergencies such as El Niño could put global development targets at risk and deepen widespread human suffering in areas already hard hit by floods and droughts, top United Nations officials said in Rome today. According to the UN, scientists are predicting an increasing likelihood of the opposite climate phenomenon, La Niña, developing. This will increase the probability of above average rainfall and flooding in areas affected by El Niño-related drought, whilst at the same time making it more likely that drought will occur in areas that have been flooded due to El Niño. The UN estimates that without the necessary action, the number of people affected by the combined impacts of the El Niño/La Niña could top 100 million. [Southern Africa's silent food crisis: CSIS report]

The State of World Fisheries and Aquaculture 2016 (FAO)

Fishery products accounted for 1% of all global merchandise trade in value terms, representing more than 9% of total agricultural exports. Worldwide exports amounted to $148bn in 2014, up from $8bn in 1976. Developing countries were the source of $80bn of fishery exports, providing higher net trade revenues than meat, tobacco, rice and sugar combined.

International regulatory co-operation: the role of international organisations (pdf, OECD)

This report compiles the information collected from 50 IOs and provides an analysis of their governance, operational modalities and tools in support of international rule-making. It identifies key lessons and messages on how IOs are organised to deliver on IRC and areas of challenges that may weaken their role. This work confirms the wide diversity of IOs involved in standard-setting and rule-making activities. The traditional model of inter-governmental organisation (IGOs) has flourished along with the development of new forms of organisations with different legal standing and memberships. As a result, the OECD survey respondents cover a range of different types of organisations: inter-governmental (with either closed or open membership), supra-national, trans-governmental and private. [Building regulatory policy systems in OECD countries: draft analytical paper (pdf)]

Global Forum on Competition: update: The 15th OECD Global Forum on Competition will take place in Paris on 1-2 December 2016. High-level competition officials from more than 100 delegations worldwide will come together to discuss:

Obasanjo calls for single currency for West Africa (TODAY)

Sahel and West Africa Club: weekly newsletter

US international trade in goods and services: May 2016 statistics (pdf, UN Census Bureau)

Lungu targets turning Zambia into manufacturing hub (Daily Mail)

DRC's illegal gold trade is benefiting foreign companies (Global Witness)

Mauritius: Removal of items under the list of controlled goods at export (GoM)

Port performance: linking performance indicators to strategic objectives (pdf, UNCTAD)

China Railway Rolling Stock Corporation wants to increase business in Mozambique (MacauHub)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

Meeting of the President’s Advisory Council on Doing Business in Africa: Recommendations report

On 29 June, Deputy Secretary of Commerce Bruce Andrews, on behalf of U.S. Secretary of Commerce Penny Pritzker, attended the President’s Advisory Council on Doing Business in Africa (PAC-DBIA) in Washington.

The PAC-DBIA brought together business leaders and government officials to discuss strategies designed to strengthen commercial engagement between the United States and Africa. In the final meeting of its inaugural term, PAC-DBIA adopted five new recommendations to drive sustainable growth and investment in Africa.

Members of the Council shared their findings from a trip to Nigeria and Rwanda in January 2016. In fulfilling its ongoing mission, the PAC-DBIA identified high-potential African countries where there is significant room to advance U.S. interests in solidifying existing business relations and cultivating new initiatives for U.S. companies.

Members of the PAC-DBIA chose to travel to Nigeria and Rwanda and organized a fact-finding trip to engage in extensive dialogue with key public and private sector actors in both countries. The goal was to identify barriers and find paths to improve opportunities for doing business in Africa.

In his remarks, Deputy Secretary Andrews noted the PAC-DBIA’s impact on the Obama administration’s work, and announced the Council’s next steps to even the playing field for U.S. companies and encourage foreign direct investment into Africa. Deputy Secretary Andrews stressed the importance of events such as the upcoming 2016 U.S.-Africa Business Forum to highlight commercial opportunities in Africa.

Findings from the Trip to Nigeria and Rwanda and Related Recommendations

Message from the Chair and Vice Chair

The President’s Advisory Council on Doing Business in Africa is pleased to present a report on our January 2016 trip to Africa and our third set of recommendations on how to strengthen commercial engagement between the United States and Africa. These recommendations extend and refine our previous recommendations, based on our continued analysis of opportunities and challenges for U.S. businesses in Africa.