Search News Results

Collaboration is key to the South African supply chain

Automation and integration result in reduced errors, saved time, and execution with minimal effort

Even in the earliest history of the logistics industry, traders operating across diverse geographies, cultures, and economies knew they had to work together to expand their reach. Today, that spirit of collaboration hasn’t changed, but the technology that ties the global supply chain together certainly has.

When a company wants to increase its profit, two strategies have remained generally in use throughout time: squeeze the customer to pay more, or squeeze the supplier to reduce their prices. But for both, the result is the same: merely taking money out of their pockets and putting it into yours. Unfortunately, neither of these add any real value to anyone. In fact, value is lost when customers are forced to reduce the amount they can buy and suppliers must downgrade the quality of their product to cover costs. This isn’t collaboration, it’s just bad business.

True collaboration unlocks true value for everyone – your supplier, your customer, and your own business.

Running a single platform solution that’s integrated with all your partners’ systems empowers you to manage logistics from a central database across multiple users, functions, offices, countries, and languages.

For the last 10 years, I’ve personally been involved in helping companies collaborate using technology in one of the most diverse regions of the globe. There are major institutional voids in Africa, ranging from electricity supply to internet connectivity, and collaboration is the key to overcoming such gaps. I have seen this work in many instances, and innovative uses of technology often play a major role in bridging these gaps.

The South African Example

With emerging consumer markets flooding goods into the continent, and unprecedented volumes of resources flowing out, Sub-Saharan Africa is the place to be. According to the World Bank, the region is on a GDP growth outlook that is approaching levels that are surpassing expectations in the developed world.

Logistics operations in South Africa are in a great position to take advantage of the massive growth opportunities this represents. There’s a chance for everyone to benefit by sharing skills, goods, and knowledge. And today’s technology makes this collaboration faster, more efficient, and more immune to the stresses of international logistics by sharing it all within a single-database system.

Elements of South Africa’s economy and society can be defined by both the first world and developing world. On one side, we South Africans have embraced the technologies and practices of the west, while on the other we’re also aware of the challenges, institutional gaps, and relevant cultures that surround us. Armed with regional knowledge and cutting edge software, logistics operators and their clients can more easily overcome the undeniable challenges as they take part in Africa’s economic renaissance.

Unlocking Value, Increasing Productivity

Let’s say an order is placed in South Africa. The raw materials are procured in Brazil and sent for production in China. All of it is shipped by an international shipping line or two, with both international and local African agents being involved. From beginning to end, all deadlines are met and everything moves easily. All documents, messages, and milestones are delivered on time with no delays and no issues.

By now, you want to know how this whole supply chain example proceeded so smoothly. It’s simple: we collaborate, and we share information at every step.

Until now, all the data required to get the freight where it needed to go had to be re-keyed at every point and communicated manually via phone calls, faxes, or emails. But technology allows us to start unlocking and retaining value in the transaction. The key to this entire collaborative process is found in having to capture the information only once.

With automation and integration within each supply chain member’s own operations and between the different organizations, the result can be reduced errors, saved time, and execution with minimal effort. Imagine a manufacturer’s ERP system to manage stock notices that vital materials are running low. It can automatically send the supplier a message, which in turn triggers actions for the exporting and importing agents. This not only increases accuracy, it also reduces transactional costs between organizations.

By automating and integrating we can work to create a high-velocity, low-touch supply chain where every member collaborates more effectively and efficiently. When providers work together, their shared logistics technology frees up staff across all borders to be more accurate, more productive, and ultimately more successful.

Nachi Mendelow is general manager of business development, Africa, for WiseTech Global, a developer of cloud-based software solutions for the logistics industries.

Related News

New strategy for Sweden’s regional development cooperation in sub-Saharan Africa 2016-2021

On 22 June 2016, the Swedish Government adopted two new strategies for regional development cooperation: in sub-Saharan Africa and in Asia and the Pacific Region.

Sub-Saharan Africa

Sweden’s new regional strategy in sub-Saharan Africa will contribute to strengthened capacity to face cross-border challenges and opportunities at regional level. The strategy focuses on four areas: democratisation, human rights, human security, and climate change and environmental adaptation measures.

“Climate change and armed conflicts are two examples of challenges that transcend national borders and demand increased regional cooperation. The new strategy shows Sweden’s broad commitment to development, security and climate in the region,” says Minister for International Development Cooperation and Climate Isabella Lövin.

The new regional strategy amounts to SEK 450 million per year. In total, the strategy encompasses SEK 2.7 billion until 2021. The strategy will be implemented by the Swedish International Development Cooperation Agency (Sida) and the Folke Bernadotte Academy.

Direction

Within the framework of this strategy, Swedish development cooperation with sub-Saharan Africa is to contribute to increased regional integration and strengthened capacity to face cross-border challenges and opportunities at regional level.

The strategy will apply for the period 2016-2021 and comprises a total of SEK 2 700 million, of which SEK 2 670 million is intended for activities implemented by the Swedish International Development Cooperation Agency (Sida) and SEK 30 million is intended for activities implemented by the Folke Bernadotte Academy (FBA).

Within the framework of the strategy, Sida is expected to contribute to:

A better environment, sustainable use of natural resources, reduced climate impact and strengthened resilience to environmental impact, climate change and natural disasters

-

Strengthened capacity of regional actors to work towards sustainable management and use of common ecosystem services and natural resources

-

Strengthened capacity of regional actors to work towards increased resilience against climate change and natural disasters, including capacity for food security

-

Increased production of, and access to, renewable energy

Strengthened democracy and gender equality and greater respect for human rights

-

Enhanced capacity of regional actors to work towards strengthened democracy and the rule of law, gender equality and increased respect for human rights, with a focus on the rights of women and children

-

Enhanced capacity of civil society and media to work towards accountability and respect for human rights at regional level

Better opportunities and tools to enable poor and vulnerable people to improve their living conditions

-

Strengthened opportunities for increased economic integration and trade

-

Improved conditions, especially for women and young people, for productive employment with decent working conditions

-

Strengthened capacity of regional actors to work towards sustainable solutions concerning refugee situations and migration flows, and embrace the positive effects of migration

Human security and freedom from violence

-

Strengthened capacity of regional actors for peace and reconciliation

-

Strengthened capacity of regional actors to combat violent extremism

-

Increased influence and participation by women and young people in processes for peace and reconciliation

Within the framework of the strategy, the FBA is expected to contribute to:

-

Strengthened capacity for regional actors to prevent, resolve and deal with the effects of armed conflict

-

Strengthened capacity for regional actors to implement the UN Security Council resolutions on women, peace and security

Asia and the Pacific Region

Regional development cooperation in Asia and the Pacific Region will focus on strengthening regional actors and states to take greater responsibility concerning the environment and climate, human rights, democracy and gender equality. The focus is to be on cross-border challenges, where solutions can best be sought in regional cooperation.

“We focus regional development assistance in Asia and the Pacific Region to the places in the region facing the greatest challenges – in the human rights area and with regard to the effects of climate change and environmental damage,” says Ms Lövin.

Asia and the Pacific Region will be hardest hit by climate change. The effects are particularly evident for small island states in the Pacific Ocean.

“We now have the opportunity to contribute to strengthened regional cooperation on adaptation, renewable energy and other matters.”

The new regional strategy amounts to SEK 300 million per year. In total, the strategy encompasses SEK 1800 million for the strategy period.

Related News

From LDC services waiver to GSPs: Follow-up

Fully harnessing the potential of services and inter-linkages between the services sector and the economy as a whole calls for policy coherence and a holistic approach to services regulation and services trade liberalization, especially for LDCs, where service sector is becoming more and more important.

The recent services Waiver for LDCs that was adopted at the Eighth WTO Ministerial Conference in 2011 and extended in Nairobi in 2015 could potentially serve as a stepping stone towards further services liberalization. Aimed at least-developed countries only, the waiver has a potential to provide a comparative advantage so much needed to kick-start LDCs services trade on international markets.

However, while estimating real life benefits of the preferences generated by the Waiver, one has to consider the following issues:

-

Are such preferences granted in sectors of interest to LDCs?

-

Are they already applied to all trade partners in practice, and consequently fell into mere recognition of MFN treatment?

-

Are the preferences really beneficial to LDCs in providing broader and better market access to them?

-

What can be a next step on a way of liberalizing access for service providers from LDCs that could provide a higher degree of certainty and accountability on both sides of services trade?

The aim of the meeting on 8 July 2016 is to discuss and shed light on these questions.

The LDC Services Waiver – Operationalized?

A first look at preferences granted, constraints persisting, and early conclusions to be drawn

The notion of special treatment for LDCs in services goes back to the 2003 Decision of the Council for Trade in Services on Modalities for the Special Treatment for Least-Developed Country Members in the Negotiations on Trade in Services. Quite general, this decision aimed at defining negotiating modalities for LDCs in the area of services to ensure that Members would take the special situation of LDCs into consideration when negotiating with them. Interestingly, the LDC modalities recognised among others:

“the importance of trade in services for LDCs […] beyond pure economic significance due to the major role services play for achieving social and development objectives and as a means of addressing poverty, upgrading welfare, improving universal availability and access to basic services, and in ensuring sustainable development, including its social dimension”.

The text also highlighted the need for Members to open their services markets as a priority in sectors of interest to LDCs. A bit more than 2 years later, further developments on the matter were reflected in the 2005 Hong Kong Ministerial Declaration:

“In the services negotiations, Members shall implement the LDC modalities and give priority to the sectors and modes of supply of export interest to LDCs, particularly with regard to movement of service providers under Mode 4”.

The declaration recalled and reaffirmed “the objectives and principles stipulated in (…) the Modalities for the Special Treatment for Least-Developed Country Members in the Negotiations on Trade in Services adopted on 3 September 2003” and in relation to services negotiations, recognized “the particular economic situation of LDCs, including the difficulties they face, and acknowledge that they are not expected to undertake new commitments”.

After several years of discussions on how to effectively implement those LDCs modalities, trade ministers finally adopted on 17 December 2011 a waiver to enable developing and developed-country Members to provide preferential treatment to services and service suppliers of least-developed countries (LDCs). The waiver, initially granted for 15 years from the date of adoption, releases WTO Members from their legal obligation to provide nondiscriminatory (MFN) treatment to all trading partners (GATS Article II), when granting trade preferences to LDCs. It effectively operates as a new LDC-specific “Enabling Clause for services” and follows a two-track approach.

Two years later, however, with no progress made, Ministers came back to the issue with a subsequent decision on the ‘Operationalization of the Waiver Concerning Preferential Treatment to Services and Service Suppliers of Least Developed Countries’, adopted on 7 December 2013 at the Ninth Ministerial Conference in Bali. That decision established a process which foresaw that a High-Level Meeting – an idea akin to that of the Signalling Conference of 2008, or a pledging conference – would be held six months after the submission of a Collective Request by the LDC Group. 4 After a significant exercise in fundamental research commissioned by the LDC Group conducted by ICTSD, WTI Advisors and ILEAP and financed by TAF, the LDC Group developed the Collective Request and circulated it to Members in July 2014, followed by the High Level Meeting in February 2015, at which Members announced how they intended to respond to the LDC request.

Members had agreed that those intending to grant preferences under the Waiver would follow up by submitting specific and detailed notifications of their intended preferences by July 2015. While meeting the deadline proved challenging to some, it is remarkable given the rather sluggish beginnings of the process that to date no less than 23 Members – including several developing countries – have indeed submitted notifications and started implementation, namely Australia, Brazil, Canada, Chile, China, Chinese Taipei, the European Union, Hong Kong (China), Iceland, India, Japan, Republic of Korea, Liechtenstein, Mexico, New Zealand, Norway, Singapore, South Africa, Switzerland, Thailand, Turkey, Uruguay and the United States. Building on this success, the Nairobi Ministerial Conference in 2015 led to the decision to extend the waiver until 31 December 2030. The decision encourages Members that have not notified preferences to do so, and Members that have notified one to provide technical assistance and capacity building in order to allow LDCs to actually benefit from the preferences granted. It also asks Members to address regulatory barriers as defined in GATS article VI:4 and mentions tasks to be fulfilled by the Council for Trade in Services for a quicker and more efficient implementation of the notified preferences.

As they say, however, the proof is in the pudding. While the range of preference-granting countries itself is noteworthy, the breadth, depth and real-life relevance of the preferences offered is less obvious. As a contribution to this process, this paper carries out an in-depth assessment of the preferences offered in the context of the Waiver and the challenges facing LDCs in taking advantage of them. It starts with an analysis of the offers notified so far by preference-granting countries using both a quantitative and qualitative approach. The first step consists in analyzing each preference granted by WTO Members in a matrix. For this purpose, a comparison of the preferences was made with the DDA offer and the best PTA of each granting Member as well as with the Collective Request.

As a second step, the data accumulated in the matrix was used to draw preliminary conclusions on the actual relevance of the preferences in practice: are they granted in sectors of interest to LDCs? Are they already applied to all trade partners in practice, and consequently fell into mere recognition of MFN treatment? Generally, are preferences really beneficial to LDCs in providing broader and better market access to them? Part 3 then moves to identifying the factors that may affect – negatively of positively - LDCs’ ability to effectively benefit from preferences in the area of services, based on existing literature and empirical evidence. It reviews, among others, issues around binding supply side constrains including LDC competitiveness, firm level constrains, policy impediment, or global and regional market requirements.

The paper concludes by suggesting a comprehensive, structured and permanent support system for trade preferences in services following the original idea of a “Generalized System of Trade Preferences” proposed by UNCTAD in the mid-60s. Such an approach would not only focus on reviewing the implementation of the waiver but also on addressing supply side constrains, information and analysis deficit while providing a constructive forum for dialogue among government representatives, IGOs, private sector and relevant stakeholders.

Related News

Facilitating e-commerce can stimulate growth and development – DG Azevêdo

E-commerce can play a pivotal role in fostering growth and raising living standards, particularly for developing countries, Director-General Roberto Azevêdo told a workshop organized by the governments of Mexico, Indonesia, South Korea, Thailand and Australia and supported by the International Trade Centre (ITC).

The workshop, held at the WTO on 5 July, focused on addressing the challenges that inhibit consumers and entrepreneurs from fully seizing the trade opportunities that e-commerce can bring.

“By reducing the trade costs associated with physical distance, e-commerce allows businesses to access the global marketplace, reach a broader network of buyers and participate in international trade. Broader dissemination of such technologies means that the trade opportunities generated by e-commerce are also available to businesses in developing countries, with some of them making significant headway in recent years,” Director-General Azevêdo said.

Among the obstacles developing countries face in fully participating in e-commerce are high digital infrastructure costs, lack of compliance with legal and fiscal requirements of foreign e-markets, underdeveloped financial and payment systems and low consumer trust.

The workshop also looked at the constraints faced by micro, small and medium enterprises (MSMEs) in developing countries, which often “do not have the ability to get around these problems,” DG Azevêdo said. Africa and the Middle-East share less than 2 per cent of the world e-commerce market, the workshop heard.

Participants also discussed the role the WTO can play in lowering these barriers, through the development of multilateral rules to harmonize procedures and reduce operational costs. “We could look at how we can support small suppliers to market their products in a timely fashion, with competitive prices and reliable customer support,” DG Azevêdo said. “This would help consumers to have full confidence in buying from MSMEs in the digital environment.”

The event heard presentations from Arancha González, Executive Director of the ITC and Carlos Grau Tanner, Director-General of the Global Express Association; and from representatives of the World Economic Forum, CUTS International, the United Nations Conference on Trade and Development (UNCTAD), the International Centre for Trade and Sustainable Development (ICTSD) and Consumer International. The presentations were followed by a discussion with WTO members.

MIKTA Workshop on Electronic Commerce

Remarks by WTO Director-General Roberto Azevêdo

I’d like to start by congratulating the MIKTA countries – Mexico, Indonesia, Korea, Turkey and Australia – for their initiative and for inviting me to join in these discussions.

It is clear that electronic commerce provides some huge opportunities – for growth, development and job creation.

Therefore, I think it is equally clear that the international community should strive to ensure that these opportunities are made available to all.

E-commerce has been a feature of international trade for quite some time, but its importance has increased substantially in the past decade. The rapid technological advances and the steady increase in the number of internet users are changing the traditional way of doing business and conducting trade.

The numbers speak for themselves.

Between 2000 and 2015, Internet penetration increased from 6.5 per cent to 43 per cent of the global population.

In 2013, global business-to-consumer e-trade accounted for an estimated $1.2 trillion.

Meanwhile, the value of global business-to-business e-trade exceeded $15 trillion.

By reducing the trade costs associated with physical distance, e-commerce allows businesses to access the global marketplace, reach a broader network of buyers and participate in international trade.

Broader dissemination of such technologies also means that the trade opportunities generated by e-commerce are also available to businesses in developing countries, with some of them making significant headway in recent years.

But there is a long way still to go. Four billion people in the developing world remain offline. Of the nearly one billion people living in LDCs, around 850 million do not use the Internet. So this is a major challenge.

Being connected is essential – but we can’t just assume that people will automatically benefit from greater opportunities once they are online. It is a necessary condition, but it is not sufficient. A range of other economic and technological barriers can still cause problems – such as underdeveloped financial and payment systems, low consumer trust, and weak legal and regulatory frameworks.

Bigger companies have the ability to get around these problems, while smaller companies often do not.

It was not surprising that e-commerce was a major topic at the workshop last month on Micro, Small and Medium Enterprises (MSMEs), which was organized by another group of Members.

So I think it could be useful to look at how new technologies can facilitate the participation of smaller players in the global economy.

We could look, for example, at how we can ensure that, through multilateral rules, MSMEs benefit from harmonized procedures and reduced operational costs.

We could look at how we can support small suppliers to market their products in a timely fashion, with competitive prices and reliable customer support. This would help consumers to have full confidence in buying from MSMEs in the digital environment. Otherwise, consumers will always prefer the well-known big suppliers.

There are a range of interesting ideas out there. I have met with a number of people from the industry in recent weeks, including the founder of Alibaba, Jack Ma. He is proposing the creation of e-hubs, or digital free trade zones, for small firms. We will continue that discussion in the weeks ahead.

The intersection between MSMEs and e-commerce was also raised by business representatives at the ‘Trade Dialogue’ event that we facilitated here at the WTO on 30 May.

Some 60 business leaders attended that meeting, representing small and large companies, from developed and developing countries.

They identified e-commerce as an area where the WTO can make an important contribution. In addition to MSME issues, they also suggested that steps could be taken on:

- enhancing transparency and non-discrimination;

- harmonizing e-commerce practices and procedures, and;

- improving consumer protection.

So I think those conversations have provided some food for thought.

Clearly, the debate is complex and encompasses a wide range of issues, but it is interesting that some themes seem to recur.

I think it is important now that we take time to engage in these discussions. We need to better understand this subject – and so this workshop is very welcome. And I am pleased to see there are a range of different organisations and perspectives represented here today.

In exploring these issues, I think we should seek to build on the work that is already under way. UNCTAD, the ITC, and others, are working on these issues. WTO Members themselves are continuing their conversations in the context of the Work Programme on e-commerce, under the stewardship of Ambassador Suescum, as the Friend of the General Council Chair on e-commerce.

But, perhaps as a result of our two successful ministerial conferences, it seems that the debate is significantly more dynamic than it has been in recent years. There is a new air of openness and positivity, which I think has to be a good thing.

Now it is for Members to decide whether and how to take these discussions further within the WTO.

It is encouraging that one member has already put forward a non-paper on e-commerce issues, and I understand that others may also be forthcoming.

I hope that today’s workshop takes us closer to understanding the challenges and opportunities offered by e-commerce – and that it provides some meaningful, concrete ideas which can be fed into further discussions.

So I urge you all to have a very focused and results-orientated conversation on how the WTO can help.

I am looking forward to hearing the outcomes of your deliberations.

Thank you.

Speech delivered by ITC Executive Director Arancha González

I believe it is accurate to say that the Geneva trade community is witnessing an e-commerce revolution.

Just last week ITC, with the cooperation of DHL and E-Bay, held a ‘Caravan of Peace’ at the United Nations to showcase the power of going digital for small and medium sized enterprises (SMEs). Yesterday ITC held an e-commerce caravan and souk right here at the WTO with entrepreneurs from Cote d’Ivoire, Ethiopia, Morocco, Rwanda, Senegal, and Syria not only selling the physical goods from their countries but showcasing how these goods can be purchased using online platforms which ITC has helped to develop.

And UNCTAD is continuing to coordinate a number of the agencies in Geneva around an e-trade for all partnership that will be launched at UNCTAD XIV in Nairobi later this month. Therefore this event today organized by MIKTA is perfectly timed. I thank you for inviting ITC to be part of this.

In the WTO e-commerce has been on the agenda for many years. But recently the interest levels have increased. Why?

Because this is a booming market. Just in Africa this market is estimated to grow from US$ 8 billion in 2013 to US$ 50 billion in 2018. Because virtual selling is particularly adaptable for SMEs all around the world to connect with customers hence avoiding costly intermediation and capturing a higher value of the sale.

But for this form of trade to work, the rules of trade need to be supportive. The aim must be to create a trade policy architecture that balances the need to regulate e-commerce with supporting what is at the core of digital solutions: fast, technology driven, less expensive and more convenient. Despite the disruptive nature of new technologies and ways of transacting, effective e-commerce remains premised on three main elements from the trade policy perspective: trade facilitation, non-tariff barriers and services.

The WTO Trade Facilitation Agreement is the framework with which goods purchased online can get from point A to point B without unnecessary red tape. This is why having it enter into force is a crucial ingredient to make e-commerce happen. And improving it to ensure a fast route for small transactions – a big part of what MSMEs trade on-line – so called de-minimis, would be of great help to them.

This will mean also better identifying the non-tariff barriers that exist which may prevent this from happening at optimum efficiency.

The ability to offer globally connected digital solutions is very much linked to services regulations that support rather than hinder the establishment of platforms and payment solutions, specifically financial services; that support faster and more performing logistic and distribution services; that protect consumers through insurance services. And which embrace, rather than restrict competition in the related sectors. There is a clear need to better understand the services related policies around e-commerce and I am pleased to see that this will be one of the issues discussed during the sessions today.

ITC is working with policy makers and SMEs around the world to make e-commerce and digital solutions an integral part of the business ecosystem. Building on the information we have collected through our work, we have launched two publications over the last few months, which provide some important and practical information to help better position e-commerce.

The first one, ‘International e-commerce in Africa: the way forward’ is a practical assessment of the challenges and opportunities which SMEs face in Africa in using e-commerce. Despite e-commerce representing an estimated $15 trillion in annual business-to-business transactions and over $1 trillion in annual business-to-consumer trade, developing countries, especially in Africa, still have substantial untapped potential to exploit this approach.

The current share of consumer e-commerce by African enterprises is below 2% for example. This can be a game changer for SMEs in Africa and in the developing world.

A second publication launched in China last month on ‘Bringing SMEs onto the e-Commerce Highway’, examined major policy challenges in four key segments of the online retail: 1) establishing an online presence for business, 2) international e-payments, 3) international delivery and 4) after-sale services. It also contains a number of real-life case examples from developing country SMEs and provides checklists that explain what needs to be at the firm level, in the immediate business environment and at the national policy level in order for e-commerce to function smoothly and for SMEs to benefit from it.

ITC will continue to be your partner in providing both the important policy perspective on e-commerce and the on the ground experiences.

For example, with the World Bank, we are supporting MSMEs in Jordan, Morocco and Tunisia to increase exports of their goods and services through ‘virtual marketplaces’. This has ranged from supporting public and private sector discussions on these issues with the aim of targeting policy changes to improve the business environment for e-commerce polices and regulations, to helping SMEs become better equipped in terms of e-payment and risk insurance systems. In Rwanda we are working to empower SMEs to internationalise through the ‘made in Rwanda’ e-commerce platform in partnership with DHL.

Just yesterday at the ITC JAG, I signed a partnership agreement with Ebay, which will bring together ITC’s on the ground expertise with SMEs with Ebay’s enviable track record in providing platforms for entrepreneurs to use digital solutions to reach a consumer base in real time.

The cooperation will include ensuring MSMEs ITC works with gain higher on-line visibility as well as access to Ebay’s network of fulfilment centers to ensure more cost effective logistics. The possibilities here are incredible- the merging of ITC’s trade and market intelligence with data from Ebay’s research and analysis will help SMEs to better target product and market combinations in e-commerce.

Today as you discuss the policy elements around e-commerce I ask you to pay special attention to the practical ways of ‘doing e-commerce and e-trade’.

In my view, the trade policy architecture does not have to be remade for e-commerce, rather we have to ensure that it responds to the reality on the ground. WTO tools allow for adaptability to evolutions, as it happened for telecom and financial services Post Uruguay Round.

In your work to take the issue of e-commerce forward in the WTO, I encourage you to ensure that MSMEs are part of the intelligence gathering that will go into this process. It is an opportunity and a tool for them to multiply their customer base and deepen their trading footprint. Our collective aim must be to facilitate connectivity.

Thank you.

Related News

The differentiated effects of non-tariff measures

Non-Tariff Measures (NTMs), and in particular technical regulations, are here to stay. Diversity of effects calls for a new policy paradigm.

Trade costs matter

A large number of empirical studies and surveys document the importance of trade costs as a factor determining the competitiveness of developing country-based enterprises and national trade performance. This includes not only export values but also participation in international production networks and diversification into new products and new markets. Strikingly, most trade cost components have fallen for all groups of countries but more slowly in low-income countries. Transaction costs remain high for countries with lower levels of per capita income[1]. As a consequence, these countries may have not been able to take up crucial trade, production and development opportunities.

Trade transaction costs consist of two broad categories. The first category encompasses exogenous factors such as geographic distance. The second category includes endogenous trade costs that are a direct consequence of policy choices. Standard trade policy instruments such as tariffs have been at the core of policy actions at both the multilateral and regional level for a long time. Overall results are mixed, and the scope for further significant tariff liberalization has shrunk in most countries and most sectors. The Trade Facilitation Agreement recently concluded by WTO members contains provisions on expediting customs procedures and cooperation between customs and other relevant authorities and is expected to reduce transaction trade costs. This is important and good news. However, it does not address another, probably even more important trade cost component.

NTMs, the new frontier

The new frontier for trade policy has shifted towards Non-Tariff Measures and in particular technical regulations (sanitary and phytosanitary (SPS) measures and technical barriers to trade (TBTs)). Figures 1(a) and 1(b) illustrate the distribution of NTMs across broad categories and sectors[2].

Figure 1: NTMs incidence

")

")

For each category, both the frequency index (i.e. the percentage of HS 6 digit lines covered) and coverage ratio (i.e. the percentage of trade affected) are reported. We observe that international trade flows are highly regulated through the imposition of technical barriers (TBT), with more than 30 per cent of product lines and almost 70 per cent of world trade affected. Quantity and price control measures affect about 15 percent, and sanitary and phytosanitary measures (SPS) about 10 per cent of world trade. When looking at the coverage of NTMs by broad category, one can observe that agriculture is the most affected, with the majority of world agricultural trade subject to SPS and TBT measures.

While technical regulations are not new trade policy instruments, they have become core determinants of market access opportunities especially for firms in developing countries. Recently published UNCTAD research shows that low-income countries’ exports of agricultural goods to EU markets are disproportionately negatively impacted by SPS measures.[3] The result is consistent with the hypothesis that market access is increasingly determined by the capability to comply with the regulatory framework and that countries at a lower level of development find themselves outcompeted. However such mechanisms may also be at work within any specific country.

Theoretical insights suggest that the effect of a technical regulation on export performance may depend on the size of a firm, provided that size is associated with (for instance) productivity, and hence with the ability to overcome the additional costs of exporting imposed by new technical regulations. In other words, not all firms will be able to cope with the higher costs of new technical regulations, be it a fixed cost of adaptation and/or a variable trade cost. Ongoing UNCTAD research on Peruvian firms exporting to Latin American Integration Association countries supports these theoretical insights.

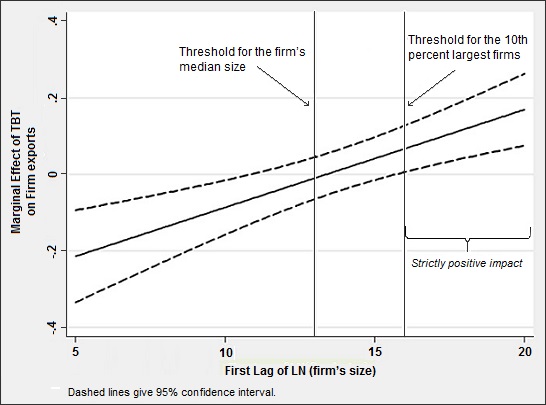

Results indicate that technical regulations tend to push small firms away from world markets and leave the largest shares of exports to large multinational firms, further strengthening their global influence. Figure 2 shows the effect of technical barriers to trade on export value as a function of the size (measured by lagged total exports) of exporting Peruvian firms. The largest 10 per cent of Peruvian exporters are found to benefit from the implementation of a new TBT in LAIA destinations in terms of export value while the smallest 50 per cent are likely to lose.

Figure 2: The impact of TBTs on Firms’ exports

Note: estimates obtained for data on Peruvian firms exports to ALADI countries during the 200-2014 period.

Implications for policy

While technical regulations may impede exports and in particular exports of small and medium producers in developing countries, they are important instruments to achieve sustainable development. Technical regulations and standards have primarily non-trade objectives, such as public health and safety, and protecting the environment. It would be misleading to look at technical regulations as we look at tariffs. In light of the existing evidence more efforts have to be devoted to facilitate and possibly streamline the implementation of NTMs.

-

First, governments should ensure that NTM requirements are scientifically based. Public authorities should also accelerate the standardization process. Collaboration with private certifiers can play an important role in this process.

-

Second, developing countries’ concerns should be addressed specifically. The inclusion of these countries in the standard-setting process should be increased, and special attention should be paid to their small and medium firms. Intensifying technical assistance and capacity building activities in order to help developing countries and their exporters to fulfil NTM requirements is highly desirable. Special efforts should also be made in order to integrate these activities with national ones.

-

Third, in addition to technical assistance and capacity building programs, private sector based initiatives could also be contemplated to promote the participation of small and medium enterprises in export markets. Governmental and non-governmental organizations could instigate the establishment of cooperatives within which small and medium enterprises could exchange and collaborate on issues related to the compliance with technical regulations on international markets. Encouraging long term exporter contracts could also be useful.

-

Fourth, as leading firms in developing countries are key actors in driving compliance with standards, their active implication should be recognized by public authorities and non-governmental institutions.

-

Finally, systemic and systematic collection of relevant data should be placed at the core of political agendas at the national regional and international levels.

[1] Arvis, Jean-François & Shepherd, Ben & Reis, José Guilherme & Duval, Yann & Utoktham, Chorthip, 2013. “Trade Costs and Development: A New Data Set.” World Bank – Economic Premise, 104, pp1-4.

[2] Originally published in UNCTAD, 2015. “Key Statistics and Trends in Trade Policy 2015.”

[3] Nicita, Alessandro & Murina, Marina, 2015. “Trading with Conditions: The Effect of Sanitary and Phytosanitary Measures on the Agricultural Exports from Low-income Countries.” forthcoming in The World Economy.

Fugazza, Marco & Olarreaga, Marcelo & Ugarte, Christian, 2016. “Trading with Hurdles: Too Big to Stumble.” Policy Issues in International Trade and Commodities Research Studies Series #78, UNCTAD.

Related News

tralac’s Daily News Selection

The selection: Tuesday, 5 July 2016

Trade-Related Developments: report to the Trade Policy Review Body from the Director-General (WTO)

The number of trade remedy investigations initiated by WTO Members has increased during the review period. Metal products, and in particular steel products, chemicals and plastics and rubber account for the largest shares of these initiations. As for previous review periods, more initiations were recorded than terminations, and anti-dumping measures made up the overwhelming majority of trade remedy actions. The analysis of sunset reviews of anti-dumping and countervailing measures initiated in 2008 and 2009 seems to indicate that there is no discernible change in extensions versus expiry of measures coinciding with the financial crisis.

During the review period, the Committees on Sanitary and Phytosanitary measures and on Technical Barriers to Trade saw significant developments. The share of SPS notifications from developing countries remained high, accounting for about two-thirds of all notifications, and confirming the increased participation of developing countries in the total number of notifications since 2007. An increase in the number of notifications does not, however, automatically imply greater use of measures taken for protectionist purposes. In the TBT area, the Committee has recorded a significant increase in the number of specific trade concerns. The 116 new and previously-raised STCs discussed during review period confirm the upward trend, observed over the past years, of a greater number of STCs being raised in the TBT Committee. [Download, pdf]

Namibia: Standards of cattle production (The Namibian)

The furore over the new import regulations imposed by South Africa on Namibian livestock is surprising. A long time ago already, Namibian farmers decided that our internal market was too small and our farming environment too inhospitable to support mass-production of livestock and meat. Insufficient production capacity would inhibit us competing at regional level with other SADC countries whose populations numbered tens of millions of people, especially with the 55 million South Africans; let alone compete in a rapidly globalising world. We therefore decided to concentrate on the quality of our livestock and meat rather than its quantity, as this would give us a competitive advantage.

COMESA: ‘Let’s harmonise sanitary, food regulation’ (Daily Mail)

There is need to harmonise sanitary and phyto-sanitary regulatory frameworks aimed at addressing food security, food health and trade and industrial development in the region, COMESA assistant secretary general Nagla El Hussainy has said. During the seventh COMESA technical meeting on SPS, Ms El Hussainy said trade within COMESA, Southern African Development Community and East African Community grew from $30.6bn in 2004 to $102.6bn. And Ministry of Agriculture permanent secretary Julius Shawa said investments in SPS capacity is still low with most countries lacking coherence in the establishment of SPS priorities and related investments.

Kenya and Rwanda’s manufacturing sector: AfDB reports examine technology, innovation and productivity policy issues

Rwanda (pdf): This approach of leapfrogging technology transfer would also allow Rwanda to participate in global value chains which in general is problematic because of its landlocked status and resulting high transport costs in both time and money to major ports. Air transport is hence the only feasible option and that is only feasible for high value components such as electronics. The likely target areas would be global technology for local markets, where Rwanda could seek to capture industrial activity in emerging consumer or industrial goods for sale into the EAC. Buying relocaters would fit well with this since, for example, the acquisition of failing refrigerator plant in, say, Europe would provide the basis for a partnership deal with European suppliers of that firm to continue to provide the inputs that Rwanda would turn into fridges for the EAC market. Rwanda should experiment in the art of quantum leaps in technology by setting up a state-owned industrial holding company that buys select failures in the industrialised world. The criteria for selecting losers should be roughly as follows:

Kenya (pdf): Tax incentives remain an important strategy for attracting foreign investors wishing to exploit the natural resource base in Kenya and those viewing Kenya as an export platform for EAC and Eastern and Southern Africa regional markets. Recent manufacturing incentives schemes in Kenya have, however, been ineffective. Reform of the incumbent incentives including those related to export zone processing, manufacturing under bond, and other incentives involving tax refunds is therefore necessary to address the challenges reducing their utilization. Review should target ensuring quick tax refunds and tight control of the refund process to reduce cases of abuse of the schemes including elimination of corruption. As these are potentially contradictory objectives, improved monitoring technology and institutional reforms will be necessary. The current schemes also need to be reviewed to reward more use of high technology and research and development.

Kenya: Diaspora remittances increase slightly in May 2016 (Central Bank)

Remittance inflows to Kenya increased by 2.3% in May 2016 compared with 1.7% growth in April 2016. The increase in May 2016 is reflected in inflows from Europe and the rest of the world. Cumulative inflows in the 12 months, to May 2016, increased by 11.1%, to $1,636 million, from $1,472 million in the year to May 2015. [Multinationals, tea pickers lock in fight that threatens the industry (Daily Nation)]

Ugandan investors negotiate tough junction into EAC (Daily Monitor)

Contrary to what their counterparts who have raised their respective national flags high making use of the freedoms through investing into other member states, Uganda is taking baby steps. Uganda has witnessed an influx of Kenya’s blue print brands such as KCB, Equity Bank, Fina Bank, Insurance Company of East Africa, chain retail supermarkets like Nakumatt and Tuskys, Brookside Dairies which bought off the country’s largest dairy corporation. Tanzania, the region’s second economic power, has also established foot prints in Uganda through Bakhresa Group with brands like Azam Television, mineral water, confectionaries and soft drinks. Uganda’s presence in other member states is hard to trace apart from a few Simba Telecom outlets which have spread wings into Kenya and Tanzania. This begs the big question: Is Uganda more porous compared to her neighbours?

RSA citrus trade sees Brexit opportunities (Fruitnet)

South Africa’s citrus industry says the UK Brexit vote could see a "normalisation" of citrus trade between Southern Africa and the UK, unencumbered by protectionism, tariffs and technical barriers to trade. The South African Citrus Growers Association says at present UK plant health regulations are the same as those of the EU, as these were harmonised in 1992. Entry requirements for citrus shipped from Southern Africa to UK are the same as entry requirements for citrus shipped to the mainland European member states of the European Union. “An independent UK will in all likelihood introduce its own plant health regulations, or at least remove or rescind those regulations that have no impact on the UK. Since the UK does not have any citrus (produce any citrus), plant health regulations on citrus imports should be easier to comply with than present EU regulations.”

Kenya’s forex reserves dip by Sh28bn as CBK fights to stabilise shilling after Brexit (Business Daily)

Kenya’s foreign currency reserves plunged by Sh28 billion last week as the Central Bank of Kenya used its fire power to stabilise the market in the wake of financial markets’ turmoil that followed Britain’s recent vote to leave the European Union. The CBK’s reserves stood at $7.237 billion (Sh732.45 billion) at the end of last week, equivalent to 4.73 months of import cover, having declined by $280 million from the previous week’s $7.517 billion (Sh760.8 billion) or 4.91 months of import cover, according to weekly official data. [Brexit chaos pushes Kenya to back burner (Daily Nation)]

Brexit makes SABMiller deal sweeter (IOL), Headwinds for India: Brexit and its impact via other countries (LiveMint)

Lesotho: Country Partnership Framework 2016-2020 (World Bank)

The World Bank Group Board of Executive Directors on 30 June endorsed a five-year Country Partnership Framework for Lesotho, expected to deliver $154m over 2016 to 2020 to projects in support of the Mountain Kingdom’s efforts to improve public sector efficiency and effectiveness and promote private sector job creation. Government spending in Lesotho is highly correlated with volatile SACU revenues (see Figure 1(b)). In the last decade, Lesotho shifted from an export driven economy to one driven by government spending. In the past four years, the government maintained public spending above 60% of GDP. The biggest contributor to this spending was the wage bill, which grew from 18.9% of GDP in 2012 to 23.1% in 2015/16 – among the highest in the world. However, such growth in public expenditure, which is dependent on volatile SACU revenues, has made the macroeconomic environment less stable, and cannot sustainably drive economic growth to address Lesotho’s extreme poverty and shared prosperity needs. Lesotho urgently needs to restore fiscal sustainability, focusing in particular on public spending. Lesotho is facing three adjustment scenarios - back-loaded, insufficient and ordered adjustment. [Download]

A selection of postings on Zimbabwe’s economy, trade prospects:

Rand might save the Zim economy (IOL)

The deVere Group, a global adviser on specialist global financial solutions, is one of those championing Zimbabwe’s adoption of the rand. As its manager for Zimbabwe, Botswana and Mozambique, Shane Helberg, recently said: “Whilst the rand perhaps isn’t as weighty as the US dollar for international trade - as it’s more volatile against major currencies - it must be noted that the dollar has not been effective in arresting the freefalling economy in recent times. Using one primary currency, the rand, for commerce, is likely to be beneficial for several key reasons.” For one thing, using just one semi-convertible currency rather than the present basket, reduces confusion and uncertainty and creates stability and certainty, which foreign investors want. Adopting the rand should also boost trade links with South Africa, Zimbabwe’s major trading partner. One could add, in particular, that it would boost Zimbabwean exports to South Africa. [Prioritise addressing policy inconsistency: IMF (NewsDay)]

Govt to set up standards regulatory authority (The Herald)

Zimbabwe’s Minister of Industry and Commerce Mike Bimha has said the appointment of Bureau Veritas as an import inspection agent is an interim measure and Government is working towards setting up a standards regulatory authority. Government last year signed a four-year Consignment-Based Conformity contract with the French global company. Minister Bimha said the Ministry of Industry and Commerce is in the process of identifying staff for the new regulatory authority.

Zimbabwe explores Tanzania to grow exports (NewsDay)

Zimbabwe's trade facilitation body, ZimTrade has called on local companies to consider growing exports to Tanzania’s pharmaceuticals, construction and leather products sectors to improve the country’s trade position and ease the cash crisis. Official figures show that Tanzania’s import bill for 2015 stood at $9,7bn, with China being the largest supplier, contributing 44%. Regionally, South Africa has a 5,6% share, while Zimbabwe contributes less than 1%. In 2015, 79% of Zimbabwe’s exports to Tanzania were construction and mining equipment, with the remaining 21% being mainly clothing and textiles, paper and printing services, as well as tobacco.

Egypt's BoP deficit jumps 260% in Jul-Mar on falling tourism revenues, transfers (Ahram)

Egypt’s balance of payments deficit leaped a whopping 260% in the first nine months of the current fiscal year due to ongoing fall of tourism receipts, services income and transfers, the Central Bank of Egypt said Sunday. The overall BoP deficit reached $3.6bn from July to March in the fiscal year 2015-2016, compared to $1bn in the same period of the previous year as the current account deficit rose by around 75% to reach $14.5bn from $8.3bn.

SA-India trade update (GCIS)

India is now SA 6th largest trade partner. Trade in 2015 was almost R95bn. Trade with India represented 4.9% of SA imports and 4.1% of exports. South Africa’s Trade statistics shows that India’s exports to South Africa increased from R29bn in 2011 to R54bn in 2015, while South Africa’s exports to India increased from R24bn in 2011 to R41bn. The trade surplus is in favour of India. Efforts are underway to promote SA exports of especially value-added products. In order to deal with the trade imbalance, the dti has undertaken outward missions to India including: [SA-France trade update (GCIS)]

Zanzibar Declaration on timber trade: update on implementation (TRAFFIC)

East African member states will establish a Secretariat to oversee the effective implementation of the Zanzibar Declaration and Bi-Lateral Timber Trade Agreements, with Zambia also requesting to become a signatory. The announcements came following a meeting hosted by the Kenya Forest Service and WWF Kenya to build on the commitments made in the Zanzibar Declaration on Illegal Trade in Timber and Forest Products that was finalized and signed in September last year at the XIV World Forestry Congress in Durban, South Africa.

OECD-FAO Agricultural Outlook 2016-2025

This year’s Outlook includes a special focus on the prospects and challenges facing agriculture in sub-Saharan Africa. The rise of the middle class, rapid urbanisation, as well as increased commercial interest in Africa’s resources and farmland, will all shape the sector’s development. As the region faces rapid population growth, agriculture will continue to be the single largest source of employment for many young people. The Outlook foresees a further increase of food imports into sub-Saharan Africa, because demand for food is expected to grow at more than 3% over the coming decade, while total agricultural production is projected to rise by only 2.6% a year, despite improvement in productivity.

Africa Carbon Forum 2016 closes in Kigali

US and WTO partners begin implementation of the Expansion of the Information Technology Agreement (USTR)

Namibia’s Competition Commission appoints acting CEO, Vitalis Ndalikokule (The Namibian)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

Making politics work for development: Harnessing transparency and citizen engagement

Too often, government leaders fail to adopt and implement policies that they know are necessary for sustained economic development.

Political constraints can prevent leaders from following sound technical advice, even when leaders have the best of intentions. Making Politics Work for Development: Harnessing Transparency and Citizen Engagement focuses on two forces – citizen engagement and transparency – that hold the key to solving government failures by shaping how political markets function.

In today’s participative world, citizens are not only queueing at voting booths, but are also taking to the streets and using modern communication technology to select, sanction, and pressure the leaders who wield power within government. This political engagement can function in highly nuanced ways even within the same formal institutional context and across the political spectrum, from autocracies to democracies. Political engagement becomes unhealthy when leaders are selected and sanctioned on the basis of their provision of private benefits rather than public goods, giving rise to a range of government failures.

“This book not only provides an authoritative statement of what we know about how to align political incentives with the interests of society, but it does so with an eye to making change happen even in the face of political opposition. The World Bank will never be the same again” – James Robinson, University Professor, Harris School of Public Policy, University of Chicago.

The solutions to these failures lie in fostering healthy political engagement within any institutional context, and not in circumventing or suppressing it. Transparency – citizen access to publicly available information about the actions of those in government and the consequences of these actions – can play a crucial role by nourishing political engagement. The report distills policy lessons for governments, international development partners, and civil society on how best to target transparency initiatives so that the provision of public goods becomes the focus of political contestation.

“This pathbreaking report places politics at the heart of the development dialogue – exactly where it belongs. It provides constructive ideas for harnessing the forces of transparency and citizen engagement in ways that are suited to diverse institutional contexts so that reform leaders can overcome political constraints to their countries’ development goals” – Asli Demirgüç-Kunt, Director of Research, Development Research Group, The World Bank.

Even so, unhealthy political engagement may persist. But to build institutions that are capable of tackling public goods problems, politics needs to be addressed and cannot be side-stepped. Targeted transparency is one way to move in the right direction: it complements everything else policy makers do and holds the potential to make politics work for development rather than against it.

“A lesson for us at the World Bank also comes out of this research. We can do more… to work with our clients to diminish political constraints to achieving development goals… To do this we have to overcome the fear of talking about politics, and confront it as part of the challenge of development. That is what we are doing through this report” – Kaushik Basu, Senior Vice President and Chief Economist, The World Bank.

This Policy Research Report was prepared by the Development Research Group of the World Bank by a team led by Stuti Khemani. The other authors of the report were Ernesto Dal Bó, Claudio Ferraz, Frederico Finan, Corinne Stephenson, Adesinaola Odugbemi, Dikshya Thapa, and Scott Abrahams.

Related News

USTR announces major expansion of trade preferences for least developed and African countries

Aiming to promote poverty alleviation and economic growth in poorest countries

The Office of the United States Trade Representative announced on 30 June 2016 the outcome of the Obama Administration’s Annual Product Review under the Generalized System of Preferences (GSP) program.

This review adds new duty-free status for travel goods (including luggage, backpacks, handbags, and wallets) for Least Developed Beneficiary Developing Countries (LDBDCs) and African Growth and Opportunity Act (AGOA) countries.

GSP is a 40-year-old trade preference program under which the United States provides duty-free treatment to many imports from beneficiary developing countries and additional products for LDBDCs.

“Trade preference programs such as GSP and AGOA can make a powerful contribution to lifting people out of poverty and supporting growth in some of the poorest countries in the world, while also reducing costs to American consumers and businesses,” said U.S. Trade Representative Michael Froman. “We have used these programs to give beneficiary countries a vital leg up vis-à-vis more advanced competitors.”

Based on the Administration’s review of various issues and petitions related to eligibility of products under the GSP program, President Obama also made several other determinations today affecting product coverage under GSP, including the following:

-

The removal of products from specific GSP countries where the country is sufficiently competitive and so as to no longer need tariff preferences to compete in the U.S. market, including fluorescent brightening agents and PET resin from India;

-

The granting of competitive need limitation (CNL) waivers, ensuring continued GSP duty-free benefits, for 114 products from 15 countries.

The full results of the GSP 2015/2016 Annual Review are available on the USTR website and will be announced in the Federal Register.

Background

Under the GSP program, approximately 5,000 products from 122 beneficiary developing countries and territories, including 43 least-developed countries, are eligible for duty-free treatment when exported to the United States. Nearly 1,500 of these products are reserved for duty-free treatment for LDBDCs only. In 2015, the total value of imports that entered the United States duty-free under GSP was $17.4 billion.

The Trade Preference Extension Act (TPEA) of 2015 gave the President, for the first time, the authority to add certain travel and luggage goods products to GSP, subject to the regular, petition-driven review process. The 27 HTS subheadings cited in the TPEA included luggage, handbags, backpacks, and pocket goods (such as wallets).

As part of the GSP 2015/2016 Annual Review, an interagency committee led by USTR (the GSP Subcommittee of the Trade Policy Staff Committee) received and considered requests seeking:

-

to add or remove products from the list of those eligible for duty-free treatment under GSP;

-

to waive product exclusions for certain countries based on statutory requirements related to competitiveness (CNLs); and

-

to withdraw or limit a country’s eligibility for GSP trade benefits based on statutory eligibility criteria, including whether a country is taking steps to afford internationally recognized standards for worker rights, whether it provides important investor protections including enforcement of arbitral awards, and the extent to which a country adequately and effectively protects intellectual property rights.

For those petitions accepted for review, the USTR-led committee holds public hearings, solicits public comments, and – in the case of product petitions – reviews analyses prepared by the U.S. International Trade Commission of the economic impact of product eligibility decisions on domestic industries and consumers. Any change to the lists of products or countries eligible for GSP benefits requires a presidential determination.

Related News

Report to the TPRB from the WTO Director-General on trade-related developments

This trade-monitoring report reviews trade-related developments during the period from 16 October 2015 to 15 May 2016. During this seven-month period, there seems to have been a relapse in WTO Members’ efforts at containing protectionist pressures. Not only is the stockpile of trade-restrictive measures continuing to increase, but also more new trade restrictions were recorded during the period, covering both import and export measures.

The implementation of new trade-restrictive measures by WTO Members increased over the review period. Since mid-October 2015, WTO Members applied 154 new trade-restrictive measures – an average of 22 new measures per month compared to 15 in the previous interim report. Import tariff increases, customs procedures and various local content measures constitute the main factors behind this upward trend in the overall monthly figure. The 22 new trade-restrictive measures adopted per month by WTO Members are close to the peak observed in 2011 of 23 new measures per month.

During the same period, WTO Members implemented 132 measures aimed at facilitating trade. At almost 19 trade-facilitating measures per month, this represents an increase over the previous mid-year report’s monthly average of 16 measures. However, the trade-facilitating monthly average remains below the monthly average of trade-restrictive measures, thus reversing the positive trend identified over the past years.

Overall, the stockpile of restrictive measures introduced by WTO Members continues to grow. Of the 2,835 trade-restrictive measures (including trade remedies) recorded for WTO Members since 2008, only 708 had been removed by mid-May 2016. The total number of these restrictive measures still in place now stands at 2,127 – an increase of more than 11% during the review period. Although some WTO Members have been eliminating trade-restrictive measures, the rate at which this is done is far too low to dent the overall stockpile of restrictive measures. Of the total number of trade-restrictive measures recorded for WTO Members since 2008, the share of eliminations, or roll-back, makes up 25%.

World trade was volatile in 2015 as diverging outlooks for developed and developing economies unsettled global financial markets and prompted sharp movements in commodity prices and exchange rates. The volume of world merchandise trade grew by 2.8% last year as trade fell sharply in the first half of the year before recovering in the second half. Weak import growth in developing economies (0.2%) was cushioned by stronger import demand in developed countries (4.5%). Import growth was particularly weak in large emerging economies such as China (-4%) and Brazil (-15%). Meanwhile, exports grew slightly faster in developing economies (3.3%) than in developed countries (2.6%). This was balanced by stronger positive import growth in the United States (6.5%) and the European Union (4.5%). Despite positive trade growth in volume terms, the dollar value of world trade fell sharply (-13% for merchandise, -6% for services), largely as a result of lower commodity prices and the general appreciation of the U.S. dollar.

Prospects for 2016 and beyond remain uncertain. The most recent WTO trade forecast of 7 April 2016 predicted merchandise trade volume growth of 2.8% in 2016, unchanged from 2015, but volatility is likely to persist. Exports of developed and developing economies should grow at around the same rate (2.9% in the former and 2.8% in the latter). Meanwhile, imports of developed economies are expected to outpace those of developing countries, with an increase of 3.3% compared to a rise of 1.8%. Preliminary trade volume statistics for the first quarter of 2016 indicate that world trade fell around 1% in the first quarter of 2016 compared to the last quarter of 2015.

The number of trade remedy investigations initiated by WTO Members has increased during the review period. Metal products, and in particular steel products, chemicals and plastics and rubber account for the largest shares of these initiations. As for previous review periods, more initiations were recorded than terminations, and anti-dumping measures made up the overwhelming majority of trade remedy actions.

The analysis of sunset reviews of anti-dumping and countervailing measures initiated in 2008 and 2009 seems to indicate that there is no discernible change in extensions versus expiry of measures coinciding with the financial crisis.

During the review period, the Committees on Sanitary and Phytosanitary (SPS) measures and on Technical Barriers to Trade (TBT) saw significant developments. The share of SPS notifications from developing countries remained high, accounting for about two-thirds of all notifications, and confirming the increased participation of developing countries in the total number of notifications since 2007. An increase in the number of notifications does not, however, automatically imply greater use of measures taken for protectionist purposes. In the TBT area, the Committee has recorded a significant increase in the number of specific trade concerns (STCs). The 116 new and previously-raised STCs discussed during review period confirm the upward trend, observed over the past years, of a greater number of STCs being raised in the TBT Committee.

In the area of agriculture, despite poor notifications’ compliance recorded for some Members, the whole membership continued to use Article 18.6 of the Agreement on Agriculture (AoA) to ask questions on the implementation of commitments. A large number of these questions focused in particular on Members’ domestic support policies.

This report suggests that general economic support measures implemented by WTO Members are on the rise. The monthly average of 14 such measures recorded in the review period approaches the number recorded immediately after the onset of the global financial crisis. However, the numerical counting of such measures and programmes does not provide any indication regarding the extent of these measures, nor their potential impact. The main beneficiaries of such support during the review period included multiple sectors, infrastructure programmes (including several energy-related projects), various industries in the manufacturing sector, the agricultural sector and the telecommunications sector. Several programmes provided specific support to export-related activities or enterprises, including SMEs. Several important policy developments in a very diverse range of services sectors took place during the review period. The overwhelming majority of these services measures see either further liberalization of trade in services or the strengthening and clarification of relevant regulatory requirements.

The OECD has contributed two topical boxes to this report. The first looks at the evolving agricultural policies and markets and the implications for multilateral trade reform. The second seeks to assess the gains from implementing the WTO Trade Facilitation Agreement (TFA).

Several other important trade-related developments also took place during the review period, including in the areas of the Trade Facilitation Agreement, the Information Technology Agreement expansion and the Agreement on Government Procurement.

The overall assessment of this monitoring report has outlined the profound volatility which characterizes world trade today and the current unsettled nature of international financial markets. Despite a number of positive developments, the global environment remains challenging. To address slow economic growth, Members need to get trade moving again, not put up barriers between economies. The best safeguard we have against protectionism is a strong multilateral trading system.

Recent Economic and Trade Developments

Overview

The volume of world merchandise trade partially recovered in the second half of 2015 following a sharp decline in the first half that affected all major economies to varying degrees. Import growth was sluggish in developing Asia and negative in regions that predominantly export natural resources. These slowdowns were cushioned by stronger import demand in Europe and North America as economic activity picked up in those regions.

Global trade volume growth for the whole of 2015 was 2.8%. Despite the modest, positive growth in global trade volumes, the dollar value of world merchandise trade fell sharply in 2015, dropping by 13% to US$16.0 trillion largely as a result of lower commodity prices and a general appreciation of the U.S. dollar. The value of world commercial services trade also declined by 6% to US$4.7 trillion in 2015.

Several factors contributed to the lacklustre performance of trade in 2015, including: slowing economic growth in China and the rebalancing of the country’s economy away from investment and towards consumption; recessions in other large developing economies, particularly Brazil; falling petroleum prices, which reduced the export revenues of oil producing countries; and volatility in exchange rates and financial markets, possibly exacerbated by divergent monetary policies in the United States, Europe and China.

Economic Developments

2015 marked the fourth consecutive year with world trade volume growth below 3%, as well as the fourth year in a row with world trade growing at close to the same rate as world GDP. Growth rates for trade and output in 2015 were also below their average rates since 1990 of 5% and 2.7%, respectively. The slow pace of trade growth relative to GDP growth over the past four years stands in contrast to the period from 1990 to 2008, during which merchandise trade grew 2.1 times as fast as world GDP on average.

The recent spell of slow trade growth is unusual, but not unprecedented, and as a result its importance should not be exaggerated. World trade volume growth was in fact weaker between 1980 and 1985, when five out of six years saw trade growth below 3%, including two years of outright contraction.

Strong fluctuations in exchange rates since 2014 have had a strong impact on nominal trade statistics, most of which are denominated in current U.S. dollars. In January 2016, the U.S. dollar was up 19% compared to January 2014. Although the dollar has weakened somewhat since then, it was still up 13% in April 2016 compared to January 2014. The appreciation of China’s yuan has also moderated since the last monitoring report.

Dollar appreciation can cause trade denominated in other currencies (e.g. intra-EU trade) to be undervalued when measured in dollar terms. As a result, trade statistics in nominal dollar terms should be interpreted with care under current circumstances.

Prices for oil and other primary commodities bottomed out in January-February but have rebounded somewhat since then. The traditional inverse relationship between the level of the U.S. dollar and the price of oil has continued to hold, with the recent easing of the dollar mirrored by a modest rise in fuel prices. Despite the rebound, fuel prices were still down around 60% in April compared to the beginning of 2014. Further production declines could bring about a partial recovery in fuel prices, although a return to US$100 oil/barrel is unlikely.

Other Selected Trade Policy Developments

Trade Facilitation

Following the adoption of the amendment protocol, delegations started to launch their domestic processes for ratifying the Trade Facilitation Agreement. As at 3 May 2016, 77 acceptance instruments were deposited, which represents more than 70% of the ratifications required for the Agreement to enter into force. Members also continued to notify the commitments they designated for implementation as of the Agreement’s entry into force. As at 3 May 2016, 83 of those so-called “category A-notifications” were presented. Delegations already started to notify the commitments they consider to require more time (“category B”) and the acquisition of implementation capabilities through the provision of assistance and support for capacity building (“category C”). Four such category B and C notifications were received by time of reporting (3 May 2016).

The new WTO Trade Facilitation Agreement Facility that was launched in 2014 was put into action in 2015 and aims to provide a platform for information on WTO trade facilitation and to help developing and least-developed members find the assistance they need for the preparation of notifications, ratification of the Agreement, and for its implementation. It also aims to coordinate donor assistance.

To achieve these goals, a new Facility website was created to provide information on donor programmes, to provide case studies and other materials to assist with implementation and to track progress on ratification and notifications received. The Facility conducted, or was involved in, eight events for Parliamentarians to help them gain a better understanding of the new Agreement. The Facility assisted Members to prepare their category A, B and C notifications by conducting national and sub-regional workshops; and by coordinating with partner organizations to conduct workshops. It also assisted Members to find support for implementation of the Agreement in a variety of ways, for example, by providing donor information on the Facility website, by organizing workshops featuring the available donor support, and by direct matchmaking.

Government Procurement