Search News Results

New UN report reveals barriers to inclusive development and highlights key steps to progress

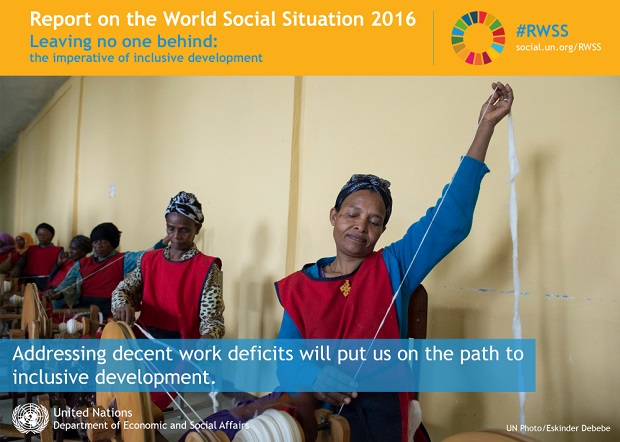

The United Nations Department of Economic and Social Affairs has just released its 2016 Report on the World Social Situation, which includes important new findings about persisting inequalities in education and economic opportunity and, challenges the international community to work harder to break down barriers to participation.

While there has been unprecedented global social progress, it has not been evenly experienced. Some 40 per cent of the world’s population does not have access to education in a language they understand. Children of ethnic minorities and those who are disabled are much less likely to finish their primary and secondary educations. Even among those who are educated, youth, migrants, and indigenous peoples continue to be underpaid and unpaid. In some cases, social and economic inequalities have actually worsened.

The theme of this year’s report is ‘Leaving No One Behind – The Imperative of Inclusive Development.’ It examines key causes of social exclusion and identifies social, economic and political disadvantages that some groups face as a result. The report concludes with concrete policy recommendations that are central to the 2030 Sustainable Development Agenda.

“The Sustainable Development Goals recognize that development will only be sustainable if it is inclusive,” said Wu Hongbo, the UN Under-Secretary-General for Economic and Social Development, adding: “Pursuing development grounded in social justice will be fundamental to achieving a socially, economically and environmentally sustainable future for everyone.”

A central pledge of that Agenda is to ensure that ‘no one is left behind;’ inclusiveness and shared prosperity are at the core of sustainable development. The report argues that in order to promote social inclusion, barriers to participation must be broken down by revising laws, policies, institutional practices, discriminatory attitudes and behaviours, and taking steps to ensure that participation is easier.

The report’s analysis focuses on three sets of indicators: those measuring access to opportunities – such as education and health; access to employment and income; and those measuring participation in political, civic, and cultural life.

Of course, many of these indicators overlap – lower levels of health and education tend to correlate with high levels of poverty and unemployment, for example.

Such inequalities tend to persist even after the structural conditions that created them change. That is, formal barriers may disappear, but discrimination can operate in less overt ways to perpetuate inequality.

For example, labour markets continue to reflect socially driven distinctions based on race, age, gender and other personal attributes, even after the effects of educational attainment and other sociodemographic traits are taken into account.

“Not only are these differences in life chances fundamentally unfair, they also lead to loss of human potential and development opportunities,” said Assistant Secretary-General for Economic and Social Development Lenni Montiel.

Such trends extend to participation in political, civic, and cultural life as well, such as in voting patterns and engagement in political activities. It is perhaps unsurprising, then, that the data reveals lower levels of trust and confidence in policing and justice systems among ethnic and racial minorities.

It is not enough for countries to remove discriminatory policies; subtler forms of discrimination, through attitudes and entrenched practices, must be confronted and rooted out, contends the report.

While there is no “one size fits all” solution for all countries, certain efforts like a universal approach to social policy and integration of measures that tackle discrimination have been successful in the past.

The report also advocates that stakeholders must promote inclusive institutions. Examples of ways to achieve that goal are by engaging with civil society, supporting equitable work environments, and challenging exclusionary attitudes.

Such changes, however slow to unfold, are necessary for sustainable progress, especially at the highest levels in powerful institutions.

Related News

Rwanda hailed for enhancing cross-border trade

Rwanda has been lauded for its efforts to promote cross-border trade, which is viewed as a vehicle for economic growth and poverty eradication among developing countries.

This was noted during the opening of a two-day Enhanced Integrated Framework (EIF) Board Meeting in Kigali yesterday.

The meeting also combined with a workshop on cross-border trade.

It sought to consolidate key policies and strategies with a focus on promoting broad-based economic growth, employment creation, trade development and poverty reduction in Least Developed Countries (LDCs).

The workshop brought together high-level government officials, as well as representatives of EIF and other partners involved in the implementation of the National Cross Border Trade Strategy in Rwanda.

The EIF is a core part of the Sustainable Development Goals, directly referenced in Target 8.A.

The EIF is the only Aid for Trade programme exclusively designed for Least Developed Countries.

The programme brings together partners and resources to support the world’s poorest countries in using trade for poverty reduction, inclusive growth and sustainable development, according to officials.

Over the past seven years, the EIF global partnership supported 142 projects in Least Developed Countries, equivalent to over $200 million.

According to Eloi Laourou, the LDCs Group coordinator, hosting the meeting in Rwanda was very important given the remarkable progress that the country has registered over the years.

“There is no substitute for Rwanda’s rapid growth in trade, technology and innovations among the least developed countries in the region; the country is becoming a model LDC for rapid economic growth and we applaud you for that,” Laourou said during his opening remarks.

He called on governments to ease the policy and legislative environment which, he said, not only helps the LDCs to boost their trade but also attracts local and foreign investment.

“Sound public policies stimulate sound public-private partnerships, and thus sound private sector investment,” he said.

Ratnakar Adhikari, the EIF executive director, hailed Rwanda for promoting cross-border trade, especially focusing on women, saying it would help them enhance their income, knowledge, expertise, entrepreneurship abilities among other opportunities.

Adhikari observed that supporting women is emphasised under the global sustainable development goals.

“Rwanda is not only one of the fastest growing economies in Africa, but it’s also leading the way in cross-border trade and provides a good example of how charting economic development progress in a unified front can significantly attract foreign investments and boost economic growth,” he added.

EIF donated $3 million for construction of cross-border markets in Karongi District and the Cyanika market (in Burera District) along the Uganda border, according to Adhikari.

Francois Kanimba, the Minister for Trade, Industry and EAC affairs, said that cross-border trade generated $ 300 million this year – both formal and informal trade.

It is estimated that between 70-80 per cent of cross-border traders are women, with 90 per cent of these women traders relying on cross‑border trade as their sole source of income.

Kanimba said Rwanda will retain friendly policies to facilitate doing business, security and infrastructure development.

“EIF is one of Rwanda’s key development partners. Not only has EIF brought in their own projects but they have also helped us leverage wide-ranging support from the private sector and other development partners to implement the national cross-border trade strategy,” said the minister.

“This, in turn, has helped the Government bring economic development and opportunities to our border regions and to some of our most vulnerable citizens, including women in informal cross-border trade,” he added.

Based in Geneva, EIF supports 51 least developed countries. Over the past seven years, the EIF global partnership has supported 142 projects in LDCs, equivalent to over $200 million, according to officials.

Related News

ECCAS leaders discuss security, trade

President Paul Kagame, yesterday, attended the 8th Extraordinary Session of the Heads of State of the Economic Community of Central African States (ECCAS) in Libreville, Gabon.

The Heads of State summit, chaired by President Ali Bongo Odimba of Gabon, was also attended by Presidents Idriss Deby Itno of Chad and Faustin-Archange Touadera of Central African Republic.

Other countries were represented by high-level officials.

Rwanda rejoined the 11-nation regional bloc in 2015 as part of efforts to tap into the potential in the region in the form of investments and duty free markets.

The leaders discussed a number of pertinent issues, including the rise of terrorism in parts of the region as well as active militia groups in DR Congo, Central Africa Republic, and Burundi who threaten to disrupt peace and security in the region.

President Bongo, who’s also the current Chairperson of the ECCAS, called on member states to continue embracing the spirit of fraternity and partnership in their efforts to tackle challenges facing the central African region.

The Heads of State summit also reviewed the elections that took place in Gabon this year and the issues around them.

The meeting also discussed intra-Africa and cross-border trade, as well as maritime and aviation development within the region.

ECCAS is in the process of setting up a free trade area in a bid to boss trade among member countries.

Member states have since been requested to submit a list of products they intend to export to the other partner states upon the launch of the free trade area.

To fund the establishment and operationalisation of the free trade area, the bloc’s ministers in charge of trade and finance agreed on a special tariff to be imposed on imports by member states for products originating outside the region.

The proceeds were earmarked as contributions to meet the bloc’s operating costs as well as compensate potential revenue loss.

Fifty per cent of the proceeds are to be used for compensation of potential revenue losses resulting from the liberalisation of tariffs within the ECCAS free trade area.

The grouping fixed a 0.4 cent levy on all imports from outside the region.

However, Rwanda has since sought to be exempt from the funding model as the country has committed to use the import levy model in two other cases.

Rwanda is signatory to a similar import levy arrangement of 1.4 per cent under the East African Community (EAC) with proceeds going to joint infrastructure projects.

The country is also committed to another import levy under the African Union, whereby 0.2 per cent levy on eligible imports is expected to raise about $1.2 billion every year.

Instead, Kigali wants to meet its financial commitments to the ECCAS Secretariat through other means.

ECCAS is comprised of Angola, Burundi, Cameroon, Chad, Central African Republic, Congo, DR Congo, Equatorial Guinea, Gabon, Rwanda, and Sao Tome & Principe.

Related News

President Kenyatta addresses EALA

President Uhuru Kenyatta is challenging the East African Legislative Assembly to concert its efforts in ensuring the integration process is not only on course, but geared towards meeting the aspirations and high expectations of the people. The President is emphatic that the people of the region want nothing else but a Community that works for all and that is effective.

In this regard, the President is calling on the Assembly to up the stakes on the sensitisation process and on its consultations with legislative processes including engagement with the Partner States’ National Assemblies as envisioned under Article 65 of the Treaty of the Establishment of the EAC.

The President’s remarks were delivered on his behalf by the Speaker of the Senate, Rt Hon Ekwe Ethuro at the Special sitting of the 3rd Meeting of the 5th Session held at the Parliament Chambers (Senate) yesterday. In attendance were EALA Members, former Members led by Speaker Emeritus, Rt Hon Abdirahin Abdi and representatives of the Private Sector. The President noted the various achievements realised by the Community to date.

“I note with appreciation the progress that the Community has made to date. Eleven (11) years ago, we established the EAC Customs Union. It has generated positive results. This is clearly demonstrated by the trend in intra-EAC trade over the period. For instance, the value of the total intra-EAC trade rose from US Dollars 1.8 billion in 2004 to US Dollars 5.1 billion US Dollars in 2015 representing a significant growth of 190 percent,” he said.

The President hailed the business community whom he termed keen partners and drivers of the integration proces. “I laud and commend them for their efforts in boosting our investment profile and partnership in creating jobs for our people. We are therefore duty-bound to support them in addressing the challenges they face in conducting and expanding their businesses in the region,” he added.

The speech noted the various challenges the region continues to face. “There still exists a considerable number of trade restricting measures that are a hindrance to actualizing free trade in the EAC. Among the obstacles, include long clearing procedures; road blocks and changes in applicable regulations, which together, contribute to impact trade negatively,” it said in part.

The Head of State reiterated Kenya’s commitment to the integration process and cited the infrastructure projects as keen in the integration process.

“We have every reason to take pride in what we have achieved in here in Kenya. We have commenced work on the Standard Gauge Railway (SGR) and we expect it to be operational by the middle of 2017. On-going development works on the Port of Mombasa and regional roads confirms Kenya’s commitment to building and achieving sound infrastructure for the greater benefit of the region,” he said.

The President noted that EAC needed a strong oversight body and hailed the EALA for rising up to the occasion.

“For example, among the notable achievements of this Assembly include the passage of over 20 Bills cutting across various areas of integration. The Assembly’s legislative priority and performance in the last four years has indeed exhibited clear appreciation and understanding of matters that are of great relevance and urgency in deepening and widening the EAC integration,” the President remarked.

In his remarks, the Speaker of EALA, Rt Hon Daniel F. Kidega, maintained that citizens of the region were keen to see the process of integration fortified.

“I can confirm the Assembly is often inundated by citizens’ concerns to see the Common Market agenda become a reality. Essentially, it is important that we open our East African markets to African people and beyond to create jobs and opportunities. Likewise, we must avoid situations where we export jobs and allow cheap goods from outside the EAC to permeate the local markets,” Speaker Kidega noted.

The Speaker noted the fight against Corruption needs to be taken a notch higher in the Partner States. “At the regional level, EALA is on the verge of enacting a Bill on Whistleblowers and on Anti-Corruption, thereby, putting in place a legal framework to report instances of corruption to authorities – given the fact that the vice knows no borders,” he added.

The Speaker termed matters of peace and security as of paramount importance to the development in the region and further called for the fight against terrorism to be sustained.

He termed the approximation of the national laws in order to create uniformity within the Partner States as necessary and called on the Partner States to move with haste in the matter.

An EALA Report adopted at the Sitting shows that Republics of Rwanda and Uganda have each approximated ten pieces of laws each, Republic of Kenya (6 laws), United Republic of Tanzania (6 laws) and Republic of Burundi (3 laws). Approximation of National Laws is vital in line with the Article 126 (2b) of the Treaty for the EAC is fundamental.

The Siting came to an end with the next plenary expected to be held in January in 2017.

Related News

Britain won’t turn its back on Africa following Brexit – MP Lord Paul Boateng

Brexit does not mean that the British government will turn its back on Africa, Lord Paul Boateng, a Member of the United Kingdom’s House of Lords said Monday.

Speaking at the first ever Africa Trade Week rum which is being hosted by the Economic Commission for Africa and the African Union, Mr. Boateng said Brexit presents Africa and the UK with an opportunity to “put development at the heart of our trading relationship with Africa in a way frankly that it has not always been in relation to the EPAs, let’s be frank about it”.

“The UK recognizes that and we will seek every opportunity to minimize the disruption in our trading relationship and take every opportunity to seize this chance to re-fashion the relationship between the UK and Africa in terms of trade so intra-African trade becomes an opportunity which we can seize together,” he said.

Contributing to debate on Africa-E.U. Economic and Trade Cooperation and Brexit implications for Africa, Mr. Boateng assured participants, including African Ministers of Trade, Finance and Transportation as well as senior government officials, heads of Regional Economic Communities (RECs), African CEOs and executives, representatives of international development agencies, civil society and others, that trade relations between the UK and Africa will not be affected following Brexit.

“There is clearly a need in the aftermath of Brexit for there to be a degree of reassurance given to Africa that Brexit doesn’t mean that the United Kingdom is going to turn its back on Africa and I’m able to assure you that right across the political divide in the UK, in both Houses, Africa and the UK’s historic link with Africa remains central to our thinking,” he said.

“Yes there’s uncertainty at this time, that is inevitable, when such a momentous decision is made,” said Mr. Boateng.

“Yes there is a hazard always when you think about the scale of the task that lies ahead in terms of mapping out the future of the trading relationship between the UK and Africa but I think I can give the absolute assurance that we see this in the UK as an opportunity to be seized.”

He said he was concerned by the issue of infrastructure in most African countries. Mr. Boateng was born and brought up in the Gold Coast in Ghana.

“I am the grandson of cocoa and cassava farmers. My grandmother grew cassava, my grandfather grew cocoa and when I look at our village in Tafo in the eastern region of Ghana, two things strike me, first of all, that in the 1950s there was a direct rail link between Tafo, a heart of cocoa growing region and Takoradi, which at that time was our main port,” he told participants.

“That rail link no longer exists and that has had a damaging effect on agriculture in Ghana but Ghana is not alone in seeing the deterioration of its infrastructure so the United Kingdom recognizes the importance of infrastructure in terms of promoting intra-African trade.”

The second matter which I can’t but help notice, he said, is that right next door to my grandmother’s farm was a West African Cocoa Research Institute and that was a major resource for West Africa in terms of agricultural support and extension and research at the highest level so it produced every year a handful of PhDs now sadly due to decades of neglect and the impact of the structural adjustment of the 70s and the 80s, that emphasis on higher education and the link between higher education, science, technology and innovation and agriculture simply went now we are seeking to revisit that but I would argue that that too is a very important part of our struggle in order to increase agricultural productivity of Africa.

“Without that we are going to be in difficulties but the good news is it seems to me that is changing and the UK and our department of international development is making its contribution to that,” Mr. Boateng said.

Participants will be in Addis Ababa for the week attending the first ever Africa Trade Week, a multi-stakeholder platform for the advancement of the Continental Free Trade Area (CFTA) and intra-African Trade.

Related News

African countries should align AGOA and their developmental integration agenda – Minister Davies

The Minister of Trade and Industry, Dr Rob Davies has emphasised the importance of export diversification and industrialisation in Africa. He was speaking in Addis Ababa, Ethiopia where he was moderating the Africa Trade Week Panel Discussion on Africa Growth and Opportunity Act (AGOA) and the Continental Free Trade Area (CFTA).

The session considered AGOA implementation over the remaining period of the legislation granting the trade preference up to 2025. It also reflected on the future of Africa-US trade relations beyond AGOA based on the type of trade arrangements that would support Africa’s regional integration agenda. Minister Davies said African countries need to increase their utilisation of the trade preferences granted by the United States (US) under AGOA to attract Foreign Direct Investments into priority sectors that are eligible under AGOA and that can favour industrialisation.

“African countries should also ensure that there is alignment between AGOA and their development integration agenda, focus on their industrialisation and preserve policy space aimed at enhancing efforts to diversify their exports base and integrate supply chains so as to take advantage of market access opportunities under AGOA,” added Minister Davies.

The Panel also highlighted the low levels of utilisation of AGOA trade preferences by eligible countries in Sub-Saharan Africa. These are largely attributed to supply-side constraints, productive capacity constraints, onerous rules of origin requirements, lack of capacity to meet stringent sanitary and phytosanitary measures, labelling requirements in the US, as well as the fact that some products of export interest to the African countries are not covered under AGOA.

In terms of future US-Africa trade relations, the panel stated that the US is expected to advance a trading relationship based on reciprocity. Minister Davies noted that the US proposed a number of options for post AGOA trade relations. He indicated that these options need to be carefully considered by African countries to ensure that their developmental priorities are not compromised.

Panel members agreed that the Continental Free Trade Area (CFTA) that is currently under negotiation can be a driver of structural transformation for sustained economic growth and enhanced intra-Africa trade and investment in the continent.

Earlier in the Africa Trade Week programme, former South African Ambassador to WTO, Dr Faizel Ismail spoke on a coherent approach to achieving the African Union’s Agenda 2063 through the CFTA. Ismail indicated that the success of the CFTA and the implementation of continent’s integration agenda would be dependent on the adoption of an inclusive approach. He indicated that there is a need for academics and civil society to be greater involved in trade policy formulation.

“So they need to identify these challenges and opportunities for Africa. But they also need to become participants in the process of negotiating the Continental Free Trade Area (CFTA) so that the CFTA becomes a living process that includes the dynamics of both the different stakeholders on the ground and also that it is customised to the actual conditions and objectives of the people on the ground,” he added.

Related News

Op-Ed: The impact of Brexit on South Africa

South Africa can be reasonably confident that by the end of 2019, at the latest, the UK will not legally be part of the European Union (EU), nor a signatory to the EU’s myriad trade agreements, including the recently agreed Economic Partnership Agreement (EPA) between the EU and the South African Development Community (SADC). What is less clear is the nature and character of the trading relationship the UK will have with the EU after Brexit is formalised.

Equally unclear is the kind of trading relationship South Africa will have with the UK. As the below quotes illustrate, opinions are sharply divided:

‘Brexit will be terrible for Africa’s largest economies’ – Quartz Africa, 2016

‘For South Africa, the implications (of Brexit) through direct trade links will be relatively minimal’ – Daniel Mminele, Deputy Governor of South African Reserve Bank, 2016

The UK and the EU face a period of continuing uncertainty and complexity as they come to terms with the consequences of Britain’s vote five months ago to “leave”. The process of how and when the UK leaves, the nature of the all-important post-Brexit UK-EU relationship and the impact of the post-Brexit agreement on Britain’s national income are significant unknowns.

Of primary concern to South Africa’s interests, especially exports, is the impact of Brexit on the UK economy. The most significant threat of Brexit to South Africa will arise from a reduced export demand if the UK economy is damaged as a result of leaving the EU. Predicting the impact of Brexit on South Africa is further complicated by the need to negotiate a new South Africa-UK trade agreement to replace the existing EU agreements, which will no longer apply to South Africa-UK bilateral trade after Britain leaves the EU.

In assessing the impact of Brexit on South Africa, two stand-out questions therefore arise:

-

How important is the UK to the South African economy?

-

What impact will Brexit have on the UK economy and, in particular, South Africa’s interests in the UK economy?

How Important is The UK to the South African Economy?

According to the most recent economic data, in 2015 South African merchandise trade, both imports and exports, to the 28 members of the EU amounted collectively to $38.3-billion, representing approximately 26% of South Africa’s total merchandise trade. The EU28 is by far South Africa’s largest trading partner, almost 40% bigger than its second most important trading partner, the Southern African Development Community (SADC). The UK accounts for approximately 15% of all South Africa’s trade with the EU, representing 3.7% of South Africa’s global trade.

.jpg)

In terms of exports, in 2015 South African merchandise exports to the 28 members of the EU amounted collectively to $15.1-billion, representing approximately 20% of South Africa’s total exports. The UK received 20% of all South Africa’s exports destined for the EU, representing 4% of South Africa’s global exports. South Africa’s exports to the UK are dominated by three key items: precious metals and stones (39% of all exports to the UK); fruits and nuts, mainly fresh fruit (16%) and; vehicle and vehicle parts (15%). For certain items and regions, for example agriculture from the Western Cape, UK trade is important to the regional economy.

In 2015, the UK was South Africa’s third most important export market for agriculture. In 2014, approximately 40% of South Africa’s exotic fruit exports, 30% of all fruit exports and 25% of wine exports were destined for the UK market. Clearly, high-value South Africa agricultural exports to the UK are important.

.jpg)

A summary of key South African merchandise exports to the UK in 2015.

While significant, amounting to just over $3-billion in 2015, the importance of South African merchandise exports to the UK should not be exaggerated. In 2015, South Africa exported more to the rest of sub-Saharan Africa ($18.7-billion) than to the EU and more to India ($3.1-billion) than to the UK. That year South Africa’s exports to Botswana alone were approximately 15% more than to the UK.

But South African-UK economic links extend far beyond merchandise trade. According to Moody’s, South Africa has been the largest recipient of British foreign direct investments (FDI) in Africa, standing at 30%, with a particular focus on mining and financial services. According to the South African Reserve Bank, a significant 46% of South Africa’s global direct investments originate from the UK, amounting to approximately $54-billion, representing 60% of all EU FDI in South Africa. South Africa’s FDI in the EU is also disproportionally concentrated on the UK, standing at 30%. In the area of FDI, finance and portfolio investments, the South Africa-UK relationship is significant.

Brexit therefore has the potential to impact South Africa on numerous fronts. The most obvious pathways are:

-

Bi-lateral South Africa-UK trade, either positively or negatively. In particular, slower UK growth (as a result of Brexit) impacting South Africa’s trade (and investments). Lower UK growth will lead to reduced UK imports which will, in turn, lessen South African exports to the UK.

-

Access to the Single Market for British companies and South African companies located in the UK.

-

South Africa-EU trade and collaboration agreements will in future not include the UK.

What impact will Brexit have on the UK economy and, in particular, South Africa’s interests in the UK economy?

Moody’s believes the biggest threat to South Africa will be “reduced export demand” if the Brexit negotiations damage the UK economy. A key concern for the UK, South Africa and South African firms located in the UK is the level of access the UK will have to the EU Single Market after 2019 and how that level of access will impact on the UK economy.

The long-term impact of Brexit on the UK economy will depend on how and on what terms the UK exits the EU. Several reviews have already identified several complex scenarios. However, it is best to conceptualise any future UK-EU agreement as being on a continuum between “Hard” Brexit – wherein the UK refuses to budge on issues such as free movement of people, taxation, environmental legislation, etc, in all likelihood leading to denial of benefits of the Single European Market (SEM) – and “Soft” Brexit – relatively free movement of people, goods, capital and services, and the UK remaining a de facto member of the SEM though not part of formal EU decision-making. In between the “Hard” and “Soft” Brexit extremes there exist a number of other possible alternative trading relationships, based primarily on the use of bilateral agreements to govern specific areas of trade.

It is simply not possible to predict with any accuracy the long-term impact of Brexit on the UK economy. Not only is Article 50 – the invocation of which by the UK triggers the formal negotiation process between the UK and the remaining 27 EU members – untried, but the nature and character of the post-Brexit agreement (Hard, Soft or somewhere in the middle) is at this stage unknown. And the post-Brexit agreement will be the determining factor. With 44% of UK trade with Europe it is hard to conclude anything other than the UK economy is vulnerable to a poor post-Brexit deal, especially one that effectively restricts UK access to the SEM. The UK economy, especially investments and FDI, is also vulnerable to uncertainty.

The most recent independent forecasts used by the UK government predict that the real effect of Brexit will be to cut the potential size of the UK economy by 2.4% in 2020. The most significant threat of Brexit to South Africa will arise from reduced export demand if the negotiations damage the UK economy. But with UK-destined exports standing at just 4% of South Africa’s total exports and a reasonable worst case scenario of the British economy shrinking between -2.5% and -5.0% of GDP by 2020 if a Hard Brexit approach is adopted, the direct impact of Brexit on the South African economy is likely to be marginal. While Brexit is not unimportant for the South African economy, its negative economic impacts on South Africa overall are likely to be negligible. Nevertheless, for certain South African industries, especially agriculture (wine and fresh fruit, especially grapes), precious stones and motor vehicles, the UK economy is disproportionally important and these sectors are more vulnerable if the UK economy is damaged by the process and impacts of Brexit.

The Common Agricultural Policy

Whatever happens in the post-Brexit negotiations, the UK will not be part of the Common Agricultural Policy (CAP). This is particularly important for South Africa, with its competitive and seasonally complementary agricultural industries. The UK’s very significant agricultural imports from the EU will almost certainly be reduced, due to trade barriers and the functioning of the CAP, opening up opportunities for South Africa to export more agricultural products to the UK. The well-respected Consultancy Agra Europe argues that “what is certain is that no UK government would subsidise agriculture on the scale operated under the EU”.

Far from Brexit having a negative impact on South Africa, there may well be increased opportunities for South African agricultural exporters, especially of wine, fruits, beef and sugar. The impacts on South African agriculture will depend on the decisions the UK makes about its agricultural tariff regime, but that regime is almost certain to be less restrictive that the current CAP. This will mean additional opportunities for South Africa’s competitive agricultural exporters that already have a high profile in South Africa’s exports to the UK. The level of access afforded to South African agriculture to enter the UK market, after the existing South Africa-EU trade regime no longer applies to the UK, will be critical.

The Future South Africa-UK trading regime

Until South Africa’s first democratic election in April 1994, access to the EU market was governed by its MFN status, which is at the very bottom of the EU’s complex hierarchy of trade privileges. South Africa’s market access to the EU was therefore on terms similar to the world’s most powerful states, such as the USA and Japan. In November 1994, South Africa applied for Lome membership, an application that was rejected by the EU on the grounds of WTO compatibility and the need to promote reciprocity.

Currently, South Africa’s trade relations with the EU (including, of course, the UK) are governed by a separate South Africa-EU Agreement: The Trade Development and Co-operation Agreement (TDCA), signed in July 1999. The TDCA established a free trade area that covers 90% of bilateral trade between the EU and South Africa.

The liberalisation schedules contained in the TDCA were completed by 2012. However, this will soon be replaced following the signing (signed but not yet ratified) of the Economic Partnership Agreement between the European Union and the SADC EPA Group. In February 2007, South Africa joined the Economic Partnership Agreement (EPA) negotiations as part of the Southern African Development Community Group. The SADC EPA, agreed and signed in June 2016, now needs to be ratified in the 28 EU Member States, the five Southern Africa Customs Union (SACU) Member States and Mozambique, according to national ratification procedures. The SADC EPA guarantees Botswana, Lesotho, Namibia, Swaziland (BLNS) and Mozambique duty-free and quota-free access to the European market. South Africa’s access, which is being enhanced from its current position, is less favourable than the BLNS states and Mozambique.

South Africa’s trade relations with the UK are, until such time as the UK legally leaves the EU, governed by South Africa-EU Agreements. The same is true for the BLNS and Mozambique. This affords South and southern Africa favourable and asymmetric access to the EU market, including the UK. However, the level of preferential access afforded to South African merchandise trade to enter the UK market, through European agreements, will be removed when the UK leaves the EU. The existing South Africa–EU trade regime, come 2019, will no longer apply to the UK.

A new South Africa (SACU/SADC)-UK trade and development agreement will therefore need to be negotiated, signed and ratified by 2019. The options are to:

-

Modify slightly the recently signed EPA to cover a transitional period.

-

Accept the existing EPA Agreement.

-

Negotiate a new South Africa-UK Agreement. (A new South Africa-UK trade, tariff and quota regime would probably take more than two years to negotiate and the outcome would be uncertain.)

-

Accept EPA but renegotiate agricultural access to the UK market, which will be fundamentally reformed by the UK leaving the CAP. Agricultural access would appear to be one of the key issues for discussion and of significant interest to South Africa.

In Conclusion

From the evidence presented here, Brexit is likely to have a marginal impact on the South African economy as a whole. Even under a worst-case scenario of a “Hard” Brexit, and the imposition of WTO MFN tariffs, UK GDP could fall by an estimated -2.4% to -5.0%. This is unlikely to damage seriously South Africa’s exports to the UK.

Nonetheless, if a substantial reduction of UK imports does take place it could have a significant negative impact on certain South African industries, especially agriculture. On the other hand Brexit could open up certain opportunities for South Africa, in the very same sectors identified as vulnerable to a significant reduction in UK imports. When the UK leaves the CAP, opportunities will almost certainly exist for South Africa to expand its agricultural exports. The scale of this opportunity will depend on the UK agricultural regime designed to replace the CAP.

Until the UK and EU27 are in a position to clarify their post-Brexit trading relationship, it is very difficult for South Africa to assess what it will need to prioritise in its trade negotiations with the UK (and perhaps even the EU). However, the UK will almost certainly prioritise negotiating its post-Brexit EU trading agreement, alongside renegotiating its membership of the WTO. After that, the UK’s priority will be focused on establishing trade agreements with its largest trading partners, especially the USA, Canada, India, Australia, China etc. With the UK’s current trade negotiating capacity being severely limited – it has not had to do this kind of work for over 40 years – South Africa is not going to be a priority trade agreement.

The threat to South Africa is that, by default, Brexit could lead to a worsening of its access to the UK market until such time as a new South Africa/SACU/SADC-UK trade agreement is negotiated. The priority for South Africa is to avoid this default position, and negotiate, even temporarily, a UK trade deal that is close to, or better than, the existing EU arrangement. A secondary priority would be to focus on identifying and supporting, both domestically and through trade agreements, offensive trade interests which stand to gain from the Brexit change.

Professor Richard Gibb has published several books and numerous articles on regional integration in both Europe and southern Africa. Previously Pro Vice-Chancellor at the University of Plymouth (UK) and Provost of Abu Dhabi University, he now acts as a consultant on international trade agreements. He is also an Associate of The Brenthurst Foundation.

A longer version of this article is published as a recent Brenthurst Foundation Discussion Paper by the author.

Download:

![]()

The Impact of Brexit on South Africa | Brenthurst Discussion Paper

Related News

Tax revenues reach new high as the tax mix shifts further towards labour and consumption taxes

Tax revenues collected in advanced economies have continued to increase from last year’s all-time high, with taxes on labour and consumption representing an increasing share of total tax revenues, according to new OECD research.

The 2016 edition of the OECD’s annual Revenue Statistics publication shows that the OECD average tax-to-GDP ratio rose slightly in 2015, to 34.3%, compared to 34.2% in 2014. This is the highest level since the Revenue Statistics series began in 1965. An increase in tax-to-GDP levels was seen in 25 of the 32 OECD countries that provided preliminary data in 2015, while tax-to-GDP levels fell in the remaining seven countries.

Consumption Tax Trends 2016 highlights that VAT revenues are the largest source of consumption tax revenues in the OECD, and have now reached an all-time high of 6.8% of GDP and 20.1% of total tax revenue on average in 2014. This is up from 6.6% of GDP and 19.8% of total tax revenue in 2012. Revenues from VAT rose as a percentage of GDP in 22 of the 34 OECD countries that operate a VAT and fell, only slightly, in 5 countries compared to 2012.

The new data shows that the structure of tax revenues continues shifting towards labour and consumption taxes. The combined share of personal income taxes, social security contributions and value-added taxes were higher in 2014 than at any point since 1965, at 24.3% of GDP on average in 2014.

The share of personal income taxes in total tax revenue continues to increase since the crisis, whereas the share of corporate tax revenues has not yet recovered to pre-crisis levels. Personal income taxes increased to 24% of total revenue in 2014, versus a pre-crisis level of 23.7% in 2007. The share of corporate taxes to total revenue in 2014 was 8.8%, relative to 11.2% in 2007. The share of social security contributions to total revenues also increased sharply after the crisis, from 24.7% of total tax revenues in 2007 to 26.8% in 2009. Since then they have decreased slowly as a percentage of total tax revenues to 26.2% in 2014.

In 2015, the largest increases in the overall tax-to-GDP ratio relative to 2014 were seen in Mexico and Turkey, and strong increases were also seen in Estonia, Greece, Hungary and the Slovak Republic. The largest falls in 2015 were seen in Ireland, Denmark, Iceland and Luxembourg. The fall in Ireland was due to exceptionally high GDP growth in 2015, mainly due to transfers of intangible assets into the Irish jurisdiction by a number of multinational enterprises. Excluding Ireland, the average OECD tax-to-GDP ratio in 2015 was 34.6%, an increase of 0.3 percentage points since 2014 for the remaining 34 countries.

Revenue Statistics also contains a special feature on “Current issues on reporting tax revenues”. This chapter discusses methodological issues in the classification of taxes used in Revenue Statistics, which is set out in the Interpretative Guide. A key issue discussed in the special feature is the treatment of non-wastable tax credits and the impact of different approaches to reporting these credits.

Detailed Country Notes provide further data on national tax to GDP ratios and the composition of the tax mix in OECD countries.

Key Findings:

-

Compared with 2014, the average tax burden in OECD countries increased by 0.1 percentage points to 34.3% in 2015. This followed a rise of 0.9 percentage points between 2009 and 2014, reversing the decline from 33.8% to 32.4% between 2007 and 2009.

-

The largest tax ratio increases between 2014 and 2015 were in Mexico (2.3 percentage points) and Turkey (1.3 percentage points). Other countries with substantial rises were Estonia, Greece, Hungary and the Slovak Republic (greater than one percentage point).

-

The largest falls between 2014 and 2015 were in Ireland (5.1 percentage points, due to exceptionally high GDP growth in 2015), Denmark (3 percentage points) and Iceland (1.8 percentage points). Luxembourg also showed a fall of more than one percentage point.

-

Underlying the OECD average, individual countries show widely differing trends. For example, Norway recorded a fall of 4.0 percentage points between 2007 and 2015, while Greece recorded an increase of 5.6 percentage points.

-

Historically, tax-to-GDP ratios increased through the 1990s, to a peak OECD average of 34.0% in 2000. They fell slightly between 2001 and 2004, but then rose again between 2005 and 2007 to an average of 33.8% before falling back sharply during the crisis.

-

Denmark has the highest tax-to-GDP ratio among OECD countries (46.6% in 2015), followed by France (45.5%) and Belgium (44.8%).

-

Mexico (17.4% in 2015) and Chile (20.7%) have the lowest tax-to-GDP ratios among OECD countries. They are followed by Ireland, which has the third lowest ratio among OECD countries at 23.6%, and Korea at 25.3%.

-

Data for 2014, the latest year for which a breakdown of revenues by category of tax is available for all OECD countries, show that revenues from personal and corporate income taxes are continuing to recover following the sharp falls of 2008 and 2009. However, the share of these taxes in total revenues remains at 33.7%, somewhat below their 36% share in 2007.

-

In 2014, an average of 24.3% of revenues is attributed to sub-central levels of government in Federal countries in the OECD - about two thirds of this is attributed to State and one third to local governments. The same applies to Spain, which is classified as a regional country in the publication. In the 25 unitary countries, 11.7% of revenues are attributed to local governments.

Consumption Tax Trends

Standard VAT rates in the OECD reached a record level of 19.2% on average in 2015 and have remained stable since. Ten OECD countries now have a standard VAT rate above 22%, against only four in 2008. The average standard rate of the 22 OECD countries that are members of the European Union (21.7%) is significantly above the OECD average.

Most OECD countries have implemented or announced measures to collect the VAT on the ever-rising volume of online sales by offshore sellers in line with the International VAT/GST Guidelines and the OECD/G20 BEPS Action 1 Report, Addressing the Tax Challenges of the Digital Economy.

Country Notes provide further data on national consumption tax trends and the effectiveness of VAT/GST collection in OECD countries.

Related News

DG Azevêdo: “We must ensure that the gains of trade are better shared across society”

In a speech to the OECD’s Global Strategy Group on 28 November, Director-General Roberto Azevêdo stressed the importance of making the case for trade amid a rise in anti-globalisation sentiment in many countries. Governments also need to work on creating a better, more inclusive model of globalisation and ensure the benefits of trade reach further and wider through new trade reforms. This is what he said:

These are proving to be testing times for the global economy.

The outlook for trade growth has weakened significantly. In September the WTO downgraded its forecasts for trade growth in 2016 from 2.8 per cent to 1.7 per cent. If realized, this would mark the slowest pace of trade growth since the financial crisis. This is of course largely due to the lacklustre performance of the global economy – and not the other way around.

At the same time, foreign direct investment flows have not returned to pre-crisis levels.

Both trade and investment are important ingredients for global economic integration, growth and prosperity, so this should be of particular concern. And of course the two are very closely linked.

For example, services trade now accounts for almost two thirds of global inward FDI stock. And FDI is fundamental because:

-

First, it is the main vehicle for the supply of services in foreign markets; and

-

Second, it is critical in enabling global supply chains to function properly.

More open trade policies can boost FDI and strengthen a positive relationship between the two.

Of course, recent political developments will also have an effect on the trading landscape – from the Brexit referendum in the UK to elections in many major economies. It’s too early to say what all of this will mean, but of course, we will be watching the developments very closely.

In addition, all of this is taking place amid a rise in anti-globalisation discourse in many countries and communities. And trade is often singled out as a major cause of instability in labour markets. I would firmly dispute this point, and I’ll come back to it in a moment. However, my biggest concern is not that such arguments are being made. My concern is the echo that they attract from the people. It is real and heartfelt.

Trade is essential for economic growth and development around the world.

However, a proper argument for trade must recognize that it is not a panacea or silver bullet. Trade will not fix widespread shortcomings in terms of economic, social and educational policies that lead to low productivity and asymmetries in wealth distribution. Such quandaries would require a much more encompassing set of policies.

A proper case for trade would also need to recognize that it is not perfect and that, despite the overall gains it brings to the economy, it can have negative effects in some parts of society. Those effects can have a big impact on some people’s lives. And for these people, the net overall benefits for the economy are no consolation. So there is a responsibility on leaders to reflect, and to respond.

We all know how fundamental trade is for economic growth and job creation. But it is also vital that it is perceived as such. So, effective communication is key.

I think there are a number of steps that we need to take.

First, we have to work harder to make the case for trade. And we must do so in a credible, well-informed, and balanced way.

For example, a charge often leveled against trade is that it sends jobs overseas, particularly in manufacturing. Trade can cause this kind of displacement, but the effect should not be overstated.

Technology and innovation are having a much bigger impact on the structure of labour. Studies suggest that around 80 per cent of job losses in advanced economies are due to technology and innovation. Almost 50 per cent of existing jobs in some developed countries are at high risk of automation today. And the number is higher in many developing countries.

Like trade, technological progress is indispensable for sustained growth and development. The answer is not to reject these forces. We must embrace them and learn to adapt.

At present anti-globalisation sentiment is being manifested mostly in developed economies. In developing economies – and particularly in Africa – globalisation and trade are seen as a way for improving lives and livelihoods. But we shouldn’t be complacent about this.

I’m sure everyone is familiar with Branko Milanovic’s famous ‘elephant curve’ graph, and the more in-depth analysis by the Resolution Foundation, showing that incomes have stagnated for the middle classes in advanced economies in recent years. This stagnation has fueled feelings of being left behind by globalization.

However, if you look at income gains in developing countries alone, you see a similar pattern emerging. The biggest gains are going to the richest segments of society. If this doesn’t change over the coming years, we could see that feeling of being left behind spreading to communities around the world.

And this brings me to my second point, which is that we have to act domestically.

If we are going to create a better, more inclusive model of globalisation, then we must ensure that the gains of trade are better shared across society. Domestic policy will be the key factor here.

As I’ve said, unemployment and other dislocations are not strictly or mainly a trade issue, so trade measures alone will not address this disorder. We need a more far-reaching response which also deals with the wider changes in the economy that are being driven by technology and innovation.

This will require action in a number of areas, for example, to ensure that people can have the right skills to participate and to have access to the jobs being created in today’s markets. More active and cross-cutting labour market policies will be essential, also touching on aspects of education and skills, help for smaller companies, and improved adjustment support to the unemployed.

The OECD average for spending on active labour market policies is 0.6 per cent of GDP. Some countries allocate much less than this; and some considerably more. Of course there is no single recipe for success here, but it is important to look at where things have been done well. Countries such as Singapore, Denmark and South Korea have adopted adjustment programmes with great success.

Given we are hosted this evening by Denmark, I would like to say a few words about the Danish model.

Denmark spends 1.5% of its GDP on labour market policies known as “flexicurity” – so that’s significantly above the OECD average.

The approach combines greater labour market flexibility – not less! – with improved training support and enhanced unemployment insurance. It guarantees 90% of the previous wage if an employee is laid-off.

From the evidence I’ve seen, I must say that it seems, overall, to be a fairly successful model – with job creation remaining relatively high. Despite the flexibility in the labour market, there is a sense of security. And, interestingly, most people in the country perceive globalisation as an opportunity, rather than as a threat.

Of course, this is not just about governments – there is also a role here for business. I think that initiatives like the OECD Guidelines for Multinational Enterprises are very important, for example by informing businesses about their impact in their communities, helping to encourage positive practices.

Now, let me turn to the third step that I think we need to take. And that is to act globally.

Trade is sometimes perceived as an activity that benefits just a few, or only the big players. While I would have strong reservations concerning such an assertion, I think it is clear that smaller players face greater challenges and higher costs than the large corporations. So we should seek to address this. I think we can do more to ensure that the benefits of trade reach further and wider through new trade reforms.

Clearly we are in a period of change. Some countries are looking afresh at their trade policies. But even if policies and approaches change, I don’t see anyone turning against trade per se – not yet anyway.

As the only organization dealing with trade rules on a global level, I have no doubt that the WTO will continue to play an important role.

Indeed, over the past few years, the WTO has shown that it can deliver. Since 2013, the WTO has done so in a number of very significant deals, including – but not limited to:

-

The Trade Facilitation Agreement to cut trade costs and red tape, which could boost global exports by up to 1 trillion dollars per annum.

-

The Information Technology Agreement, which eliminates tariffs on a range of new-generation IT products – trade in which is worth around 1.3 trillion dollars each year.

-

And a deal to abolish export subsidies in agriculture, which delivered on a key target of “Zero Hunger” – one of the UN’s Sustainable Development Goals.

These are the biggest reforms in the global trading system for 20 years, all delivered since 2013. And, as we speak, a group of members is making progress in a deal to eliminate tariffs in environmental goods like wind turbines and solar panels. Ministers will be meeting at the WTO this weekend to try to finalize this agreement. I will be doing all I can to support a successful outcome.

As a result of the progress made in recent years, members now want to deliver more.

Members are discussing how to deal with longstanding issues, such as agriculture (including domestic support), services, and market access for industrial goods.

In agriculture, discussion is intense but gaps remain difficult to bridge. In services there is ongoing work on domestic regulation and services trade facilitation, among other areas. In rules I would underline the debate on fisheries subsidies, which has attracted a lot of attention.

Active discussions are also happening in areas like:

-

How to help smaller companies to trade, and

-

How to harness the power of e-commerce to support inclusiveness.

Work on these issues can be very important in helping more people to join trade flows. Among OECD countries, SMEs account for more than 60 per cent of employment.

The internet itself has the potential to bring many new entrants into the market, and cut trade costs related to physical distance.

However, in OECD countries, around 20 per cent of the population still doesn’t have access to the internet. In Africa, only one in four people use the internet – and, in LDCs, only one in seven people.

So there is huge unexplored potential here.

These conversations at the WTO are at an early stage. So we’ll see where members want to take them in the New Year – particularly as we look ahead to our next Ministerial Conference, which is being held in Buenos Aires in December 2017.

I’ll conclude now as I began: these are testing times for the global economy.

I think we all have a responsibility to respond.

That’s what we’ll be trying to do at the WTO. And I look forward to working with the OECD, and all of you, to achieve it.

Thank you.

Related News

IMF Executive Board provides further guidance to enhance the financial safety net for developing countries

On November 16, 2016, the Executive Board of the International Monetary Fund (IMF) discussed a staff paper on “Financing for Development: Enhancing the Financial Safety Net for Developing Countries – Further Considerations”, which identifies areas where current guidance on Fund policies needs to be clarified in regard to the access of developing countries to financial support from the Fund.

The staff paper examines a number of issues raised by Executive Directors and by the International Monetary and Financial Committee (IMFC) since the issuance to the Board in June 2015 of a staff paper on “Financing for Development: Enhancing the Financial Safety Net for Developing Countries.”

That paper had proposed a number of measures to expand access to Fund resources for developing countries, including a 50 percent increase in access limits to Fund concessional resources for those members deemed eligible to access the facilities supported by the Fund’s Poverty Reduction and Growth Trust (PRGT) – a proposal that was endorsed by the Board on July 1, 2015.

The new paper provides clarification on a number of issues pertaining to access to Fund resources for PRGT-eligible members. The issues examined include: a) access of PRGT-eligible members to Fund instruments that draw on the General Resources Account (GRA); b) the role of access norms in providing indicative guidance on what could constitute the appropriate level of access; c) the adequacy of PRGT-eligible members’ access to precautionary financial support; and d) the adequacy of safeguards to prevent repeated use of the Rapid Credit Facility (RCF) as a substitute for arrangements with ex post conditionality.

The paper does not propose specific reforms to the Fund’s concessional facilities at this juncture. A comprehensive review of PRGT resources and facilities is planned for 2018.

Executive Directors welcomed the opportunity to discuss the Fund’s policies and practices in regard to the access of PRGT‑eligible members to the Fund’s concessional and GRA resources, as called for by the International Monetary and Financial Committee (IMFC) at its Spring 2016 meeting. Directors agreed that the current concessional financing toolkit is generally well calibrated, and appreciated clarification of existing policies and the revisions underway to the Low‑Income Countries Handbook.

Directors reaffirmed that a PRGT‑eligible member has the right to access GRA resources on the same conditions as any other Fund member. They also noted that, given the financial benefits to the member from borrowing on concessional terms, staff should continue to advise PRGT‑eligible members considering Fund financial support to seek support from the PRGT up to the applicable limits before seeking GRA resources.

Directors welcomed the clarification of the current policy on blending. They agreed that the presumption of blending PRGT with GRA resources should continue to be applied to PRGT‑eligible members meeting the income or market access thresholds for blending; these countries would have access to PRGT resources only in conjunction with access to GRA resources. Directors also agreed that this presumption does not normally apply where the member is in debt distress or at high risk of debt distress.

Directors noted that PRGT‑eligible members that are not presumed to blend can access PRGT resources exclusively up to the applicable PRGT access limits. They also noted that these members, to the extent that they meet the applicable policies on access to GRA resources, are not precluded from accessing these resources, either on a standalone basis or in conjunction with PRGT resources.

Directors reaffirmed that access to GRA resources is subject to the general policies governing GRA access and that total access to Fund resources (the sum of GRA and PRGT resources made available) should be determined case by case on the basis of the standard criteria, including balance of payments need, program strength, and capacity to repay the Fund, informed by debt sustainability analysis. Many Directors encouraged the staff to be more open to considering requests for higher levels of access to Fund resources as allowed within the current access rules, while safeguarding the Fund’s resources. Some Directors noted that this was of particular relevance in the current juncture, where a number of low‑income and frontier market economies had sizeable financing needs that could well exceed the applicable PRGT limits.

Directors underscored that access norms, as used in PRGT facilities, are neither a ceiling nor a floor on the level of access provided in PRGT‑supported arrangements. Norms should help to inform the assessment of access levels but should not be misconstrued as access limits or entitlements.

Directors agreed that the record of usage of the Rapid Credit Facility (RCF) suggests that the existing safeguards are adequate to prevent repeated use of the RCF as a substitute for arrangements with ex post conditionality and called for continued monitoring in this regard. For countries receiving support under the RCF that are also seeking to build a track record toward an upper credit tranche (UCT)‑quality program, Directors agreed that the use of a staff‑monitored program (SMP) to build such a track record would normally be the preferred option, while noting an assessment of the policy commitments made in the context of disbursements under the RCF could also be used for that purpose. Hence, a number of Directors underscored that use of an SMP to build a track record in such circumstances, while preferable, should not be required, providing flexibility to accommodate individual country circumstances.

Directors were of the view that the existing array of Fund facilities provided substantial room to provide PRGT‑eligible members with Fund support on a precautionary basis. Most Directors did not see a need to establish new facilities in the PRGT targeted specifically at providing precautionary support to PRGT‑eligible members at this juncture.

Directors emphasized the importance of continued attention to maintaining the adequacy and flexibility of the PRGT lending toolkit, including by reviewing access norms and limits, blending policy, interest rate structure, and safeguarding mechanisms for maintaining the self‑sustaining capacity of the PRGT. In this regard, they looked forward to the planned comprehensive review of PRGT resources and facilities in 2018, in accordance with the normal five‑year cycle for such reviews, as well as the upcoming meeting on the Fund’s role in assisting small states build resilience to natural disasters and climate change.

Related News

tralac’s Daily News Selection

The selection: Tuesday, 29 November 2016

Diarise: World Economic Forum on Africa (3-5 May 2017, Durban)

Key statements from the opening session at Africa Trade Week 2016:

UNCTAD’s Mukhisa Kituyi: “To me the Abuja Declaration was important. It was a starting point towards where we are but even if there had not been an Abuja and a Lagos Plan of Action, the reasons for creating a Pan African free trade are important even from today’s challenges so we have enough reasons from today apart from our inherited responsibility from Abuja”

ATPC’s David Luke: “These include Africa’s trade relations with Asia, Europe, the United States and emerging markets; how trade can support gender equality and empowerment; perspectives from the regional economic communities and the CFTA negotiations and related flanking measures”

African Union Commissioner Fatima Haram Acyl: Africa needs to bring the cost of doing business down,[which] would significantly boost trade performance with trade facilitation, which looks at procedures and controls governing the movement of goods across borders, enabling Africa to do that.

African Civil Society statement on the Continental Free Trade Agenda

From 26-27 November, civil society organisations from Africa met under the umbrella of the Africa Trade Network in Addis Ababa, in advance of the Africa Trade Week and the seminar of the CFTA to discuss the challenges of Africa’s economic transformation and integration and role of the CFTA. We have come to the following conclusions and make the following demands: [Download the French version, pdf]

SA at Africa Trade Week: Minister Rob Davies will also attend the African Union’s Ministers of Trade meeting where ministers will consider the progress of the CFTA negotiations. On the side-lines of the Africa Trade Week 2016 meeting, Minister Davies will meet the Ministers of Trade of Kenya, Egypt, and Nigeria to discuss the enhancement of cooperation and advancing regional economic integration in Africa.

Tanzania: Major blow for government as mega-factory shuts down (IPPmedia)

The fifth phase government’s industrialisation drive has been dealt a heavy blow by the unexpected closure of the country’s currently biggest cement plant run by Dangote Industries (Tanzania) Limited due to rising production costs and a ‘technical glitch’at the $500 million (1.1 trillion/-) factory. The abrupt suspension of the relatively new plant’s operations is reported to have caught the government by surprise, at the same time reigniting a row over the quality of the country’s coal reserves amid reports that the factory managers were preferring to import coal from South Africa instead of using local supplies. The Ministry of Energy and Minerals recently announced a ban on coal imports from South Africa, insisting that the Dangote cement plant must use coal mined in Tanzania because it meets quality requirements. But now the factory management has responded by shutting down operations indefinitely.

Foreign firms hit by tax demands rethink Tanzanian expansion (Reuters)

Some of Tanzania’s biggest foreign investors say they could scale back their operations or expansion plans because of tougher demands placed on companies, including higher tax bills, as part of the president’s drive to overhaul the economy. At least six companies are rethinking their business and investment plans, according to Reuters interviews with senior executives at a dozen of the biggest foreign firms operating in Tanzania, or their local arms, in sectors including mining, telecoms and shipping. Three said they could scale back operations in the East African nation, two said they planned to expand in other countries on the continent instead, while one said it was in the process of withdrawing from Tanzania altogether.

Mauritius hosts regional workshop on Post Clearance Audit (GoM)

A five-day workshop on Post Clearance Audit, which is an effective measure for trade facilitation as well as compliance verification, kicked off yesterday at the Mauritius Revenue Authority Regional Training Centre, Mer Rouge. Some 30 delegates from 19 countries of the East and Southern Africa region are participating in this workshop with the aim to assist the Customs administrations to implement or reinforce PCA.

ASEA conference: Africa’s exchanges urged to be innovative and integrate to attract more investment (New Times)

Rwanda’s equity market capitalisation to GDP ratio stood at 32.93% in 2015 compared to 48% in Kenya. In monetary value, the country’s stock exchange has kept a steady performance in the last five years, registering a market capitalisation of almost $4.2bn of 2015. The Rwanda Stock Exchange market capitalisation was at Rwf2.751 trillion at the close of yesterday’s trading session compared to Rwf2.820 trillion on 4 January 2016. Five years since the bourse was launched in Rwanda, there are seven companies and 13 government and corporate bonds listed on the exchange and eight trading members as well as two licensed custodians. However, Dr James Ndahiro, the RSE chairman, said there is still need to deal with challenges facing the industry, including the lack of innovative products.

Building a regional solution to bridge Eastern and Southern Africa’s science and technology gap (World Bank)

Last month, we launched the project’s second phase, ACE II, in Nairobi – a far-reaching initiative that seeks to strengthen 24 competitively selected centres in Eastern and Southern Africa to deliver top quality and relevant post-graduate education in regional development priority sectors that need it the most. The ACE II’s expected impact will be unprecedented once achieved. In five years, its selected 24 centers are expected to enroll more than 3,500 graduate students in their specialized areas, with at least 700 students pursuing PhDs, and more than 1,000 would be women. The project also aims to have more than 300 research collaborations with the private sector and academic institutions, and generate about $30 million in external revenue to make the centers sustainable.

Germany to support three new UNIDO projects: including Africa’s pharmaceutical industry project (UNIDO)

The first project on “Devising practical approaches for mobilizing investment capital and transfer of technology for Africa’s pharmaceutical industry” capitalizes on UNIDO’s previous work in Africa’s pharma industry, and seeks to further mobilize public and private partners through the newly incepted ITPO Bonn, which was formalized last week by Gerd Müller, Federal Minister of BMZ and Director General LI Yong on the occasion of the Organization’s 50th Anniversary celebrations. “This is a very important initiative”, said Li. “Together with the heads of State and Government of the African Union as well as with our development partners, including Bill Gates, we agreed that a lot of attention needs to be paid to this specific sector as it pertains both to the health of people and the manufacturing of generic drugs. We are thankful to Germany for its continued support”.

Two commentaries on the Doing Business 2016 report:

José Antonio Ocampo, Edmund Fitzgerald: Doing Business should stop promoting tax competition (Project Syndicate): The World Bank Group has just released Doing Business 2017: Equal Opportunity for All, the latest version of its flagship report. According to the Bank, the annual report is one of the world’s most influential policy publications, as it encourages countries to reduce the regulatory burden on the private sector. But there is a serious flaw in the report’s formula: the way it treats corporate taxation. A race to the bottom in corporate taxation will only hurt poor people and poor countries. If Doing Business is to live up to its own slogan, “equal opportunity for all,” it should abandon the tax indicator altogether.

Cecile Fruman: Why gender equality in doing business makes good economic sense (World Bank): For the first time since it was launched in 2002, the World Bank Group’s annual Doing Business report this year added a gender dimension to its measures, including to the annual ranking on each country’s ease of doing business. Looking at gender differences when it comes to starting a business, registering property or enforcing contracts, Doing Business shows that 23 countries impose more procedures for women than men to start a business. Sixteen countries limit women’s ability to own, use and transfer property. And in 17 economies, the civil courts do not value a woman’s testimony the same way as a man’s. This pattern might give the impression that such legal differences are really only an issue in a selected group of countries. But Doing Business’ sister publication – Women, Business and the Law (pdf) – tells us otherwise.

6th Africa Regional Platform on Disaster Risk Reduction: statement of the East African Community

What are our future plans? The East African Community commits to implement its Disaster Risk Reduction Law as soon as it is assented to and in line with the Sendai Framework on Disaster Risk Reduction. In this regard, the EAC priorities will be the following: [SADC Ministers adopt Regional Disaster Preparedness and Response Strategy]

Rwanda: Why hotels and supermarkets continue to import fresh food (New Times)

According to the Ministry of Trade, Industry and EAC Affairs, Rwanda designed the Domestic Market Recapture Strategy 2015 (pdf) geared at helping the country reduce the growing trade deficit, by promoting production and consumption of locally-made products. The ministry also identified priority sectors that can quickly contribute to Rwanda’s domestic market recapturing, including floriculture and horticulture production. The ministry says the domestic market recapturing strategy study could enable the country to save almost $450m per year or 17.8% reduction on the current import bill. Agro-processing, light manufacturing and the construction materials are the key priority sectors identified by government in its push to reduce the country’s widening import bill. Under the Domestic Market Recapture Strategy 2015, implemented by the Ministry of Trade, Industry and EAC Affairs, it is hoped Rwanda can save up to $450m annually. [Rwanda: Enhanced communication key to increased tax compliance – survey]

Supply chain risk in sub-Saharan Africa tops the chart (Bizcommunity)

Supply chain risk in Sub-Saharan Africa remains the highest in the world and continued to increase during the third quarter of the year as South Africa and Nigeria’s economies struggled. Supply chain risk in sub-Saharan Africa worsened from 5.544 to 5.558 during the third quarter of 2016, as measured by the Chartered Institute of Procurement and Supply Risk Index (pdf), powered by Dun & Bradstreet. The Index tracks the impact of economic and political developments on the stability of global supply chains.

Magufuli, Lungu agree to jointly kick-start TAZARA recovery (IPPMedia)

President John Magufuli and the visiting Zambian leader Edgar Lungu yesterday pledged to take decisive action to revive the perennially cash-strapped Tanzania-Zambia Railways Authority (TAZARA) and a joint crude oil pipeline project owned by the two neighbouring countries. President Magufuli expressed dismay at a drastic decline of cargo volumes carried by TAZARA from around 5 million tonnes a year at its peak in 1976 to just 128,000 tonnes a year presently. He said the performance of the Tanzania-Zambia oil pipeline project (TAZAMA) has also dropped from handling 1.1 million tonnes of crude oil per year to just 600,000 tonnes. Magufuli said he has agreed with his Zambian counterpart to review and amend the TAZARA Act of 1995 so as to scale-up the company’s efficiency.

Malawi: Nacala Rail and Port Value Addition Project GPN (pdf, AfDB)

The main goal of the technical assistance project is to improve on the efficiency and competitiveness of local businesses in the Nacala Corridor to enable them to take advantage of the newly constructed transport infrastructure, and to achieve accelerated economic and social growth in Malawi. The specific objectives are as follows:

Seeing opportunity in textile imports, Kenya plans cotton revival

To stop relying on Western hand-me-downs, African countries are importing Chinese textile companies

Kenya: New plan to take export zones to all 47 counties

Mozambique: IMF to initiate discussions on a new programme

Outgoing AUC commissioner for infrastructure and energy, Elham Ibrahim: ‘PIDA was my major milestone’

Benin opens 8th edition of Chinese products’ trade fair for West Africa

Related News

First ever Africa Trade Week opens in Addis Ababa

The first ever Africa Trade Week opened in Addis Ababa on Monday with the Economic Commission for Africa’s David Luke, urging participants to come up with solutions to unanswered questions about the Continental Free Trade Area.

Speaking on behalf of Abdalla Hamdok, ECA Acting Executive Secretary Mr. Luke said the CFTA is a bold initiative aiming to bring together 54 African countries with a combined population of more than one billion people and a combined gross domestic product of more than US$3.4 trillion.

African leaders, with the CFTA, aim to, create a single continental market for goods and services, free movement of business persons and investments and expand intra-African trade, among other things. The CFTA is also expected to enhance competitiveness at the industry and enterprise levels on the continent.