Search News Results

A review of the UNCTAD report on trade misinvoicing, with a focus on South Africa’s gold export

In July 2016, the United Nations Conference on Trade and Development (UNCTAD) published a report titled “Trade Mis-invoicing in Primary Commodities in Developing Countries: The cases of Chile, Cote d’Ivoire, Nigeria, South Africa and Zambia.”

This report contained serious accusations. The report asserted, among other things, that South African miners of silver, platinum group metals, gold and iron ore had systematically and fraudulently indulged in mis-invoicing in order to evade taxes and other legal obligations.

In respect of gold, specifically, the report stated: “Between 2000 and 2014, under-invoicing of gold exports from South Africa amounted to $78.2 billion, or 67% of total gold exports” and that this “does not appear to be a simple matter of undervaluation of the quantities of gold exported, but rather a case of pure smuggling of gold out of the country.”

The Chamber at the time disputed the veracity of the report and its conclusions – as did SARS and Statistics SA. The Chamber went further, and commissioned an independent inquiry by economic consultants Eunomix.

The final report is now available in full on the Chamber website.

Given the lack of rigour and unreliable methodologies used in UNCTAD’s report which the Chamber previously pointed out to the UN agency, the Chamber of Mines again calls on UNCTAD to withdraw this report and acknowledge its shortcomings.

Related articles

-

Chamber of Mines releases final independent report on trade misinvoicing

-

UNCTAD welcomes discussion, transparency on commodities and misinvoicing

-

Trade mis-invoicing – South Africa’s Chamber of Mines response to UNCTAD-sponsored report

-

Some countries losing up to 67% of commodity exports to misinvoicing

Related News

tralac’s Daily News Selection

The selection: Tuesday, 13 December 2016

President Paul Kagame yesterday hosted the fourth AU Reform Advisory Group meeting: update

An assessment of the short term impact of the ECOWAS-CET and EU-EPA in Senegal (World Bank)

In recent years, there have been major changes in the trade policy landscape in West Africa that will affect Senegal. When initially designed in the mid-2000s, the CET was organized in four tariff bands: 0 percent for essential social goods, 5% for goods of primary necessity, raw materials and specific inputs, 10% for intermediate goods and 20% for final consumption goods. Since then, Nigeria has obtained the introduction of a fifth band at 35% for ‘specific goods for economic development’ (essentially agricultural goods and some consumer goods). The first section of the paper presents an analysis of the impact of the CET and EU-EPA on protection levels, trade flows and state revenues, changes in the price of the consumption bundles for households and impact on firm’s profits. The second section underlines some key elements of an accompanying policy agenda and a third section concludes.

Nigeria: ECOWAS’ sweet poison (The Nation)

I understand the old debate about the unfriendliness of our ports, the crippling bureaucracy and the mind-boggling corruption said to make doing business such hell and how this makes the neighbouring ports attractive. No doubt, there is a lot to be said of the need to streamline our port operations and procedures to make the more competitive and business friendly. After cycles of interminable reforms, they are legitimate arguments to make now and for all time. At issue is whether these concerns should be allowed to obviate mounting concerns about duplicity of our ECOWAS neighbours, particularly when their activities are injurious to us. We must of course understand that none of these goods are produced in the sub region, which of course raises the unlikelihood of their ban being seen as a violation of the ECOWAS protocol on free movement of goods and services. Moreover, the idea that a supposedly friendly neighbour will deliberately set itself up as a transit camp for goods destined for a third party country in brazen violation of its own domestic policies would seem far beyond the pale of modern trade protocols. That, unfortunately is the terrible situation which the sub regional body has found itself. [The author: Sanya Oni] [Related: Ports hurdles may hamper policy on imported vehicles, Nigerian lawmaker seeks free-float rollback via currency bill, NEPC: Nigeria ready for AGOA]

Benin: 16 economic policy notes to better inform decision making (World Bank)

Fourteenth Replenishment of the African Development Fund: update (AfDB)

A global coalition of donors pledged to support the structural transformation of African economies and the African Development Bank’s High Five priorities by agreeing on $7.06bn over the next three years to support development projects and programs in the 38 lower income African countries supported by the African Development Fund. The African Development Fund will shift more resources to support the private sector in the region, even as it helps countries dealing with fragility to address their most pressing developmental challenges. The increased resources devoted to these countries reflect their strong need for concessional funding. Recognizing the private sector’s key role in the transformation of African economies, the Fund will allocate over $280m to the Private Sector Credit Enhancement Facility. This Facility will leverage approximately $840m of private sector financing, of which at least 50% will be in higher risk countries. The Fund will continue to promote financial instruments that crowd in resources from the private sector, such as financial guarantee products.

Africa must act now if it is to feed itself in 2050 – scientists (Thompson Reuters Foundation)

Africa will be able to grow enough cereals to feed its growing population by 2050, but only if it breaks a culture of complacency and starts now to invest more in agriculture, scientists said on Monday. Sub-Saharan Africa currently imports about 20% of its cereal needs, and this could rise to at least 50% by 2050, researchers said in a report published on Monday in the Proceedings of the National Academy of Sciences.

Knowledge management crucial for Africa’s growth (SciDev)

The observation was made last month (14-16 November) during information and knowledge management training workshop on nutrition security and trade organised in Kenya jointly by the Africa Union Commission, NEPAD Agency and the COMESA Secretariat. It brought together technical experts from 11 COMESA member states - Burundi, Egypt, Ethiopia, Kenya, Madagascar, Seychelles, Sudan, Swaziland, Uganda, Zambia and Zimbabwe - working in trade, agriculture and nutrition security.

SADC Development Finance Institutions’ Chief Executive Officers’ Forum: update (The Chronicle)

The two-day workshop, at Victoria Falls, was attended by 31 development finance institutions in Africa and 25 chief executive officers and was held under the theme: “How to effectively use PPPs to enhance service delivery and development infrastructure.” The workshop sought to discuss PPPs in light of slow uptake by countries where only South Africa and Mauritius have active PPPs despite the concept being adopted by the region in 2013. [Peter Leon: What are the expectations of foreign and domestic investors for a welcoming investment climate in the SADC community? (Politicsweb)]

EAC borrows leaf from Japan, Vietnam for automotive industry (New Times)

According to Jean-Baptiste Havugimana, the EAC director for productive sectors, experts from partner states and the Secretariat travelled to Tanzania, Kenya and Uganda “to compile baseline information on the status of automotive industry,” and to Vietnam and Japan for a benchmarking exercise. “These missions took place from September 20 to October 7. Thereafter, the team will visit other countries in East Africa (Burundi, Rwanda) for in-depth analysis, and to others in Africa such as Ethiopia, Nigeria and South Africa for benchmarking,” Havugimana told The New Times at the weekend.

EAC must double efforts if Monetary Union is to be achieved, officials say (New Times)

Despite the apparent concern, however, Njoroge remains firm that preparatory work is still going on. The governors of the central banks, he assured, are following up on issues that were supposed to be implemented by the EAMI. “And, a lot of work is being done. A lot of monitoring mechanism as well as the n implementation of the convergence criteria has been developed. And it is being used in monitoring how we are doing in the implementation of the convergence criteria,” he said. Other than Burundi, it is said, Rwanda, Kenya, Uganda and Tanzania have prepared the medium term convergence programme and ministers of finance approved. The approved plans provide a trajectory on how the bloc moves from 2016 to 2021.

East Africa: One-stop border posts, axle-load laws set for January (The East African)

The laws were due to take effect on 1 October but for a failure to secure the signature of the new Heads of State Summit chairman, Tanzania President John Pombe Magufuli, in time. Alfred Kitolo, director of infrastructure services at Kenya’s Ministry of East African Community Affairs, said the EAC Council will now have the gazette notice with the two laws signed during the EAC Summit in January, whereupon implementation can start.

Zimbabwe: Government in drive to boost export growth (The Herald)

Government has launched the Rapid Results Approach for ease of doing export business as part of its efforts to close competitiveness gaps and halt negative export growth. According to the 2017 National Budget, the country’s export performance is expected to further decline by 6,9% to $3,3bn. Last year, total imports were $6bn against exports of $3,6bn resulting in an average monthly deficit of $275m. The 100-day RRA is expected to help enhance the country’s export earnings by tackling the key impediments to the export process, Industry and Commerce Minister Mike Bimha said in a speech read on his behalf by his permanent secretary Abigail Shonhiwa.

Botswana: Ghost town chronicles meltdown of Botswana’s metals industry (IOL)

The streets of Selebi Phikwe in northeastern Botswana no longer teem with trucks, and once-busy shop assistants and bank tellers wait for the rare customer. Since state-owned mining company BCL closed its loss-making copper and nickel operation that was the economic lifeblood of the area two months ago, the settlement of 50 000 has become a virtual ghost town. The government says it can’t afford the 8 billion pula ($748m) needed to recapitalize the mine. Instead, it’s asked former central bank Governor Linah Mohohlo to oversee a plan to rescue the region.

Revealed... most Tanzanians ignorant of EAC protocols (IPPMedia)

Interviewed, different government officials and other stakeholders said that the presence of numerous ‘panya’ routes, absence of security in many parts of Kigoma Region pose a big challenge in the East Africa Customs Union and Common Market protocols. Generally, Kigoma residents, farmers and business community do not know how the EAC common markets and customs union works. In an exclusive interview by this paper Kigoma residents and businessmen said they don’t know the opportunities accrued from the EAC community at large. Kigoma regional government officials and law enforcers who sought anonymity said that the government must wake up because generally many Tanzanians don’t know what EAC mean to them, its functions and protocols. That’s why some of them are being easily lured and then used by foreign businessmen and tax evaders.

DHL Global Connectedness Index: globalization surpassed pre-crisis peak, advanced modestly in 2015

In addition to a comprehensive overview on the state of globalization, the 2016 report also provides detailed insights into the connectedness of individual countries and regions. The index ranks countries on their depth (intensity of international flows) and breadth (geographical distribution of flows), which combine for an overall connectedness score between 0 and 100. Countries in South & Central Asia and Sub-Saharan Africa suffered a drop in their average levels of global connectedness.

$56bn and growing: it’s time India addressed the trade deficit with China (The Wire)

India’s trade deficit with China in 2015-16 stands at $52.69 billion. And it is expected that this will go up even further this year. This by itself should not be a cause for worry, as India runs deficits with 16 out of its top 25 trade partners. The fact is that India buys more than it sells worldwide. But the real problem is that there is no obvious solution in sight as yet and therefore the question that arises is, for how long can this huge deficit with China be maintained? India’s trade relations with China have had a checkered history and, unfortunately, continue to remain hostage to political developments between the two countries, albeit much less now than earlier. [The author, R.S. Kalha, is a former secretary at the Ministry of External Affairs] [Indo-China trade volume to touch $65 billion during 2016]

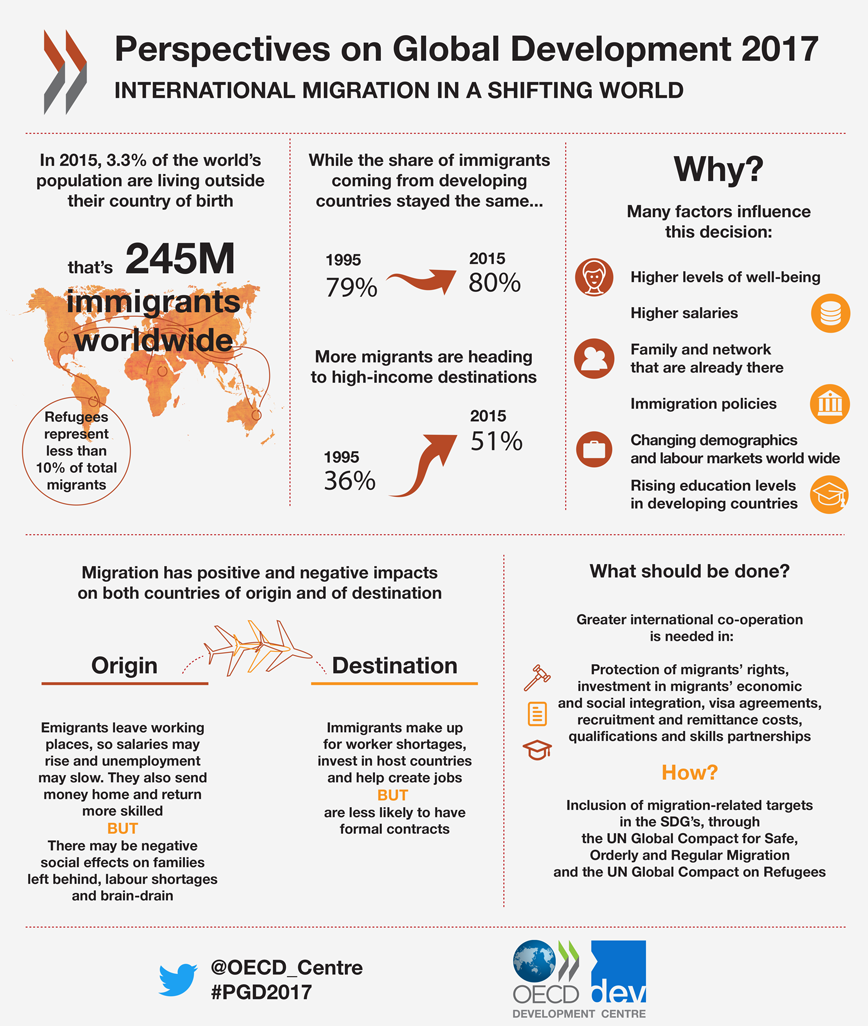

Perspectives on Global Development 2017: international migration in a shifting world (OECD)

The 9th Global Forum on Migration and Development meeting was held in Dhaka, Bangladesh (10-12 December) under the overarching theme “Migration that works for Sustainable Development of all: Towards a Transformative Migration Agenda”. This year’s Forum is focused on three main pillars: economics, sociology and governance of migration and development. The overarching theme is based on a ‘SDG Plus’ approach, i.e. to incorporate and advance, in the context of deliverables, a range of migration specific issues. [Various downloads available]

Africa’s climate: Helping decision-makers make sense of climate information (Future Climate for Africa)

The report has 15 factsheets covering specific regions including East Africa, Southern Africa, Central Africa and West Africa and six countries – Malawi, Rwanda, Senegal, Tanzania, Uganda and Zambia. The FCFA, a five-year, £20 million (almost $25m) programme with funding from the UK Department for International Development and the UK’s Natural Environment Resource Council, began in 2014 and has groups of researchers creating climate change data to aid policymaking in Africa. [Mauritius: Commonwealth Climate Finance Access Hub update, Small states’ resilience to natural disasters and climate change: role for the IMF]

Innovative research helps Rwanda raise $9m in tax revenue (IDS)

The study was conducted by the International Centre for Tax and Development in partnership with the African Tax Administration Forum, and in collaboration with the RRA. It was largely funded by UK Aid from the UK government, which highlighted the project as “high impact” in a recent Research Review. Not only did the project help raise additional revenue, it also catalysed innovations in the RRA’s operations (such as automatically personalising communications and expanding the functionality of its SMS platform), helped build research capacity within the RRA, and provided practical policy recommendations. [Various downloads available] [Botswana: BURS adopts new systems to broaden tax base]

President Sirleaf leads high-level ECOWAS delegation to The Gambia

EAC, development partners’ high level dialogue: update

IGAD, EU commit to drought resilience, free movement of persons in IGAD region

Zimbabwe: Diaspora remittances to drop 17% on firming US$

Safaricom in talks with five firms on M-Pesa’s future

‘Pressure on’ for African govts in 2017 in ICT

Tanzania: 2017 Finscope survey gets underway

Calestous Juma, Sujata Bhatia: If we develop Africa’s bioeconomy it will be as transformative for us as digital has been

Related News

EAC must double efforts if Monetary Union is to be achieved, officials say

The East African Community (EAC) is behind schedule as regards establishment of the East African Monetary Institute, a key body meant to carry out preparatory work for the East African Monetary Union (EAMU), officials have said.

When regional leaders approved the EAMU Protocol, in 2013, it provided for gradual establishment of four institutions, including the East African Monetary Institute (EAMI), a transitional institution responsible for laying the foundation for the EAMU.

“We are already lagging behind. It was supposed to be in place by 2015,” said Peter Njoroge, deputy director for economic affairs in Kenya’s Ministry of EAC Affairs.

Establishing the EAMI; initiating the pertinent legal instruments, identifying the host partner state, signing host country agreements and operationalising the institute were activities for 2015.

“However, even the legal framework for establishing these institutions has to be negotiated. We have to go through the normal process of negotiating how it is to be structured, and, you know, issues of negotiations take some time,” Njoroge added.

“That partly explains why we took longer and why we are yet to have the institution in place”.

By 2018, three other institutions: the East African Surveillance, Compliance and Enforcement Commission; the East African Statistics Bureau; and the East African Financial Services Commission, are supposed to be in place, according to the EAMU road map. Other activities to be concluded by 2018 include coordination and harmonization of fiscal policies, as well as coordination and harmonization of the monetary and exchange rate policies during the transition to the Monetary Union.

Luckily, the legal framework for EAMI and the statistics bureau have been developed. Regional ministers of finance who convene under the Sectoral Council on Finance and Economic Affairs cleared the requisite Bills, he said.

But there is a dilemma. The Bills were supposed to be considered by the EAC Sectoral Council on legal and judicial affairs which comprises regional Attorneys General, Solicitors General and justice ministers, but this has not happened.

It is the sectoral council that must ultimately check whether Bills meet the necessary legal requirement for EAC institutions.

Njoroge said: “Unfortunately, our Attorney Generals rarely meet and they have kept on postponing meetings.

Two Bills were supposed to be discussed by the sectoral council in a meeting earlier scheduled last month, but unfortunately the Attorney Generals were not available.

Until the sectoral council on legal and judicial affairs meets, there will be very little that will be happening about the Bills”.

Innocent Safari, Permanent Secretary at Rwanda’s Ministry of Trade, Industry and East African Community Affairs, also acknowledged that the delay “is basically caused by non meeting of the sectoral council on judicial and legal affairs which is supposed to clear the legal instruments establishing EAMU.”

Safari said: “It was last held, up to ministerial level, in November 2014. It has become very difficult for the attorneys general to meet and this has culminated into continuous postponement of this sectoral council.”

Preparatory work unconstrained?

Despite the apparent concern, however, Njoroge remains firm that preparatory work is still going on. The governors of the central banks, he assured, are following up on issues that were supposed to be implemented by the EAMI.

“And, a lot of work is being done. A lot of monitoring mechanism as well as the n implementation of the convergence criteria has been developed. And it is being used in monitoring how we are doing in the implementation of the convergence criteria,” he said.

Other than Burundi, it is said, Rwanda, Kenya, Uganda and Tanzania have prepared the medium term convergence programme and ministers of finance approved.

The approved plans provide a trajectory on how the bloc moves from 2016 to 2021.

The EAMU Protocol lays groundwork for a monetary union within 10 years and allows Partner States to progressively converge their currencies into a single currency.

In the run-up to achieving a single currency, Partner States aim to harmonize monetary and fiscal policies; harmonize financial, payment and settlement systems; harmonize financial accounting and reporting practices; harmonize policies and standards on statistical information; and, eventually establish an EAC Central Bank.

Whenever EAC finance ministers convene, Njoroge said, they also review progress in implementation of EAMU.

The Monetary Union which comprises three sectors – financial; trade; along with investment promotion and private sector development – aims to promote and maintain monetary and financial stability. This is also aimed at facilitating economic integration to attain sustainable growth and development of the region.

Related News

Fourteenth Replenishment of the African Development Fund

Donors agree on US $7.06 billion to the African Development Fund (ADF); increased financing for fragile countries; and scaled up support to the private sector

A global coalition of donors pledged to support the structural transformation of African economies and the African Development Bank’s High Five priorities by agreeing on US $7.06 billion over the next three years to support development projects and programs in the 38 lower income African countries supported by the African Development Fund (ADF).

“We are appreciative of the support of the donors of the African Development Fund, especially in the difficult global economic environment,” said the President of the African Development Bank Group, Dr. Akinwumi Adesina.

“I also appreciate the strong support of our donors for the vision, direction and ongoing reforms of the Bank Group to deliver greater developmental impacts for Africa. The African Development Fund will continue to play a significant role to build resilience for the economies of low income countries in Africa, especially those experiencing conditions of fragility or vulnerability,” added Adesina.

The African Development Fund will shift more resources to support the private sector in the region, even as it helps countries dealing with fragility to address their most pressing developmental challenges. The increased resources devoted to these countries reflect their strong need for concessional funding.

Recognizing the private sector’s key role in the transformation of African economies, the Fund will allocate over US $ 280 million to the Private Sector Credit Enhancement Facility. This Facility will leverage approximately US $ 840 million of private sector financing, of which at least 50% will be in higher risk countries. The Fund will continue to promote financial instruments that crowd in resources from the private sector, such as financial guarantee products.

The ADF is the concessional window of the African Development Bank Group, which contributes to poverty reduction and economic and social development in low-income African countries. The funding will support the five key priorities of the African Development Bank Group: Light up and Power Africa, Feed Africa, Industrialize Africa, Integrate Africa, and Improve the quality of life for the people of Africa. In addition, it will address four critical cross-cutting areas: fragility, governance, climate change and gender.

Related articles

Related News

East Africa: One-stop border posts, axle-load laws set for January

East African Community laws on the one-stop border posts (OSBPs) and the vehicle axle load control will not take effect until January over a technical lapse.

The laws were due to take effect on October 1 but for a failure to secure the signature of the new Heads of State Summit chairman, Tanzania President John Pombe Magufuli, in time.

Alfred Kitolo, director of infrastructure services at Kenya’s Ministry of East African Community Affairs, said the EAC Council will now have the gazette notice with the two laws signed during the EAC Summit in January, whereupon implementation can start.

The two laws were passed in 2013. Previously, after passage, a law would be moved to each of the five capitals (minus South Sudan which joined recently) to be signed by the president of the each member country.

As the EAC partner states wait for the January meeting to get the gazette notice signed, stop-gap measures are being implemented.

“The delay did not affect business because the partner states were operating OSBPs based on bilateral agreements which were consistent with the OSBP Act,” said Dennis Kashero, the communications director at TradeMark East Africa (TMEA).

The existence of these OSBPs has made it possible for TMEA’s investments in the electronic single window and tracking system to become operational. These mean the Single Customs Territory (SCT) is also working in the EAC.

“As a result of SCT implementation and OSBP clearance process, transit of cargo destined to Uganda from Mombasa has been reduced from 18 days in 2012 to 4-5 days,” said Mr Kashero.

Mr Kashero added that OSBP infrastructure made it possible for immigrations officials to be in one office. Thus, immigration officials are able to clear passengers once and much faster on either side of the border.

The assertion that there are bilateral agreements temporarily working, as the countries wait for operationalisation of the EAC laws is backed by Mr Kitolo. He highlights the case of Kenya, where the national laws that puts the maximum axle load at 48 tonnes have been repealed.

Before the passing of East African Community Vehicle Load Control Bill in 2013, Kenya’s axle load limit was 48 tonnes. But according to Mr Kitolo the vehicle load limit has been increased to the Tanzania and Uganda standard of 56 tonnes.

“It is just that the transporters have not yet adopted the new rules,” says Mr Kitolo.

While the axle load limit appears not to have changed, the existence of OSBPs has eased the movement of goods and services in East Africa. There is however a challenge for non-customs officials. The OSBP project only covered the integration of information and communications technology for customs systems like Asycuda (for Uganda and Rwanda) and Simba (for Kenya).

According to Mr Kitolo, in this case, an immigration official will have to physically move with the documents he worked with across the border, and feed them into the computers of the respective countries.

Lost time

Ronah Sserwadda, the director of trade and integration at Uganda’s Ministry of EAC Affairs added that time is lost when government officials have to ask each other what the other has done.

“We want systems to talk to each other, so that officials from the different countries don’t have to spend time asking what the other did,” she said.

Currently, added Ms Sserwadda, the EAC countries have different border control systems.

But TMEA officials say these challenges won’t be solved by operationalisation of the laws.

According to Mr Kishero, immigration is independent of the OSBP arrangement. TMEA is only handling customs related systems and immigration departments would have to look elsewhere for support.

This is the same problem with the agriculture ministries. Since most of the exports are agricultural products, having agriculture officials actively talking each other would ease trade.

Mr Kitolo said implementation in this area has been slow, the exception being with the traders who cross with goods worth less than $2,000. For such traders, the rules of origin forms are found at the border. Traders with a lot more goods are forced to go to the different capitals of the EAC to confirm the origin of the commodities.

Ms Sserwadda however said that having presidents sign the laws represents acknowledgement, and this can set the stage for starting the implementation and national investment in the case of each partner state.

African policymakers get new, reliable climate data

Climate change in Africa is least-researched and poorly understood, but a new report could help decision-makers get reliable scientific information about it to aid planning.

The report, from Future Climate for Africa (FCFA), has new information that could be used in decision-making, leading to great potential benefits for millions of Africans affected by climate change.

Julio Araujo, FCFA research officer based in South Africa, says that scientific literature on climate change in Africa is significantly low.

The FCFA, a five-year, £20 million (almost $25 million) programme with funding from the UK Department for International Development and the UK’s Natural Environment Resource Council, began in 2014 and has groups of researchers creating climate change data to aid policymaking in Africa.

A statement released by the FCFA on the report last month (9 November) says: “Climate modelling indicates that east Africa is expected to warm in the next five to 40 years, although changes in rainfall are much less certain,” adding that extreme events such floods and droughts could increase in the future.

However, lack of scientific data makes the region to be severely understudied.

According to the report, Southern African economies are exposed to weather and climate vulnerabilities, and sectors such as agriculture, energy, and water management are most effected.

Essential resources, therefore, are at great risk but most government departments still depend on planning based on a three-to five-year time horizons, ignoring that climate projections are based on decades-longer timeframes.

The report explains that past data being applied by ministries could be inaccurate because of wrong assumptions, noting that climate change could negatively impact African economies, especially in the future if it is not addressed.

The report has 15 factsheets covering specific regions including East Africa, Southern Africa, Central Africa and West Africa and six countries – Malawi, Rwanda, Senegal, Tanzania, Uganda and Zambia.

“In order to effectively influence relevant policies in a country or region, you will need to engage with the relevant decision makers at that scale,” Araujo tells SciDev.Net. “Working with decision-makers to produce appropriate information that is usable will lead towards positive changes in the policies and investments, which will in turn benefit the smallholder farmers who are adversely impacted by climate change.”

Daniel Olago, an environmental geoscientist at the Institute for Climate Change and Adaptation, University of Nairobi, Kenya, concurs and attributes low research on Africa’s climate change to challenges such as widely spaced weather stations and missing data, few meteorological scientists in research and a more “chaotic” climate system.

According to Olago, there is a need for reliable scientific information about the continent’s changing climate because sectors such as agriculture and pastoral livestock depend largely on rainfall and support the livelihoods of many people.

“The changing climate is… resulting in changes in the timing, distribution, intensity, and amounts of rainfall during the seasons relied upon for planting or natural replenishment of pasture,” he tells SciDev.Net.

This has resulted in major crop and livestock losses, depressed and variable productivity, with concomitant adverse impacts on people’s livelihoods and well-being, Olago adds.

Related News

Better international co-ordination could lead to more worldwide benefits from migration

Despite growing economic dynamism in many developing regions, international migration flows are not being diverted towards these new alternative poles but rather are concentrating in advanced economies, according to a new OECD Development Centre report.

Perspectives on Global Development 2017: International Migration in a Shifting World shows that while the share of global migrants originating from developing countries has remained fairly stable at around 80% over the last 20 years, the share of developing country migrants heading to high-income countries has jumped from 36% to 51% of the world total. The report documents the impact of migration on developing countries and discusses policies that can help maximise gains from it and foster development.

Various factors influence today’s migration patterns. Notwithstanding rapid economic growth in many developing economies, the average per-capita income differential between developing and advanced economies has increased from around USD 20,000 in 1995 to more than USD 35,000 in 2015, making the latter even more attractive for migrants. While well-being in developing countries has improved in areas like life expectancy, security, health and education, the disparity with advanced countries remains high. The presence of migrant networks (family, friends and community) already living in destination countries facilitates migration, reinforcing the concentration in a few preferred destinations.

Other factors affecting migration patterns include immigration policies, rising education levels in developing countries, and changing demographics and labour market needs worldwide.

The share of the world population living outside their country of birth has risen from 2.7% in 1995 to 3.3% in 2015, an increase of about 85 million people in two decades to roughly a total of 245 million international migrants.

“Migration is a natural result of economic development that can benefit both countries of origin and destination. This trend is here to stay, so it has to work for all countries,” said Angel Gurría, the OECD Secretary General. “Improved co-operation would help developing, emerging and advanced economies better manage migration to the benefit of all, making sure that there are more winners and fewer losers from migration.”

Migration can have both positive and negative impacts on countries of origin as well as those of destination. For the countries migrants are leaving, the loss of labour can relieve pressure in over-crowded labour markets, propping up wages and easing unemployment. Moreover, migrants send home remittances and bring knowledge and ideas as they return. But emigration also can come with economic and social costs, such as labour shortages, a loss of educated and skilled workers and social repercussions for family members left behind. Public authorities in countries of origin need to address such costs while putting in place conditions to maximise the benefits.

Countries of destination can benefit from migration to make up for worker shortages, especially in specific sectors. Immigrants also contribute more than just their labour: they also invest in their host country and help create jobs. Besides, immigrants are less likely than native-born citizens to receive government transfers. However, immigrants are less likely to have formal labour contracts than native-born workers. Public policies in developing countries of destination need to invest in immigrants’ economic and social integration and address the potential impacts that large inflows can exert on the capacity of public services, notably at the sub-national level.

As the number of people migrating is likely to continue to increase, the need is growing for greater international co-operation to manage migration flows as well as a framework for handling refugee crises – which are a separate and smaller phenomenon than economic migration. Even with the current crisis, refugees represent less than 10% of total migrants worldwide.

Better international co-operation should span areas such as the protection of migrants’ rights, visa agreements, recruitment and remittance costs, as well as qualifications and skills partnerships.

To reach these ambitious objectives, the successful inclusion of migration-related targets in the Sustainable Development Goals is a key step towards establishing commitments that can be monitored multilaterally, regionally and nationally. The United Nations’ proposed Global Compact for Safe, Orderly and Regular Migration is a positive development towards promoting more effective international co-operation. The Global Compact on Refugees will be another important component towards creating a robust framework to deal with future refugee crises.

Highlights from the report were discussed on 11 December 2016 at the Global Forum on Migration and Development in Dhaka, Bangladesh during a session on the future for international migration in a shifting world, with the participation of experts from the OECD Development Centre, including Federico Bonaglia, Deputy Director.

Global Forum on Migration and Development (GFMD)

The Global Forum on Migration and Development is a series of activities throughout the year that culminate in a week-long programme of government and civil society meetings that have been taking place since 2007.

The Forum emerged from the first UN General Assembly High Level Dialogue on International Migration and Development in 2006, as a process outside of the UN system where policymakers and stakeholders from countries all over the world come together to discuss about migration and development.

To this day, it remains the only global mechanism available to discuss migration and development with the full range of actors involved in migration – from grassroots organisations all the way to national governments and international organizations.

The 9th meeting was held in Dhaka, Bangladesh on 10-12 December 2016 under the overarching theme “Migration that works for Sustainable Development of all: Towards a Transformative Migration Agenda”. This year’s Forum is focused on three main pillars: economics, sociology and governance of migration and development.

The overarching theme is based on a ‘SDG Plus’ approach, i.e. to incorporate and advance, in the context of deliverables, a range of migration specific issues, ideas and elements that have already been recognized inter alia in the two UN General Assembly High level Dialogues on International Migration and Development (2007, 2013) and in various other dialogues/platforms, global consultative processes and outcome documents over the past decade.

Related News

Innovative research helps Rwanda raise $9m in tax revenue

In North America and Europe, substantial research has been conducted to evaluate the effectiveness of various communication strategies for improving the compliance of taxpayers. For the first time, a similar study has been carried out in Africa, generating important research findings and helping to raise an additional $9 million USD in tax revenue for Rwanda.

On the whole, studies in the West have found deterrence messages about the penalties taxpayers will face if they do not declare or under-declare their income to be the most effective. In contrast, the new study reveals that Rwandan taxpayers are generally more responsive to friendly messages, either gentle reminders of deadlines or information related to the importance of tax revenues for funding public services.

The effectiveness of non-deterrence strategies is good news for low-income countries, where enforcement is severely limited by lack of financial and human resources. It also fits with the Rwanda Revenue Authority (RRA)’s vision of a modern tax administration, as Commissioner General Richard Tusabe said at the research presentation in Kigali on Monday, “Encouraging voluntary compliance is at the core of the RRA’s customer-oriented approach.”

The study also found that non-traditional and low-cost channels of communication, such as emails and SMS messages, were very effective in the Rwandan context. This is also an important finding for low-income countries, which must find cost-effective ways of generating revenue.

The study was conducted by the International Centre for Tax and Development in partnership with the African Tax Administration Forum, and in collaboration with the RRA. It was largely funded by UK Aid from the UK government, which highlighted the project as “high impact” in a recent Research Review. Not only did the project help raise additional revenue, it also catalysed innovations in the RRA’s operations (such as automatically personalising communications and expanding the functionality of its SMS platform), helped build research capacity within the RRA, and provided practical policy recommendations.

By using the RRA’s administrative data and experimental methods, the project is not only ground-breaking, but also highlights the importance of embedding rigorous evaluation in the design and implementation of new policies. As Mick Moore, the CEO of ICTD said, “Governments are constantly experimenting with new measures to improve tax compliance, but often don’t know which ones work. This kind of research can help them answer those questions so they can adopt the most effective strategies.”

Related News

EAC borrows leaf from Japan, Vietnam for automotive industry

East African Community experts have concluded consultative missions in Vietnam and Japan, a benchmarking exercise aimed at borrowing a leaf on how the Asian nations developed their automotive industries.

According to Jean-Baptiste Havugimana, the East African Community (EAC) director for productive sectors, experts from partner states and the Secretariat travelled to Tanzania, Kenya and Uganda “to compile baseline information on the status of automotive industry,” and to Vietnam and Japan for a benchmarking exercise.

“These missions took place from September 20 to October 7. Thereafter, the team will visit other countries in East Africa (Burundi, Rwanda) for in-depth analysis, and to others in Africa such as Ethiopia, Nigeria and South Africa for benchmarking,” Havugimana told The New Times at the weekend.

In October, a three-day meeting of a broad spectrum of stakeholders and experts from the automotive industry, finance, customs and trade sectors as well as vehicle manufacturers from EAC was held in Nairobi, Kenya.

It was aimed at reviewing and validating progress report on the comprehensive study on automotive industry.

The stakeholders would then provide inputs toward its finalisation and inform the EAC and potential investors on policy options and modalities to promote and develop the motor vehicle industry.

The initial benchmarking study missions revealed that usage of local content was one of the drivers for the growth of the automotive sector.

“This is an area that EAC needs to explore further and adopt appropriate measures that will consequently spur the development of the sector,” reads part of an EAC statement.

The experts also noted the need for policy coherence within different sectors for the progress of the automobile sector.

‘Need for volumes’

It was observed that for the industry to grow, there is need for volumes that can lead to economies of scale and, therefore, a regional approach to develop the sector and leverage on the EAC, Common Market for Eastern and Southern Africa (COMESA) and Southern African Development Community (SADC) tripartite free trade area.

The EAC industrialisation policy and strategy (2012-2032), now under implementation, aims at transforming the bloc’s manufacturing sector through higher value addition and product diversification based on comparative and competitive advantages of the region.

In 2015, the 16th Ordinary EAC Summit directed the Council to study modalities for promotion of motor vehicle assembly in the region and to reduce importation of used motor vehicles from outside the Community.

The 17th Ordinary Summit, in March, took note of progress and the roadmap towards finalisation of the comprehensive study on EAC’s automotive industry.

It directed the Secretariat to expedite the process and report to the 18th Ordinary Summit, which is expected next month.

In line with the policy directives, the EAC Secretariat, with financing from Japan International Cooperation Agency (JICA), commissioned a study to be finalised in April next year.

A draft progress report outlining the initial policy issues emerging from the benchmarking missions was prepared.

During the benchmarking missions, Japanese academicians shared their global best practices of promoting the automotive industry in the region, while the EAC delegation made presentations on the status and challenges facing the automotive industry in their countries.

Accordingly, it was observed that the motorcycle sector is growing rapidly in across EAC. With the rise in number, it was noted, the sale price drops due to economies of scale.

The EAC Secretariat and JICA say, along with the increase of production volumes, local production is gradually initiated for parts and materials that meet the effective minimum production scale.

In addition to complete build-up unit sales itself, they say, demands are increased for repair services.

The motorcycle sector is, thus believed to offer opportunity for rapid development of the region’s automotive industry.

According to Richard Ndahiro, a regional financial services professional, for an EAC auto industry to take off, a regional approach to the manufacturing sector is the right way to go so as to reach the economies of scale that allow competition with established global manufacturers.

“On the demand side, key drivers for uptake will be: quality of the automotives. The perception that local products are of lower quality remains a barrier,” Ndahiro told The New Times.

“Access to asset financing is key to unlock affordability for a larger segment of EAC population to acquire these automotives.”

Potential boost to agriculture

The Rwandan economist added that the bloc’s automotive industry would be “a big boost in the mechanisation of agriculture and other productive sectors in the EAC.

For example, he said, by providing automotive tools and equipment that are well customised to the “realities of our rural setting” and farmers.

He said the ability to move people, goods and services across the region, remains a big huddle partly due to poor infrastructure, “which is now being tackled,” but also because vehicles remain a luxury.

After noting the potential since Kenya and Uganda already have promising motor vehicle assembly plants, it is said that EAC leaders decided to nurture the automotive industry in the Community.

Their objective is to phase out imported old vehicles so that new ones are assembled in the region thus creating jobs and cutting on pollution from the imported used vehicles.

The automotive industry, one of the world’s most lucrative economic sectors by revenue, is a wide range of companies involved in design, development, manufacturing, marketing, and selling of motor vehicles.

Kenya, the region’s leader in motor vehicle assembly, boasts three plants: Kenya Vehicle Manufactures, Association Vehicle Assemblers, and General Motors East Africa Limited, which focus on assembly of pick-ups and heavy commercial vehicles.

Uganda’s Kiira Motors Corporation this year unveiled its Kayoola prototype electric bus.

Related News

tralac’s Daily News Selection

The selection: Monday, 12 December 2016

Kenya’s Amina Mohamed: It is time to unleash Africa’s full potential

Starting tomorrow: In Brazzaville: UNECA-convened meeting on the implementation of the African Mining Vision in Central Africa; In Ouagadougou: WAEMU Commission and Ferdi conference Regional integration in West Africa – progress and challenges

New uploads from the recent UNU-WIDER, SA National Treasury conference: presentations, poster sessions

African Continental Free Trade Area: policy and negotiation options for trade in goods (UNCTAD)

In the case of the CFTA, the current timetables and time targets may need to be reviewed. This basically stems from the fact that African economies are at such level of variation in terms of development, macro-economic policy regimes, infrastructural development, and others which may not allow the conclusion of the negotiations in 2-4 years. This will certainly require a serious introspection by the Heads of State and Government at their earliest convenience. Given all of the above, it may be more realistic to expect the CFTA negotiation in goods to take about 2-4 years to complete. This time period would be more in tune with experience and best practices from the field. [The analyst: Magdi A. Farahat]

‘Regional banks are vital to connect Africa to the global economy’ (City Press)

An ever-increasing regulatory burden has severely constricted the global banking sector, with dire consequences for trade flows and development in emerging markets. Deputy chief executive of Barclays Africa Group, David Hodnett, said that “There is no doubt in my mind that if regulatory reform continues to follow the trajectory we have seen so far, there will be no banks left that are truly global.” With the pull back of global banks in the region, Hodnett said regional banks would need to become a bigger feature on the financial services landscape in Africa, as these are vital to ensure the continued connectedness of Africa to the global economy.

SADC Brokers discuss ways to boost cross border trading (Namibian Economist)

The Committee of the SADC Stock Exchanges (CoSSE) hosted its inaugural SADC brokers’ networking session, at the Johannesburg Stock Exchange [last] week. Vice Chairman of CoSSE and the CEO of the Namibian Stock Exchange Tiaan Bazuin, who oversaw the session said: “Now, the idea is to have all SADC brokers signing associate agreements with brokers in each SADC country with the aim of trading each other’s stocks; they would have to share information and allow foreign investors to have a broader range and view of the happenings in other African markets. This is the first step towards more harmonisation, regionalisation and integration. It is about how to interconnect markets and how to grow other African markets outside the massive South African markets. Most importantly it will help us to keep African capital in Africa instead of shipping it off overseas,” he added.

Donor coordination and transport in West Africa: towards people, partnership and prosperity? (ECDPM)

West Africa is not to be left behind, with a recent workshop in Abidjan, Côte d’Ivoire about moving “Towards a more coordinated approach to corridor development in West Africa” and a further donor meeting on how to improve their coordination around trade facilitation in Accra last week. In the swirl of thoughts and debates following those discussions, four key points keep coming back that might help shape further progress in ECDPM work and beyond: [The analyst: Bruce Byiers]

How Nigeria’s economic challenges affect West Africa – ECOWAS (Premium Times)

The depreciation of the naira and other economic challenges affecting member states have slowed down ECOWAS economic integration and the adoption of a single currency, the News Agency of Nigeria reports. This was one of the main issues discussed at the technical meeting of the ECOWAS Macroeconomic Policy Committee on Multilateral Surveillance in Abuja on Thursday. The out-going Chairperson of the committee, Ommy Sar Ndaiye, said that it was pertinent for member states to develop strategies to address the prevailing economic challenges. The ECOWAS Commissioner, Macroeconomic Policy and Economic Research, Mamadou Traore: “The deadline for the adoption of single currency is fast approaching. This committee should set an agenda to look into the progress made so far and identify challenges that may hinder its smooth operation.” [Dip in Nigeria’s currency a blow to ECOWAS agenda]

Automobile import ban through land borders: threat or trophy? (Nigeria Today)

On Monday, December 5, the federal government announced the prohibition of importation of vehicles, new and used, through land borders. The statement said there was a presidential directive restricting all vehicle imports to Nigerian Sea Ports only and the order would take effect from 1 January 2017. According to Adeniyi: “The restriction on importation of vehicles follows that of rice, whose imports have been banned through the land borders since April 2016. Importers of vehicles through the land borders are requested to utilise the grace period up till December 31, 2016 to clear their vehicle imports landed in neighbouring ports.” The government may have, with this restriction, acceded to one of the requests made by Nigerian Automotive Manufacturers Association to ease their operations.

Nigeria’s ban on ‘tokunbo’ cars, rice cripples Benin economy (New Telegraph)

The Federal Government’s ban on rice imports to Nigeria through the land borders has taken a heavy toll on the economy of neighbouring Benin Republic as its seaport, Cotonou Port, patronised over the years by Nigerian and Asian importers in their bid to either totally evade Customs Duty or avoid the high port charges by Nigerian seaports, has seen a drastic reduction in its use. The multi-billion dollar imports which the port normally handles, have always either been smuggled into Nigeria or entered into the country through approved border stations, but the port charges, freight forwarding charges and the labour charges go to Benin Republic, making the country parasitic on Nigeria as 95% of the cargoes the Cotonou Port handles in a year is consumed by Nigerians.

Experts to Buhari: Don’t succumb to blackmail on EPA treaty (Daily Trust)

A coalition of livestock rearer, farmers and other agricultural experts have urged President Muhammadu Buhari not to succumb to pressures and blackmails on the contentious Economic Partnership Agreements between the EU and ECOWAS countries. They made the call in Abuja at a stakeholders meeting jointly organised by the Association for the Promotion of Livestock in the Sahel and Savannah (APESS), the Confederation of Traditional Livestock Organisation (CORET), the Network of Breeders’ Organisation and Pastoralist in Africa ‘Reseau Billital Marrobe’ (RBM) and the Network of Farmers’ and Producers Organisations in West Africa (ROPPA).

5th Ministerial Retreat of the Executive Council: statement by Dr Nkosazana Dlamini Zuma

As citizens become more aware of their rights, including the programmes of Agenda 2063, we are likely to see more such mobilization around these aspirations. On governance, as we implement our national, regional and continental frameworks, we are also rebuilding the planning and implementation capacity destroyed primarily during the dead decades of structural adjustments. This process is uneven, but we must build the capacity of our institutions as we implement our programmes. The 5th Retreat will also consider the draft Commodities strategy, looking at oil and gas, minerals and agricultural products, so that these natural resources contribute towards job creation, industrialization, our collective food security and transformation.

Tanzania: Coal debate lingers despite Dangote’s assurance to JPM (The Citizen)

The owner of the Mtwara-based Dangote cement factory, Mr Aliko Dangote, says he is against his company’s decision to import coal and gypsum for use at the factory. “We will utilise whatever we have locally, and already we have been assured of getting the amount of coal that we want. I also gave the President my firm commitment for further investments, and we are looking into other areas like agriculture and coal,” the Nigerian billionaire said after holding talks with President John Magufuli at State House on Saturday. President Magufuli reiterated at the meeting what his ministers had been saying in the wake of the controversy surrounding cement manufacturers’ energy needs. “It is unthinkable for the country to allow the importation of coal while quality stocks that can last for over 200 years are available,” he said. However, Mr Dangote’s assurance did little to dismiss concerns on the quality and quantity of local coal, which were recently revealed by a government-commissioned report. [Dangote, Tanzania government reach natural gas supply deal]

Mozambique Economic Update: Facing hard choices (World Bank)

According to the report, the policy response has picked up pace in the second half of 2016. A revised budget for 2016 was a first step in adjusting the fiscal framework to the new realities. The Central Bank of Mozambique, stepped-up its monetary tightening regime. There are now signs that pressures on the external position are easing as imports have declined and the metical has remained relatively stable since October 2016. In addition, the initiation of an independent audit of the Empresa Moçambicana de Atum (EMATUM), Mozambique Asset Management (MAM), and Proindicus loans is a key step in rebuilding confidence. However, a sharper focus on fiscal adjustment in the medium term is still needed to restore fiscal sustainability. The Economic Update notes that Mozambique’s gas production prospects shape expectations for a recovery in growth to 6.6% by 2018. In the meantime, existing megaprojects are showing resilience and may benefit from a boost in the near term from an improving outlook for key commodity prices.

Spar Zambia to be sold off (Lusaka Times)

Innscor Africa Chief Executive Officer Julian Schonken said on Wednesday during the presentation of the company’s results that he expects the selloff Spar Zambia to be concluded by end of this year. Mr Schonken said: “Once the disposal of Zambian operations is concluded, we are essentially a Zimbabwe centric. We do need to look abroad but before we do that, we have a lot of work to do in Zimbabwe. We have had too many instances of good Zimbabwean businesses ourselves included outside out in the region and really battling because educational levels are completely different, the infrastructure is not what we are used to, there is bureaucracy. So we are going to be careful about how we do business before we go to other geographies,” Mr Schonken said.

Falling exports take their toll on SA’s current account deficit (Business Day)

SA’s current account deficit widened more than expected in the third quarter, as the value and volume of exports fell amid weaker output data from the productive sectors of the economy. The surplus on the trade account in the second quarter — when GDP growth also lifted to a surprise 3.5% — swung to a small deficit in the third quarter, which led the current account deficit to expand to 4.1% of GDP, the Reserve Bank said on Friday. That is up one percentage point from a deficit of 3.1% in the second quarter, and compares with economists’ forecasts of between 3.3% and 4% of GDP.

Rwanda’s dairy exports generated over Rwf9bn in 2016 (New Times)

Rwanda’s earnings from export of dairy products increased from $85,000 in 2012 to $11.5 million in 2016, Rwanda Dairy Competitiveness Programme II Impact Report shows. By 2016, according to the report, 78,000 additional litres of milk were being processed per day in Rwanda, helping meet a growing need for milk used in value added products. This move brought the quantity of milk processed daily to 110,000 litres. The report was released last week during the closure of dairy programme which ran from 2012 to 2016. [Kenya: Costly levies on farm produce open window to cheap imports]

Study shows food safety regulations will promote agriculture exports (AfDB)

Despite concerns over acceptance of African agricultural produce in the EU, a study on Tuesday revealed that the adoption of food safety regulations will promote inter-regional trade of agriculture commodities to the EU. The study, “Food safety regulations and export responses of developing nations: lessons from South Africa and Namibia’s fresh and frozen fish exports to the EU” was presented by Shingirirai Mashura, a Certified Economist from the University of Zimbabwe. Mashura delivered the paper during a session on agricultural trade, at the ongoing 11th African Economic Conference in Abuja

IFAD’s Kanayo Nwanze: Africa is squandering its potential

David Bennett: African agriculture needs trade not aid

Uganda: Experts warn government on Tripartite pact

AU to publish “The African Factbook”

Madagascar: World Bank Group commits $1.3bn support

Overview of developments in the international trading environment: annual report by the WTO Director-General

India’s trade grows 10% in Q3, currency ban to hit agri exports: Maersk Line (The Hindu)

From Bhutan’s red rice to goat meat from Mozambique: unique products can boost exports from the poorest countries

Related News

African Continental Free Trade Area: Policy and negotiation options for trade in goods

Introduction

Trade has been the motor of economic, social and political integration of African countries for many centuries prior to the establishment of Africa’s first regional body, the Organization of African Unity (OAU), in 1963. The OAU strived towards boosting intra-African cooperation and integration in the economic field at the continental level. It saw the formation of several regional economic communities that were created first with a view to consolidating the economic space of a particular region to harness potential benefits of such integration; and secondly, these would serve as the pillars or building blocks for eventual formation of a continental economic community. In 1980, the OAU adopted the Lagos Plan of Action for the Economic Development of Africa 1980-2000, articulating a regional development plan for Africa that included the formation of an African Common Market.

While several programmes and institutional creation proliferated, the level and rate of implementation of trade integration programmes of many regional economic communities (RECs) faltered. Weak implementation at the RECs level meant that efforts towards building up the continental community also wavered. With a view to reviving and launching the continental integration project, the OAU Abuja Treaty Establishing the African Economic Community was adopted in June 1991. It articulated the formation of a continental free trade area as a stepping stone toward the realisation of the African Economic Community. Momentum towards implementing this objective gathered speed with the formation of the African Union (AU) in 2002, replacing the OAU. AU member States paid greater attention to continental integration. In fact, Article 3 in the AU’s Constitutive Act, establishes that the third objective of the AU is to “accelerate the political and socio-economic integration of the continent”.

Subsequently, the AU decided to concentrate the process of fostering continental economic integration through trade integration. At the 2012 AU Summit, Heads of State and Government adopted a Decision on the Establishment of a Continental Free Trade Area (CFTA) by the indicative date of 2017 and endorsed the Action Plan on Boosting Intra-Africa Trade (BIAT) which identifies seven areas of cooperation namely trade policy, trade facilitation, productive capacity, trade related infrastructure, trade finance, trade information, and factor market integration. Then in June 2015, at the twenty-fifth Summit of the African Union, held in South Africa, African Heads of State and Government agreed to launch negotiations on the creation of the CFTA by 2017 through negotiations on the liberalization of trade in goods and services. This initiative presents major opportunities and challenges to boost intra-African trade.

In order to multiply the benefits of the CFTA and promote developmental regionalism in Africa, a comprehensive vision of trade and development needs to be in place. Expanded markets for African goods and services, unobstructed factor movements and the reallocation of resources should promote economic diversification, structural transformation, technological development and the enhancement of human capital. The CFTA must be ambitious in dismantling barriers and reducing costs to intra-African trade and in improving productivity and competitiveness. It must provide for governments to involve nonstate actors, especially private sector, civil society and academia, in the discussions on the intent, content and design of CFTA so that the resulting agreement can create opportunities for businesses to exploit and bring about benefits to ordinary citizens.

Key Considerations for Accelerated CFTA Negotiations

The Negotiating Mandate

Usually the first step to be addressed by States in any negotiating process leading to an FTA is for the countries to secure a negotiating mandate, through national consultative processes, and convey that to their negotiators. This mandate describes the objectives, scope and content of the agreement from the perspective of the country or regional body. In most cases, the initial mandate is defined fairly broadly since economies usually aim for comprehensive FTAs. In any case, the mandate informs the negotiators whether they can negotiate on goods, services and investment, and what their broad objectives in each of these areas should be.

Once the negotiations are under way and the ambit of possible outcomes becomes clearer, these negotiating objectives are then often refined through the repeat of the mandate process. In the course of a complex negotiation, this process may be repeated several times. In this way, the negotiating mandate gets redefined from time to time. Sometimes it gets broader as the negotiations proceed. What seems difficult at the start can turn out to be quite manageable later on. Most countries have processes of this kind, though the details will differ.

The national consultations are particularly important in gathering the views and interests of non-States actors such as the private sector, civil society and academia and workers. The non-State actors are, by virtue of their status, are not included in trade negotiations processes which are mainly intergovernmental (or government-to-government). Hence the importance of national consultative processes to garner the views of non-States actors is a prerequisite for them to own the outcomes of negotiations. Likewise, the negotiations conducted among member States could involve occasions or platforms where non-State actors are informed of progress made and provided an opportunity to provide suggestions on the draft agreement.

The Negotiating Team

The negotiating mandate is promoted by a country negotiating team that is assembled by the Government body responsible for trade negotiations. This can be done in more than one way. However, the overall approach taken by States tends to show many similarities. For example, they usually appoint a chief negotiator, drawn from the department or ministry responsible for that country's trade negotiations. This person then becomes responsible for progress on negotiating the entire agreement. He or she may also be the main conduit for contact with ministers, senior representatives of the private sector and heads of nongovernmental and intergovernmental organisations.

Whether the chief negotiator also takes charge of one or more subject areas, such as market access for goods, will depend on the magnitude and complexity of the negotiations and on the customary way of the country's management of negotiations. It is usual to appoint a deputy chief negotiator, especially when it is clear that the negotiations will be substantial.

The chief negotiator is usually assisted by lead negotiators who will look after one or more of the chapters of the proposed agreement. Services and investment sometimes have separate lead negotiators, partly because of the complexity of the subjects, and partly because domestic responsibility for these areas often does not lie with trade ministries. Services negotiations especially may impinge on the responsibilities of many ministries, such as education, justice, finance, communications and transport. An issue to be considered, however, is that an FTA is an instrument promoting international economic relations, and its contents have to be approached from that perspective.

National ministries in most cases have well-established channels of communication with the private sector which can be used to support the efficient conduct of the negotiations. No two negotiations are the same, and the number of lead negotiators and their responsibilities will depend largely on the substance of the negotiations.

Preparing for the negotiations and ensuring that positions are understood and the right arguments developed requires a major effort. This places considerable demands on the chief negotiator and his or her communications skills. Negotiating teams will need to be arranged around the lead negotiators. These teams usually consist of experts in their areas as well as generalist officers. The number and composition of these teams will probably change during the negotiations. This is because negotiations on some chapters finish early. In other cases, the teams have to deal with quite specific issues which call for the use a different kind of expert.

Regardless of the necessity of such changes, a negotiating party should aim to keep the core members of negotiating teams unchanged as much as possible. This applies especially to leaders. Their ability to recall the negotiating history of the agreement will always be welcome, and at times it will be essential. The chief negotiator’s position should change only when this becomes absolutely unavoidable. Achieving this desirability is made easier by the fact that free trade negotiations are typically concluded within two to four years, or longer.

Another important aspect of assembling a team is the need to ensure that it has funding for the conduct of the negotiations. Money will be required for intensive domestic and international travel by sometimes quite large teams. It may also be necessary to hire negotiating venues and to employ interpreters and translators. The budget cycle in most negotiating parties is, however, usually one year only. If this is the case, the negotiators must therefore ensure that their requirements are included in relevant funding bids.

In the case of regional FTAs, like the CFTA, which is supported by the AUC, there is need within the Commission to set up a CFTA negotiation team with a lead official to support the Commissioner of Trade and Industry in mobilizing the Commission to support member States in the negotiations. Such a structure already exists in the AUC which is an important achievement.

The Negotiating Process

Most negotiating processes consist of plenary (formal) meetings and many informal meetings. The plenary is normally used to adopt decisions and to keep the various teams informed of progress in other parts of the negotiations. Plenaries are not suitable for resolving difficult problems, but they can be used to explain to all participants in the negotiations where difficulties remain and what are the possible solutions to address them. The plenary discussions promote transparency of the negotiations. Plenaries could accordingly be kept focussed and take place as and when the need for arises. Plenaries occur less frequently than informal meetings.

It is usually much more convenient to have the specific of issues of negotiations discussed in small groups of countries with a real interest in resolving them. Many issues in the negotiations will be difficult. Some will arise in the first meeting, and remain till the end of the negotiations.

Adequate time should be provided to negotiators to produce a quality agreement. If the timetable is too compressed, the danger exists that some important issues will not be considered adequately. The other side of the coin is that the expectation of ample time tends to encourage a feeling that there is plenty of time to negotiate hence delays occur. Experience has shown that the important negotiation issues to all parties need to be addressed for negotiations to proceed smoothly to a conclusive end with a balanced agreement.

As noted above, in addition to the formal negotiations process, opportunities need to be provided for involving non-state actors to inform negotiators of their concerns and interest.

The Negotiation Content

The parties to the negotiations usually start with developing a reasonable timetable for the negotiating sessions and a set of principles which will broadly govern the conduct and content of the negotiations. These principles have to be detailed enough to offer genuine guidance. At the same time, they have to be flexible enough to be able to accommodate easily any changes to plans may have been formed and adopted.

Where there is a disagreement over including an issue in the negotiations, it is almost invariably better to start with agreeing that everything is on the table. It may well be that in some cases agreement to complete negotiations on a given issue is in the end not possible, and that the parties then decide to leave things for resolution at a higher (political) level. Such a body is the High-Level African Trade Committee (HATC) in the case of the CFTA. That decision should, however, be made only after other available options have been explored thoroughly. This is where chief negotiators play a key role.

The CFTA as a “supra-regional” agreement

In many ways the CFTA is to be an innovative and ground-breaking supra-national and supraregional arrangement. It is a mega-regional agreement of over 50 countries. It is thus proposed that a more direct approach is applied to the CFTA negotiations; an approach that would, in some ways, start from a clean slate, with a clear directive as to the level of ambition. This is particularly important in view of the results of trade impact studies reviewed previously.

Given the short time available for negotiating and implementing the CFTA, within the indicative date of 2017, it is proposed that:

-

The negotiating mandate issued by the AU Heads of State and Government could endorse a comprehensive and deep liberalization agreement covering substantially all the trade in goods, trade in services, and complementary supportive policy areas. The mandate should include the removal of customs/border obstacles, including the adoption of unified customs documentation and clearance process based on the single window approach. It should institute the enhancement of trade facilitation measures as an essential back-up support to liberalization of trade.

-

The mandate should also address specifically technical barriers to trade and sanitary and phytosanitary barriers. Greater convergence on these policies will help to mollify their potential trade distorting effects, and instead bring about a positive impact on intra-African exports in agriculture, food and industrial products.

-

Services trade in the CFTA has to be included from the start, not only to allow for potential trade-offs in market access all parties in agriculture and industry, but also to allow a more efficient use of the continent’s resources in critical areas such as road building, financial services, transport and logistics, and ICT. It is also important to include services in the CFTA, to facilitate further work on the issue of labour mobility within the continent.

-

In order for the CFTA to play a deep economic integration role, African states should look into incorporating investment and competition regimes into the mandate. This will provide not only clarity for the relevant national business communities, but will also provide a safety-net against potential negative abuses of the CFTA by transnational corporations,

-

As RECs would form the basic pillar from which the CFTA would be constructed, the inclusion of RECs in CFTA negotiations is necessary.

Inclusiveness and Transparency of Negotiations

Citizens, businesses and organisations outside the government will be affected by the CFTA. It is, therefore, important that in line with best practices in the field, the negotiating mandate should include direction on the processes of inclusiveness and transparency. This is to guarantee the maximum engagement by all parties affected by the negotiation, and minimise potential resistance by them and by parliaments at the conclusion of negotiations. Some of the bodies that will have to be consulted or may wish to be consulted, and who is included in negotiating teams depends on the conditions in a particular country. The following are some, in alphabetical order, that should be consulted:

- Agricultural producer and farming associations.

- Chambers of commerce and industry.

- Consumer bodies.

- Education and training providers.

- Importer and exporter associations.

- Specific-industry associations.

- Intellectual property associations.

- Professional associations.

- Standard-setting bodies.

- Parliaments, their committees and members.

- Media and information resources.

- State/Departmental/County institutions.

- Special-interest NGOs, particularly those working in the field of environment, labour rights, and women/youth.

- Academia.

The range of groups approached in this way will obviously depend on the countries concerned and the type of agreement envisaged. If, for example, the aim is an agreement limited to goods, the range of services providers that need to be consulted is narrower than would be the case in an agreement covering goods and services. But in the case of a genuinely comprehensive agreement, as is the case with the CFTA, the range of possibly interested organisations and individuals will be large, and will require an important effort to manage.

It is also advisable that a public-relations/media/information effort is deployed throughout the negotiation process, with frequent updates to keep interested parties “in the loop”. It also requires that a feedback process is instituted to allow negotiators to have a “feel” for potential pressures from local parties.

Indeed, and in the CFTA context, the African Trade Forum, one of the organs of CFTA architecture adopted by the AU Summit, is already operational. At its Second Session that was jointly organized by the AUC and UNECA in Addis Ababa in September 2012, it made important recommendations on the implementation of the consultative processes within the CFTA that are line with the proposals above.

Leadership Roles and the AU