Search News Results

Reviews set out UK vision for an open, modern development system

New Bilateral and Multilateral Aid Reviews set out a vision for global development that will tackle the challenges of the 21st century.

The UK will champion an open, modern and innovative approach to development that will effectively tackle the global challenges of the 21st century while delivering the best results for the world’s poorest which is in our national interest, the International Development Secretary Priti Patel set out in two reviews launched on 1 December 2016.

Raising the standard: The Multilateral Development Review 2016 and Rising to the challenge of ending poverty: The Bilateral Development Review 2016 establish how the UK will address the global response to problems that threaten us here at home such as the migration crisis, cross-border conflict, climate change and disease pandemics.

In the reviews, the International Development Secretary makes clear that Britain’s aid contribution is an investment in our future security and national interest.

In an extensive and detailed look at the UK bilateral and multilateral development systems, the reviews confirm the geographic regions of focus for the UK, which multilateral organisations the Department for International Development (DFID) will work with, and the tools that will be used to maximise our impact as we tackle poverty across the globe.

The reviews highlight best practice in the global development system, as well as examples of poor performance that will face urgent action.

The UK is clear in its demand for high performance across the board and will maintain pressure on multilateral organisations and NGOs to ensure results, value for money, transparency and accountability.

International Development Secretary Priti Patel said:

From leading the international response to the Ebola outbreak in Sierra Leone to getting lifesaving humanitarian aid to millions of people in Syria, UK aid supported by the British public has had an incredible impact on helping the world’s poorest people.

But the global approach to development needs to adapt and reform to keep pace with our rapidly changing world. As a world-leader, the UK will be at the forefront of these efforts: promoting pioneering investment in the most challenging and fragile countries, making greater use of cutting-edge technology, and sharing skills from the best of British institutions from the NHS to our great universities.

Improving the way the UK delivers aid along with our multilateral partners is vital to deliver the best results in fighting poverty and value for taxpayers’ money.

Global Britain is outward looking and we will use our aid budget to help build a more stable, more secure, and more prosperous world for us all: this is not only the right thing to do – it is firmly in our interests.

Bilateral Development Review 2016

The Bilateral Development Review 2016 focuses on how the UK can deliver the best results on the ground for the world’s poorest people.

Key features of the Bilateral Development Review include:

-

The UK is calling for further transparency and even stronger measures on value for money, for both the UK and its NGO partners. The international aid system as a whole must become more effective, transparent and accountable to the poorest people in the world, and to taxpayers.

-

The UK’s bilateral development programmes will focus on security, migration, people with disabilities, health, and ending the reprehensible practices of modern slavery and child exploitation. The UK will ensure these priority areas are consistently considered in all areas of work.

-

The UK will tackle the major global challenges of the 21st century by strengthening global health security, creating job opportunities and making the best use of technology and research. As set out in the UK’s Aid Strategy, 50% of DFID’s spending will go to fragile states and regions, including in the Middle East and Africa.

-

In the foreword, the International Development Secretary sets out how the UK will continue to speak out against outrages in Syria and harness the spirit of urgency and impact that the UK showed during the Ebola crisis and apply it to the even greater task of eradicating extreme poverty.

Multilateral Development Review 2016

Britain’s support to multilateral development agencies will build on work which in 2014 immunised 56 million children in some of the world’s poorest countries, helped 10.4 million young people living through humanitarian emergencies to access education and provided access to clean water for 27.8 million people.

Key features of the Multilateral Development Review include:

-

By encouraging multilateral agencies to collaborate, the UK has helped secure significant results while ensuring value for money. For example, Gavi, the Vaccine Alliance, worked with UNICEF to order vaccines in bulk, which has saved around £900 million over the past 5 years. Gavi’s UK-backed vaccine programmes saved the lives of more than 4 million children between 2011 and 2015.

-

Reviewing the multilateral system has real impact. For example, the Food and Agriculture Organization (FAO) was put into special measures after the 2011 Multilateral Aid Review. Since then, they have modernised their management structure and delivered over US$100 million of efficiency savings between 2011 and 2015 and their performance is ranked as ‘good’ in this year’s review.

-

The UK government expects and insists that every penny of taxpayers’ money is spent in an efficient, transparent and demonstrably effective way. DFID is therefore introducing improvement plans for poor performing agencies.

UK aid spend will continue to be reviewed and partners will be held to account to make sure the international development system is delivering the best results for the world’s poorest and the best value for the UK taxpayer.

Related News

Globalization resets: The retrenchment in cross-border capital flows and trade may be less dire than it seems

The two decades following the Cold War were celebrated and decried as the era of globalization. Cross-border movement of capital, goods, and people expanded inexorably.

Between the fall of the Berlin Wall in 1989 and the early onset of the global financial crisis in 2007, international capital flows grew from 5 percent of global GDP to 21 percent; trade leaped from 39 percent to 59 percent; and the number of people living outside their country of birth jumped by more than a quarter.

But today the picture is more complex. International flows of capital have collapsed. Trade has stagnated. Only the cross-border movement of people marches on.

Do these developments portend the start of a new era – perhaps one of deglobalization? Such a reversal is possible: the rapid globalization of the late 19th century gave way to the deglobalization of the early 20th. And yet, in the absence of a shock comparable to World War I or the Great Depression of the 1930s, history seems unlikely to repeat itself. A look beyond the headlines suggests that globalization is changing rather than stagnating or reversing.

Capital flows

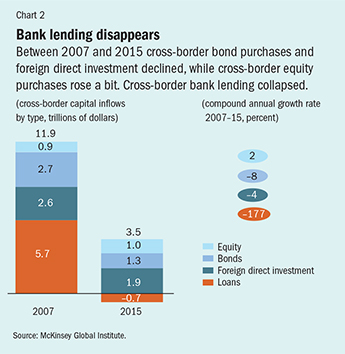

Consider first the trends in global capital movement – the most compelling area of the deglobalization story. The McKinsey Global Institute (Lund and others, 2013) reports that, in 2008, cross-border flows of capital crashed to 4 percent of global output, a fifth of their peak the previous year (see Chart 1). That collapse, and the even lower level of cross-border financing in 2009, reflected the extraordinary freeze-up of financial markets following the September 2008 bankruptcy of the U.S. investment firm Lehman Brothers. But what is more remarkable is that financial globalization has yet to recover. McKinsey, in an update of the data used in its 2013 study, reports cross-border flows fell to 2.6 percent of global GDP in 2015 and over the period 2011–15 averaged just 5.4 percent of global GDP – a quarter of the 2007 level.

What might explain this? The first clue can be found by separating cross-border finance into four categories (see Chart 2). One of these – portfolio equity investment, that is, investors’ purchases of shares in foreign stock markets – is up slightly in dollar terms since 2007. Two types of flows – bond purchases and foreign direct investment – have fallen, but not dramatically. It is the fourth – bank lending – that has collapsed. In 2015, net cross-border lending was actually negative, as banks called in more international loans than they extended. Taking these figures together, McKinsey calculates that the evaporation of cross-border bank lending explains three-quarters of the overall fall in cross-border finance since 2007.

To some extent – indeed, probably to quite a large extent – the retreat from cross-border lending represents a healthy correction. In the years before 2007, two parallel manias boosted international lending unsustainably: European banks were loading up on U.S. subprime mortgages, and banks in northern Europe were lending prodigiously to the Mediterranean periphery. It is therefore not surprising that the collapse of cross-border lending has been concentrated among banks in Europe. According to the Bank for International Settlements, euro area banks reduced their overseas claims by almost $1 trillion annually in the eight years following the Lehman Brothers bankruptcy, a far more dramatic contraction than occurred in other regions.

Getting it right

Seen in this light, the years leading up to the financial crisis are not a useful guide to how much financial globalization is normal or desirable. Cross-border capital flows peaking at 21 percent of global output reflected a toxic mix of ambition and credulity, notably among European banks. But if 2005-07 was an aberration, what is the appropriate benchmark for global integration?

One way to answer this question is to consider the period from 2002 to 2004, a relatively calm interlude between the early 2000s crash of internet-based companies (the so-called dot-com collapse) and the U.S. subprime borrowing and euro area bank lending mania later in the decade. In those three years, cross-border capital flows averaged 9.9 percent of global GDP. Judging by that benchmark, the new normal of 2011-15 is just over half the old normal of the previous decade. By this measure, financial deglobalization may have overshot.

There is, however, a second way of answering the question, for what was normal even in the calm years of the early to mid-2000s may not necessarily have been desirable. Since that time, there has been a reappraisal of the case for cross-border finance. For one thing, some of its theoretical advantages appear to be just that: theoretical. In principle, financial globalization allows savers in rich countries to reap high returns in fast-growing emerging market economies, thus easing the rich-country challenge of paying for retirement. Meanwhile, it supplies foreign capital to emerging market economies, allowing them to invest more and thereby catch up faster with the rich world. But in reality, many large emerging markets have grown by mobilizing domestic savings, exporting capital rather than importing it. The textbook case for financial globalization exists mostly in textbooks.

If the upside of financial globalization has been elusive in practice, the downsides have grown more obvious. First, global capital tends to rush into small open economies during good times, aggravating the risk of overinvestment and bubbles; it flees in bad times, exacerbating recession. That has led middle-income nations to experiment with capital controls. Second, cross-border banking involves large, complex, and hard-to-regulate lenders, which poses risks to society that became evident during the 2008 bust. Because of those risks, regulators in the rich world have discouraged banks from foreign adventures, which has added materially to deglobalization. Forbes, Reinhardt, and Wieladek (2016) show that, in the case of Britain, regulatory discouragement of foreign lending can be remarkably powerful, accounting for about 30 percent of the attrition in cross-border lending by U.K. banks during 2012-13.

Although there is no denying that finance is less international than it used to be, it is debatable whether this retrenchment is best described as “deglobalization,” with its connotations of retreat, or as something more positive – “sounder global management.” After all, the new regulatory restrictions are at least partly a response to the risks of cross-border financing, which suggests a desirable level of flows considerably lower than the 9.9 percent of global output during 2002–04. If the optimal ratio were, say, around 5 percent, today’s degree of financial globalization might be just about right.

Trade retreat

Now consider the second form of globalization: trade. Here, there is less doubt about the benefit of cross-border activity. The great development success stories of east Asia were built on exports. From Africa to Latin America to south Asia, autarky, in which states prefer self-sufficiency to trade, has fared badly as a formula for poverty reduction. According to economists Gary Hufbauer and Euijin Jung (2016), progressive trade expansion since World War II has added more than $1 trillion a year to U.S. national income, and the global gains are commensurately larger. Although it is true that trade, like technological advances, can skew the distribution of income, the benefits of globalization to the overall economy far outweigh the losses to workers hurt by imports. So the right response to inequality is not protectionism. It is taxing and spending policies that redistribute some of the overall gains to those who are hurt by trade. That this redistribution has so far been inadequate is a failure of politics rather than of globalization.

Because trade is so beneficial, the current backlash against it is damaging. The Doha Round of global trade talks has failed; the Trans-Pacific Partnership faces an uncertain path to ratification; efforts to conclude the Transatlantic Trade and Investment Partnership have stalled. By opting to leave the European Union, British voters demonstrated indifference to the benefits of Europe’s single market – or at least their unwillingness to accept migration as the price of membership. In the United States, the recent presidential campaign showed how support for trade has withered. Republican presidential candidate Donald Trump promised to impose punitive tariffs on trading partners. Democratic candidate Hillary Clinton abandoned her support for the Trans-Pacific deal.

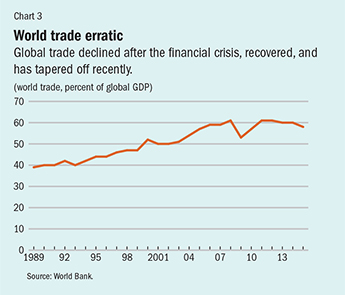

This backlash mirrors a sharp deceleration in the growth of trade relative to GDP. Between 1990 and 2007, global trade grew at about twice the rate of global output; since 2008, it has lagged global growth. As with financial globalization, this setback has outlasted the immediate aftermath of the Lehman crisis. Measured as a share of global GDP, trade crashed in 2009, then recovered sharply in 2010-11. But starting in 2012, it drifted sideways and then down (see Chart 3).

And yet, as with finance, this seeming shock to the project of constructive globalization is not as bad as it looks. A small part of the slowdown reflects the erection of myriad subtle trade barriers – what Hufbauer and Jung term “microprotectionism.” The IMF recently examined the effects of this uptick in protectionism and called them “limited.” So a larger part of the trade slowdown reflects statistical factors that should not be interpreted as setbacks to globalization. Some part may even reflect shifts that prove how effectively globalization is working.

Take, for example, the decline in trade from 60 percent of global GDP in 2014 to 58 percent in 2015 – a fall equivalent to $4.5 trillion. A good chunk of this decline is a statistical illusion: the dollar was stronger and commodity prices were lower, so the dollar value of trade went down. Most obviously, the oil price was 48 percent lower in 2015 than in 2014, causing an $891 billion drop in the value of oil traded, even though the number of barrels traded actually increased (BP, 2016). This effect alone explains a fifth of the shortfall in trade relative to GDP in 2015. Meanwhile, the price of iron ore was down 43 percent, and wheat was down 24 percent. These price adjustments make trade look anemic, but they tell us nothing about the health of globalization.

Trade can also be affected when production moves closer to consumers, even when this is not prompted by protectionist impediments to cross-border commerce. For example, a breakthrough in drilling technology, called fracking, has reduced the U.S. need to import oil and gas. The maturation of manufacturing supply chains in Asia may be having a similar effect. China used to assemble products such as the iPhone, importing such complex components as semiconductors. Today, China’s increasing sophistication allows it to make components domestically, reducing imports. In this way, ironically, China’s trade-based development model, which is a prime example of the success of globalization, has allowed it to reduce some aspects of its trade dependence.

Two final considerations encourage the conclusion that trade’s apparent stagnation is not a grave setback – at least, not yet. First, as the world economy becomes richer, it shifts naturally from manufacturing to services, and services are traded less, partly because of higher protectionist barriers in service industries. Second, to the extent that current account imbalances shrink, trade may decelerate, even though smaller imbalances are a sign of healthier globalization. In 2007, according to the World Bank, China ran a current account surplus equivalent to 10 percent of its economy – meaning that a shortfall in domestic spending required it to generate net exports worth a tenth of output. But by 2015, China’s current account surplus had shrunk to just 3 percent. China is now spending more of its income, so it is no longer compelled to ship so much of what it makes abroad. Of course, China could theoretically trade more even while avoiding a trade surplus. But reductions in savings imbalances may be a factor behind sluggish trade data. Savings deficits have shrunk in the United States and Mediterranean Europe even as China’s savings surplus has fallen.

In sum, trade is a clearly beneficial aspect of globalization. A world with minimal trade barriers allows producers in each country to concentrate on its comparative advantages, learn through global competition, and reap economies of scale. The policy backlash against trade is therefore troubling, especially since a less open and competitive world will mean slower gains in productivity, adding to the squeeze on middle-class incomes that trade’s critics lament. But the trade data, sometimes cited to support the view that we are deglobalizing already, do not justify despondency – at least, not yet.

Migration grows

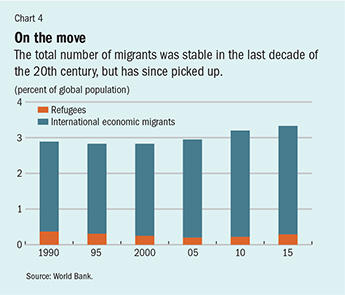

The third aspect of globalization, the movement of people, has been growing of late. During the 1990s, there was almost no increase in economic migration relative to global population: at the start of the decade, economic migrants accounted for 2.5 percent of the world’s people; in 2000 the share was 2.6 percent (see Chart 4). Since the turn of the century, however, migration has gained momentum, rising to 3 percent of global population by 2015. Some 222 million people now live outside their native countries, suggesting that expatriate opportunities outweigh the psychological benefits of rootedness – proximity to family and a sense of cultural affinity.

Tragically, trends in flows of refugees fleeing wars and other instability have followed a similar pattern, according to the World Bank. From 1990 to 2005, refugees declined as a share of global population, from 0.37 percent to 0.20 percent. But that trend has since reversed, with the refugee share rising to 0.29 percent in 2015 – still lower than the proportion in the first half of the 1990s, when millions fled the fighting in the former Yugoslavia, but bigger in absolute numbers. In 2015 there were 21 million refugees, more than the peak of 20 million in 1992. Moreover, the number of internally displaced people is higher now. The global problem of war and disaster-driven displacement is now at a record.

More positive than negative

If globalization is the process of sharing ideas and resources across borders, the evidence reviewed here is more positive than otherwise. Financial globalization has reversed, but the new level may be healthier. What’s more, foreign direct investment – the most stable, knowledge-intensive, and productive form of cross-border capital flow because it gives those in recipient countries a direct role in running a business – now accounts for a far larger share of total cross-border flows. With respect to trade, the political climate is damagingly hostile, but recent trade data are less worrisome than they appear. Meanwhile, the movement of people, perhaps the most important of the three traditional forms of globalization, continues to outpace global population growth. If globalization is ultimately about freeing individuals to seek inspiration and opportunity beyond their borders, or even just to escape harsh circumstances at home, there is little sign of a slowdown.

But the most compelling ground for optimism lies elsewhere. During the past 15 years or so a fourth channel for globalization has emerged, one that was barely recognized when the Berlin Wall came down. Ideas, data, news, and entertainment are now shared globally on the internet, in volume that dwarfs the traditional channels of interaction across borders. The McKinsey Global Institute (Manyika and others, 2016) reckons that this digital globalization now exerts a larger impact on growth than merchandise goods trade. Millions of small businesses that lack the scale to venture abroad physically have turned themselves into exporters by participating in online marketplaces. Some 900 million people use social media to connect with friends or colleagues across borders. Millions of students study in virtual classrooms, taught by people on the other side of the world.

The progress of globalization depends on two forces: technology, which eases travel and communication, and politics that underpin an open world. The remarkable thing about the 1990s was that both forces operated together: cheaper travel and telephony were reinforced by the opening up of China and by a series of breakthroughs in trade liberalization – the North American Free Trade Agreement, the European single market, and the Uruguay Round of global trade negotiations.

There is no denying that the world finds itself in a new era: technology still drives integration forward, but political resistance is growing. And yet, for the moment, the drag from politics seems weaker than the thrust from technology. Absent some truly cataclysmic shock – something akin to a world war or a depression – the best bet is that globalization will march on.

Sebastian Mallaby is the Paul A. Volcker Senior Fellow for International Economics at the Council on Foreign Relations and author, most recently, of The Man Who Knew: The Life & Times of Alan Greenspan.

Opinions expressed in articles and other materials are those of the authors; they do not necessarily reflect IMF policy.

References

British Petroleum (BP), 2016, Statistical Review of World Energy (London).

Forbes, Kristin, Dennis Reinhardt, and Tomasz Wieladek, 2016, “The Spillovers, Interactions, and (Un)Intended Consequences of Monetary and Regulatory Policies,” NBER Working Paper 22307 (Cambridge, Massachusetts: National Bureau of Economic Research).

Hufbauer, Gary, and Euijin Jung, 2016, “Why Has Trade Stopped Growing? Not Much Liberalization and Lots of Microprotection,” Peterson Institute for International Economics report (Washington).

International Monetary Fund (IMF), 2016, World Economic Outlook (Washington, October).

Lund, Susan, Toos Daruvala, Richard Dobbs, Philipp Härle, Ju-Hon Kwek, and Ricardo Falcón, 2013, Financial Globalization: Retreat or Reset? (Washington: McKinsey Global Institute).

Manyika, James, Susan Lund, Jacques Bughin, Jonathan Woetzel, Kalin Stamenov, and Dhruv Dhingra, 2016, Digital Globalization: The New Era of Global Flows (Washington: McKinsey Global Institute).

Using aid for structural change in fragile states could help curb rising instability

The world has grown more violent over the last decade, interrupting a long-term trend of increasing peace and disproportionately impacting civilians. This is despite rising financial flows to the most vulnerable places, according to a new OECD report.

States of Fragility 2016: Understanding Violence calls for more development aid to be used to tackle the root causes of fragility and instability, including building legitimate and inclusive political systems and institutions, strengthening security and access to justice, supporting economic growth and ensuring the availability of basic services..

Analysis of multiple data sources shows that global violence is at its worst level since the end of the Cold War, with nearly half the world’s population, or 3.34 billion people, living in proximity to or feeling the impact of political violence. Conflict is one cause of violent deaths, but in 2015 more people died violently in countries not afflicted by conflict. Central America is the region that suffers the most lethal violence, followed by Southern Africa, the Caribbean and South America.

Low- and Middle-Income countries bear a disproportionately high share of the burden of political and social armed violence, which often impedes development gains.

“If the challenges faced by these countries are not met, progress on combating climate change and achieving the Sustainable Development Goals will be stalled and millions of people will remain mired in poverty and conflict, the migration crisis will not be resolved, and violent extremism will continue to increase,” said OECD Deputy Secretary-General Doug Frantz, presenting the report during the 2nd High-Level Meeting of the Global Partnership for Effective Development Cooperation in Nairobi.

Defining fragility as the combination of exposure to risk in five areas – economic, environmental, political, social and security – and the insufficient capacity of the state or system to manage, absorb or mitigate those risks, the OECD estimates that more than 1.6 billion people, or 22% of the global population, live in fragile areas. While the number of people living in extreme poverty is falling, the number of extremely poor people living in fragile places is set to increase to 542 million in 2035 from 480 million in 2015.

The report notes that while the global economic impact of violence has been estimated at USD 13.6 trillion for 2015, or 13.3% of GDP, only a tiny amount of development aid is invested in violence reduction outside of conflict situations.

Total financial flows to fragile places, including official development assistance (ODA), foreign direct investment and remittances increased by 206% between 2002 and 2014 in constant terms to more than USD 2.04 trillion. ODA represents 32% of that total. While ODA remains an important tool for fragile states, some of it tends to be unevenly distributed and targeted at the symptoms rather than the real drivers of fragility.

Related News

New Great Lakes Trade Facilitation Project rolls out

The implementation of Great Lakes Trade Facilitation Project (GLTFP) has begun with earnest with the launching of recruitment for Trade Information Officers to be based at selected locations in the eastern borderlands of the Democratic Republic Congo and the neighboring countries of Rwanda and Uganda.

The GLTFP is financed by the World Bank and implemented by COMESA. Its objective is to facilitate cross-border trade by increasing the capacity for commerce and reducing the costs faced by small-scale traders, majority of who are women.

The project will build on existing Trade Information Desks (TIDs) established by COMESA in the selected border region including Goma in DRC and Rubavu in Rwanda, Kasindi (DRC) and Mpondwe (Uganda), Bunagana (DRC) and Bunagana (Uganda).

A total of 20 additional TID Officers will be recruited to complement the existing capacity as well as for the new desks that will be identified through the on-going assessment mission mounted by the COMESA Secretariat in the Great Lakes region. Additional Officers (TIDO) will be added to the posts where there is one.

In meeting with the COMESA team, the regional government authorities in Rusizi and Rubavu (Rwanda) and their counterparts in Bukavu and Goma in DR Congo have welcomed the initiative and pledged to support it to ensure the largely informal trade is gradually formalized.

The new desks are expected to be at Mahagi in DRC and Goli in Uganda and Bukavu (DRC) and Rusizi (Rwanda) border regions. The new Trade Information Desk Officers will help traders apply the COMESA Simplified Trade Regime (STR) whose objective is to facilitate cross border traders by providing general information about applicable duty and documentary requirements, taking complaints and reports of incidents, and assisting with conflict resolution.

Besides working with traders, the desk officers will work with various border agencies such as immigration, Customs and security officials, local cross-border traders associations, as well as with local government authorities.

tralac’s Daily News Selection

The selection: Monday, 5 December 2016

Starting today, in Abuja: the African Economic Conference 2016 on the theme ‘Ending hunger and enabling food security in Africa’. Twitter updates: #2016AEC

A guide to last week’s UNU-WIDER conference in Pretoria: ’Regional growth and development in Southern Africa: new data, new approaches, and new evidence’

Part I (pdf): The Republic of South Africa faces the imperative of escaping economic stagnation. The broad-level economic ills besetting South Africa are well known but bear brief repetition: real GDP per capita has hardly grown for nine years; productivity growth has been slow and appears to be slowing; the unemployment rate has recently been increasing from already extraordinarily high levels; and inequality remains stubbornly very high. Part II (pdf) considers southern Africa as a whole. It takes stock of the experience of the past two decades and seeks to chart realistic paths forward from a regional growth and development perspectives. It is structured as follows. Section 2 provides background and motivation including a discussion of the philosophy of the research programme undertaken within the framework of this project. Section 3 considers six specific areas where a regional growth and development perspective may have particular promise. These areas are: the spread of regional supermarket chains; the poultry value chain; trucking; mining equipment and related services; energy including bio-energy; and confronting climate change. [Downloads: research outputs and project documentation, tralac’s participation]

Intra-African trade and investment updates:

In Algiers: Business investment forum calls for action to improve intra-Africa trade (New Times)

Delegates at the three-day African Business and Investments Forum held over the weekend in the Algerian capital, Algiers, have once again urged business and political leaders in Africa to remove barriers that limit countries across the continent from trading with each other. Described by organisers as the first of its kind in the country and elegantly called the ‘Algiers Rendezvous’, the meeting attracted about 1000 participants from more than 40 African countries. “It took me about 20 hours to come to Algeria. We need to be better connected in order to work together,” said Amina Mohamed Jibril, Kenya’s Cabinet Secretary for Foreign Affairs. “Yogurt is imported at 83% in Africa. What is complicated in making yogurt?” wondered former Executive Secretary of the United Nations Economic Commission for Africa, Dr Carlos Lopes, essentially challenging his fellow Africans to explore the economic benefits of manufacturing. He also accused African financial institutions of being “lazy”, saying that they aren’t doing enough to support small businesses while they sit on an $80-billion capital that remains non-invested and sits idle in the banks’ coffers as they fear to invest it on the continent.

Egypt-COMESA: New customs tariffs on luxury goods aim at reducing imports – Egypt ministers (Ahram)

Minister of Finance Amr El-Garhy and Minister of Trade and Industry Tareq Kabil said on Sunday that the recent decision to raise tariffs on a number of luxury goods aims to support local industry and reduce imports. Last week, Egypt raised tariffs on 320 different luxury goods, including some fruits, cosmetics, stationary and electronic gadgets, between 40 and 60%. The increase was the second such hike in taxes on imported luxuries this year. The two ministers said in a joint statement that the rise in the rate of imports during recent years had put a huge burden on the nation’s economy, leading to a $49bn deficit in the public budget. This situation required critical decisions to limit imports and support local industry in a way that preserves Egypt’s international trade agreements, according to the statement. The ministers added that imported goods from parties that have free trade agreements with Egypt such as the EU, the COMESA African grouping, the Arab region and Turkey would not by affected by the new decision. [Egyptian government’s decision to exempt poultry from import taxes angers local producers]

@Trade_Kenya: Egypt-Kenya Business Council meeting in Cairo. @Kiptoock & chair Hossam Farid

Nigeria, Morocco agree to promote gas project to foster regional integration (Premium Times)

Nigeria and the Kingdom of Morocco have agreed to promote a regional gas pipeline project that would connect Nigeria’s gas resources, those of several West African countries and Morocco. The Minister of Foreign Affairs, Geoffrey Onyema, said the pipeline project would be designed with the participation of all parties involved to create a competitive regional electricity market with the potential to be connected to the European energy markets. He said Nigeria and Morocco also agreed to develop integrated industrial clusters in the sub-region in sectors such as manufacturing, Agro-business and fertilizers to attract foreign capital and improve export competitiveness. The News Agency of Nigeria reports that at the end of the 3-day official visit of King Mohammed VI to Nigeria, 21 bilateral agreements were signed between Nigeria and the Kingdom of Morocco. [Nigeria, Morocco and new levels of intra–African bilateral relations]

Dangote, Moroccan Group sign MoU on fertiliser production (Vanguard)

Nigeria’s agricultural sector has received a major boost as the Dangote Group and the OCP Group of Morocco signed an agreement to boost fertiliser production and business in the country. The partnership is expected to lead to the creation of an integrated African platform and a global leader in fertiliser production, A statement from the Dangote Group announced this on Sunday in Abuja. It said that the collaboration between the two African conglomerates would help the Dangote mix the mass deposit of phosphate in Morocco with the gas potential in Nigeria to produce fertiliser for the development of the agriculture sub-sector in Africa.

We want more trade with Egypt: Tunisian investment minister (Ahram)

Tunisia hopes for trade growth with Egypt, Tunisian Minister of Investment, Development, and International Cooperation Mohammed Fadel Abdel Kafi told Ahram Online at Tunisia’s 2020 investment conference. Abdel Kafi said in exclusive statements to Ahram Online that the size of economic cooperation was still tenuous, adding that he met Egypt’s minister of international cooperation, Sahar Nasr, in November to discuss economic cooperation between the two countries. In November, Nasr and her Tunisian counterpart discussed means to enhance cooperation between the two sides in the upcoming period, especially in the international, regional and Arab financial institutions, to obtain optimum benefit from both countries’ development partners.

Zambia-South Africa: Lungu dates South Africa (Times of Zambia)

President Edgar Lungu is this week expected in South Africa for a three-day State visit at the invitation of his South African counterpart Jacob Zuma. The President would be accompanied by Foreign Affairs Minister Harry Kalaba, Energy Minister David Mabumba, Tourism and Arts Minister Charles Banda and Commerce, Trade and Industry Permanent Secretary Kayula Siame, among other Government officials. "President Lungu and President Zuma will also address a gathering of Zambian and South African captains of industry, business entities and executives organised under the auspices of the Zambia-South Africa Business Forum," Mr Mwamba said.

Sixth SA-China Bi-National Commission: communique (The Presidency)

The Commission received and deliberated on reports of the Sectoral Committees on foreign relations, trade and investment, science and technology, mining, energy and education. They also reviewed the progress made with regard to the South Africa-China relations over the past three years and identified the way forward for the continuously expanding bilateral relations. The BNC witnessed the signing of the following Agreements: (i) MoU between the Department of Trade and Industry and the Ministry of Commerce regarding Co-Operation on Special Economic Zones and Industrial Parks; (ii) Framework Agreement between the National Development and Reform Commission of the People’s Republic of China and the Department of Trade and Industry of Republic of South Africa for Developing Cooperation on Production Capacity.

Profiled, recently published African trade statistics:

Nigeria: foreign trade statistics, 3rd quarter 2016 (National Bureau of Statistics): Nigeria’s import trade by direction showed the country imported goods mostly from China (with an import value of ₦478.7bn or 19.8% of total imports). This was followed by Belgium (₦331.3bn or 13.7%), Netherlands (₦299.7bn or 12.4%), the US (₦165.5bn or 6.9%) and India (₦121.3bn or 5.0% of total imports). Imports by economic region revealed that the country consumed goods largely from Europe, with import value of ₦1,158.4bn or 48.0%. The country also imported goods largely from Asia, with import goods valued at ₦843.27bn or 34.9%. Goods valued at ₦294.5bn, or 12.2% of total import trade, was imported from America. Import trade within the continent of Africa totalled ₦87.9bn or 3.6%, while imports from the region of ECOWAS amounted to ₦8.5 billion (see Table 4).

Mauritius trade deficit widens as exports drops (Statistics Mauritius): Mauritius’ trade deficit widened by 15.9% in the third quarter from the same period last year, as exports from the Indian Ocean island nation tumbled, the statistics office said on Tuesday. The deficit, at 21.17 billion Mauritius rupees ($590 million), was 11.7% higher than the second quarter, Statistics Mauritius said in a statement. The value of exports fell 12.6% to 20.71 billion rupees after exports of machinery and transport equipment tumbled by 47.1%. Imports dropped 0.2% to 41.88 billion rupees. [Detailed Trade Data by HS/Country Year 2005-2016]

South Africa: October merchandise trade statistics (SARS): Data from the SA Revenue Services showed that the trade balance switched to a R4.41bn deficit in October from a revised R6.9bn surplus in September. SARS said exports fell 11.1% on a month-on-month basis, while imports were up 0.4%. Profiled regional highlights: The Africa trade balance surplus was R20 086 million – a 4.0% increase in comparison to the R19 322 million surplus recorded in September 2016. BLNS trade recorded a trade balance surplus of R9.51bn in October, a result of exports of R12.49bn and imports of R2.98bn.

Intra-SACU trade data analysis (tralac): The objective for this paper is to examine intra-SACU trade with a special emphasis on the position of Botswana in this trade and the role of re-exports. The latter has become possible with the publication by the International Trade Centre of this re-export data, although we hasten to add that there is not a comprehensive coverage of the SACU in this data. Botswana’s data is available for 2015, but re-export data is only available for 2014. Namibian trade data is available for 2015 as mirror data, but re-exports are only available for 2013, while overall data for Swaziland is also available for 2015 in mirror data but re-exports are only until 2007. South Africa, the partner of most interest, does not have reported re-export data, and this is a significant omission from SACU’s trade data. Finally, Lesotho does not have re-export data either. Thus, we found that there was limited data to work with if we wanted to examine re-exports. [The analysts: Maria Nthebolan, Carla O Tema, Ron Sandrey]

Madagascar economic update (World Bank): Non-mining exports performed well in 2016. Exports recorded between January and October 2016 are estimated at $1,687 million, a 17% increase compared with the same period last year. However, the fall in nickel prices since 2015 and declining production volumes has adversely affected exports. In the first ten months of 2016 Madagascar exported $410 million worth of mining products, a decline of 10% compared to the same period the year before. The value of non-mining exports increased by 22.3% in 2016, largely driven by higher revenues from vanilla and cloves. Exports from free zone companies also increased from $434 million in 2015 to $546m in 2016, mainly resulting from textiles and shrimps exports to the Euro zone area. Under the Africa Growth and Opportunities Act the value of Madagascar’s exports is estimated to have tripled in 2016. [The analysts: Natasha Sharma, Faniry Razafimanantsoa]

Profiled trade policy postings:

Rwanda: Govt waives tax on leather, textile raw materials (New Times): The decision announced at the weekend was taken in collaboration with local leather and textile manufacturers in the face of government’s policy to ban second-hand leather and footwear products. The decision became effective Friday, 2 December 2016. Innocent Safari, the Permanent Secretary Ministry of Trade, Industry and EAC Affairs, explained at the weekend that the exemption applies to both import duties and Value Added Tax (VAT). The tax exemption applies to local investors recognised by MINEACOM; with no limitations on the quantity of leather and textile raw materials to be imported as the country seeks to satisfy the local market demands and export fine products abroad.

Tanzania: Private sector to shape EPA deal (Daily News): Tanzania’s Industry, Trade and Investments Minister Charles Mwijage told members of the private sector at the CEO Roundtable gala dinner in Dar es Salaam on Saturday that the government would take on board their views in reaching a position on the protracted negotiations of the trade deal with the EU.

Related News

African Economic Conference 2016: Ending hunger and enabling food security in Africa

Researchers, policy-makers and development partners converge in Abuja, Nigeria, for the 11th African Economic Conference (AEC) from December 5-7, 2016, to share ideas on topical African development issues including how to end hunger and ensure food security in Africa.

About 300 participants are expected to attend the annual event co-organised by the African Development Bank (AfDB), United Nations Development Programme (UNDP) and the United Nations Economic Commission for Africa (ECA), on the theme “Feed Africa: Towards Agro-Allied Industrialization for Inclusive Growth.”

The meeting will be officially opened by Nigeria’s President Muhammadu Buhari, AfDB President Akinwumi Adesina; Acting ECA Executive Secretary, Abdalla Hamdok; UN Assistant Secretary General and Director of UNDP Regional Bureau for Africa, Abdoulaye Mar Dieye.

This central theme is in line with the current African and global development agenda. Tackling poverty, hunger and food insecurity are central concerns of the Sustainable Development Goals (SDGs). The theme also builds on the African Union Agenda 2063 which underscore the right of Africans to be well-nourished and lead healthy and productive lives.

Furthermore, the Comprehensive Africa Agricultural Development Programme (CAADP), as well as the June 2014 Malabo Declaration emphasise the centrality of a structural transformation of African agriculture to growth and poverty eradication on the continent. In consonance with these goals, agriculture and industrialization are at the heart of the core activities of AfDB, ECA and UNDP and their vision and long-term strategy for a prosperous and inclusive Africa.

Participants at the African Economic Conference will be challenged to investigate the situation in which, despite overall macroeconomic growth and improved broad governance across the continent, Africa still has the highest rates of poverty and hunger in the world. No fewer than 230 million of the 795 million people suffering from chronic undernourishment globally live in Africa, resulting in the highest prevalence of undernourishment worldwide.

The African Economic Conference provides a unique platform to assess these challenges and the impact of current growth strategies in Africa; focusing on the agricultural and industrial sector.

Participants will discuss successes, lessons learned and identify remaining gaps, challenges and emerging issues on the topic. The conference will encompass in-depth presentations of policy-oriented research by both established academics and emerging researchers from the continent and beyond, who will debate and recommend policy options on how to accelerate Africa’s agricultural and industrial transformation.

After three days of intensive deliberations and brainstorming, the Conference is expected to come up with mechanisms for a sustainable inclusive green and scale agro-industry appropriate for a continent which is home to 600 million hectares of uncultivated arable land, roughly 60 percent of the global total.

Background

The theme for the 2016 African Economic Conference (AEC) is “Feed Africa: Towards Agro-Allied Industrialization for Inclusive Growth”. This theme is timely and in line with the current African and international development agenda. Ending poverty and overcoming hunger and food insecurity permanently come first and second, respectively, in the Sustainable Development Goals (SDGs) endorsed in September 2015 by UN member States. This commitment is also stressed by the African Union Agenda 2063 that recognizes the right of all Africans to be well-nourished and lead healthy and productive lives. Furthermore, the Comprehensive Africa Agricultural Development Programme (CAADP), as well as the June 2014 Malabo declaration, highlight that a structural transformation of African agriculture is central to growth and poverty eradication on the continent. Consistent with these goals, agriculture and industrialization are at the heart of the work by the African Development Bank (AfDB), the United Nations Economic Commission for Africa (ECA) and the Nations Development Programme (UNDP) and their vision and long-term strategy for a prospered and inclusive Africa.

Global experiences suggest that the attainment of food security requires high and sustained growth, underpinned by enhanced agriculture productivity and a sustainable structural change that includes the broader engagement of people. In particular, African countries need to revisit their agricultural policies and practices, while paving the way for an agro-allied industrial development. The AEC will bring together policy-makers, researchers and development practitioners from Africa and from around the world to make strategic contributions for accelerating agro-allied industrial development. The Conference will provide an opportunity to assess the impact of current growth strategies in Africa; focusing on the agricultural and industrial sector. In addition, the conference will discuss successes, lessons learned and identify remaining gaps, challenges and emerging issues on the topic. It will encompass in-depth presentations of policyoriented research by both established academics and emerging researchers from the continent and beyond who will debate and recommend policy options on how to accelerate Africa’s agricultural and industrial transformation.

Challenges and opportunities of the theme

Despite the overall macroeconomic growth and improved governance enjoyed broadly across the continent, Africa still has the highest rates of both poverty and hunger in the world. Out of about 795 million people suffering from chronic undernourishment globally, 230 million live in Africa; resulting in the highest prevalence of undernourishment worldwide, at around 20%. Even in abundant regions, food shortages can happen according to the period of the year, mostly due to poor conservation techniques or post-harvest losses. In Sub-Saharan Africa, up to 150 kgs of food produced per person is lost every year; and depending on the crop, between 15% and 35% of food may be lost before it even leaves the field.

How can Africa feed Africa, and the rest of the world? A partial response appears straightforward: Africa needs to increase food production away from subsistence production and weak productivity. There is little justification that Africa, which has about 2/3 of all the arable land left in the world, is unable to feed herself; spending around US$35 billion per year on food imports, putting additional strain on scarce foreign exchange reserves. In addition to increasing food supplies, Africa needs to better manage and integrate the entire food chain from the farm to storage, transport, processing and marketing. In the current policy and research environment, there is significant momentum behind developing and promoting the agricultural sector as a catalyst to industrialization. Developing an industrial agri-businesses would raise productivity in the sector and ultimately support economic growth and structural transformation by enabling the labor force to move from the agriculture sector into manufacturing and services.

A comprehensive transformation of the agriculture sector in Africa towards agro-allied industrialization requires investments in technology and innovation in order to improve the productivity of land and especially labor (e.g. new tools, improved seed, water control, fertilizers) including innovation in the commercialization of agriculture products. Farmers should be given incentives to adopt new technologies by making them affordable, to raise their productivity and expand their output. Land reforms would not only increase production scale but also enhance security of tenure and thus encourage investment, as well as adequate insurance and financial instruments suited to the agricultural production cycle that would support the adoption of technological innovations and expand the use of intermediate inputs, agricultural extension services, and appropriate pricing mechanisms.

More globally, structural transformation requires that industry be leveraged in the agriculture sector. Further efforts are necessary to encourage the development of large commercial farmers and to connect them with small-scale farmers through mutually beneficial contract farming (out-grower schemes) such as to support larger agriculture production in an inclusive way. Agribusiness initiatives will constantly seek value addition to agriculture products to be better connected with regional and global agriculture value chains. To enter into contract with agribusiness farmers and get the guarantee to supply leading firms, smaller-scale farmers will also get the incentives to meet required production standards within the value chain. Ultimately, an agro-allied industrialization will enhance the efficiency and value addition in the agriculture sector by connecting farmers to markets. In the form of skills and capital to produce in larger quantity while meeting higher quality standards, it will facilitate commercialization of Africa’s agriculture through more effective integration in agriculture value chains.

Providing adequate institutional and business environment as well as supporting trade finance are also key in encouraging private sector participation and investment in the agro-business industry and raising the comparative advantage of exporters in this sector. Ultimately, agro-allied industrialization is expected to reduce the export of raw material and diversify national economies in Africa. Developing competitive trade services through the provision of infrastructure and financing will support large-scale farmers in their marketing and export activities.

Developing an agro-allied industrialization in Africa requires to advance an inclusive growth agenda given that half of the labor force in the continent works in the agriculture sector in rural areas, of which 80 percent are smallholder farmers and a significant share are female workers. Land reform, better tailored and more accessible financing and insurance schemes are necessary for small-scale farmers not only to raise productivity but also to provide the most vulnerable with mitigation measures and enhance their resilience to the growing risks related to climate, market and political shocks. Land access based on customary rights, in particular, disadvantage women and favor unequal distribution of the arable land. There remains significant research and policy gaps regarding the pathways that would lead to such transformations with the view to alleviate high poverty rates in rural spaces, smooth transitory income, and enable food insecure households to meet their food and nutritional needs as well as link smallholder farmers to larger agro-business firms. It is also important to recognize the key role played by women through gender-specific policies as a core strategy. In this regard, adequate policies are needed to overcome multiple market failures and imperfections and to improve an inclusive access to modern inputs, labor, land, finance, and other agricultural factors of production and markets in order to enable a dual structural transformation of agriculture and industry.

Last but not least, Africa must endorse a green agriculture to industrialize in a sustainable way, in order to avoid long run stagnation in crop production and rising cost of inputs. Governments need to establish a sound regulatory and institutional framework to take advantage of technology in promoting a green agriculture. Information and communication technology, for instance, increasingly support in a green and sustainable way the diffusion of market information, production knowledge and geographical information among the various stakeholders in the agriculture sector. Developing skills in biotechnology would also improve yields and make them more resistant to weather shocks while ensuring health and environmental safety. Besides to larger scale agriculture production, further efforts should be devoted to the improvement of water management in such a way as to intensify irrigation to reduce Africa’s dependence on rain-fed agriculture while strengthening resilience to climate change.

Download

![]()

Feed Africa: Strategy for agricultural transformation in Africa 2016-2025 (7.93 MB)

Related News

Business investment forum calls for action to improve intra-Africa trade

Delegates at the three-day African Business and Investments Forum held over the weekend in the Algerian capital, Algiers, have once again urged business and political leaders in Africa to remove barriers that limit countries across the continent from trading with each other.

Described by organisers as the first of its kind in the country and elegantly called the ‘Algiers Rendezvous’, the meeting attracted about 1000 participants from more than 40 African countries.

Its discussions have focused on how to stimulate and promote intra-African trade and partnerships, good governance for pro-growth public-private partnerships, and promoting continental integration through joint infrastructure projects and human capital development.

But with current global economic fortunes dwindling, the delegates have called for more intra-Africa trade and more African solidarity to unleash the continent’s economic potential and prosperity.

Ali Haddad, president of the Algerian CEOs’ forum which co-organised the summit with the Algerian government, said that the current turn of events in the global world should inspire Africans to work more collectively for their development and self-reliance.

“Against the backdrop of current geostrategic upheavals, the need for exchanging with our closer friends is overwhelming. Each one of our nations chooses its path depending on its experiences but we are convinced that no state in Africa can alone address the looming future challenges on its own,” he said at the launch of the forum on Saturday.

Describing the current political changes in Europe and America where nationalist sentiments are growing, with the United Kingdom having voted to leave the European Union, Haddad called for more solidarity in Africa to end food insecurity and heavy reliance on imported manufactured goods.

“We are bound to unify ourselves for the good of our continent and people,” he said, urging African leaders to embrace Pan-Africanism ideals of solidarity and warning them that mobilisation of foreign development aid is likely to be more and more difficult in the future.

With the share of formal intra-continental trade in Africa measured at around 10 per cent of the continent’s global trade today, delegates at the meeting pushed for a better rate and urged African governments to create a better environment to ease internal trade across the continent, starting with a functional transport infrastructure.

“It took me about 20 hours to come to Algeria. We need to be better connected in order to work together,” said Amina Mohamed Jibril, Kenya’s Cabinet Secretary for Foreign Affairs.

At 10 per cent, the rate of trade between African countries is considered very low if compared with over 80 per cent for inter-European trade and 60 per cent in Asia.

While experts speaking at the ‘Algiers Rendezvous’ over the weekend urged African governments to create a good environment for intra-Africa trade, they also called upon African entrepreneurs to be more creative and move into industrialisation and big cash investments.

“Yogurt is imported at 83 per cent in Africa. What is complicated in making yogurt?” wondered former Executive Secretary of the United Nations Economic Commission for Africa, Dr Carlos Lopes, essentially challenging his fellow Africans to explore the economic benefits of manufacturing.

He also accused African financial institutions of being “lazy”, saying that they aren’t doing enough to support small businesses while they sit on an $80-billion capital that remains non-invested and sits idle in the banks’ coffers as they fear to invest it on the continent.

“It’s a paradox that people outside Africa see it as an investment opportunity but Africa-based operators keep talking about perceived risks for investments,” he said.

The meeting, which kicked off on Saturday and ends today (Monday), was organised by the Government of Algeria and the country’s business leaders with partners that include the African Development Bank (AfDB) and the Arab Bank for Economic Development in Africa (BADEA).

Related News

Ministers commit to integrate biodiversity into key economic sectors in order to achieve global biodiversity targets

Ministers from around the world committed to working together to save biodiversity and take urgent action to achieve the Aichi Biodiversity Targets, and backed this with a host of specific commitments.

In the “Cancun Declaration,” agreed on 3 December 2016 as part of the UN Biodiversity Conference, ministers dealing with environment, agriculture, forestry, fisheries and tourism, declared that they would make the additional efforts needed to ensure the effective implementation of the Convention on Biological Diversity and its Cartagena and Nagoya Protocols, including the Strategic Plan for Biodiversity 2011-2020 and its Aichi Biodiversity Targets.

Braulio Ferreira de Souza Dias, Executive Secretary of the Convention on Biological Diversity, said “The Cancun Declaration, and the powerful commitments made here at the High Level Segment send a strong signal that countries are ready to increase efforts to achieve the Aichi Targets. I look forward to this momentum carrying through the next two weeks, and then the coming years of the United Nations Decade on Biodiversity.”

H.E. Rafael Pacchiano Alamán, Secretary of Environment and Natural Resources of Mexico, said “I thank all the participating countries for showing political will and achieving this Ministerial Declaration that ensures your commitment to the mainstreaming of the conservation and sustainable use of biodiversity for well-being.”

“I’m optimistic because in the Ministerial Declaration we are all committing to raise the level of our ambition to ensure mainstreaming. The best investment that we can make for the well-being of our people is stopping the loss of biodiversity.”

UN Environment Executive Director Erik Solheim said, “UN Environment welcomes the Cancun Declaration as a timely and absolutely critical commitment to meeting the Aichi Biodiversity Targets. For the first time, through the efforts of all parties, we are really speaking meaningfully to one another about the real value of biodiversity to tourism, to agriculture, to forestry, to fisheries – to the very lifeblood of our economies.”

“We call on countries to use the momentum of this declaration to lay out in practical steps over these next two weeks how they will meet the Aichi Biodiversity Targets. Biodiversity makes business sense. Biodiversity makes common sense. It’s the food we eat, the water we drink, and the air we breathe. Let’s follow this declaration with action.”

Naoko Ishii, CEO of the Global Environment Facility, said “The continued loss of biodiversity is part of a broader pattern of unsustainable pressure on our global commons such as the climate, forests, water, land and oceans. We have reached a dangerous point, and we now need a fundamental transformation in our key economic systems if we are to avoid devastating consequences in the future.”

“We need to continue our efforts to strengthen biodiversity mainstreaming, and the Cancun Declaration on Mainstreaming Biodiversity can serve as an important guidepost in that regard” she said.

Agriculture

Participants recognised the importance of mainstreaming and enhanced policy coherence for environmental protection as well as for the vitality and profitability of agricultural sectors. The 2030 Agenda for Sustainable Development, through its integrated nature, was seen to be a major driver of the transformation needed to make agriculture more sustainable and to achieve the Aichi Biodiversity Targets.

Tourism

Delegates discussed the importance of reducing adverse impacts of tourism development on ecosystems and local communities while also leveraging the capacity of tourism to be a unique tool for financing conservation, and for raising awareness and educating travellers on the value of nature and culture.

Fisheries

Fisheries discussions looked at ways that legislation and policies could resolve issues of overfishing in small-scale and large scale fisheries, and emphasised the important role of regional fisheries organizations in coordinating responses. Ensuring sustainable fisheries and aquaculture is possible through commitment to work together, and with various stakeholders, including industry, consumers, retailers and trade, academia, and various other civil society groups.

Forestry

Effective mainstreaming of biodiversity into the forestry sector will need continued strengthening of technical capacities, and enhanced partnerships among stakeholders. The need for new and additional resources for sustainable forest financing was also noted, as well as the role of international cooperation. Several participants expressed support for the collaborative work between CBD and other organizations and agencies. Some noted the role of organizations in raising awareness of mainstreaming approaches and drew attention to reports on forest genetic diversity.

This declaration will be forwarded to the United Nations General Assembly, the High-level Political Forum on Sustainable Development 2017 and the Third United Nations Environmental Assembly.

The Cancun Declaration was supported by strong commitments from countries representing all United Nations regions, and a variety of Aichi Biodiversity Targets, including:

-

Presented by Guatemala, a commitment by the Like Minded Mega-Diverse Countries, which harbour over one third of all terrestrial biodiversity, to carry out over 200 priority actions to support actions that will enhance implementation of Aichi Target 11.

-

France and other participants in the International Coral Reef Initiative agreed to a variety of targets and actions to in support of Aichi Target 10 to protect coral reefs and their ecosystems, including actions to reduce pollution from plastic microbeads and sunscreen, actions to harmonize monitoring and other long-term management activities and actions which encourage financing for projects and initiatives which help protect and restore coral reefs, mangroves and sea grasses.

-

Netherlands and 11 other European Countries, inspired by the IPBES report on pollinators, announced the creation of a “coalition of the willing” to protect pollinators, contributing to Aichi Targets 7 and 14.

-

For Target 9, Brazil committed that at least three invasive alien species will be brought under control and an early warning system will be designed by 2020. Brazil also committed that 100% of threatened species will be under conservation tools by 2020, and 10% of them shall have their conservation status improved by the same date, contributing to Aichi Target 12.

-

Germany announced support for Aichi Target 20 with the continuation of funding for climate change mitigation and adaptation projects through its International Climate Initiative (IKI) for 500 million euros per year.

-

Japan will continue its support to capacity-building activities in developing countries through to the end of the Decade with a multimillion dollar commitment through to 2020 and will mobilise individuals to take action to support achievement of all the Aichi Targets.

-

New Zealand committed to bring together a broad coalition of actors from all levels to develop new initiatives, methodologies and techniques to increase the effectiveness control of invasive alien species in support of Aichi Target 9.

-

In support of Aichi Target 16 on the Nagoya Protocol for Access and Benefit Sharing, South Africa will develop and implement species management plans for high value plant species through its BioPANZA programme and will set milestones for the cultivation of indigenous biological resources and community participation in product development.

-

Peru, Mexico, Ecuador and Guatemala, together with FAO, the Darwin Initiative and Biodiversity, in support of implementation of Aichi Biodiversity Target 13. The initiative is entitled “Towards the Implementation of Aichi Target 13 in centers of origin Coalition For food and agriculture countries”. It encourages countries to take action to preserve genetic diversity and safeguard both native varieties of crops and their wild relatives. The commitment proposes a roadmap of collaborative engagement and action to be implemented before 2020.

The High Level Segment closed yesterday. The UN Biodiversity conference continued on 4 December 2016, with the opening of the Conference of the Parties to the Convention on Biological Diversity and the Meetings of the Parties to the Cartagena and Nagoya Protocols. The conference continues until 17 December 2016.

The Convention on Biological Diversity (CBD)

Opened for signature at the Earth Summit in Rio de Janeiro in 1992, and entering into force in December 1993, the Convention on Biological Diversity is an international treaty for the conservation of biodiversity, the sustainable use of the components of biodiversity and the equitable sharing of the benefits derived from the use of genetic resources. With 196 Parties so far, the Convention has near universal participation among countries. The Convention seeks to address all threats to biodiversity and ecosystem services, including threats from climate change, through scientific assessments, the development of tools, incentives and processes, the transfer of technologies and good practices and the full and active involvement of relevant stakeholders including indigenous and local communities, youth, NGOs, women and the business community.

The Cartagena Protocol on Biosafety and the Nagoya Protocol on Access and Benefit Sharing are supplementary agreements to the Convention. The Cartagena Protocol, which entered into force on 11 September 2003, seeks to protect biological diversity from the potential risks posed by living modified organisms resulting from modern biotechnology. To date, 170 Parties have ratified the Cartagena Protocol. The Nagoya Protocol aims at sharing the benefits arising from the utilization of genetic resources in a fair and equitable way, including by appropriate access to genetic resources and by appropriate transfer of relevant technologies. It entered into force on 12 October 2014 and to date has been ratified by 90 Parties.

Related News

Zambian President Lungu dates South Africa

President Edgar Lungu is this week expected in South Africa for a three-day State visit at the invitation of his South African counterpart Jacob Zuma.

The two heads of State will hold a series of bilateral meetings aimed at strengthening cooperation between countries.

Zambian High Commissioner to South Africa, Emmanuel Mwamba, who announced the occasion, said Mr Lungu, is expected in that country on Wednesday.

The President would be accompanied by Foreign Affairs Minister Harry Kalaba, Energy Minister David Mabumba, Tourism and Arts Minister Charles Banda and Commerce, Trade and Industry Permanent Secretary Kayula Siame, among other Government officials.

“On Thursday, President Lungu will hold meetings with President Zuma in Pretoria, during which important decisions are expected to be made by the two leaders.

“President Lungu and President Zuma will also address a gathering of Zambian and South African captains of industry, business entities and executives organised under the auspices of the Zambia-South Africa Business Forum (ZSABF),” Mr Mwamba said.

This is according to a statement issued in Lusaka yesterday by Press Secretary at Zambia’s High Commission in South Africa, Nicky Shabolyo.

Mr Mwamba said Mr Lungu’s visit will be preceded by the signing of a Joint Commission for Cooperation (JCC) between the two countries, through which issues of common interest and concern will be addressed.

He said the session of the JCC would be held in Pretoria today and tomorrow, after which a ministerial session would follow on Wednesday.

Mr Mwamba said additional cooperation agreements in agriculture, tourism, infrastructure, trade and energy between the two countries were also earmarked for assent.

“Mr Kalaba and South African Minister for International Relations, Maite Nkoana-Mashabane, will sign the memorandum of understanding of the JCC on behalf of their countries.

“Ms Siame will lead the senior official delegation from Zambia to the JCC session that will consider areas of cooperation under political and diplomatic, economic, social, security and defence segments,” he said.

Mr Mwamba said President Lungu will, on Friday visit an energy project as part of the quest to find solutions to the power deficit that has befallen Zambia.

He said Mr Lungu would also meet Zambians living in South Africa and visit Freedom Park in Pretoria, where he will lay a wreath.

Freedom Park is the memorial site for the people killed in the first and second wars and the apartheid era.

Meanwhile, Patriotic Front Kasama Central Member of Parliament Kelvin Sampa has urged lawmakers to revisit the Law Association of Zambia (LAZ) Act and ascertain if the organisation is still functioning within its original mandate.

Mr Sampa alleged that LAZ has veered away from its mandate of providing guidance to the nation on legal matters owing to its current style of operating like a Non-Governmental Organisation (NGO).

He alleged that the association is peddling the agenda of the opposition United Party for National Development (UPND), a situation which had compromised its relevance in the country.

“I am calling on our seasoned lawyers in this country to stand up and salvage the image and the crucial role of LAZ which is on the verge of being compromised under the current leadership.

“Society looks up to LAZ to provide unbiased and non-politically inclined guidance and should demand that the original LAZ is brought back,” Mr Sampa said in Lusaka yesterday.

He said it was important to interrogate whether or not LAZ was designed to serve as a political pressure group, hence his interest in consulting the parliamentary statute that enshrines its existence.

Mr Sampa also warned UPND president Hakainde Hichilema and his vice Geoffrey Mwamba to desist from taking politics to places such as markets because such maneuvers were detrimental to effective service delivery.

Related News

Madagascar Economic Update: Agriculture and rural development

This edition of the Madagascar Economic Update is part of a series of short economic updates produced by the World Bank on a biannual basis. The first part of this brief has the World Bank’s assessment of recent economic developments and the outlook over the short to medium term. The second part of this update focuses on Agriculture and Rural Development.

Part One: Recent Economic Developments

International and Regional Developments

The global economy is evolving in a context of low commodity prices, weak global trade and reduced capital flows. The 2016 global growth forecast has been revised downward to 2.4 percent against an initial forecast of 2.9 percent at the beginning of the year. This revised outlook is driven by weaker demand in the more advanced economies, where sluggish growth in China in particular has impacted global trade and the demand for commodities.

These global conditions, combined with political uncertainty and drought in certain parts of the region are affecting economic activity in sub-Saharan Africa. Overall, the growth forecast for the continent has been reduced to 1.6 percent, the lowest level in 20 years. The growth trajectory diverges significantly between countries. Major exporters of natural resource commodities such as Nigeria, Angola and Chad have been most affected, while economic activity in importing countries such as Mauritius, Rwanda and Kenya has remained strong.

The Malagasy economy may be subject to changing demand from trading partners and commodity price volatility. Madagascar’s largest trading partner is France, although trade levels have been declining. Other important trading partners include the United States, China and European Union countries such as the Netherlands and Germany. Lower commodity prices have presented mixed fortunes for Madagascar. On the one hand, as a net fuel importer lower oil prices have benefitted the economy. On the other hand, lower nickel prices have affected production and export values. These trends highlight the importance of Madagascar continuing with reforms and policies to promote competitiveness, while also improving sources of internal growth through enhancing productivity in key sectors such as agriculture.

External Sector

In 2016 the current account balance continued to improve. Foreign direct investment (FDI) flows have contributed to an improvement in the current account balance. Foreign currency reserves have increased the months of import cover from 2.9 months in 2015 to an estimated 3.3 months in 2016. Following the completion of investments for the two major mining operations in 2011, FDI flows related to the extractive industries have declined. The most recent data available suggests that FDI is increasingly oriented toward financial sectors, telecommunications and manufacturing activities.

Broader changes in the economy have improved the current account balance. The completion of the investment phase of mining operations in 2011 moderated capital intensive imports. The effects of lower commodity prices for imports such as petroleum products and rice, and the intensification of exports from the mining sector since 2013 has further strengthened the current account balance.

Non-mining exports performed well in 2016. Exports recorded between January and October 2016 are estimated at US $ 1,687 million, a 17 percent increase compared with the same period last year. However, the fall in nickel prices since 2015 and declining production volumes has adversely affected exports. In the first ten months of 2016 Madagascar exported US$ 410 million worth of mining products, a decline of 10 percent compared to the same period the year before. The value of non-mining exports increased by 22.3 percent in 2016, largely driven by higher revenues from vanilla and cloves. Exports from free zone companies also increased from US$ 434 million in 2015 to US$ 546 million in 2016, mainly resulting from textiles and shrimps exports to the Euro zone area. Under the Africa Growth and Opportunities Act the value of Madagascar’s exports is estimated to have tripled in 2016.

The cost of imports has been moderated as global petroleum prices remain favorable. Imports in 2016 are estimated at US$ 2,337.7 million. The main components of these imports are raw materials with a large proportion destined for free zone enterprises, petroleum products and foodstuffs, where the latter cost more in 2016. However, crude oil prices are forecasted to rise in 2017 from US$ 53 per barrel to US$ 55 per barrel, which will affect the cost of imports and subsidy provision to JIRAMA.