Search News Results

Blockchain will become ‘beating heart’ of the global financial system

Blockchain will fundamentally alter the way financial institutions do business around the world, according to a new World Economic Forum report, The future of financial infrastructure. However, the effects will be hidden, coming from new processes and architecture based on blockchain rather than radical fintech innovation or new currencies such as bitcoin.

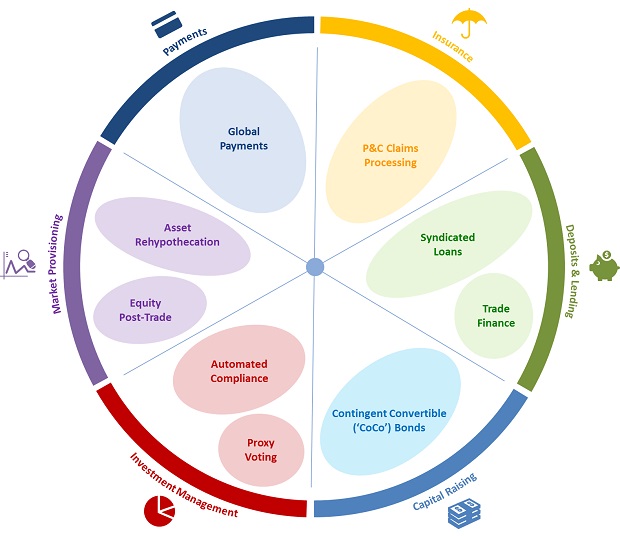

The report focused on nine individual uses of blockchain across six separate activities in financial services – insurance, payments, market provisioning, investment management, capital raising, and depositing and lending – to build a picture of how processes in each could be transformed by the technology. It also considers how other emerging technologies in the industry, such as biometrics, cloud computing, cognitive computing, machine learning, quantum computing and robotics, will combine with blockchain to drive further transformation.

Use cases

Some of the processes the report found would be replaced by blockchain include bread-and-butter activities of financial institutions, such as:

-

International payments and wire transfers, which currently involve a lot of manual steps and fees ciated

-

Rehypothecation, or the repackaging of mortgages, which caused the last global financial crisis ciated

-

Compliance reporting of banks to regulators, currently a long and ineffective process.

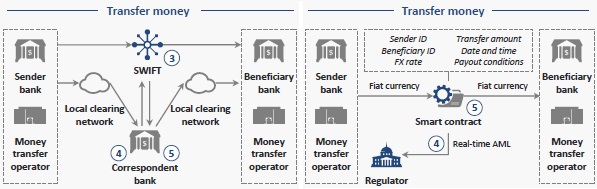

With blockchain promising to simplify back-end banking processes, making them cheaper, securer and more accessible, one area where it could have a profound impact is in creating an inter-bank, blockchain-based fiat currency to streamline the arduous process for transferring money, as illustrated below. Such process innovation would cause blockchain technology to enter the finance bloodstream.

Transfer money process, current (left) and future (right) state

“Rather than stay at the margins of the finance industry, blockchain will become the beating heart of it,” said Giancarlo Bruno, Head of Financial Services Industries, World Economic Forum. “It will help build innovative solutions across the industry, becoming ever more integrated into the structure of financial services, as mainframes, messaging services and electronic trading did before it.”

Blockchain could thus redraw the structure of financial institutions and the back-end of services as we know them today. Blockchain could allow consumers to pay less for all kinds of financial activity, from international payments to the trading of stocks and bonds. It could also give regulators new capabilities, allowing them to stop regulatory violations before they start and to watch more effectively for warning signs of financial crises.

However, Bob Contri, Global Financial Services Industry leader, Deloitte Global, and a co-sponsor of the report, said competing financial institutions will need to come together to achieve these results. “Before full adoption is possible, there are factors that need to be addressed, including an uncertain regulatory environment, lack of standardization efforts and the need for a formal legal framework,” he said.

Similar to any technological innovation, blockchain comes with a set of risks that must be considered, the report also notes. These include errors in the design, malicious autonomous behaviour as a consequence of human decisions, and potential gaps in security across all inputs and outputs. Challenges such as these must be overcome if the economic and social benefits of blockchain are to be realized.

“While there is no doubting the transformative potential of blockchain technology, it is not a blanket cure for inefficiency in financial services. At this stage of evolution, the critical task is knowing where to focus your efforts. Blockchain will have the greatest impact when applied to business problems involving a shared repository of information, multiple writers, minimal trust, the presence of intermediaries and interdependencies between transactions. Without these conditions, blockchain may not be the answer,” said Rob Galaski, Partner, Deloitte.

“The financial services infrastructure will be radically changed by blockchain technology. It will redraw processes and call into question policies that are the groundwork of today’s business models,” said Jesse McWaters, Project Lead, Disruptive Innovation in Financial Services, World Economic Forum. “Our research looks to the future state of blockchain technology and by starting this conversation we believe this will help further build perspective for what is to come.”

The report is the most recent phase of the Forum’s ongoing Disruptive Innovation in Financial Services project. It draws on over 12 months of research, engaging 200-plus industry leaders and subject matter experts through interviews and multistakeholder workshops.

Related News

EAC Assembly passes key report on Poaching, urges governments to reform laws, get though on those plundering wildlife resources

The East African Legislative Assembly resumed its session in Arusha, Tanzania on 23 August 2016, where it debated and passed a critical report on poaching in the region. The Assembly in essence, urged EAC Partner States to reform wildlife laws and to put in place initiatives that promote upkeep of communities that neighbor the wildlife conservancy areas.

The Oversight report on poaching presented to the House by the Chair of the Agriculture, Tourism and Natural Resources Committee, Hon Christophe Bazivamo, further urges Partner States to develop/improve wildlife conservation strategies and protection measures through patrols, joint cross border operations, surveillance and information sharing.

With it, the Assembly says Partner States should and can provide part of the revenue collected from wildlife tourism to the communities living around the National Parks to promote conservation.

The report emanates from a workshop on poaching and fisheries held in Mwanza, Tanzania and in Nairobi, Kenya in August 2014. Its objective was to sensitize Parliamentarians on the escalating problem of poaching and illegal wildlife trafficking in EAC region and to solicit their views on strategies and measures that could be adopted in addressing the problem. The workshop further sought to consider existing international and regional policies, strategies and regulatory framework/instruments on wildlife management on the one side as well as the current and proposed national and regional initiatives toward strengthening wildlife conservation on the other hand.

The report was a follow-up on the Resolution moved in the House by Hon. Ogle Abubakar on “Escalating problem on Poaching and Illegal Wildlife trafficking in EAC” in August 2013 in Arusha.

The Committee was only able to visit the Serengeti National Park and the Mwaloni Kirumba fish market in Mwanza, Tanzania as well as the Nairobi National Park. The Serengeti National Park is dubbed as one of the park’s with the greatest concentration of game in the region and famed for over two million wildebeest, half a million Thomson’s gazelles and a quarter of a million, zebras. The Committee observed that mining settlements are interfering with the migration path of some animals and mechanized agriculture has taken over where wildebeests would historically breed their calves.

This has caused a loss of habitat for many species in the Serengeti. At the same time, Hon Bazivamo informed the House that non-authorized people enter into Serengeti National Park for various reasons. Such include poaching, hunting, cutting trees/firewood, grazing, fishing, cultivation and mining. Persons also traverse the parks collecting grass, medicine, honey, water and seeking refuge.

In Kenya, the Assembly was informed that proliferation of small arms and light weapons created an avenue for wildlife poaching. Other documented challenges include inadequate man power (rangers), skills, equipment and transport as well as human settlement around key rhino and elephants’ areas.

The Report also highlights findings of the fishing sector following a visit to the Mwaloni-Kirumba fish market in Mwanza as well as a presentation by experts on fisheries on the Lake Victoria. It states in part that the increasing number of fishermen to 1.5% between 2012 to 2014 means the sector is in danger of collapse in the future.

“Usually, any natural water points (such as lakes, rivers) have a maximum number of fishing effort it can accommodate so that the fisheries become sustainable, above which the fisheries become depleted, unsustainable and will eventually collapse,” a section of the report says.

The report also informs the House of decrease of the use of long-line hooks as well as the use of prohibited illegal gillnet as challenges despite its decrease in usage by 7.2%.

During debate on Tuesday, Hon Martin Ngoga said Police in Rwanda recently intercepted ivory cargo transiting through the country and said further deficiencies in legislation on matters of poaching need to be effectively handled.

“We have to look into the shortcomings on legislations with a view to coming up with regional piece of legislation or strengthening those of Partner States,” the legislator said.

Hon Ngoga remarked that there was abundance of political will in resolving the poaching impasse but said such capacities need to be strengthened. Hon Taslima Twaha said the water hyacinth continued to be a challenge in Tanzania saying it was depriving fish of existence.

“The technology that was used in the Republic of Kenya in Kisumu could be shared in Mwanza to address the problem,” Hon Twaha said. He said fish and specifically the nile perch was good for health of all citizens and that it was vital for the demands of the region to be fully met before any exports. Hon AbuBakr Ogle said the Middle East and specifically China was a big beneficiary of poaching menace and it was necessary for the Government and the EAC to partner together to end the vice.

Hon Shyrose Bhanji said the fish market provided labour opportunities for those in the fishing business. She remarked that the Serengeti national park which straddles Arusha, Manyara and Mwanza which had a rich ecosystem for a number of years was now deprived and pegged at 30%. “The Park needs to be preserved and mining activities should be suspended and stiff penalties meted to poachers. Our governments must come together to fight the malpractices,” she said.

Hon Isabelle Ndahayo said corruption was a key ingredient of poaching and the region needs to stem the vice. “We have debated the matters over and over again, passed a number of resolutions. The conservation areas are shared and a joint strategy is necessary. The Council of Ministers must deal with the matter squarely,” Hon Ndahayo said.

Hon Nusura Tiperu said the adoption of the report was a key indication that the Assembly is passionate about ending poaching. “Governments must be tough and act to save those working to deplete numbers. Animals have no borders and laws that are defined within national borders may not suffice. Instead a regional mechanism is key,” Hon Tiperu said.

Hon Maryam Ussi, Hon Pierre Celestin Rwigema, Hon Dr Odette Nyiramilimo, Hon Patricia Hajabakiga also supported the report.

Third Deputy Prime Minister and Minister for EAC, Republic of Uganda, Rt Hon Kirunda Kivejinja said a regional mechanism was necessary to contain poaching. Kenya, United Republic of Tanzania and Uganda are beneficiaries of the Ivory Fund whose contributors include; Netherlands, Germany, China, UK, France Belgium and South Africa. Kenya and Tanzania have been identified to be among the eight countries of concern with respect to increased illegal trade in elephant ivory and directed by the Convention on International Trade on Endangered Species (CITES) Parties through the Standing Committee to put in place actions aimed at reducing the illegal trade.

» Download: Report of the Committee on Agriculture,Tourism and Natural Resources on the Oversight Activities on Poaching, 2 June 2016 (PDF, 8.69 MB)

Related News

tralac’s Daily News Selection

The selection: Tuesday, 23 August 2016

SADC Secretariat records E160m operating surplus (Swazi Observer)

The Southern African Development Community Secretariat has recorded a healthy operating surplus of $11.8m (approximately E160m), for the 2015/2016 financial year. The good news was revealed by the SADC Director for Budget and Finance Clement Kanyama yesterday. Kanyama said the recorded surplus showed an increase from 2014/2015 financial year, as the SADC Secretariat recorded E139m ($10.3m). Kanyama said 2015/2016 revenue was $78.6m made up of $51.6m from Member States and $27m from grants, which were recognised as contributions based on the SADC Secretariat compliance with condition, as specified in each financing agreement. “The total expenditure was $66.8m and total assets under the control of SADC Secretariat of $101.1m,” he said.

Southern African Business Forum seeks projects to spur socio-economic growth (Swazi Observer)

SADC Lawyers’ Conference: full text of the speech by Jeff Radebe (pdf), Minister in The Presidency for Planning, Monitoring and Evaluation

Has SA’s foreign policy smoothed the way for companies in Africa?: commentary by George Rautenbach (Business Day)

AU’s Kigali summit decision on the Continental Free Trade Area (AU)

The Heads of State and Government decided to establish a High Level Panel of five eminent persons (one from each region) to champion the fast tracking of the Continental Free Trade Area (CFTA), ahead of its proposed launch in 2017. They also called on Member States to speak with one voice on all issues related to trade negotiations with third parties.

Rwanda has formally rejoined ECCAS: two updates

Rwanda back to Central Africa bloc, 10 years on (The EastAfrican): Rwanda has formally rejoined the Economic Community of Central African States (ECCAS), after Foreign Affairs Minister Louise Mushikiwabo presented the instruments of ratification to the economic bloc on August 17. The return repositions the country to benefit economically, politically and diplomatically in the Central African region. Rwanda, which had been a member of ECCAS since 1981, was readmitted into the bloc last year, almost 10 years after leaving. When it left, it cited the need to focus on its membership in the East African Community and the Common Market for Eastern and Southern Africa.

Rwanda eyes big opportunities from central African bloc (Global Times): Francois Kanimba, Rwanda minister of trade and industry said that Rwanda will reap big from various regional economic groupings. "Our country joining ECCAS is a big opportunity for Rwandan traders to sell their goods and services on a bigger platform across the continent. Local producers will benefit from increased market size which is an important factor facilitating innovation and competition," he added. Kanimba stated that Rwanda has gained a lot from being a member of multiple regional blocs since each bloc has comparative advantages to the other, ultimately strengthening the country's economic institutions.

South Africa: trade and industrial policy outcomes from Cabinet Lekgotla (GCIS)

Cabinet took strategic decisions to secure higher impact implementation of the Industrial Policy Action Plan including: (i) That the Department of Public Enterprises and National Treasury will consolidate procurement for locomotives into a single institution (Transnet) to ensure efficiency and compliance with the localisation requirements; (ii) Finalising the evaluation of financial incentives for business to strengthen conditionalities and achieve greater value for money to enhance more inclusive growth; (iii) A trade statistics architecture developed by the South African Reserve Bank, National Treasury, SARS and Stats SA will identify and hold illicit financial flows; (iv) Introducing legislative amendments to implement the 30% set asides (a new Procurement Bill developed by National Treasury) by March 2017 and unlock the potential of SMME’s, cooperatives and the township and rural enterprises. (v) Implementing the new Preferential Procurement Regulations by end August 2016 as an interim measure to this radical intervention.

Government will continue to focus on labour-intensive sectors, including the need for various mechanisms to support greater impact on jobs, such as the use of our incentive programmes, amongst others: clothing, textiles, leather and footwear value-chain; agro-processing and business process services. The successful Oceans Economy intervention will scale up projects to expand coastal and marine tourism in order to realise significant job creation.

South Africa: Minister Ebrahim Patel welcomes action against collusion and price-fixing in steel industry (GCIS)

The Minister of Economic Development, Ebrahim Patel, has welcomed the announcement of a R1,5bn fine payable by ArcelorMittal, the country's largest steel-maker, for price-fixing and collusion in the steel industry. This is the largest single fine imposed against a single company thus far by the competition authorities. The company also undertook, as part of the settlement with the authorities, to invest R4, 6 billion in new capital spending to upgrade its plants and improve its competitiveness. The settlement further provides for a pricing mechanism that will cap the company's margin on flat steel products for a period of five years. [Increase in wheat tariff slammed]

South Africa – Zimbabwe trade war: time for WTO intervention? (Tutwa Consulting)

Should Zimbabwe’s action be regarded as safeguard action, that is, provisional safeguard measures, a violation of both the WTO Agreement on Safeguards and of Articles 20 and 20 BIS of the SADC Trade Protocol is apparent. For instance, the measure imposed should only be a tariff increase pending an investigation and not a ban requiring a license which can only be issued to prevent shortages in the local market where domestic production cannot satisfy demand. Interestingly, SI 164 as well as the subsequent press statement by the Minister of Industry and Commerce do not make any reference to any enabling provisions of the SADC Trade Protocol or WTO provisions, as if Zimbabwe is not bound by its trade liberalization commitments regionally and internationally – only domestic legislation is mentioned. While the SADC Trade Protocol provides a mechanism, Annex VI, to be followed in the event of a dispute, to date no trade dispute has been considered under this system. [The analyst: Nkululeko Khumalo]

Zimbabwe: Govt seals multilateral road deal (The Herald)

Zimbabwe yesterday signed a “framework agreement,” with an Austrian construction firm Geiger International and a Chinese Company, China Harbour Engineering, setting the stage for the rehabilitation, dualisation and upgrading of the Beitbridge–Harare and Harare-Chirundu highways. “The signing of this framework is an important milestone in the negotiations that will result in the implementation of the construction of this very important road in Zimbabwe through a combination of Build Operate Transfer and loan financing models,” he said, dismissing claims that it would cost $2.1bn. “The section from Beitbridge to Harare shall be implemented as a BOT, with a concession period of 20 years, while the section from Harare to Chirundu — including the Harare ring road — will be implemented as a combination of a loan and private sector investment contributed by CHEC.”

Beitbridge redevelopment: many intentions, no action (The Herald)

95% of cargo transported in the region is by road with a delay of three days at the border increasing transport costs by about $500 per truck per day which is passed on to the importer. In other terms some unscrupulous officials have turned the port of entry and the entire town into a danger zone for travellers and transit population. Beitbridge Border Post used to be the port of choice for many travellers in the last five years, with importers or travellers in transit opting to put up in local hotels in the town, soon after getting their goods or vehicles cleared at the border. However, that has changed as a result of the mercenary attitude among border officials.

SMEs and GVCs in the G20: implications for Africa and developing countries (GEGAfrica)

The paper first reviews, in broad outline, key contours of the global debate on GVCs and what they imply for trade and investment policies. Broad implications for SMEs wishing to integrate into, and upgrade within, GVCs are also developed. The paper then relates the broad positions of key international institutions on the matter. These institutions represent large and small businesses, and international governmental agencies charged with developing policy perspectives on the issue. Broad implications for SMEs are drawn from this survey, and related to the debate previously charted. Finally, South African, and to some extent African, realities are compared with the policy perspectives emerging from the international institutions surveyed, in light of the GVC policy debate. The paper concludes with recommendations for the South African government. [The analysts: Peter Draper, Chiziwiso Pswarayi], [Emerging economies hope to get economic boost from G20 summit]

Why business operators should embrace arbitration (New Times)

Dr Fidelle Masengo, secretary general of the Kigali International Arbitration Centre, said arbitration is new in Rwanda, adding that they are going to conduct awareness drives to educate business operators on the concept. He argued that arbitration benefits all parties involved in commercial disputes, saying it is not costly in terms of money and time compared to resort to courts of law. “We are already training lawyers and business people about the benefits of this form of settling commercial conflicts so they avoid lengthy and costly court processes,” he said. He said KIAC is working with the Private Sector Federation and some specific sectors, like mining, services and banking, sensitising them on how they can use arbitration to settle disputes. He said the centre has already trained a sizeable number of professional arbitrators to handle such cases.

Rwanda: What new online portal means for agric export-import enterprises (New Times)

The new online portal will reduce the transaction and administrative time and costs associated with issuance of permits and certificates by up to 45%; the current direct transaction costs to apply for a permit or certificate is $5.67, this is expected to drop to less than $3 per transaction. Already, 150 companies and 50 individuals registered with the system following during its three-month piloting. During this period, a total number of 120 import permits and 207 phytosanitary certificates were issued. [Prices soar in Rwanda as Burundi’s ban on food exports bites]

Tanzania: State urges speed on LNG plant (Daily News)

President John Magufuli has directed the Ministry of Energy and Minerals to fast-track the construction of a liquefied natural gas plant in Lindi Region to cost $30bn (65 trillion/-). “I want to see this project taking off, there have been a lot of unnecessary delays...just accomplish whatever is creating any bureaucracy so that our investors can begin the work with immediate effect,’’ he said. The president was speaking at the State House in Dar es Salaam yesterday after receiving a progress report on the multi-trillion grand project for construction of Liquefied Natural Gas (LNG) plant at Likong’o area in Lindi Region. The report was presented by an official of the Norwegian Company, Statoil Country Representative, Mr Oystein Michelsen, who insisted that after completion of the construction of the envisaged gas plant, production would continue for a period of not less than 40 years. [Nissan earmarks Tanzania for growth in Africa]

Namibia: Team Namibia calls for public sector to procure local (The Namibian)

“Attempts to persuade the public sector to procure local have proved to be futile as imported goods are purchased, despite the availability of their locally manufactured counterparts. The public sector should be the driving vehicle and exemplary agent for ensuring that our Namibian manufacturers and service providers are their first choice of preference,” Roberta da Costa, CEO of Team Namibia, add.

The political and economic dynamics of foreign aid: a case study of US and Chinese aid to Sub-Sahara Africa (pdf, ERSA)

This study sought to answer four specific questions. First, what are the determinants of Chinese and American aid allocation decisions to SSA countries? Second, how has US aid allocation determinants changed with the arrival of China into the aid field in SSA? Third, is there any credence to assertions that China is primarily motivated by access to resource in SSA? Fourth, how significant is recipient governance in the decision of both countries aid allocation decision to SSA.[The analysts: Kafayat Amusa, Nara Monkam and Nicola Viegi]

Agreement on trade in services between India and the Association of Southeast Asian nations: report by the Secretariat (WTO)

This report, prepared for the consideration of the Agreement on Trade in Services between India and the Association of Southeast Asian Nations (ASEAN), has been drawn up by the WTO Secretariat on its own responsibility and in full consultation with the Parties. The Agreement on Trade in Services under the framework agreement on comprehensive economic cooperation between India and the Association of Southeast Asian Nations is ASEAN's 6th regional trade agreement. It is however ASEAN's 3rd Agreement covering trade in services. The Agreement is India's 14th RTA but India's 5th RTA in trade in services. In commercial services, India ranked 5th globally in terms of both global exports and imports, amounting to $156bn and $147bn, respectively. This represents 3.15% and 3.07% of world exports and imports, respectively. Among the ASEAN members, Singapore accounted for the largest share of world trade followed by Thailand and Malaysia. Among the newer ASEAN members (Cambodia, Lao PDR, Myanmar and Viet Nam) Viet Nam had the largest share of exports and imports of commercial services, while Lao PDR has the smallest share. [ASEAN in a climate of change: spotlight on sustainable energy in Malaysia, Thailand, Vietnam (Economist Corporate Network)]

World Bank facilitates water sector talks between Egypt, Sudan, Ethiopia (Daily News)

Angola: EIU forecasts economy will grow 1.3% in 2016 (Macauhub)

UN health agency’s African member States adopt new malaria framework (UN)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

How infrastructure development can turn around Africa’s fortunes

Africa has been touted as the new destination for investors. However, the continent still faces a myriad of challenges that hold back its potential, especially efforts aimed at improving business environment and alleviating poverty to ensure sustainable economic growth.

That’s why Africa needs leaders who can tackle these challenges and translate them into opportunities to achieve the ‘Africa we want’ as per the theme of the recently-concluded 27th African Union summit in Kigali.

Supportive policies and infrastructure that promote entrepreneurship and trade on the continent will play a critical role in helping the continent rise from the ‘ashes’ to achieve the African renaissance dreams proclaimed by the likes of former South African President Thabo Mbeki, experts say.

According to Teddy Kaberuka, an economic analyst in Kigali, infrastructures, including transport, power and information and communication technologies (ICTs) facilities, are instrumental in supporting growth in the global economy. That’s the reason why African countries must prioritise infrastructure development to ensure sustainable economic growth on the continent.

“The only way Africa can increase its production and strengthen its economy is by investing heavily in infrastructure development to support the production and ease access to markets and encourage intra-regional trade. Therefore, government must invest more in the energy, ICT and transport sectors because these are enablers of trade and development,” he said. “Without enough power, the continent’s production capacity will be affected, condemning the continent to rely on European imports.”

Kaberuka adds that transport and ICT sector are essential to ensure access to markets by farmers and the industrial sector.

With the majority of the continent’s enterprises falling in the category of small-and-medium enterprises (SMEs), experts call on African leaders to put in place policies and regulations that propel them further and help make them sustainable. The SME sector is the backbone of Africa’s economies, employing the majority of the continent’s youth and supporting millions of households.

However, the challenge of poor infrastructure and cumbersome border policies must be addressed for intra-country and intra-region trade to flourish. Most African countries are not trading with each other, preferring to trade with Europe and America where they face immense challenges as they largely deal in primary products.

According to AU statistics, improving the continent’s infrastructures, like roads, energy and ICTs, can add up to 2 per cent to GDP growth rate per year and also increase productivity by 40 per cent. The World Bank attributed more than half of impressive growth recorded in Africa to infrastructure development on the continent because it offered many countries the required stimulus for growth.

Christian Rwakunda, the Ministry of Infrastructure permanent secretary, said putting in place right infrastructure is key driver for socio-economic development. He says improving transport networks and access to reliable energy and ICTs will reduce the cost of operations and ensure efficient production and service delivery.

“For instance, development of an efficient regional railway transport system would cut the cost of export/import by almost half and reduce the transit significantly. This would open up new opportunities for export and increase regional trade,” he notes.

In addition, access to affordable and efficient energy for local industry is essential to grow the sector which is still almost dormant, he adds. Rwakunda says access to affordable power promotes growth of micro-industries allowing more Rwandans and Africans generally to engage in processing of raw materials into finished products and earn more revenue.

He says lack of efficient infrastructure facilities and skilled human resource has led to high costs of investment, while private investments remain low compared to the expectations of developing countries.

“As a result, development and operation costs remain high in Africa. For example, the recent development of the methane gas power project on Kivu Lake required skilled personnel do carry out research. Besides, implementation of infrastructure projects by foreign firms reduces benefits for local populations,” he says. The PS notes that such situations are mitigated by knowledge transfer programmes to benefit the host countries.

“To address these issues, Rwanda has put in place an investor-supportive investment policy as well as created an enabling environment. The government also promotes public-private partnerships, especially for key projects and export-oriented investments.”

“In addition, technical and vocational education has been given priority to bridge the skills gap in the industrial and other sectors,” he says.

He adds that the government encourages local content development at all levels, including human resources, local materials, local partnership or sub-contracting. Rwakunda says the African leaders need to address the key challenges affecting the continent’s development through regional frameworks that will help fast-track the implementation of the African Agenda. These efforts are crucial for the realisation of the ambitious continental free trade area (CFTA) initiative that seeks to promote trade with the continent, among others.

The CFTA will be made up of over one billion people, with a GDP of $3 trillion. It will also boost trade by 50 per cent among African countries by 2022. The continent’s gross domestic product (GDP) is also estimated to rise from $1.7 trillion in 2010 to $2.6 trillion by 2020, while consumer spending will grow from $860 billion to $1.4 trillion over the period.

Already, plans are underway by three regional blocs on the continent to create the largest free trade area on the globe, from the Cape to Cairo. The tripartite free trade area will bring together the East African Community, the Common Market for Eastern and Southern Africa and the Southern African Development Community into a single new zone. This is envisaged to ease barriers to trade, and stimulate $1 trillion worth of economic activity across the region of more than 600 million people.

However, there is need to support the private sector with improved infrastructure and other facilities and initiatives to enable free movement of people and goods. Easing movement of goods and people is critical in driving the trade and that why the launch of the African e-passport at the Kigali AU summit was a key milestone for the continent that could help in the realisation of this goal. This remarkable step could help drive trade on the continent and spur sustainable socio-economic development.

Some of these efforts could eventually help address most of the challenges hampering business growth across the continent, which will in the long-run contribute to the realisation of the new Africa aspirations, making the African renaissance a reality.

Related News

Summary of 27th AU Summit Decisions: tax imports to finance AU; establish Protocol to issue African passports to citizens; and CFTA

The Twenty-Seventh Ordinary Session of the Assembly of the African Union (AU) in Kigali, Rwanda, ended on an extremely high note. It was hailed by many, including the Chairperson of the AU Commission, Dr. Nkosazana Dlamini Zuma as the best Summit ever.

“This is the best Summit we’ve had, we must maintain it, while striving to get better and better.” Dr. Dlamini Zuma remarked in a tweet that has been retweeted several times. The Chairperson also expressed gratitude to the current Chairperson of the Union, President Idriss Deby Itno of Chad, host President Paul Kagame of Rwanda, Heads of State and Government, AU Commissioners, the people of Rwanda, AU Commission Staff and Service Providers for delivering a successful Summit.

The richness of the 27th AU Summit was as a result of both a streamlined programme focusing on strategic areas and their outcomes, as well as the smooth organisation by the host country and the AU Commission.

Over Thirty-five (35) Heads of State and Government personally attended the Summit, with a few others represented by Vice Presidents and Foreign Affairs Ministers. Burundi attended the Permanent Representative Committee, but was absent from both the Executive Council and the Summit.

An historic and landmark decision on financing the Union, was taken by the Heads of State and Government, who met in a retreat together with their Finance and Foreign Affairs Ministers. They had decided to convene the retreat during the 26th Summit in January 2016.

Some countries were awarded for the progress made in promoting women’s right and gender equality, according to the recently introduced Gender Scorecard. The three main categories awarded were: social, economic and political. Winners in the various categories included: in the social category were: Algeria and Tunisia; economic category was South Africa; and Rwanda topped the political category. Algeria was awarded for being the overall winner in categories pulled together, though not having featured topmost on the economic and political categories.

Following is the summary of key Decisions taken at the 27th AU Summit:

1) Extension of the current Commission’s mandate

2) Financing the Union through import Levy

3) African Union Passports to African citizenry

4) Continental Free Trade Area (CFTA)

5) Peace and Security Decisions on South Sudan, Burundi, Libya and Terrorism

6) Appointment of Judges of the African Court on Human and Peoples’ Rights

7) Theme, date and venue of next Summit

8) Declarations

1. Extension of the current Commission’s mandate

The much-anticipated elections of new members of the AU Commission took place on 18 July 2016, but none of the three candidates, running for the position of the Chairperson of the Commission, received the required two-thirds of Member States’ vote. After seven (7) rounds of voting, the last of the three candidates obtained 23 votes, with 28 Member States abstaining.

Of the fifty-four (54) Members States eligible to vote, fifty-three (53) were present and voted. Only Burundi did not vote since they were absent from the Summit.

Therefore, the Summit decided, as it had done in 2012, to extend the mandate of the current Commission leadership comprising the Chairperson, Deputy Chairperson and the eight Commissioners, until the next elections, which will take place in January 2017, at the Headquarters in Addis Ababa, Ethiopia. During this period, the process will be reopened new candidates, as well as the current contenders, to apply.

2. Financing the Union through import Levy

In an unprecedented decision, the Summit has decided to institute and implement a 0.2 percent Levy, with effect from 2017, on all eligible imported goods into the continent to finance the AU’s operational projects, programmes and peace and security operations budget.

While the specific mechanisms are being worked out, the amounts collected will automatically be paid by Member States into an account opened for the AU within the Central Bank of each Member States for transmission to the AU in accordance with the assessed contribution.

The Summit also appointed President Paul Kagame of Rwanda to lead the ongoing institutional reform of the Union (the AU Commission and the Organs) to ensure that the AU structures and modus operandi are aligned with the demands of integration and implementation of Agenda 2063, and to enable more effective and efficient use of resources and business-oriented delivery. President Paul Kagame is expected to present a report during the January 2017 AU Summit in Addis Ababa, Ethiopia.

3. African Union Passports to African citizenry

Following the launch of the African Union Passport and the overwhelming enthusiasm that greeted it, the Assembly also decided to encourage all Member States to adopt the African Passport and to work closely with the AU Commission to facilitate the processes towards its issuance at the national level, based on international and continental policy provisions.

The Commission will provide technical support to Member States to enable them to produce and issue the African Passport to their citizens. The Commission has to put in place an implementation roadmap for the development of a Protocol on the Free Movement of persons in Africa by January 2018, which should come into immediate effect in Member States, in line with the continental transformation framework, Agenda 2063.

4. Continental Free Trade Area (CFTA)

The Heads of State and Government decided to establish a High Level Panel of five eminent persons (one from each region) to champion the fast tracking of the Continental Free Trade Area (CFTA), ahead of its proposed launch in 2017. They also called on Member States to speak with one voice on all issues related to trade negotiations with third parties.

5. Peace and Security Decisions on South Sudan, Burundi, Libya and Terrorism

Following the Report of the Chairperson of the Commission on the state of peace and security in Africa, the following Decisions were taken on: i) South Sudan, ii) Burundi, iii) Libya, and iv) Terrorism.

i) South Sudan

The Assembly strongly condemns the outbreak of fighting that took place on 7 July 2016 in Juba, resulting in loss of lives and other tragic impacts on civilians, as well as the cowardly attacks against diplomatic missions; It expresses deep concern at the slow pace and recurring setbacks on the implementation of the Agreement on the Resolution of the Conflict in the Republic of South Sudan signed in August 2015, and reiterates its disappointment at the lack of its implementation.

The Assembly endorses the communique of the Summit meeting of the Heads of State and Government of the IGAD-Plus, in particular with respect to the reinforcement of UNMISS as proposed by the UN Secretary-General and the call to the UN Security Council to extend the Mission of UNMISS with a revised mandate, including the deployment of a regional protection force to separate the warring parties, protect major installations and civilian population and demilitarize Juba; looks forward to the plan Peace and Security Council visit to South Sudan and stresses the critical importance of convening a pledging conference in support of South Sudan.

ii) Burundi

The Assembly expresses deep concern over the continued targeted killings and other acts of violence in Burundi and deplores the recent assassinations. It reaffirms the determination of the AU to spare no effort to help Burundi restore and rebuild peace, security and stability, reiterating the need for a truly inclusive dialogue, involving all the Burundian stakeholders, led by the East African Community Mediator, President Yoweri Museveni of Uganda, with the Support of the Facilitator, former President Benjamin Mkapa of Tanzania.

The Assembly urges the Burundian Government to fully honour the commitment to facilitate the speedy deployment, including issuance of visa and other requirements, of the 200 AU human rights observers and military experts.

iii) Libya

The Assembly reiterates the commitment of the AU to assist the Libyan parties in finding lasting solution to the crisis facing Libya. The Assembly comments the Chairperson of the AU, President Idriss Deby Itno, for his initiatives and support provided towards reconciliation in Libya. It reiterates its support to the Libyan stakeholders and encourages the efforts of the AU High Representative for Libya, former President Jakaya Kikwete of Tanzania.

The Assembly reaffirms that only political dialogue can bring a durable solution to the crisis facing Libya and that military intervention can further escalate and complicate the situation. It calls on AU Member States to provide the necessary political and moral support to the Government of National Accord of Libya.

iv) Terrorism

The Assembly Decides to establish an AU Special Fund for Prevention and Combating of Terrorism and Violent Extremism, to be funded through voluntary contributions. It requested the AU Commission to work out the modalities for its establishment and functioning mechanism.

6. Appointment of Judges of the African Court on Human and Peoples’ Rights

The Summit appointed two Judges of the African Court on Human and Peoples’ Rights (AfCHPR) for a six (6)-year term. They are: Marie-Theresa MUKAMULISA from Rwanda and Ntyam ONDO MENGUE from Cameroon. The remaining two Judges shall be elected in January 2017 only from among female candidates from the Northern and Southern regions, in respect of equitable geographical and gender representation in AU Organs.

7. Theme, date and venue of next Summit

The Twenty-Eighth Ordinary Session of the Assembly will be held in Addis Ababa, Ethiopia from 24th to 31st January 2017, under the theme of 2017: Harnessing Demographic Dividend through investments in the Youth”.

8. Declarations

The 27th AU Summit also made declarations on the Summit theme, ‘The African Year of Human Rights with Particular Focus on the Rights of Women’; a Declaration on the “Commemoration of the 10th Anniversary of the Operationalization of the African Court on Human and Peoples’ Rights;” and on the situation in the Middle East and Palestine.

Related News

SADC Secretariat records E160m operating surplus

The Southern African Development Community (SADC) Secretariat has recorded a healthy operating surplus of US$11.8 million approximately E160 million for 2015/2016 financial year.

The good news was revealed by the SADC Director for Budget and Finance Clement Kanyama yesterday.

This was during the start of the 36th Ordinary SADC summit hosted by the country. The SADC financial standing means His Majesty King Mswati III, who will assume chairmanship of the organisation will inherit a healthy organisation.

Kanyama said the recorded surplus showed an increase from 2014/2015 financial year, as the SADC Secretariat recorded E139 million (US$10.3 million).

Kanyama said 2015/2016 revenue was E1 trillion (US$78.6 million) and it was made up of E700 million (US$51.6 million), from Member States and E370 million (US$27 million) from grants, which were recognised as contributions based on the SADC Secretariat compliance with condition, as specified in each financing agreement.

“The total expenditure was E900 million (US$66.8 million) and total assets under the control of SADC Secretariat of E1.4 billion (US$101.1 million),” he said.

He further said the 2015/16 financial year was the first year for SADC to operationalise the RISDP, which was revised was the summit in April 2015. “The revised RISDP has front loaded implementation of industrialisation programmes and related actions to enable member states to benefit fully from the SADC Free Trade Area,” he said.

Kanyama further revealed that for 2016/2017 financial year, the SADC Secretariat budgets provided E580 million (US$42.578 million) from member states funds and E450 million (US$32.990 million) from grants as availed by International Cooperation Partners.

“The SADC Council of Ministers will also consider proposals for revision of 2016/2017 budget of the SADC Secretariat. The 2016/2017 SADC Secretariat Budget and detailed activity plans continue to implement programmes, projects and action derived from the RISDP and Strategic Indicative Plan for the Organ (SIPO),” he said.

Programmes

He said programmes under implementation included coordination of SIPO interventions in the area of politics, defence and security cooperation. It also includes programmes, projects and actions aimed at consolidation of SADC Free Trade Area within the Community and enabling infrastructure.

“The Regional Industrialisation Strategy and Roadmap for 2015-2063 has been developed. Implementation processes are now underway and the operationalisation of the Regional Agricultural Policy (RAP) as well as programmes, projects and actions in the area of health, HIV and AIDS, education and skills development, and labour and employment and gender and development,” he said.

Related News

Rwanda back to Central Africa bloc, 10 years on

Rwanda has formally rejoined the Economic Community of Central African States (ECCAS), after Foreign Affairs Minister Louise Mushikiwabo presented the instruments of ratification to the economic bloc on August 17.

The return repositions the country to benefit economically, politically and diplomatically in the Central African region.

Rwanda, which had been a member of ECCAS since 1981, was readmitted into the bloc last year, almost 10 years after leaving. When it left, it cited the need to focus on its membership in the East African Community and the Common Market for Eastern and Southern Africa.

Since its readmission, countries such as Chad, which did not have diplomatic representation in Rwanda, have opened diplomatic ties with the country. One of Rwanda’s most hostile neighbours for over a decade has been the Democratic Republic of Congo, a key member of the Central African bloc.

But both countries now seem to have buried the hatchet after a meeting between President Paul Kagame and Joseph Kabila last week.

After their meeting, Rwanda praised the DRC for its progress in eradicating negative forces – a marked departure from previous pronouncements where Rwanda criticised the DR Congo for harbouring the FDLR rebel group.

This cooling of the longstanding animosity between the two countries was key to ensuring the growth of Rwanda’s economy – considering that Rwanda’s exports to the DRC represent 75 per cent of its informal cross-border exports.

Its readmission to ECCAS has opened up more opportunities for Rwanda and boosted economic ties with the other 10 member states.

For example, Angola received its first Rwandan envoy, Alfred Kalisa, in September last year, while several bilateral agreements have been signed with countries like Equatorial Guinea and the Republic of Congo (Brazzaville).

Rwanda has built business ties with Congo-Brazzaville, with both countries having a joint commission that evaluates recommendations made by politicians and investors, as well as identifying new areas of co-operation.

Last month, Rwanda and Gabon launched a One Network Area – the first of its kind – which is expected to boost trade between both countries.

Rwanda is also a contributor to peace-building in the region, having contributed about 750 peacekeepers to the United Nations Multidimensional Integrated Stabilisation Mission in the Central African Republic.

Prof Simeon Weihler, dean of social, political and administrative sciences at the University of Rwanda believes that this offers advantages to Rwanda’s diverse market and friendly neighbours.

“Joining multiple economic blocs poses no problem in theory, but could raise implementation challenges if bi-lateral trade arrangements result in contradictory or inconsistent regulations. The desire to build and fortify inter-African trade is an oft-stated goal, and augments Rwanda’s overarching development objectives,” he said.

Related News

What new online portal means for agric export-Import enterprises

Claude Niyomugabo, a produce dealer in Kigali, last month failed to close a huge deal after failing to obtain the necessary import documentation in time.

Niyomugabo is not alone as many other agro-dealers, importers and exporters had fallen victim to the previously bureaucratic and tedious process of acquiring import or export certification.

The bureaucratic procedures had often resulted into delays in terms of delivering farm inputs to farmers affecting sales and crop productivity. However, this could soon become history, thanks to a new online portal unveiled last week, which will ease the process and make it more efficient.

The facility has automated the systems and processes used by Rwanda Agricultural Livestock Inspection and Certification Services (RALIS) to regulate and facilitate businesses involved in international trade in the agricultural sector in Rwanda.

The portal, launched on Friday, was developed by the Ministry of Agriculture and Animal Resources with $150,000 funding from TradeMark East Africa (TMEA), a trade facilitation non-profit organisation.

The new online portal will reduce time and cost to issue import and export certificates, as well as permits of plants, animal materials and agrichemicals by 45 per cent, according to Tonny Nsanganira, the State Minister of Agriculture.

According to Beatrice Uwumukiza, the RALIS director general, the portal will enhance enforcement, as well as ensure transparency and accountability among stakeholders, including traders, transporters and government agencies.

Uwumukiza said the facility that uses the Electronic Single Window system will ease clearance activities and exchange of information among government agencies. The system will help eliminate the Sanitary and Phytosanitary (SPS) non-tariff barriers (NTBs), and this has been a priority area under the market integration pillar of the newly launched Tripartite Free Trade Area (TFTA).

Denise Uwase from Kayonza District is optimistic the initiative is a double win, not only for importers and exporters, but also farmers as it will improve access to inputs like fertilisers and improved seeds, as well as boost produce export.

“This means that those trading in plant and plant materials, animal and animal products and agrichemicals will spend less time and money when acquiring import and export permits,” Uwase said.

The portal targets importers and exporters of plant and plant materials, animal and animal products, and agrichemicals into and out of Rwanda. It will enable traders to make applications and receive import and export permits from the comfort of their offices, without making physical trips to the ministry. This is aligned to government’s vision of making Rwanda a paperless economy through automating all government services to the public and the private sector.

About the portal

The trade portal comprises of two interlinked platforms – a front-end login portal, where RALIS stakeholders will access services ranging from information on Sanitary and Phytosanitary requirements, international and Rwanda trade regulations and features to request for services.

The second platform is a management information system to be used by RALIS to process requests for services. The management information system has been integrated with the Rwanda Electronic Single Window, enabling information sharing between Rwanda Revenue Authority (RRA) and the Ministry of Agriculture and Animal Resources.

It will also be integrated with financial systems, such as the national payment gateway and banking systems, further reducing transaction and administrative costs. The linkages within the system will enhance inter-government agency coordination with the aim of improving service delivery and good governance in Rwanda, said Dr Savio Hakirumurame, the brain behind the portal.

Hakirumurame said that the portal targets importers and exporters of plant, plant materials, animal and animal products, and agrichemicals into and out of Rwanda. Traders will be able to make applications as well as receive import and export permits from the comfort of their offices, without making physical trips to the ministry.

This is aligned to the government’s vision of making Rwanda a paperless economy through automating all government services to the public and the private sector. The new online portal will reduce the transaction and administrative time and costs associated with issuance of permits and certificates by up to 45 per cent; the current direct transaction costs to apply for a permit or certificate is $5.67, this is expected to drop to less than $3 per transaction.

Already, 150 companies and 50 individuals registered with the system following during its three-month piloting. During this period, a total number of 120 import permits and 207 phytosanitary certificates were issued.

Other key benefits of the portal will include improved service delivery and better governance around the management of certificates and permits for the sector. The portal will ease the process of getting prerequisite documents by exporters dealing in time sensitive sectors such as horticulture, according to Lillian Uwintwali, the managing director of M-AHWII, an agri-tech ICT firm, said.

In a world where document forgery has become common, the portal will enable secured and transparent management of documents making it possible for destination market authorities to trust trade documents from Rwanda – and this will enable Rwandan exports to undergo less document scrutiny in the export markets.

Related News

Increase in wheat tariff slammed

The SA Chamber of Baking said on Friday that it did not support the 30 percent tariff increase on wheat imports as this could lead to consumers paying more for a loaf of bread. This would put a strain on an already struggling consumer.

Geoff Penny, the executive director of the SA Chamber of Baking, said the chamber’s calculations had shown that the price of bread could go up by as much as 20 cents a loaf if the tariffs were implemented. She said the pending increase would hit the poorest of the poor most.

“Bread is a staple food and this will hit the lower Living Standards Measure (LSM) group. It might not be too much for the upper LSM consumers, but for those who can’t afford, a 20c increase will be a bit too much,” Penny said.

“We are more concerned about these marginal costs increases and as a chamber we don’t support the tariffs. However, it would be up to the retailers and bakers to determine how much the price of bread will go up by. Because this is a free market, the store promotions on bread and depending where one buys the bread can soften the price increase.”

Urged to publish

Last week, GrainSA won a ruling in the North Gauteng High Court in Pretoria, urging the government to publish the new wheat import tariff.

The court ordered the government to bring into force the expected 30 percent tariff increase on wheat imports after delays held up trading in the market.

It said the government should publish the new levy of R1 591.40 a ton in its official gazette needed before the rate could be formally applied.

Wandile Sihlobo, a senior agricultural economist at Agricultural Business Chamber, said that the tariff increase would in all likelihood lead to an increase in the price of bread.

Sihlobo, however, said although the tariff increase was 30 percent, this would not mean that the price of bread would go up by 30 percent as well.

“The bakers will pay more for their wheat and they might be tempted to pass the costs to the consumer,” he said.

“But this will be determined by the activity between the buyer and the seller. It is too early to tell now whether this will lead to price increases or not in the future. We can only monitor and see once the tariffs are implement what effect they will have on the price of bread.”

Protecting farmers

Sihlobo said the tariffs were protecting the local wheat farmers against unfair competition.

“From the producer perspective, domestic wheat farmers need to be protected from unfair competition from highly subsidised foreign imports,” he said.

JSE-listed companies RCL Foods and Pioneer Foods, who are among the country’s biggest players in the bread industry, elected to leave the industry to determine whether the price of bread should go up, because of the expected wheat tariffs.

“RCL Foods feel that as the wheat pricing is an industry-wide issue, it would be best to approach the SA Chamber of Baking for comment,” said the company.

Grain SA Wins Wheat Tariff Court Case

The Court ruled in favour of Grain SA in Pretoria on 18 August 2016 in an urgent application urging the Government to publish the new wheat import tariff. The new tariff of R1 591.40 per ton triggered on 24 May 2016 and Government dragged their feet in the publishing thereof until the Court made a ruling today. The Court instructed SARS to publish the new tariff in the Government Gazette no later than Wednesday 24 August 2016.

“It is a sad day that we need to manage Government through the Courts, but at least this worked for us,” said Jannie de Villiers, CEO of Grain SA. It already took the Government Departments involved 60 working days without a commitment as to when it will be published. Grain SA also lodged an urgent case in April 2016 for exactly the same reasons, but SARS published the tariff on the day of the Court case – 84 working days later.

Trading in the South African wheat market almost came to a halt given all the uncertainties and delays. We need certainty. It is unfortunate that the consumers did not benefit from this delay as the cheaper international prices of wheat were not passed on to the battling consumers by decreasing bread prices.

Grain SA believes that this ruling will assist the whole value chain to bring certainty to the market and give some indication as to some reasonableness in administering these tariffs.

Related News

Minister Ebrahim Patel welcomes action against collusion and price-fixing in steel industry

The Minister of Economic Development, Ebrahim Patel, on 22 August 2016 welcomed the announcement of a R1,5 billion fine payable by ArcelorMittal, the country’s largest steel-maker, for price-fixing and collusion in the steel industry.

This is the largest single fine imposed against a single company thus far by the competition authorities. The company also undertook, as part of the settlement with the authorities, to invest R4,6 billion in new capital spending to upgrade its plants and improve its competitiveness. The settlement further provides for a pricing mechanism that will cap the company’s margin on flat steel products for a period of five years.

“The action by the competition authorities is part of a crackdown against abuse of market power and price-fixing that undermine the performance of the economy, imposes unnecessary costs on downstream factories and damages local jobs,” Minister Patel said.

“South Africa’s competitiveness and industrial performance require an efficient basic steel supplier industry. High levels of concentration together with collusion undermine our national goals. Companies collude because they believe they can get away with it. Over the past seven years, the competition authorities have focused on collusion and abuse of market dominance involving key input costs in the economy, such as steel-making, fertilizers, construction and telecommunications and well as important basic goods such as bread, poultry and flour,” he said.

“Our resolve is clear: we want to promote investment-led economic growth, not collusion-induced economic stagnation. South Africa is open for business and the message we want to send is that we will act against conduct that damages competition and jobs,” Minister Patel said.

“This can be a boost for small business and for new investors,” he said.

“We look forward to seeing more competitive prices and will be monitoring price increases through the committee set up under the International Trade Administration Act, drawing on the information available from the company’s customers. We will not hesitate to act against any further abuse of market power in the steel industry should this be necessary. We have recently brought into effect the provisions in the Competition Act that criminalize collusion and impose jail terms of up to ten years on directors and employees found guilty thereof,” Minister Patel said.

Related News

Agreement on Trade in Services between India and the Association of Southeast Asian Nations: Report by the WTO Secretariat

Trade Environment

The Agreement on Trade in Services under the framework agreement on comprehensive economic cooperation between India and the Association of Southeast Asian Nations (hereafter “the Agreement”) is ASEAN’s 6th regional trade agreement (RTA). It is however ASEAN’s 3rd Agreement covering trade in services. The Agreement is India’s 14th RTA but India’s 5th RTA in trade in services.

In commercial services, India ranked 5th globally in terms of both global exports and imports, amounting to US$156 billion and US$147 billion, respectively. This represents 3.15% and 3.07% of world exports and imports, respectively.

Among the ASEAN members, Singapore accounted for the largest share of world trade followed by Thailand and Malaysia. Among the newer ASEAN members (Cambodia, Lao PDR, Myanmar and Viet Nam) Viet Nam had the largest share of exports and imports of commercial services, while Lao PDR has the smallest share.

Commercial services trade for India in 2005-2014 show that India has run a constant trade deficit in these services. While its exports are dominated by other business services and computer and information services, key imports are transport and other business services.

Figures on India’s bilateral commercial services trade with ASEAN have not been made available.

In terms of commercial services trade, ASEAN’s top three traders (both for exports and imports) were Singapore, Thailand, and Malaysia. In general travel and transport services are important exports and imports although other business services are also important notably for Indonesia, the Philippines and Singapore.

Based on available data on total inward and outward foreign direct investment (FDI) stocks with the world for each ASEAN Member State, Singapore remains the largest source and destination for FDI. It is also the largest investor in India and the largest recipient of FDI from India among ASEAN members.

Regarding total foreign direct investment flows by ASEAN member states during 2005-2014, for its investment in India, Singapore has consistently been the largest recipient and provider of direct investment from and to the world, respectively. Malaysia and Indonesia have consistently been the second and third largest providers of FDI during the period surveyed. Thailand and Malaysia have consistently been next as the second and third largest recipients of FDI, respectively, for most of this period. In the second part of the period, Indonesia became the third destination for FDI, following Singapore and Thailand.

Characteristic Elements of the Agreement

The Agreement was signed by India and the ASEAN member states (hereafter “the Parties”) on 13 November 2014 and entered into force on 1 July 2015. It was notified to the WTO by the Parties on 20 August 2015 under GATS Article V:7(a).

The Agreement was negotiated under the Framework Agreement on Comprehensive Economic Cooperation between the Republic of India and the ASEAN and the Protocol to amend the Framework Agreement, signed in 2009. It should also be seen in connection with the Agreement on Trade in Goods that entered into force on 1 July 2003; the ASEAN-India Agreement on dispute settlement mechanism (hereafter the “DSM agreement”), which was signed in 2009; and the Agreement on investment that was signed on 12 November 2014. The text of the Agreement is available, together with its Annex, on the official website.

Structure of the Agreement

The Agreement is composed of four Parts and 34 Articles. It also contains an Annex on movement of natural persons. Each Party’s Schedules of specific commitments are attached to and form an integral part of the Agreement. Moreover, the GATS Annexes (on the movement of natural persons supplying services, air transport services, financial services, and telecommunications) shall apply to the Agreement, mutatis mutandis (Article 28).

Part I of the Agreement provides the scope of its disciplines and definitions. Part II contains the main obligations and disciplines while Part III addresses the Parties’ specific commitments covering market access and national treatment, as well as additional commitments. It refers to the Parties’ individual Schedules of specific commitments and addresses the application and extension of commitments as well as the procedure applicable to the modification of Schedules. Part IV contains other and final provisions covering areas such as the relationship between the Agreement and other agreements; the incorporation of annexes and possible future legal instruments; comitology (contact points and Joint Committee on Services); the review of the implementation and operation of the Agreement; amendments to the Agreement; dispute settlement; denial of benefits; the entry into force of the Agreement; and withdrawal from it or its termination.

The Parties may adopt legal instruments in the future pursuant to the provisions of the Agreement. Such instruments shall form an integral part of the Agreement (Article 24).

Provisions on Trade in Services

Scope and Definitions

The Agreement applies to measures of a Party affecting trade in services. Trade in services is defined as the supply of a service through the four modes of supply6 defined by the GATS.

The Agreement does not apply to: i) services supplied in the exercise of governmental authority; ii) laws, regulations or requirements on government procurement of services in the exercise of non-commercial resale and use; and iii) cabotage in maritime transport services (Paragraph 2 of Article 1).

The newer ASEAN Member States, Cambodia (which joined in 1999), Lao PDR (1997), Myanmar (1997) and Viet Nam (1995) enjoy special and differential treatment and flexibility under the Agreement (preamble of the Agreement). The increasing participation of these Parties shall be facilitated through negotiated specific commitments taking into account, inter alia, their need to improve access to technology, to distribution channels and information networks, and the liberalization of market access in sectors and modes of supply of export interest to them. Appropriate flexibility shall also be accorded to these Parties for progressive liberalization in terms of specific commitments undertaken in line with their respective stage of development (Article 16).

Denial of Benefits

Article 31 on the denial of benefits is based on Article XXVII of the GATS and allows a Party to deny the benefits of the Agreement, inter alia, for the supply of a service, if it establishes that the service is supplied from or in the territory of a third-party; or if it establishes that a natural person is not a “natural person of another Party”, or that a juridical person is not a “juridical person of another Party”.

General Provisions on Trade in Services

Market access

The market access provisions mirror the language of Article XVI of the GATS (Article 18). The Parties’ market access commitments are contained in their Schedules of specific commitments.

National and MFN treatment

The national treatment provisions mirror the language of Article XVII of the GATS (Article 17). The Parties’ national treatment commitments are contined in their Schedules of specific commitments. The Agreement does not contain provisions on MFN treatment.

Commercial presence

No specific provision on commercial presence, per se, is stated by the Agreement. The limitations on commercial presence in the services sectors are contained in the Parties’ schedules of commitments.

The Agreement on Investment of the Framework Agreement on Comprehensive Economic Cooperation between the Parties contains a provision affecting the supply of a service by a Party’s service supplier through commercial presence in the territory of another Party. The Agreement on Investment shall not apply to measures adopted or maintained by a Party to the extent that they are covered by the Agreement (Paragraph 4(a) of Article 1 of the Agreement on Investment).

Performance requirements

No specific provision on performance requirements, per se, is stated by the Agreement. The limitations related to performance requirements in the subscribed services sectors are contained in the Parties’ schedules of commitments. Parties’ additional commitments, including those regarding qualifications, standards or licensing mattes are included in their Schedules of specific commitments (Article 19).

Senior Managers and Boards of Directors

No specific provision on senior managers and boards of directors, per se, is stated by the Agreement. The limitations that may be applicable to senior managers and boards of directors in the services sectors are contained in the Parties’ schedules of commitments.

Movement of natural persons

There is no specific provision on the movement of natural persons in the Agreement. However, where commitments are undertaken by a Party on the movement of natural persons, the categories of natural persons for whom commitments are undertaken are defined in the Annex on Movement of Natural Persons, where applicable. This Annex identifies and provides definitions for three categories of natural persons: (i) business visitor; (ii) contractual service supplier; and (iii) intra-corporate transferee.

The GATS Annex on Movement of Natural Persons Supplying Services shall, mutatis mutandis, apply to the Agreement (Paragraph 1 of Article 28).

Liberalization Commitments

Part III of the Agreement contains disciplines related to the specific commitments made by each Party in their individual Schedules. A GATS-like “positive listing” approach is used for their commitments in market access, national treatment, and additional commitments. Modification and withdrawal of commitments are governed by Article 22. Notification of changes followed by negotiations with the affected Party and the necessity to agree on compensatory adjustment are disciplined. If the Parties are unable to reach an agreement on compensatory adjustment, the matter shall be resolved under the DSM Agreement. In such cases, the modifying Party may not modify or withdraw its commitment until it has made compensatory adjustments in conformity with the findings of the arbitration.

The Parties’ Schedules of specific commitments identify the services sectors and sub-sectors for which commitments are made, and specify, by mode of supply, the conditions and limitations that may be applicable to market access and national treatment-related commitments. It lists as well additional commitments that the Parties may wish to register (Article 19).

The sections below compare each Party’s GATS schedule with its respective Schedules of specific commitments attached to the Agreement. Improvements over existing GATS commitments are a reduction in limitations to market access and/or national treatment, a relaxation of the form of establishment under mode 3, and/or additional commitments and increased coverage. However, horizontal limitations in the GATS Schedule of Specific Commitments and reservations covering all sectors are not included. Moreover, mode 4 commitments and limitations are, to a large extent, excluded. The following sections are to be read in conjunction with the Parties’ schedules of commitments under the Agreement.

India

India has a single Schedule that is applied to Brunei Darussalam, Cambodia, Lao PDR, Malaysia, Myanmar, Singapore, Thailand and Viet Nam, and two separate individual Schedules that are applicable to Indonesia and to the Philippines (Article 22).

Horizontal commitments

India’s horizontal commitments in the Agreement, almost identical for all its ASEAN partners, partly match those under the GATS. Additional national treatment limitations are registered for some types of transfer of equity; on the repatriation of sale proceeds of immovable property; on certain aspects of taxation laws; and on the acquisition of land. Subsidies are unbound. Under mode 4, the horizontal commitments in the GATS serve as a basis for those in the Agreement, with some specific commitments made in particular for the provision of computer and related services.

Sector-specific commitments

Under the Agreement, India’s services schedule builds on its commitments under the GATS. It both expands the coverage of its specific commitments and improves market access and/or national treatment by withdrawing some limitations (for the latter in particular in relation to modes 1 and 2).

With respect to sectors for which it has commitments under the GATS, India makes improvements, under the Agreement, in relation to professional services (though not with respect to the Philippines); computer and related services, and some other business services (though no improvement is made with respect to Indonesia and the Philippines). Improvements are also made in some telecommunication services and, marginally, some audiovisual services (motion picture or video tape distribution services); general construction work for civil engineering; some health services – in particular hospital services (though this is not applicable with respect to the Philippines); hotel and restaurant services and travel agencies and tour operators services (improvements for the latter two tourism subsectors not benefitting the Philippines); and some maritime transport services (with a number of limitations and not in favour of the Philippines).

As under the GATS, no commitment is made, under the Agreement, in distribution services; education services; environmental services; and recreational and cultural and sporting services. India’s partial GATS commitments in financial services are repeated, without improvement, in the Agreement.

ASEAN Member States

The specific commitments of the ASEAN Member States are contained in separate individual Schedules. While some ASEAN Member States Schedules are similar to their GATS specific commitments, others have made commitments higher than their GATS commitments in terms of coverage and depth. It is understood that, in the latter case, their GATS commitments continue to apply to the other Parties, even if not specifically included in the Schedules in the Agreement.

Regulatory Provisions

Domestic regulation

Article 5 largely replicates the disciplines contained in Article VI of the GATS. It also binds the Parties to bring the results of the negotiations related to Article VI.4 of GATS into effect under the Agreement, as appropriate.

Recognition

Under Article 6, the Agreement mirrors the provisions in paragraphs 1 through 3 of Article VII of the GATS.

Upon request by a Party, the Parties shall also encourage their respective professional bodies or professional regulatory authorities, to negotiate arrangements for mutual recognition of education or experience obtained, requirements met, or licences or certifications granted in that service sector, with a view to the achievement of “early outcomes”. Progress in this regard will be reviewed by the Parties in the course of the review of the Agreement pursuant to Article 27.

The provisions of the DSM Agreement shall not apply to disputes arising out of, or under, the provisions of agreement or arrangements for mutual recognition that may be concluded by the Parties’ respective professional bodies or professional regulatory authorities.

Subsidies