Search News Results

Importing food is harming the continent, UN agency head to tell African leaders

The US$35 billion a year that Africa spends on importing food should be used to create local jobs in agriculture, according to Kanayo F. Nwanze, President of the UN’s International Fund for Agricultural Development (IFAD).

Addressing the sixth Tokyo International Conference on African Development (TICAD) in Nairobi tomorrow, Nwanze is expected to tell African leaders that the potential for prosperity on the continent is enormous, but investments need to be redirected to developing the agricultural sector.

Although it has a quarter of the world’s arable land, Africa generates only 10 per cent of global agricultural output.

“African leaders are failing their people by their weak investments in agricultural inputs and infrastructure, and their lack of policy support for the sector,” said Nwanze on the eve of his departure.

“If even a portion of the money used for food imports was spent on creating jobs in rural areas, not only would the world’s largest youth population see a viable future on the continent, but Africa would be able to feed itself,” he said.

Convened by Japan, the purpose of TICAD is to promote high-level policy dialogue between African leaders and partners, with a focus on African-led development. This is the first time that TICAD will be held on the African continent. It will run until 28 August.

Although Africa is the world’s second fastest growing economic region, more than 300 million Africans live below the poverty line. Most live in rural areas and depend on agriculture for their livelihoods. Unemployment rates are close to 40 per cent.

“Economic growth alone is not enough. If we want a continent with food security and social stability, we have to ensure that development focuses on people. They do not want handouts. They want economic opportunities,” said Nwanze.

“At TICAD this year, I hope we can go beyond talking about Africa’s potential and discuss what is practically needed for Africa’s people to seize that potential,” he added.

While at TICAD, Nwanze will also participate in the launch of Japan’s Initiative for Food and Nutrition Security in Africa which will establish a framework for African countries to collaborate to improve their nutrition status.

Japan is a founding member and a leading contributor to IFAD – a specialized United Nations agency and international financial institution that invests in agriculture and rural development in developing countries around the world.

Related News

Govt must improve private sector engagement – FSE&CC

Federation of Swaziland Employers and Chamber of Commerce (FSE&CC) Chief Executive Officer Bonisiwe Ntando, says although government involves the private sector when adopting policies, for now the engagement remains superficial.

Ntando was responding to the issues raised during the ongoing second annual Southern African Business Forum (SABF) Conference. One of the issues was that governments should engage and consult with the private sector when drafting or adopting polices.

“I think there is more that we can do in terms of the consultations, because in most cases we find there are already policies in place which we were never consulted during their drafting. So maybe now it is a start of good things to come. I am hopeful, because we need to influence these policies as they are done to be used by the private sector,” she said.

She said for Swaziland specifically, the consultations were not that effective.

“We have just set up a trade facilitation committee, whereby private sector participates in, but, it is a new committee and you can imagine how old SADC is, why was the private sector not involved all along? However, we hope that now as we have started on this new path, the consultations will be sustained.”

Ntando said participating in the conference came with many benefits as the region was developing at a very fast pace, “what we need to address though as the country is we take time to utilise the availed opportunities. As you can see, some of the decision and declarations were made some years back and by now we should have reaped the benefits that came with them. But, we are very slow to implement, we need to jump at such opportunities.”

She said the private sector, in most instances, they hardly have access to the policies, sometimes it is even hard to know there were new policies because the private sector in most cases did not form part of the delegations, “its government most of the time and by the time they come back, no one would come to present these issues to us, unless we get a high level statement. That is not enough; we need to do more than just that.”

Ministry of Commerce, Industry and Trade Principal Secretary Jinnoh Nkambule said private sector engagement was one of the areas that needed to be strengthened.

“We have a committee, the national trade facilitation, where we meet with the revenue authority, private sector, and relevant government departments. We are collectively working to ensure that doing business becomes easy in Swaziland. If there are challenges, especially on the movement of goods, we work collectively to find amicable solutions,” he said.

Nkambule said government prioritised private sector engagement and would continue to broaden its scope for the benefit of this sector.

Related News

SACU: The capabilities driving participation in global value chains

Global value chains have altered the nature of global trade and offer significant opportunities for developing countries to expand exports, access technology, and raise productivity. Policy makers rightly seek to understand what it takes to participate in global value chains. In practice, this means understanding what it takes to attract lead firms and upgrade to higher value-added activities.

Recent literature has pointed to a range of underlying characteristics that may drive participation in global value chains. Using a modified factor-content methodology, this paper shows that proximity to markets, efficient logistics, and strength of institutions are among the most important capabilities. However, the paper also shows that each sector has a unique mix of capability requirements. Fixed structural characteristics limit the range of sectoral possibilities for a given country, but, by reducing policy-related gaps, a country may be able to increase its competitiveness for participating in global value chains.

The paper applies the methodology to Southern African Customs Union countries, and demonstrates that, by filling gaps in underlying capabilities, these countries could increase participation in certain global value chain sectors.

Introduction

The emergence of global value chains (GVCs) and their rapid expansion over the past two decades has transformed the global trade environment. GVCs involve task‐based trade across multiple stages of the production process that take place across a number of different countries, in which multiple inputs and exports of intermediate goods and services are necessary to produce a final good, which may also be exported. This “second unbundling” of global trade was made possible by a combination of improved shipping technology, revolutionary changes in ICT, and global trade liberalization that enabled multinational firms to take advantage of differences in comparative advantage across locations to establish integrated networks of intra and inter‐firm production and trade.

GVC‐oriented trade is seen to offer significant opportunities for developing countries, especially smaller ones, to benefit from global integration by changing the nature of competitiveness. In the past, for a country to become an apparel exporter, for example, it would need design capabilities and textile mills; to export in the automotive sector, it would need to produce engines and all subcomponents, as well as have the scale to carry out assembly. Under the new GVC dynamics, a developing country can specialize in certain activities (sewing, specific components or subassemblies) within the chain and trade in intermediates. In this sense, GVCs denationalize comparative advantage, as global lead firms construct global production networks by exploiting the most competitive locations for specific activities.

Given this situation, and in an environment where developing countries are urged to “join” and “upgrade” in GVCs, policy makers in developing countries rightly seek to understand what it takes to do so. And, in practice, this means understanding what it takes to attract lead firms to place stages of the production value‐adding process in their country. Here, the advice remains a bit less clear in several ways. First, identifying what specific aspects of a country’s competitiveness matter most for GVC trade remains a question. Policy advice points to aspects like trade facilitation, trade agreements, non‐tariff measures (NTM), contract enforcement, and property rights protection. On the other hand, the emergence of countries like Bangladesh and Vietnam as major players in global production networks suggests that it may be all about low wages and large labor forces; while the development of automotive value chains in Central and Eastern Europe points more to relative wages, technology, and proximity. This points to a second practical challenge – the fact that what drives competitiveness in GVCs is likely to vary across GVC sectors as well as across GVC positions (upstream or downstream). Finally, with competition for GVC investment taking place in a truly global market, factor competitiveness relative to other countries matters a lot.

To inform policy recommendations, the empirical research literature in recent years has begun to address the determinants of GVC participation but has yet to yield a clear picture. Most studies have focused on evaluating the importance of a certain characteristic, such as trade facilitation, transport, trade logistics, time zones, technology gaps, or exchange rates or trade policy. A number of studies have looked at the determinants of production fragmentation in general and of supply chain trade between countries. Other studies attempt to estimate the relative contribution of a host of possible drivers to GVC participation. Among the findings is that non‐policy factors (structural characteristics like geography that cannot be changed in the short‐ or medium‐term) matter more than policy factors.

However, sector‐level analysis is usually not conducted or conducted at a low level of sectoral disaggregation or while testing only a small range of possible drivers. Firm‐level studies have assessed the determinants of offshoring strategies, identifying the importance of factors like productivity and both skills and capital intensity at the firm level. Finally, a separate segment of the literature assesses GVC participation’s impact on economic outcomes such as growth and employment.

So while these studies, along with the policy literature on GVCs, give us a sense of what factors are likely to be important in determining GVC dynamics, the question of which specific drivers matter most and when they matter most for country‐level participation in GVCs remains open. One of the reasons for this is that data that identify clearly what is and is not “GVC trade” are still problematic, despite the significant progress that has been made in recent years. Another reason is that there are significant links across many of these drivers, making endogeneity a problem.

In this context, the purpose of the following empirical exercise is to shed further light for policy makers on where to focus efforts to drive competitiveness for GVC participation. We do this by generating “revealed capability intensity” (RCI) measurements of traded goods, extending the traditional theory of factor‐content of trade to account for the capabilities that would be most relevant in task‐based trade, and utilizing these measurements to illustrate how underlying capabilities shape participation of Southern African Customs Union (SACU) countries in global value chains.

This paper is a product of the Trade and Competitiveness Global Practice Group. It is part of a larger effort by the World Bank to provide open access to its research and make a contribution to development policy discussions around the world.

Related News

Africa benefits from net positive remittances flows

International remittances has become a major source of foreign currencies for most of African countries and have been found to be more stable and dependable than other forms of foreign currency inflows such as Foreign Direct Investment (FDI) and Overseas Development Aid (ODA). In 2015, African economies received – both from overseas and Intra-African corridors – officially recorded remittances amounting to US$66 billion.

The five top sending countries to Africa are United States (US$ 8,87 billion), Saudi Arabia (US$ 8,36 billion), France (US$ 6,72 billion), United Kingdom (US$ 5,51 billion) and Italy (US$ 3,36 billion).

Intra-Africa Remittances represent 20 percent (US$ 12,8 billion). Cameroon (US$ 2,15 billion), Cote d’Ivoire (US$ 1,66 billion), South Africa (US$ 1,06 billion), Ghana (US$ 1 billion) and Nigeria (US$ 0.9 billion) are also the five top African sending countries to other countries within Africa.

The top ten African remittances receiving countries are Nigeria (US$ 20,66 billion), Egypt (US$ 19,71 billion), Tunisia (US$ 2,35 billion), Algeria (US$ 2,0 billion), Ghana (US$ 2,0 billion), Senegal (US$ 1,61 billion), Kenya (US$ 1,56 billion), Uganda (US$ 1,07 billion), Mali (US$ 0,89 billion) and South Africa (US$ 0,87 billion).

The impact of remittances varies across the continent and compared to GDP, remittances have become very significant in many countries such as Liberia (24.6%), The Gambia (21.2%), Comoros (20.2%), Lesotho (17.4%) and Cabo Verde (10.5%). Though recorded remittances flows to and within Africa are stable and growing, they are still significantly understated as large volume of remittances are being sent through informal/unregulated channels.

High Cost of Remittance flow within Africa

The African Institute for Remittances (AIR) to work with key market players to lower the cost of sending money to and within Africa

Remittances transfers is one of the most important sources of external resources in many African countries that has real impacts on lives of millions of recipient families across Africa. However, remittance senders to and within Africa continue to suffer from the high costs of sending money home.

Though significant reductions has been achieved since 2010 where the average cost was above 12%, the cost of sending remittances to and within Africa – according to the data collected during the second quarter of 2016 – are still the highest. Further, the top ten most expensive corridors in the world are all intra-Africa originating from South Africa and Tanzania, both sending mainly to their neighboring countries.

The average cost of sending money to and within Africa, in the second quarter of 2016, was 9%, which was 1.4 percentage points more expensive than the global average transfer costs for the same period and 6% above the target set by the Sustainable Development Goals (SDG) to reduce transfer costs to the level of 3% by 2030.

A key priority of the African Institute for Remittances (AIR) is to lower the costs of sending money to and within Africa, and will engage key market players including regulators, Remittance Service Providers (RSPs), technology providers, and remittance senders and receivers. In this regard, the Institute works towards the improvement of transparency and enhancing competition and efficiency within the remittances market in Africa.

The AIR, in the framework of its Technical Assistance/Capacity building programmes, is working with AU Member States and Partners towards improvement of remittances data measurement, compiling and reporting systems in Africa. The Institute has started consultations with several Central Banks in AU Member States in this regard. A Consultative forum was held in Naivasha, Kenya, in December 2015 followed by a Consultative and Stock-taking workshop in Harare, Zimbabwe, from 10-12 August 2016 and nine Central Banks have already been identified to benefit from the technical Assistance in the 2016/2017 period. In the coming months, AIR will firm up country-specific TA programmes.

The AIR is conducting quarterly surveys on remittances price structures. Collected data are published in the Institute’s remittances price database Send Money Africa (SMA).

Related News

NEPAD-IPPF strengthens capacity to improve stock of well-prepared bankable infrastructure projects

The NEPAD Infrastructure Project Preparation Facility, NEPAD-IPPF, has concluded a two-day workshop that brought together over 20 staff members, representatives from the African Development Bank’s Departments of Transport, ICT, Energy, Environment and Climate Change, Resources Mobilisation and External Finance.

The two-day seminar, held in Abidjan, was also attended by other AfDB Infrastructure Specialists in energy from field offices covering Zambia, Mozambique, Rwanda and Angola, and was aimed at defining modalities for improved delivery aligned to the new NEPAD-IPPF Strategic Business Plan (SBP) covering the five-year period 2016-2020. The SBP seeks to increase the stock of well-prepared bankable infrastructure projects across Africa which can attract financing

The first day of the retreat focused on translating the newly approved five-year Strategic Business Plan (SBP), into actionable goals. Under the new SBP, NEPAD-IPPF seeks to prepare between 60 to 80 regional infrastructure projects in energy, transport, trans-boundary water and ICT with reparation costs of between US$150 million to US$250 million over the five-year period and this will require additional resources from existing and potential donors.

NEPAD-IPPF, supports African governments, Regional Economic Communities (RECs) and African infrastructure-related institutions such as Power Pools and to prepare bankable, investment-ready projects that can attract financing for implementation.

Since inception, NEPAD-IPPF has awarded 67 grants for preparation of regional infrastructure projects in Energy, Water, Transport and ICT, resulting in investment financing of over US$ 7.78 billion, thusresponding directly to Africa’s integration and development efforts.

Discussions at the retreat also focused on strengthening internal capacity of NEPAD-IPPF with new working clusters based on defined roles and value addition through enhanced collaboration and synergies to improve operational effectiveness, efficient delivery and enhanced interface with clients. The four clusters are Project Delivery; Financing and Partnerships; Portfolio Management; and Communications and Outreach.

As a means of augmented its capacity, NEPAD-IPPF has recently recruited four new staff. These are Alex Ndiku Mbaraga, Project Preparation Specialist in charge of transport projects; Karine Mbengue-Maingé, Resource Mobilisation Specialist; Monde Nyambe, Infrastructure Project Finance Specialist and Binny Prabhakar, Project Preparation Specialist in charge of energy projects. The new additions to the existing NEPAD-IPPF team are expected to further enhance the operational effectiveness of the Facility so that it is better able to respond to the needs of its primary clients and ultimate beneficiaries, the African countries.

“Bringing together our staff and partners gave us the opportunity to take part in stimulating conversations and ensure the New Strategic Business Plan is delivered into actionable goals with key performance indicators,” said Shem Simuyemba, Manager for NEPAD-IPPF, who added: “A project is not a project until it is bankable and can attract financing for implementation. Our ambition for the next five years is to accelerate our project delivery, strengthen our performance and results.”

NEPAD-IPPF is a multi-donor Special Fund hosted by the African Development Bank and supported by a number of donors, including Canada, Germany, the UK, Spain, Norway and Denmark.

Related News

Cooperation in Disaster Management can be a catalyst for deeper partnerships in BRICS

Minister Des van Rooyen on BRICS Ministers of Disaster Management meeting

The Minister for Corporative Governance and Traditional Affairs (CoGTA), honourable Des van Rooyen in his capacity as the Minister leading the National Disaster Management Centre (NDMC) in South Africa attended the second meeting of BRICS Ministers of Disaster Management in Udaipur, Rajasthan, India from 22 to 23 August 2016.

This meeting follows the one that was convened in earlier this year in Russia attended by Deputy Minister for CoGTA, honourable Obed Bapela. The April meeting concluded with the signing of the St Petersburg Declaration on 20 April 2016.

This Declaration and Joint Action Plan of BRICS emergency services for 2016-2018 reaffirms the shared commitment to strengthen mutual cooperation in emergency management and the sharing of experiences to protect lives, livelihoods and properties amongst BRICS member countries.

In his address to conference, the Minister empahsised the strategic importance of BRICS as it provides economic benefits such as increased trade an investment opportunities and assisting South Africa to increase its voice internationally. “South Africa can play a leading role BRICS by helping to facilitate deeper integration of relations between African states and other BRICS member countries and focusing on other niche advantages,” said Minister van Rooyen.

The Minister’s attendance of this meeting in India is in line with the South African Disaster Management Act, 2002 (DMA) which calls for the establishment of arrangements for cooperation in international disaster management and the establishment of joint standards of practice.

This conference also speaks to the Section (16)3 which encourages the NDMC to establish links with institutions and foreign disaster management agencies performing the similar functions so as to exchange information and to have access to international expertise in an assistance in respect of disaster management.

The meeting held in India from 22-23 August 2016 deliberated on areas of cooperation with respect to floods risk management and forecasting of extreme weather events in the context of changing climate among the BRICS Countries and increased frequency and intensity of disasters, both natural and man-made.

What was clear from the meeting is that BRICS member countries face the common challenges of Disaster Management in the form of floods and extreme weather events. To this effect, the meeting also benefitted from the wisdom of stakeholders and experts who attended and delivered presentations at the meeting and working in the field of floods risk management and forecasting of extreme weather events.

The conference as part of its resolutions accepted that cooperation in disaster management is a key element of building peace and prosperity which is one of the key concepts in the BRICS partnership. “Cooperation in disaster management can also act as a catalyst for deeper partnership in other areas of BRICS cooperation,” said Minister.

Useful lessons can be learned within the BRICS partnership as some of the countries share a similar disaster risk profile as South Africa and there are many good practices that can be shared in this area. The meeting finally established a joint task team to implement the roadmap action plan.

Udaipur Declaration of BRICS Ministers For Disaster Management

WE, the Ministers for Disaster Management of the Federative Republic of Brazil, the Russian Federation, the Republic of India, the People’s Republic of China and the Republic of South Africa, met in Udaipur, Rajasthan, India on 22nd and 23rd August 2016 at the 2nd Meeting of the BRICS Ministers for Disaster Management;

RECALLING, the Ufa Declaration signed at the 7th BRICS Summit on 9th July 2015, which identifies the need to promote cooperation in preventing and developing responses to emergency situations (Art.35), acknowledging the fruitful discussions on natural disasters within the context of BRICS cooperation in Science, Technology and Innovation (Art.35) & reiterating BRICS commitment to mitigate the negative impact of climate change (Art.53);

RECALLING, our commitments towards implementation of the Sendai Framework for Disaster Risk Reduction, the Sustainable Development Goals and the Paris Agreement on Climate Change and our shared vision to play proactive and responsible role both at the regional and global levels with respect to disaster risk management;

RECOGNISING, with concern the growing level of disaster losses in our nations as well as increasing exposure of our people, economies, infrastructure and other social & cultural assets to various natural hazards;

REALISING, the urgent need to enhance awareness among all BRICS sector institutions and stakeholders to be able to address the interlocking issues of disaster risk reduction, climate change adaptation and sustainable development to effectively reduce adverse impacts of natural and human-induced disasters;

REAFFIRMING, the commitments of St. Petersburg Declaration of 20th April 2016 and agreed joint action plan for developing cooperation in the field of emergency management and working towards improving tools for monitoring and forecasting of emergencies, risk assessment and mechanisms of interaction in the provision of assistance in case of emergencies;

DO HEREBY:

-

Commit to continue to work towards a more risk resilient future by reducing existing disaster and climate related risks through integration of disaster risk management measures into sustainable development.

-

Promote cooperation in developing and disseminating innovative disaster risk management (DRM) solutions/practices in respect of key sectors of development;

-

Promote exchange of information on best practices relating to DRM to assist nations to continue to develop effective and appropriate responses to disaster risk reduction challenges;

-

Promote investments in disaster risk management and climate change adaptation through cohesive and integrated structural and non-structural mitigation measures including risk financing and risk transfer, in both public and private sectors;

-

Strengthen mechanisms/ initiatives on forecasting and early warning for managing the effects of extreme weather events;

-

Proactively analyze future disaster threats emanating from climate change, continue sharing and disseminating climate risk information to support ongoing and future efforts to manage disaster risks related to climate change in all development sectors;

-

Strengthen the capacities of national, regional and local institutions to monitor and reduce risk as well as enhance adaptive capacities of stakeholders through the promotion of education on DRM; and

-

To take necessary measures to implement joint action plan agreed in the 1st Meeting of the BRICS Ministers for Disaster Management at St. Petersburg in April 2016.

For implementing the above:

WE AGREE to Set up a Joint Task Force on Disaster Risk Management for regular dialogue, exchange, mutual support and collaboration among BRICS Countries. The Joint Task Force shall consist of one representative from each BRICS country and will be chaired by rotation by the representative of the country holding chairmanship of BRICS during that year. The Joint Task Force shall meet on the sidelines of the meeting of the BRICS Ministers for disaster management and may also hold additional meetings as necessary, including through video conferencing. As a follow on to St. Petersburg meeting, the Udaipur meeting agreed on a road map for implementation of the Joint Action Plan.

Adopted in Udaipur, Rajasthan, India on the Twenty Third Day of August in the Year Two Thousand and Sixteen.

23RD AUGUST 2016, UDAIPUR, RAJASTHAN, INDIA

Related News

tralac’s Daily News Selection

The selection: Thursday, 25 August 2016

The Kilimanjaro Declaration (Africans Rising Movement)

This week's tralac e-newsletter is posted: access here

Organic farming in Africa has rich potential, but is increasingly underfunded (UNCTAD)

An example of the opportunity comes from an East African regional programme, which saw the region's organic exports grow from $4.6 million in 2002/03 to $35 million in 2009/10, according to the International Federation of Organic Agriculture Movements. The programme led to a common regional organic standard and significantly increased crop yields in Burundi, Kenya, Rwanda, Uganda, and Tanzania. Despite such success stories, almost a quarter (23%) of organic farmers, exporters, and experts from 16 African countries said they felt that access to financing had become more restrictive in the last five years. The results were published by UNCTAD in a new technical paper (pdf) on financing organic farming in Africa. In the same survey, 64% said the situation had not changed while just 13% said access to funding had improved.

SADC Agricultural Development Fund: update (Swazi Observer)

The Southern African Development Community E17.5bn ($1.3m) Agricultural Development Fund regulations are expected to be finalised by November 2016. The fund will contribute about 50% to the Regional Agricultural Implementation Plan, while the rest will be contributed by governments and the private sector. SADC Regional Agricultural Policy Technical Director Martin Muchere further projected that “the SADC ADF constitution and institutional management sustainability plan would be developed by December, domestication is projected to be conducted by March 2017, facility expenditure frameworks by June 2017, and facility expenditure frameworks developed by December 2017.”

EALA report on outreach, sensitisation activities

The EALA has passed a key report of its outreach and sensitisation activities and called for more awareness among the people on the benefits of EAC integration. The Assembly further wants the specific interest groups including youth, women, civil and co-operative societies to be fully involved in the integration process and the pillars of integration including the Political Federation, fast tracked. The growing stature of Kiswahili also did not escape the attention of the legislators. The Sensitisation Report (pdf) presented by Hon Patricia Hajabakiga, Chair of EALA Rwanda Chapter, is a culmination of outreach and sensitisation activities carried out in the Partner States by the various country Chapters of EALA in June 2016. The activities held between June 9th to 28th, 2016 were anchored under the theme: EAC Youth Agenda: Accessing the Gains.

Zambia urges COMESA to attract more foreign direct investment (Global Times)

The Zambian government has challenged a regional trading bloc to do more to make the region a more conducive area for investment attraction and business development, a senior Zambian official said Wednesday. Siame Kayula, Permanent Secretary for Commerce, Trade and Industry, said COMESA still had a lot to do in terms of investment attraction. "COMESA deserves better than the $19.7bn attracted during the year 2015 in terms of foreign direct investment. We need to do much more not only to attract but also to retain more foreign investments and encourage domestic investments," she is quoted as saying by the Times of Zambia. In remarks delivered during a meeting of experts on the adoption of the revised COMESA Common Investment Area framework, Kayula said Zambia welcomes the revision of the framework as a legal instrument that was designed to increase investment flows with the regional bloc, adding that it will help member states create a stable region and good investment environment.

De-risking in Africa on the rise (SWIFT)

SWIFT data shows that many countries in Africa have seen a reduction in the number of foreign counterparties, the overseas banks with which African banks transact. The data was part of a new report looking at the impact of global regulations on correspondent banking networks, called ‘Addressing the unintended consequences of de-risking – Focus on Africa’, which was released at the SWIFT Business Forum South Africa, in Johannesburg. The report shows that de-risking is on the rise in several African countries. South Africa lost more than 10% of its foreign counterparties between 2013 and 2015. In Angola the decline was even steeper, with the number of foreign counterparties dropping by 37% in two years. Mauritius has also seen a sharp decline of 18%. The data shows that Nigeria’s international banking network has experienced limited de-risking.

RMB continues to penetrate the South African market (SWIFT)

SWIFT data shows that Renminbi usage in payments in South Africa increased by 65% over the last 12 months and by 112% in the last two years, moving the country from position #30 in July 2014, to #24 in July 2016. Excluding domestic traffic, RMB payment messages increased in volume by 70% in the last 12 months. In addition, nearly 40% of RMB payments by South African institutions have been offshore payments exchanged with countries other than China and Hong Kong, compared to 16% in July 2015. In July 2016, the RMB bounced back to its position as the fifth most active currency for global payments by value with a share of 1.90%, a slight increase from 1.72% in June 2016. Overall RMB payments value decreased by 0.68% compared to June 2016, whilst in general all payments currencies decreased by 10.08%.

Reinventing financial sector regulation in South Africa (tralac)

From an outward investment perspective, these changes may encourage South African financial institutions to focus attention on other markets in the region as they face a more challenging regulatory environment in South Africa. On the other hand, the new regulations could see South African financial institutions focus on regulatory compliance, rather than business expansion. This would also apply to the capacity and willingness of institutions to expand and innovate domestically. The specific requirements of the various new and changed sectoral regimes will also have the potential to create new barriers and opportunities to trade and investment as well as having implications for financial inclusion. [The analyst, Ashly Hope, is tralac research advisor]

Uganda: Experts warn SMEs over foreign currency loans (Daily Monitor)

Financial experts have warned Small and Mid-Sized Enterprises under the Top 100 Mid-Sized Companies Club 2015 against taking foreign currency loans due to the lower interest rates than the Shilling. By mid this year, interest on foreign currency loans averaged 8.11%, much lower than the 23% charged on Uganda Shilling loans. According to Bank of Uganda between February and April, there was growth in foreign currency denominated loans rebounded by 1.2% from minus 2.3%.

BRICS meet on trade arbitration mechanism (Business Standard)

Finance Minister Arun Jaitley will inaugurate BRICS conference here on arbitration on August 27 which will deliberate on ideas and insights regarding dispute resolution mechanism among the 5 emerging nations that form the group. As a lead up to the BRUCS Summit, India has initiated a number of events within the spirit of the BRICS, one of which being the Conference on 'International Arbitration in BRICS: Challenges, Opportunities and Road ahead', the Finance Ministry said in a statement today. The conference brings together national and international experts from BRICs countries in the field of international arbitration, with an aim to assess, evaluate and debate ideas and insights regarding dispute resolution mechanism and arbitration which are integral to economic growth and stability, it said.

Kenya creates ministerial committee to implement WTO's Bali treaty rules (Xinhua)

"We have a committee of 52 Heads of the State agencies including the Kenya Ports Authority, the Kenya Revenue Authority and Kentrade - a newly formed state company tasked to work towards the harmonization of trade," Kiptoo told Xinhua. "The trade ministry is working towards making the committee a formal state body through a ministerial gazette notice, which would give it the legal powers to start work," he said. Kiptoo said Kenya urgently needs to close a huge trade deficit, caused by the rise in import volumes, currently valued at $10bn against the export volumes, currently valued at $6bn. "We need an exports strategy which we hope to launch very soon. This policy is based on an international trade policy which will be approved by the Cabinet. The Council of Governors is currently being consulted on this. Once this is done, we shall roll out the trade remedies bill, which aims to stop export dumping," Kiptoo said.

COMESA, Egyptian Competition Commissions sign agreement (CCC)

The COMESA Competition Commission has concluded a Cooperation Framework Agreement with the Egyptian Competition Authority regarding the application and enforcement of the COMESA Competition Regulations. The agreement is expected to facilitate and promote coordination between the Commission and the ECA in the harmononization and implementation of their competition laws and policies and lessen the possibilities or impact of divergent outcomes. The salient issues that the Cooperation Framework Agreement cover include:

Rwanda to host first COMESA investment summit (Rwanda Eye)

The summit will be the first edition of the Global African Investment Summit of COMESA. The summit is expected to attract over 1,000 public and private sector leaders representing US$200 billion of funds and with an interest in the investment, trade and business opportunities arising in the region. [Next week: AITEC Banking & Mobile Banking COMESA 2016 Forum]

Mauritius to hold 2016 Africa Partnership Conference (Concord Times)

Following the success of the Mauritius Africa Partnership Conference in 2014, the Board of Investment will be hosting the Africa Partnership Conference 2016 in collaboration with the World Association of Investment Promotion Agencies from 20-21 September. [Programme]

Nigeria approves 3-year budget plan, projects low growth in 2019 (Premium Times)

“Let me share with you some of the key parameters and assumptions which will be underpinning the 2017-2019 MTEF. Oil price benchmark: We intend to use 42.50 dollars as reference price in 2017. We are projecting 45 dollars in 2018 and 50 dollars in 2019. So, we are keeping to the very conservative in terms of the reference price of crude oil, even though we are expecting it to go higher than this. But, we are keeping to an extremely conservative price scenario. In terms of oil production, we are keeping to the same level of this year for 2017 and that is 2.2 million barrels per day. For 2018, 2.3 million barrels per day; and for 2019, 2.4 million barrels per day. In terms of growth rate, we are targeting 3% growth rate in 2017 and 4.26% growth rate in 2018 and a 4.04 per cent growth rate in 2019. [Only 10 million Nigerians pay taxes, says tax review panel]

Egypt cannot afford to postpone tough economic reforms: Sisi (Ahram)

There is no time to postpone economic reforms that should have been put in place years ago, Egypt's President Abdel-Fattah El-Sisi said in a lengthy, three-part interview with the editors in chief of Egypt's state-owned newspapers. El-Sisi said that there needs to be a distinction between Egypt’s economic reform programme and the IMF accord, elaborating that it was not acceptable for Egypt to have a "guardian" that dictates how the country should go about improving its economic situation. [Africa’s next big devaluation is seen unfolding in Egypt]

Namibia: Towards a logistics hub for Southern Africa (SAIIA)

This paper uses FDI in Namibia’s logistics sector as a case study to investigate these issues. Logistics development is identified as a priority for inclusive economic growth in Namibia, with a focus on the Port of Walvis Bay and its associated transport corridors. FDI has played an integral role in the construction and operation of the port and the transport corridors. [The analyst: Mark Schoeman] [Botswana Roads Design Manual update]

Dar, Lusaka review legal hitches to revitalise TAZARA (Tanzania Daily News)

The Tanzania and Zambian governments are reviewing Tanzania-Zambia Railway Authority Act of 1995 to allow private investments in the joint-owned railway and make it run commercially. Addressing stakeholders of TAZARA in Dar es Salaam yesterday during a trilateral cooperation of Zambia, Tanzania and China to mark 40th Anniversary of the authority, Assistant Director in the Department of Monitoring and Evaluation from the Ministry of Works, Transport and Communication, Mr Aunyisa Meena, said undergoing reforms and amending TAZARA act were inevitable if the authority is to remain relevant in the cut-throat competition in the market.

Car makers flag SA as base for drive into Africa (Business Day)

This explains why SA-based car companies are at the forefront of a new organisation, the African Association of Automotive Manufacturers. "The aim is promoting a policy environment that is conducive to the development of the automotive sector," says Jeff Nemeth, AAAM chairman and president and CEO of Ford sub-Saharan Africa. Nemeth is in Nigeria for meetings with President Muhammadu Buhari as well as representatives of the country’s National Automotive Design and Development Council and its National Automotive Manufacturers Association. But there is one country that SA might need to be aware of. "There is a lot of noise coming out about Morocco," says Messaris. "There has been lots of investment." Morocco increased its automotive production 24.3% in 2015 to a total of 288,329 vehicles. It is now the second-largest automotive manufacturing country in Africa after SA.

Algeria's trade deficit up 27% yr/yr in January-July (Reuters)

The importance of mapping tech hubs in Africa, and beyond (World Bank Blogs)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

Africa is on the ascent and Singapore must ride this wave, says Tharman

Singapore is ideal Asian gateway for African firms; DPM also points to policy failures in advanced world as reason for globalisation’s bad rap

Globalisation has earned itself a “bad reputation” because of policy failures in the advanced world, and Deputy Prime Minister Tharman Shanmugaratnam believes this sort of negative narrative around globalisation should have no place in either Asia or Africa.

At the opening of the Africa-Singapore Business Forum on Wednesday, he cautioned Asia and Africa – the world’s biggest sources of consumption growth over the next few decades – against echoing the type of anti-trade and anti-globalisation sentiment that’s being felt elsewhere.

“Globalisation still has many miles to go as far as our regions are concerned, and we should avoid getting too taken by this negative narrative coming out of Europe and the US, that comes out of policy failures,” he said.

Mr Tharman, who is also Coordinating Minister for Economic and Social Policies, was the guest-of-honour at the opening of the biennial conference organised by International Enterprise (IE) Singapore.

With trade and investment central to integrating the economies in Africa and Asia, he called for greater cooperation from both sides to work on good projects together and make them successful.

The Singapore government is already busy spreading its wings further across Africa, with Industry Minister S Iswaran signing new bilateral agreements with Mozambique, Ethiopia and Nigeria at the start of the forum.

More than 60 Singapore companies, including water-solutions provider Hyflux and shipping firm Pacific International Lines, are operating across more than 50 African countries, and counting.

The latest available figures show that bilateral trade between Singapore and Africa has grown at a compounded annual growth rate of 5.2 per cent since 2005, reaching S$11.5 billion last year; as of end 2014, Singapore’s cumulative direct investments into Africa stood at S$22.1 billion.

During the hour-long dialogue at the Grand Copthorne Waterfront Hotel, Mr Tharman made the point that Singapore has to build stronger links with Africa, India and the rest of the emerging world; he explained that a more diversified strategy builds resilience and would help the country weather the speed bumps in the global economy.

Overall, he expressed optimism about Africa’s prospects, describing the continent as one with huge potential, many opportunities and a sense of enterprise.

“We’ve got to be part of that opportunity. Africa is on the move,” he said.

Mr Tharman also made a pitch for Singapore’s strengths and advantages, urging African companies to use the Republic – a key financial centre and logistics hub – as a base to expand into the rest of Asia.

“We are a convenient base with regard to logistics and the orientation of our businesses and people, and African companies based here have found it to be an advantage to their expansion into Asia,” he said.

More African businesses are also eyeing Singapore as the ideal city to site their overseas offices.

Addressing the 450 delegates at the forum earlier, IE Singapore chief executive Lee Ark Boon said that Africa’s largest manpower staffing company, Adcorp Holdings, had recently announced that Singapore would be the headquarters for its “rest of the world” operations.

He said that his agency anticipated and welcomed more firms from Africa to establish themselves in Singapore and grow their Asian footprint.

Mr Tharman said Singapore can offer its vast experience in infrastructure planning and development, as well as the country’s “relentless focus” on skills upgrading and ensuring workers here can progress from basic to specialised skills.

He added that Singapore is useful to others because of its expertise on both Asia and Africa, and the emerging regions in general.

“The expertise is in the businesses themselves, it’s in the community of analysts, it’s also in the risk-management community, which is in Singapore. So we concentrate expertise, we provide financing and we have a safe, predictable environment for businesses to base their operations for the long term,” he said.

“That’s our role, we try to foster businesses and foster deals, even if we are not the originators of the deals.”

While Singapore will do what it can to share its knowledge and work with companies and governments abroad, it does have its limitations sometimes, Mr Tharman said.

“We have to be honest about the scale of our ambition. We are small. What we can do, we will do as well as we can.”

Related News

A growing logistics industry in Africa represents opportunities for Middle East investors and experienced developers

The logistics sector is a growing focus for property development in Sub-Saharan Africa, on the back of rising demand for modern warehouse space from retailers and consumer goods manufacturers. This trend is being driven by the growth of the region’s middle classes, the expansion of its consumer markets and the increased prevalence of mobile retailing.

“As Sub-Saharan Africa undergoes a wave of modern commercial property development, the logistics sector is emerging as a focus for activity. Already some leading Middle Eastern developers have targeted the sector; Kuwaiti based Agility has ambitious plans to create a network of logistics hubs across Africa, while Dubai’s DP World has been granted a concession to develop and operate a new logistics centre in Kigali, Rwanda,” says Andrew Marshall, Senior Surveyor in Logistics, at Knight Frank Middle East.

“GCC countries such as the United Arab Emirates and Saudi Arabia have gained global prominence with their world-class infrastructure and transport systems. Combining their strength in developing high-spec warehousing and sophisticated infrastructure, with the growth potential that the African logistics market offers, the opportunities cannot be emphasized enough. We realise however that for this to materialise, efforts need to focus on improving security, increasing transparency and combating corruption, along with establishing robust legal frameworks,” says Dana Salbak, Associate Partner and Head of Research, at Knight Frank Middle East.

Sub-Saharan Africa’s emerging logistics property sector

Modern logistics property is currently scarce across much of the Sub-Saharan region, but there is a growing need for high quality new development.

According to Knight Frank’s Logistics Africa 2016 report, there is rising demand for high quality logistics space from retailers and consumer goods manufacturers seeking to expand their African operations and improve distribution networks and supply chains. Such occupiers demand properties built to high technical specifications that support modern retailing, distribution and manufacturing practices.

Highlights from the report include:

-

Developers active in the logistics sector include those from the Middle East and China, as well as South African developers seeking to transfer their expertise to the rest of Africa.

-

Africa’s poor transport infrastructure although a major challenge for logistics operators, presents a real opportunity on the back of the numerous large-scale projects across Africa which aim to improve transport networks.

-

Drone technology has the potential to help logistics operators overcome transport infrastructure challenges, and several projects are underway exploring the use of drones in Africa.

-

Future demand for logistics property will be shaped by the rapid growth of online retailing in Sub-Saharan Africa, which is being driven by the increased penetration of smart mobile devices. The African online retail sector is forecast to be worth US$50 billion by 2018, representing a six-fold increase in value in the space of five years.

-

Around 90% of Africa’s trade happens by sea, making its ports crucial locations in logistics networks. Several major new ports are under construction across the continent and sites near to ports are highly desirable for logistics property development.

Transport infrastructure challenges

Overcoming Africa’s poor transport infrastructure is a major challenge to logistics operators.

Poor transport infrastructure is an inhibitor to the growth of many African logistics markets, with road and rail links between key economic hubs remaining patchy. Although there is a Trans-African Highway network, first conceived by the United Nations Economic Commission for Africa in the 1970s, large parts remain unbuilt and many sections are in poor repair and essentially unusable as trade routes. The cost of moving goods in Africa is, on average, estimated to be two or three times higher than in developed countries and transport costs can represent as much as 50-75% of the retail price of goods. The poor quality of road and rail networks forces logistics companies such as DHL Express to transport the majority of its cargo by air.

There are numerous large-scale transport infrastructure projects currently underway across the continent, which should help to improve transport connectivity within Africa. Current major projects include the East African standard gauge railway which aims to connect Kenya, Uganda, Rwanda and South Sudan, and the West Africa rail loop connecting Côte d’Ivoire, Burkina Faso, Niger, Benin, Togo and Nigeria. However, infrastructure improvements will struggle to keep pace with the astonishing speed at which Africa’s cities and economies are growing.

Innovative solutions have been proposed to overcome Africa’s challenging transport infrastructure. There are, for example, projects underway exploring the use of cargo drones. Foster + Partners has unveiled plans for a droneport in Rwanda, which would be used to transport medical supplies and commercial goods via unmanned flying vehicles. Drones could allow logistics operators to move goods to locations without reliable road networks and may prove to be a “leapfrog” technology for Africa, in the same way that mobile telecommunications have allowed many Africans to skip fixed-line networks and move straight to wireless technology.

Port developments

Around 90% of Africa’s trade happens by sea, making its ports crucial points in logistics networks.

Despite its reliance on sea transport for international trade, Sub-Saharan Africa’s ports are small by global standards. Durban, the region’s busiest container port, handles approximately 2.7 million twenty-foot equivalent units (TEUs) per year, less than one-thirteenth of the volume handled by the world’s busiest port Shanghai. Over the coming decades, the ports of Sub-Saharan Africa will require substantial expansion and modernisation in order to cope with the greater trade volumes that should accompany its population growth and economic development.

There are currently a large number of port development projects proposed or under construction across Sub-Saharan Africa, involving both the expansion of existing facilities and the creation of entirely new ports. Five of the largest new port schemes are highlighted on the map to the right. A common feature of many of these projects is the involvement of Chinese firms, whether as investors financing the projects or contractors building them. The most ambitious of the new port schemes aim to become the dominant ports within their regions; for example, the new ports at Lamu in Kenya and Bagamoyo in Tanzania are being positioned to compete with existing ports at Mombasa and Dar es Salaam to be the largest in East Africa.

Port locations are important hotspots for logistics operators and property developers in Sub-Saharan Africa. It is logical for firms building distribution networks in African countries to locate their logistics hubs near to ports, especially given the time and cost involved in transporting goods to inland commercial centres.

Online retail and modern supply chains

The growth of online retail markets will influence future demand for logistics property in Africa.

The rise of retail e-commerce, which is currently estimated by the research house eMarketer to be a US$2 trillion global industry, has shaped logistics property markets worldwide over the last decade. International retailers have increasingly demanded properties suited to the efficient fulfilment of online orders. However, online retail is a still a nascent sector in much of Africa; even in South Africa, the most sophisticated retail market in the Sub-Saharan region, online sales are only just expected to reach 1% of the overall retail market in 2016. This is a threshold which was passed more than a decade ago in many developed markets.

While small by global standards, Africa’s online retail sector has started to grow at a fast pace, driven primarily by the increased penetration of smart mobile devices into the continent’s markets. Sub-Saharan Africa is the fastest growing mobile phone market in the world, with GSMA Intelligence estimating that the number of unique mobile subscribers reached 381 million in 2016. Mobile users in Africa are increasingly migrating to smart devices, as these become more affordable. GSMA estimates that smartphone connections represented 23% of total mobile connections in Africa in 2015, but they are forecasted to be the majority by the end of the decade.

Mobile phones are the most prevalent communications technology in Africa, with consumers using them for tasks that might be more commonly performed on laptops or desktop computers elsewhere in the world. Mobile banking has been embraced by African consumers, and many online retailers receive the majority of their orders via mobile phones. The growth of smartphone usage across Africa will support the continued rise of online retail activity; Frost & Sullivan forecasts that e-commerce in Africa will be worth US$50 billion in 2018, up from US$8 billion in 2013.

Related News

Organic farming in Africa has rich potential, but is increasingly underfunded

Organic farming offers an excellent and lucrative export opportunity for Africa, but access to finance is harder to come by than five years ago, an UNCTAD survey has found.

An example of the opportunity comes from an East African regional programme, which saw the region’s organic exports grow from $4.6 million in 2002/03 to $35 million in 2009/10, according to the International Federation of Organic Agriculture Movements. The programme led to a common regional organic standard and significantly increased crop yields in Burundi, Kenya, Rwanda, Uganda, and the United Republic of Tanzania.

Despite such success stories, almost a quarter (23%) of organic farmers, exporters, and experts from 16 African countries said they felt that access to financing had become more restrictive in the last five years.

The results were published by UNCTAD in a new technical paper on financing organic farming in Africa. In the same survey, 64% said the situation had not changed while just 13% said access to funding had improved.

“Based on our survey, the most critical areas in terms of the need for external funding highlighted by stakeholders in organic agriculture were certification, the organization of smallholder farmers into production groups, marketing, and the purchase of equipment,” Malick Kane and Henrique Pacini wrote in the report.

“Unfortunately these are precisely the areas for which respondents said financing was becoming scarcer,” added Mr. Kane.

Funding for Africa’s agriculture in general has come under pressure in recent years, falling to an average of 2.7% of national budgets in 2013 according to the Food and Agriculture Organization of the UN. This happened despite a 2003 African Union commitment to allocate 10% of national budgets to this area. Also, the share of commercial credit made available for agriculture in Africa fell to an average of 2.8% in the same year, while the global average is 5.8%.

Specialist organic farmers looking for financing have seen knock-on effects, despite the premiums they can charge to export their goods to lucrative rich markets.

“With regard to price premiums, significant variations have been recorded depending on the commercialized crops, periods and markets,” Mr. Pacini said, but based on available estimates, premiums for organic products can range from 10% to 100% (or more) of the price of conventional varieties.

“These premiums play an important role in the profitability of organic crops as they compensate for additional costs incurred by organic farmers, such as those arising from compliance to organic practices and certification,” he said.

While established organic exports like coffee and cocoa benefit most from the access to finance, the UNCTAD paper notes that crops like organic pineapples, mangoes, bananas and even potatoes have enormous export potential.

“Our work highlights the fact that limited credit-guarantee mechanisms and insufficient capacity of commercial banks to integrate the specifics of organic agriculture are major hindrances on the ability of organic farmers and exporters to finance their activities in Africa,” said Mr. Kane.

Mr. Pacini added: “In view of the current situation, we strongly advocate for a coordinated effort to improve the data collected about both the domestic and export value of organic products so that a better business case for organic agriculture can be made in Africa”.

Related News

‘Time for a policy reset’: Taking a closer look at recent African economic trends

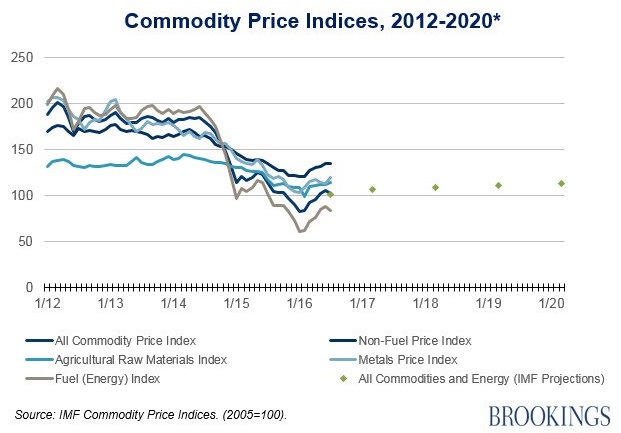

Commentary around recent developments in the economies of sub-Saharan Africa has centered on a trifecta of threats: low commodity prices, China’s slowdown, and the rising cost of external borrowing.

The region’s robust growth over the 2000-2014 period, analysts say, is slowing down. Commodity exporters in particular are confronting an array of macroeconomic challenges – from growing fiscal deficits to inflation and currency volatility. But do these discouraging trends signal an end to Africa’s rise? Should African governments, businesses, and economists prepare themselves for continued stagnation in the years ahead?

According to the International Monetary Fund (IMF), no. In fact, this is the opportune time for reflection and change, Director of the IMF’s Africa Department Antoinette Sayeh argued at a recent Brookings event launching the IMF’s Regional Economic Outlook for sub-Saharan Africa. As debates on the right mix of policies to address these shocks remain ongoing, Sayeh and panelists Steven Radelet, nonresident senior fellow at Brookings, and Amadou Sy, director and senior fellow of the Brookings Africa Growth Initiative, provided their views on the most effective strategies to respond to the commodity slump, increase financing in African countries, and leverage new sources of revenue.

Commodity shocks undermine growth

In an April 2016 research paper, “Growth in Sub-Saharan Africa: The Role of External Factors,” Brookings Senior Fellows Amadou Sy and Ernesto Talvi emphasize that understanding the external economic environment – and specifically, building up safeguards against future shocks – is vital to maintaining robust economic growth in sub-Saharan Africa. Based on an analysis of the region’s seven largest economies, they find that “almost half of sub-Saharan Africa’s output fluctuations since 1998 can be explained by a small set of external factors – namely, GDP growth in G-7 countries, GDP growth in China, oil and non-oil commodity prices, and borrowing costs for emerging economies in international capital markets.”

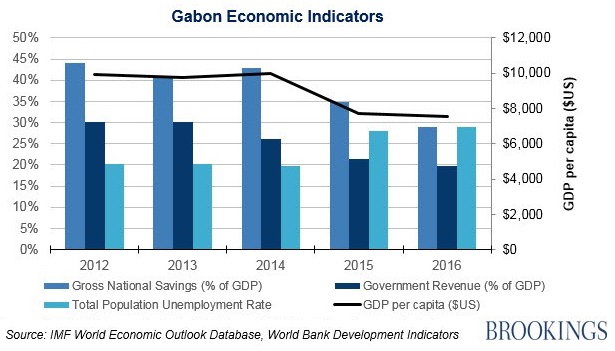

Indeed, Sayeh emphasized the magnitude of dropping commodity prices on many countries (Figure 1): Oil exporters like Angola, Republic of Congo, Equatorial Guinea, and Gabon experienced a decline in their commodity terms of trade ranging between 25 percent to 45 percent of GDP since 2011. Metal exporters have similarly taken a major hit. In the end, she argued, a scenario of “lower for longer” – or rather, no immediate rebound from the oil price slump – will be the case going forward.

Source: IMF

Yet low oil and other commodity prices have not hindered growth across the board in sub-Saharan Africa, Sayeh noted. For example, non-resource-rich countries have not experienced the same dip in growth as in their resource-rich neighbors (Figures 2 and 3). Oil importers such as Côte d’Ivoire, Kenya, and Senegal have actually seen a reduction in their energy import bill and are generally faring better than oil exporters, as a result of the price slump.

Source: IMF

Still, resource-rich countries, the IMF report stresses, require a “robust, prompt policy response,” including fiscal adjustment and exchange rate flexibility, to preserve macroeconomic stability. For countries outside of currency unions, allowing currencies to depreciate and exchange rates to absorb the shock can help limit the impact on growth. Countries in currency unions, on the other hand, do not have the exchange rate tool at their disposal and should make event greater efforts at fiscal consolidation, by limiting spending and avoiding excessive monetary financing. Meanwhile, non-resource-rich countries should use this boon of low oil prices to build buffers for softening future shocks.

Costs of financing increases

Just as the need for financing has increased – to fill the mounting fiscal gaps among commodity exporters – African frontier markets are facing “substantially tighter global financial conditions,” Sayeh noted. Investors are demanding higher risk premiums from the region’s borrowers with greater vulnerabilities. According to the IMF, the average sub-Saharan Africa bond spread is far higher than the emerging market group’s spread (Figure 4). This is largely driven by a few of the hardest hit commodity exporters (Gabon, Ghana, Nigeria, Tanzania, and Zambia, to name a few). On the other hand, sovereign bond spreads of net oil importers Côte d’Ivoire, Kenya, and Senegal have remained relatively stable, given their greater resiliency to the drop in oil prices.

Source: IMF

Domestic resource mobilization

Finally, Sayeh also recognized that many African countries are still missing out on an important source of revenue: domestic resource mobilization (see Figure 5). In the run-up to the Third International Conference on Financing for Development (FfD) in Addis Ababa last year, Sy argued a similar point. Despite improvements in government revenue collection mechanisms, tax collection in the region remains below what it should be. Sayeh recommended that African countries focus on “expanding both the tax base and tax compliance… with a view to not overburdening a given category of tax payers.”

Source: IMF

Similar calls for increasing domestic resource mobilization are echoing across the continent. In February of this year, at a Brookings private event, former President Thabo Mbeki of South Africa and the High-Level Panel on Illicit Financial Flows from Africa discussed how illicit financial flows from Africa are one of the biggest hindrances to domestic resource mobilization. As one discussant pointed out, strengthening the capacity of African countries’ tax administrations would help make taxes harder to evade.

Moreover, some participants at the February event noted that governments should re-examine their tax systems to ensure that they do not unduly impact the poor and ultimately exacerbate inequality in some of the poorest and most unequal countries in the world. Oxfam International Director Winnie Byanyima in a January 2016 Africa in Focus post argued that tax systems in Africa are particularly regressive – which disproportionately affect poor people – with indirect taxes such as value-added tax making up on average 67 percent of tax revenues in sub-Saharan Africa. Byanyima points out that governments and their multilateral partners should promote more progressive and efficient forms of taxation, contending that “governments can both raise and spend more progressively.”

Related News

BRICS meet pledges to work for inclusive growth

Call for greater role of their respective countries in global bodies

A two-day conference of the BRICS Women Parliamentarians’ Forum ended here on Sunday with a call for women’s involvement in the development process for ensuring inclusive growth.

Lok Sabha Speaker Sumitra Mahajan said the governments should strengthen innovative partnerships with civil society groups to assess effectiveness of their development initiatives.

Conflicting views too

While discussing the strategic partnership among the BRICS countries, the delegates stressed the need for greater role of their respective countries in the global bodies and strategies for combating global terrorism.

Some conflicting views emerged in the plenary session on “Perspectives on implementation of sustainable development goals (SDGs)”.

When Wen Ma, head of the Chinese delegation and member of standing committee of National People’s Congress of China, called for her country’s bigger role in international affairs, proportionate to its “clout”, the Indian side retorted by affirming that New Delhi too had enough clout and it deserved membership of the Nuclear Suppliers Group (NSG).

China has been opposing India’s membership in the elite 48-nation NSG, leading to strained relationship between the two countries.

Even as the delegates from other countries stayed back to get a taste of Rajasthani hospitality, the Chinese delegation left for Delhi immediately after the valedictory session.

According to official sources, the Chinese delegates, including Ms. Wen Ma and Lu Sai Xia, were scheduled to fly from Delhi to Guangzhou in China late on Sunday night.

In her concluding remarks, Ms. Mahajan said the active involvement of women parliamentarians would result in a greater responsiveness towards citizens’ needs and lead to “greater harmony, meaningful development and inclusive growth.”

The Lok Sabha Speaker laid emphasis on inclusiveness in development to make it sustainable and effective and said the role of legislations to achieve sustainable development was equally significant. “Development must be inclusive if it is to be equitable, sustainable and effective,” she said.

Referring to SDGs, Ms. Mahajan said that as lawmakers, it was the responsibility of women parliamentarians to oversee and monitor the implementation strategies and mechanisms of the targets put in place by their respective governments.

She called upon the delegates to learn from best practices in the BRICS member-countries to deal with the effects of climate change and to promote women’s welfare. She cited the initiatives and action plans taken up in Brazil, Russia, China and South Africa for fostering an environment favourable for women’s growth.

In her valedictory address, Rajasthan Chief Minister Vasundhara Raje said the BRICS could play a catalytic role in forging partnership among women lawmakers for mainstreaming SDGs. All member-countries of the BRICS had large populations, making it imperative that the development processes were sustainable, she said.

A Jaipur Declaration adopted on the conclusion of the conference stated the pledge of women parliamentarians to work together in the fields of economic growth, social inclusion and environment protection by intensifying mutual cooperation and strengthening strategic partnerships.

Related News

SA Renminbi usage up 65%

Strong trade links with China driving Renminbi uptake, says SWIFT.

Renminbi usage for payments in South Africa has increased by 65% over the last 12 months and by 112% over the last 24 months, says global financial messaging services firm SWIFT.

According to the firm, renminbi payment messages, excluding domestic traffic, increased by 70% over the past 12 months. SWIFT data also shows that nearly 40% of renminbi payments by South African firms have been offshore payments, exchanged with countries other than China and Hong Kong, up from 16% in July 2015.

“The renminbi, in general, has had huge uptake over the last few years for two reasons. One is trade with China – they are a major player in the commodities market. The second is due to the Chinese desire to make the renminbi a world leading currency, in line with their own status as the second largest global economy. In broad terms you’d expect it to follow closely behind the dollar and euro just based on trading bloc size,” Harry Newman, head of banking at SWIFT told Moneyweb.

Newman added that South Africa’s strong trade links with China as well as the establishment of a domestic Renminbi clearing centre along with Singapore’s increased use of the renminbi for payments has stimulated usage of the currency.

“South Africa trades a lot with China, though sometimes this isn’t entirely evident. Just because trade doesn’t go directly to China doesn’t mean it isn’t trade with China. It might go through another location first, for example Singapore which is a shipping hub, but ultimately is trade with China,” he said.

Although Chinese demand for some South African commodities has fallen from historic highs, Newman said the currency in which invoices are billed could explain the increase in renminbi usage. If more invoices are paid in renminbi then the volume of renminbi payments will grow even if the trade remains the same, he said.

“There are also a few reports of some companies offering small discounts for payment in renminbi, which would of course encourage people to switch as well,” he added.

SWIFT expects the Memorandum of Understanding on the Promotion of China-Africa Cooperation, signed during the Forum on China-Africa Cooperation in Johannesburg in December 2015, to increase commercial exchanges between China and countries in Africa and have a positive impact on future renminbi volumes.

As at July 2016, the renminbi was the fifth most active currency for global payments, with a market share of 1.9%, SWIFT said.

RMB continues to penetrate the South African market

SWIFT’s RMB Tracker shows that RMB usage across South Africa has more than doubled in volumes over the past two years

SWIFT data shows that Renminbi (RMB) usage in payments in South Africa increased by 65% over the last 12 months and by 112% in the last two years, moving the country from position #30 in July 2014, to #24 in July 2016. Excluding domestic traffic, RMB payment messages increased in volume by 70% in the last 12 months. In addition, nearly 40% of RMB payments by South African institutions have been offshore payments exchanged with countries other than China and Hong Kong, compared to 16% in July 2015.

“South Africa has experienced a major shift in RMB growth over the last two years, strengthening the country’s trade relations with China and Hong Kong,” says Harry Newman, Head of Banking, SWIFT. “The establishment of an RMB clearing centre in South Africa in July 2015, as well as Singapore’s increased use of the RMB for payments with South Africa, have been a catalyst for RMB growth in the region.”

During the Forum on China-Africa Cooperation, held in Johannesburg in December 2015, China and representatives from50 African countries agreed to actively implement a Memorandum of Understanding (MoU) on the Promotion of China-Africa Cooperation in the area of infrastructure (fields of railway, highway, regional aviation networks and industrialisation). They will give priority to encourage Chinese businesses and financial institutions to expand investment through various means, such as Public-Private Partnerships (PPP)[1]. This MoU will increase the commercial exchanges between China and the African continent and should positively impact RMB volumes in the future.

In July 2016, the RMB bounced back to its position as the fifth most active currency for global payments by value with a share of 1.90%, a slight increase from 1.72% in June 2016. Overall RMB payments value decreased by 0.68% compared to June 2016, whilst in general all payments currencies decreased by 10.08%.

[1] Source: Ministry of Foreign Affairs of the People’s Republic of China, http://www.fmprc.gov.cn/mfa_eng/zxxx_662805/t1323159.shtml

![]()

![]()

Related News

tralac’s Daily News Selection

The selection: Wednesday, 24 August 2016

Looking ahead: the First African Forum for National Trade Facilitation Committees (UNCTAD)

UNCTAD will organize the first African Forum for National Trade Facilitation Committees from 17-21 October in Addis Ababa. The meeting aims at: (i) bringing the opportunity to NTFCs all over the African continent to share best practices; (ii) providing a platform to discuss existing challenges and opportunities for the future growth of NTFCs; (iii) empowering the leaders of African NTFCs. The event will also hold parallel sessions on the particular role of the private sector and Customs in the NTFC.

African Union Commission: financial report and audited financial statements for the year ended 31st December 2014 (pdf)

Kumi Naidoo: African Civil Society Initiative, background

SADC Summit updates:

SADC reviews Secretariat organisational structure (SARDC): The Southern African Development Community is reviewing its organisational structure to ensure that it adequately responds to new and emerging issues in the region’s revised development blueprint. “Through a competitive selection process Ernst & Young was engaged in April 2016 to undertake the SADC Secretariat Organisational Structure and Infrastructure Review,” Mufaya told journalists on the sidelines of the meeting of SADC Standing Committee of Senior Officials ahead of the 36th Summit of SADC Heads of State and Government set for 30-31 August. He said the consultants commenced work in April and “their first draft report will be considered by Council (of Ministers)”, which will meet prior to the 36th Summit of SADC Heads of State and Government.

SADC Standing Committee of Senior Officials (SARDC): Outgoing chairperson of the SADC Standing Committee of Senior Officials, Dr Taufila Nyamadzabo concurred, saying deeper regional integration in southern Africa hinges on the implementation of agreed decisions. “It is important that we increase the pace of implementation and monitoring of our regional activities, programmes and projects,” said Nyamadzabo, who is the Secretary for Economic and Financial Policy in Botswana. Incoming chairperson of the SADC Standing Committee of Senior Officials, Bertram Stewart – the Principal Secretary for Economic Planning and Development in Swaziland – pledged to strengthen the push towards implementation of regional strategies.

Regional strategic action plan on integrated water resources development and management (2016-2020) (pdf): The RSAP IV is the implementation plan for the water component of the Regional Indicative Strategic Development Plan, a blue print of SADC programmes. It is also a strategic plan to implement the water chapter of the Regional Infrastructure Development Master Plan (RIDMP). To effectively respond to the region’s challenges, the RSAP IV proposes a suit of participatory and delivery approaches to water and services such a nexus approaches, indigenous knowledge-based solutions, disaster risk management-based systems, climate resilience building, blending both built and ecological infrastructural solutions, ground-surface water integrated planning and development and others. [Calming the waters: why we need to better integrate climate and water policy]