Search News Results

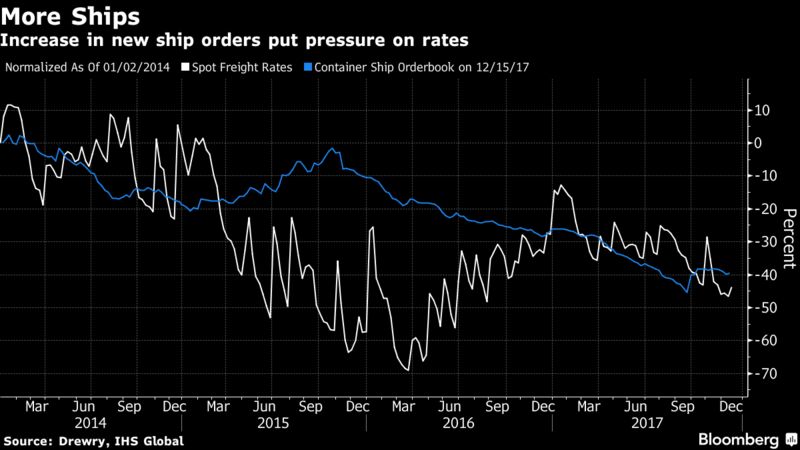

More mega-ships are a big problem for cargo carriers

Container shipping companies are bracing for a challenging year – they will have more space available for carrying goods than the amount of cargo that’s out there.

Corrine Png, chief executive officer of research firm Crucial Perspective, estimates freight-carrying capacity on container ships will rise 5.9 percent this year, outstripping demand growth for the first time since 2015.

That’s largely because more than 40 huge container vessels ordered at least two years ago are ready to be delivered for service, creating an abundance of ship stowage. With some of the space expected to be left empty, container lines could be forced to charge lower fees for shipping goods, even as they try to overcome years of accumulated losses in an industry downturn that has seen at least one company collapse.

More than 90 percent of global trade is transported by sea. The five charts below show what’s in store for shipping companies.

1. More space to carry goods

As more large vessels are delivered and put into service in 2018, ships’ cargo-carrying capacity is expected to expand the most in three years.

2. There could be more ships and even more stowage

Some container lines could take advantage of currently low shipbuilding prices to order more vessels, Png says. As history has shown, sea-freight fees tend to be squeezed when the ship orderbook expands, due to concern there will be an excess of space.

3. Asian and European buyers spend the most

Companies need to raise a combined $144 billion to take delivery of all vessels this year. Of that amount, 73 percent will come from buyers in Asia and Europe.

4. Bigger vessels will be in demand

Container ships are estimated to account for 98 of this year’s orders across vessel types and 120 for next year. Overall, the number of ships on order is expected to rise 54 percent to 662 this year and to 820 in 2019, said Park Moo-hyun, an analyst at Hana Financial Investment Co. in Seoul.

5. Most are crude oil and dry bulk ships

Crude tankers and dry bulk carriers make up more than 60 percent of total deliveries scheduled for this year, and container ships account for 19 percent. Hana Financial’s Park sees a “steady increase” in demand for large container vessels that can each carry more than 15,000 boxes.

Related News

Global economy to edge up to 3.1 percent in 2018 but future potential growth a concern

Current slack in global economy expected to fade

The World Bank forecasts global economic growth to edge up to 3.1 percent in 2018 after a much stronger-than-expected 2017, as the recovery in investment, manufacturing, and trade continues, and as commodity-exporting developing economies benefit from firming commodity prices.

However, this is largely seen as a short-term upswing. Over the longer term, slowing potential growth – a measure of how fast an economy can expand when labor and capital are fully employed – puts at risk gains in improving living standards and reducing poverty around the world, the World Bank warns in its January 2018 Global Economic Prospects.

Growth in advanced economies is expected to moderate slightly to 2.2 percent in 2018, as central banks gradually remove their post-crisis accommodation and as an upturn in investment levels off. Growth in emerging market and developing economies as a whole is projected to strengthen to 4.5 percent in 2018, as activity in commodity exporters continues to recover.

“The broad-based recovery in global growth is encouraging, but this is no time for complacency,” World Bank Group President Jim Yong Kim said. “This is a great opportunity to invest in human and physical capital. If policy makers around the world focus on these key investments, they can increase their countries’ productivity, boost workforce participation, and move closer to the goals of ending extreme poverty and boosting shared prosperity.”

2018 is on track to be the first year since the financial crisis that the global economy will be operating at or near full capacity. With slack in the economy expected to dissipate, policymakers will need to look beyond monetary and fiscal policy tools to stimulate short-term growth and consider initiatives more likely to boost long-term potential.

The slowdown in potential growth is the result of years of softening productivity growth, weak investment, and the aging of the global labor force. The deceleration is widespread, affecting economies that account for more than 65 percent of global GDP. Without efforts to revitalize potential growth, the decline may extend into the next decade, and could slow average global growth by a quarter percentage point and average growth in emerging market and developing economies by half a percentage point over that period.

“An analysis of the drivers of the slowdown in potential growth underscores the point that we are not helpless in the face of it,” said World Bank Senior Director for Development Economics, Shantayanan Devarajan. “Reforms that promote quality education and health, as well as improve infrastructure services could substantially bolster potential growth, especially among emerging market and developing economies. Yet, some of these reforms will be resisted by politically powerful groups, which is why making this information about their development benefits transparent and publicly available is so important.”

Risks to the outlook remain tilted to the downside. An abrupt tightening of global financing conditions could derail the expansion. Escalating trade restrictions and rising geopolitical tensions could dampen confidence and activity. On the other hand, stronger-than-anticipated growth could also materialize in several large economies, further extending the global upturn.

“With unemployment rates returning to pre-crisis levels and the economic picture brighter in advanced economies and the developing world alike, policymakers will need to consider new approaches to sustain the growth momentum,” said World Bank Development Economics Prospects Director Ayhan Kose. “Specifically, productivity-enhancing reforms have become urgent as the pressures on potential growth from aging populations intensify.”

In addition to exploring developments at the global and regional levels, the January 2018 Global Economic Prospects takes a close look at the outlook for potential growth in each of the six global regions; lessons from the 2014-2016 oil price collapse; and the connection between higher levels of skill and education and lower levels of inequality in emerging market and developing economies.

Global Economic Prospects: Sub-Saharan Africa

Recent developments

Growth in Sub-Saharan Africa is estimated to have rebounded to 2.4 percent in 2017, after slowing sharply to 1.3 percent in 2016. The rise reflects a modest recovery in Angola, Nigeria, and South Africa – the region’s largest economies – supported by an improvement in commodity prices, favorable global financing conditions, and slowing inflation that helped to lift household demand. However, growth was slightly weaker than expected, as the region is still experiencing negative per capita income growth, weak investment, and a decline in productivity growth.

Although oil producers in the region continue to deal with the effects of the earlier oil price collapse, growth rebounded moderately in metals-exporting countries, reflecting an uptick in mining output amid rising metals prices, while growth in non-resource-intensive countries – largely agricultural exporters – was broadly stable, supported by infrastructure investment and crop production.

Fiscal deficits narrowed slightly in 2017, the result of large spending cuts in some oil exporters. However, government debt continued to rise across the region compared to 2016, as countries borrowed to finance public investment.

Outlook

Growth in the region is projected to continue to rise to 3.2 percent in 2018 and to 3.5 in 2019, on the back of firming commodity prices and gradually strengthening domestic demand. However, growth will remain below pre-crisis averages, partly reflecting a struggle in larger economies to boost private investment.

South Africa is forecast to tick up to 1.1 percent growth in 2018 from 0.8 percent in 2017. The recovery is expected to solidify, as improving business sentiment supports a modest rise in investment. However, policy uncertainty is likely to remain and could slow needed structural reforms. Nigeria is anticipated to accelerate to a 2.5 percent rate this year from 1 percent growth in the year just ended. An upward revision to Nigeria’s forecast is based on expectation that oil production will continue to recover and that reforms will lift non-oil sector growth. Growth in Angola is expected to increase to 1.6 percent in 2018, as a successful political transition improves the possibility of reforms that ameliorate the business environment.

Non-resource intensive countries are expected to expand at a solid pace, helped by robust investment growth. Côte d’Ivoire is forecast to expand by 7.2 percent in 2018; Senegal by 6.9 percent; Ethiopia by 8.2 percent; Tanzania by 6.8 percent; and Kenya by 5.5 percent as inflation eases.

However, given demographic and investment trends across the region over the longer term, structural reforms would be needed to boost potential growth over the next decade.

Risks

The regional outlook is subject to external and domestic risks, and is tilted to the downside. Although stronger-than-expected activity in the United States and Euro Area could push regional growth up due to greater exports and increased mining and infrastructure investment, an abrupt slowdown in China could generate adverse spillovers to the region through lower-than-expected commodity prices.

On the domestic front, excessive external borrowing without forward-looking budget management could worsen debt dynamics and hurt growth in many countries. A steeper-than-anticipated tightening of global financing conditions could also lead to a reversal in capital flows to the region. Protracted political and policy uncertainty could further hurt confidence and deter investment in some countries.

Rising government debt levels highlight the importance of fiscal adjustment to contain fiscal deficits and maintain financial stability. Structural policies – including education, health, labor market, governance, and business climate reforms – could help bolster potential growth.

Regional Summaries

East Asia and Pacific: Growth in the region is forecast to slip to 6.2 percent in 2018 from an estimated 6.4 percent in 2017. A structural slowdown in China is seen offsetting a modest cyclical pickup in the rest of the region. Risks to the outlook have become more balanced. Stronger-than-expected growth among advanced economies could lead to faster-than-anticipated growth in the region. On the downside, rising geopolitical tension, increased global protectionism, an unexpectedly abrupt tightening of global financial conditions, and steeper-than-expected slowdown in major economies, including China, pose downside risks to the regional outlook. Growth in China is forecast to moderate to 6.4 percent in 2018 from 6.8 percent in 2017. Indonesia is forecast to accelerate to 5.3 percent in 2018 from 5.1 percent in 2017.

Europe and Central Asia: Growth in the region is anticipated to ease to 2.9 percent in 2018 from an estimated 3.7 percent in 2017. Recovery is expected to continue in the east of the region, driven by commodity exporting economies, counterbalanced by a gradual slowdown in the western part as a result of moderating economic activity in the Euro Area. Increased policy uncertainty and a renewed decline in oil prices present risks of lower-than-anticipated growth. Russia is expected to expand by 1.7 percent in 2018, unchanged from its estimated growth rate in 2017. Turkey is projected to moderate to 3.5 percent this year from 6.7 percent in the year just ended.

Latin America and the Caribbean: Growth in the region is projected to advance to 2 percent in 2018, from an estimated 0.9 percent in 2017. Growth momentum is expected to gather as private consumption and investment strengthen, particularly among commodity-exporting economies. Additional policy uncertainty, natural disasters, a rise in trade protectionism in the United States, or further deterioration of domestic fiscal conditions could throw growth off course. Brazil is expected to pick up to 2 percent in 2018, from an estimated 1 percent in 2017. Mexico is anticipated to accelerate to 2.1 percent this year, from an estimated 1.9 percent last year.

Middle East and North Africa: Growth in the region is expected to jump to 3 percent in 2018 from 1.8 percent in 2017. Reforms across the region are expected to gain momentum, fiscal constraints are expected to ease as oil prices stay firm, and improved tourism is anticipated to support growth among economies that are not dependent on oil exports. Continued geopolitical conflicts and oil price weakness could set back economic growth. Growth in Saudi Arabia is forecast to accelerate to 1.2 percent in 2018 from 0.3 percent in 2017, while growth is anticipated to pick up to 4.5 percent in the Arab Republic of Egypt in FY 2018 from 4.2 percent last year.

South Asia: Growth in the region is forecast to accelerate to 6.9 percent in 2018 from an estimated 6.5 percent in 2017. Consumption is expected to stay strong, exports are anticipated to recover, and investment is on track to revive as a result of policy reforms and infrastructure upgrades. Setbacks to reform efforts, natural disasters, or an upswing in global financial volatility could slow growth. India is expected to pick up to a 7.3 percent rate in fiscal year 2018/19, which begins April 1, from 6.7 percent in FY 2017/18. Pakistan is anticipated to accelerate to 5.8 percent in FY 2018/19, which begins July 1, from 5.5 percent in FY 2017/18.

Related News

Mozambique Economic Update: Making the most of demographic change

Mozambique is shifting to a period of slowing growth and increasing concentration. A stronger fiscal policy response and increased transparency are key for recovery, says a new World Bank report.

The second half of 2017 indicates the slowdown in Mozambique’s economic performance may be taking hold and shifting this once fast-growing economy to a more modest pace of growth, bringing economic growth down to a level barely above that of population growth.

GDP growth is expected to dip to 3.1 percent in 2017, despite increases in coal and aluminum exports. Whilst these exports boomed, small and medium enterprises (SMEs) have fallen back even more, especially in the manufacturing sector, which contracted for this first time since 1994.

The World Bank’s new Mozambique Economic Update (MEU) notes that small and medium enterprises (SMEs) are crowded out, and that not even the sizable growth of commodity exports is sufficient to counteract the effects this is having on the economy.

The level of concentration has also increased in 2017: Just a few commodities dominate exports, representing a larger share of foreign currency inflows, which heightens the country’s exposure to external shocks.

The concentration of output in the extractive and minerals sector keeps Mozambique on the path of a two-speed economy, one less capable of generating enough jobs to absorb a net inflow of the almost 500,000 people entering the labor force each year.

Trends observed in 2017 make it clear that Mozambique needs to double its efforts to support small and medium enterprises and look beyond the extractive sector for more balanced growth.

The scale of the shocks faced by Mozambique’s economy over the past two years has been immense. However, as commodity prices and conditions for agriculture improve, and external factors become less of an impediment, the economy turns to the policy response to pursue recovery. Decisive monetary policy measures and strong commodity export performances have helped to stabilize the Metical and bring inflation down in 2017. Fiscal policy also began responding, but at a slower pace.

Making the most of demographic change

In order to examine future demands on Mozambique’s economy, the special focus of December’s Economic Update discusses the challenge of transforming Mozambique’s growing and youthful population into a demographic dividend. This is ever more urgent given the drift towards a natural resource extraction based economy with low employment generation.

Mozambique lags behind other sub-Saharan African countries in kicking off its demographic transition. By 2011, its total fertility rate was estimated at an average of 5.9 children per woman, one of the highest in the world. The World Bank estimates that reducing fertility rates would represent an enormous boost to prosperity: an estimated increase in real per capita GDP of 31 percent by 2050.

“Transforming Mozambique’s population trends into a demographic dividend is an immense challenge, but so are the potential gains,” said Peter Holland, World Bank Program Leader for Human Development.

Mozambique could actively promote policies to trigger the transition, with jobs for women and better family planning services. A sharper focus is also needed on building skills for youth and an economy that grows.

The Update also calls for a sharper focus on building skills for youth, with particular emphasis again on women and an economy that grows whilst generating productive jobs for the next generation of Mozambicans.

Monetary policy

This report emphasizes that more needs to be done to stabilize the macroeconomic outlook and rebalance the policy mix with definitive fiscal policy measures. And, though monetary policy has been decisive, and contributed to stabilizing the currency at a critical time, it has also heightened the cost of credit.

Space is now opening for the monetary policy cycle to begin easing as inflation continues to fall, which would improve the private sector’s access to financing. This requires a tighter fiscal policy response and more sustainable levels of debt.

It would also require a more proactive approach to tackling the fiscal risks coming from weak state-owned enterprises, as well as necessitating increased transparency in the handling of the investigation into Mozambique’s hidden debts to restore both investor and donor confidence.

Related News

China’s impacts on SSA through the lens of growth and exports

The International Monetary Fund (IMF) points out three identified spillover channels through which China may influence the world economy: trade, external financing and commodity prices. This paper specifically quantifies China’s impacts on 44 sub-Saharan African (SSA) countries in an effort to identify the potential transmission channels.

The analysis reveals that (i) after joining the WTO in 2001, China has started to impact significantly on SSA growth: one-percent increase in China’s GDP per capita leads to 0.02 percent increase on the SSA’s GDP per capita; (ii) oil and investment-goods exporters benefit more from China’s growth; (iii) compared to China’s consumption, its investment growth acts as a more important channel in influencing SSA; (iv) exports to China, highly linked to China’s growth, is an important indicator for SSA’s exports.

Given the growing influence of China’s economy on SSA countries, it is urgent for SSA countries to be well prepared to better take advantage of China’s rebalancing, proactively search a sustainable way to continuously enhance productivity, and successfully integrate into the world value chain for industrial upgrading.

Introduction

China’s economic performance, since early 1980s, is phenomenal by various criteria, characterized by long-duration, high growth rate and world-wide spillover effects. The 36-year average growth rate of China’s GDP per capita is as high as 8.8 percent while the global economy experienced an average growth rate of 2.4 percent. The rapid economic expansion has made China’s economy more influential in the global economy and thus attracted more researchers’ attention.

Numerous papers have studied the growing economic power China has exerted at different economic aspects, on various regions or countries, and via various channels. Most of them assume that China’s spillover has increased proportionately with its economic output (or trade) without experiencing any structural break, but this may not be underpinned by observations especially when we consider a series of economic reforms and initiatives accompanying China’s growth which have amplified the magnitude of China’s global influence in an exponential way.

Exports from Sub-Sahara Africa (SSA) to China has increased dramatically in the past two decades, particularly after 2001 when China joined the WTO. Surpassing the US in 2012, China has become the second largest exporting partner of SSA only after EU. Is it possible that the magnitude of China’s impacts on SSA is significantly different before and after a certain time point around the year of 2002? While the paper does not infer any conclusion from the simple correlations of growth of GDP per capita, it notes that advanced economies, emerging markets, and the rest of the world have also experienced jumps in correlations with SSA.

Guided by these observations, the paper does not take for granted that China’s impacts on SSA remain structurally stable since 1980. Instead, the authors run regressions with different sample periods to check the existence of a structural break in China’s impacts. The regression results and economic intuition jointly direct the study to focus on the period of 2003 to 2015 due to the implied structural break stemming from China joining the WTO.

Given vast variation in economic characteristics among 44 SSA countries, it is meaningful to explore the implications of country heterogeneity on the degree of economic dependence on China. For example, iron-ore-exporting countries may heavily rely on China’s construction industry while SSA countries exporting cotton are likely to be sensitive to China’s domestic consumption. Accordingly, this paper divides SSA countries into groups following well-accepted criteria and investigates common features for each group.

Another interesting angle to gauge China’s impacts is to disaggregate China’s growth into consumption and investment to quantify the exact effects of China’s GDP components. This growth disaggregation also contributes to the study of what role SSA country heterogeneity play for China’s impacts just as mentioned in the paragraph above.

If China’s impacts on SSA are well quantified, a following question would be what the potential transmission channels are? how China influences SSA? In this context, the paper seeks to assess the traditional channels of trade and FDI by examining whether China-related variables are among the determinates of SSA’s total exports and exports to China.

In summary, the paper seeks to answer the following questions:

-

Is China’s economic growth significant for SSA growth? Does it evolve over time?

-

Does country heterogeneity play a role?

-

Which component of China’s GDP is more important: consumption or investment?

-

What role does Chinese economy play in SSA’s exports?

For China’s impacts on SSA’s GDP growth, the paper follows the setup of classic growth literature and adopt the difference GMM approach to address regressor endogeneity. This method can provide more reliable empirical results on China’s spillover to SSA, which is instrumental in policymakers’ understanding the potential economic implications of China’s rebalancing, namely lower growth rates accompanied by a shift from investment-driven to consumption-driven economic model.

The views expressed in this IMF Working Paper are those of the author(s) and do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

Related News

The role of trade policies in building regional value chains – some preliminary evidence from Africa

Regional value chains (RVCs) are considered as an important step towards greater integration into global value chains (GVCs), but African countries trade very little value added with each other. Trade in value added within the region is still by far the lowest in comparison with Asia and Latin America, but the recent increase allows for an optimistic outlook with respect to the evolution of regional production networks.

Based on the UNCTAD-Eora GVC database,[1] this paper estimates a panel model from 2006 to 2012 for 37 African countries and sheds light on the role of trade costs in building RVCs in Africa.

First evidence is provided on the effect of (i) charged and faced tariff rates on capital goods, raw materials and intermediates and (ii) additional trade costs capturing border inefficiencies and poor infrastructure. Results indicate a significantly negative effect on foreign value added of charged tariffs on capital goods and higher time to trade. In addition, higher regulatory quality and a stronger telecommunication infrastructure seem to be positively correlated with a country’s ability to participate in RVCs.

Introduction

International trade is increasingly shaped by the existence of value chains, regionally and globally. Decreasing transaction costs have encouraged multinational corporations to outsource stages of production, retaining the most profitable phases along the supply chain. More complex products and a greater division of labor allow more countries to participate in global trade by specializing in specific tasks without the need to produce the entire product. Developing countries can leverage participation in value chains as a stepping stone towards greater integration into the global economy which promises a rise in labor productivity and total factor productivity through knowledge spillovers and technology transfer.

African countries are highly under-represented in global value chains (GVCs) although their participation has significantly increased over the course of the last decade. The example of the great world factories in Europe, North America and Asia shows that building regional value chains (RVCs) is an important step towards participation in GVCs by increasing the market for exports and imports. However, the share of intra-African trade in value added is low at nine percent, compared to 45 percent in Asia and 18 percent in Latin America. Although it is essential to understand the dynamics and characteristics of RVCs in order to implement efficient policy instruments for facilitating regional trade in value added, the literature on RVCs in Africa is sparse.

To the best of the author’s knowledge there is no study which empirically explores determinants of RVCs in Africa. The study at hand attempts to close this gap in the literature. By doing this, the analysis builds on empirical literature on African global value chain participation on the one hand. Kowalski et al. (2015) and IMF (2016) are the only two publications that empirically address the determinants of African countries’ trade in value added with the world. On the other hand, sector- and country-specific literature on African regional value chains is discussed to show that a reduction of regional transaction and trade costs is even more crucial to increasing RVC integration than gross trade since products have to cross the border twice. This is theoretically underlined by the two-dimensional fragmentation model by Kimura (2007) which centralizes service link costs as a major constraint to the fragmentation of production processes. Service link costs arise by connecting production blocks and include trade and transportation costs, as well as economic transaction costs (e.g. telecommunication costs and deficiencies in legal systems and economic institutions).

This paper purely focuses on the role of trade policies in regional trade in value added within Africa. Policy makers are usually confronted with a set of trade policy instruments in the form of different tariff rates. High tariffs on important inputs such as production equipment might be more restrictive than tariffs on raw materials, especially for resource abundant countries. Despite recent integration efforts among African countries, intraregionally applied tariffs are still high compared to cases in Asia and Latin America. In addition, time delays caused by poor infrastructure and border inefficiencies restrict intra-regional trade. For trade in parts and components, delays in arrival are even more prevalent than for trade in finished goods since the full production process could be interrupted. In light of the potential Continental Free Trade Area (CFTA) which is currently negotiated, the aim of this study in identifying the impact of these constraints becomes highly relevant.

This study uses newly published international input-output tables, obtained from the UNCTAD Eora GVC database, to quantify trade in value added between African countries and to evaluate each country’s position in the RVC. The empirical analysis concentrates on the backward integration perspective, defined as imported foreign value added (FVA) from the region embedded in a country’s exports to the region. On average, 6.0 percent (in 2012) of the value added exports to African countries are also sourced from within the region.

Southern African countries such as Namibia, Botswana and Swaziland are considered to be the most integrated countries, mainly attributed to their proximity to the regional hub, South Africa. Moreover, all African countries, except South Africa, presently import more inputs from within region than they did in 2006. Between 2006 to 2012, real imported FVA increased by 114 percent while total value added trade increased by 53 percent. The stronger increase in FVA indicates a strengthening of regional production networks. The research question that naturally arises is why some African countries have experienced a stronger increase in value added trade and have managed to integrate into RVCs to a greater extent than other countries. Given the fact that imported foreign value added from the rest of the world is approximately zero, an analysis of trade diversion from third countries towards the region is not essential and allows a pure concentration on regional preferential trade liberalization.

An extensive literature review provides a theoretical framework for the empirical analysis. Qualitative literature on Africa, as well as examples from Asia and Latin America are particularly instructive in understanding the role of trade facilitation and structural factors in building RVCs. A panel of 37 African countries from 2006 to 2012 is estimated using a fixed-effects (FE) estimator, controlling for auto-correlation and cross-sectional correlation among standard errors. The results suggest that trade barriers are significant determinants of a country’s ability to join and upgrade within RVCs. Among different tariff rates, the charged tariff on capital goods is most restrictive to imported FVA. The proxies for non-tariff barriers (NTBs) also indicate a negative effect on RVC participation. In addition, higher regulatory quality and a stronger telecommunication infrastructure are positively correlated with the evolution of RVCs.

This paper was completed during an internship in the Division for Africa, Least Developed Countries and Special Programmes at UNCTAD.

[1] Environmental Accounting Framework Using Externality Data and Input-Output Tools for Policy Analysis

Related News

IMF Executive Board 2017 Article IV Consultation with Benin

On December 1, 2017, the Executive Board of the International Monetary Fund concluded the Article IV Consultation with Benin.

Benin showed mixed macroeconomic performance in 2016, with the economy weathering negative spillover stemming from a difficult external environment. Growth was about 4 percent, but a recovery is expected in 2017-18, owing to strong agricultural production, an increase in public investment, and a buoyant tertiary sector. Economic growth is accelerating and inflation remained negative in 2016 and through end-August 2017 but is forecasted to average 0.6 percent in 2017.

The medium-term outlook continues to show favorable signs, with high economic growth and low inflation. Cuts in recurrent spending have contributed to a smaller than programmed budget deficit of 6.0 percent of GDP in 2016 from 8.0 percent in 2015. The fiscal consolidation path foresees a further reduction of the deficit to 1.8 percent of GDP in 2019, below the West African Economic and Monetary Union convergence criterion of 3 percent of GDP.

Despite the favorable medium-term economic outlook, some challenges remain that need to be addressed going forward. These include prioritizing public expenditures to foster inclusive growth and to reduce poverty; accelerating the tax and customs administration reforms to mobilize more domestic resources; making public investment more efficient to sustain the expected growth over the medium term, addressing the rising burden of domestic debt service, and strengthening debt management to preserve public debt sustainability.

Staff Report

Strengthening the Pillars for a Structural Transformation of the Economy

Inclusive growth has been elusive. Following a decade of mediocre economic performance, growth over the last 3 years (2013-15) averaged 5.2 percent, closing the gap with the sub-Saharan Africa (SSA) average in per capita GDP growth However, this solid macroeconomic performance did not translate in a meaningful reduction in poverty, which remains a major challenge calling for a higher and more inclusive growth over the medium term. Low and stagnant productivity in the agriculture sector is the primary cause of the limited poverty reduction in rural areas.

The government is committed to structurally transform Benin’s economy by scaling up investment and diversifying the economy. On April 7, the Board approved the authorities’ request for a three-year arrangement under the ECF. Executive Directors underscored the importance of adhering to policies that preserve macroeconomic stability and public debt sustainability. At the time of the 2017 IMF/World Bank Annual Meetings, Benin became a full participant in the G20 Compact with Africa (CWA) Initiative in the hope of bolstering private sector financing of the Government’s Action Program (GAP), 2016-21.

The government’s reform agenda suffered some setback but the authorities remained committed to it. In April, a revision of the Constitution aimed at fostering transparency and accountability by public office holders did not pass. Also, little progress is being made with reforms of audit institutions. Nonetheless, the authorities are developing strategies to ensure that the reform program will continue unabated, reiterating their commitment to improve governance and transparency and strengthened accountability for public office holders.

Recent Developments

GDP growth is recovering based on agriculture. Benin achieved an economic growth rate of 4.0 percent in 2016; up from 2.1 percent in 2015. Strong GDP growth in 2016 is mainly due to favorable weather conditions and better access to agricultural inputs. By contrast, the depreciation of the naira, coupled with the decline in 2016 of the activities related to cotton ginning, negatively impacted the secondary sector (2.6 percent growth in 2016 vs. 10.1 percent in 2015). Despite a difficult sub-regional context, the tertiary sector showed a 3.4 percent increase in value added compared to an initial forecast of 2.7 percent.

The current account deficit (including grants) is expected to remain elevated in 2017. After a brief improvement in 2016, it is projected to reach 9.1 percent of GDP, reflecting the investment scaling up in 2017 with imports of goods and services increasing by about 19 percent.

Policy Discussions

Discussions focused on how to: (i) accelerate reforms to create fiscal space; (ii) preserve debt sustainability; (iii) diversify the economy and promote inclusive growth, and (iv) promote good governance and transparency.

Promoting Diversification, Inclusive Growth, and Financial Deepening

Economic diversification and development of the financial sector are essential to enhance the inclusiveness of growth. Despite the agricultural sector’s strong contribution to economic growth over recent years, Benin faces critical challenges regarding export diversification and domestic production. Based on cross-country experiences, the Selected Issue Paper (SIP) prepared by staff on: Growth, Structural Transformation, and Export Diversification shows the type of structural reforms and economic diversification that could contribute to boost and sustain growth in Benin. These reforms should:

-

aim at improving infrastructure and trade networks, reducing barriers to entry for new products, deepening financial markets, fostering more efficient financial intermediation and access to markets, and investing in human capital (Box 4);

-

reinforce Benin’s relative good standing regarding the extent of foreign value added in its exports – traditionally referred to as backward integration, and

- focus more on sectoral policies such as developing high value added agro-commodity crops, promoting agro-processing, and developing the tourism sector – efforts to improve education outcomes, bolster governance and transparency in regulation should complement these sectoral policies.

Box 4. Stages of Transformation and Diversification

Benin’s economy remains poorly diversified and there has been some de-industrialization with the output share of manufacturing falling from 22 percent in 2000 to 12 percent in 2012. Today, agriculture employs around 70 percent of Benin’s workforce and contributes approximately to 22 percent to its GDP. Benin is addressing de-industrialization with policies to boost value-added in agriculture and tourism. One of the pillars of the GAP is the structural transformation of the economy to create more value added in agriculture and tourism, both identified as key drivers of future growth. Specifically:

-

Cross-cutting policies aimed at achieving efficiency gains in public investment, boosting private investment in energy and transport and strengthening education, skills, and human capital. Initiatives have been implemented to improve the business environment, although further progress in increasing access to electricity, facilitating paying taxes, and obtaining credit are needed.

-

In the agricultural sector, the government has developed policies aimed at: (i) creating seven regional poles for agricultural development and promoting high value added sectors such as pineapples, cashew nuts, cotton, maize, cassava, and rice, (ii) evolving the processing industry through technological innovations, and (iii) boosting continental aquaculture.

- In the tourism sector, investment projects seek to: (i) build a tourist pole around Voodoo art, and (ii) recreate the historic city of Ouidah to make it the flagship destination of memorial tourism in Africa.

Staff underscored the need to address weaknesses of the financial infrastructure and business environment to spur banks’ lending to the private sector. Although macroeconomic conditions in recent years have been favorable for financial stability, Benin’s financial sector remains under-developed and vulnerable, limiting its ability to support credit to the private sector and, ultimately, economic growth. The large number of unauthorized microfinance institutions (MFIs) raises stability risks. An SIP reviewed the financial sector’s contribution to sustainable economic growth, outlined stability concerns, and explored how to further improve financial inclusion.

Strengthening the Business Environment by Promoting Good Governance

A favorable business environment is critical for private sector-led growth. The authorities initiated several reforms aimed at improving the business and investment climate to support the process of economic diversification and improve the still weakly inclusive character of growth (MEFP ¶6). Heavy reliance on private investment to help address the infrastructure gap and Benin’s participation in the G20 CWA have heightened the importance of these reforms (MEFP ¶9). However, little progress is being made in: (i) strengthening audit institutions; (ii) addressing weaknesses in the doing business indicators; and (iii) addressing corruption and improving governance and transparency.

Ongoing reforms are expected to improve the business climate. Although Benin has continued to implement reforms, their ranking in the World Bank Doing Business Indicators has declined two positions in 2017. Benin ranks at 155 in 2017, with slight improvements on indicators covering the difficulty of starting a business, getting credit and protecting minority investors. The authorities plan to make progress regarding access to electricity, paying taxes, and enforcing contracts. Corruption has been identified in the 2017-2018 Global Competitiveness Index as one of the most problematic factor for doing business and some other third-party indicators suggest continued challenges for Benin. Additional steps should be taken to decisively tackle corruption, including through continued efforts towards establishing an effective AML/CFT regime to help deter, detect and prosecute the laundering of acts of corruption.

The authorities are committed to strengthen the AML/CFT and anticorruption frameworks. On November 2, 2017, the authorities approved for submission to the National Assembly a bill on AML/CFT, which coalesce existing legislation on the fight against money laundering with that on combating the financing of terrorism (MEFP ¶16). The authorities will further strengthen the framework for combating corruption, improve transparency, and proceed with a coherent implementation of the legislative and regulatory framework for AML/CFT.

Annex III. External Sector Assessment

The external sector assessment does not raise immediate concerns, but highlights the need to boost competitiveness. It found that the real effective exchange rate is broadly consistent with fundamentals although competitiveness remains weak. Benin’s current account deficit has improved in 2016 indicating significant export growth. However, this latter is projected to widen in 2017, reflecting scaling-up of investment. A gradual improvement of the current account deficit is expected from 2018 as investment and import growth stabilize.

Recent Developments of the Balance of Payments

The current account deficit excluding grants has improved in 2016. However, a widening of the current account is expected in 2017 due to the investment scaling up. From 2015 to 2016, the deficit of the current account narrowed from 8.2 percent of GDP to 7.5 percent of GDP. However, in 2017 the deficit is expected to widen and reach 9.4 percent of GDP. This evolution is mainly explained by higher imports of capital goods related to new investments. A gradual improvement of the current account deficit is expected from 2018 onwards as investment and import growth stabilize. By 2021, when the scaling-up of investment comes to an end, the current account deficit would narrow to 6.9 percent of GDP.

The external financing is mainly comprised of concessional financing and foreign direct investment (FDI). External financing of the current account deficit remained relatively stable over recent years. Short-term capital flows and medium- and long-term private loans were equivalent to 1 percent of GDP. Foreign direct investment inflows were equivalent to 1.5 of GDP in 2016 and are expected to reach 1.9 percent of GDP during 2017-21. Other capital flows, such as project loans, remained on average at 2.3 percent of GDP over the period 2014-2016 and are expected at 3 percent, on average during 2017-21.

Gross international reserve coverage in the WAEMU dropped sharply in 2016 and debt risks remain contained despite an increase in public debt led by high fiscal deficits. Gross international reserves coverage in WAEMU system declined substantially since 2010 when it stood at 6.6 month of imports, reserve coverage stabilized at around 4½ months of imports in 2013-14. In 2016, regional reserves in the WAEMU declined significantly by CFAF 1000 billion (about $2 billion) to stabilize at 3.7 months of imports. At end 2016, gross reserves covered about 55 percent of narrow money and 74 percent of short-term debt. International reserves increased by $2.7 billion in 2017, reaching 4.2 months of imports at end-September. Benin’s gross external debt is at 22.5 percent of GDP in 2016 (below the average WEAMU countries).

Selected Issues Paper

This Selected Issues paper on Benin was prepared by a staff team of the IMF as background documentation for the periodic Article IV consultation with the member country. The following topics were covered: a) Growth, structural transformation, and export diversification; b) Financial inclusion and development; c) Efficiency of public investment in Benin: an empirical assessment; d) Macro-structural policies and inequality; and e) Fiscal incidence and inequality.

Growth, Structural Transformation, and Export Diversification

While Benin has delivered high economic growth over recent years, it faces critical challenges regarding export diversification and domestic production. Based on cross-country experiences, this note evaluates the type of structural reforms and economic diversification that could contribute to boost and sustain diversified growth in Benin, underscoring the need for improving infrastructure, trade networks, and market access, reducing barriers to entry for new products, deepening financial markets, and investing in human capital.

The Structure of the Beninese Economy

During the last decade, growth in Benin has been comparatively highly volatile. Per capita GDP growth however has been stagnating. Real economic growth rebounded to 4 percent in 2016 compared to 2015, where the growth rate slowed significantly to 2.1 percent due to weak agriculture output generated by unfavorable weather and negative spillovers from Nigeria. From 2006 to 2016, real GDP growth averaged 4.2 percent (with a maximum of 7.2 percent in 2013 and a minimum of 2.1 percent in 2010 and 2015), driven mainly by the services. Growth remains volatile, despite having strengthened in recent years. Per capita GDP growth has been stagnating and Benin has been lagging six fastest growing non-resource intensive SSA-economies. Inflation turned negative in 2016 after a moderate increase in 2015. The fiscal deficit grew from -0.4 percent of GDP in 2012 to -6.2 percent of GDP in 2016, with a maximum of -8.0 percent of GDP in 2015. The fiscal deficit growth was essentially driven by a net increase in current transfers, especially subsidies to the cotton and electricity sectors, as well as a higher wage bill, while tax revenues weakened. The external current account deficit dropped by 1.5 percentage points of GDP in 2016 compared to 2015 mainly due to continued strong export performance.

In addition, economic growth was not inclusive. Notwithstanding recent progress, Benin remains a low-income country with 11 million people and a per capita income of US$790 in 2015. Agriculture accounts for a quarter of GDP and 51 percent of the country's employment with cotton as its primary export commodity. The informal sector, including subsistence agriculture, contributes up to almost 60 percent of GDP and engages over 80 percent of the labor force. Re-export to Nigeria contributes up to a quarter of the government’s revenue. Nonetheless, rapid population growth – averaging 3.5 percent per year – led to a modest and unequal increase in household consumption. Poverty levels grew from 36.2 percent in 2011 to 40.1 percent in 2015. Due to its low productivity, growth was modest in agriculture, which employs almost half of the labor force. The economy remains poorly diversified and vulnerable to external shocks, underscoring the urgency to promote economic diversification. In particular:

-

Poverty remains spread and it is characterized by significant regional disparities. Female-headed households have typically experienced lower poverty levels, divested of economic opportunities.

-

There is a dichotomy between economic growth and poverty reduction. During the last five years, higher growth was mainly driven by more capital-intensive sectors like banking, telecommunications and maritime activities at the port of Cotonou. In contrast, agriculture, which is a main driver of poverty reduction, have grown, mostly, from expansion of cultivated land and the associated labor rather than increase in productivity.

-

Rapid population growth further limited the growth in per capita income and its impact on poverty reduction. Furthermore, regional trade had a negative spillover from the Nigeria’s economic slowdown and policy changes. There were diminished opportunities in both goods and services between Benin and Nigeria affecting the broader sector of informal trade, where gas flows informally from Nigeria to Benin, and in the broader consumer goods sector, where rice, chicken, edible oil, used cars, used clothing etc., flow from Benin to Nigeria.

Diversification slowly advances led by the agriculture and service sectors. There has been relatively little evidence of structural change in Benin over time. The sectoral composition of output has remained remarkably stable and the level of diversification low. During the period 2010-2016, the primary sector contributed by 0.5 percent to the real GDP growth while the secondary and tertiary sectors agriculture accounted for around 1 percent and 2.2 percent respectively, shares that have changed little since 1990 for when data are first available. The level of output diversification – based on a Theil Index measure – is also low and has remained stagnant, in contrast to faster growing benchmark countries, which have witnessed sharp increases in diversification over time.

The agricultural sector in Benin is highly dependent on rainfall patterns and, mostly, on one major commodity (cotton). Despite its low productivity, agriculture remains one of the main sources of growth and employment in Benin. Nonetheless, to further contribute to economic growth and poverty reduction, the agriculture sector needs to buttress its productivity considerably. Specifically, agricultural production systems heavily rely on increases in cropped areas and family labor, with limited use of improved inputs, production methods, and farm equipment. Agricultural exports are concentrated on three groups of products: cotton, fruits (pineapple), and nuts (cashews) and oilseeds (soy and cottonseed). Nonetheless,

-

to address the needs of a growing urban population, the country continues to import a large share of horticultural products from neighboring countries (mostly, Burkina Faso and Nigeria), rice from Asia, wheat, frozen meat and milk from Europe, and frozen poultry products from Brazil.

-

the agricultural sector faces the triple challenges of diversifying exports (consolidating cotton exports and increasing export volume for pineapple and cashew nut), increasing food production, and sustainably increasing farm and post-harvest productivity – these challenges must be addressed by improving the structural vulnerability of the country’s agricultural production system to floods and occasional droughts; and

-

access to financing is limited outside the cotton system. The country’s agricultural trade performance is generally weak, with a persistently negative agricultural trade balance.

Benin has experienced a modest de-industrialization, contrasting with a sharp industrial expansion in this sector among benchmark countries. The share of the manufacturing sector in output fell from 22 percent to 12 percent in Benin during the period going from 2000 to 2012 but increased from 10 percent to 16 percent in the Asian peer group between 1990 and 2012. Conversely, the share of the agricultural sector has declined across low-income countries over time but has remained elevated in Benin. During the decade 2000-2009, the share of the agricultural sector was estimated on average at 24 percent. It remained constant and has been valued at 22 percent during the period 2010-2016.

Benin has exhibited good performance regarding integration into value chains recently. The Regional Economic Study (2015) showed that integration into global value chains had indeed been accompanied by a pickup in income levels. To measure the depth of this integration, the REO relied on the extent of foreign value added in a country’s exports – traditionally referred to as backward integration. By this measure, rising depth of integration has been associated with rising income over time for developing and emerging market economies higher share of its exports enter as inputs for other countries’ exports, reflecting the still-predominant role of commodities in many countries’ exports in the region. By this metric, Benin is aligned with the rest of SSA.

Growth and Factor Inputs

Low human capital accumulation and total factor productivity appear to have driven volatile growth. A growth decomposition exercise suggests that two thirds of growth over the past two decades can be attributed to labor accumulation, while capital accumulation accounts for almost a third. In contrast, human capital and productivity appear to have been the main drivers of the mediocre growth performance, and are the factors in Benin lags most relative to other countries. These factor ‘gaps’ suggest that policies should target access and quality of education, public financial management (PFM) reforms to improve the efficiency of public investment, and key areas of the business environment, such as contract enforcement, access to credit and efficient electricity provision.

Benin’s competitiveness is impaired by structural bottlenecks and a challenging business climate. The 2016 Doing Business Indicators (DBI) report ranks Benin 155th (out of 189 countries), worse than most peer countries in the region. Indicators related to education, health, access to water, and infant mortality have improved in recent years but at a slow pace. Growth has been accompanied by a low level of job creation with widespread underemployment affecting especially women and the youth in urban areas. However, the participation of women in services has shown an improvement in the last decade. FDI is keeping its pace with SSA but more investment is needed.

Benin has maintained a steady sectoral share in the last decade. Notwithstanding the increase in overall participation recently, Benin was lagging almost half of the SSA countries in terms of its manufacturing and services as a share of GDP. Structural changes that followed the country after 2004 gradually brought the country to a much more favorable position today. Comparing Benin to SSA countries presently, the share of manufacturing and services is ahead of most of the SSA countries, reaching 75 percent of GDP. While its exports per capita remain lower than for most SSA countries, they improved a lot during this ten-year period.

Export Diversification

Export diversification has not taken place. African benchmark countries diversified quite strongly after 1990 and have caught up to Asian benchmark countries whose diversification levels were already comparatively high before that time. The number of export partners has increased on average, but the shares of the main export partners remain dominant. Cross-country experiences show that policies need to build on a country’s endowments and existing strengths and be tailored to tackle specific challenges to yield successful diversification.

Product diversification could yield growth gains. Further increasing product variety similar to diversification could yield further growth gains. Based on the estimates in IMF (2014a), a one standard deviation increase in LIC’s export diversification raises the growth rate by about 0.8 percentage points. For Benin, this translates into estimated growth gains of 0.2 percentage point if export diversification was raised to levels observed in comparators like Vietnam.

Conclusions

Benin’s competitiveness is impaired by structural bottlenecks. A challenging business climate, low productivity, and weak human capital. Low and stagnant productivity in the agriculture sector is perhaps a primary cause of the limited poverty reduction in rural areas.

Policies to promote structural transformation and diversification should focus on addressing weaknesses that hinder entry into new lines of economic activity. Further progress on strengthening the business climate, addressing electricity shortages, and increasing human capital could provide significant benefits.

In particular, measures that could help improve productivity in the short run includes:

-

the support the promotion of large-scale adoption of improved technologies (production, postharvest, processing and storage), including climate-smart production systems, reduce vulnerability of farming activities to climate change and weather vagaries of farming activities;

-

development of production and market infrastructure to enhance productivity through efficient water management, reduction of post-harvest losses and better access to market through warehouses and other facilities;

-

support to value chain coordination and access to finance through sustainable use of the financial management instruments set up under the original project;

-

institutional support to the Ministry of Agriculture and other stakeholders in the sector (civil society and producers’ organizations) with a particular focus on capacity building. Furthermore, measures to improve education and productivity could render significant impacts on the informal economy, which is estimated to be at more than half of GDP. Product diversification could yield higher growth rates.

Financial Inclusion and Development

While access to finance is improving, relatively to other sub-Saharan countries, a number of reforms could foster financial deepening and financial inclusion and complement efforts to promote the expansion of the private sector and employment creation.

Background

Benin’s financial sector is shallow, segmented, and with limited financial inclusion. Benin has a small and segmented financial sector in which 3 categories operate: the banking sectors, the microfinance institutions and other nonbank financial institutions. As of end-2016, there were 15 commercial banks, with 4 banks holding about 80 percent of credits to the banking system.

Banks’ capital adequacy has increased from 8.8 percent (end-June 2015) to 10.6 percent, above the 8 percent minimum but still below the WAEMU and SSA averages. The ratio of non-performing loans (NPLs) remains high when compared against peer countries in the WAEMU region. Other indicators are also lagging behind WAEMU averages, including the provisioning ratio for NPLs (12 percent of risk-weighted assets in 2014-15), the liquidity ratio, and profitability indicators.

Although the banking system remains stable, its depth has not improved. The banking sector is broadly sound but plays a limited role in financial inclusion. According to the BCEAO estimations (2010), there is a low level of access to banking service. More precisely, the number of deposit accounts in commercial banks relative to the active population is around 5 percent. In Benin, the banking services are targeting the high income urban population, the low population density and the large size of the informal sector limited the access to the banking services. In addition, the interbank market is no existent.

Financial Access and Development

The authorities are striving to enhance financial services delivery by addressing hindrances to financial inclusion and deepening, covering access, depth, and efficiency.

-

Although the number of bank branches has been recently increasing, in particular in rural areas, there is room to further expand financial inclusion by strengthening the regulatory framework of agency banking. High documentation requirements to open, maintain, and close accounts and for loan applications could impede access to finance (participation costs).

-

To further enhance credit culture and cover all, the authorities could consider setting a credit reporting bill to unify the collateral registration system, avoiding any potential fragmentation across registries. It could also be useful to strengthen the insolvency/bankruptcy procedure, and improve land titling, which can ease collaterals demanded by lenders. Further, improving contract enforcement in the judiciary sector could contribute to relax collateral constraints and addressing gaps in financial market infrastructure.

-

Intermediation efficiency. Efficiency is generally associated with the state of competition and is reflected in interest spreads and banks’ overhead costs. Intermediation costs (i.e., high interest rates and fees) reflect asymmetries of information between borrowers and banks. Access to an account in Benin compares poorly with averages from low income countries.

Financial development has modestly improved in Benin over the past ten years. The composite index of financial development suggests that financial development in Benin has been lackluster over the past three decades. Relative to middle-income countries (Mauritius, Namibia, Seychelles, and South Africa), Benin shows a modest improvement in achieving higher rates of financial development and lacks behind the average for SSA countries and other regions.

Lastly, Benin is performing relatively well regarding access to finance and use of mobile banking but there is scope for further progress. Benin holds around 5 percent of the total volume of mobile transactions in the WAEMU region with a total number of subscription of 12 percent.

The benefits from developing financial institutions in Benin are large. Thus, an appropriate sequencing would emphasize developing institutions at early stages, with increasing attention to developing markets as income per capita rises. Benin could adapt regulation and infrastructure to make investment by private sector participants easier while allowing them to hedge risks and enabling capital to be efficiently channeled into investment projects.

Related News

2018 New Year Message of the Chairperson of the African Union Commission, Moussa Faki Mahamat

2017 has been a particularly eventful year, with the assumption of duty of a new Commission. I have had the privilege of serving with a diverse group of individuals over the past nine months, and the results have been encouraging.

Youth has been at the center of our agenda, as the African Union works to open up opportunities for them in every field. 2017 was the year of Harnessing the Demographic Dividend through Investment in Youth. This made it possible to renew our commitments, as African States and institutions, to achieve our targets for young people, including through reducing the proportion of youth unemployment by at least 2% annually. In adopting the African Union Demographic Dividend Roadmap, Member States have pledged to open up financial services for young people, promote entrepreneurship, increase investments in health, education, and create spaces for youth civic engagement and political participation. They further pledged to mobilize investments in sectors with the potential for high employment multiplier effects and to engage the corporate sector to encourage on-the-job training and philanthropic programmes.

Member States also renewed their commitments to empowering the youth through the ratification, domestication and full implementation of all African Union Shared Values instruments, including the African Youth Charter and the African Charter on Democracy, Elections and Governance.

I am pleased that several African Union Member States have launched the Continental Demographic Dividend Roadmap and committed to report annually on progress made. The vast majority of Member States completed the development of their Demographic Dividend profiles. This now gives us a clearer picture of the high-impact areas that require strategic investments in order to harness the demographic dividend. I call upon the Member States that have not yet done so to complete these profiles.

Reports of African migrants being auctioned as slaves in Libya by international criminal networks were received with shock across the continent and beyond. In response, the Commission took a number of steps, including working with the Libyan authorities, as well as the United Nations, the European Union, the International Organization for Migration and the High Commissioner for Refugees, as part of an African Union-led task force, to facilitate and accelerate the voluntary repatriation of migrants. I requested the African Commission on Human and People’s Rights to carry out an investigation into the situation and to report as soon as possible. Alongside this, the Commission will also take additional steps to address the underlying drivers of irregular migration.

In November, we celebrated the 30th anniversary of the African Commission on Human and People’s Rights, which was established to further the advancement of our people. While the task of making these aspirations into reality is a long one, we are confident that it will be achieved.

This year, the Commission reevaluated the effectiveness of its previous policies and strategies with respect to gender equality and women’s empowerment on the continent. On this basis, a new gender equality and empowerment strategy has been developed, which ensures better alignment with agenda 2063, places stronger emphasis on tangible results and accountability, and promotes innovative practices.

Regional integration remained a priority for the African Union. Significant progress has been made regarding the negotiations over the Continental Free Trade Area (CFTA). Following the 4th meeting of the African Ministers of Trade, held in Niamey in December 2017, it is envisaged that the CFTA agreement and other related documents would be adopted in March 2018. The CFTA, which is a flagship project of Agenda 2063, will create a market of over 1.2 billion people. Its establishment will significantly increase intra-African trade, create economies of scale and regional value chains, and augment job opportunities. In parallel, a legal framework for the management of migration and mobility – the Protocol to the Treaty Estabilishing the African Economic Community Relating to the Free Movement of Persons, Right of Residence and Right of Establishment has been elaborated. It is due for adoption by the African Union Summit of January 2018.

The Commission will also accelerate the implementation of a number of continental policies, including in the area of infrastructure, with the Programme for Infrastructure Development in Africa (PIDA), and agriculture, with the Comprehensive Africa Agriculture Development Programme (CAADP). In this respect, greater emphasis will be placed on food security and safety.

Another Agenda 2063 flagship project is the Single African Air Transport Market. This initiative is a follow-up to the Yamoussoukro Declaration of 1999, and will be launched in January 2018, on the margins of the African Union Summit. Twenty-three Member States have pledged their solemn commitment to the Single Air Market, the implementation of which will increase the number of routes, reduce the cost of air travel and contribute to the expansion of intra-African trade and tourism. I call on all Member States that have not yet done so to join this important initiative.

On the institutional building front, the Assembly of Heads of State and Government took an important decision to transform our Union into an effective and efficient institution capable of accelerating progress towards economic integration, peace, security and overall prosperity for African citizens. In line with this decision, I have established a Reform Implementation Unit to co-ordinate the implementation process. I am particularly pleased with the progress we are making on the “Financing the Union” agenda. In 2018, Member States will be funding almost 40% of the African Union programme budget, compared to less than 5% in 2015 when the initiative was launched. A number of measures will be taken to strengthen overall finance and budget management accountability. In January 2018, I will be submitting a progress report, setting out a number of reform implementation proposals and recommendations, for discussion by the Summit.

Several successful elections were held in Member States. I note, in particular, the peaceful conduct of presidential and representative elections in Liberia. This bears testimony to the commitment of the Liberian people and leaders to sustain peace in their country. I congratulate the peoples and Governments of the countries that held elections for their commitment to ensuring smooth electoral processes, moving us closer to realizing the spirit and letter of the African Charter on Elections, Governance and Democracy. I urge all concerned to respect the will of the people, abide by their national and international obligations, and to use non-violent and legal means in resolving electoral disputes.

As we work towards building stronger institutions and promoting prosperity, the fight against corruption assumes even greater importance and urgency. It is a well-recognized fact that corruption hinders efforts aimed at promoting democratic governance, socio-economic transformation and peace and security. It creates inequality in our societies and erodes the rule of law. While empirical evidence shows that Africa has made some encouraging steps in the last five years, huge challenges remain. In recognition of these, the African Union Assembly declared 2018 as the African Anti-Corruption Year (Project 2018), with the theme “Winning the Fight Against Corruption: A Sustainable Path to Africa’s Transformation.”

The African Union remains committed to working with the Member States to deliver on the ambitious Agenda 2063 flagship project of Silencing the Guns by 2020. We all need to rededicate ourselves to ending violence and sustaining peace in our continent, including by bringing to a successful conclusion the ongoing peace processes in Mali and the Central African Republic, ensuring that the elections planned in the Democratic Republic of Congo in December 2018 take place on time and in a conducive environment, consolidating progress made in Somalia, and ending the threat posed by terrorism in the Sahel, the Lake Chad Basin, and in Horn of Africa.

It is my earnest hope that the south Sudanese stakeholders will deliver on the commitments made in the Agreement on Cessation of Hostilities, Protection of Civilians and Humanitarian Access signed as part of the IGAD-led Revitalization Forum that took place in Addis Ababa in December 2017. The people of South Sudan, who have endured so much pain and suffering, desperately need and deserve peace.

We have had several key engagements with our strategic partners. We started the year with a high-level African Union Commission-United Nations Secretariat meeting. We renewed our commitments to work together on Africa’s peace, security and governance challenges. In November, the African Union-European Union Summit took place. The outcomes of these meetings stand to significantly enhance the quality, effectiveness and impact of these partnerships.

As we enter 2018, we should remember all those who lost their lives not because they lost the will to live, but because of the deadly cloud of conflict, intolerance and disregard for human life and endeavor. We ought to do more and better in 2018 to ensure a future for ourselves, our children, our continent and our world, where the right to life, peace, opportunity and protection should be the basic barometer of our shared humanity.

We should not also forget the women and men serving in African Union or United Nations peace operations in Africa. In 2017, many of them were killed in the line of duty. Their sacrifices should not be in vain.

I wish you all, fellow Africans, a prosperous and peaceful 2018 for our Continent and its people.

Related News

The task at hand as Kagame takes over African Union Chair

The 29th Ordinary Session of the Assembly of the African Union (AU) held in Addis Ababa, Ethiopia in July 2017, elected Rwanda to lead the Union for a period of one year, in 2018.

The 30th Ordinary Session of the Assembly of the Heads of State and Government, that convenes in Addis Ababa, Ethiopia, from January 28 to 29, will therefore be chaired by President Paul Kagame in his capacity as Chairman of the Union.

He takes over from his Guinean counterpart, President Alpha Condé.

It will be the very first time that Rwanda will lead the Union since the latter was launched in 2002.

At the 27th AU summit in Kigali in July 2016, African leaders tasked President Kagame to lead a new effort to reform the AU Commission and the Union to make them more efficient.

The AU Chair is the ceremonial head of the Union elected by the Assembly of Heads of State and Government for a one-year term.

Accelerate reforms

The Minister of State in the Ministry of Foreign Affairs, Cooperation and East African Community Affairs, Amb. Olivier Nduhungirehe said the Chairmanship of President Kagame will accelerate the AU reforms programme which will allow his successors to continue on the same path, thus allowing Africa to reach its goal of self-sustenance and having its voice heard on the international scene.

Uduak Amimo, a broadcaster based in Kenya who covered Ethiopia and the AU for the BBC from 2009 to 2011, said President Kagame will bring a plain-speaking, hands-on, action-packed style to the continent that emphasises focused, responsible leadership and ownership of Africa’s development.

She said his style will have some African leaders uncomfortable because he will call them out, as he did “when they trooped to Europe for a security Summit on Africa.”

“He will lead from the front as he did in offering to resettle African migrants stranded in Libya and at risk of being enslaved,” Amimo said.

“In driving the reforms agenda at the AU, he will demand that attitude and mindsets change both at the commission itself and in how African leaders engage with and support the AU.

“Those reforms will not gather dust on shelves as many of our African decisions and initiatives have done. Under his leadership and direction, a critical mass of African countries will implement the reforms and we will see a more autonomous AU.”

According to Dr. Marco Jowell, the Director of Africa Research Group and research fellow at the School of Oriental and African Studies (SOAS), University of London, there is an opportunity for pragmatic and realistic strategic direction of Pan-African ideals which Kagame is very well placed to provide.

“Kagame is clearly highly respected by the AU having been tasked with leading its reform which bodes well for chairmanship of the continental body. He has also steered Rwanda to be leading peacekeeping contributor and is a champion of economic development and African trade, core elements of the AU’s agenda,” Dr. Jowell said.

“The ideas are there, but pragmatism, consensus and the implementation of feasible activities is required for the AU to effectively meet some of its expectations.”

Peace and security

Africa faces insecurity though leaders have set 2020 as the year by which conflicts on the continent will have been resolved.

Nduhungirehe said that Kagame, as AU Chairman, will work closely with his counterparts around the continent on strengthening the pillars for the Agenda 2063, a strategic framework for the socio-economic transformation of the continent over the next 50 years.

“The Agenda 2063 entails the end of conflicts on the continent by 2020. This means that President Kagame will have to work closely with regional organisations and other heads of state to find sustainable solutions to conflicts and prevent their causes,” Nduhungirehe said.

“Most of the conflicts we have on the continent could have been avoided if countries could talk peace,” he added.

Besides the vulnerability associated with climate change and other factors there are hot spots of insecurity associated with war and conflict that require the AU’s attention. These range from the Boko Haram insurgency in Nigeria; a never ending armed conflict in the Darfur region of Sudan, the Central African Republic conflict; violence in South Sudan; repeated attacks by Somalia-based Al-Shabab terrorist group on Kenya with far-reaching effects; and Islamist militant and terrorist activity in the Maghreb and Sahel regions of North Africa.

Nduhungirehe noted that the AU has a panel of wise personalities mostly composed of former Heads of State and Government that are usually sent on missions around the continent to prop up peace talks between governments and the opposition on pertinent issues. The AU maintains peacekeepers in different African countries.

During Kagame’s Chairmanship, the Union is set to start implementing reforms under the oversight of a steering committee, the minister added.

“Africa is the poorest continent with over a billion people, but it has good weather with a lot of natural resources that could help it prosper. This means that we have a hard task of making good use of our people, land and other resources,” Nduhungirehe noted.

Donor dependence

Nduhungirehe said that it’s sad that 80 per cent of AU programmes are funded by donors though Africa could do it by itself.

Under the Kagame-led reform plan, each country will deduct 0.2 per cent of its tax income from taxable imports and contribute it to the AU commission to help the Union achieve self-reliance.

So far, 20 countries (out of 54) started remitting the contribution. It is hoped that all will have come onboard by year end.

Navigating complex continental diplomatic relations, lack of capacity