Search News Results

African leaders prep for summit on continental trade deal

African national leaders concluded the 30th Ordinary Session of the Assembly of the African Union last week, with the summit adopting a series of decisions on issues related to continental economic integration – including on the next steps for the Continental Free Trade Area (CFTA), as well as the free movement of people and air travel.

The two-day meeting in Addis Ababa, Ethiopia, also saw participants discuss progress towards realising the continent’s own development vision, Agenda 2063, as well as the UN’s 2030 Agenda for Sustainable Development. The African Union (AU) and the UN signed a framework agreement on implementing those two broad development-oriented agendas in a mutually supportive way.

High on the meeting agenda was the fight against corruption, a topic chosen as this year’s summit theme. Various African leaders emphasised that despite a growing recognition of the necessity to tackle this problem, more work needs to be done at all levels.

“We must seize the opportunity of the theme of this year on the fight against corruption to take decisive action against this scourge that impedes development and undermines social cohesion,” said Moussa Faki Mahamat, Chairperson of the AU Commission, in his address to the meeting.

The summit was also marked by the election of Rwandan President Paul Kagame as the new AU chairperson. He succeeds Guinean President Alpha Condé and will guide the work of the organisation over the coming year.

CFTA summit: the final countdown?

African leaders agreed to hold an extraordinary summit on 21 March in Kigali, Rwanda, with the goal of considering legal texts related to the CFTA and signing the agreement establishing the free trade area. It will be preceded by an extraordinary session of the Executive Council on 19 March, also in Kigali.

“Scale is essential. We must create a single continental market, integrate our infrastructure, and infuse our economies with technology. No country or region can manage on its own. We have to be functional, and we have to stay together,” said Kagame in his opening remarks to the AU Assembly.

The projected mega-FTA is expected to bring together the 55 members of the African Union into a continental market with a cumulative GDP exceeding US$3.4 billion and a total population of over one billion people. If concluded and implemented successfully, it would become the largest free trade area in the world in terms of membership.

Negotiations towards establishing the CFTA were launched in 2015 with the initial goal of concluding a first phase covering trade in goods and services by the end of 2017. Despite significant progress achieved at the end of last year, however, sources say that members are still working to finalise talks on all aspects related to phase one negotiations. Phase two will move the talks towards discussing topics such as competition policy and intellectual property.

While negotiators completed their work on the Agreement Establishing the Continental Free Trade Area and the Protocol on Trade in Services in November 2017, additional discussions are needed to resolve remaining sticking points involving trade in goods. This includes aspects related to rules of origin, sensitive and excluded products, trade remedies, and infant industries.

Negotiations resumed this week with a view towards bridging remaining differences ahead of the March summit, and the process of legal scrubbing is currently underway for the texts that have already been finalised.

The AU also announced last week at the summit a “strategic partnership” with the AfroChampions Initiative, a group of public-private projects driven by well-known African government officials and business leaders. This new collaboration will aim to promote the CFTA by boosting engagement with the continent’s entrepreneurs.

“By sharing the reflections of its members and their ‘on-the-ground’ experience, the AfroChampions Initiative will allow us to develop more relevant approaches on many technical subjects – especially with regards to common customs tariffs, facilitation of intra-African trade, and free movement of workers, goods, and capital,” said Albert Muchanga, the AU Commissioner for Trade and Industry.

Free movement of people, air travel

In another effort to strengthen continental integration, the AU Assembly adopted a protocol that provides for the progressive implementation of free movement of people, right of residence, and right of establishment on the continent, as well as a related draft implementation roadmap.

While many observers have noted that free movement of people could play a central role in unleashing the continent’s economic potential, some have also warned that implementing this policy in practice will require real commitment from member states, which could prove challenging given the divisions which have emerged during the discussions so far.

While describing the importance of having the CFTA in place, Kagame said that “freedom of movement for people in Africa is equally important,” and suggesting that in his view the goal could be reached this year.

The AU summit also saw the formal establishment and launch of the Single Market for Air Transport in Africa (SAATM), a move aimed at enhancing connectivity at a continental level and developing the aviation and tourism sectors. “This is an initiative whose execution has been long awaited,” noted AU Commission Chairperson Moussa Faki Mahamat.

So far, 23 member states have committed to the immediate implementation of the 1999 Yamassoukro decision, which provides for the liberalisation of air transport services on the continent. They will be the initial members of the SAATM. This list includes Benin, Burkina Faso, Botswana, Cape Verde, Republic of Congo, Côte d’Ivoire, Egypt, Ethiopia, Gabon, Ghana, Guinea Conakry, Kenya, Liberia, Mali, Mozambique, Nigeria, Rwanda, Senegal, Sierra Leone, South Africa, Swaziland, Togo, and Zimbabwe.

“The realisation of a Single African Air Transport Market is vital to the achievement of the long-term vision of an integrated, prosperous, and peaceful Africa under the AU Agenda 2063,” said an AU press release.

Like the CFTA and the free movement of people, the creation of a unified air transport market in Africa is among the flagship projects of the first ten-year implementation plan of Agenda 2063.

“By committing to break down these barriers, we will send a tremendous signal in Africa and beyond, that it is no longer business as usual,” said Kagame at the AU summit.

UN-AU partnership

Speaking during the AU Assembly’s opening ceremony, UN Secretary-General António Guterres reaffirmed the UN’s strong commitment to work towards addressing the continent’s most pressing challenges.

At a time of growing debate over the benefits of multilateralism, he said that the UN and the AU “can show that multilateralism is our best and only hope.”

The two intergovernmental organisations signed the AU-UN Framework for the Implementation of Agenda 2063 and the 2030 Agenda for Sustainable Development, which aims at fostering greater cooperation and ensuring that both agendas are effectively integrated into African countries’ national development plans.

“Our two agendas – the 2030 Agenda and Agenda 2063 – are mutually reinforcing. Eradicating poverty in all its forms is our overarching priority,” said Guterres.

Through taking a harmonised approach and using this new framework agreement to guide their shared work, the AU and the UN aim to optimise resource mobilisation and use, while avoiding duplication of efforts.

Going forward, the UN chief also identified five areas for enhanced partnership between the UN and the AU: peace and security; inclusive and sustainable development; climate change; migration; and the fight against corruption.

Supporting gender equality

Another theme that received significant attention was gender equality, with the AU Assembly calling on member states to implement all the commitments made in the Solemn Declaration on Gender Equality in Africa.

Adopted in July 2004, the declaration reaffirmed African countries’ “commitment to continue, expand, and accelerate efforts to promote gender equality at all levels,” followed by a series of 13 specific pledges on various gender-related matters.

“For women especially, we need to unreservedly accord them their full rights and roles,” said Kagame during the opening ceremony.

African Union officials at the event said that the AU has done well to ensure that its leadership roles see strong representation from women, while calling for more work to be done to address the gender leadership gap both within the organisation and at the national level.

Guterres, for his part, noted in his speech the valuable role that women and young people can play in bringing African countries’ development goals to fruition.

“Women’s full participation makes economies stronger and peace processes more successful,” he said.

Related News

Brazil circulates proposal for WTO Investment Facilitation deal

Brazil submitted an extensive draft proposal for a potential agreement on investment facilitation to the WTO’s General Council last week, in a bid to jumpstart more “structured discussions” on the subject.

The proposal, which was circulated on 1 February, serves as a response to the call made by 70 WTO members in a “Joint Ministerial Statement on Investment Facilitation for Development,” which was released on 13 December on the margins of the WTO’s Eleventh Ministerial Conference (MC11).

The MC11 statement followed the work done by the “Friends of Investment Facilitation for Development” (FIFD) group, which had led to informal discussions on the subject last year. The FIFD group had also helped convene a high-level investment facilitation meeting in Abuja, Nigeria, with the support of regional partners last November.

That same MC11 document had confirmed that this group of members would begin holding “structured discussions with the aim of developing a multilateral framework on investment facilitation,” along with welcoming any other interested members to join the initiative.

This framework, they said, would be “flexible” and “responsive” given members’ respective priorities, while also preserving the right to regulate “in order to meet their policy objectives.”

The group had also confirmed plans to meet early in the new year “to discuss how to organise outreach activities and structured discussions on this important topic,” without setting a concrete date for doing so. The Brazilian proposal is the first formal document to emerge on investment facilitation and the WTO since MC11 drew to a close in mid-December.

Illustrative example of a future deal

In its submission, the Brazilian delegation clarifies that the draft proposal is not intended to serve as a negotiating text, but rather is meant to serve as a “concrete illustration” of what an agreement on investment facilitation could look like. The submission, they say, could help serve as a starting point for a “more focused and text-based discussion” on the subject, along with supporting outreach efforts towards bringing more WTO members on board.

The Brazilian text is more extensive and detailed compared to earlier proposals submitted by various delegations in 2017. The scope and the main elements, however, remain the same. These include articles that aim to improve the transparency, predictability, and efficiency of regulatory and administrative frameworks related to investment policies and measures. Proponents of these measures say that these would then provide a more stable and secure enabling environment for investors to undertake sustainable investments in host economies, thus promoting trade and economic growth.

The Brazilian proposal includes examples of articles that would strengthen institutional or “electronic” governance, such as by setting up a “single electronic window” that would publish relevant documents and help streamline the application and admission procedures for incoming investments.

The proposal also includes an article that would establish a national focal point, in other words a delegated authority which would mediate and facilitate investor concerns with public authorities and would also operate the above-mentioned single electronic window.

In line with previous proposals submitted last year by other delegations, the Brazilian text emphasises that issues such as investment protection, dispute settlement “not foreseen” under current WTO dispute rules, and market access, as well as government procurement, are outside the ambit of an investment facilitation accord.

Brazil has also included a range of other illustrative articles, such as “voluntary principles and standards of corporate social responsibility” for investors to undertake in other countries, along with suggested provisions for special and differential treatment (S&DT) for developing country and least developed country (LDC) members. These provisions include technical assistance, additional time for implementing certain articles, and the exclusion of LDCs from meeting some requirements.

The South American country has also outlined how a potential “WTO Committee on Investment Facilitation” could work, including reviews on implementation, cooperation with other international agencies, and the potential establishment of subsidiary bodies.

Questions remaining

Going forward, it remains to be seen how the proposal will be received among both current participants in the investment facilitation joint statement, as well as the WTO’s wider membership. Earlier attempts to discuss investment facilitation-related issues at the General Council last year and in minister-facilitated meetings during MC11 were strongly opposed by a coalition of countries, which included India and South Africa.

Some sceptics of the investment facilitation initiative have suggested that the subject falls outside the organisation’s mandate, while some have said the issue of investment facilitation is no different than the original “Singapore” issue of investment that had been considered for inclusion in the Doha Round of trade talks, only to be dropped from consideration.

Along with trade and investment, the other “Singapore” issues, so named for the location of the 1996 WTO ministerial which set up working groups to discuss certain subject areas, were trade facilitation, trade and competition policy, and transparency in government procurement. Only trade facilitation advanced to formal WTO negotiations from this working group process.

Another open question is whether and how the process for more “structured discussions” on new issues, such as investment facilitation, would be integrated within the WTO’s structures and formal processes.

The investment facilitation talks are not the only new initiative being pursued by WTO member groups in the wake of MC11. Joint ministerial statements were also released on e-commerce and on micro, small, and medium-sized enterprises (MSMEs), along with a declaration on trade and women’s economic empowerment. All of these drew the backing of several WTO members, who urged others to consider signing on.

Related News

EAC Monetary Union Bills in the offing

Two key Bills critical to the establishment of the East African Community Monetary Union were tabled for the First Reading in Kampala, Uganda on 7 February, 2018.

The EAC Monetary Institute Bill 2017 and EAC Statistics Bureau Bill 2017, tabled by the Chair of the Council of Ministers, Hon Julius Wandera Maganda, sailed through the First Reading and were committed to the respective EALA Committees.

The object of the EAC Monetary Institute Bill, 2017, is to provide for the establishment of the East African Monetary Institute (EAMI) as an institution of the Community responsible for preparatory work for the EAC Monetary Union. In accordance with Article 23 of the Protocol on the EAC Monetary Union, the Bill is expected to provide for the functions, governance and funding for the Institute as well as other related matters.

Closely related to the EAMI Bill is the EAC Statistics Bureau Bill, 2017, which also seeks to establish the Statistics Bureau as an Institution of the Community under Article 9 of the Treaty and Article 21 of the Protocol on Establishment of the EAC Monetary Union.

The Bill provides for the functions, powers, governance and its funding with a view to establishing an institution responsible for statistics in a bid to support the East African Monetary Union.

The EALA Committee on Communications, Trade and Investment is to hold public hearings on the EAC Statistics Bureau while the EAC Monetary Institute Bill will be handled by the General Purpose Committee.

The Speaker, Rt Hon Ngoga Karoli Martin said though the bills were tabled by the Council of Ministers, they were coming to the House close two years late. He therefore urged the Assembly to give both Bills the due attention deserved.

Meanwhile, Hon Amb Dr Augustine Mahiga, Minister for Foreign Affairs and East African Co-operation in the United Republic of Tanzania was sworn in as an ex-officio Member of EALA.

Hon Amb Dr Mahiga was led in to the House by Hon Josephine Lemoyaan, Hon Abdulla Makame and Hon Happiness Elias Lugiko.

In his maiden speech immediately thereafter, the Minister registered appreciation to EALA and congratulated the Speaker and Members for their election. He further congratulated the Members of the Republic of South Sudan for joining the Assembly and noted the region looked forward to ensuring it (South Sudan) maximizes the benefits of integration.

The Minister remarked that EALA had made major contribution and remained a significant player in the process of integration. “You are the custodian of the Treaty and the one that oversights Government – speaking without fear or favour on where we need to improve,” Amb Dr Mahiga said.

“You are the indispensable link to the people of East Africa, he added saying EALA was essential in bringing people behind the integration process,” the Minister added.

Related News

Bill seeking to ease cross-border movement tabled in parliament

A newly proposed law on immigration and emigration in Rwanda would make it easier for people in border communities to cross borders without difficulty, Members of Parliament in the Lower House heard yesterday.

The MPs on Thursday approved the basis of a draft law that seeks to amend the current law on immigration and emigration matters, which has to be reviewed to incorporate penalties on immigration and emigration related offences among other changes.

While presenting the draft law in Parliament yesterday, the Minister in the Office of the President, Judith Uwizeye, said that provisions have been added in the draft law to make it easy for people living in border communities to travel to neighbouring countries.

Under Article 57 of the draft law, the government has proposed that the Directorate General of Immigration and Emigration be allowed to work in consultation with local leaders and other relevant authorities to establish more crossing points to strictly facilitate movements of border communities.

The draft law directs the directorate to put in place instructions governing the management of the crossing points.

“It’s important that we make it easy for Rwandans to travel to neighbouring countries, especially those who live near the borders. Some of them would travel long distances to reach a gazetted border post,” Uwizeye told MPs.

Immigration officials told The New Times that the move aims to close a gap in the law whereby people in some border communities were not explicitly allowed by the law to cross the nearby borders without using designated border posts.

Once it has come into force, the new law will recognise other crossing points other than gazetted borders to ease the movement of border communities.

Many legislators welcomed the move but suggested that the government should devise mechanisms at the proposed crossing points to ensure that they aren’t abused.

“Increasing border posts is a good thing but it should go hand in hand with increasing security equipment such as search equipment for travellers,” said MP Athanasie Nyiragwaneza.

Minister Uwizeye said that control mechanisms will be put in place as different crossing points are opened and she agreed with the lawmaker that some equipment should be procured for use by border posts.

“Yes, we will increase equipment. You also know that Rwanda has opened its borders to foreigners and that’s why we will increase control mechanisms at our borders,” she said.

Apart from easing travel for people in border communities, the draft law also seeks to institute new types of travel documents, redefine what migration crimes are, and provide penalties for such crimes.

Officials said in an explanatory note to the immigration draft law that the opportunity to modify the existing legal framework has come at a time when the law needed to be reviewed to bring on board various changes that occurred in the country in the area of Immigration and Emigration.

They said that the proposed review of Law no. 04/2011 of 21 March 2011 on Immigration and Emigration in Rwanda serves to facilitate the mobility of Rwandans and foreigners in the country by easing entry and exit procedures, but with necessary safeguards to ensure that Rwanda’s openness is not abused by criminals.

Related News

Côte d’Ivoire Economic Update: Skilled labor force and connectivity needed to modernize economy

With a GDP growth rate projected to reach 7 percent in 2018 and 2019, Côte d’Ivoire continues to be one of the most dynamic economies in Africa.

The sixth Economic Update for Côte d’Ivoire, launched on 8 February 2018 by the World Bank notes the undeniable performance of the Ivoirian economy, but also points out the urgent need to encourage greater private sector participation and to improve public finance management, especially in education and health.

The report entitled, At the Gates of Paradise, proposes a strategy based on three complementary pillars:

-

Opening the country’s economy to attract foreign investors in order to benefit from transfers of technologies and skills.

-

Strengthening local competencies to assimilate, adapt and successfully implement new technological tools.

-

Lowering physical and virtual transportation costs, by improving the performance of the Ivoirian ports (and their related connections), but also by reducing the costs associated with the use of mobile telephone and Internet tools.

Additionally, the report focuses on how the country can make up its technological lag. “Economic theory has long demonstrated the key role played by technological innovation in a country’s development process,” said Jacques Morisset, Lead Economist, World Bank.

“To be successful, Côte d’Ivoire must not only open up to the exterior but also enhance the skills of its labor force and the connectivity of its economy. These two factors play an essential role in the dissemination of new imported technologies and their adaptation to the local economic fabric.”

This model for the dissemination of technology has been implemented by numerous countries in Asia and more recently in Africa.

“The strategy behind the success of money transfers by mobile phones that is now spreading all over Africa would help firms operating in Côte d’Ivoire become more competitive and so create productive jobs for the fast-growing labor force,” said Pierre Laporte, World Bank Country Director in Côte d’Ivoire. “It will enhance the excellent performance achieved the country these last few years.”

At the Paradise’s Doors – Key Messages

After analyzing recent developments in the Ivoirien economy and its outlook for the short and medium term, this sixth report on the economic situation in Côte d’Ivoire focuses on how the country can make up its technological lag.

Although Côte d’Ivoire has embarked on a trajectory of strong growth after more than a decade of political instability, its aim of becoming an emerging economy will not be achieved without more productive businesses, as they are the country’s main employers and generate most of its revenues.

State of the Ivorian economy

With a rate of growth that is expected to hold steady at around 7.6 percent in 2017, Côte d’Ivoire continues to be one of the most dynamic economies in Africa, if not the world. As the catch-up effects that prevailed at the exit from the post-electoral crisis of 2011 have dissipated, this solid performance is explained by the rebound of agriculture owing to favorable rainfall and higher prices. It also demonstrates Côte d’Ivoire’s resilience to internal and external shocks.

The political and social climate, which deteriorated in the first half of the year as a result of the demands of some military personnel and civil servants, has calmed, and the sharp drop in cocoa prices has been offset by an excellent harvest.

The main monetary and financial variables stayed on their trend in recent years. Inflation held steady at around 1 percent annually owing to the prudent monetary policy of the BCEAO. Credit to the economy grew around 14 percent, reflecting strong demand in the private sector and the banks’ gradual diversification toward small and medium enterprises. The financial system is stable, respecting regional prudential ratios, and the rate of nonperforming loans stands at around 8 percent.

Although the current account deficit has stabilized at around 1 percent of GDP, this conceals significant developments. The 20 percent increase in exports reflects rising agricultural prices and good harvests. Imports have remained relatively stable, although the increase in purchases of oil has been offset by a decline in purchases of capital and intermediate goods. Inflows of external capital have financed the current account deficit, particularly government borrowing on the international market, with the result that the international reserves have risen significantly.

The Government’s fiscal position remains under control, although its deficit rose from 4 percent of GDP in 2016 to 4.5 percent in 2017. A number of factors explain this deterioration. First, the Government had to undertake additional expenditures to respond to the demands of certain groups in the armed forces and the public sector. As well, the authorities chose to absorb the rising oil prices and the decline in cocoa prices on the international markets by reducing the taxes on these products rather than allowing these fluctuations to flow through to pump prices and producer prices for cocoa beans. The fiscal policy was thus mobilized in support of cocoa producers and transport companies/motorists in 2017 to keep the social peace.

To offset this new spending, the authorities achieved budget savings over the year. Capital expenditures were reduced from the amount in the approved budget, and the authorities were also successful in increasing the collection of some taxes, particularly the corporate income tax.

Two initiatives helped reduce fiscal risks and improve public management in two sectors that are strategic for the country. First, the Government undertook to improve the payment of its electricity bills in the context of a consolidation plan intended to reduce the deficit in this sector. Second, a financial audit of some operations on the cocoa market identified numerous irregularities. Their correction should improve the governance within this market. These two initiatives send a positive signal that should encourage private sector investment.

The fiscal deficit has been financed by concessional aid and nonconcessional borrowing.

While the Government mainly accessed the regional market in 2016, in 2017 it tapped the international markets as it had in 2015. The issuance of euro bonds in June 2017 for a net amount of US$ 1.2 billion was a resounding success, with demand standing at four times this amount and a yield lower than the yield of the previous issuance in 2015. A portion of these bonds was denominated in euros, limiting the exchange risk for the country. However, the level of the public debt increased, from 47 percent of GDP in 2016 to over 50 percent in 2017.

Côte d’Ivoire’s short- and medium-term outlook remains encouraging. The GDP growth rate should reach 7 percent in 2018 and 2019. Modern services such as communications, finance and transport should continue to support the Ivoirien economy, and construction should also continue to grow steadily. All of these sectors should benefit from the country’s rapid urbanization and economic growth. The industrial sector should grow owing to the expansion of the food processing industry. The contribution of agriculture should be comparable to previous years although it remains dependent on weather conditions.

Prices, money and credit should maintain their current trajectory. The current account deficit is expected to stabilize at around 2 percent of GDP, while remaining vulnerable to changes in the terms of trade and weather conditions.

The fiscal adjustment planned for 2018 and 2019 is a key feature of the Government’s economic policy. It is aimed at maintaining debt sustainability and achieving the WAEMU target. The fiscal deficit should decline from 4.5 percent of GDP in 2017 to 3.0 percent of GDP in 2019. This adjustment is based on an increase in revenues (approximately 0.8 percent of GDP) and a reduction in current expenditures, which should return to their 2016 levels as a percentage of GDP (i.e., without the 2017 security spending). This strategy requires improving the efficiency of public spending so that the Government can achieve its ambitious infrastructure and social service objectives without spending more. There seems to be significant room for improvement both in the management of public investment and in the provision of public services in the areas of education and health.

Côte d’Ivoire has thus far benefited from generally favorable terms of trade and weather conditions in recent years, unlike the majority of African countries. However, the Ivoirien economy remains vulnerable to external risks such as fluctuations in the prices of agricultural and mining products, weather conditions, global and regional security risks, and a tightening of the regional and international financial markets.

On the domestic front, the presidential elections planned for 2020 could create uncertainties and even some instability, which could slow private investment. The Government could be tempted to spend more to support economic activity and maintain the social and political peace. The Government must also successfully increase its revenues while controlling its spending in order to avoid further debt, since the sustainability of the public debt has deteriorated, as indicated in the recent joint analysis by the International Monetary Fund (IMF) and World Bank.

As of end-2017, Côte d’Ivoire continues to be classified as a country with a moderate risk of debt overhang. However, it seems more vulnerable to slower economic growth, higher interest rates or a deterioration in its fiscal position owing to the steady increase in its debt in recent years. This risk is even higher if the debt of the public enterprises is taken into account, particularly enterprises in the energy sector. Contingent risks relating to some public banks (currently undergoing restructuring) and the public-private partnership programs should also be taken into account.

How to accelerate the economic transformation of Côte d’Ivoire?

Since the end of the crisis in 2012, the performance of the Ivoirien economy has been remarkable, with a per capita growth rate exceeding 5 percent per year. Despite this upturn, per capita income is today below levels in the early 1980s and has just caught up to the level reached in 1990. Although the political events that rocked Côte d’Ivoire largely explain this relative stagnation of incomes, they are not the entire explanation.

An examination of the economic growth factors during the period 2002 through 2014 shows that although Ivoiriens worked more, they did not necessarily work better. The employment rate did indeed increase significantly (even faster than the population growth rate), but incomes did not follow the same positive trend, for at least two reasons. The first is that labor productivity in the key sectors increased only slightly during this period and even declined in agriculture. The second reason is that while Ivoiriens left unproductive sectors to move to those with higher productivity, this movement was only partial and gradual. By way of comparison, in East Asia intersectoral productivity gains were 3 to 5 times more rapid, while the structural transformation generated by labor mobility contributed to 2 percent of growth each year as against just 0.5 percent in Côte d’Ivoire.

Labor productivity within the Ivoirien economy has risen since 2012, by about 4-5 percent per year, but businesses still lag behind the production frontier achieved by the emerging countries. This lag exists in the productivity of both labor and capital and in almost all sectors of the economy. Only a few productivity niches have appeared, such as mobile telephony and money transfers.

To make up this lag, Côte d’Ivoire must improve its economic and institutional framework. According to economist D. Rodrik, such an improvement in the overall framework within which businesses operate can accelerate a country’s speed of convergence with the economies of the most advanced countries by making the private sector more efficient. This movement is already under way in Côte d’Ivoire as shown by the increase in its score in the Country Policy and Institutional Assessment (CPIA) from 2.7 in 2010 to 3.4 in 2017, the largest increase among the developing countries as measured by the World Bank over the past 10 years. This increase reflects the efforts undertaken by the Ivoirien authorities to improve the country’s macroeconomic, structural, institutional and legal conditions. However, this progress will have an impact only in the medium term, as the effect on the productivity of businesses is generally slow.

The speed of Côte d’Ivoire’s convergence could accelerate if it adopts and adapts new technologies by means of a technological catch-up initiative or an unconditional convergence, i.e., one that is not necessarily linked to the conditions that prevail in the country. Few countries have successfully achieved this catch-up without having prioritized openness to the rest of the world through foreign investment and exports. These two vectors promote the transfer of technology and skills since the vast majority of new technologies, including those that can shape the Africa of tomorrow, are often proprietary developments by companies in advanced countries. Seeking partnerships should therefore be a priority.

A focus of Côte d’Ivoire’s National Development Plan is to increase foreign direct investment (FDI) and exports. Although some specific initiatives have been launched, particularly in the agri-food processing sector, this strategy has not yet taken off. The weight of FDI and exports in GDP has not increased in recent years. According to the World Bank only 3 percent of Ivoirien companies use imported technology licenses as against 15 percent in the rest of Africa. Moreover, Ivoirien companies spend less on research and innovation than their African counterparts.

To be successful, Côte d’Ivoire must not only open up to the exterior but also enhance the skills of its labor force and the connectivity of its economy. These two factors play an essential role in the dissemination of new imported technologies and their adaptation to the local economic fabric. This model for the dissemination of technology has been implemented by numerous countries in Asia and more recently in Africa, including Rwanda and Ethiopia. To use the words of a senior Malaysian official, “the contribution of foreign investment and exports is proportional to their capacity to train local workers and entrepreneurs, who will in turn train other workers and entrepreneurs.” Good connectivity is also essential to the flow of products, services, persons and ideas.

This report proposes a strategy involving three complementary pillars that will help generate a virtuous circle allowing Côte d’Ivoire to make up its technological lag and converge more rapidly with the most advanced countries:

-

Pillar one: A policy of openness must be defined on the basis of Côte d’Ivoire’s comparative advantages. An indicative list of potential products is proposed on the basis of the theories of revealed comparative advantages and product space. These industries can potentially attract foreign investors and turn toward exports in order to benefit from transfers of technologies and skills, which are still badly needed in Côte d’Ivoire.

-

Pillar two: The capacity to assimilate, adapt and successfully implement a new technological tool will, to a great extent, depend on the skills available in the country. Unfortunately, Côte d’Ivoire’s lag in terms of the development of its human capital is an obstacle. While the reform of the education system is essential, it must be accompanied by training partnerships with private companies, particularly foreign companies, and training of Ivoiriens abroad. Here, the openness will help strengthen local competencies, which will in turn themselves reinforce the country’s openness.

-

Pillar three: Good connectivity facilitates trade and increases the size of the market, generating economies of scale that are often essential to the establishment of foreign businesses and development of export activities. This requires lowering physical and virtual transportation costs and also reducing distances, for example through urbanization. The priorities are to improve the performance of the Ivoirien ports (and their related connections), to reduce the costs associated with the use of mobile telephone and Internet tools (1.5 to 3 times more expensive than in Ghana, for example) and to better manage the urbanization process by increasing the economic density of cities while controlling congestion costs.

Understanding the State of the Ivorian Economy in Five Charts

The Sixth Economic Update for Côte d’Ivoire notes the undeniable performance of the Ivoirian economy, but also points out the urgent need to work on certain aspects. The main needs are to encourage greater private sector participation and to improve public finance management, especially in education and health.

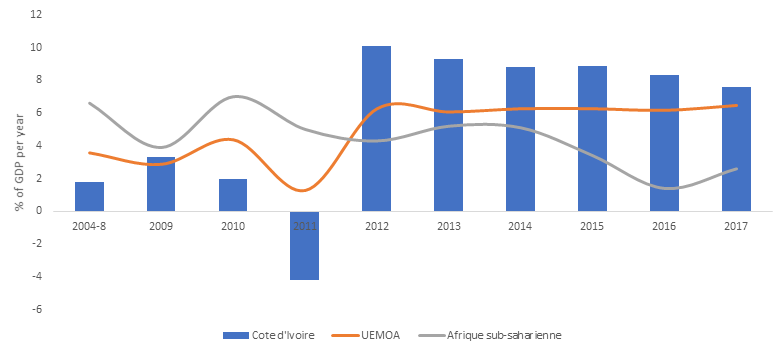

Côte d’Ivoire’s economic growth remains among the fastest on the African continent

In 2017, Côte d’Ivoire continued to be one of the most buoyant economies in Africa, with a growth rate expected to hold steady at around 7.6% (Chart 1). This positive performance is due to the recovery in agriculture, and shows Côte d’Ivoire’s resilience to domestic and foreign shocks. The short- and medium-term outlook remains encouraging. The GDP growth rate is forecast at 7% in 2018 and 2019. Nonetheless, the Ivoirian economy remains vulnerable to external risks such as fluctuations in agricultural and extractive commodity prices, climate conditions, global and regional security risks, and tight regional and international financial markets.

Chart 1. Côte d’Ivoire’s economic growth (Source: World Bank).

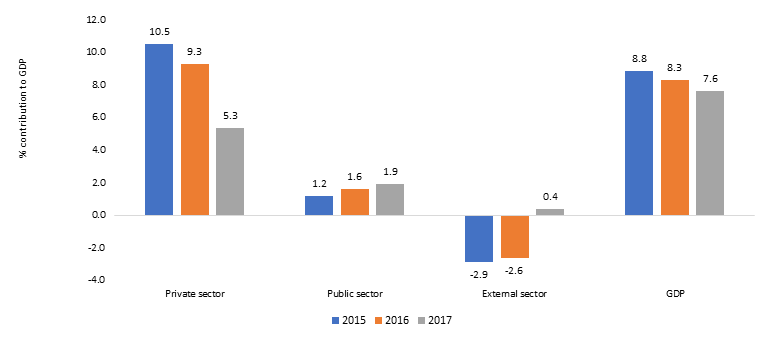

Growth increasingly driven by the public sector as the private sector’s contribution slows

The private sector’s contribution to Ivoirien growth has decreased since the end of the crisis in 2012 (Chart 2). However, there has been an increase in the foreign and public-sector contributions associated with the Government’s pro-cyclical policy and a positive external environment (in terms of export revenues and foreign investments). The authorities have taken forward an ambitious public investment program to narrow infrastructure and social services gaps, which had widened over more than a decade of political crises.

Chart 2. A downward trend in the private sector’s contribution (Source: World Bank).

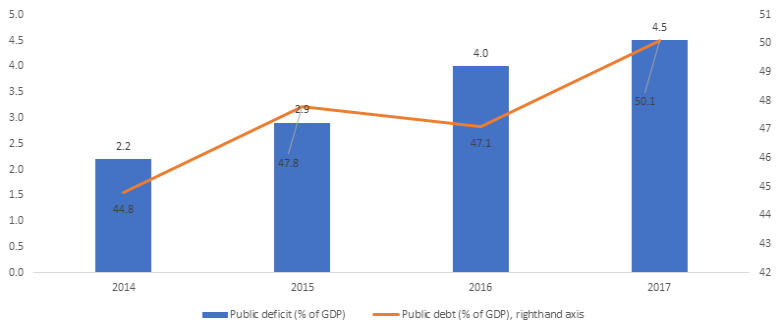

Budget deficit and public debt have both grown

The Government’s fiscal situation deteriorated in 2017. The budget deficit grew from 2.9% of GDP in 2015 to 4% of GDP in 2016 and 4.5% in 2017 (Chart 3). The deterioration in the fiscal situation was due to stagnating domestic revenues (around 19.5% of GDP), whereas public expenditure increased more sharply (+0.6% of GDP) owing to security and social contingencies.

Chart 3. Growth in budget deficit and public debt (Source: World Bank and IMF).

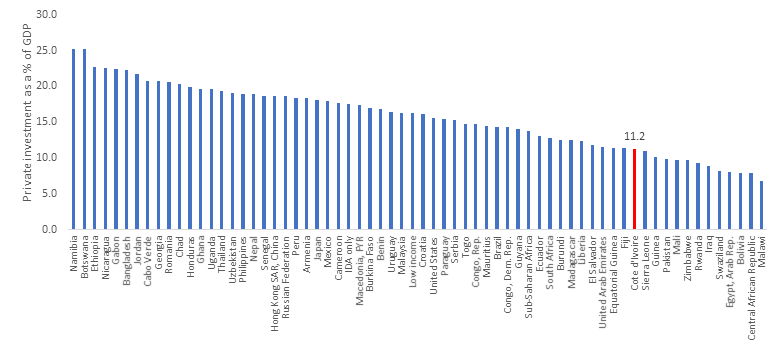

Private investment is still relatively low and needs to be encouraged

The rate of private investment jumped between 2011 and 2017, rising from 5.7% to 12.0% of GDP between 2011 and 2012 before stabilizing at approximately 11% of GDP between 2013 and 2017. Yet this rate is still too low, as shown by Chart 4, especially when compared with the emerging countries, where it can top 25% of GDP, and even the stronger-performing Sub-Saharan African countries such as Ghana (19%) and Uganda (18%). Côte d’Ivoire has also failed so far to attract significant inflows of foreign direct investments, which account for just 1.5-2% of GDP, far from the rates observed in Ethiopia and Mozambique. The development of the private sector is decisive if Côte d’Ivoire is to maintain its rapid growth rate and redistribute the fruits of economic growth more equitably across the entire population.

Chart 4. Share of private investment in GDP per African country (Source: World Bank)

Public expenditure efficiency needs to be improved, especially in the social sectors

In addition, the fiscal consolidation planned by the Ivoirien authorities in 2018 and 2019 is creating an urgent need to improve the efficiency of public expenditure. If the central government cannot spend more, it will have to spend better to achieve its ambitious infrastructure and social services goals. It will need to improve both the allocation of public expenditure (“knowing where to spend”) and its financial efficiency (“knowing how to spend”).

The report provides a comparative analysis (Chart 5) of a sample of some 20 countries in the sub-region and countries that could serve as models for central government to improve the efficiency of its education and health expenditures (which account for nearly one-third of the budget). This analysis shows that, despite considerable central government expenditure on education, the results in terms of primary school enrolment remain disappointing. By way of comparison, Benin spends proportionally less than Côte d’Ivoire, but has a higher rate of pupils enrolled in primary education.

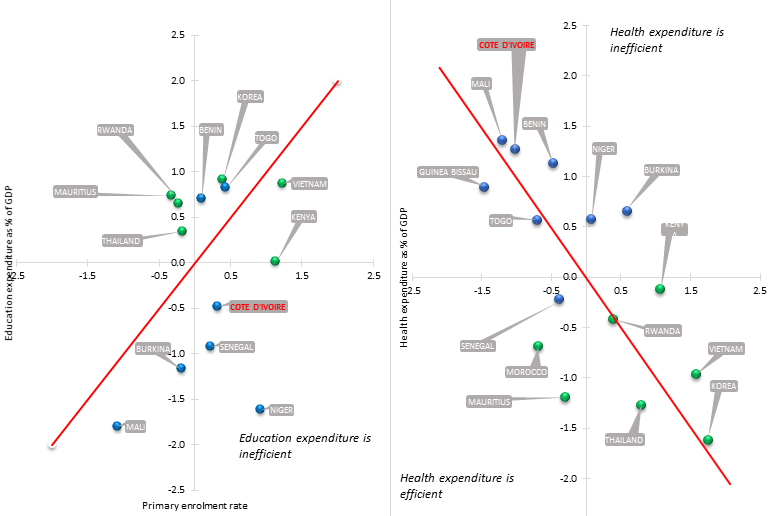

The fact that Côte d’Ivoire spends relatively little on the health sector explains its modest maternal mortality outcomes. Only Mali and Guinea Bissau put fewer resources into health than Côte d’Ivoire.

Chart 5. The efficiency of public expenditure in the social sectors (Source: World Bank). Note: Each variable is measured in terms of deviation from the sample’s mean. The blue dots represent the WAEMU member countries.

Related News

tralac’s Daily News Selection

tralac’s Weekly e-Newsletter is posted: SADC Tribunal saga continues before the South African courts

Featured tweets: (i) @AdanMohamedCS: The are now 54 Japanese companies in Kenya as of Jan 2018, increasing from 30 companies in December 2014. Some leading investors include Toyata Tshusho, Isuzu Motors, Honda Motors, Nissin Foods, Yamaha Assembling among many others. (ii) @GileadTeri: Tanzania imports 40 million pairs of shoes every year. Domestic production is between 2-4 million.

The Second Ministerial Review Conference of Africa-Turkey Partnership takes place next week in Istanbul

South Africa: Standard Bank launches branch dedicated to Chinese business community (Xinhua)

South Africa’s leading commercial Bank, Standard Bank Group, on Thursday launched its first branch dedicated to service the Chinese business community in Africa. Speaking at the launch, Chinese Consul General in Johannesburg Ruan Ping said the bank’s “first Mandarin Banking Branch in South Africa” bears witness to the vital role the private sector plays towards strengthening China-South Africa relations. George Lo, Executive Head of Africa China Banking at Standard Bank, said establishing the branch is part of the bank’s strategy in recognizing the commercial value of Chinese doing business in South Africa and Africa at large, and facilitating regional trade. The full-service dedicated branch was opened at an event at Crown Mines in Johannesburg. “This is another step in the bank’s ongoing commitment to deepen and grow the Africa-China investment and trade corridor. We chose this area, because it’s where many entrepreneurs and businessmen from neighbouring countries obtain their supplies from Chinese wholesalers,” George Lo added.

Smart phones drive new global tech cycle, but is demand peaking? (IMF)

Over a decade of spectacular growth, demand for smart phones has created a new global tech cycle that last year produced a new smart phone for every fifth person on earth. This has created a complex and evolving supply chain across Asia, changing the export and growth performance of several countries. While our recent analysis of Chinese smart phone exports suggests that the global market may be saturated, demand for other electronics continues to support rising semiconductor production in Asia. Smart phones have become a key metric of global trade. In 2016, global smart phone sales reached almost 1.5 billion units. Smart phones have become the main computing platform for many people around the world, supplanting personal computers. As the figure shows, demand for smart phones has surged while sales of PCs have declined. [The authors: Benjamin Carton, Joannes Mongardini, Yiqun Li]

FDI and supply chains in horticulture: diversifying exports and reducing poverty in Africa, Latin America, and other developing economies (CGD)

Prior research on foreign investment and supply chains in emerging markets has focused almost exclusively on the creation of international networks in manufacturing and assembly. This paper extends that research, looking beyond manufacturing into supply chain creation in horticulture - in particular, vegetables, fruits, and flowers, raw, packaged, processed - in Africa, Latin America, and other developing regions. How have some developing countries managed to break into the ranks of horticultural exporters, while others have not? What are the obstacles to entering international supply chains for horticultural exports? How can emerging market economies maximize positive impacts on rural employment, on gender employment, and on externalities for local communities? The paper concludes with an investigation of policy implications for developing country governments, for the World Bank and regional financial institutions, and for other providers of external assistance. [The author: Theodore H. Moran]

Zimbabwe: 2018 Monetary Policy Statement (BoZ)

Performance and Impact of the Export Incentive Scheme: In order to ensure that Zimbabwean exports are competitive under the auspices of a dollarized economy, the Bank established the $200m and $300m export incentive facilities which are monetised by bond notes. Since its inception in 2016, the export incentive scheme has enhanced competitiveness of Zimbabwe’s exports and this has significantly contributed to the growth of exports which grew by 36% from $2.8bn in 2016 to $3.8bn in 2017. Table 1 shows the cumulative export incentive and bond notes disbursed, and export receipts generated since inception of the export incentive scheme in May 2016.

Regional Payments Developments: The Central Bank is committed to regional payment system initiatives and has encouraged banks and other payment service providers to utilise the SADC Integrated Regional Electronic Settlement System (SIRESS) platform to settle regional cross-border transactions. Since the implementation of SIRESS in July 2013, the number of local banks participating on SIRESS has risen to 15 whilst transactional values have also increased as shown in Figure 5.

Merchandise Trade Developments: Over the period January to November 2017, total merchandise trade (exports and imports) stood at $8,408.5m, representing a 15.8% increase from $7,262.5m recorded over the corresponding period in 2016. The increase was on account of increases in merchandise exports and imports of 36.8% and 4.5%, respectively. Consequently, for the period under review, the country’s trade deficit narrowed from $2,181.6m in 2016 to $1,456.7m in 2017. A narrowed trade deficit reduces pressure on foreign exchange reserves.

Zimbabwe-Mozambique Machipanda border: bureaucracy tests truckers’ patience (Club of Mozambique)

Hundreds of trucks are stuck in queues for days waiting to cross the Machipanda border in Manica on their way to or from neighbouring Zimbabwe, leaving drivers vulnerable to criminal gangs and their nerves stretched to breaking point. Excessive bureaucracy in Zimbabwean customs clearance is allegedly to blame. According to information provided by the Mozambican customs authorities to the Commander-in-Chief of Police, Bernardino Rafael, a truck is processed every five minutes on the Mozambican side of the border, but on the Zimbabwean side the same procedure takes between thirty to forty minutes. Due to this slowness in customs clearance, the line of waiting trucks is four to five kilometres long, threatening the safety of drivers who are forced to wait long hours for clearance.

Kenya: Government defends forced use of SGR (Business Daily)

The government has defended a directive to transport all imports coming in through Mombasa port via standard gauge railway to Nairobi’s inland container depot. Kenya Railways managing director, Atanas Maina, confirmed the order but says it was reached through consultation with other players including Container Freight Terminal owners. He also denied that the move to ferry cargo to Nairobi will interfere with CFS’s work. “All we are doing is shifting a point of cargo handling and not writing off the whole role that CFSs play. There are roles to play in Nairobi. ICD cannot handle the 28 million tonnes. There is still a lot of opportunities for them to do business,” said Mr Maina on Wednesday, adding that there would be no job losses in Mombasa.

Ghana: GUTA cautions government over new levies and taxes (Ghana News Agency)

Dr Joseph Obeng, the National President of the Ghana Union of Traders Associations, has asked government not to introduce any new levies and taxes that would take them out of business. Currently, he said, the trading community was overburdened with 16 levies and taxes, which cumulatively took between 50 and 55% of their importing capital. Dr Obeng expressed the Association’s unhappiness over government’s intention to introduce a Cargo Tracking Note at the country’s entry point as another levy on importers to shore up government’s revenue. Dr Obeng also observed that government had started implementing the African Union levy, which the trading community were already displeased about it, because they expected government to take monies from the ECOWAS levy for that purpose. “We’re not happy with the AU levy because not all the African countries are collecting it and so why should Ghana rush in implementing it. In fact, government should be fair with importers because the Common External Tariffs, which government introduced some years ago has raised the levies importers’ are paying and we’re gradually falling out of the ECOWAS market.”

Global mining firms sue Kenya for $3.2bn compensation (The East African)

Trade Principal Secretary Chris Kiptoo says Kenya is actively involved in about 10 suits before a Dubai-based disputes tribunal. “There are ongoing cases at ICSID with claims amounting to Ksh334 billion. We have seen how vague language in investment treaties can result in massive payouts. Kenya has developed a model investment treaty and an investment agreements policy with clear rules and responsibilities,” said Mr Kiptoo at the 11th Annual Forum of Developing Country Investment Negotiators in Nairobi.

International Centre for Settlement of Investment Disputes: 2017 caseload (ICSID)

The International Centre for Settlement of Investment Disputes registered a record 53 cases in 2017 under its trademark ICSID Convention Rules and Regulations and Additional Facility Rules. The 2017 figure, published in the latest edition of ICSID Caseload – Statistics (pdf), represents a slight uptick from preceding years: 48 cases were registered in 2016 and 52 in 2015. ICSID has registered an average of 39 new cases each year over the last decade. ICSID also provides administrative support for investor-State arbitrations under the UNCITRAL rules and other ad hoc dispute settlement provisions. In 2017, 8 cases were administered under UNCITRAL rules and another 5 under ad hoc provisions.

The largest share of newly registered cases involved States from Eastern Europe and Central Asia (36%), followed by the Middle East and North Africa (15%), Sub-Saharan Africa (15%), and South America (13%). In 2017, 15% of new cases involved the financial sector. Cases involving energy and extractives also remained prominent. Of the arbitrations that concluded in 2017, 78% were decided by a tribunal, and the remainder were settled or otherwise discontinued.

Book review: The political economy of the investment treaty regime

Government regulatory space in the shadow of BITs: the case of Tanzania’s natural resource regulatory reform

Won Kidane: Alternatives to Investor-State Dispute Settlement – an African perspective

Playing with financial fire: a South Perspective on the international financial system

Extra-Ordinary Sectoral Council on Trade, Industry, Finance and Investment starts in Arusha

The three-day meeting started yesterday with the session of senior officials, to be followed today by the session of Permanent/Principal Secretaries/Undersecretaries. The meeting concludes tomorrow with the Session of Ministers or Cabinet Secretaries. Agenda items include: deliberation on the long standing Non-Tariff Barriers to trade; consideration of the two pons of ad valorem of 35% and specific duty rate of tariffs for used clothing under AGOA Out of Cycle Review; consideration of the update on EU-EAC Market Access Upgrade Project; consideration of the EAC Trade and Investment Report 2016, adoption of the One Stop Border Posts Manual. [Related: @Trade_Kenya: Declining intra-trade within EAC block, from $55bn in 2015 to $45bn in 2017, dominated Extra-Ordinary Council on Trade, Industry, Finance and Investment as partner States ponder on resolving long standing Non Tariff Barriers]

EAC organs grapple with acute shortage of skilled staff (The East African)

A shortage of professional staff at the EAC Secretariat and its organs will feature on the agenda of the upcoming summit in Kampala. The registrar of the East African Court of Justice said this week that the EAC’s judicial arm is one of the key organs affected. “The entire spectrum of the EAC is facing a shortage of staff. It is among the matters to be discussed at the summit,” said Yufnalis Okubo, the EACJ registrar. Mr Okubo said Monday that the Arusha-based court has a skeleton staff of only 28 out of nearly 300 professionals needed.

UK pledges additional funding to expand ITC’s SITA project (ITC)

The UK, through DfID, has pledged an additional GBP 2.4m in seed funding to the International Trade Centre’s Supporting Indian Trade and Investment for Africa (SITA) project. The funding will enable new spin-off initiatives and expand some existing activities within the SITA project. ITA enhances South-South trade and investment cooperation between India and five East African countries (Ethiopia, Kenya, Rwanda, Uganda and United Republic of Tanzania), and across several priority sectors: pulses, spices, sunflower oil, coffee, information technology, leather and textiles and apparel.

Related News

Standard Bank launches branch dedicated to Chinese business community

South Africa’s leading commercial Bank, Standard Bank Group, on Thursday launched its first branch dedicated to service the Chinese business community in Africa.

Speaking at the launch, Chinese Consul General in Johannesburg Ruan Ping said the bank’s “first Mandarin Banking Branch in South Africa” bears witness to the vital role the private sector plays towards strengthening China-South Africa relations.

George Lo, Executive Head of Africa China Banking at Standard Bank, said establishing the branch is part of the bank’s strategy in recognizing the commercial value of Chinese doing business in South Africa and Africa at large, and facilitating regional trade.

The full-service dedicated branch was opened at an event at Crown Mines in Johannesburg.

The move unlocks future business and trade potential between the continent and the world’s second largest economy, Lo said.

“This is another step in the bank’s ongoing commitment to deepen and grow the Africa-China investment and trade corridor. We chose this area, because it’s where many entrepreneurs and businessmen from neighbouring countries obtain their supplies from Chinese wholesalers,” he added.

“This model is not just about servicing the Chinese, but, importantly, also Africans looking to trade with China. We expect this to be the first of many opportunities to come,” Lo said.

The branch will have staff fluent in both Chinese and English who can service the Chinese customers and everyone else. Standard already has over 100 Chinese-speaking relationship managers, bankers and advisors, including Chinese-speaking traders on the bank’s trading floors, Sibongiseni Ngundze, Executive Head, Retail and Business Banking at Standard Bank said.

The Crown Mines area has become a regional trade hub for neighbouring countries, with several Chinese markets being established.

The Standard Bank Group has a strong footprint across 20 African countries, and the Crown Mines branch opening follows the successful launch of the world’s first dedicated Africa-China Banking Centre at its Simmonds Street offices in Johannesburg in June last year.

“The development of dedicated branches for Chinese clients in South Africa is one of the tangible practical transactional platforms that cements this relationship. We are actively expanding and will continue to invest across these exciting markets,” Lo said.

China has been the largest contributor to global growth since 2008, and continues to be a key investor in Africa. Meanwhile, the country’s trade with Africa totaled 170 billion US dollars in 2017, up 14.1 percent year on year, according to Chinese customs data.

Related News

Zimbabwe: 2018 Monetary Policy Statement

Enhancing financial stability to promote business confidence

Presented by Dr. J P. Mangudya, Governor of the Reserve Bank of Zimbabwe

The Statement comes at a time when the economy is experiencing renewed hope and confidence ushered in by the new economic dispensation, following the formation of a new leaner cabinet by His Excellency, the President, in November 2017. This renewed hope and confidence would need to be supported by going back to basics to restore business confidence and to foster discipline within the national economy. Accordingly, this Monetary Policy Statement seeks to buttress this confidence trajectory by putting in place measures that gradually liberalise the foreign currency market in order to indicate that the country is ‘open for business’.

The Bank has continued to make concerted efforts to address cash shortages, which are a direct reflection of the tight foreign currency macro-economic environment that is exacerbated by the transmission impact of the persistent fiscal deficit on the financial sector. Addressing this current macro-economic imbalance requires a sharp rise in foreign exchange reserves and an improvement in the fiscal balance. It is against this backdrop that the interventions by the Bank in the foreign exchange market through nostro stabilisation facilities have greatly assisted the economy to meet the ever growing demand for foreign exchange and, in doing so, stabilising parallel market activities and sustaining the financing of critical imports such as fuel, electricity, cash, medicines and essential consumer goods. In addition, policy interventions to promote exports continue to bear fruit as evidenced by the continued narrowing of the current account deficit. In this regard, Zimbabwe’s current account balance is now within the international best practice range and also consistent with macroeconomic convergence targets under the SADC and COMESA guidelines.

This, notwithstanding, the country’s high import dependency continues to exert pressure on foreign exchange earnings, thus fueling parallel market activities for foreign exchange. This economic situation is compounded by the growing fiscal deficit which remains the major driver of increased deposits or money supply in the banking sector, creating foreign currency liquidity shortages in the economy and causing inflationary pressures through domestic monetary emission on the RTGS platform.

Opening up of the economy to business is therefore the most sustainable cure for the major challenges the country is facing. Opening Zimbabwe for business means attracting investment, foreign and domestic, that is required to increase production, jobs, fiscal space, exports and eventually the happiness index for Zimbabweans. It moves the economy beyond stabilisation. Opening up the economy also calls for local business to improve on their efficiencies and competitiveness in order to brace for competition from foreign investors.

The Bank is convinced that by opening up the economy for business, the country has struck the right chord for the sustainable transformation of the economy. It is in this optimistic context that the Bank is coming up with measures to gradually open the foreign currency market in order to restore investor confidence within the economy under the new narrative to open Zimbabwe for business. Specifically the measures presented in this Statement are meant to address the following:

-

Further promoting the use of mobile and electronic payment systems (plastic money);

-

Enhancing the use of the local generated RTGS funds to generate exports;

-

Improving the foreign currency market;

-

Enhancing rewards to exporters and reducing cost of doing export business;

-

Providing generators of forex assurances of ease of access to foreign currency;

-

Enhancing foreign currency retention threshold;

-

Enhancing nostro stabilisation facilities to provide assurances to foreign exchange earners of forex availability and to meet the import requirements of essential commodities;

-

Improving ease of access to productive facilities;

-

Addressing the needs of the diasporans;

-

Reinforcing the arrears clearance and re-engagement programme;

-

Providing guidance on the continuation of the multi-currency system;

-

Providing guidance on the Presidential Amnesty on externalised assets and funds; and

-

Providing update on the acceptability of the 99-year land leases as collateral at banks.

Conclusion

The narrative “open for business” means that Zimbabwe is ready and willing to embrace a paradigm shift to attract investors, both local and foreign, for the total transformation of the economy in respect of increased production, jobs, exports, fiscal space, access to capital and foreign finance. Improvement in these economic variables will greatly benefit the monetary environment and, in doing so, enhancing financial stability and confidence within the national economy. A healthy foreign exchange buffer will strengthen the value of RTGS funds and gradually reduce cash shortages.

“Open for business” is not just a narrative. It calls for a dramatic change in the conduct of business from the business as usual approach. We need to walk the talk to re-balance the economy through a tight rein on fiscal deficit – increasing revenue collections and holding expenditures constant – whilst at the same time enhancing Zimbabwe’s access to foreign finance and increasing foreign inflows from exports and international remittances. These measures will be buttressed by accelerating the arrears clearance and re-engagement programme under the Lima, Peru, principles of engagement with the International Financial Institutions and Development Partners.

The policy measures enunciated in this Statement should therefore be seen as the initial move to gradually open the foreign currency market to show that Zimbabwe is open for business. 2018 should therefore be a defining year for Zimbabwe. The future of Zimbabwe is in our hands.

Global and regional economic developments

The global upswing in economic activity, which started in the second half of 2016 is strengthening, supported by robust growth in emerging economies. As a result, global economic activity is projected to improve from a growth of 3.2% registered in 2016 to 3.7% in 2017 and 3.9% in 2018.

Despite this development, growth remains weak in some countries, with inflation below target in most advanced economies. Growth in China, India and other parts of emerging Asia remains strong, while several commodity dependent economies in Latin America and sub-Saharan Africa show some signs of improvement.

In sub-Saharan Africa, growth is estimated at an average of 2.7 percent in 2017, up from 1.4 percent recorded in 2016. Growth is expected to further increase to 3.3 percent in 2018, with sizable differences across countries. This growth remains below the previous growth rates of above 5% recorded in 2014. There are, however, mounting vulnerabilities in the region, notably, rising public debt, financial sector strains and low external buffers. Public debt is high not only in oil exporting countries but in many fast-growing economies as well.

The improved global economic performance in 2018 has spill over effects on demand for Zimbabwean commodities and hence increased economic activity in the domestic economy.

Commodity Price Developments

International commodity prices continued their recovery from the rock-bottom levels registered at the beginning of 2016, although they remained depressed compared to the levels that were attained in 2012. More specifically, energy, base metals, precious metals and agricultural commodity prices showed some resilience in 2017 due to strong demand, particularly from China’s property, infrastructure, and manufacturing sectors and amid various supply bottlenecks globally.

Balance of payments developments

Consistent with developments in the sub-Saharan African economies, the country’s external sector position is showing signs of improvement, on account of policy measures being taken by Government and the Reserve Bank to boost exports and contain the import demand.

Merchandise Trade Developments

Over the period January to November 2017, total merchandise trade (exports and imports) stood at US$8,408.5 million, representing a 15.8% increase from US$7,262.5 million recorded over the corresponding period in 2016. The increase was on account of increases in merchandise exports and imports of 36.8% and 4.5%, respectively. Consequently, for the period under review, the country’s trade deficit narrowed from US$2,181.6 million in 2016 to US$1,456.7 million in 2017. A narrowed trade deficit reduces pressure on foreign exchange reserves.

Merchandise exports for the period January to November 2017 increased by 36.8%, from US$2,540.4 million realized in 2016 to US$3,475.9 million in 2017. The increase in the year on year merchandise exports was mainly on account of increases in exports of nickel (mattes, ores & concentrates), gold, ferrochrome and black tea. Exports composition remained unchanged showing Zimbabwe’s dependence on the export of commodities.

Gold, flue-cured tobacco, nickel (mattes, ores & concentrates) ferrochrome and diamonds dominated the country’s exports, contributing about 80% of total export earnings. The country’s exports were mainly destined for the SADC region with South Africa and Mozambique absorbing 62.8% and 10.5%, respectively. The country’s major exports to South Africa include platinum group of metals (PGMs), gold and nickel. These commodities are further exported to their final destination by South Africa.

Total merchandise imports for the period January to November 2017 amounted to US$4,932.6 million, a 4.5% increase from US$4,722.0 million realized over the corresponding period in 2016. The increase in merchandise imports was mainly attributable to increases in importation of energy (fuel and electricity), maize seed, machinery, fertilizers and medicines. The country sourced its imports mainly from South Africa (40.5%), Singapore (22.4%), China (8.8%), Zambia (2.5%) and Japan (2.5%).

Reflecting the combined effects of positive developments on merchandise trade in 2017 and the need to boost domestic production for both export and local consumption through importation of raw materials and intermediate goods, the current account deficit is estimated to have slightly increased from US$591.3 million in 2016 to US$618.1 million in 2017.

International Money Transfers

For the year 2017, inward international remittances amounted to US$1.4 billion compared to US$1.6 billion received in 2016 representing an 11% decrease. Of the US$1.4 billion, Diaspora remittances amounted to US$698.9 million. The Bank is encouraged by the trend where Authorised Dealers are investing in enabling technologies that broaden financial inclusion, reduce remittances cost and increase remittance access points for the convenience of senders and recipients. These efforts towards formalization of remittances is key in building sufficient capacity for leveraging on the developmental impact of remittances.

Related News

Kenyan government defends forced use of SGR

The government has defended a directive to transport all imports coming in through Mombasa port via standard gauge railway (SGR) to Nairobi’s inland container depot (ICD).

Kenya Railways managing director, Atanas Maina, confirmed the order but says it was reached through consultation with other players including Container Freight Terminal (CFS) owners.

He also denied that the move to ferry cargo to Nairobi will interfere with CFS's work.

“All we are doing is shifting a point of cargo handling and not writing off the whole role that CFSs play. There are roles to play in Nairobi. ICD cannot handle the 28 million tonnes. There is still a lot of opportunities for them to do business,” said Mr Maina on Wednesday, adding that there would be no job losses in Mombasa.

CFS owners and transporters have this week decried looming job losses due to the directive that they say forces importers to ferry cargo directly to the Inland Container Depot (ICD) in Embakasi, Nairobi.

According to the directive, all un-nominated cargo will be transported through the rail.

Mr Maina was speaking in Mombasa while accompanied by Kenya Port Authority managing director Catherine Mturi-Wairi and Nairobi ICD manager Simon Wahome.

“I am certain that they (CFS owners) have identified opportunities and are doing what they need to do to ensure we create the good realignment that makes it possible for us to bring the benefit from the cargo and reduce the cost of transport,” he said.

Ms Wairi said KPA has been engaging all players including shipping lines and cargo owners and employed a marketing strategy to reduce the tariffs for transportation.

“The movement of cargo cannot be done without the cargo owner’s direction on the same. On our part as KPA we have given them a very good tariff that currently for local we are giving 80 dollars for 20 foot container and 120 for a 40 foot container,” she said.

Related News

tralac’s Daily News Selection

Featured trade infographic, @ECA_OFFICIAL: Intra-Africa trade in agricultural products is underexploited. Trade liberalization under CFTA is expected to result in significant export volume growth across several food sectors.

Underway in Nairobi: 11th Annual Forum of Developing Country Investment Negotiators

Nigeria has made it more difficult for foreigners to work in the country (Quartz Africa)

An executive order signed by Nigeria’s president Buhari on Monday “prohibits the ministry of interior from giving visas to foreign workers whose skills are readily available in Nigeria.” It’s not a blanket ban though. The executive order states that foreigners will be considered for jobs “where it is certified by the appropriate authority that such expertise is not available in Nigeria.” The executive order also tells government agencies to “give preference to Nigerian companies and firms in the award of contracts.” But the restriction on hiring foreigners could be seen to conflict with the government’s recent move to more open visa policies.

Kenya now playing catch-up to Ethiopia on mega projects (The Standard)

Ethiopia is tipped to stretch its lead on Kenya in economic growth, spurred by increased investment in development projects. According to the Africa Construction Trends report 2017 released by audit firm Deloitte yesterday, for every Sh100 that Ethiopia budgeted for, Sh40 went to projects in key sectors of the economy compared to Kenya’s Sh20. This means that Ethiopia – which in 2016 overtook Kenya to become the largest economy in Eastern Africa – is in good stead to stretch its lead over Kenya. According to the report, although Kenya had the largest number of projects between 2016 and 2017, the total value of projects in Ethiopia was almost twice those in Kenya. [Ethiopia, Kenya need to exploit economic opportunities - Ambassador]

Kenya to start exporting oil in 2021/22, says Tullow (The Standard)

Kenya could start exporting oil on commercial scale in the next five years, Africa-focused oil and natural gas producer Tullow Oil said on Wednesday. “The exploration and appraisal campaign in Kenya has confirmed the presence of substantial oil resources in the South Lokichar Basin. After over six years of hard work, we can now move forward to commercialising these low cost resources through a phased development of the basin involving a central processing facility and an export pipeline to the Kenyan coast,” said Mark MacFarlane, Executive Vice President for East Africa. “In 2018, we will focus on taking the project towards Final Investment Decision in 2019 with a prudent and flexible plan of execution that can take advantage of low oil services costs and deliver first oil and cash flow as soon as possible. With good progress being made in Uganda towards FID, East Africa is on the verge of becoming a major oil exporting region.”

Kenya: Maize imports from Uganda rise sharply to top Sh1.47bn (Business Daily)

Maize imports from Uganda rose sharply between October and November last year compared with the same period in 2016, as high prices in Kenya following a shortage of the grain helped spur the trade. Data from the Eastern African Grain Council indicates that cross-border trade between the two countries increased from 1,408 tonnes in the fourth quarter of 2016 to 47,563 tonnes estimated at Sh1.47 billion in the same period last year. EAGC regional manager for marketing and communication Jacinta Mwau said the price differential and improved production in Uganda helped to raise volumes of grain traded between the two neighbouring states.

Kenya: Cheap Chinese, Indian, UAE imports threaten local firms (The Star)

In its fourth-quarter Barometer report, the business lobby said 63% of manufacturers complained cheap imports make local products uncompetitive. The Barometer represents a six-month forecast. The most-affected firms are Sameer Africa, which makes tyres, and Eveready East Africa, which manufactures batteries. Many other products, including textiles, are also hurt by imports. “It’s necessary to fast-track implementation of the Trade Remedies Act 2017 [that] seeks to deal with unfair trade practices such as dumping, subsidising and import surges,” KAM said. To ease the problem, the association wants full enforcement of existing laws to ensure fair trade practices and a level playing field. Last month, South Korean-based electronics giant Samsung announced it had abandoned plans to build an assembly plant in Kenya. It cited failure by the government to put in place mechanisms to protect manufacturers from cheap electronics imports.

Kenya: Govt to zero rate taxes on imported raw materials (KBC)

The government plans to zero rate both the Import Declaration Tax and the Railway Development Levy on all imported raw materials to be used in manufacturing processes locally. The revenue shortfall will then be recovered by increasing tax on imported finished products. This according to Industry and Trade Cabinet Secretary Adan Mohammed will cushion locally produced goods from unfair competition posed by cheap imported goods.

Uganda: Informal trade costs Shs900b in maize revenue (Daily Monitor)

Uganda’s failure to enforce regional standards aimed at eliminating cheap imports and informal trade is depriving the country of Shs900bn export revenue annually. Bank of Uganda statistics indicate that last year, the country formally exported maize worth $70m (Shs254bn) out of the 4 million metric tonnes. However, industrial players are saying the earnings were less than the country’s annual revenue potential of $320m (Shs1.1 trillion) if everybody played their part. In a bid to protect Uganda’s maize from cheap imports outside East Africa and informal traders who distort the market, sector players want government to enforce the regional standards. In an interview with Prosper Magazine, the chairman of the Grain Council of Uganda, Mr Chris Kaijuka, said: “We want government through the ministry of Trade, to enforce the EAC Maize standards so that traders start trading formally.” He said Uganda is being flooded with maize imports from Brazil and the Southern African countries.

Kenya: Smuggling of hides hurts did to grow leather trade (The East African)