Search News Results

Investor treaties in trouble

Several countries are reviewing these agreements, prompted by the number of cases brought by foreign companies who claim that changes in government policies affect their future profits.

The tide is turning against investment treaties that allow foreign investors to take up cases against host governments and claim compensation of up to billions of dollars.

Indonesia has given notice it will terminate its bilateral investment treaty (BIT) with the Netherlands, according to a statement issued by the Dutch embassy in Jakarta last week.

“The Indonesian Government has also mentioned it intends to terminate all of its 67 bilateral investment treaties,” according to the statement.

It has not been confirmed by Indonesia. But if this is correct, Indonesia joins South Africa, which last year announced it is ending all its BITS.

Several other countries are also reviewing their investment treaties.

This is prompted by increasing numbers of cases being brought against governments by foreign companies who claim that changes in government policies or contracts affect their future profits.

Many countries have been asked to pay large compensations to companies under the treaties.

The biggest claim was against Ecuador, which has to compensate an American oil company US$2.3bil (RM7.6bil) for cancelling a contract.

The system empowering investors to sue governments in an international tribunal, thus bypassing national laws and courts, is a subject of controversy in Malaysia because it is part of the Trans-Pacific Partnership Agreement (TPPA) which the country is negotiating with 11 other countries.

The investor-state dispute settlement (ISDS) system is contained in free trade agreements (especially those involving the United States) and also in BITS which countries sign among themselves to protect foreign investors’ rights.

When these treaties containing ISDS were signed, many countries did not know they were opening themselves to legal cases that foreign investors can take up under loosely worded provisions that allow them to win cases where they claim they have not been treated fairly or that their expected revenues have been expropriated.

Indonesia and South Africa are among many countries that faced such cases.

The Indonesian government has been taken to the International Centre for Settlement of Investment Disputes (ICSID) tribunal based in Washington by a British company, Churchill Mining, which claimed the government violated the United Kingdom-Indonesia BIT when its contract with a local government in East Kalimantan was cancelled.

Reports indicate the company is claiming compensation of US$1bil to US$2bil (RM3.3bil to RM6.6bil) in losses.

This and other cases taken against Indonesia prompted the government to review whether it should retain its many BITS.

South Africa had also been sued by a British mining company which claimed losses after the government introduced policies to boost the economic capacity of the blacks to redress apartheid policies.

India is also reviewing its BITS, after many companies filed cases after the Supreme Court cancelled their 2G mobile communications licences in the wake of a high-profile corruption scandal linked to the granting of the licences.

But it is not only developing countries that are getting disillusioned by the ISDS. Europe is getting cold feet over theinvestor-state dispute mechanism in the Trans-Atlantic trade agreement (TTIP) it is negotiating with the United States, similar to the mechanism in the TPPA.

Two weeks ago, Germany told the European Commission that the TTIP must not have the investor-state dispute mechanism.

Brigitte Zypries, a junior economy minister, told the German parliament that Berlin was determined to exclude arbitration rights from the Transatlantic Trade and Investment Partnership (TTIP) deal, according to the Financial Times.

“From the perspective of the [German] federal government, US investors in the European Union have sufficient legal protection in the national courts,” she said.

The French trade minister had earlier voiced opposition to ISDS, while a report commissioned by the UK government also pointed out problems with the mechanism.

The European disillusionment has two causes.

ISDS cases are also affecting the countries. Germany has been taken to ICSID by a Swedish company Vattenfall which claimed it suffered over a billion euros in losses resulting from the government’s decision to phase out nuclear power after the Fukushima disaster.

And the European public is getting upset over the investment system. Two European organisations last year published a report showing how the international investment arbitration system is monopolised by a few big law firms, how the tribunals are riddled with conflicts of interest and the arbitrary nature of tribunal decisions.

That report caused shock waves not only in the civil society but also among European policy makers.

In January, the European Commission suspended negotiations with the United States on the ISDS provisions in the TTIP, and announced it would hold 90 days of consultations with the public over the issue.

In Australia, the previous government decided it would not have an ISDS clause in its future FTAs and BITS, following a case taken against it by Philip Morris International which claimed loss of profits because of laws requiring only plain packaging on cigarette boxes.

In Malaysia, the ISDS is one of the major controversial issues relating to the TPPA. Many business, professional and public-interest groups want the government to exclude the ISDS as a “red line” in the TPPA negotiations.

Prime Minister Datuk Seri Najib Tun Razak had also mentioned investment policy and ISDS as one of the issues (the others being government procurement and state-owned enterprises) in the TTPA that may impinge on national sovereignty, when he was at the Asia-Pacific Economic Cooperation Summit and TPPA Summit in Indonesia last year.

So far, the United States has stuck to its position that ISDS has to be part of the TPPA and TTIP. However, if the emerging European opposition affects the TTIP negotiations, it could affect the TPPA as this would strengthen the position of those opposed to ISDS.

Meanwhile, we can also expect more countries to review their BITS. Developing countries seeking to end their bilateral agreements with European countries can point to the fact that more and more European countries are themselves having second thoughts about the ISDS.

Martin Khor is Executive Director of the South Centre. The views expressed are entirely his own.

Related News

CET: Is Nigeria ready for ECOWAS Common Market?

As the much anticipated uniform tariff for ECOWAS region will become reality from January 1, 2015, Olushola Bello looks at the benefits and implications of the Common External Tariff (CET)

Tariff For All

When a group of countries form a customs union they must introduce a common external tariff. The same customs duties, import quotas, preferences or other non-tariff barriers to trade apply to all goods entering the area, regardless of which country within the area they are entering. It is supposed to be designed to end re-exportation; but it may also inhibit imports from countries outside the customs union and thereby diminish consumer choice and support protectionism of industries based within the customs union.

The common external tariff is a mild form of economic union, but may lead to further types of economic integration. In addition to having the same customs duties, the countries may have other common trade policies, such as having the same quotas, preferences or other non-tariff trade regulations apply to all goods entering the area, regardless of which country within the area they are entering.

Important examples of Common External Tariff are those of the Mercosur countries (Brazil, Argentina, Venezuela, Paraguay and Uruguay) and the Common Customs Tariff of the Customs Union of Belarus, Kazakhstan and Russia. Similar to free trade areas, however, external countries have to pay tax on goods and services that are entering.

The South American as well as the eastern European examples of the CET and the customs union nations stated above, each have a country with the characteristics that Nigeria possesses in the West African region. At various social and economic levels, Brazil in South America and Russia in Eastern Europe are to their regions what Nigeria could be to the West African region.

History Of ECOWAS

In May 25, 1975, fifteen West African countries came together to form the Economic Community of West African States (ECOWAS), with the aim of making the region a strong economic powerhouse in Africa. The countries are Benin, Burkina Faso, Cape Verde, Côte d‘Ivoire, Gambia, Ghana, Guinea, Guinea Bissau, Liberia, Mali, Nigeria, Niger, Senegal, Sierra Leone and Togo. The lofty objectives of ECOWAS is to promote economic integration in all fields of endeavours, particularly industry, transport, telecommunications, energy, agriculture, natural resources, commerce, monetary and financial policies, social and cultural matters.

Rules Under The New CET

The Nigeria Custom Service came out with a new regime, five per cent duty is applicable for 2,146 tariff lines under the basic raw materials and capital goods category;10 per cent for the 1,373 tariff lines that qualify as intermediate products category; while 20 per cent duty is reserved for the 2,165 tariff lines under final consumer products. Some 5,899-tariff lines are covered under the new tariff regime with the rate ranging between zero and 35 per cent for the 130 tariff lines that fall into the category of specific goods that contribute to the promotion of the region’s economic development.

The CET is a precursor to a regional customs union, which is predicated on the harmonisation and convergence of national fiscal, monetary and trade policies of member states for the attainment of economic integration by the 15-nation economic community with a combined population of more than 300 million people.

With the view to enhancing the economic integration process in West Africa, the Authority of ECOWAS Heads of State and Government met in Extraordinary Session in Dakar, Republic of Senegal in October 2013 and agreed on the creation of a 1.5 per cent community integration levy, whose scope and operationalisation would be the subjects of further regional reflection, as part of the mechanisms to enable the regions cope with the challenges of implementation of the new tariff regime.

Example Of CET Benefits

Similar to these nations in terms of population, land mass, agro ecological endowments as well as skilled manpower availability, Nigeria potentially could be the biggest beneficiary of the West Africa customs union expected to kick-off in January 2015. Brazil and Russia effectively leveraged on size, capacity and resources as well as other more latent factors and have since become the leading powers not just in their sub regions but also in the entire world.

Before they kicked off the economic union with their neighbours, they took all the steps necessary to ensure that they took full advantage of all the nations’ God-given socio economic endowments which, within a relatively short time, helped them emerge as some of the world leading economies resulting in the now popular global economic acronym referred to as BRICS (Brazil, Russia, India, China and South Africa).

Benefits And Shortcomings Of CET

Stakeholders are of the view that the benefits of CET will increase turnover due to a larger domestic market; enlargement of member states industrial sector through higher economics of scale; higher production and productivity; higher capital accumulation (Economic growth) and strengthening of national institutions through peer learning among members.

Many empirical studies of the European Union have found that integration leads to higher economic growth; productivity growth; less macroeconomic fluctuations; increased intra-regional exports, and higher foreign direct investment. They attribute the shortcomings of the CET to loss of national trade policy, sovereignty to regional institutional arrangements; loss of lobbying ability by the producers and workers; low level of tariff which can lead to dumping and de-industrialisation; loss of government revenue coming from tariff.

Different Views

Analysts have said despite the benefits CET will have on the economy of the country, without proper dimensioning of the risks, rewards and how best Nigeria can put its natural and positional gifts to use to ensure that it takes full advantage of the opportunities, it might just bring to the country more harm than good.

With infrastructural conditions within Nigeria still a far cry from what is desirable and in most cases, worse than what is obtainable in smaller nations in the sub region; security challenges attaining unprecedented levels and fiscal as well as monetary policy indicators running amok, it is not difficult to conclude that Nigeria will very likely crash-land into the much anticipated customs union and lose the advantage of its mass market to its minuscule neighbours.

State Of Readiness

The director general of Lagos Chamber of Commerce and Industry (LCCI), Mr Muda Yusuf said the ECOWAS Council of Heads of States recently approved the new CET which shall come into effect on January 1, 2015. “We welcome the policy as it would advance the cause of economic integration of the West African sub-region. It is a move intended to improve the collective well-being of the citizens of the sub-region and promote the development of the various economies”, he said.

He pointed out that the move is also expected to consolidate the sub-region as a customs union and create a market of an estimated 500 million people as this offers great opportunities for investors through the advantage of economies of scale. Yusuf highlighted that the new policy regime includes scrapping of import prohibition list, scrapping of export prohibition list, abrogation of import duty waivers, abrogation of import levies and loss of sovereign authority on tariff policy.

Window Of Opportunity

The director general of the Nigerian Association of Chambers Of Commerce Industry Mines and Agriculture (NACCIMA), Dr John Isemede said that the effect of CET within ECOWAS region could discourage smuggling and promote regional trade. “The only key thing is that it should ordinarily reduce smuggling within the region.

“This is because what has promoted smuggling is disparity in tariff. If a product in Nigeria is attracting 70 per cent and the same product in Cotonou or Togo is attracting 10 per cent, it is likely that smugglers and other unpatriotic traders will follow the rules of the lowest tariff but if the same tariff obtains between Lagos and Mauritania then there is no advantage of smuggling by unscrupulous traders.”

He explained that implementing CET in the region will promote regional trade, “people will be able to plan better now because they know that the tariff will not change overnight, which has been a challenge for Nigeria in particular”. “If there is any need to change tariff, ECOWAS as a body must meet, the 15 countries as a group must agree to that tariff change. So that will make for better planning and companies will be able to plan long term, fully aware that their tariff will not change overnight and affect their investment output”.

Challenges Ahead

Isemede pointed out that West Africa is a sub-region and a custom union region due to different nations and currency, saying that countries like Nigeria, Ghana, Gambia are Anglophone nations while Togo, Benin, Burkina Faso, are Francophone. He explained that VAT is five per cent in Nigeria, 20 per cent in the francophone countries and then 15 per cent in Ghana, saying that if all these VAT are not harmonised, we can now talk about one external tariff. He added that cost of doing business in Nigeria is high when compared to other countries, that is why goods shipped into the country are cheaper than the ones made in the country. He called on ECOWAS to harmonise the different VAT in the countries for the smooth implementation of the policy. He, however, said that CET will not take Nigeria there except the VAT are harmonised as smuggling will still continue.

The president of Manufacturers Association of Nigeria (MAN), Kola Jamodu, said if the proposed CET is adopted by Nigeria as it is currently constituted, it would have huge implications for the Nigerian manufacturers. “We are of the view that if the CET is adopted as it is without giving consideration to MAN position, Nigeria will lose the right to use fiscal policy measures as instruments to attract foreign investments into the major sectors of the economy and would no longer be in a position to use fiscal policy as an effective instrument to protect its fledging manufacturing base, among others.”

Yusuf pointed out that the policy has a downside and the implications for the economy, particularly the manufacturing sector will be profound. “Currently, the Nigerian manufacturing sector suffers significant competitiveness issues which include the following: High energy costs, high costs of funds, high regulatory charges, high ports charges and other related charges, high cost of logistics amongst others”.

He stated that these are issues to worry about especially at a time when unemployment has become a major problem for the economy. Therefore in order to avoid the collapse of what is left of the Nigerian manufacturing sector, some immediate policy responses are imperative.

Way forward

In order for Nigeria manufacturing companies not to be affected by the adverse effect of CET, Yusuf proposed the following policy options Import duty on raw materials, machineries and other vital input for manufacturing should be scrapped, VAT on raw materials and machineries should be scrapped and there should be generous tax allowances on infrastructure related expenditures. Also, there should be strong anti-dumping measures to protect local industries.

He said that all these are essential for the Nigerian manufacturers to be able to remain in the business under the proposed CET regime. The President of Nigeria, Goodluck Jonathan has promised that Nigeria has successfully negotiated a strong CET agreement with ECOWAS partners on the need to protect the country’s strategic industries from foreign domination.

While the minister of finance, Ngozi Okonjo-Iweala also assured manufacturers that efforts were on gear to establish a development finance institution in order to make credit accessibility easy and reduce high cost of funds, emphasising that efforts would be made to ensure that Nigerian manufacturers gained from the forthcoming Common External Tariff scheme.

Related News

African Finance and Economic Planning Ministers’ Annual Conference holds in Abuja from March 25

The Seventh Joint AU Conference of Ministers of Economy and Finance and ECA Conference of African Ministers of Finance, Planning and Economic Development will be held on 25-30 March 2014 in Abuja, the Nigerian capital.

Organized by the United Nations Economic Commission for Africa and the African Union Commission in collaboration with the Nigerian government, the conference will bring together African ministers responsible for finance, economy and economic development, as well as governors of central banks and key leaders from the private sector.

With the theme: “Industrialization for Inclusive and Transformative Development in Africa”, the conference’s objective is to provide a platform for policy makers to articulate proposals for speeding up the implementation of the Accelerated Industrial Development of Africa (AIDA) and increase commitment and actions to advance Africa’s industrial development agenda.

“Building on the Joint Annual Session (2013) held in Abidjan, this conference will be an opportunity to identify challenges that need to be addressed at the national, regional, continental, and international levels to promote the coherent industrial development of Africa,” says Carlos Lopes, Executive Secretary of the (ECA). In 2013 member states were urged to adopt coherent industrial policies, create institutional industrial policy mechanisms and coordinate line ministries to improve policy implementation.

The 2014 Economic Report on Africa, jointly produced by the ECA and the AUC, will also be launched during the meeting. The theme of this year’s report is “Dynamic industrialization in Africa: innovative institutions, effective processes and flexible mechanisms.” Stressing the importance of industrialization as a “precondition for Africa to achieve inclusive economic growth,” the report offers an institutional framework for designing and implementing industrial policy in Africa.

The rationale for industrialization in Africa is grounded in the fact that most African economies concentrate economic activity in the extractive and commodity-producing sectors. In turn, the capital-intensive nature of the sector and the limited inter sectoral linkages between the primary sector and other sectors of the economy create limited opportunities for value chain development, value addition and job creation. Moreover, the primary sectors are characterized by low productivity and low wages which render employees vulnerable to poverty.

While countries are making concerted efforts in this regard, experts recognize that the road to industrialization is paved with challenges such as productivity and competitiveness necessary to take advantage of globalization and transform economies. Also, lack of infrastructure and technological advancement are constraints to doing business and undermines productivity.

“Reversing the status quo and making advances in technology or infrastructure will not happen by chance in the continent. Well thought out strategies with adequate allocation of resources in R&D, for instance, are required,” says Mr. Lopes.

Related News

African Development Bank President Kaberuka emphasizes the role of GVCs for Africa’s growth

The president of the African Development Bank, Donald Kaberuka, has expressed great optimism over Africa’s growth indicating that a full absorption of the continent into the global value chains is needed for job creation and transformation. The Bank’s president made the comment at an event held at the Graduate Institute of International andDevelopment Studies in Geneva on the topic “Africa in the new Millennium: Development Prospects and Challenges” on 20th March 2014.

This was subsequent to a three day Africa CEO Forum held in Geneva which saw the attendance of 800 CEOs of local and foreign companies operating in the continent. Recounting Africa’s growth over the past decade “…from a continent that was only known to worth additional aid to a one of 800 CEOs” Dr. Kaberuka believes they could be no better signs of growth.

He pointed out that Africa’s growth is attributable to “painful economic and political reforms undertaken in the 1990s” as well as external factors such as the emergence of the “new growth poles” in the global economy including India and China and the IT revolution which, he said, “reduces the cost of doing every business in the continent”. Citing various examples, he believes that the current landscape of the global value chain vis-à-vis outsourcing presents opportunities for job creation in the continent for future transformation.

He said natural resources, for example, which have previously been used to “buy arms” and promote conflicts is now used “to build the foundation of a future modern economy” and this has the capacity to close the infrastructure gap in the continent if investment in the infrastructure sector can be “de-risked” enough.

Africa’s trade prospects and economic notoriety took to the news in the millennium and many experts believe that the continent’s prominence in the global economy could soar higher frontiers with a good mix of economic, political and social policies. Current attention is growing in the role of the private sector in Africa and significance of international trade is emphasized across the region which has culminated into signing of numerous Free Trade Agreements. Experts believe the region is set for higher trajectories in the near future.

Related News

Rawlings blames Africa for being passive in global affairs

The African continent cannot continue to allow some members of the developed world to interfere and meddle in its affairs, while it becomes a passive observer.

The continent cannot look on while elected presidents are plucked out of their countries and humiliated in a crude manner.

A former President of Ghana, Mr Jerry John Rawlings, made these comments when he was addressing the 10th anniversary celebrations of the Pan-African Parliament in Johannesburg, South Africa on Tuesday.

The theme for the celebration was “Ten Years of the Existence of the Pan-African Parliament: Reflections on its Role”.

Today, Libya is but a pale shadow of itself, with militants ensuring, on a daily basis, that political authority does not take root, he lamented.

Spirit of determination

Mr Rawlings said some Africans had chosen to blame Laurent Gbagbo and al- Qathafi for the fate that befell their respective countries, but he refuted that and said the continent was equally to be blamed for looking on when the global powers entered the continent and virtually staged coups in countries.

“It is significant to note, however, that in the midst of the political turmoil Liljya finds itself, its national football team put up a brave and determined fight to win the CHAN tournament earlier this year,” he said.

He explained that the feat was a ckar manifestation that beneath all the pessimism and negativity laid a spirit of determination which had to be nurtured, guided and supported into a positive governance structure in the continent.

Strong voice

Mi Rawlings said the continent needed to merge its power into one meaningfully strong voice.

The said if the continent was keen on making its voice heard, then it could not continue to procrastinate in the matter of integration.

According to him, Africa has power in numbers and resources. It has power also in size and cultural uniqueness, and this can be blended into a powerful voice of reason.

“Integration may sound ambitious for a huge 54-member organisation, but continued delay further relegates the continent to the depths of irrelevance.

“We need to question why the West is so uncomfortable about the Ukraine and Crimea issue when evidence abounds of gross Western interventions in the recent past, as earlier stated, and in the distant and not too distant past,” he said.

He said the position of the West and their media, with respect to the Ukraine issue, was shocking.

He explained that the inconsistencies of the West, its hypocrisy arid the massive misrepresentation were an insult to the intelligence of the world.

Mr Rawlings said far lesser circumstances hadi elicited the overreaction, as well as the political and military intervention of th6 west, and yet.

A stronger justification from a historical point of view, from a security/military standpoint and the recent political behaviour in Ukraine had precipitated Russia’s reaction.

African Union

According to him, the continent cannot discuss the role of the Pan-African Parliament without placing significant emphasis on the African Union (AU).

The Pan-African Parliament was established as part of the ambitious plan to unify the continent and to integrate the continent not just economically, culturally and socially, but also politically, Mr Rawlings said.

He said the Pan-African Parliament had undeniably played a significant role in establishing various protocols of the African Union, thereby enhancing the AU’s relevance.

The Parliament has also offered significant support towards strengthening legislatures across the continent, and those structures were crucial to the eventual integration of the continent.

Mr Rawlings said notable among the roles of the African Union Parliament was the monitoring of elections across the continent.

“Your declaration of the August 2013 election in Zimbabwe as free and fair is commendable, although others sought to denigrate the process,” he added.

According to him, after 10 years in existence, there are questions about the autonomy of the Parliament and its lack of legislative powers.

Related News

New financing for Africa’s roads, rail without high debt

As Central African countries seek new sources of financing for infrastructure, policymakers will have to avoid high indebtedness, a conference in Cameroon was told.

Sub-Saharan Africa’s strong growth over the past decade has highlighted the importance of infrastructure development.

Senior officials, academics, business executives, and civil society figures from Central Africa and representatives of international financial institutions gathered in Yaoundé, Cameroon, on March 10 for a regional conference on “Financing the Future: Infrastructure Development in Central Africa.”

The one-day event examined options for infrastructure financing, including how to leverage existing financing and promote innovative alternatives. The event also emphasized the role of private capital in infrastructure financing.

Delegates heard, however, that a robust private sector response depends on the returns from public infrastructure investment. Infrastructure development should therefore proceed alongside reforms aimed at improving the business and investment climate. Appropriate safeguards, as well as review of the risks faced by governments, are also essential to effective private sector participation.

Public-private partnerships

The conference considered several core issues, including the need to optimize domestic financing, especially from natural resources, and streamline inefficient expenditure to free up fiscal space for investment; national and regional infrastructure projects; and domestic and international financing options, including public-private partnerships.

Central African officials acknowledged that infrastructure is critical to the region’s continued resurgence. They agreed that investing in infrastructure can boost growth, raise productivity, and assist poverty reduction. However, they noted that building and upgrading infrastructure is costly and implies large financing needs during the construction phase and for subsequent maintenance.

For Central African countries, increasing investment without taking on excessive debt will continue to be a crucial policy challenge. Conference participants widely agreed that a good debt management strategy is important as infrastructure investments are scaled up.

Right financing mix

The conference recognized that the right financing mix will depend on multiple factors, including financial development, indebtedness, business environment, and each country’s home-designed development strategy.

The conference also signaled the IMF’s commitment to strengthen its partnership with its African membership at a time ofoptimism about the region’s economic achievements and prospects.

Opening the conference, IMF African Department Deputy Director Anne-Marie Gulde-Wolf observed that “Better road and rail networks are necessary to increase regional trade and investment; higher levels of power generation will improve the productivity of businesses; better communication services will facilitate cross-border financial transactions; access to clean water and sanitation will improve the general health of the population, thus contributing productively to development.”

Savvy about scaling up

Gulde-Wolf stressed that while the choices of available financing options can open up opportunities for African countries, governments also have to be savvy about how they finance their scaled-up investments.

She added that the Cameroon conference is part of the build-up to a major conference on Africa jointly organized by the government of Mozambique and the IMF in Maputo, Mozambique.

The outcome of the Cameroon conference will be presented at the Mozambique conference, where representatives from sub-Saharan African countries will gather on May 29–30 to discuss “Africa Rising: Building to the Future”. Both Alamine Ousmane Mey, Minister of Finance of Cameroon, and Seth Terkper, Minister of Finance and Economic Planning of Ghana, will be among the panelists in Maputo.

Over the past six months, the IMF has held conferences in Kenya to examine the tasks that country faces as it moves toward emerging-market status, and in Ghana, where senior officials from West African Economic and Monetary Union countries discussed the challenges of regional financial sector integration.

Related News

Trade barriers worsen food insecurity

Africa is not achieving its potential in food trade. The growing demand for food is increasingly being met by imports from the global market. This, coupled with rising global food prices, is leading to ever mounting food import bills.

Clearly something has to change. Business as usual with regards to food staples in Africa is not sustainable.

Fortunately, there is a solution to this problem within Africa. The potential to increase agricultural production is enormous.

Yields for many crops are a fraction of what farmers elsewhere in the world are achieving, and output could easily increase twofold or threefold if farmers were to use updated seeds and technologies. Also, large swathes of fertile land in Africa remains idle. Open regional trade is essential because demand is becoming increasingly concentrated in cities, which need to be fed from food production areas throughout the continent. Different seasons, rainfall patterns and variability in production, which will increase as the climate changes, are not conveniently confined within national borders.

A model of food security based around national self-sufficiency is becoming more and more untenable. Cross-border trade in food provides farmers in Africa with the opportunity and incentive to supply the growing demand.

But the potential for farmers to satisfy much of the rising demand for food through regional trade is not being exploited. Currently, only five percent of continental imports of cereals is provided by farmers.

These farmers face more barriers in accessing the inputs they need and in getting their food to consumers in African cities, than suppliers in the rest of the world. Smallholders who sell surplus harvest typically receive less than 20pc of the consumer price of their products, with the rest being eaten away by various transaction costs and post-harvest losses. This clearly limits the incentive to produce for the market.

Many of the key barriers to trade in food staples relate to regulatory and competition issues along the value chain. As tariffs have come down, it has become increasingly apparent that a tangled web of rules, fees and high cost services are strangling regional trade in food.

In some cases, the policies that are restricting trade are deliberately protectionist. In many cases, however, they reflect poorly designed or badly implemented policies resulting from the lack of broad stakeholder participation and weak capacity in government departments and agencies.

Rules and regulations limit access to inputs of seeds and fertilisers and extension services, critical if productivity potentials are to be achieved. In Ethiopia, for instance, the use of improved hybrid maize could contribute to a quadrupling of productivity and completely replace commercial imports.

Transport and logistics costs, especially for small farmers, can gobble up as much as half of the delivered price of staples. While there is plenty of need for further improvements in infrastructure, the key reason for high transport costs is often the lack of competition. Transport cartels are still common in many regions, and the incentive to invest in modern trucks and logistics services are very weak.

Opaque and unpredictable trade policies also continue to raise trade costs. Trade in staples in Africa continues to be affected by measures such as export and import bans, variable import tariffs and quotas, restrictive rules of origin and price controls.

Often, these are decided upon without transparency and are poorly communicated to traders. This creates uncertainty about market conditions and limits cross-border trade.

Inefficient distribution services also hamper regional trade in food. Poor people in the slums of Addis Abeba pay more for food staples than the wealthy pay at supermarkets.

This shows that, in many countries, the distribution sector is not effectively linking poor farmers and poor consumers. Price controls imposed across the region and the cartels in place in several African countries represent a serious impediment to competition.

All these barriers raise costs and increase uncertainty, make regional markets smaller and increase volatility. Indeed, the price of maize in Africa has been more volatile than the world price of maize. Policies that reduce transaction costs and increase competition in the provision of services, affecting the production and distribution of food staples, would reduce the gap between consumer and producer prices.

The development of institutions that would support farmers in reducing risks and raising productivity is compromised when the trade policy environment for staples is difficult and uncertain. Effective standards regimes depend upon private sector involvement, but in many countries the process of defining standards is often dominated by government agencies.

Private investments in storage capacity, which would help to reduce the enormous post-harvest losses and allow farmers to sell when prices are most favourable, are undermined when policies that influence prices, such as export bans, are uncertain and lack transparency. Commodity exchanges, which have the potential to reduce transaction costs for farmers by reducing the number of intermediaries and improving the conditions of exchange, cannot thrive without even-handed and predictable policies. Operating across borders would allow exchanges to build a sufficient trading volume to exploit economies of scale and be more profitable.

Institutions that can help address food security concerns and so reduce the political risk from reform will only flourish if there is a change in the way that food trade policies are defined and implemented. For example, futures and options markets provide an alternative to holding physical stocks through food security reserves, and weather-indexed insurance can mitigate the impacts of climatic shocks on farmers.

Despite commitments towards opening up regional trade in food, implementation has been very weak. Few governments have sought to build a constituency for reform.

Opening up food staples to regional trade will lead to both winners and losers. Where reform reduces the mark-up between producer and consumer prices, it is farmers and poor consumers who will gain, while intermediaries earning rents, both in public sector agencies and in the private sector, will lose.

Reform becomes particularly difficult when politicians themselves are involved in the production and distribution of food. The absence of a stable and predictable policy environment breaks down trust and constrains private-sector investment in food staples, which in turn limits production and trade. And it encourages governments to continue to hedge against the failure of the private sector to adequately supply food when shortages do arise.

By and large, the nature and range of the barriers to trade along the value chain, and the need to invest in market-supporting institutions, shows that delivering an integrated regional food market involves more than a simple one-off commitment, and that reforms cannot be implemented at the stroke of a pen. Thus, for many policymakers, the goal of open and competitive regional markets will not occur during their electoral terms.

The reform strategy thus needs to define incremental steps that encourage investment by offering certainty to the private sector about policies. It should deliver real and visible benefits, while allowing policymakers to move at a pace consistent with their capacities and political risks.

A regional approach to food security in Africa will allow governments to more effectively and efficiently meet their objectives of ensuring access to food for their populations. This brings the prospect of not only benefits to farmers and consumers, but also of a significant number of new jobs in activities along the value chain of staples – in producing and distributing seeds and fertilisers, in advisory services, consolidating and storing grains, transport and logistics, distribution, retailing and processing.

Related News

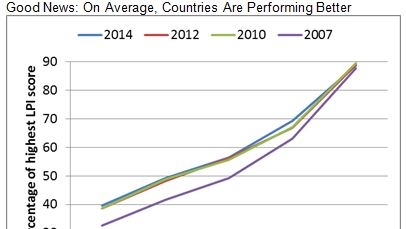

Logistics Performance Index (LPI) Report: The gap persists

The gap between the countries that perform best and worst in trade logistics is still quite large, despite a slow convergence since 2007, according to a new World Bank Group report released today. This gap persists because of the complexity of logistics-related reforms and investment in developing countries, and despite the almost universal recognition that poor supply-chain efficiency is the main barrier to trade integration in the modern world.

The report, Connecting to Compete 2014: Trade Logistics in the Global Economy, ranks 160 countries on a number of dimensions of trade – including customs performance, infrastructure quality, and timeliness of shipments – that have increasingly been recognized as important to development. The data comes from a survey of more than 1,000 logistics professionals. The World Bank Group’s International Trade Unit has produced the Logistics Performance Index (LPI) about every two years since 2007.

“The LPI is trying to capture a rather complex reality: attributes of the supply chain,” said Jean-François Arvis, Senior Transport Economist and the founder of the LPI project. “In countries with high logistics costs, it is often not the distance between trading partners, but reliability of the supply chain that is the most important contributor to those costs.”

In the 2014 LPI report, Germany showed the world’s best overall logistics performance. Somalia had the lowest score. As with previous editions, the 2014 report finds that high-income countries dominate the world’s top-ten performers. Among low-income countries, Malawi, Kenya, and Rwanda showed the highest performance. In general, the trend across past reports has been that countries are improving and low-performing countries are improving their overall scores faster than high-performing countries.

The 2014 report finds that low-income, middle-income, and high-income countries will need to take different strategies to improve their standings in logistics performance. In low-income countries, the biggest gains typically come from improvements to infrastructure and basic border management. This might mean reforming a customs agency, but, increasingly, it means improving efficiency in other agencies present at the border, including those responsible for sanitary and phyto-sanitary controls. Often, multiple approaches are required.

“You can’t just do infrastructure without addressing border management issues,” Arvis said. “It’s difficult to get everything right. The projects are more complicated, with many stakeholders, and there is no more low-hanging fruit.”

Middle-income countries, by contrast, usually have fairly well-functioning infrastructure and border control. They generally see the biggest gains from improving logistics services, and particularly outsourcing specialized functions, such as transportation, freight-forwarding, and warehousing.

In high-income countries, there is a growing awareness of – and a demand for – “green logistics,” or logistics services that are environmentally friendly. In 2014, about 37 percent of LPI survey respondents shipping to OECD countries recognized a demand for environmentally friendly logistics solutions, compared with just 10 percent of those shipping to low-income destinations.

In recent years, as tariffs have dropped globally, logistics and other aspects of trade facilitation have gained profile as an arena for reducing trade costs. A 2013 study by the World Bank Group and World Economic Forum found that reducing the high transactions costs and unnecessary red tape faced by traders could provide a significant boost to global GDP. In January, the World Trade Organization (WTO) finalized a “trade facilitation agreement” that sets standards for faster and more efficient customs procedures and contains provisions for technical assistance and training in this area. The World Bank and six other multilateral finance institutions supported the WTO’s efforts in a unified statement in October.

In this broad context, the LPI is increasingly respected by policy makers. In Indonesia, for example, the index is formally used to measure the trade ministry’s performance. The Asia-Pacific Economic Cooperation (APEC) organization uses the LPI to measure the impact of an initiative to improve supply-chain connectivity. The EU Commission has used the LPI in its Transport Scoreboard and in its 2013 evaluation of the EU Customs Union.

“The LPI is a concrete tool for raising awareness and spurring improvements,” said Jeffrey Lewis, Director of the Economic Policy, Debt and Trade Department. “It allows us to evaluate constraints across a broad set of countries.”

The World Bank Group’s support for trade facilitation improvements among its client countries has been substantial. The World Bank Group spent $5.8 billion in 2013 on trade facilitation projects, recognizing that logistics barriers hamper developing countries’ participation in the international trading system.

The LPI can provide a reference point, but it should not be considered an exhaustive diagnostic tool. The LPI is sometimes compared to the Doing Business ranking – and has some topical overlaps – but it differs in a number of ways. While Doing Business uses data on regulations that are “on the books,” the LPI uses survey data from logistics professionals who answer questions about their experiences in various countries. This approach is an effort to more accurately capture the day-to-day reality faced by the private sector.

Related News

Changing Times: How the MINTs are taking over from the BRICs

Is the party over for the BRIC economies? After years of hype, Brazil, Russia and India have enjoyed impressive growth but appear to have lost their shine.

China, the world’s second-largest economy, which has at times had growth in the double-digits, is worrying markets as it appears likely to slow down.

Over the years, analysts have put their hopes on other groups of promising emerging economies, from the CIVETS group to the Next 11.

And now Jim O’Neill, the former Goldman Sachs economist who famously coined the term BRIC, is leading the charge for Mexico, Indonesia, Nigeria and Turkey, otherwise known as the MINTs.

O’Neill maintains that China is of huge economic significance – he has joked that he should have originally opted for the term “C” rather than “BRIC” – and is not eager to write off the other economic giants he first brought to prominence in 2001.

But he believes the MINTs, which he has covered in a recent book as well as a BBC documentary, have a number of reasons for optimism.

He notes that they have large, relatively young populations, meaning that they could grow extremely quickly over the coming decades without having to boost their productivity – unlike much of the west, where ageing populations lurk.

He also points out that each of the MINT nations enjoys an excellent location for future trade, particularly as new global powers emerge.

Mexico is neighbour to two huge markets in the form of the USA and Latin America. Indonesia sits at the heart of Southeast Asia. Nigeria, O’Neill has argued, could benefit hugely from being in Africa if nations there become more stable and eager to trade. And Turkey has the advantage of straddling the border between the east and west.

As O’Neill acknowledges, expectations may be low for these markets. The group has been dogged by problems well known to emerging market investors, from Turkey’s heavy-handed government to corruption in Nigeria. And it is not the first set of emerging markets to be highly praised, only to disappoint investors.

But he believes the markets may be pleasantly surprised. O’Neill, who travelled around the countries on research last year, meeting some of the business and political elite, has reminisced about the “wow” factor he got from witnessing major projects in Turkey and Nigeria.

While O’Neill may not be alone in such optimism, it is yet to be seen if investors are won over, and if the MINTs can overcome people’s reservations over the coming years.

Kate Phylaktis, director of the emerging markets group at Cass Business School, argues that while the group has huge potential, much work needs to be done.

“There are a lot of young people wanting to work, which is not the case in some of the other countries,” she says. “That is in their favour, but they have to create the opportunities for these people to work. They need the mobilisation of capital to create these opportunities by attracting foreign investment, because they have poor levels of education and infrastructure.”

She argues that attracting foreign investment is currently a difficult task for many of the emerging markets. Earlier this year, the tapering of quantitative easing was followed by capital flight from such investments. This ended with central banks in some countries, including Turkey, having to fight to shore up their currency, as investors moved to perceived safe havens.

As tapering continues and the threat of a Chinese slowdown looms, there may be similar crises to come in 2014 and beyond.

This could be a challenge to central banks, tasked with defending their currencies. And Phylaktis believes that more developed emerging markets, such as the BRICs, could fare better because of greater experience.

“The more developed the economies, the less affected they will be,” she says. “I think one advantage the BRICs have to the MINTs is their financial markets have a greater depth.

“In China, they were able to handle the [currency crisis] situation. Giving the impression you can handle the situation is important, and I don’t think the MINT countries have that.”

The MINTs may still lack the prestige of the BRIC group, but their future looks brighter than in the west, where recent years have been spent struggling to shake off the effects of the financial crash.

In 2014, the World Bank expects Turkey to grow by 3.5 per cent and Mexico by 3.4 per cent. Indonesia is expected to grow by 5.3 per cent, and Nigeria 6.7 per cent.

In the next few years, the World Bank expects MINT growth to plateau or rise only slightly. This is a long way from China’s peak, when it was growing by between 10 and 12 per cent. But the MINTs have natural strengths, and there is plenty of room for reform. While the BRICs are unlikely to go away, Jim O’Neill may have found a new success story.

Related News

Negotiators meet on trade, transformation and Africa’s role in global markets

At a retreat of African World Trade Organization negotiators this week, the Executive Secretary of the Economic Commission for Africa, Mr. Carlos Lopes said that the benefits of Africa’s trade negotiations will be judged against the capacity of international trade to spur a far-reaching transformation of the Continent’s economies. The transformation would be capable of providing employment to our youth, and lifting the standards of living of millions of poor Africans.

During the two day retreat, participants discussed key multilateral trade issues, including how Africa’s integration into the global market can best serve the objective of transforming the Continent’s economies.

Mr. Lopes noted that not all patterns of specialization are the same: some leave you entrenched in the production of raw materials in an extractive mode of production reminiscent of the colonial times, while others allow you to gradually exploit the learning by doing, and climb up the product ladder towards increasingly sophisticated goods.

“We should not focus on trade as an end in itself, but rather as a spring board to support structural transformation. A springboard that is all the more necessary, since the majority of African economies represents rather small markets,” he said.

Touching on the outcome of the recent agreement achieved at the 9th WTO Ministerial Conference in Bali, Mr. Lopes highlighted some positive elements for Africa such as the revival of the multilateral process, whose relevance had been threatened by the prolonged stalemate of the Doha Development Agenda and by the proliferation of bilateral agreements and the move to plurilateral negotiations.

He, however, stressed that many of Africa’s own priorities within the Doha Development Agenda have either remained unsolved – notably on Agriculture and Special and Differential Treatment – or have found only a partial and often non-binding solution as is the case for Duty Free Quota Free market access for LDCs, preferential rules of Origin, and the removal of agricultural export subsidies by developed countries.

The retreat is being held in the context of agreed collaboration between the UN Economic Commission for Africa and the African Group through the AU mission in Geneva in response to issues pertaining to the 9th WTO Ministerial Conference of Bali. Over the last year, ECA has provided financial and substantive assistance to the African Group of negotiators, with the aim of contributing towards forging a common regional position.

Participants included representatives from WTO, UNCTAD, and International Trade Centre, as well as the South Centre, International Centre for Trade Sustainable Development (ICTSD), and Advisory Centre on WTO Law (ACWL).

Related News

Africa must do more to unlock opportunities of rising intra-African trade

Growth in intra-Africa trade is outpacing trade between Africa and rest of the world. However, more needs to be done to boost intra-African trade to take advantage of the increasing commercial depth of Africa’s rapidly expanding consumer markets.

Exports by African countries to their peers on the continent has surged by 32% since the 2008 economic downturn, compared to growth of just 5% in exports to the rest of the world. Nevertheless, in 2011, intra-African trade accounted for merely 9% of the continent’s total trade with the world, compared to 25% for Latin America and almost 50% for Asia.

Ms Anne-Marie Woolley and Ms Megan McDonald, joint heads of Standard Bank’s Structured Trade and Commodity Finance (STCF) business in Africa, believe that given the right focus, intra-African trade can be a driving force for growth in Africa.

“Although intra-African trade has grown significantly over the last five years, it is off a very low base and remains vastly below par when compared to other developing regions of the world,” said Ms Woolley, Head of Standard Bank’s London-based STCF Team. “Yet while there are challenges, there are substantial opportunities that can arise from boosting intra-African trade, particularly when one considers that sub-Saharan Africa is expected to grow by more than 6% this year, outpacing most of the developed world in terms of growth.”

Some of the structural issues impeding intra-African trade include poor road and rail infrastructure, restrictive tariff structures, the unavailability of foreign exchange and the lack of trade-related financial solutions. While African governments are well-placed to assist in addressing the structural barriers to trade on the continent, equally so are financial institutions able to take the lead in attending to the problems impacting the availability of financial services.

“With many international banks having reviewed their risk appetite and subsequently withdrawing from, or limiting their exposure, to trade finance in Africa, an opportunity exists for local banks to step into the vacuum,” said Ms McDonald, Head of Standard Bank’s Johannesburg based STCF team. “Much of the growth in regional trade can be attributed to finance provided by African banks, being able to leverage off their local market knowledge and ‘on the ground’ presence and thereby acting as important catalysts in driving regional trade activity.”

Evidence of the dormant opportunities that can be unlocked by boosting trade within the continent is particularly true of the agricultural sector, which has the potential to provide more immediate benefits than manufacturing, which takes far longer to develop.

Intra-African flows account for about 20% of Africa’s total agricultural trade activity, compared to averages of 78% for the European Union and 60% for Asia. While African countries produced just 3.5% of the world’s rice in 2011, they were responsible for 35% of global rice imports that year, indicating the potential opportunities that exist for the continent’s rice producers.

Ethiopia is another clear example, accounting for as much as 40% of Africa’s coffee exports. Yet in spite of this, Ethiopia made just 3% of the USD1.2 billion it earned by exporting coffee beans in 2012 by doing business with other African nations.

“The trade data shows what can be achieved if African nations made greater strides in conducting trade with each other,” said Ms Woolley.

“They could potentially unlock billions of additional dollars simply by placing more focus on trading with their African peers.”

South Africa, the continent’s largest economy, is also missing out on potential trade opportunities within Africa. Of the USD2.3 billion South Africa earned by exporting fruit in 2012, only 8% came from the rest of Africa; with Angola absorbing 15%, followed by 12% for Benin and 11% for Mozambique.

Similarly, other African nations could benefit by boosting their trade links with South Africa. Of the USD1.2 billion of South Africa’s expenditure on cereal imports in 2012, just USD19m (1.5%) was sourced from other parts of the continent; while 15% of the USD86 million of coffee imported into South Africa in 2012 originated from Africa.

Nevertheless, there are certain “bright spots” on the continent where intra-African trade is flourishing. Standard Bank research shows that East Africa enjoys by far the deepest levels of trade integration on the continent.

Of the total exports from the five-member East African Community (EAC), 43% are directed to the rest of Africa, a ratio consistent with levels observed in Asia. On an individual basis, 49% of Uganda’s exports were absorbed by African partners in 2011, followed by 48% for Kenya, 36% for Tanzania and 35% for Rwanda.

In contrast, trade integration within the Southern African Development Community (SADC) is comparatively low, with just 14% of its member economies’ total exports going to other African markets. The Economic Community of West African States (ECOWAS) and the Common Market for East and Southern Africa (COMESA) have similarly low levels of trade integration with the rest of the continent, with the export ratio standing at a mere 15% for both trade blocs.

“There is definitely an opportunity for the various regional trading blocs in Africa to work more closely together,” said Ms McDonald.

“Greater cooperation in areas such as harmonising tax regimes, lowering tariff barriers, improving infrastructure, streamlining bureaucratic barriers and promoting the free-flow of goods across borders could pay huge economic dividends over time.”

Related News

Africa Clean Energy Corridor to boost renewable energy

Energy ministers and delegates from 19 countries committed to the creation of an ambitious initiative, the Africa Clean Energy Corridor, at a meeting in Abu Dhabi, convened by the International Renewable Energy Agency (IRENA). The Corridor will boost the deployment of renewable energy and help to meet the rising African energy demand with clean, indigenous, cost-effective power from sources including hydro, geothermal, biomass, wind and solar. The ministers and delegates endorsed the Action Agenda on the eve of IRENA’s Fourth Assembly, set to begin on January 18 in Abu Dhabi.

“The Africa Clean Energy Corridor will provide the continent with the opportunity to leapfrog into a sustainable energy future,” Adnan Z. Amin, IRENA’s Director-General said at the meeting. “The dynamic development that Africa will see in the next decades needs to extend to the energy sector, and Africa’s abundant renewable energy resources are a perfect match to meet rising demand in a sustainable and cost-effective way – from Cairo to Cape Town.”

Electricity demand is expected to triple in Southern Africa, and quadruple in Eastern Africa over the next quarter-century. As power demand multiplies, the region’s current dependence on fossil fuels becomes increasingly economically and environmentally unsustainable. A regional approach to developing the vast renewable energy resources will help optimize the energy mix and attract more investment. The Africa Clean Energy Corridor builds on, and adds to, the transmission network laid out in existing programmes for infrastructure development in Africa.

“The Africa Clean Energy Corridor helps leverage the tremendous opportunity that renewable energy presents, for the best of the African states and the entire continent,” H.E. Alemayehu Tegenu, Ethiopia Minister of Water, Irrigation and Energy, said. “The fact that IRENA, with its resources and know-how, is able to facilitate this large-scale, trans-border initiative demonstates the importance of the organisation for Africa and the deployment of renewables.”

The Action Agenda includes the identification of renewable power development zones to cluster renewable plants in areas high with renewable resource potential; integrated resource planning to include greater shares of renewable energy in the energy mix; new financing models and investment frameworks; knowledge and capacity building by IRENA; and public information campaigns.

——————–

About the International Renewable Energy Agency (IRENA)

The International Renewable Energy Agency (IRENA) is mandated as the global hub for renewable energy cooperation and information exchange by 124 Members (123 States and the European Union). Over 43 additional countries are in the accession process and actively engaged. Formally established in 2011, IRENA is the first global intergovernmental organisation to be headquartered in the Middle East.

IRENA supports countries in their transition to a sustainable energy future, and serves as the principal platform for international cooperation, a centre of excellence, and a repository of policy, technology, resource and financial knowledge on renewable energy. IRENA promotes the widespread adoption and sustainable use of all forms of renewable energy, including bioenergy, geothermal, hydropower, ocean, solar and wind energy in the pursuit of sustainable development, energy access, energy security and low-carbon economic growth and prosperity.

Effective regional integration demands ending protectionism

Uhuru Kenyatta, the charismatic president of Kenya, is one of the most popular African figures on social media platforms. His 375,000 followers receive updates about his government through his official Twitter account. For a leader who faces accusations from international institutions, such as the International Criminal Court (ICC), and Western governments, for his alleged involvement in the post-election crisis of 2008, the online sphere seems to have provided him a rare frontier to build a unique political base.

For Kenyatta, Twitter seems to be a place where he addresses the personal side of governing, embedded with less bureaucracy and protocol. Of course, there is enough manifestation of political correctness in his tweets. Nonetheless, he seems to have a very good grasp of balancing populism and integrity.

His tweets relating to the state visit he made to Ethiopia last week were no different. They show the intimate side of a president of a nation that aspires to build economic hegemony in Eastern Africa, using its competitive advantage in the services and manufacturing sectors. One of the tweets he made on March 12, however, signifies his ambition to enhance the economic relationship between Kenya and Ethiopia, in a different way to how it has for long been.

“For far too long, we have completely ignored growing trade and investment between Kenya and Ethiopia. That is something that I intend to turn around,” Kenyatta tweeted.

As much as the tweet is about Kenya, it is also about Ethiopia. Ever since they came into power, the Revolutionary Democrats have been shy about opening the border for enhanced trade and investment. Their economic policies have largely been oriented towards protectionism, especially of strategic sectors, such as finance, telecommunications and agriculture.

Now, Kenyans seem to favour a more open business regime in the very sectors that the EPRDFites are committed to maintaining a stronghold. They wish to expand their leverage in these sectors and establish a strong presence in the largest market of the East African region.

Surely, the sensitivity of the EPRDFites for opening up the borders for more trade and investment emanates from the structural weakness of the very economy they lead. Largely dependent on the rain-fed, subsistent and smallholder agriculture, the economy is not sufficiently matured in industrial and services production. Whatever is gained as a surplus from the agriculture sector is flowing to industry so slowly that structural transformation remains distant.

Even the intensive addition in production capacity and market linkages being created through huge public investment in infrastructure is not facilitating industrial development as expected. Hence, the nation’s economy performs well below the other economies of the region, not to mention Kenya.

This very emphasis of the ruling EPRDFites on the structural fault lines of the Ethiopian economy seems to be what caused them to refuse proposals of regional integration. One would, therefore, predict what officials of Prime Minister Hailemariam Desalgn’s Administration might have felt in listening to Kenyatta’s aggressive speech about swift regional integration.

Certainly, they would prefer a rather less hasty integration, with priority given to inter-country infrastructure development. Hailemariam’s suggestion of a special economic zone (SEZ) on either side of the border could be taken as a valid signal to the preferences of his administration when it comes to regional integration.

Of course, this stance of the EPRDFites has for long been firm. In all international and local forums, wherein the issue of regional integration has been debated, the Revolutionary Democrats have been declaring their preference to a regionalisation that prioritises infrastructure development.

In their favour, the infrastructure base of the nation has seen tremendous enhancement over the past two decades of their reign. Major economic backbones, such as telecommunications, energy, roads, housing, health and education, have seen a major leap forward under their leadership. Access to services relating to these backbones has, therefore, witnessed a considerable improvement. No doubt that their push in these sectors – evidenced by the more than 80pc share of total public investment – has a lot to contribute to the persistent growth of the economy, averaging 10.6pc, according to World Bank records, over the past decade.

It all ends there, however. The infrastructural base is not translating into competitive industrial and service value addition that enables the nation to compete with its neighbouring peers. Therein lies the deep seated insecurity of the ruling EPRDFites towards enhanced regional free trade areas, such as the East African Community (EAC) and the Common Market for Eastern & Southern Africa (COMESA).

If one is to go by the historical stance of the EPRDFites, and the evidence developed under their sponsorship, the desire of Kenyatta may take more time to be realised. Not even the ratification of the Special Status Agreement (SSA) that the two nations signed in 2012 is enough, as it settles for a consensus that falls short of full liberalisation.

Regardless of the compendium of evidence produced under the sponsorship of the Revolutionary Democrats- including the latest study on the pros and cons of joining COMESA, undertaken by professors at the Addis Abeba University (AAU)- global evidence shows that regional trade integration has a lot to offer to national economies. These entail increased investment flow, better market outreach, productivity gains, macroeconomic resilience and improved shock absorption capacity.

According to a study published by the African Union, African Development Bank (AfDB) and the United Nations Economic Commission for Africa (UNECA), one percent trade integration in Africa could result from a two percent to 2.5pc expansion in gross domestic product (GDP). Members of the COMESA free trade area (FTA), for example, have seen a two percentage point increment in their merchandise export share to GDP.

Ethiopia could be no different. After all, its protectionism has not helped it create competitive national industrial and service champions. Hence, its loss from opening trade up to regional players could not possibly be greater than its benefit.

That is why Hailemariam and his comrades ought to take the desire of Kenyatta seriously and work towards its realisation, albeit in a way that fits with the comparative advantage of the very economy they oversee. They can no more afford to refuse the discussion of regional integration and shy away from regional free trade areas.

Regionalising the local policy framework, both macroeconomically and sectorally, could be a starting point. This certainly involves indentifying the strengths and weaknesses, pros and cons of regional integration in each sector of the economy. The effort could then move towards putting in place concrete institutional and policy solutions to optimise the nation’s benefit from regional integration.

Preparing the business sphere for the tide of regionalisation is also important. It ought to be made clear to them that protectionism is an unsustainable path. Anything that is to long last must be built under competition.

As Kenyatta rightly said, it has taken far too long for the era of protectionism to end. No country, not least Ethiopia, can afford to live under the comforts of protectionism. It is now time to jump onboard regional integration with full gusto.

Related News

Africa CEO Forum 2014: African Business leaders gather in Geneva

The AFRICA CEO FORUM 2014, one of the most important gathering of African business leaders taking place in Geneva from 17 to 19 March, has been officially opened.

Organised by Groupe Jeune Afrique in partnership with the African Development Bank(ADB), the second AFRICA CEO FORUM welcomed “680 participants, speakers and journalists from more than 38 countries”.

This level of participation is already a measure of the success of this year’s AFRICA CEO FORUM, whose mission is to bring together economic actors from French and English speaking Africa to strengthen regional ties, promote public-private sector dialogue with the goal of building an environment conducive to new business development. It further stimulates African entrepreneurship, innovation and creativity.

The opening ceremony, chaired by Donald Kaberuka, president of the African Development Bank and Amir Ben Yahmed, Managing Director of the Groupe Jeune Afrique and Chair of the AFRICA CEO FORUM, recalled the primary purpose of this major event.

“The year 2013 was marked by a new 16% progress of foreign direct investments. The IMF is forecasting a global growth of 6.5% for 2014. I have lost count of the number of Africa CEOs who are now part of the international rankings of the economic press.

However, we cannot ignore the fact that most of the emerging countries which were considered only a few months ago as the engines of the world economy are today transforming into weak links. So when we elaborated the programme of this second edition of the AFRICA CEO FORUM we intended to take hindsight and reflect together on the ways of accelerating the transformation of our continent”, recalled Amir Ben Yahmed.

A first day of rich an substantive discussions

The first day of the AFRICA CEO FORUM, comprising one plenary session and two knowledge sessions devoted to key topics such as the competitiveness of African companies and the issue of local transformation of the continent’s natural resources, was enriched by the contributions of several high-profile speakers from Africa and the rest of the world.

For Moulay Hafid ELALAMY, Minister of Industry, Trade, Investment and Digital Economy: “We have a current competitiveness and it will persist only if Africa continues to wake up”

“This issue of competitiveness is critical if we want to continue and attract foreign investments and develop human capital, promote employment and thus, further develop this middle class and the local market implied for the CEOs” noted Amir Ben Yahmed.

“When there is discussion around the African economy, there are so many different views. The reality is that they all reflect a certain reality. One thing is certain though, and on this there is a broad consensus. People agree on the imperative of Africa moving up the regional and global value chains, and providing all the services associated with that… We are here to figure out how to take Africa to the next stage. From ‘hopeless’, to ‘rising’, to ‘hopeful’. The African Development Bank is proud to be your partner in this journey. Together we will take Africa to the next level”, added Donald Kaberuka.

Thanks to its rich and substantive programme, composed of high-level sessions and one-to-one business meetings, the AFRICA CEO FORUM 2014 has become the place to be for all those driving the continent’s growth.

About the Africa CEO Forum

Developed in partnership with the African Development Bank, the AFRICA CEO FORUM is an event organised by Groupe Jeune Afrique, publisher of Jeune Afrique and The Africa Report, and by Rainbow Unlimited, a company specialising in the organisation of business promotion events and manager of the Swiss-African Business Circle (SABC).

Related News

Why should the SADC EPA allow export taxes?

Negotiations on the SADC EPA are close to completion, but to finalize the deal limitations on export taxes should be abandoned. An acrimonious battle on the issue will impose more costs than allowing export taxes.

On 1 October 2014, the ten-year negotiations on free trade agreements between the European Union and groups from Africa, the Caribbean and the Pacific (ACP) will come to an end. It remains uncertain if all parties will have completed their Economic Partnership Agreement, or EPA. But on that day in October, regardless of the state of the deal, the EU will put an end to the difficult and at times acrimonious negotiations. The stakes remain high. The EPAs are meant to replace the long-standing Cotonou agreement, which gave ACP countries duty-free access to the wealthy European market. This access provided a competitive edge that will disappear if no agreement is reached. In SADC, Botswana, Namibia and Swaziland would lose duty free access to the profitable EU market; while South Africa and Angola, Mozambique and Lesotho would maintain access under the Trade Development and Cooperation Agreement (TDCA) and Everything But Arms agreements respectively.

Thankfully, the negotiations on a Southern African Development Community (SADC) EPA are close to completion, but a range of the most difficult issues have been left until last, and must now be overcome. Five remaining issues have consistently stood in the way of the completion of a deal. They are export taxes, the Most Favoured Nation (MFN) clause, agricultural safeguards, rules of origin, and regional integration. Each barrier remains important, but export taxes are particularly divisive. A change of mindset on the issue and a removal of requirements on export taxes would be a welcome step towards completing a workable EPA.

Fairness vs. policy space

Exports taxes are, as the name suggests, duties placed on exports. Export taxes are usually applied to commodities, in an attempt to divert supply of the good away from the export market and into the domestic market, thus driving the price up internationally and down locally. While they have sometimes been used to generate government revenue or improve food security, the primary use of export tariffs is to encourage local processing and beneficiation of basic goods. The EU insists on a ban on all export taxes for South Africa and Angola, and a ban on export taxes for other SADC EPA countries in all but a few extreme cases.

The EU sees export taxes as fundamentally unfair. Export taxes can drive up prices, harming the importer – in this case the EU – while relatively wealthy countries like South Africa benefit at their expense. The EU sees Africa as a vital strategic source of basic commodities, and is concerned about anything that can interrupt their supply of cheap raw materials. African countries see export taxes as a means to move up the value chain, and to break the colonial relationship in which they sell unprocessed goods to the rich world, and then buy back processed goods, making a loss in the process. They see the development of domestic processing as way to industrialize, creating jobs and moving the continent up the value chain. Both positions are legitimate, but there is nevertheless a clear avenue for resolution on export taxes.

The SADC EPA should allow export taxes

Simply put, the EU should abandon its objection to export taxes, for three reasons.