Search News Results

Reserve Bank of Zimbabwe: 2016 Mid-Term Monetary Policy Statement

Walk The Talk to Restore Trust and Confidence

Background and Context

This Mid-Term Monetary Policy Statement is issued in terms of Section 46 of the Reserve Bank Act (Chapter 22:15). The major objectives of this Statement are to highlight the global and domestic financial developments; to provide an assessment of the monetary policy measures taken by the Bank in May 2016 to stabilize the economy; to present new measures to restore confidence within the economy; and to offer policy advice to deal with the fiscal and current account deficits in order to change Zimbabwe’s economic narrative to production and productivity which is very vital or imperative to restore trust and confidence within the national economy.

The policy measures presented in this Statement are designed to augment the measures taken by the Bank in May 2016. The new measures include the elimination of administrative hurdles of contracting offshore loans, resuscitation of the credit guarantee scheme to enhance local production by small to medium scale enterprises, putting in place nostro stabilization facilities to deal with delays in the remittance of outgoing foreign payments, promotion of internal devaluation using market-based mechanisms to restore competitiveness in the national economy, and encouraging the fast-track elimination of bottlenecks that are hampering the ease of doing business within the economy especially in the export production sectors.

The measures and policy advice which are well aligned to those presented by the Honourable Minister of Finance and Economic Development in the Mid-Term Fiscal Review Statement are designed to deal with the structural imbalances that continue to stress the economy. The structural imbalances are evidenced by the large current account and fiscal gaps generated by the difficult internal and external conditions, a legacy of dollarisation policy inconsistencies/contradictions, policy slippages and procrastination in the implementation of critical Government policies. These imbalances are further exacerbated by adverse weather conditions and weak investor sentiment leading to the under performance of the national economy.

The under performance of the economy which started in 2012 – three years after dollarisation – is also greatly attributable to the legacy of policy inconsistencies/ contradictions when the country went into dollarisation in March 2009, by default and not by design, to tame hyperinflation. This was soon after the formation of the Government of National Unity in February 2009. The policy inconsistencies/contradictions which were secondary to the political settlement include over liberalisation of both the current and capital accounts at a time when the country had very limited access to foreign finance due to debt overhang, and non- conducive investment climate due to sanctions and unattractive domestic investment policies; wrong choice of trading currency and; failure to benchmark with regional comparators to maintain competitiveness.

It is therefore a combination of the current internal and external imbalances and historical challenges that need to be urgently addressed for the proper functioning of the multi-currency exchange system that, de facto, is currently totally dominated by the use of US$. This situation requires the nation to do things differently and WALK THE TALK to transform the economy by changing the narrative from consumption to production. The economy is hungry for production and productivity. With the public sector wage and salary bill being one of the highest in the world at more than 90% as a share of fiscal revenue and inflation at -1.4% being low or in negative territory (deflation) for two years now since 2014, real wages and salaries have increased, crowding out capital and social expenditure – thus undermining the economy’s capacity to enhance employment and to be competitive.

The business climate, on the other hand, affected by limited access to foreign finance; unfinished business on land security tenure and investment regulations; and high input costs, has not been conducive to attracting the much needed domestic and foreign investment. In addition the increasing fiscal gap in the absence of external financing has led to a decline in private sector activity and a reduction in domestic credit as financial institutions try to contain foreign exchange induced demand pressures attributable to lending activities.

As if the above harsh conditions are not enough, the economic impact of the El-Nino induced drought also increased the need for imports to reduce food insecurity, whilst the decline in mineral prices depressed export proceeds. In addition, amid low investor sentiment, the appreciation of the US$ induced higher than expected demand for this currency, reduced remittances in US$ terms, especially from South Africa and the United Kingdom (following Brexit) and generated speculation. With South Africa being Zimbabwe’s main trading partner – accounting for around 50% of total trade – where the rand depreciated against the US$, competitiveness has also been severely eroded.

Whilst efforts taken by Government to deal with the above fragile economic situation have been commendable, a stronger than anticipated impact of exogenous shocks highlighted above continued to exacerbate the economic slowdown and precipitated the decline in fiscal space and the cash shortage situation.

Walking the Talk within the above context of weak economic conditions requires policy precision and urgent implementation of necessary reform measures to transform the economy. The process won’t be easy but must be done. It requires national sacrifice, sincerity and integrity. It requires the ability to share the adjustment or transformation burden across the board and between the fiscal and monetary policies. Reliance on one policy instrument to manage the current structural imbalances would not be sustainable to transform the economy and to restore trust and confidence.

Overall, transforming the economy from a consumptive to a productive one requires fiscal discipline, production discipline, policy discipline, and message/communication discipline (speaking with one voice) in order to achieve the optimal levels of economic turnaround depicted by the following economic functional identities:

i. Liquidity = f*(Exports/Forex Earnings)

ii. Exports/Import Dependence = f(Production)

iii. Production = f(Investment Climate/Incentives/ Ease of Doing Business)

iv. Investment Climate = f(Policy Measures/Policy Consistency)

* f is read as function of

The rest of this Monetary Policy Statement is organized as follows; Section 2 discusses external sector developments and their implications on domestic economic activities. Section 3 looks at the status of the financial sector. Section 4 discusses the impact of policy measures introduced by the Reserve Bank in May 2016. Section 5 provides new policy measures to enhance confidence and production in the economy. Section 6 provides policy advice and Section 7 is the Conclusion. The Appendices provide an update on the re-engagement, a brief RTGS and Nostro concepts within the context of the multi-currency exchange system and an update on closed banks.

External Sector and Inflation Developments

Global Economic Developments

Global economic recovery has remained fragile with adverse consequences on developing economies like Zimbabwe. The situation has been exacerbated by the referendum outcome which approved Britain’s exit (Brexit) from the European Union.

The Brexit vote has deepened economic, political and institutional uncertainty within the EU, threatening the growth momentum witnessed in the first half of the year. This uncertainty has negatively affected investor confidence and financial market conditions. Moreover, the bumpy adjustment in China also continues to undermine sustained global economic recovery.

The recent global economic developments, have compelled the International Monetary Fund (IMF) to downwardly revise the initial global economic growth projections for 2016, by 0.1 percent, on account of the negative macroeconomic consequences, especially in advanced European economies. Consequently, the IMF is now projecting the global economy to grow by 3.1 percent in 2016 and 3.4 percent in 2017.

Growth in Sub-Saharan Africa is expected to decelerate from 3.3% in 2015 to 1.6% in 2016, representing a 1.4% decline from the initial forecasts in April 2016. This slowdown is primarily driven by the downturn in international commodity prices and Brexit fallout. Moreover, economic growth prospects for regional economies, notably, South Africa, Botswana and Zambia remain vulnerable to the downturn in international commodity prices and the depreciation of domestic currencies.

International Commodity Price Developments

International commodity prices have generally remained subdued over the recent past mainly on account of weakening growth prospects in China, the world’s largest metal consumer. This notwithstanding, global commodity prices reflected a modest recovery, albeit from a low base, during the first half of 2016 on the backdrop of transient stabilisation of global markets.

Specifically, gold prices firmed by 16.3%, from an average price of US$1 096.68/oz in January 2016 to US$1 274.99/oz in June, 2016. Similarly, platinum increased by 15.3% from US$853.65/oz in January 2016 to US$984.45/oz in June, 2016.

Implications of global economic developments on domestic economic activity

The effects of the weak global economy are being transmitted to the local economy mainly through depressed commodity prices and weakening trading partner currencies on the back of a relatively strengthening US$.

The sustained low commodity price environment, particularly for precious minerals and base metals have implications on the domestic economy as the country mainly depends on primary and semi-processed minerals. Weaker prices for precious and base metals imply lower export revenues for Zimbabwe, while depressed oil and food prices have a moderating effect on the country’s fuel and food import bill.

Moreover, the strengthening of the US$, coupled with sustained low commodity prices environment, has weakened growth prospects of the country’s major trading partners, notably South Africa, Botswana and Zambia. This development has resulted in sustained depreciation of these countries’ domestic currencies to the detriment of Zimbabwe’s trade competitiveness.

Resultantly, the manufacturing sector in Zimbabwe has continued to lose competitive ground. The exchange rate based loss in competitiveness has conspired with other supply side rigidities affecting the economy to intensify the influx of relatively cheaper imports into the economy.

Balance of Payments Developments

Merchandise Trade Developments

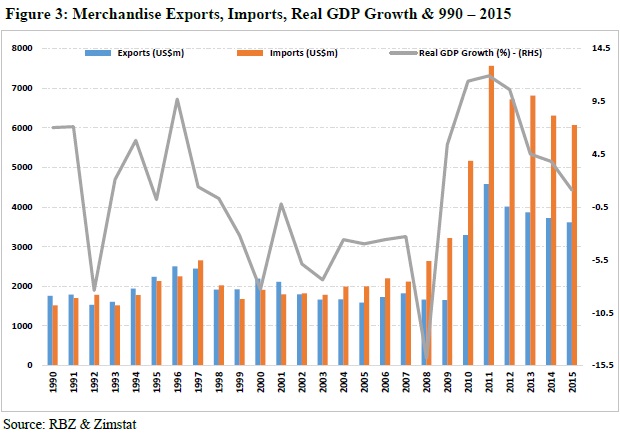

The economy has continued to be affected by sustained mismatches between export receipts and imports as evidenced by the disproportionate import absorption relative to exports especially for the period 2008-2015; a sign of weak economic fundamentals and over liberalisation of current and capital accounts.

Figure 3 shows the Zimbabwe’s merchandise exports, imports and real GDP growth over the period 1990-2015. The graph also shows the sensitiveness of the economy to various shocks and vagaries, including droughts.

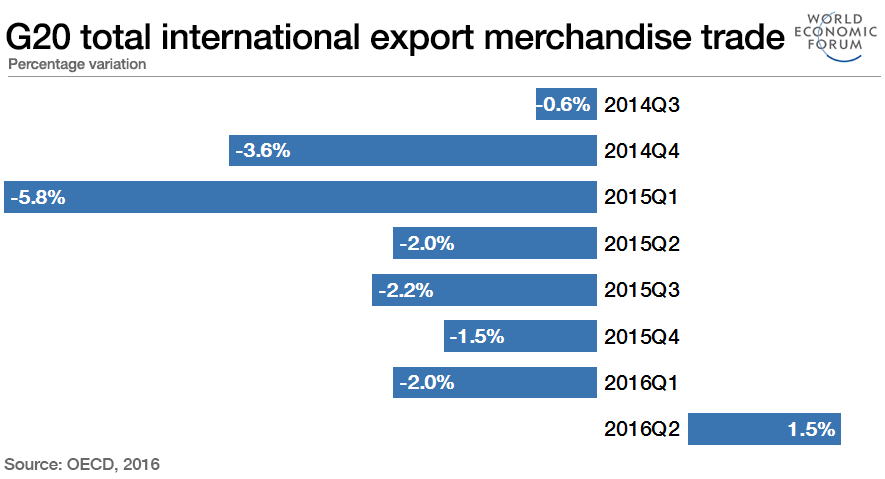

Over the period January to June 2016, merchandise exports declined by 8.7%, from US$1,232.3 million realized in 2015 to US$1,125.0 million in the corresponding period in 2016. Similarly, merchandise imports for the period January to June 2016 amounted to US$2,496.6 million, a 14.4% decline from US$2,917.1 million realized over the comparative period in 2015.

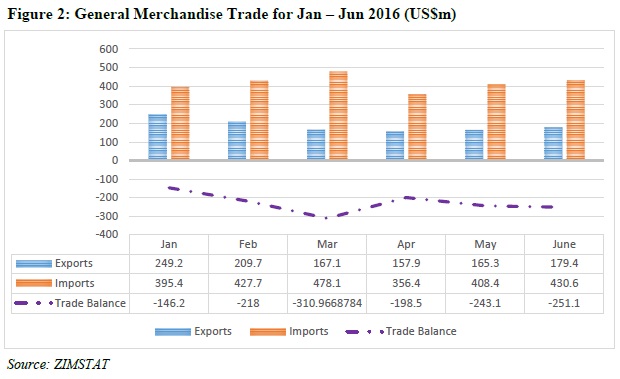

Figure 2 shows monthly merchandise exports and imports development for the period January to June 2016.

The decline in export and import performance is a reflection of the overall slowdown in economic activity, emanating from the drought induced contraction in agriculture, depressed commodity prices, suppressed capacity utilization in the manufacturing sector, as well as continued difficulties in accessing external lines of credit.

A combination of foreign currency management measures, including the prioritization of imports announced by the Reserve Bank in May 2016 and restrictions on selected imports by the Ministry of Industry and Commerce in July 2016, as well as the effects of a stronger US$ on the country’s terms of trade are expected to lead to a 0.9% decline in the import bill in 2016. Food imports (maize and wheat) are, however, expected to surge owing to the El Nino induced drought that ravaged the Southern African region, including Zimbabwe.

Continued reliance on imports of finished goods is unsustainable as it undermines current efforts to resuscitate domestic industrial production, leading to significant trade and current account deficits.

International Remittances

The continued appreciation of the US$ against regional currencies has also affected the dollar denominated value of remittance inflows, particularly from South Africa, which have over the years been a significant source of foreign currency in the country. The weakening of the South African rand against the US$, imply that Zimbabweans who are in South Africa are no longer in a position to send the same amount of money in US$ they used to remit back home. The rand value remittances have gone down in US$ terms.

This is evident from the decline in diaspora remittances of 13% from US$457.9 million for the period January to June 2015 to US$397.3 million in the corresponding period in 2016. This development has, therefore, affected general market liquidity in the economy with adverse effect on aggregate demand and sustained economic recovery.

Foreign Private Capital Flows

Private sector offshore external loans have been an integral source of liquidity in the economy since adoption of the multi-currency exchange system in 2009. These loans, as opposed to equity injection, have mostly been utilized for working capital and capitalization.

In the period from January 2016 – June 2016, the Bank approved and registered a total of 156 facilities with a monetary value of US$976.4 million. As is the norm, the agriculture sector has the highest contribution of 49% which is mostly buoyed by the tobacco sector. A comparison with the same period in 2015 shows that as at 30 June 2015, a total of 185 facilities had been approved with total monetary value of US$1.2 billion.

It is evident that due to the perceived unfavourable investment climate in Zimbabwe, investors have since devised a method to mitigate this perceived risk by using loans to finance their investments in the country as opposed to equity financing. This is also particularly true for some significant investors who have resorted to using the Engineering Procurement and Construction (EPC) model of investment as opposed to cash injection or equity into Zimbabwe like what they do in other countries such as Angola, Ethiopia, Mozambique, Zambia and Nigeria.

Policy Measures to Enhance Confidence and Production

The following policy measures are being put in place to enhance confidence and production in the economy, while simultaneously ensuring sustained financial stability:

-

Ease of securing offshore loans;

-

Incentivising inflows from the diaspora and private unrequited transfers;

-

Nostro stabilisation facilities of US$215 million;

-

US$20 million gold development initiative for small scale gold producers;

-

US$10 million horticulture/floriculture pre- and post-shipment facility;

-

Resuscitation of the credit guarantee scheme;

-

Establishment of an offshore financial centre;

-

Guidance on interest rates charged by microfinance;

i. Ease of Securing Offshore Loans. The current Exchange Control policy states that all external loans and commercial credit applications above US$10 million, for both the private sector and state owned enterprises, need prior approval by the Reserve Bank.

In order to enhance the ease of securing offshore lines of credit, the threshold of external loans that do not need prior Exchange Control approval is, with immediate effect, increased to US$20 million. Authorised dealers will still be required to register all such loans, in the usual manner, with the Reserve Bank.

In the same vein, the banking public should ensure that all unregistered offshore facilities should be regularised with the Reserve Bank through their banks.

ii. Incentivising inflows from the diaspora and private unrequited transfers. In view of the critical role of diaspora remittances in the economy and in order to enhance the remittance of such funds, the Bank shall be extending the export incentive scheme at a level of between 2.5-5% to diaspora remittances including any form of private unrequited transfers on funds remitted to Zimbabwe through normal banking channels with effect from 1st October 2016.

iii. Foreign Exchange/Nostro Stabilization Facilities of US$215 million. In order to deal with the current delays in the processing of outgoing foreign payments by banks the Bank has managed to secure facilities in an amount of US$215 million from international finance institutions to deal with the outgoing foreign payments backlog. In addition, negotiations are at an advanced stage to raise US$330 million from regional sources to enhance production and improve the liquidity situation in the country

iv. US$20 million gold development initiative facility to support small scale and artisanal miners. The Reserve Bank has secured US$20 million for Fidelity Printers and Refiners (FPR) to support small-scale and artisanal mining operations in order to increase gold production in the country.

With underground gold reserves estimated to be around 13 million tonnes, Zimbabwe’s rich gold reserves are clearly under-exploited. Only 586 tons have been officially mined over the past 36 years from 1980 to August 2016 as shown in Table 13. There is therefore great scope to vigorously promote the mining of gold across the country in order to liquefy the economy.

The gold development initiative (GDI) i.e the formalisation process of the small scale gold producers which will be executed according to responsible gold mining standards will need to be supported by fast-tracking the ease of doing business policy measures that include the reduction of cost of doing business as follows:

-

Reduction in custom milling fees from the current US$8 000 on the basis that when the fee was US$2 000 there were 485 millers which were registered but now at US$8 000 the registered millers are now around 51. The challenge is that there are many millers who cannot afford to pay the required fee of US$8 000 but are still operating and selling their gold on the black market and/or smuggling gold out of the country.

-

Reduction of licence fee for explosives. At US$100 about 5 000 small scale gold producers were registered and when the fee was increased to U$2 000 only 300 registered.

-

Reduction of the Environmental Management Agency (EMA) fees. The fee for exploiting the environment at 2% of gross revenue is extremely high. Consideration should be made to scrap this fee in order to enhance gold production.

-

Rural District Council (Land Development Tax) fees. These charges should be reviewed downwards based on ability to pay and must be determined in the context of all the other taxes, fees and charges that are applied to the mining industry.

-

Environmental Impact Assessment (EIA). The fee at between 0.8%-1.2% of total cost (with a maximum cap of US$2 million) remains high and is a huge barrier to investment. Reducing this to a rate of 0.05% of the project cost with a reasonable upper limit of US$50 000 would be in line with international best practice.

-

Reduction of Exploration Licenses, Claims and Related charges. The ground fees currently levied on prospective and mining firms in Zimbabwe are exorbitant.

v. US$10 million horticulture and floriculture pre and post shipment facility Horticulture and floriculture has previously been a fast growing export source with Zimbabwe having been one of the top exporting country in Africa in the 1990s. In order to increase production and exports of this sub-sector the Bank has arranged a facility of US$10 million for the pre and post-shipping requirements for producers of horticulture and floriculture. The facility would be disbursed through normal banking channels.

vi. Resuscitation of the credit guarantee scheme. The Reserve Bank is resuscitating the Credit Guarantee Scheme under the Export Credit Guarantee Company (ECGC) to support SMEs to increase production with effect from 1st October 2016.

The guarantee scheme, which used to be operational, was discontinued in 2002 as the guarantee limit had become too insignificant to support any meaningful business due to economic circumstances prevailing at the time. The credit guarantee scheme will address the challenge of lack of adequate and acceptable collateral, which is among the major challenges faced by marginalized groups including SMEs, women, youth, small holder farmers and rural population in accessing bank credit. The resuscitation of the credit guarantee scheme will go a long way in stimulating productive lending to the marginalized groups which will stimulate economic growth and poverty reduction.

vii. Guidance on interest rates charged by microfinance institutions. Microfinance has been identified as an important pillar of the National Financial Inclusion Strategy in Zimbabwe. However, the high costs of traditional microfinance loans limit the effectiveness of microfinance as a developmental and poverty-reduction tool. The high cost of microfinance loans is partly a reflection of the high cost of funds and the high transaction cost of traditional microfinance operations associated with high volumes of small, low-value loans.

The Reserve Bank has noted with concern that while banks’ lending rates have declined to an average of 15% per annum, some microfinance institutions continue to charge interest rates of over 20% per month. In this respect, microfinance institutions are expected to reduce their lending rates in the spirit of building inclusive financial systems and sustainable economic development. Accordingly, all microfinance institutions are urged to reduce their effective lending rates to a maximum of 10% per month effective, 1 October 2016. Future adjustments would need to be in tandem with the improvement on the tenure of the operating licences of microfinance institutions which are renewed on an annual basis.

vi. Establishment of an Offshore Financial Centre. The Bank is proceeding to putting in place mechanisms to establish an offshore financial centre as a confidence building measure under the auspices of the Special Economic Zones. Details of this initiative shall be unveiled in line with developments on the establishment of the Special Economic Zones in the country.

Policy Advice

1. Dealing with fiscal deficit in a sustainable manner that promotes economic growth requires a combination of the following measures;

-

Leveraging and securitisation of the country’s vast resources (minerals, non-core assets, residential and commercial land) to obtain capital for development and to close the fiscal deficit. The country’s enormous potential for sustained growth and poverty reduction is achievable through leveraging and securitisation of the country’s generous endowment of natural resources.

-

Acceleration of the reform and reorganisation of state owned enterprises (SOEs) including disposal through joint ventures and/or outright sale of some of the non-core SOEs to raise capital for development and to close the fiscal deficit. Additionally, production can be enhanced by granting investors contracts under long lease-back, build-operate-transfer (BOT) or build-own-operate-transfer (BOOT) agreements.

-

Putting in place an attractive investment climate to generate investment-led growth. Investment, like people, likes security. Security of investment is a good or conducive investment climate. Security of tenure is the best form of reward or incentive for business. Putting in place a conducive investment climate, fortunately, costs almost nothing yet the cost of not having it is horrendous.

-

The clarification of the Indigenisation Policy by His Excellency, the President, in April 2016 was a critical milestone towards improving the investment climate but the Act is yet to be aligned to the Policy. Similarly, regularisation of the 99-year land tenure security to make it a bankable document is yet to be done. Regularisation of these two policy documents will cost almost nothing but yet taking action on them would be tremendous as it would signal that domestic and foreign investment is welcome in Zimbabwe. We need to Walk the Talk to see this through in order to create an investor friendly environment.

-

Work being done by the Office of the President and Cabinet on the ease of doing business is quite commendable. What is now needed is to Walk the Talk by fast-tracking the implementation of all the identified areas of improvement especially as they pertain to the regulatory environment of doing business in Zimbabwe. Business license application forms, for example, should be available on-line, identical to all applicants and processed as a routine procedure.

-

Putting in place effective performance management systems across the board to ensure that performance commensurate with rewards and to inculcate positive work ethics. Special government projects that include the Brazil’s More Food Programme and the Directed Agriculture Programme should also be subject to this scrutiny.

2. Dealing with the current account deficit through internal devaluation to restore competitiveness. The use of the multi-currency exchange system puts Zimbabwe in a special circumstance that takes away the flexibility of adjusting the nominal exchange rate to maintain relative competitiveness. This unique situation is similar to the experience of countries within the Euro area, for example, which are unable to reverse a loss of competitiveness and balance of payments imbalance through a nominal devaluation of the currency.

For countries in this predicament, the loss of competitiveness can only be reversed internally, through relative gains in the efficiency in production and or through action to reduce cost of production i.e. internal devaluation – aimed mainly at reducing wages and other related labour costs.

Historical experiences with internal devaluation have been mixed. Others have been successful whilst other “successful” internal devaluation have been accompanied by falling demand and recession. The truth of the matter is that there are always pros and cons with devaluations, whether it is nominal or internal devaluation. Management and choice of internal devaluation is therefore critical.

Whilst there is general acceptance across the board in Zimbabwe about the need for internal devaluation in the country, there is no consensus on its form and format. Statistics at the Reserve Bank shows that the country would need to gradually devalue by up to 45% over a three year period to restore competitiveness.

Internal devaluation in Zimbabwe can be achieved through two possible approaches. The first approach would be for reduction in wages and salaries, accompanied by a similar reduction in the cost of finance and utility charges. Once this is done, the country would need to find a comparator to benchmark with to ensure that costs would not increase again without being checked. The challenge of this approach is that it can lead to further reduction in aggregate demand and to depression and recession. An equilibrium position would therefore need to be determined for this approach to produce desirable results.

The second approach, which also takes account of peculiarities in Zimbabwe, would be to achieve internal devaluation by a combination of improving the competitiveness of the country’s exports whilst simultaneously levelling the playing field between importers and domestic producers. This external rebalancing approach would incentivize foreign exchange earners (including all depositors) who are the generators of foreign currency whilst at the same time levying all payments of imports of goods and services (including withdrawals).

The intention of this approach would be to manage foreign exchange using market based mechanisms. There would be no charges on the use of plastic money and other electronic payment means. This approach would be neutral to net cash depositors. This will, therefore, be a market mechanism to support increased use of plastic money and for attracting foreign exchange deposits.

The downside risk of this second approach is that it would increase prices within the economy. The Bank, however, believes that the levy on imports would have a minimal effect on inflation given that the country is currently in deflation. Allowing some level of inflationary pressures in the economy would help to increase company revenues and profitability with positive multiplier effects on Government revenues, employment and GDP growth.

Most firms in Zimbabwe have already implemented or are in the process of implementing the first approach of internal devaluation of reducing wages and salaries. In view of these developments, it would be prudent to buttress the first approach by the second approach of internal devaluation to deal with the current account gap. The Bank shall be accelerating the second approach of internal devaluation after consultations with business and consumers.

3. Enforcement of local procurement by Government, in line with existing local procurement rules, is essential to conserve scarce foreign exchange and create a multiplier effect to stimulate local suppliers. The increased local business activity will, in time, boost fiscal space through increased taxes.

Conclusion and Outlook

The main message of this Monetary Policy Statement is that the Zimbabwean economy which is under stress as a result of harsh external conditions, structural imbalances and legacy policy inconsistencies/contradictions requires urgent and decisive steps to generate investment-led recovery in order to revamp production across all the sectors of the economy. Walking the Talk is critical because the large current account and fiscal gaps generated by these imbalances have inhibited private investment and restricted economic growth to as low as 1.1% in 2015 and projected at 1.2% in 2016. Enhanced production will increase employment, fiscal space, exports, economic growth and reduce import dependence and poverty. This is the panacea to restore trust and confidence.

Prudent fiscal policy is the main lever to deal with the internal imbalances and create an economic environment conducive to economic transformation. Accordingly, measures taken by the Bank in May 2016 and those presented in this Statement would need to be aligned to the fiscal policy measures presented by the Hon Minister of Finance and Economic Development in the 2016 Mid-Year Fiscal Policy Review Statement.

The measures would need to be supported by concessional external financing. Thus, with fresh foreign financing being an integral part of the envisaged Zimbabwe transformation agenda, completion of the re-engagement process is critical to improve Zimbabwe’s country risk premium.

The policy measures in this Statement and those announced by the Minister of Finance and Economic Development in the Mid-Year Fiscal Policy Review Statement, combined with fast-tracking re-engagement with the rest of the world will pave way for sustained growth and development. This would lead to an increase in economic growth from 1.2% this year to high single digits over the next three years, while inflation would be limited to lower single digits and international reserves would recover significantly.

Overall, the medium term looks favourable for Zimbabwe. Strong economic policies would also have an immediate impact in increasing competitiveness and attracting investment. The financial system which is currently constrained by the environment would be enabled to allocate scarce resources to the most effective use, and support production while facilitating the build-up of foreign exchange reserves.

I thank you.

Related News

Forced displacement: A developing world crisis

Rooted in 10 conflicts, majority of refugees have been hosted by 15 countries, says new World Bank report

One global issue at the forefront of World Bank Group work this year and beyond is the forced displacement of people and its impact on ending extreme poverty. Forced displacement is a crisis centered in developing countries, which host 89 percent of refugees and 99 percent of internally displaced persons, says a new World Bank report. At its root are the same 10 conflicts which have accounted for the majority of the forcibly displaced every year since 1991, consistently hosted by about 15 countries – also overwhelmingly in the developing world.

Not just a humanitarian issue, forced displacement is emerging as an important development challenge, and the development approach to providing support to it is multifold. “Forcibly Displaced – Toward a development approach supporting refugees, the internally displaced, and their hosts” is a groundbreaking study conducted in partnership with the United Nations High Commissioner for Refugees (UNHCR), which examines the role of development in resolving the challenge of forced displacement.

It responds to the growing need to better manage these crises as an important development challenge, part of an overall effort to reduce poverty and achieve the Sustainable Development Goals. The aim of development support is to address the longer term, social and economic dimensions of displacement, in close collaboration with humanitarian and other partners working in complementary ways.

While the current crisis is severe – with a reported 65 million people living in forced displacement – the report finds that over the past 25 years, the majority of both refugees and Internally Displaced Persons under UNHCR’s mandate can be traced to just a few conflicts in the following areas: Afghanistan, Iraq, Syria, Burundi, the Democratic Republic of Congo, Somalia, Sudan, Colombia, the Caucasus and the former Yugoslavia.

Since people typically flee to neighbors of their countries of origin, the responsibility of hosting has not been shared evenly. About 15 countries have consistently been hosting the majority of refugees. At the end of 2015, Turkey, Lebanon, and Jordan, Syria’s neighbors, hosted 27% of all refugees worldwide; Pakistan and Iran, Afghanistan’s neighbors, hosted 16%; and Ethiopia and Kenya, Somalia and South Sudan's neighbors, hosted 7%.

“Forced displacement denies development opportunities to millions, creating a major obstacle to our efforts to end extreme poverty by 2030,” said World Bank Group President Jim Yong Kim. “We’re committed to working with our partners to help the displaced overcome their ordeal and seize economic opportunities, while ensuring that host communities can also benefit and continue to pursue their own development.”

“The search for durable solutions for refugees, internally displaced and stateless persons is central to our mandate,” said United Nations High Commissioner for Refugees (UNHCR) Filippo Grandi. “Enabling dignified and productive lives through development investment is key to this challenge. Working in a cooperative and complementary partnership, I hope humanitarian and development agencies can make a real difference in the lives of the world’s poorest and most marginalized populations.”

Unlike economic migrants who move to places where there are jobs, the forcibly displaced are fleeing conflict and violence, often suffering from a loss of assets, lack of legal rights, absence of opportunities, and a short planning horizon. They need dedicated support to overcome these vulnerabilities and regain confidence in their future – so they can work, send their children to school, and have access to services. Left without support, the displaced may face hardship and marginalization, as do those who are negatively affected in host communities, which can hamper development efforts.

The report identifies three phases of forced displacement where development institutions can intervene to help reduce the costs of the crisis.

1. Prevention and preparedness:

-

Help potential hosts prepare before large numbers of people arrive by planning for contingencies, developing instruments to transfer resources rapidly, and creating ‘surge capacity’ for service delivery. Forced displacement peaks at an average of 4.1 years after its onset, giving countries time to prepare.

-

Strengthen the resilience of those who stay behind, by financing investment in stable parts of unstable countries to maintain livelihoods. People weigh the risks of staying against the risks of leaving, and the majority stay, coping until they have exhausted all other options.

2. Mid-crisis action:

-

Support host communities in addressing long-standing development issues, such as improving the business environment and reducing inequalities, which the presence of forcibly displaced may exacerbate.

-

Strengthen and expand delivery of education, health, urban and environmental services to cope with the increase in population.

-

Encourage policies that enhance freedom of movement and the right to work for the displaced, which are in the interest of host communities as well.

-

Help the displaced move to places where there are opportunities, create jobs in hosting areas, or invest in skills and education that are in demand in the labor market

3. Rebuilding Lives:

-

Support successful return by creating jobs and opportunities in communities receiving returnees, and assist with recovery efforts.

-

Help those in displacement integrate locally, by providing development support for countries that are willing to provide adequate legal status to refugees.

Financing the global response will take significant resources. Development institutions can broaden financing approaches including contingent financing to support preparedness; policy or results-based financing; and guarantees to stimulate stronger private sector investment. Middle-income host countries need access to concessional financing, and low-income host countries require additional resources.

Local Solutions to the Global Forced Displacement Crisis

Forced displacement is not a new phenomenon. Many countries – especially in the developing world – have been managing these situations for years, at times decades. The ongoing Syrian crisis has provided renewed impetus for the global community to re-think how to support local and national governments to help the displaced and hosts alike.

“All the conflicts we are seeing worldwide at the current moment have become the epitome of everything that can go wrong in a conflict situation, and a lightning rod for the international community to realize that the status quo isn’t working,” said Ede Ijjasz-Vasquez, Senior Director for the World Bank’s Social, Urban, Rural and Resilience Global Practice. “Recognizing that every situation is different, we at the World Bank have focused on the need for tailored solutions that work for specific host country situations. Over the years, we have found that good development programs need to be informed by a good understanding of displaced populations and the communities that host them, and the relationship between them. We must help them help each other.”

As the Bank works to expand its support for the displaced as well as their host communities, not only in low-income countries but in middle-income countries as well, many ongoing efforts across the world, including the Great Lakes, the Horn of Africa, and the Sahel regions, in Jordan and Lebanon, as well as in Pakistan and Azerbaijan among others, may provide insight on approaches that work.

Every situation will have its own unique challenges, but ensuring that local host communities are supported and involved in long-term planning decisions, and enhancing job opportunities are among important elements of Bank support. Supporting and enhancing sustainable environmental and ecosystem services, including integrated natural resources management, is also necessary to overcome the environmental degradation and loss of vegetation cover that can result from an inflow of large numbers of people.

Supporting host communities

-

In the Horn of Africa and the Great Lakes, areas hosting refugees and Internally Displaced Persons (IDPs) are often under-developed and underserved, and the Bank is taking a regional approach to improve access to services and economic opportunities. In Zambia, for example, the Bank is supporting both former refugees and host communities through a Community-Driven Development approach, strengthening large scale and community infrastructure to improve education and health services, as well as create economic and market opportunities. In the Democratic Republic of Congo, the Eastern Recovery Project focuses on developing agricultural markets in areas that have experienced high levels of population movement, benefitting hosting communities, displaced families and returnees. Through the Intergovernmental Authority on Development (IGAD), the Horn of Africa Project will help harmonize policies and practices related to forced displacement with the establishment of a regional secretariat for forced displacement and mixed migration.

-

In Azerbaijan, 7% of the population (approximately 623,000 people) is displaced. After two decades, the displaced have not been able to build self-reliance, lacking access to high quality social infrastructure and housing. The problem is aggravated by the fact that most internally displaced are hosted by already poor communities. To respond to this challenge, the government of Azerbaijan has been implementing the Azerbaijan IDP Living Standards and Livelihoods Project since early 2012 to improve living conditions and increase the economic self-reliance of the internally displaced. To ease the burden on host communities and facilitate integration of IDP populations, the project finances small- to medium-sized infrastructure projects through a community driven approach. To date, more than 400 communities throughout the country have benefitted from these infrastructure developments.

-

In Jordan, where most refugees live in towns and cities, long-term predictable financing to twenty local authorities who are each hosting significant numbers of refugees has enabled them to plan and expand water and waste management services, install new street lighting, rehabilitate roads, and provide new sporting and recreational facilities. These are important steps to ensure that host communities continue to be hospitable and reduce any possible tension as a result of increased pressure on services and the environment.

-

In Lebanon where, like Jordan, refugees live amongst host communities, the Bank is providing communities with immediate relief through investing in critical infrastructure at the local level and targeted social initiatives that promote interaction and collaboration between refugees and host communities. The Bank also scaled up its support to the government’s safety net program to host communities impacted by the Syrian crisis to reduce poverty and increase social cohesion. In addition, the Bank helped the public education system absorb a large number of school-age Syrian refugees, while at the same time ensuring Lebanese students also stay in school and overall quality of education is enhanced.

-

Pakistan has had a long history of managing displaced people – hosting over 1.5 million Afghan refugees for decades, the largest protracted refugee population globally (UNHCR). The Pakistan government is also managing a large number of temporarily displaced people within its own borders in Federally Administered Tribal Areas (FATA), supported by the Bank. The World Bank-administered Multi-Donor Trust Fund (MDTF) was formed in August 2010 at the request of the government of Pakistan and development partner countries to respond to the crisis in Khyber Pakhtunkhwa (KP), FATA, and Balochistan to support the reconstruction, rehabilitation, reforms, and other interventions needed to build peace and create the conditions for sustainable development.

Creating jobs and opportunities for both hosts and the displaced

-

In the Great Lakes and Horn of Africa, where host communities depend on traditional livelihoods, such as agriculture, fisheries, and pastoralism, the Bank is providing training to improve production practices, supporting new technologies and equipment, improving storage and processing infrastructure, and increasing access to finance. Local consultations and assessment of local markets with the communities and local governments taking the lead have informed the Bank’s approach. In Zambia, for example, the project supports livelihoods ranging from access to agriculture and vocational training, to development of small-scale sub-projects or irrigation systems, for the most vulnerable former refugees and host community members.

-

In Azerbaijan, the IDP Living Standards and Livelihoods Project supports livelihoods-related activities that provide resources and build skills for IDPs, so that they can compete in the labor market or to start their own businesses and, down the road, to help them obtain better-paid and more secure jobs. The project supports training and grants for business start-up, forming and funding of income-generating groups in IDP communities, and provision of micro-credit for business activities. Businesses are varied in nature but usually build on the agricultural skills that IDPs brought from their home communities, including cattle husbandry, sheep rearing, and crop production, but the project also financed opening of bakeries, retail shops, catering businesses and cafés. Despite the relatively short time these income-generating groups have been operating, most already generate robust incomes. The project provides young people with vocational training and support for business start-up, and also aims to achieve gender balance and reach equal numbers of young women and men.

-

In Jordan, an upcoming program on “Economic Opportunities for Jordanians and Syrian Refugees” will support the Government meet its commitment for providing Syrian refugees with access to the labor market by improving the investment climate and formalizing Syrian employment by facilitating the issuance of work permits. In return, Jordan will benefit from favorable access of Jordanian goods into European markets. The World Bank will also leverage its municipal program to finance labor-intensive works benefiting both Jordanians and Syrian refugees.

-

In Lebanon, an upcoming program on “Roads and Employment” is expected to create about 1.5 million labor days of direct short-term jobs for low-skilled Lebanese and Syrian communities through rehabilitating the roads network of the country. Additional jobs will also be created in the supply chain industries, as well as the engineering and consultancy services in Lebanon.

-

Through the Pakistan MDTF, a total of 1,471 matching grants have been disbursed and an estimated 23,000 jobs have been created through this support in KP and FATA.

Whether it is the Bank’s support to public service provision and local authorities in Jordan and Lebanon, or local government and community-based organizations in rural Africa, ensuring long-term sustainability will require coordinated programming to ensure effectiveness and reduce duplication for improving the quality of services.

“Implementation is challenging enough,” said Markus Kostner, Global Lead for Stability, Peace and Security in the World Bank’s Social, Urban, Rural and Resilience Global Practice, “but much more needs to be done to build, incentivize, and facilitate coalitions of governments, the private sector, civil society, development and humanitarian actors, and affected people to prevent, contain, and respond to current crises, and also look ahead to anticipate and prepare for new ones.”

Related News

EAC states accused of withholding support in war on fakes

A regional forum on Wednesday said inadequate commitment by East African governments has adversely affected the war on trade in counterfeit products.

The forum held in Nairobi said anti-counterfeit agencies in member states have been denied adequate funding for staff, facilities and regulatory frameworks that would promote the war against counterfeit goods.

A panel session, moderated by Kenya Association of Manufacturers (KAM) Chief Executive Phyllis Wakiaga, heard that EA governments hardly provide adequate security to anti-counterfeit inspectors during raids which makes it difficult to implement laws.

Dr John Akoten, Kenya’s Anti-Counterfeit Agency (ACA) Acting Chief Executive, noted that the multiple agencies dealing with counterfeit goods and services have created loopholes in the prosecution of suspects since it is difficult to line up witnesses from various agencies to tender evidence.

The agencies include ACA, Kenya Industrial Property Institute and Copyright Board.

Related News

The People’s President? Citizens’ assessment and expectations of the fifth phase government

Almost one year into the fifth phase government: citizens approve of the removal of ghost workers, free primary education and the dismissal of public servants. But they disapprove of the sugar import ban and price directive.

When citizens were asked to name actions by President Magufuli’s that they approve of, more than six out of ten mentioned the removal of ghost workers (69%), free education (67%) and the dismissal of public servants (61%). When asked to name actions that they disapprove of, three out of ten (32%) mentioned the sugar import ban and price directive. However six out of ten citizens (58%) say that they do not disapprove of any of his actions. Overall approval ratings for President Magufuli are at 96%. This is comparable to approval ratings for previous Tanzanian presidents. Other government leaders also have high levels of approval although none as high as the President. Citizens report that they approve or strongly approve of their village/street chairperson (78%), their local councilor (74%) and their MP (68%).

These findings were released by Twaweza in a research brief titled The People’s President? Citizens’ assessment and expectations of the fifth phase government. The brief is based on data from Sauti za Wananchi, Africa’s first nationally representative high-frequency mobile phone survey. The findings are based on data collected from 1,813 respondents across Mainland Tanzania (Zanzibar is not covered in these results) between 4 and 20 June 2016.

In addition to strong approval ratings, nine out of ten citizens (88%) are confident that President Magufuli can maintain his current momentum until the end of his term.

The majority of citizens also report that they think there have been improvements in almost all public services under the fifth phase government. The Tanzania Revenue Authority leads as 85% of citizens say services there are improved under the new government. Citizens also think services are better in schools (75%), police stations (74%), courts (73%), health facilities (72%) and water service providers (67%). It is important to note that these data show citizens’ perceptions of services and do not necessarily represent any hard improvements. Similarly, almost all citizens (95%) say that civil servants in service delivery, like doctors and teachers, as well as administrative civil servants have become more accountable and efficient.

However citizens themselves admit that they are not very informed about major national issues. Only 4% of citizens feel well informed about national politics and only 9% feel informed about health and education. This indicates that reported improvements in services are based on personal experiences or very localized information. However citizens remain hungry for more information on the sectors that impact their lives. When asked what topic they would like to ask their village chair, councilor or MP about, health, education, water and roads consistently emerged as critical issues. When it comes to President Magufuli, two out of ten citizens (18%) would like to ask him about prices and inflation.

A similar pattern emerges when citizens are asked whether they know and have engaged with local, district or national leadership. Almost all citizens (96%) know their village executive officer and almost half of them (47%) have interacted with him or her. However only 2 out of 10 citizens (21%) know their district executive director and only 4% have interacted with him or her.

Despite this strong approval for the work of the fifth phase government and President John Pombe Magufuli personally, citizens are keen for the principles of democracy and justice to be followed. Eight out of ten citizens think that public officials should only be dismissed when proof of wrongdoing has been established. A similar proportion of citizens (75%) think that officials should be dismissed for failing to perform their duties rather than for disobeying the President’s orders. And despite their enthusiasm for the dismissals of public servants, citizens hold mixed views on the impact of the public dismissals. Although nine out of ten (90%) say these dismissals deter other public servants from wrongdoing, four out of ten (37%) also think that it demoralizes other government officials. And half of citizens (48%) think that the dismissals will only cause public servants to find new ways to hide their wrongdoing.

“Citizens are very positive about the performance of the fifth phase government and President Magufuli in particular. They report that public servants across the board are more accountable and that they have noticed improvements in public services. However citizens are also concerned about due process. For example, they want proof of wrongdoing to be established before officials are named, blamed and shamed. They are also worried about decisions that affect their pockets, like the sugar ban. This shows that they will not just blindly approve of all of the actions of a popular president. They continue to value the fundamental principles of good governance,” said Aidan Eyakuze, Executive Director of Twaweza.

“The most exciting thing about these results” he continued “is the suggestion that citizens’ expectations have shifted. Previously there was a sense of a vicious circle of apathy in which experience of poor performance lowered expectations, which in turn allowed poor performance to continue unchallenged. But recent developments, have shown that public sector performance can improve. Citizens could well come to expect higher standards as a permanent and pleasant new norm.”

Related News

tralac’s Daily News Selection

The selection: Thursday, 15 September 2016

Featured infographic, @ITCnews: Sweet trade - 3 out of 5 top exporters of cocoa beans are located in Africa, ITCdata shows

African factories have room to grow (Business Day): Of the $430bn additional manufacturing output McKinsey believes is possible, up to $209bn could come from a category called "global innovations for local markets" that includes motor vehicles and chemicals, where research and development is a key component, and which already accounted for 27% of African output in 2015. The regional processing of goods such as food and beverages, with the largest share of manufacturing today at 38%, could add as much as $122bn. Resource-intensive manufacturing of cement and petroleum products could contribute another $72bn of additional output, and labour-intensive manufacturing of such products as apparel and footwear the remaining $27bn. Such a step change in manufacturing in Africa is, without doubt, achievable. [The authors: Tenbite Ermias, Acha Leke] [Download the McKinsey Global Institute report Lions on the move II]

Integration critical to industrialization in Africa (AfDB): For the CFTA to fulfill its promise in helping Africa to industrialize, some deliberate policy choices have to be made to create a conducive environment for the continent’s participation in global value chains, and in particular on rules of origin (RoO) and trade in services. With regard to the RoO, there must be harmonization of these rules across the entire continent if Africa is to truly have a single market. While there are large areas of overlaps across products, there are some significant differences across some of the RECs, particularly with the SADC RoO. Also, the RoO must be as flexible and pragmatic as possible. Restrictive RoO tend to constitute trade barriers more than they facilitate trade. With reference to services, the increasing “servicification of manufacturing”, referring to the role of services as inputs in manufacturing, emphasizes the importance of having a competitive services sector as a bedrock for industrialization. Services increasingly make up a larger share of the value of finished manufactured products. Consequently, the need for a competitive services sector is critical to any discussion on value addition on the continent include – both in terms of enabling products to be cost competitive and creating opportunities for value addition. [The analyst: Babajide Sodipo]

Newly posted African trade and development conference documentation:

The concept note for the African Mining Vision CSO Forum, underway in Nairobi.

The full set of documentation ahead of the third meeting of the steering committee of support to the transport sector development programme (21-22 September, Addis Ababa). Two profiled reports, below:

Report on the corridor assessment and ranking for selecting at least One Pilot Smart Corridor (pdf): The consultant collected data and information necessary for assessing and ranking the ten transport corridors according to the agreed multi-factor criteria for selecting at least one pilot smart corridor as per the project terms of reference. Both the ten corridors and the criteria were agreed on at the Validation Committee meeting of February 2016. Here are the results of the assessment and ranking of the ten corridors: North-South 80.0, Northern 73.5, Dar es Salaam 59.5, Maputo 58, Djibouti 53.5, Beira 50, Central 48, Dakar- Bamako-Niamey 47.5, Abidjan-Lagos 41, Douala-N’Djamena-Bangui 30. From a technical point of view and based on the results above, the consultant recommends that the North South Corridor be selected as the pilot smart corridor.

Transport Policy Framework: draft (pdf): The Transport Policy Framework (White Paper) is a consultative document that contains the required policy initiatives. It is intended to inform discussions at a first stage of the process that brings together the AU, REC’s, UNECA, the Fad and member states for preparing a co-ordinated response to the challenge of implementing a transport system that integrates the continent over the next 15 years, whereas taking into account the long term needs of the sector and the long term objectives of PIDA.

The draft agenda for the First African Forum for National Trade Facilitation Committees (17-21 October, Addis Ababa).

TRIPS flexibilities and anti-counterfeit legislation in Kenya and the EAC: implications for generic producers (UNCTAD-UNIDO)

Kenyan regulatory laws include sufficient remedies to enforce quality standards and to prevent the registration of medicines bearing labels that mislead patients as to the characteristics of a drug. Thus, an extension of the Anti-Counterfeit Act to drug quality issues appears inappropriate and not necessary. The Act should be limited to counterfeit trademarks and copyrights in line with Article 51 of the TRIPS Agreement. Any reference to patents should be removed to avoid misunderstanding and potential application of criminal sanctions to generic manufacturers. This would be incoherent with other policy developments in Kenya and the EAC, where remarkable efforts have been made to prepare a policy environment that is conducive to local generic production, related investment and trade within the EAC.

Namibia: Leniency policy for cartels (The Namibian)

Namibia should consider introducing a leniency policy as a way of dealing with cartels in the economy. This policy is said to have worked well all over the world, including in neighbouring South Africa. The chairperson of the Competition Tribunal of South Africa, Norman Manoim said in an interview that consideration should be given as to whether the policy can be adopted without waiting until there has been a change to the legislation. Manoim was one of the guest speakers invited by the Namibian Competition Commission for its ‘Competition & Consumer Week’ held in Windhoek with a theme ‘Cartels and their impact on the economy’.

Why geographical indications for Least Developed Countries? (UNCTAD)

It is legitimate for developing countries, including LDCs, to consider GIs as an alternative to valorize and market their products embedded in rich environmental settings; or by protecting well-known geographically based products already recognized by consumers in the market (Yeung and Kerr, 2011). The cases of Bhutanese red rice, Harenna wild coffee, Wenchi volcanic honey, Pink rice from Madagascar and mullet bottarga from Mauritania show environmentally friendly production processes. Thus, producers in LDCs should be supported by long-term policies and programs aimed to promote collective action, traceability, monitoring and business development. It is necessary to examine the environmental impact after GI implementation due to a possible growth in demand. For example, following questions should be constantly posed and monitored: [The report is based on case studies, which include Ethiopia, Madagascar, Mozambique, Mauritania, Senegal] :

MEPs back trade deal with six African countries (EU)

The European Parliament approved an agreement granting duty-free access to the EU for products from Namibia, Mozambique, Botswana, Swaziland and Lesotho, and improved market access for South Africa on Wednesday. “This agreement will help our African partner states to reduce poverty and can also facilitate their smooth and gradual integration into the world economy. There are also many safeguards in the deal to ensure that local people truly benefit from this cooperation. The language on human rights and sustainable development is one of the strongest that you will find in any EU agreement”, said rapporteur Alexander Graf Lambsdorff (ALDE, DE), before the vote. MEPs approved the deal by 417 votes to 216, with 66 abstentions.

Bitange Ndemo: ‘Are we capable of negotiating global treaties?’ (Business Daily)

A new book, “Bounded rationality and economic diplomacy: the politics of investment treaties in developing countries”, has some insights that reveal the continent’s weakest link with respect to international treaties – the capacity to negotiate effectively while protecting its interest. We can choose to turn the idle capacity within academic institutions into a formidable negotiation teams that could not just help Kenya but the region. This can only be done through a deliberate effort to develop capacity. Of greater importance is the political will to do the right thing to avoid politicization of the economic process. [The writer is an associate professor at University of Nairobi’s School of Business]

Lesotho: water security and climate change assessment (World Bank)

Despite its abundant water resources, Lesotho remains vulnerable to the impacts associated with regular and recurrent floods and droughts, the report revealed. The floods in 2011 were the largest in the country since the 1930s, while the drought in 2015-16 period was the most severe on record. All the climate models indicate that average mean surface temperatures will rise, but precipitation projections vary greatly. The report also recommends improved data needed to continue to develop more sophisticated analyses of the complex issues around the country’s most important natural resource. Data constrains around agriculture, the economic uses and value of water, climate and hydrology have the potential to undermine future opportunities.

South Africa: Gauteng’s Township Stock Exchange project (GCIS)

As part of mainstreaming the township economy and transforming our townships into centres of innovation and manufacturing, we will also next month launch the Township Stock Exchange. The Gauteng township economy is estimated by the World Bank to be worth over R10bn. It is the critical site of the informal sector and more than 1.5 million people. Properly supported, it can contribute to inclusive growth and sustainable economic empowerment of the majority of our population. We believe this is a critical intervention that will help us build a vibrant manufacturing industry in our townships. Already large numbers of township entrepreneurs are makers of things - they are involved in manufacturing, albeit on a minimum scale. As this government, working together with the private sector, we are determined to support these home-grown, genuine entrepreneurs and catapult them to the next level. [The author: Premier David Makhura]

South Africa: The Real Economy Bulletin - Second Quarter 2016 (TIPS)

Behind the trends: Exports were the main driver of the surge in growth in the GDP in the second quarter of 2016, largely thanks to the auto industry. Critical for export growth was the persistence of relatively competitive exchange rates as well as some recovery in the U.S. and Europe in the past year. While welcome, these developments emerged in the context of fairly gloomy prospects for growth in the medium term. Growth in the BRICS: Divergent developments in the BRICS in the past five years illustrate the extraordinary impact of the slowdown in Chinese growth on middle-income economies. They also show how this kind of sharply slower growth can play out in greater political contestation and uncertainty. Growth in the SADC: The rest of Africa now represents around 30% of South Africa’s export market, up slightly from 2010. The bulk of South African exports to the rest of the continent go to Namibia, Botswana, Mozambique, Zambia and Zimbabwe. Because the region is growing rapidly compared to most other regions, despite the end of the commodity boom, it represents a significant opportunity.

Mozambique: Tomaz Salomão praises Bank of Mozambique for supporting limits on dollar use (Club of Mozambique)

Speaking at the Agrarian and Fishing Sectors Business Forum in Manica on Monday Salomão praised Rogério Zandamela’s appointment as governor of the Bank of Mozambique, and said that the first decision taken by his team was right. “A major concern that has been raised in this meeting is the issue of the slippage of the metical. On Friday, the central bank made an announcement which I believe was right. I mean restricting the movement of dollars in our country as a way of strengthening of the metical,” he said. Tomaz Salomão raised other concerns at the forum, such as the under-invoicing of exported products, and challenged ministries to address the situation to boost foreign exchange earnings.

Zimbabwe adopts Rand-based tourism pricing (The Chronicle)

Players in the local tourism industry have resolved to adopt a “rand-based” pricing system to cushion their businesses from the prevailing cash crisis. In the context of weakening regional currencies, the use of the strong US dollar has negatively affected tourist arrivals as the country is viewed as an expensive destination. Recent reports indicate that some tourists wanting to visit Victoria Falls, for instance, now prefer flying into Livingstone in Zambia from where they undertake tourism activities and only cross to Zimbabwe as Zambian clients — prejudicing the country of the precious earnings. Last week Finance and Economic Development Minister Patrick Chinamasa revealed that the approach (rand-based pricing system) has been agreed upon by the Government, players in the hospitality sector and the Reserve Bank of Zimbabwe. [Zimbabwe to scrap horticulture export permits]

Clearing the jam at Djibouti (African Business Magazine)

But such is Ethiopia’s growth – both in terms of economy and population; its current population of around 100m is set to reach 130m by 2025, according to the United Nations – that some say it’s going to need all the ports it can get. “Ethiopia’s rate of development means Djibouti can’t satisfy demand – even if Berbera is used, Ethiopia will also need [ports in] Mogadishu and Kismayo in the long run, and Port Sudan,” Ali says. “The bottleneck is not because of the port but the inland transportation – there aren’t enough trucks for the aid, the fertiliser and the usual commercial cargo,” Aboubaker says, explaining that even with other ports such as Berbera offering more docking options in the future, the problem of not enough trucks matching demand would lead to the same dilemma as now. It’s estimated that 1,500 trucks a day leave Djibouti for Ethiopia and that there will be 8,000 a day by 2020 as Ethiopia tries to address the shortage. [The author: James Jeffrey)

Tanzania: Freight forwarders oppose Kigali plan (The Citizen)

The Tanzania Freight Forwarders Association is up in arms against Rwanda’s request to clear own consignment at the Dar es Salaam Port. TAFFA chairman Steven Ngatunga advised the government to reject the proposal, saying it will deny Tanzanians employment at their own port.

Rural Development Report 2016 (IFAD)

Chapter 3: Structural and rural transformation in Africa. The agricultural sector has grown absolutely and declined relatively, as resources have shifted to other sectors, primarily services. The demand for services comes in part from the agricultural sector. Much demand is generated by resource rents (and in some countries official development assistance) channelled back into the economy through public spending (Gollin et al. 2013). The rapid growth in the service sector shows a high degree of responsiveness to new opportunities, but sustained growth in that sector will require technical change in agriculture to shift the foundations of the middle class from the public sector to competitive manufacturing and services.

Private investment in food systems is expanding quickly (World Bank 2013). What Reardon (2015) calls the “quiet revolution” in food supply chains spans retail, wholesale, first- and second-stage processing, packaging, branding and logistics. Also targeted for investment is the full range of product transformation functions: trucking, processing, storage and wholesaling. These transformations in food systems are very uneven among and within countries, with sharp differences in opportunity based on proximity to cities and access to key assets.

Trade delegation from Africa seeks food security at Big Iron (Grand Forks Herald)

This year’s group was heavily represented by sub-Saharan countries, a difference from the usual guest list that often is heavily represented by visitors from Soviet Union countries, where agriculture is more similar to Upper Great Plains farming. This year’s delegation is the largest to date from Africa. Visitors came from Angola, Benin, Ethiopia, Liberia and Nigeria. Dalva Ringote Allen, chairman of the board of directors of the Republic of Angola’s Ministry of Economy’s Institute of Business Foment, was among those leading a 56-member delegation from her country, focusing on developing agriculture in the wake of declines in oil prices, which the country exports.

Ethiopia is now the largest coffee market in Africa

ECOWAS states urged to adopt uniformity in Single Window Systems (GhanaWeb)

Namibia’s 20th National Rangeland Forum has started

Namibian Biomass Industry Group: case studies on demand for invader bush biomass

Nissan SA poised to expand into Africa

Jeff Nemeth: Getting wheels rolling on the continent

VW expanding its Africa commitment

CTI study roots for expertise sharing to industrialise Tanzania

Rwanda’s MINAGRI rolls out new strategy to boost agriculture

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 350 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

Realizing the potential of Africa’s economies

Africa’s economic fundamentals remain strong, but governments and companies will need to work even harder to keep the region’s economies moving forward.

Many observers are questioning whether Africa’s economic advances are running out of steam. Five years ago, growth was accelerating in almost all of the region’s 30 largest economies, but the recent picture has been more mixed: while growth has sped up in about half of Africa’s economies, it has slowed in the rest.

Between 2010 and 2015, Africa’s overall GDP growth averaged just 3.3 percent, considerably weaker than 4.9 percent a year between 2000 and 2008. But average growth hides a marked divergence, finds a new McKinsey Global Institute report, Lions on the move II: Realizing the potential of Africa’s economies.

A much less robust economic performance by two groups of African economies dragged that average down – oil exporters hit by the decline in oil prices and countries affected by the political turmoil of the Arab Spring (Egypt, Libya, and Tunisia). For the rest of Africa, growth actually accelerated to 4.4 percent in 2010 to 2015 from 4.1 percent in 2000 to 2010. In addition, long-term fundamentals are strong, and there are substantial market and investment opportunities on the table.

Future growth is likely to be underpinned by factors including the most rapid urbanization rate in the world and, by 2034, a larger working-age population than either China or India. Accelerating technological change is helping to unlock new opportunities for consumers and businesses, and Africa still has abundant resources. The International Monetary Fund projects that Africa will be the world’s second-fastest-growing region in the period to 2020.

Despite recent shocks and challenges, spending by Africa’s consumers and businesses already totals $4 trillion annually, and is growing rapidly. Household consumption is expected to grow at 3.8 percent a year to total $2.1 trillion by 2025. African businesses are an even larger spender. From $2.6 trillion in 2015, business spending is expected to increase to $3.5 trillion by 2025.

Africa could nearly double its manufacturing output to $930 billion in 2025 from $500 billion today, provided countries take decisive action to create an improved environment for manufacturers. Three-quarters of that potential could come from Africa-based companies meeting domestic demand; today, Africa imports one-third of the food, beverages, and other similar processed goods it consumes. The other one-quarter could come from more exports. The rewards of accelerated industrialization would include a step change in productivity and the creation of up to 14 million stable jobs over the next decade.

While the potential that Africa offers is undoubted, the question remains: will it be achieved? Businesses and governments will need to work harder to capture the opportunity. Africa is home to 700 companies with annual revenue of more than $500 million, including 400 with annual revenue above $1 billion, and these companies are growing faster and are more profitable than their global peers. But Africa needs more of them. It has a lower number of large companies – and they are smaller on average – than one would expect given the corporate landscapes of other emerging regions. Corporate Africa needs to step up its performance to make the most of these opportunities. The top 100 African companies have forged their success by building a strong position in their home market before diversifying geographically, adopting a long-term perspective, integrating what they would usually outsource, targeting high-potential sectors with low levels of consolidation, and investing in building and retaining talent.

Governments will need to address the continent’s productivity and drive growth by focusing on six priorities emerging from this research: mobilize more domestic resources, aggressively diversify economies, accelerate infrastructure development, deepen regional integration, create tomorrow’s talent, and ensure healthy urbanization.

Delivering on these six priorities will require a transformation in the quality of Africa’s public leadership and institutions, as well as governance. All these imperatives require the vision and determination to drive far-reaching reforms in many areas of public life, and they require capable public administration with the skill and commitment to implement such reforms. What the past five years have shown is that Africa’s diverse economies – its economic lions – now need to improve their fitness in order to make the most of their undoubted long-term growth potential and to continue their march toward prosperity.

Related News

Only targeted policies focused on rural people will eliminate poverty in developing countries, concludes new report

Economic growth is not enough to save those threatened daily with starvation. Governments need to tailor policies and investments to transform rural areas in developing countries if they want to eliminate poverty, according to a new global study released by the International Fund for Agricultural Development (IFAD) on 14 September 2016.