Search News Results

The Continental Task Force on the Continental Free Trade Area considers the drafts of technical documents in preparation for the launch of the negotiations

The 4th Meeting of the Continental Task Force (CTF), commenced on 10 April 2015 in Dakar, Senegal. The meeting was organized by the Department of Trade and Industry of the Africa Union Commission in preparation for the launch of the Continental Free Trade Area (CFTA) negotiations at the Summit of the Heads of State and Government to be held in June 2015. During the next two days, Experts from the African Union Commission, the Regional Economic Communities (RECs), the African Development Bank (AfDB) and the United Nations Economic for Africa (UNECA), will consider all the preparatory issues and review essential technical documents that will enable the Assembly to launch the CFTA negotiations.

The CTF is established to ensure that the CFTA negotiations are conducted efficiently and within the agreed timelines. Its expected results are to finalize drafts of the various technical documents that will be submitted to the meetings of Trade Experts, Senior Trade Officials and the Meeting of African Union Ministers of Trade that will be held from 08 to 15 May, 2015 in Addis Ababa, Ethiopia.

In her opening remarks, the Director for the Department of Trade and Industry, Mme Treasure Thembisile Maphanga recalled the importance and the objectives of the meeting. “We have a responsibility as a Task Force to ensure that negotiations for the CFTA are on track and will take place as scheduled and in line with their road map and mandate through an effective monitoring and evaluation mechanism,” she mentioned.

“We are gathered here today, primarily to update each other on the progress that has been made with regards to the directive we received from the last AU Ministers of Trade meeting which was to look at the overview on the progress of the various technical studies on technical issues which are related to the Continental Free Trade Area such as the Rules of Origins, Trade in Services and many other important issues,” she added. Mrs. Maphanga underscored the fact that the progress on the CFTA cannot be achieved without considering the capacity building at all the levels involved in the negotiations at the national, regional a level.

She encouraged the participants to share with the meeting their regional experience in order to enrich the documents and to further consolidate a strategy on preparing and conducting negotiations at the continental level.

The Chair of the meeting, Dr. Gbenga Greg. Obideyi, Director of Trade at the Economic Community of West African States (ECOWAS) commission, commended the African Union Commission on the progress made and success achieved so far on the Continental Free Trade Area programme. “This is a very important part of the institutional framework for the achievement of the Continental Free Trade Area and we need to come up with a very formidable strategy to ensure that the African Union Commission succeeds in this programme,” he said.

He urged the participants to be advocates for the success of the CFTA. “If the RECs are the building blocks for the CFTA, then we have to ensure that our political leaders take the leadership and ownership. As technocrats in the RECs, our role is to provide our leaders with the necessary support they need to make the CFTA a reality,” he insisted. To conclude his remarks, Dr. Gbenga wished the participants a very fruitful and successful meeting.

Related News

From Billions to Trillions – Transforming development finance

Post-2015 Financing for Development: Multilateral Development Finance

Statement by the Heads of the African Development Bank, the Asian Development Bank, the European Bank for Reconstruction and Development, the European Investment Bank, the Inter-American Development Bank, the World Bank Group and the International Monetary Fund

2015 marks a critical year for development, as the international community works towards agreeing on a set of Sustainable Development Goals (SDGs) to meet the dual challenges of overcoming poverty and protecting the planet. With their welcome emphasis on issues such as the environment, employment, infrastructure, and inequality, the SDGs send a clear message to policy-makers and development practitioners. As leading sources of policy advice and financing for developing countries, international financial institutions (IFIs) fully support this comprehensive approach. However, the resources needed to implement such an ambitious agenda far surpass current development financial flows.

Achieving the SDGs will require moving from billions to trillions in resource flows. Such a paradigm shift calls for a wide-ranging financing framework capable of channeling resources and investments of all kinds – public and private, national and global. There is no substitute for concessional resources, especially for the poorest, most fragile or conflict-torn countries. But marshalling other types of financing at the levels needed will demand greater efforts to unlock, leverage, and catalyze more public and private flows. Financing from private sources, including capital markets, institutional investors and businesses, will become particularly important. Countries also need to improve their institutional and policy environments to attract more private investment and financing, at the same time as they pursue truly sustainable and inclusive growth, so prosperity translates into poverty reduction and social progress.

IFIs are well-positioned to assist member countries in creating such an enabling environment. Guided by our institutional mandates and our member countries’ own development goals, we are committed to helping raise an important part of the required flows, either through direct financing, leveraging our capital or catalyzing other resources. We are determined to continue:

-

Combining our knowledge and experience with our member countries’ perspectives, offering policy and technical advice tailored to local conditions;

-

Building a global safety net by providing counter-cyclical support to economies affected by adverse shocks;

-

Helping countries implement actions for climate change adaptation and mitigation and disaster risk management;

-

Working to strengthen domestic financial markets and deepen financial inclusion;

-

Promoting the highest social, environmental and governance standards;

-

Attracting more concessional funding to provide grants and concessional lending to low-income, fragile and conflict-affected countries.

But we could and should do more. Within our respective mandates, we can and should do more to provide innovative financing and policy solutions customized to the particular needs of each country, subnational entity and region. We need to work harder on sharing the experiences, lessons learned and best practices acquired through our work. This will include working with member countries to translate the SDGs into national targets and introduce and implement the policies and programs needed to achieve them. We also need to further improve coordination and complementarity among IFIs and with other public and private sector actors. And we have to enhance how we measure effectiveness in order to continue to learn from what works and what does not.

2015 brings critical opportunities to change the future, from July’s Third International Conference on Financing for Development in Addis Ababa to the UN Summit on the SDGs and the 21st Conference of the Parties to the UN Framework Convention on Climate Change in Paris in December. This is a challenging agenda, but improving lives and protecting our planet deserve no less. We must work together to generate the needed financial resources and achieve the transformative vision that the SDGs entail. With our member countries in the lead role, we accept this challenge, and stand ready to play our part.

Financing the Post-2015 Development Agenda: Role of the WBG, MDBs and IMF

The multilateral development banks (MDBs) and the IMF have produced a joint discussion note, “From Billions to Trillions: Transforming Development Finance,” which proposes a preliminary vision for the collective role of the institutions looking toward the Addis Financing for Development conference and beyond.

To meet the investment needs of the SDGs, the global community needs a paradigm shift to move the discussion from “billions” in overseas development assistance (ODA) to the “trillions” in investments of all kinds: public and private, national and global, in both capital and capacity.

The joint discussion note will be discussed at the Development Committee meeting of the IMF-World Bank Group Spring Meetings on April 18, 2015.

Related News

African trade policies have to match its industrialization imperative

While the last 15 years have seen relatively high levels of growth driven by a commodity super-cycle and strong internal demand from a growing middleclass, Africa is still dependent on commodities for most of its export earnings. There is now broad consensus that, without diversified economies, Africa will remain prone to exogenous shocks and trapped in the paradox of high growth rates, coexisting with high levels of unemployment and extreme poverty. It is for this reason that the last four issues of the Economic Report for Africa have investigated the fundamental policy questions and challenges facing the transformation process and endeavoured to shed light on, and bring coherence to, policy priorities at national, regional and continental levels.

I continue to call for accelerated industrialization as key to the structural transformation of African economies. The deep focus on industrialization in Africademonstratesour commitment to ensure that policy research and statistics are strategically relevant to African governments’ priorities. The new industrial policies being developed by several member States and regional economic communities have greatly benefited from the research, statistics and debates generated by our focus on this critical subject.

The key factors constraining trade and industrialization in Africa are related to Africa’s narrow production and export base, which is dominated by low-value products such as raw materials and primary commodities. This is compounded by very high trade costs, tariffs and non-tariff barriers to intra-African trade and Africa’s access to international markets. We have no alternative but to increase our share of global exports. While in the 1970s, Africa accounted for 4.99 per cent of world trade and East Asia 2.25 per cent, by 2010, we had regressed to 3.33 per cent, while East Asia had soared to 17.8 per cent. Limited by poor infrastructure and inefficient logistics, lack of adequate skills and quality inputs, insufficient provision of credit and financial services, ours has become a story of lost opportunity. The time has come for us to awake. Africa’s current trade policy plays a major role in our inability to excel.

The 2015 edition of the Economic Report for Africa suggests that trade and industrial policies are now delinked from each other. As a result, African countries exhibit high levels of protectionism with no tangible benefits in terms of productivity improvements. This is exacerbated by rent-seeking behaviourwhich precludes the harnessing of dynamic comparative advantages. Accordingly, tariff structures often do not reflect industrial policy considerations, but are the unsystematic result of successive rounds of reforms. If one looks more closely at imported inputs, it is clear that tariffs are weighing very heavily on the competitiveness of African countries. They stimulate neither the supply responses upstream nor the competitiveness of downstream industries. When properly applied, tariff structures are an instrument for a coordinated strategic approach and for consistency between trade and industrial policy frameworks. I like to call such approach “smart protectionism” – better defined as making the rules work for you. Everybody wants it, but we have not succeeded in making it happen.

Pursuing trade reforms in a strategic manner is a means of promoting and strengthening a country’s competitiveness and creating favourable conditions for enhanced participation in value chains.

Where global value chains are concerned, there is a growing body of research that points to the relevance of the services sector in terms of both contribution to value addition and employment creation. Put differently, a dynamic services sector – think for instance of financial services or ICT – can exert wide-ranging spill-overs that lift productivity and enhance value along the chain. Within Africa, however, trade in services is still restricted by a number of (mainly regulatory) barriers.

Against this background, it is vital that negotiations for the continental free trade area also encompass intra-African trade in services. This would not only contribute to improve the scope for the emergence of regional value chains, but also ensure that the gains stemming from the creation of the Continental Free Trade Area are more fairly distributed among African countries, particularly those economies that are developing significant service hubs.

In addition, harnessing trade strategically means that African countries ensure that the sequencing of trade liberalization is consistent with their transformative agenda and commitment to regional integration. In other words, the sequencing of trade liberalization should prioritize the reduction of tariffs and removal of non-tariff barriers within Africa. The fact is that intra-African exports often face higher levels of protection vis-à-vis Africa’s exports to the rest of the world, and the situation may worsen. Our goal should be to have tariffs reduced between regionaleconomic communities, in order to avoid offering lower tariffs to Europe than those within Africa, which could become one of the consequences of the Economic Partnership Agreements in the absence of an ambitious Continental Free Trade Area Agreement. Other limiting factors, such as non-tariff barriers, remain particularly pervasive and add to the burdens weighing on the competitiveness of African producers, as these barriers remain particularly high between regional economic communities.

Unilateral trade preferences alone can hardly enable the conditions required for the development of regional value chains. Let us realize that Africa can no longer afford to negotiate trade agreements as if industrialization did not matter. We need to keep before us, as our lodestar, the message that trade can indeed support industrialization, but that harnessing this opportunity requires a coherent policy framework.

Related News

African Ministers call for strong Paris agreement, climate finance flows

Private and Public Sectors Join in Quest for Market and Finance Opportunities at 7th Africa Carbon Forum

Ministers from governments across Africa have renewed their call for a strong and universal climate change agreement with increased flows of funds, including through market and finance opportunities, sufficient to fulfill Africa’s development aspirations.

With countries set to approve a new climate change agreement under the UN in Paris in December, African ministers stressed the region’s readiness and requirement for accelerated private and public financing of low-carbon development. Africa, with its vulnerable populations and vast potential, has perhaps the most to lose from climate change and the most to gain from an effective climate change agreement.

“I agree with Ministers that the last 10 years in the implementation of the Clean Development Mechanism is a very valuable asset and that market mechanisms can play a significant role in raising the level of ambition, and supporting climate action,” said Ms. Hakima El Haite, Delegate Minister in charge of Environment of Morocco.

“In these last eight months before Paris, the focus must shift from restating negotiating positions to finding common ground solutions,” said UNFCCC Deputy Executive Secretary Richard Kinley at a day-long ministerial segment at the Africa Carbon Forum 2015 hosted by the Kingdom of Morocco. “All countries have something to gain from the Paris agreement and it is in everyone’s interests to reach a strong conclusion as soon as possible this year. If Heads of State come to Paris, it must be to adopt an agreement that is robust and ready for them.”

Clean Energy to Unlock African Sustainable Development Potential

The African Carbon Forum 2015 focused on programmes to unleash private sector finance, such as through the Clean Development Mechanism, and scale up other forms of climate finance to strengthen the sustainable development of African countries.

According to the International Energy Agency Africa Energy Outlook 2014, 625 million people in Sub-Saharan Africa, about two-thirds of the population, are without secure access to electricity. Some 730 million people in the region still rely on cooking mostly with wood, harming health and destroying vital forest cover.

“The coming months provide African countries with a significant opportunity to align their contributions to the Paris climate agreement with their own long-term sustainable development priorities,” said Mr. Kinley.

Countries are busy detailing their Intended Nationally Determined Contributions (INDCs), which they will submit as their contribution to climate action under the Paris agreement. INDCs for 35 countries have been submitted to date. On April 1, Gabon became the first African country to submit an INDC.

Climate Finance and a Strong CDM Are Key to Success

Two clear messages emerged from participants at the African Carbon Forum. First, linking climate finance to results is essential to stimulate greater funding for both mitigation and adaptation to climate change. Second, developing countries, including Africa, need tools like the Clean Development Mechanism if they are to successfully shift to a low-carbon emitting development path. Paris provides the continent with a unique opportunity to anchor carbon markets in the long-term climate agenda in line with scaling up climate action and sustainable development based on their national priorities.

A consistent theme during the Forum was the need to preserve and improve the CDM beyond 2020 as a tool for providing continued climate finance and technology to developing countries, especially in Africa. This would capitalize on the capacity and infrastructure already built up by countries and stakeholders. It is widely expected that this will be one of the issues to be resolved in Paris.

Participants particularly highlighted the usefulness of the CDM’s established rules in measuring, reporting and verifying results and its possible role to help define and clarify the content of INDCs. The workshop also concluded that African countries could look at how best to link and leverage finance through the Green Climate Fund at the same time as increasing use of the CDM.

The Forum noted that the INDCs provide Africa with an ideal vehicle through which public policy developments can be transparently displayed by countries to shift toward a low-carbon and sustainable development path.

What the Forum Organizers said about Climate Change and Development in Africa

John Kilani, Director, Sustainable Development Mechanisms programme, UNFCCC: “Throughout this African Carbon Forum, I have sensed the extraordinary will of the continent to act, and to use the tools that are functioning and at their disposal now, such as the Clean Development Mechanism. I share the sentiment expressed by many participants here, that it is time to support Africa's dynamism in particular by exploring how the GCF can channel climate finance for the implementation of CDM projects in Africa, and finally unleash the continent's mitigation potential. With the Paris agreement in mind, I trust that African countries will reflect this reality in their INDCs.”

John Christensen, Director, United Nations Environment Programme DTU Partnership: “The African Carbon Forum 2015 has clearly demonstrated the engagement and commitment by countries in the region to contribute to a balanced and fair outcome at the COP in Paris. Countries are preparing their INDCs, and presentations at the Forum indicate that these will have both ambition and at the same time send clear signals of the need to balance adaptation and mitigation aspects within a broader green economy development framework.”

Neeraj Prasad, Manager, Climate Change Group, World Bank Group: “Here’s what participants at the Forum are saying: a clear and fair global climate architecture, which can protect the more vulnerable regions, such as Africa, needs to be a part of the Paris narrative. Participants are demonstrating a very high level of commitment to helping the Paris process hear Africa’s voice in getting climate policies right.”

Kurt Lonsway, Manager, Environment and Climate Change Division, African Development Bank: “As we move towards the goal of a global climate change agreement in Paris in December, the 7th Africa Carbon Forum reinforced the need to have adequate, predictable, sustainable climate finance resources to address Africa’s challenges in transitioning to low carbon development, smart agriculture, and sustainable urban development key topics at this year’s ACF. These areas should be at the core of Africa’s development priorities and how they are integrated into the countries’ INDCs will help determine the successful implementation of INDCs beyond Paris. We all know current climate financial flows are currently insufficient to meet all of Africa’s climate change challenges, but it will be critical for African countries to demonstrate the ability to effectively deploy those resources that are available to help contribute to the global climate change goals.”

Dirk Forrister, President and CEO of International Emissions Trading Association: “As we've heard over the past couple of days, there is a great opportunity for the private sector to invest in a low carbon future for Africa, using market forces to bring innovative technologies so that the continent can develop in a sustainable way. The Paris agreement can help facilitate this by setting the right parameters for business to invest, including agreeing rules and guidelines for carbon markets.”

This year’s Africa Carbon Forum attracted over 600 participants of 53 countries, including 23 ministers or senior officials, policymakers, project developers and investors, and built on the success of last year’s forum in Windhoek, Namibia. Discussions centered on international and national policies and operational issues related to carbon markets, mechanisms and finance.

The Forum is organized under the umbrella of the Nairobi Framework by the UNFCCC, United Nations Environment Programme along with the UNEP-DTU Partnership, World Bank, African Development Bank and the International Emissions Trading Association.

The Nairobi Framework was launched in 2006 by then UN Secretary-General Kofi Annan to assist developing countries, especially in sub-Saharan Africa, to improve their level of participation in the Kyoto Protocol’s Clean Development Mechanism.

Related News

At UN-backed conference, Ban calls for more investment to achieve sustainable energy

United Nations Secretary-General Ban Ki-moon on 15 April 2015 called on business leaders to expand investment in low-carbon growth and opportunities to advance sustainable energy for all and tackle climate change, in a statement to The Future of Energy Summit 2015, organized by Bloomberg New Energy Finance.

“Energy is a story of global progress,” Mr. Ban Ki-moon said. “Smart investors are opening new markets, facilitating new business models, and supporting entrepreneurs in developing countries.”

Noting that global investment in renewable power and fuels in 2014 spiked by more than 15 per cent over 2013, with investments in developing countries growing by more than a third, he pointed out that renewable energies still contribute less than 10 per cent of global electricity, but that incentives can shift this forward.

“I am here to urge you to take action for sustainable energy,” Mr. Ban said.

Currently one out of five people lives without access to electricity, and nearly 40 per cent of the world’s population rely on wood, coal, charcoal or animal waste to cook and heat their homes, leading to over four million deaths each year from the effects of indoor smoke. Addressing this while also reducing greenhouse gas emissions and tackling climate change is a crucial challenge.

Mr. Ban pointed to the new UN-led Global Energy Efficiency Accelerator Platform which aims to double efficiency by 2030, save more than a gigaton of carbon emissions a year and save tens of billions of dollars.

“These significant sums are just part of what is possible. I count on your help to realize the enormous potential out there,” he said, recalling that the private sector, at the Climate Summit last September, announced plans to mobilize over $200 billion in financial assets towards low-carbon and climate-resilient development.

In line with the trend, Mr. Ban said he hoped that the Paris Climate Conference in December would only succeed with a credible climate finance package. To put the global economy on a path to low-carbon growth, he called for carbon pricing, the phase-out of inefficient fossil fuel subsidies and stronger energy efficiency standards.

Mr. Ban also announced that the UN will convene the second annual UN Sustainable Energy for All Forum in May in New York, working with the World Bank and other key partners. The first-ever Global Energy Ministerial will be held on 20 May, gathering leaders from government, business and civil society for cutting-edge discussions on key energy issues, including financing.

Launched by the UN Secretary-General in 2011, the Sustainable Energy for All initiative, a multi-stakeholder partnership, aims to achieve three inter-linked global targets namely to ensure universal access to modern energy services, to double the global rate of improvement in energy efficiency and to double the share of renewable energy in the global energy mix, all by 2030.

At the UN, governments have already identified sustainable energy as one of the new generation of sustainable development goals that are expected to be adopted in September.

Also speaking at today’s event, Kandeh Yumkella, the Special Representative of the Secretary–General and Chief Executive of the Sustainable Energy for All Initiative (SE4All), called on the private sector to seize the opportunity by innovating and investing to help achieve the initiative’s objectives.

“The speed and scale of interventions we need to transform our current energy system and ensure shared prosperity lie in the private sector,” said Mr. Yumkella.

Related News

Insurers must adapt to ‘informal’ African market

Insurance companies are struggling to gain a foothold in Africa, where populations tend to favour community insurance schemes called tontines. These are often informal agreements between trusted friends and family members. EurActiv France reports.

Insurance is overwhelmingly an issue for rich countries. This does not seem likely to change, as 80% of the world’s insurance policies are held by the richest 10% of the population.

“Insurance is quite a new thing in Africa”, said Claude Fischer-Herzog, Director of Confrontations Europe.

“For Africans, insurance remains an elitist product”, said Hermann Kouassi, Executive Director of the Economic and Business Club of the Diaspora (CEADI). “And the fear of fraud is very strong, and often justified,” he added.

Less Elitist alternatives

But insurance, and particularly micro-insurance, has an important role to play in the economic progress of the developing world.

Micro-insurance, which is a form of protection against threats to the lives and livelihoods of low-income people in developing countries, represents a potentially vast market in Africa.

“In western and central Africa, 700,000 people hold micro-insurance policies that cost just €1 per year and guarantee their capital in the case of their death,” Frédéric Baccelli, Director General of Allianz Africa, explained.

“Insurance can secure a country’s economic growth against threats posed by the climate, for example,” said Jérémy Brault from Proparco, the branch of the French Development Agency specialising in private sector finance. “At Proparco, we have made insurance one of our target sectors.”

Tontines dominate the market

The insurance solution favoured by most communities in Africa is the “informal” tontine system. On the margins of traditional banking and insurance activities, tontines allow communities of individuals to save between friends, members of the same family or a community. “Tontines account for an important proportion of the African insurance market,” said Jérémy Brault.

Traditional insurance providers will have to adapt their products in order to seduce distrustful and often disadvantaged customers. “There is no question of applying the very individualised western models in Africa, where the prevailing model is one of intergenerational solidarity,” he explained.

But the rise of the middle classes in Africa could give the insurance sector a boost. “In Ivory Coast, for example, a more individualistic middle class is emerging, within which people will be more forward-looking”, Hermann Kouassi said.

Small share of the market

For now, the African insurance market is a relative lightweight, worth $72 billion in 2013. Frédéric Baccelli said “The insurance market in Africa is smaller than the turnover of Allianz in France”.

South Africa holds 80% of the continent’s insurance policies. The Maghreb countries account for 10% of the market, notably Morocco and Algeria, and the final 10% is spread across the rest of the continent.

Towards a single market?

Work has already begun on an African insurance single market. The Inter-African Conference of Insurance Markets (CIMA) is a group of 14 West African countries, including Cameroon, Central African Republic, Ivory Coast, Mali and Senegal.

Formed in 1992, this organisation unites the markets of its member countries by applying common codes of practice and a single supervisory authority. In 2013, the 163 companies in this embryonic single market had a combined turnover of $1.4 billion.

Frédéric Baccelli said “the annual growth of CIMA is around 7.8%. This is actually fairly low in relation to population and GDP growth in this region”.

The slow development of the insurance single market is partly down to CIMA’s restrictive regulations, according to Frédéric Baccelli: “For example, insurers have to reinvest 50% of their assets in countries of the CIMA zone, which limits their ability to make pan-African investments.”

Related News

The State of Commodity Dependence 2014

The aim of this report is to present an up-to-date overview of the commodity dependence in developing countries in a friendly and easy-to-understand manner.

In fact, commodities represent an essential source of export revenues for developing countries, but they also contribute for the main part of households’ and governments’ income in exporting countries. Moreover, commodities are also an important problematic in terms of social and political stability as well as of development in developing countries.

While the global notion of dependency is often well-known, its exact magnitude in developing countries and in the most vulnerable ones in particular, is not often well estimated. This is the purpose of the State of Commodity Dependence than to fill this information gap.

A developing country is considered as “Commodity Dependent Developing Country” (CDDC) when its commodity export revenues contribute for more than 60 per cent of its total good export earnings.

-

Two thirds of all developing countries are considered as CDDCs in 2012-2013 with 1 out of 2 located in Africa.

-

Commodity dependence increased in half of developing countries since 2009-2010

The State of Commodity Dependence 2014 report is divided in 13 sub-regional chapters; each chapter providing the same set of information:

-

A sub-regional introductory page presenting the performance of individual countries in the area for the main indicators under review in the report,

-

Individual country profiles for all countries in the sub-region. These country-specific tables aim to present – side by side – the latest available data with reference data for 30 different indicators.

Related News

European Parliament’s Trade Committee wastes ground-breaking opportunity on conflict minerals

Joint Civil Society Public Statement

Today [14 April 2015] the European Parliament’s Committee on International Trade (INTA) wasted a ground-breaking opportunity to tackle the deadly trade in conflict minerals. The Committee voted in favour of a weak and ineffective law that, if passed, would undermine global attempts to clean up the trade. It would require only a tiny number of companies importing four key minerals into Europe to source them responsibly and transparently.

INTA has failed to extend the legal requirements to the vast majority of companies involved in the trade, such as manufacturers, traders and companies importing products that contain these minerals. It also fails to regulate foreign actors that supply to European companies. Although we welcome a mandatory approach, this excessively narrow scope will likely fail to make a meaningful and lasting impact on a trade that fuels conflict and human rights abuses in countries like the Democratic Republic of Congo, Colombia, and Zimbabwe.

Civil society is calling on the European Parliament to strengthen the law when it votes in mid-May.

Despite millions of euro worth of tin, tungsten, tantalum and gold entering the EU every year from high-risk and conflict-affected areas, the EU has so far put no legislation in place to ensure these minerals are sourced responsibly.

Today’s vote in INTA follows a weak legislative proposal put forward by the European Commission in March last year. Under this proposal, responsible sourcing by importers of tin, tantalum, tungsten and gold would be entirely optional. The Commission’s proposed voluntary self-certification scheme would be open to approximately 300-400 companies – just 0.05% of companies using and trading these minerals in the EU, and would have virtually no impact on companies’ sourcing behaviour.

Investors, religious leaders, and civil society have all criticised the Commission’s approach, and have called on the EU to make sure that companies placing minerals on the EU market, whether in their raw form or as part of products, are legally required to source responsibly. Last month, the European Parliament’s Development Committee (DEVE) voted overwhelmingly in favour of such a mandatory regime. This year’s Sakharov Prize Laureate, Dr. Denis Mukwege, used his acceptance speech to urge the Parliament to do the same.

INTA has failed to respond to these calls for effective legislation and has instead favoured a largely voluntary scheme that further weakens the Commission’s proposal on a number of points. Under INTA’s scheme only a handful of European smelters and refiners that import tin, tantalum, tungsten and gold into the EU in their raw forms will be legally required to source those minerals responsibly. The regime will be entirely voluntary for other importers of these raw materials, and for companies that import or manufacture products containing them.

The law must be strengthened to make responsible sourcing a legal requirement for all companies that place these minerals on the European market – in any form. This would put the European Union at the forefront of global efforts to create more transparent, responsible and sustainable business practices. It would also better align Europe with existing international standards on responsible sourcing, and complement mandatory requirements in the US and in twelve African countries.

The Committee charged with tackling this issue has missed a critical opportunity. As a result, Parliament now risks taking a major step backwards in attempts to confront the trade in conflict minerals. We are calling on all Parliamentarians to listen to those who have spoken out on this pressing issue, and to vote for a regulation that compels all companies participating in the European market to source their minerals responsibly and transparently – a regulation of which Europe can be proud.

The INTA Committee has been designated to lead the European Parliament’s response to the conflict minerals proposal. It is expected that the Plenary of the European Parliament will vote on the conflict minerals regulation in mid-May. The result will define the Parliament’s mandate for negotiations with the Council of the European Union.

Related News

Now is the time! Use fiscal policy to support sustainable growth

In the global context of a moderate and uneven economic recovery, sound management of public finances can secure elusive growth and jobs.

In its latest Fiscal Monitor, the IMF recognizes influential factors that are assisting the recovery in many countries. Lower oil prices, growth-friendly monetary policy and slower rates of fiscal adjustment are all playing their part.

However fiscal risks remain elevated, the report warns. Advanced economies face the triple threat of low growth, low inflation and high debt. Emerging and developing economies have experienced softening growth and higher costs linked to financial and exchange rate fluctuations. Exporters of oil and commodities have been hit with lower revenues.

Smart taxation and spending and strong fiscal frameworks make a huge difference. “Fiscal policy continues to play an essential role in building confidence and supporting growth,” said Vitor Gaspar, Director of the IMF’s Fiscal Affairs Department.

The IMF Fiscal Monitor is published twice a year to track public finance developments around the world. The latest edition outlines three areas for action:

-

Strengthening fiscal frameworks

-

Reforming energy subsidies

-

Using fiscal policy to stabilize output

Advanced economies still slowed by debt

Public debt continues to present a headwind to growth. Despite significant efforts since 2010, advanced economies’ average ratio of debt to GDP remains above 100 percent. This is expected to decline only slowly in coming years and some countries’ debt projections have been revised upward.

Debt reduction efforts have been aided by stronger-than-expected growth in some countries, such as the United States. But they have been hampered by low levels of inflation levels in many advanced economies, notably in the euro zone.

Growth and inflation have the potential to significantly ease the debt burden. If Austria, Italy, Japan and Portugal could attain 4 percent nominal growth by 2017, their debt ratio could drop by as much as 10 percentage points by 2020.

Emerging markets and low-income countries

Average deficit for emerging, middle income and low-income countries is on the rise and expected to increase in 2015. Oil exporters have lost significant revenues due to the sharp drop in prices. While some have responded with fiscal tightening, others are accommodating the shock with increased deficits.

Volatility in financial markets, capital outflows, and exchange rates have raised the cost of financing for countries such as Brazil, Ecuador and Russia.

The recent Ebola outbreak added pressure to already fragile infrastructure in Guinea, Liberia and Sierra Leone. These countries were the first beneficiaries of the IMF’s newly established Catastrophe, Containment and Relief Trust. The trust will provide debt relief to countries public health crises of this kind and other disasters.

Areas for action

The Fiscal Monitor outlines three main recommendations. First, it advises strengthening fiscal frameworks so as to manage public finance risks and ensure debt is sustainable. Sound management can play a supporting role in delivering macroeconomic stability and growth.

Second, falling oil prices present an opportunity to reform energy subsidies and energy taxes. More than 20 countries have recently taken steps to cut energy subsidies, including Angola, Cote d’Ivoire, Egypt, India, Indonesia and Malaysia. Getting energy prices right would be beneficial to the economy, environment and public health. It would assist governments with their fiscal consolidation efforts or to make further investment in critical areas such as education and health. In advanced economies, taxes on labor could be cut, and paid for with higher energy taxes.

Third, the Fiscal Monitor’s analytical chapter explains why a stable macroeconomic environment is a growth-friendly one. Its analysis of 85 economies over three decades has a clear conclusion. Fiscal policy can stabilize output and gain about 0.3% extra growth annually. A blog by the IMF’s Xavier Debrun sums it up as governments needing to save in good times so they can stabilize output in bad times.

Related News

Surveys show continued economic progress in Liberia; a more uneven picture in Sierra Leone

Effects of Ebola on household welfare likely to reach well beyond the end of health crisis

The return to work continues in Liberia, led by gains for wage workers and the rural self-employed, while the picture remains mixed in Sierra Leone, where urban youth and the non-farm self-employed continued to lag behind. This is according to the latest round of high-frequency mobile-phone surveys conducted in both countries by the World Bank Group and partners, in order to assess how Ebola is impacting people’s livelihoods.

This comes as heads of state from Liberia, Sierra Leone, and Guinea prepare to meet in Washington, DC at the World Bank Group’s Spring Meetings to share their Ebola recovery plans with finance and development ministers and international partners. As Liberia approaches zero cases, and Sierra Leone sees promising declines in infection rates in recent weeks, it will be important to understand where economic recovery efforts should be targeted, and which people within each country need the most attention both now and once the health crisis has fully abated.

“Liberia has made remarkable progress in its fight against Ebola and I have great hope that all affected countries will get to and maintain zero cases,” said Makhtar Diop, World Bank Group Vice President for the Africa Region. “Even as these countries implement their respective economic recovery plans, the long-term economic and social impacts of such a prolonged and devastating outbreak will undoubtedly put many families and communities at risk. We and our partners must continue to respond quickly and effectively to support those who need it most.”

Statistics Sierra Leone has led the national data collection in that country, with support from the World Bank Group and Innovations for Poverty Action. In Liberia, the World Bank Group has worked closely with the Liberia Institute of Statistics and Geo-Information Services (LISGIS) and the Gallup Organization to conduct these mobile-phone surveys. Key findings are below.

In Liberia (read more)

-

The employment situation in Liberia continues to improve. A return in wage work and rural self-employment was offset by a typical seasonal lull in agricultural work, so the overall percentage out of work remains similar to January. Women continue to experience the worst job losses – they are typically self-employed, working as traders or in markets, the type of jobs that have been most impacted.

-

Most agricultural households report that their 2014 harvest was smaller than the previous year. These effects are not restricted to areas that have been directly impacted by Ebola, underlining the need to provide broad agricultural support across the country.

-

Food insecurity remains high, but has seen significant improvement in rural areas. Increases in urban areas have offset the decrease in rural areas, so the national level stayed about the same since January, with just under 75 percent of those surveyed reporting that they were concerned about having enough to eat in the previous week. The use of economic coping strategies such as selling or slaughtering livestock, borrowing money, and delaying investments has also leveled off, a hopeful sign that households are beginning to rebuild lost assets.

-

The use of public services appears to be rebounding. As schools have re-opened, more than three-quarters of respondents with primary school-aged children reported at least some have returned to school. Older children, however, saw a decline in attendance from last year. In both age groups, parents cited a lack of money as the main barrier to sending children back to school, rather than fear of infection. The cost constraints may be more significant for older children though as fees and costs are higher for later years of schooling, and because older children have more income generating potential for the household.

-

In health services, there appears to be a shift from private providers back to public providers, approaching pre-crisis levels.

In Sierra Leone (read more)

-

There are signs of improvement in Sierra Leone, but the economic situation remains uneven. While there have been overall improvements in employment since November – driven by urban areas, youth employment in Freetown has continuously declined and the percentage non-farm enterprises that are no longer operating has increased fourfold.

-

Stability of earnings has depended on the employment sector. Wage workers are earning around the same as they did pre-crisis, while those operating non-farm household enterprises are seeing revenues around 54 percent lower than in July-August 2014. Women in particular are affected, mostly due to the fact that they are generally working in non-farm household enterprises, the sector most heavily impacted by Ebola.

-

Food insecurity, which was high in Sierra Leone even before the crisis, continues to be a concern. Nearly 70 percent of households taking at least one action to cope with food shortages in the week leading up to the survey. Coverage of social assistance thus far reflects the disease-specific targeting of the emergency response, suggesting efforts to reach the poorest will be key as the country moves toward recovery.

-

Delivery of social services has generally improved. The utilization of maternal care services has increased significantly since November: the percentage of women who gave birth in a clinic up from 28 percent to 64 percent and the percentage who received at least one prenatal visit up from 56 percent to 71 percent. National educational radio programs, working to bridge gaps created by long-term school closings, have reached nearly 72 percent of households with school-aged children, who reported that at least some children listened to these programs.

“As the countries hardest hit by Ebola look toward economic recovery, data and evidence will be crucial to identifying and reaching those most marginalized by this crisis,” said Ana Revenga, Senior Director of the Poverty Global Practice at the World Bank Group.“We will continue to work with our partners to collect and share this information in a timely manner, in order to support their efforts today and down the road.”

A third round of mobile phone data collection in Sierra Leone is planned for April 2015, to continue to track and highlight the most pressing areas of attention for policy makers as they move toward the economic recovery phase.

In Liberia, this fifth round of data collection will be the last done by mobile phone. The World Bank Group is working with LISGIS to return to in-person surveys now that the infection risk is lower. These will allow for an even fuller understanding of what Ebola’s effects have been in that country.

Data collection at the household level complements broader efforts to understand the bigger picture, macro-economic impact of Ebola on the affected countries, as seen in a report to be released later this week.

Related News

Modest trade recovery to continue in 2015 and 2016 following three years of weak expansion

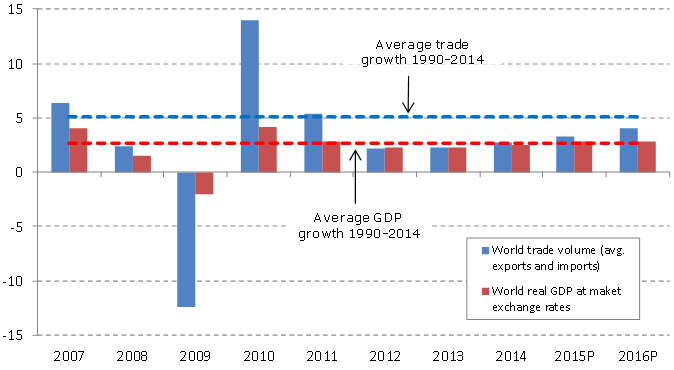

Growth in the volume of world merchandise trade will pick up only slightly over the next two years, rising from 2.8% in 2014 to 3.3% in 2015 and eventually to 4.0% in 2016, WTO economists announced on 14 April 2015.

Trade expansion will therefore remain well below the annual average of 5.1% posted since 1990.

The modest gains in 2014, marked the third consecutive year in which trade grew less than 3%. Trade growth averaged just 2.4% between 2012 and 2014, the slowest rate on record for a three year period when trade was expanding (i.e. excluding years like 1975 and 2009 when world trade actually declined).

Director-General Roberto Azevêdo said:

“Trade growth has been disappointing in recent years, due largely to prolonged sluggish growth in GDP following the financial crisis. Looking forward we expect trade to continue its slow recovery but with economic growth still fragile and continued geopolitical tensions, this trend could easily be undermined.

“But we are not powerless in the face of this gloomy picture. Trade can be a powerful policy tool to leverage economic growth and development. By withdrawing protectionist measures, improving market access, avoiding policies which distort competition and striving to agree reforms to global trade rules, governments can boost trade and seize the opportunities that it offers for everyone.”

In the short-term at least, trade expansion will no longer far outstrip overall economic growth as had been the general pattern for decades. The 2.8% rise in world trade in 2014 barely exceeded the increase in world GDP for the year, and forecasts for trade growth in 2015 and 2016 only surpass expected output growth by a small margin (Chart 1).

Chart 1: Growth in volume of world merchandise trade and real GDP, 2007-16P (Annual % change)

Figures for 2015 and 2016 are projections. Trade refers to the average of exports and imports.

Source: WTO Secretariat for trade and consensus estimates for real GDP at market exchange rates

Several factors contributed to the sluggishness of trade and output in 2014 and at the start of 2015, including slowing GDP growth in emerging economies, an uneven recovery in developed countries, and rising geopolitical tensions, among others. Strong exchange rate fluctuations, including a 14% appreciation of the US dollar against other currencies between July and March, have further complicated the trade situation and outlook.

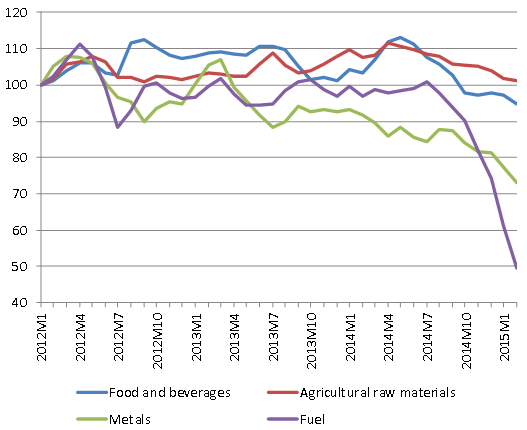

Collapsing world oil prices in 2014 (down 47% between 15 July and 31 December) and weakness in other commodity classes hit export receipts and reduced import demand in exporting countries, but also boosted real incomes and imports in importing countries. Prices have continued to fall since then, suggesting excess supply, insufficient demand, or both. Whether this turns out to be a positive or a negative development on balance for world trade in 2015 remains to be seen.

The preliminary estimate of 2.8% for world trade growth in 2014 refers to the average of merchandise exports and imports in volume terms, i.e. adjusted to account for differences in inflation and exchange rates across countries. This figure is close to our most recent forecast of 3.1% from last September but below the 4.7% rise predicted at this time last year. A number of factors contributed to our initial overestimate, most of which could not have been anticipated.

The sharp declines in commodity prices since last July were not foreseen and did not figure in last year’s estimates. The oil price drop was driven by surging production in North America, but falling demand in emerging markets also played a part, as it did with other commodities.

One year ago, economic forecasters were predicting above trend GDP growth in the United States and near trend growth in the euro area in 2014. Both predictions promised to support stronger trade growth but neither materialized, as a mix of strong and weak quarterly results in the United States only produced average growth for the year, while activity in the euro area was consistently mediocre.

Geopolitical tensions and natural phenomena also weighed on trade growth last year. The crisis in the Ukraine persisted throughout the year, straining trade relations between Russia on the one hand and the United States and European Union on the other. Conflict in the Middle East also stoked regional instability, as did an outbreak of Ebola haemorrhagic fever in West Africa. Finally, declines in first quarter trade and output in the United States were attributed to unusually harsh winter weather.

The WTO’s trade forecasts depend on GDP projections from other organizations, but these have been consistently overstated since the financial crisis of 2008-09, biasing our trade forecasts upward.

Recent surveys of business sentiment and activity point to a firming of the economic recovery in the European Union, moderating growth in the United States, and subdued activity in some emerging economies, particularly Brazil and Russia. These indicators are consistent with the current trade forecast, but WTO economists cautioned that the presence of several risk factors added to the uncertainty of their estimates.

The most prominent risk is the divergence of monetary policies in the United States and the euro zone, as the Federal Reserve contemplates raising interest rates later this year while the European Central Bank has just started its own programme of quantitative easing. Others include a re-flaring of the debt crisis in the euro area, and a stronger-than-expected slowdown in emerging markets (particularly in resource exporting regions such as Africa, the Middle East, the Commonwealth of Independent States (CIS) and South America).

Finally, the rough two-to-one relationship that prevailed for many years between world trade growth and world GDP growth appears to have broken down, as illustrated by the fact that trade and output have grown at around the same rate for the last three years. This changing relationship has made trade forecasting particularly difficult in recent years and will continue to cloud the outlook for 2015 and 2016.

TRADE DEVELOPMENTS IN 2014

Annual data on merchandise and commercial services trade in current US dollar terms are presented in Appendix Tables 1 to 6. The dollar value of world merchandise trade stagnated in 2014, as exports rose just 0.7% to $18.95 trillion. This growth rate is lower than the one for merchandise trade in volume terms mentioned above (2.8% for the average of exports and imports), reflecting falling export and import prices from one year to the next, particularly for primary commodities.

By comparison, growth in the dollar value of world commercial services exports was stronger, increasing by 4% in 2014 to $4.85 trillion. It should be noted that the commercial services values are compiled using a new services classification in the balance of payments. Thus, figures are not directly comparable to those from earlier years. Comprehensive annual, quarterly and monthly data on merchandise and commercial services trade can be downloaded from the WTO’s website.

One striking feature of the merchandise trade values in 2014 is the weakness of trade flows in natural resource exporting regions. The dollar value of exports from South America, the CIS, Africa and the Middle East fell 6%, 5.9%, 7.6% and 3.9%, respectively, as lower commodity prices cut in to export revenues. A sharp drop in imports of South America (‑4.2%) reflected recessionary conditions in leading regional economies, while an even steeper decline in CIS imports (‑11.2%) stemmed from a combination of factors, including falling oil prices and regional conflict.

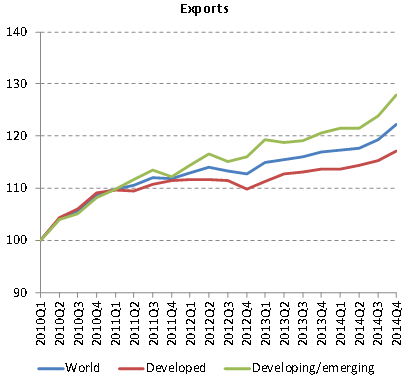

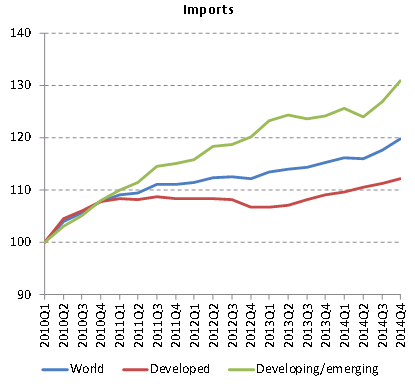

For broad country aggregates and regions that do not export natural resources predominantly, trade statistics in volume terms may provide a clearer picture of trade developments. The WTO and UNCTAD jointly produce a variety of short-term trade statistics, including seasonally-adjusted quarterly merchandise trade volume indices. These are shown in Chart 2 by level of development.

Chart 2: Volume of merchandise exports and imports by level of development, 2010Q1-2014Q4 (Seasonally adjusted volume indices, 2010Q1=100)

Source: WTO and UNCTAD Secretariats.

World exports in volume terms only increased by 1.9% in the first half of 2014 compared to the same period in 2013, but year-on-year growth in the second half rose to 3.7%. Exports of developed and developing/emerging economies were both slow in the first half (1.8% and 2.1%, respectively) but shipments from developing/emerging countries grew faster in the second half (2.5% for developed, 5.1% for developing).

OUTLOOK FOR TRADE IN 2015 and 2016

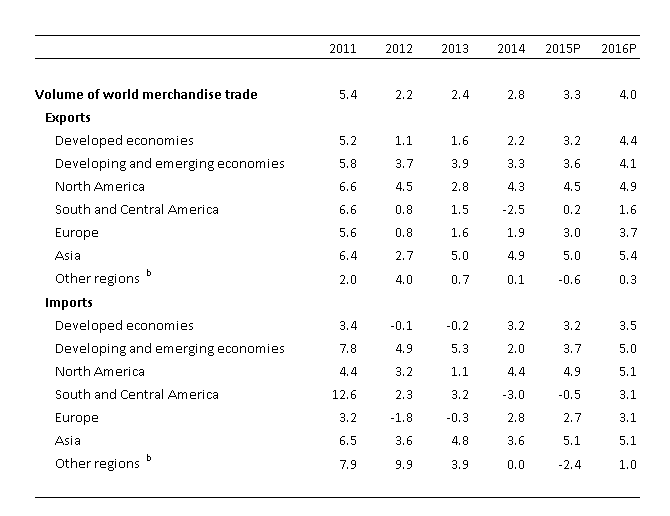

The WTO’s forecasts of 3.3% growth in the volume of world merchandise trade for 2015 and 4.0% growth for 2016 are premised on consensus estimates of world real GDP at market exchange rates from other agencies (Table 1). These figures imply multiples of trade growth over GDP growth slightly greater than 1 in 2015 and 2016, higher than the rough 1-to-1 ratios for 2012-14 but still well below the 2-to-1 ratios that were common not so long ago.

Exports of developing/emerging economies are forecast to grow 3.6% in 2015, while their imports are expected to increase by 3.7%. Meanwhile, a 3.2% rise is anticipated for developed economies on both the export and import sides.

Asia should have the strongest export performance of any region this year (5.0%), followed closely by North America (4.5%). Europe’s exports will also improve, with shipments rising 3.0% in 2015, up from 1.9% last year. The weakest export growth in 2015 will be in South America (0.2%) and Other regions (-0.6%, comprising Africa, Middle East and CIS), although small changes in export volumes from year to year are normal for resource-rich regions.

North America and Asia should both see imports increase by around 5% in 2015, while Europe records import growth of less than 3%. In contrast to this improvement, South America and Other regions are expected to record declines of 0.5% and 2.4%, respectively.

Table 1: Merchandise trade volume growth, 2011-2016 a (Annual % change)

a Figures for 2015 and 2016 are projections.

b Other regions comprise the Africa, Commonwealth of Independent States and Middle East.

Source: WTO Secretariat.

Risks to the trade forecasts are mostly on the downside. One such risk is the unbalanced nature of the global economic recovery. After an unexpected drop in its output in the 1st quarter of 2014, the United States saw its GDP accelerate and its unemployment rate fall in the remainder of the year, which in turn lifted US imports. Continued strength in the US economy would buttress global demand and reinforce the trade recovery. Conversely, any shortfall in the US performance would leave few alternative sources of rising import demand. US GDP growth could disappoint if tighter monetary conditions and lower oil prices choke off investment, including in the energy sector.

Economic conditions in the European Union are improving, but EU-wide unemployment remains high (9.8% in February) and contentious bailout negotiations between Greece and the rest of the euro area threaten to revive financial instability.

The outlook for China is also less certain than before, as activity in the world’s largest economy (measured at purchasing power parity) has eased. The 7.4% increase in Chinese GDP in 2014 was the smallest such rise in 24 years, and Chinese officials have downgraded their output targets going forward. China’s growth is still likely to exceed that of other major economies this year and next, but it may do so by a smaller margin than in the past. This suggests steady rather than accelerating import demand in China.

Chart 7: Prices of primary commodities, January 2012 - February 2015 (Indices, January 2012 = 100)

Source: IMF Primary Commodity Prices.

Lower prices for oil and other primary commodities provide some upside potential to the forecast if their positive impact on net importers of these products outweighs their negative impact on net exporters. The extent of the recent slide in commodity prices is illustrated by Chart 7. World trade could also grow faster than expected if a stronger economic recovery takes hold in the euro zone as a result of the European Central Bank’s recently announced programme of monetary easing. Any recovery in demand in the European Union would have a disproportionate impact on world trade statistics due to the fact that trade between EU members is counted in global totals.

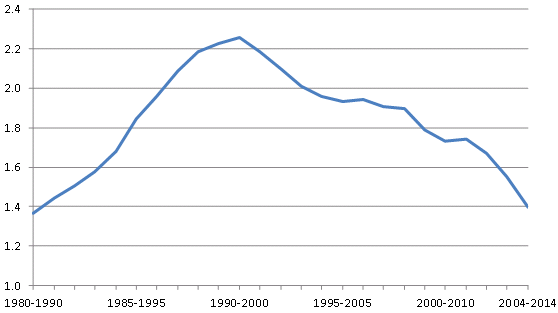

Much attention has been paid to the fact that the rough two-to-one relationship that prevailed for many years between world trade growth and world GDP growth appears to have broken down, as illustrated by the fact that trade and output have grown at around the same rate for the last three years (Chart 1). A number of explanations have been offered for the slower rate of increase recently, including adverse macroeconomic conditions, the maturation of global supply chains, and the accumulation of post-crisis protectionist measures, among others.

No definitive explanation has emerged, but some stylized facts can at least be discerned. First, the ratio of world trade growth to world GDP growth (referred to as the “income elasticity of world trade” by economists) peaked sometime in the 1990s, long before the financial crisis, but has fallen since then (Chart 8). Second, it is normal for world trade to grow slowly for a time after a global economic shock before faster growth resumes (e.g. the oil crises of the 1970s and early 1980s). Finally, a smaller global trade elasticity does not imply a lower world trade/GDP ratio, which remains at or near record levels.

These facts suggest a combination of cyclical and structural factors at work behind the trade slowdown. So while the WTO foresees continued slow trade growth in 2015 and 2016, it does not rule out a return to faster trade growth at a later date.

Chart 8: Elasticity of world merchandise trade volume with respect to world GDP at market exchange rates, 1980-2014

Note: Elasticities calculated by regressing log of world merchandise trade volume on log of world GDP at market exchange rates over 10 years.

Sources: WTO International Trade Statistics for trade, IMF World Economic Outlook database for GDP at market exchange rates.

Download the full Press Release below.

Related News

New Malawi Economic Monitor calls for restoration of macroeconomic stability

A new report by the World Bank analyzing Malawi’s economic development shows that the country’s economy continues to grow at a moderate pace and that GDP will not be overly affected by the floods that hit the country early this year. The economy is however characterized by macroeconomic instability and barriers to trade which Government needs to act on to improve growth prospects.

The maiden Malawi Economic Monitor report released in Lilongwe on 14 April 2015, is intended to provide an analysis of economic and structural development issues in Malawi, and will be published bi-annually. The first issue is titled “Managing Fiscal Pressures.” The report provides a macroeconomic outlook for Malawi, and in this first edition has a special topic on building trade competitiveness, addressing constraints that limit the country from benefiting from opportunities created by international trade.

The report indicates that Malawi’s GDP growth rate remained stable in 2014 estimated at 5.7 per cent, driven by expansion in agricultural, information and communications, and the wholesale and trade sectors. GDP growth rate is however projected to slow down to 5.1 per cent in 2015 mainly due to adverse weather which is likely to affect agricultural production, and subsequent manufacturing.

Downside risks to growth include a continued high rate of inflation averaging 23.8 per cent in 2014, high interest rates above 40 per cent, and a weak fiscal environment. Malawi’s budget position is under pressure with the country expected to run a deficit of 5.9 per cent of GDP during the 2014/15 fiscal year, compounded by the loss of budget support from donors. Further, public debt has risen sharply in recent years, with annual debt service costs now at a value equivalent to 5.3 per cent of GDP.

“With these significant challenges, Malawi needs to prioritize the restoration of macroeconomic stability through such actions as reducing the size of the budget deficit, scaling back domestic borrowing, and reforming key subsidy programs particularly the fertilizer input subsidy,” says Richard Record, Senior Country Economist for Malawi and lead author of the report. He adds that Government should continue implementing public financial management reforms to rebuild confidence in the integrity of Government accounts.

On the special focus on trade, the report observes that terms of trade have moved against Malawi over recent decades, with the unit value of exports falling compared to the unit value of imported goods. “This means the country has to trade an increasingly large volume of exports to pay for the same volume of imports. But Malawi has a real opportunity if she reduces her trade costs,” says Mombert Hoppe, Trade Economist for Malawi and contributing author.

To achieve this, the report recommends reforms for the country to build its competitiveness which include removing domestic policies that depress the performance of the export sector such as export bans; reviewing existing import and export licenses; and reducing barriers to competition in the transport sector to reduce transport prices.

Overall, the aim of the Economic Monitor report is to foster better informed policy analysis and debate regarding key challenges that Malawi needs to address in order to achieve high rates of stable, inclusive and sustainable economic growth.

Report recommendations to restore macroeconomic stability and build trade competitiveness include:

Steps to restore macroeconomic stability

-

Fiscal consolidation to reduce the size of the budget deficit

-

The application of a tight monetary policy and scaled back domestic borrowing to gradually reduce inflationary pressures

-

The reform of key subsidy programs, particularly FISP, in order to reduce fiscal pressures and to improve policy effectiveness

-

Implementation of public financial management reforms in prioritized areas to rebuild confidence in the integrity of Government accounts

Reforms to build trade competitiveness

-

Reviewing domestic policies that depress the performance of the export sector such as removing remaining export bans and ensuring that new ones are not introduced; reviewing existing import and export licenses; and streamlining the manner in which remaining licenses are applied

-

Reviewing and publishing trade regulations and their application and making them easily accessible in order to reduce costs, delays, and uncertainty

-

Consistent implementation of policy decisions to ensure a more predictable trading environment for existing firms and potential investors

-

Improving border crossing times and reducing delays and paperwork by implementing Government’s decision to reduce the number of agencies present at the border

-

Reducing barriers to competition in the transport sector in order to encourage entry and to reduce transport prices

Related News

The EPA, TISA and the LDC services waiver: How the regions are influencing Geneva

Mauritius’ intent to join TISA and the EU’s position on the LDC Services Waiver suggest a rare instance where regional negotiations – in this case, the Economic Partnership Agreements – are directly influencing discussions at the multilateral level. But bringing EPA ambitions into Geneva means bringing its lessons as well.

On the 5th February 2015, at a High-Level Meeting of the WTO Services Council, WTO Members outlined how they intended to support the growth of services trade for Least Developed Countries (LDCs), through operationalising the LDC Services Waiver agreed in 2011 at the 8th Ministerial Conference in Geneva. One month later, Mauritius announced its intention to join the plurilateral Trade in Services Agreement (TISA) negotiations.

These two events, while seemingly only tangentially related, mark a watershed moment for both Africa and the multilateral trading system. They reverse the normal dynamic whereby the WTO sets the framework for discussions at the regional and bilateral level: in this instance, regional negotiations appear to have directly shaped negotiating ambitions in Geneva.

The EPA as a testing ground

The key link is the ACP-EU Economic Partnership Agreement (EPA) negotiations. At the High-Level Meeting on the Service Waiver, the EU has essentially offered to the LDCs the same treatment as that granted to CARIFORUM under the CARIFORUM-EU EPA. In the TISA context, Mauritius is planning to table a services offer that had been originally formulated in its own EPA negotiations with the European Union (EU).

This suggests, for the first time, that the EPA negotiations – despite having been strongly criticised over their much-delayed timespan – are having a significant (albeit perhaps unintentional) impact on global trade discussions. Both the EU’s position at the High-Level Meeting and the Mauritius TISA announcement suggest that the EPA is turning into a testing ground for discussions in Geneva.

One hand, some developing countries are using the EPA to test how far they were willing extend market access to their developed partners. On the other, developed countries can explore their own willingness to extend special and differential treatment to their developing country partners.

These developments are occurring in a highly sensitive area (i.e. services) where many African ACP countries are negotiating for the first time with a developed economy, and in a context where donors and beneficiaries are negotiating a new type of “trade and development” agreement: one where trade policy is not exclusively shaped by commercial and mercantilist considerations, but rather as an explicit complement to – and arguably a subsumed extension of – development policy.

Mauritius and TISA – The role of the EPA

For Mauritius, its stated intention to join the TISA negotiations are a clear extension of a wider policy vision. A series of targeted reforms have guided Mauritius from a mono-crop/preference-dependent economy, to light manufacturing based on export processing zones, to a tourism hotspot, to plans for a global services hub. Mauritius’ plans to join TISA appear to be a natural means of attracting investment from the other TISA parties, in part as an entry-point into the wider pan-African market.

The very fact that Mauritius even has an EPA services offer to table is interesting in itself. Mauritius is negotiating as part of the Eastern and Southern African (ESA) regional configuration. The EPA negotiations between the EU and ESA have however been largely dormant for several years. While some progress has been achieved on a draft services text, little substantive exchanges had occurred with respect to offers and requests. In the meantime, Mauritius has been implementing its goods-only interim EPA.

Despite the impasse, Mauritius had already seized the opportunity of the EPA to prepare “back pocket” services offer. In the relative comfort zone of a North-South agreement where the EU was not likely to be the Mauritius’ primary target (given its continental ambitions), Mauritian negotiators could expand on their relatively thin GATS offer and build on their reform agenda for the domestic services market, all with a view to eventually bringing the offer (as a whole, or in pieces) to a wider setting. In essence, Mauritius used a regional opportunity to craft a multilateral offer.

The EU and the LDC Services Waiver: The promise (and perils) of the CARIFORUM EPA experience

For the European Union, there were clear rationales for extending the many negotiating “firsts” contained in the CARIFORUM-EU EPA services and investment chapter to the LDC Group in Geneva. There are also clear cautionary tales for the LDC Group in pursuing the opportunities therein.

In recognition of the fact that CARIFORUM’s small economies were unlikely to have significant Foreign Direct Investment (FDI) capacity into the EU, the EPA dispensed with the traditional FTA linkage between Modes 3 (commercial presence) and Mode 4 (temporary movement). The EPA instead expanded and deepened traditional categories of temporary movement outside of Mode 3 contexts, particularly those for contractual service suppliers and independent professionals. The CARIFORUM EPA focused on categories of service suppliers such as fashion models, entertainers and chefs de cuisine, where CARIFORUM’s small and developing service economies were likely to have a greater comparative advantage.

The architecture of the EPA services chapter drew from the particular hurdles facing CARIFORUM services suppliers: their small size, the complexity of (and high cost of meeting) necessary EU requirements and regulations, and the development potential of the services sector in the Caribbean. The CARIFORUM EPA implicitly recognised that overcoming these hurdles needed commercially meaningful preferences to spur ACP exports, rather than simple market opening or binding of the status quo. The approach was, in a sense, in the same spirit as the Lomé and Cotonou preferences in traditional commodities such as bananas, sugar, rice and rum.

As an extension of this “market access is not enough” approach, the EPA also explicitly linked the temporary movement provisions with critical enabling measures (e.g. encouraging regulatory bodies to negotiate the terms of mutual recognition agreements), as well a package of development cooperation funds aimed at the services sector.

Therein lies one probable rationale for the EU’s importing of the CARIFORUM EPA architecture to the LDC Services Waiver. Apart from the obvious fact that many LDCs are also ACP countries, many LDC service suppliers also share some of the structural barriers that the EPA sought to overcome. Many face a lack of knowledge of their own current and future export potential in services; a lack of understanding of market barriers in the EU (and where they were known, the existence of prohibitive barriers, such as the imposition of onerous taxes and fees); and severe supply-side constraints on small services firms.

Other, perhaps less altruistic, motivations may have prompted the EU to import its regional CARIFORUM commitments into the multilateral setting. Under political pressure to “operationalise” the Service Waiver as the LDC Group tabled its collective request, the European Commission had a ready-made package on offer – one which did not require significant additional analysis from the EU side, nor a new set of extensive and/or contentious negotiations with the EU Member States.

Yet the translation of the CARIFORUM EPA services package into the multilateral setting should also cause LDCs to pause and reflect carefully on the implementation of that very same package.

A recent EU-funded study reviewing the first five years (2008-2013) of the implementation of the CARIFORUM EPA found, inter alia, that there was little visible evidence of EU Member States’ actually having implemented the provisions on temporary movement. Some key EU markets (e.g. Germany) had yet to even ratify the EPA. Most efforts to craft mutual recognition agreements between relevant sector representatives had yet to materialise. Despite the Caribbean being a largely services-driven region, there was still a surprisingly small share of EU support dedicated to the services sector; many key projects had only recently (i.e. as of 2014) begun substantive operations.

Perhaps as a cause and consequence, the study team could not – after five years of implementation – identify a single Caribbean service supplier that had attempted to enter the EU services market using the EPA.

The CARIFORUM-EU struggle to operationalise its preferential services scheme over the (thus far) nearly seven-year life of the EPA should send clear signals to both LDCs and their potential preference-granting partners. It points to the significant practical and political difficulties in creating tangible, commercial valuable and development-oriented preferences in the services sector for small and developing economies. These difficulties in turn suggest the degree of realism over what can be achieved over the 15-year lifespan of the LDC Services Waiver.

Conclusions: The tail wagging the dog?

In a lecture in Riga in March 2015, the Director-General of the WTO seemed to downplay the importance of regional trade agreements, by stressing that “there are many big issues which can only be tackled in an efficient manner in the multilateral context through the WTO,” where the challenges facing global trade were “global problems demanding global solutions”. This article suggests however that some global problems require (or can at least draw from) regional solutions.

In regional trade agreements, WTO Members may feel more comfortable in testing difficult and unchartered waters between a smaller and better-known set of negotiating partners. Sometimes, non-trade linkages and processes (e.g. aid relationships between donor and beneficiary) can provide a comforting counterpoint to the sometimes-fraught dynamics between trade negotiating partners. This comfort zone is arguably most important for the WTO’s smallest and least-developed Members who form a majority of WTO Members, and have often argued that their small and underdeveloped markets are ill-prepared and unsuited to reap the traditional gains from multilateral trade liberalisation