Search News Results

Kenya National Trade Policy: Transforming Kenya into a competitive export-led and efficient domestic economy

Preface by the Cabinet Secretary

The National Trade Policy is being launched* at a time when the global trade landscape is facing emerging challenges. Over 70 percent of global trade is made up of manufactured goods. Intra-Africa trade averages about 12 percent whilst Kenya’s share of both the global pie as well as in Africa has been facing serious bottlenecks leading to a huge balance of trade deficit with most of our trading partners.

The Trade Policy adds impetus to the robust trade policy reforms that the country has pursued under regional and multilateral trade arrangements. It translates to Kenya’s commitments at regional and multilateral level to solidify policy measures and create opportunity for their domestication through the various instruments that are proposed. This will contribute to strengthening of regional integration and will in turn anchor our country as a dependable and predictable trading partner.

This Policy spells out complementarity with other sectors and provides a framework for these sectors to adopt policies that complement rather than compete with each other. This trade policy in particular introduces a trade agenda in several sectors such as agriculture, industry, infrastructure and ICT.

It creates opportunities for trade-led sector policy formulation to achieve sector specific trade targets. For instance, agricultural and industry policies must be geared towards responding to the national trade agenda of product and destination market diversification. Similarly, energy and infrastructure policies must contribute towards promoting competitiveness of Kenya’s trade sector. ICT, on the other hand must drive trade, in keeping with the global experience, where e-commerce is overtaking traditional commerce because of the savings associated with low cost of trading under e-commerce.

Effective implementation of the National Trade Policy is expected to transform Kenya to a most competitive and prosperous trading nation. Prospects for this transformative impact lie in opportunities in the domestic market as well as in the regional and global markets, where Kenya has immense unexploited trade potential.

The structure and content of the policy portends itself to immediate implementation. I therefore call upon the full commitment and cooperation of all stakeholders to ensure successful implementation of this policy and thus enable it to contribute in a substantial way to Kenya’s national development.

Cabinet Secretary, Ministry of Industry, Trade and Cooperatives

Executive Summary

The Policy Framework

This National Trade Policy has been formulated within the framework of the national long term policy blueprint; the Kenya Vision 2030 which is the basis of the country’s entire policy formulation and implementation for all sectors in the country. The policy formulation has been further guided by the provisions of the Kenya Constitution (2010) which recognizes the concurrent jurisdiction of the national and county governments in relation to trade matters. The policy is also underpinned within the Constitution’s provisions on the Bill of Rights, particularly the freedom of expression, freedom of the media, freedom of association, freedom of movement and residence, protection of right of property, labour relations as well as consumer rights and the Fourth Schedule. In addition, the critical International development aspirations and commitments such as the Sustainable Development Goals (SDGs) as well as regional and international trade agreements to which Kenya is a signatory have guided the formulation; notably: The World Trade Organization (WTO) agreements, the East African Community (EAC) and Common Market for Eastern and Southern Africa (COMESA) Treaties, EAC-EU Economic Partnership Agreement and the African Caribbean Pacific Cotonou Agreement.

The Focus on Trade Policy

The policy aspires to articulate the government’s aspiration towards poverty eradication and sustainable economic development through providing opportunity for expanded markets, income generation and distribution, increased employment and competitiveness. The policy advances the course for poverty reduction by mainstreaming Micro, Small and Medium Enterprises (MSMEs) in the global trade, in view of their critical role in job creation, poverty reduction and the furtherance of export diversification and economic development. Moreover, the Policy builds on the momentum of trade policy reforms that have been ongoing since the mid-1980s, when the country shifted its trade policy from import substitution to export oriented policies. The key features of this reform include the significant reduction in tariff levels as well as the reduced licensing requirements and the elimination of price controls.

Balance of Trade Deficit

The Policy is cognizant of the prevailing situation in the trade sector, where overall trade performance, as measured by the Balance of Trade, has been poor and recording a deteriorating trend that is characterized by huge balance of trade deficits. In addition, the policy is developed in the context of the already documented fact about Kenya’s share in the regional and global market, which remains low, with huge potential already having been identified in sectors that Kenya has both comparative and competitive advantage. The fundamentals behind this situation are traced to a narrow export base, which is characterized by the predominance of primary products and dependence on limited traditional destination markets. Limited value addition in the manufacturing sector and the relatively underdeveloped intermediate and capital goods industries also explain the dismal trade performance.

Trade in Services

The Policy recognizes the important role that trade in services is poised to play in overall development of the economy. The service sector which comprises tourism; transport and communications; trade and related services; and financial and business services, accounts for 60 percent of GDP. Within the service sector, there are emerging trends of growth in domestic trade brought about by the liberalization of the capital markets and the privatization program. In addition, there are new developments of the domestic oriented Business Processing Outsourcing (BPO) and Information Technology Enabled Services (ITES) which has created trade opportunities for MSMEs to provide Business Development Services (BDS). The Trade Policy will therefore facilitate improvements in the enabling of the environment for increased trade in stock and shares and outsourced services.

Unleashing Kenya’s Potential in International Trade

The National Trade Policy seeks to unleash Kenya’s potential targeting domestic, regional and global market. The multilateral, regional integration and bilateral trade arrangements that currently define the space that Kenya’s international trade enjoys present an immense opportunity for pursuit of this policy objective. The task ahead is to address the main constraints and challenges to international trade, which include;

-

Limited capacity for diversification and low value addition in production;

-

Increased use of non-tariff barriers in export markets;

-

Lack of competitiveness due to inefficient trade facilitation infrastructure;

-

Lack of medium and long term finance for SMEs;

-

Limited availability of affordable trade finance;

-

Limited negotiation capacity and uncoordinated negotiation processes; and,

-

Preference erosion, among others.

Finding Sustainable Solutions

The drive in pursuit of solutions to these constraints and challenges is the central role that trade plays in the country’s growth and development as well as poverty eradication. This is through its linkages with all the sectors of the economy where trade creates markets through which goods and services get to the consumers. Trade also plays a critical role in poverty reduction through employment creation in informal, retail, and wholesale trade and provides MSMEs with opportunities of accessing more favourable prices in regional as well as international markets thereby ensuring equitable income distribution.

Complementarity

The National Trade Policy complements other existing sectoral policies and strategies that touch on trade issues including the agriculture and rural development policy, industrial policy, livestock policy, fisheries policy, among others. The National Trade Policy aims at providing a broad and overarching policy framework for other key policies, strategies and official documents affecting trade which include the following:

-

The Kenya Constitution (2010);

-

Agricultural Sector Development Strategy;

-

National Livestock Policies;

-

National Industrial Policy;

-

Competition Policy;

-

Investment Policy;

-

Intellectual Property Policy and Strategy; and,

-

Other Sectoral Policies and Strategies.

In sum, the National Trade Policy establishes coherence with all these other documents and where possible, the policy and its implementation plan incorporates elements of these other strategies, policies and plans in order to ensure as much coherence as possible. The trade policy also becomes a point of reference for sectoral policies and strategies that will be developed in the future, to ensure that such policies and strategies are in harmony with the overall trade policy.

* The National Trade Policy was launched during the National Trade Week, hosted by the State Department on Trade from 10-12 July 2017 at the Kenyatta International Conference Centre. The National Trade Week was held to bring together stakeholders from the public and private sector in Kenya to discuss the current state of play of Trade in Kenya, review progress on key initiatives currently under implementation and to develop a consensus on the path forward towards developing Kenya as an export led economy supported by robust domestic trade.

During the course of the week, other key documents and programs that are important to the private sector were launched, including the following (download below):

Related News

Kanimba calls on Africa to renew efforts to protect its agric sector

It is high time African countries embarked on special safeguard measures (SSMs) to protect the continent’s agriculture sector, François Kanimba, the Minister for Trade, Industry and East African Community Affairs, said Monday.

Put in place by the World Trade Organisation (WTO) that regulates international trade, the SSM is a protection measure allowed for developing countries to take contingency restrictions against agricultural imports that hurt domestic farmers.

Kanimba made the call at the opening of a week-long regional advanced trade negotiation simulation skills course for 32 English speaking African countries, in Kigali, at which participants discuss the impact of mega-regional deals on WTO processes.

Kanimba said the agriculture sector, being the backbone of the continent, African countries should have placed it at the centre of negotiations.

Kanimba said agriculture distorting subsidies are still unaddressed and “expose our small-scale farmers to unfair competition” from subsidised imports from rich countries.

Rich countries spend billions of dollars subsidising their farmers, leading to chronic overproduction and dumping surpluses on global markets, a trade practice that reportedly impoverishes farmers in most African countries.

Regarding market access, Kanimba said, while most African countries enjoy duty-free quota, technical barriers to trade are being imposed by partners to products when trying to export to their markets.

African countries, he said, need to continue advocating for elimination of harmful subsidies in order to achieve promised reforms in the agriculture sector and push for defence measures and easy access to markets for their products.

Many African countries, including Rwanda, he said, have recently faced cheap imports of rice from some Asian countries.

“It is, therefore, important to reemphasise that public stockholdings for the purpose of food security are important but there is a need for fair disciplines to ensure that they are not used for exports which may result in dumping in other markets.”

Dickson Yeboah, head of intensive trade negotiations skills unit at the WTO institute for training and technical cooperation, said there is need for effective global rules on issues that matter to both developing and developed countries.

Yeboah said free trade could serve as the largest economic stimulus package to revive the global economy and fight poverty.

One of the trainees, Jesse Mathies, the assistant director for international trade in Liberia’s ministry of commerce, told The New Times that he expects to take home skills that will help improve his understanding of global trade issues both at continental and sub-regional levels.

Related News

Coordinating public and private action for export manufacturing: issues for Rwanda

One of the keys to economic transformation across Africa today is a greater role for employment-intensive, export-oriented manufacturing.

After taking due account of differences in contexts and time periods, international experience – especially in Asia but also in Africa-region leaders such as Mauritius – points to employment-intensive manufacturing as a crucial and indispensable step in the transition from poverty to development.

Rwanda is – along with Ethiopia – exceptional in Africa in that it has in place a nation-building project centred on the aim of economic transformation. Features of its political economy also mean Rwanda lends itself easily to comparison with the best-documented experiences in Asia. This paper explores the ways in which international experience of success in manufacturing-based economic transformation can provide valuable insight for Rwanda, in the areas of government coordination, engagement with and representation of the private sector, and the experimental learning process.

Executive summary

Along with accelerated agricultural progress, an expanding role for employment-intensive, export-oriented manufacturing is increasingly recognised as a critical next step in the economic transformation of Africa. This poses substantial challenges of various kinds, not least in small, landlocked countries like Rwanda. The challenges include creating institutional arrangements that are effective in coordinating public and private action around well-chosen policy goals.

In the comparative literature on industrial policy and development, six institutional requirements emerge as particularly needing to be satisfied for success in export manufacturing. Using these as a template, this report examines the status and prospects of arrangements for public–private coordination in Rwanda. Our findings draw on extensive interviews with public and private sector actors in Rwanda carried out at intervals over the past decade and ongoing under the Overseas Development Institute’s Supporting Economic Transformation (SET) programme.

The first requirement for success suggested by East Asian and other recent international experience is the establishment of economic transformation as a nation-building project, with shared commitments among key actors extending well beyond a single political cycle. Rwanda stands out in sub-Saharan Africa as a rare example of a country whose underlying political settlement gives a central place to national development goals and protects policy-making from the usual effects of political competition of the patron-client type. The settlement also includes a relatively strong commitment to private sector development. This provides a favourable starting point for building other needed elements of the institutional architecture for public-private collaboration.

Other requirements identified in the literature include the creation of a public agency with sufficient autonomy, budgetary resources and political authorisation to override inter-departmental coordination problems and engage in a practical way with credible private sector organisations. The report discusses this under three headings: coordination in government, engagement with the private sector and the credibility of private sector representation.

Coordination in government: Policy for economic transformation, including export manufacturing, is comparatively well ‘joined up’ in Rwanda, thanks to the fact that under the political settlement the relevant ministries and agencies are not to any degree political fiefdoms. An impressive-looking formal apparatus for policy coordination has also been created, on conventional civil service lines. However, the Rwanda Development Board (RDB) – the organisation that might have been expected to play the forceful coordination role associated with Asian ‘super-ministries’ – has not been given a sufficiently focused mandate or the necessary resources. Although its chief executive has cabinet rank, its mandate is limited to implementing policy and providing a broad range of services. This problem is not unique to Rwanda; similar issues have been raised about Ethiopia’s architecture for investment and export promotion.

Engagement with the private sector: The services provided by the RDB include investment facilitation and investor ‘aftercare’. However, the best Asian models, and experiences at the sector level in some African economies, include a prominent role for public sector departments that are highly knowledgeable about and even socially ‘embedded’ in the private business sectors they deal with. Lack of experience and an insufficiently focused mandate combine to deny the RDB this crucial quality. In managing relations with investors, the RDB also must contend with a wider civil service culture that is good at following rules but has been rather inflexible in terms of addressing snags in the regulatory regime in response to private sector complaints. In addressing these deficiencies, consideration should be given to the pros and cons of reforming the RDB – politically possible but organisationally challenging – or creating something largely new, for example as an adjunct to the president’s Strategic Policy Unit.

We add two important qualifications to this widely shared assessment of the limitations of the current pattern of public–private engagement in Rwanda. One is that, since 2016, the responsible ministry (now Trade, Industry and East African Community Affairs) and the RDB have significantly upgraded their engagement with firms in export sectors, including manufacturing. A series of high-level meetings have resulted in the signing of some 18 bilateral memoranda of understanding (MoUs) in which firms identify export targets and the government commits to addressing the barriers identified by the firms. This is a potential game-changer, but only if the government side can provide the concentrated, specialised capability that Asian experience shows is needed and can be offered even in an inexperienced public sector environment.

The other qualification arises from ongoing SET research showing that Rwanda’s own experience of constructive, mutually accountable engagement across the public–private divide is more diverse and interesting than it appears at first sight. As well as continuing to see a role for state, party-owned and military-linked companies, the government has actively supported medium and small domestic businesses moving into sectors, or a scale of operations, in which they previously lacked experience. These efforts, undertaken without fanfare and without central involvement of the RDB or ministries, have not yet steered significant resources into employment-intensive export manufacturing. However, they provide a sound model for doing so, which will be important in ensuring foreign anchor firms in new manufacturing sectors are quickly supported by domestic private investment in related production and infrastructure. They are also of interest in connection with the future character of Rwandan society and politics, since to a striking degree they involve business people from across the spectrum of Rwandan social backgrounds.

Credibility of private sector representation: The international literature is clear about the importance of this issue and about the difficulties it entails in the early stages of economic transformation. Using relevant comparators and historical experience, we find Rwanda’s progress in this regard to be satisfactory. The active role of government in setting up and supporting the Private Sector Federation has been consistent with global experience on the role of the state in enabling effective private sector representation. Legislation to reserve more benefits to association members should be considered as a next step.

The international evidence on economic transformation places increasing emphasis on technically justified selective support to sectors and firms, as a necessary complement to improving the broadly enabling conditions for investment. This support needs, however, to be backed by mutually enforceable performance standards, including export targets. Rwanda’s most recent experience with firm-by-firm MoUs foreshadows the kind of system that will be needed in the near future for identifying investment partners, agreeing conditional support and regulating the overall ‘deals environment’. We identify two major challenges in taking this forward. One is the lack of priority currently being given to the technical basis for investment project appraisal, as distinct from defining strategic priorities – particularly important when alarming balance-of-trade data create incentives to ‘do something’ in a hurry. The other is to get domestic firms into the emerging performance-linked support system sooner rather than later, given that in Asia this approach has paid off more with domestic than with foreign investors.

The history of industrial policy lends strong support, finally, to the importance of ‘discovery’ by both firms and their public sector regulators. Gains are maximised in this respect where there is an explicit governmental commitment to experimentation, rapid feedback and timely corrections. Rwandan policies have reflected an exceptional commitment to learning by doing over many years, and President Kagame has emphasised this in economic policy contexts in several recent speeches. However, general adoption of this way of working is in tension with rigorous rule enforcement, which remains a necessary condition of the country’s exceptionally corruption-free business environment. The suggested solution is to draw on the central lesson of Asian experience once again by concentrating available capacity to think and work in an adaptive, problem-driven way in an organisation or organisations with a tightly focused mandate.

In summary, Rwanda’s political settlement provides an unusually favourable platform for emulating the most successful experiences in other parts of the world in making the breakthrough into employment intensive, export-oriented manufacturing. However, a platform is no more than a platform, and urgent attention is needed to several of the other five requirements for success the international literature suggests. Principally lacking at this point is an adequate concentration of capability, including private sector experience and the ability to use economic appraisal techniques, in a sufficiently empowered public agency. Steps currently being taken to improve public-private coordination are important and serve to reinforce this conclusion.

» Download: Coordinating public and private action for export manufacturing: international experience and issues for Rwanda (PDF)

Related News

WCO welcomes 2017 G20’s recognition of its work on Illicit Financial Flows

The G20 leaders recognize the work of the World Customs Organization (WCO) in combatting Illicit Financial Flows (IFFs) in documents agreed following the 2017 G20 Hamburg Summit. The Secretary General of the WCO, Dr. Kunio Mikuriya, welcomes this recognition and invites WCO Members to pursue efforts to tackle this issue and to actively participate in the activities undertaken by the WCO on this topic.

The 2016 G20 Hangzhou Meeting had welcomed the “communication and coordination with the World Customs Organization for a study report” to address “cross-border financial flows derived from illicit activities, including deliberate mis-invoicing, which hampers the mobilization of domestic resources for development.” Following this mandate, and after Member’s deliberation, the WCO produced an Action Plan to capture the strategy to counter IFFs and same has been communicated to the German G20 Presidency and the G20 Heads of Customs.

The Action Plan will bring special attention to the question of trade mis-invoicing and also touch on other methods such as transfer mispricing, tax evasion and avoidance, cash smuggling, and informal funds transfer systems. WCO Secretary General Kunio Mikuriya stated that “WCO will continue its action plan to combat IFFs and further enhance its coordination with the G20”, adding that “the WCO Council has, during its 129th/130th Sessions, identified IFFs as one of the six main priorities for Customs Community, along with Trade Facilitation, Security, E-commerce, Customs-Tax Cooperation and Performance Measurement.”

Customs and the Fight Against Illicit Financial Flows World Customs Organization Action Plan

It has been well-recognized that Illicit Financial Flows (IFFs) hamper sustainable development and present a direct threat to global political and economic security. The loss of capital from corruption, organized crime, illegal exploitation of natural resources, fraud in international trade and tax evasion, deprives countries of vital revenue that could be used to develop infrastructure, provide basic social services and invest in projects to create jobs.

By undermining development efforts, IFFs contribute to persistent poverty and to the perception of corruption and poor governance that can lead to political instability. While, on the one hand, IFFs impede government efforts to mobilize domestic resources, on the other hand they can serve to finance criminal or terrorist activities.

As the first line of defence at the borders, Customs has an important role to play in combating illicit financial flows while facilitating legitimate trade. The misuse of trade for the movement of illicit funds, as well as the physical cross-border movement of money, are areas that relate directly to Customs’ competence and expertise and are subject to strong enforcement measures.

Background

The G20 Leaders’ Communiqué from the Summit held in Hangzhou, China, in September 2016 highlighted, among other things, the importance of addressing cross-border IFFs derived from illicit activities. More specifically, paragraph 36 of the Communiqué welcomed communication and coordination with the World Customs Organization (WCO) to address cross-border financial flows derived from illicit activities, including deliberate trade mis-invoicing.

The WCO welcomed this opportunity to contribute to the work of the G20 and has been proactively considering ways to work with the G20 on the development of a study on cross-border financial flows coming from illicit trade, including deliberating on this issue at its Policy Commission held in December 2016.

Related News

tralac’s Daily News Selection

Today, in Dar es Salaam: Development cooperation between China and Tanzania: trade and investment (ESRF, China Agricultural University). Twitter updates: #TanzaniaChinaConf

Starting today, in Geneva: Brazil’s Trade Policy Review

Diarise: Second Japan-Africa Business Forum (25-26 July, Tokyo)

Africa Regional Integration Index 2018: update (UNECA)

David Luke, Coordinator of the ATPC, said two issues of critical interests ahead of the publication of the Index in 2018 were how far the ARII 2018 Report captures the drivers of regional integration in Africa. Also important, he said, was for the experts to discuss to what extent the inclusion of social variables, such us the Gender Index, could promote social-sensitive integration policies on the continent. The ARII Report will have a ranking of countries not only within their respective RECs, as was the case with the first version of the Index, but also a continental ranking. [Africa Regional Integration Index: 2016 Report]

David Luke: The African trade revolution quietly afoot (African Arguments)

The CFTA negotiations are complex. The 55 participating countries span a diversity of economic and geographic configurations. 15 are landlocked, while six are Small Island Developing States. The biggest (Nigeria) has a GDP of $568bn, while the smallest (Sao Tome & Principe) a GDP of just $337m. The CFTA must likewise be crafted as a win-win agreement that leaves no one behind. Here, the UNECA has undertaken a human rights impact assessment of the initiative and advocated for a number of supporting measures. This includes strategies to protect small-holder farmers and help them integrate into regional agricultural value chains. It calls for improving border controls to help informal cross-border traders, many of whom are women and major players in intra-African trade. It also demands an approach that benefits Africa’s diversity of countries, including those which are small, island economies, landlocked or fragile states. One way to achieve this is by supporting initiatives for regional value chains and connectivity that have proven successful in Africa’s regional economic communities. [CFTA negotiations moving in the right direction]

(i) USTR announces 2018 eligibility review process, timelines (pdf): This notice announces the initiation of the annual review of the eligibility of the sub-Saharan African countries to receive the benefits of the African Growth and Opportunity Act. The AGOA Implementation Subcommittee of the Trade Policy Staff Committee is developing recommendations for the President on AGOA country eligibility for calendar year 2018. Key dates: 4 August: Deadline for filing requests to appear at the August 23, 2017 public hearing, and for filing pre-hearing briefs, statements, or comments on sub-Saharan African countries’ AGOA eligibility. 23 August: AGOA Implementation Subcommittee of the TPSC will convene a public hearing on AGOA country eligibility. 30 August: Deadline for filing post-hearing briefs, statements, or comments on this matter.

(ii) EAC officials oppose US bid to review AGOA trade deal over mitumba ban. Looming over the three-hour session before a standing-room-only audience was the Trump administration’s “America First” policy. The hearing chaired by Constance Hamilton of the US Trade Representative’s office was contentious at times. She and other US officials challenged the East Africans’ insistence that the agreed-upon three-year phase-out of used clothing imports did not amount to a “ban”. A member of Uganda’s delegation at the hearing also insisted that Tanzania’s and Uganda’s doubling of levies on used-clothing imports — from $0.20 to $0.40 per kilogramme — was not a “tariff increase” but rather a “realignment.”

(iii) CSOs back ban of secondhand clothes. “It’s against this background that as the trade working group comprising of members of civil society and manufacturers, we fully support the decision taken by the heads of states to progressively phase out second hand clothes,” they said. “It’s critical that the EAC policy space for development is not constrained.” George Magimbi, policy officer of Uganda Manufacturers Association, stressed the importance of progressively eliminating the importation of secondhand clothes so as to fulfill the four SDGs which talk of ending poverty in all its forms and supporting the industrial sector. [SEATINI: statement]

(iv) August’s AGOA Togo forum. Representatives from the private sector, civil society, and the US-sponsored African Women’s Entrepreneurship Program will participate in Forum activities 8-9 August. The Ministerial plenaries will follow on 9-10 August, bringing together senior government officials from the United States and the 38 African beneficiary countries. US Trade Representative Ambassador Robert Lighthizer will lead the US delegation, which will include senior officials from the Departments of State, Agriculture, Commerce, Labor, Transportation, Treasury, USAID, the US Trade and Development Agency, as well as the Millennium Challenge Corporation, the Overseas Private Investment Corporation, and the US African Development Fund. Members of Congress and their staff from both parties are also invited to attend the Forum.

Kenya falls short of India pulses export quota deal (Business Daily)

Kenya has failed to meet the Indian market demand for pulses two years after the signing of a memorandum of understanding for the supply of beans, peas and green grams. In the MoU signed in 2015, India had given Kenya a quota of four million metric tonnes. However, Kenya is only supplying 20 per cent of the 800,000 metric tonnes annual production. Programmes coordinator at East African Grain Council Janet Ngombalu says low production has been occasioned by a lack of awareness by farmers on certified seeds. The growers have also not understood the advantage of pulses compared to other crops such as maize they prefer to grow.

Morocco’s Sub-Saharan trade increased 9.1% in 2016 (World News)

Trade between the two sides has grown at an average annual rate of 9.1% since 2008, reaching nearly MAD 20bn in 2016. The share of these exchanges is 3% of the total in 2016, against 2% in 2008. These flows generate a surplus trade balance in favor of Morocco of MAD 11.9bn in 2016 compared of 1.3bn in 2008. West Africa remains Morocco’s largest trading partner in the region with a total of MAD 11.2bn surplus trade balance. Senegal remains the main customer of Morocco in West Africa. East Africa is the second largest trading partner of the Kingdom in sub-Saharan Africa (a 15.5% share). In addition, the study shows that Moroccan direct investment in sub-Saharan Africa is growing at an average annual rate of 4.4% to nearly MAD 3bn in 2015. These investments account for 40% of total foreign direct investment by Moroccans living abroad and 97.2% of those residing in Africa. [OCP Policy Center: Relations between Morocco and sub-Saharan Africa: what is the potential for trade and foreign direct investment?], [Rwandan firms sign trade deals with Moroccan companies]

Rwanda: Investment strategy to foster structural transformation (pdf, IMF)

Stimulating private investment in Rwanda is difficult because of the size of the economy and its land-locked status but the government is trying to address this through regional integration. The EAC trade block can help diminish the drawback of being landlocked by lowering the cost of imports and improving connectivity in terms of transportation. It has been successful in lowering non-tariff barriers and Rwanda is in the process of establishing a dry port in Kigali to ease in traffic transit through Kigali to the DRC. Realistically, Rwanda needs to look west as a destination for its exports because, up to now at least, it has been unable to compete with countries closer to the sea. Over the past 15 years, while Rwanda goods imports from Uganda have risen by almost 15 percentage points to 18% of the total, it has been unable to penetrate Uganda with its exports.

On the other hand, it has been successful in exporting to Congo. The share of Rwanda exports to Congo (mainly re-exports) has doubled over the past 5 years and now represents 26% of the total ($172m). Many of these are low value-added products because only limited transformation occurs in Rwanda (petroleum and used vehicles originating from outside of the continent). A typical product exported to Congo with some value addition is wheat flour but currently the wheat required to be converted into flour is imported from overseas because of the competitive price and quality of the import. Infrastructure is being developed at the DRC border to speed up the movement of goods. A one stop border post is being finalized in Rubavu that will require only one inspection of goods between Rwanda and DRC. Moreover, development partners have helped finance a program to support traders at the border and bilateral trade meetings between the Rwanda and DRC presidents have started. This strategy has strong potential because the north Kivu region has population base of over 14 million within 100 miles of the Rwandan border. [Rwanda: 2017 Article IV Consultation]

Angola’s ghost railway: the Caminho de Ferro de Benguela line (Business Day)

It was meant to be a game changer for the region, an artery for exporting minerals from the DRC through Lobito, the closest port to Europe and Asia. But there’s very little to show for all the money spent on it.

China and the East Africa railways: beyond full industry chain export (Brookings)

Both railways are examples of whole industry chain export, rather than the export of single, individual service contract under the railway project. From project designs to equipment procurement, from construction to financing, from supervision to the operation and maintenance of the railways after their completion, Chinese companies and banks monopolized the complete chain. This situation does not only offer the Chinese players a unique and exclusive opportunity to promote Chinese products, services, technologies, and management models, but also significantly expanded the scope of spinoff economic projects not indirectly related to the railway projects. [The author: Yun Sun]

Kenya: 400 Chinese workers sign deal to run SGR operations (Business Daily)

About 400 Chinese operators have signed a deal with China Road and Bridge Cooperation (CRBC) to be part of the daily operators of Madaraka Express train. The team comprises experienced engineers, security personnel and staff of rail operations from China who will be in Kenya for the next 10 years until the railway operation is handed over to the Kenyan team, according to Kenya Railways Managing Director Atanas Maina. Mr Maina said there are currently 300 local trained personnel manning the train. “We intend to add a few more going forward. This will depend on the volume of business and the skill sets required.”

Outcome of India’s trade deals focus of Nirmala Sitharaman’s first Geneva visit (Mint)

On her first visit to Geneva as India’s trade and commerce minister Nirmala Sitharaman is expected to underline the need to deliver development outcomes of trade deals that would address the asymmetries in the global trading system that deny equitable results to developing and poorest countries, according to people familiar with the visit. Sitharaman, who will be on a two-day visit to Geneva beginning on 18 July, will meet the WTO and UNCTAD chiefs and hold a series of meetings with trade envoys. During these meetings which will last until 19 July, Sitharaman will assess the state of play in the ongoing negotiations on a range of unresolved issues of the Doha Development Agenda as well as controversial new issues being pushed by major industrialized countries along with some developing countries, said a person familiar with her programme. [India’s trade deficit narrows to $13bn in June]

Aid for Trade Global Review 2017: profiled case stories

A total of 145 case stories were received, which included capacity building programmes in trade facilitation, experiences in building trade-related infrastructure, and improving ICT in developing countries. (i) Swedish MFA: Services trade, industrial development and the African Continental Free Trade Area (ii) TMEA: Busia One Stop Border Post, (iii) USAID: Women in informal cross border trade in Southern Africa, (iv) TMEA: Elimination of non-tariff barriers to trade in East Africa

|

Quick Links: Nigeria: ‘N7tn spent on importation of consumables in 2015’ Uganda: World Bank urged to fund warehousing and logistics system WTO Members reaffirm commitment to Aid for Trade and to development support Klaus Schade: Applaud SADC for progress in regional integration Giture Mwaura: One cannot fault the EAC cost-benefit analysis Sekou Toure Otondi: Regional integration has taken back seat in Kenya’s election. Why does it matter? Ben Murray Bruce: Africa’s future lies in trade, not in aid! |

Related News

The African trade revolution quietly afoot

In a tumultuous year for the global trading landscape, negotiations for a huge Africa-wide free trade area are progressing rapidly.

Across the developed world, longstanding advocates of free trade are in retreat. America has withdrawn from the Trans-Pacific Partnership trade agreement and stepped back from the World Trade Organisation. Meanwhile, a crisis is brewing at the heart of the European single market.

Recognition has grown that the inequalities generated by trade are not being sufficiently addressed. And this has fuelled an anti-trade populism.

Noting these tumultuous trends, international institutions from the OECD to the International Monetary Fund and G20 have sought to reaffirm the benefits of trade and argued against protectionism.

A quiet revolution

Set against this uproar, an African trade revolution is also quietly afoot. The innovation is the Continental Free Trade Area (CFTA). A boldly ambitious endeavour, the CFTA seeks to combine the economies of 55 African states under a pan-African free trade area comprising 1.2 billion people in a market with a combined GDP of $2.19 trillion.

Announced in 2012 by the African Union (AU) heads of state and government, the CFTA is the first flagship initiative of the AU’s Agenda 2063. It will reduce tariffs between African countries, introduce mechanisms to address the often more substantial non-tariff barriers, liberalise service sectors, and facilitate cross-border trade. This will also help rationalise the overlapping free trade areas that already exist within Africa.

The CFTA negotiations are complex. The 55 participating countries span a diversity of economic and geographic configurations. 15 are landlocked, while 6 are Small Island Developing States (SIDS). The biggest (Nigeria) has a GDP of $568 billion, while the smallest (Sao Tome & Principe) a GDP of just $337 million.

Rapid progress

Many outside observers have been quick to cast pessimism upon the project. This is not just because of the challenging world trade environment and complexity of negotiations, but Africa’s history of trade negotiations.

In particular, the Economic Partnership Agreements (EPAs) between the European Union and African regional economic communities have proved an infamous failure. Despite 14 years of negotiations, only one EPA – that with Southern Africa – has been concluded.

With expectations low, the rapid progress in the CFTA negotiations is therefore all the more remarkable. The first negotiating forum was launched in February 2016. Since then, five more negotiating rounds have been concluded.

The most recent, held in Niger, determined modalities for trade in goods and services. It also pronounced a level of ambition to liberalise 90% of tariff lines – substantially more than aspired to in the EPAs – and establish a review mechanism to gradually lift this further.

The remainder of 2017 will see technical working group meetings and two more negotiating rounds to refine market access offers and the legal text of the agreement. The intention is to finish negotiations by the end of this year.

One African chief negotiator commenting at the last negotiating round remarked that he had “never seen negotiations move so rapidly”.

Boosting intra-African trade

These impressive achievements are being realised by political commitment at the highest level and a pan-African resolve to cooperate and compromise. Pan-Africanist forefathers like Kwame Nkrumah would be proud.

Success also derives from a shared belief in the project. Studies by the UN Economic Commission for Africa and UNCTAD identify the potential for the CFTA to boost intra-African trade. This would help diversify Africa’s exports away from a dependence on commodities that is little changed since colonial times.

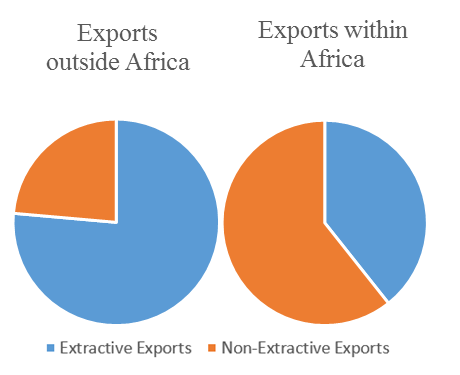

Intra-African trade is substantially more diversified than Africa’s trade with the outside world. It comprises a greater share of value-added and industrial products such as textiles, cement, soap, pharmaceuticals, and even automobiles from South Africa as well as primary and processed food items. Services such as banking, telecoms, energy and transport are also being traded across borders. The CFTA forms part of an African strategy for industrialising through trade.

Source: CEPI-BACI Trade Dataset, three year average (2012-14).

It could also help piece together Africa’s small fragmented markets to realise economies of scale necessary for industrial investment and growth. Niger’s President Issoufou Mahamadou, the African Union Champion for the CFTA, recently lamented looking upon a map of Africa as a “broken mirror”. The CFTA can help to fix this.

Making it a win-win

The CFTA, however, is no panacea. It must be accompanied by investments in infrastructure, energy and trade facilitation.

This is critical if sufficient jobs are to be created for Africa’s youth. 60% of Africa’s population is 24 or below and about to enter the workforce. Yet a shortage of opportunities contributes to high youth unemployment, poverty rates approaching 70%, and pressures to migrate.

It is also important not to overlook the origins of populist sentiment against free trade elsewhere in the world. Trade produces both winners and losers. The problem is that while gains can compensate losses in theory, that is not happening in practice.

Recognition of this has fuelled rethinking of trade policy across the world. For instance, the Canada-European Union trade agreement (CETA) was reworked following the election of the Trudeau administration to better reflect a new “progressive trade policy”.

The CFTA must likewise be crafted as a win-win agreement that leaves no one behind. Here, the UN Economic Commission for Africa has undertaken a human rights impact assessment of the initiative and advocated for a number of supporting measures.

This includes strategies to protect small-holder farmers and help them integrate into regional agricultural value chains. It calls for improving border controls to help informal cross-border traders, many of whom are women and major players in intra-African trade.

It also demands an approach that benefits Africa’s diversity of countries, including those which are small, island economies, landlocked or fragile states. One way to achieve this is by supporting initiatives for regional value chains and connectivity that have proven successful in Africa’s regional economic communities.

Light at the end of the tunnel

Light shines at the end of the tunnel for the CFTA, but obstacles remain. Implementation is a key but persistent challenge on the continent. To quote Nkosazana Dlamini-Zuma, former Chairperson of the AU Commission, “I don’t think Africa is short of policies. We have to implement. That is where the problem is”.

The commitment and belief shown in the CFTA by African leaders must be seen through for the benefits of the CFTA to be realised.

The reward would appear to be worth it. Africa’s consumer market is the fastest growing in the world. In just over 30 years from now, by 2050, it will comprise a population larger than that of India and China combined. This is the right time to seize the opportunities generated by such a large market.

Related News

EAC officials oppose US bid to review Agoa trade deal over mitumba ban

Senior officials from Rwanda, Tanzania and Uganda argued in Washington on Thursday that their collective phase-out of used clothing (mitumba) imports should not result in any loss of benefits from a US preferential trade programme.

The representatives of the three East African Community (EAC) countries spoke in opposition to an effort by a US business association to restrict their eligibility for the trade initiative known as the African Growth and Opportunity Act (Agoa).

The Secondary Materials and Recycled Textiles Association (Smart) filed a petition with US trade authorities in March urging that the three countries, along with fellow EAC member Kenya, be deemed ineligible for Agoa’s allowance of duty-free textile and apparel exports to the US market.

Lawrence Bogard, an attorney representing Smart, warned at Thursday’s US government inquiry that the association’s member companies would suffer major losses in jobs and revenues if the EAC ban on used-clothing imports is fully implemented.

Partial loss

Mr Bogard also argued that Kenya should be included among the EAC countries facing partial loss of their Agoa benefits.

The top US trade agency had announced last month that Kenya would be excused from the group of countries potentially subject to review of their Agoa eligibility.

That decision was said to be based on “recent actions Kenya has taken, including reversing tariff increases, effective July 1, 2017, and committing not to ban imports of used clothing through policy measures that are more trade-restrictive than necessary to protect human health.”

But the Smart representative suggested on Thursday that Kenya ought to be included in the Agoa eligibility review until officials in Nairobi clarify their commitments.

Smart specifically seeks confirmation that Kenya’s reported imposition of minimum tariffs on containers of used goods “will not be implemented in a manner that negates the July 1 roll-back of Kenya’s tariff increases,” Mr Bogard said.

Kenya would have far more to lose from suspension of its duty-free textile export privileges under Agoa than would any of the other EAC countries.

Kenya sold $394 million worth of textiles and clothing on the US market last year, compared to the total $43 million sum of Agoa trade for Rwanda, Tanzania and Uganda.

The Kenyan embassy in Washington says that 66,000 jobs in Kenya are linked to Agoa’s textile-export provisions.

The opposing parties presented their comments to a panel of representatives of six US government agencies: the departments of Commerce, Labour, Treasury and State, as well as the US Agency for International Development and the Office of the US Trade Representative.

Kenya was not represented at the hearing.

‘America First’ policy

Looming over the three-hour session before a standing-room-only audience was the Trump administration’s “America First” policy.

The US president has vowed to oppose any trade initiative that he deems injurious to American interests.

And Smart sought on Thursday to depict the EAC ban on used-clothing imports as a threat to thousands of US jobs.

The hearing chaired by Constance Hamilton of the US Trade Representative’s office was contentious at times.

She and other US officials challenged the East Africans’ insistence that the agreed-upon three-year phase-out of used clothing imports did not amount to a “ban.”

A member of Uganda’s delegation at the hearing also insisted that Tanzania’s and Uganda’s doubling of levies on used-clothing imports – from $0.20 to $0.40 per kilogramme – was not a “tariff increase” but rather a “realignment.”

Ms Hamilton also pointedly asked how Rwanda’s increase from $0.20 to $2.50 per kilo could be seen as consistent with the rules of the World Trade Organisation.

A Rwandan representative replied that the increase would be in effect for only one year.

Washington-based trade consultant Stephen Lande asserted that the hearing should not have been convened at all.

Taking the side of the East African representatives, Mr Lande told the panel that the US Congress intended that such official inquiries should be held only when “all other possibilities have been exhausted.”

Consultations failed

Ms Hamilton responded that prior consultations had failed to resolve the issue at hand.

She added that “Smart has the right” to petition for punitive action against countries alleged to be violating Agoa rules.

Some of the statistics presented by Smart also differed markedly from those offered by EAC representatives.

Mr Bogard put the total annual value of US used-clothing exports to the EAC countries at $124 million. A Ugandan official said the total is about $30 million.

EAC countries’ representatives also disputed Smart’s contention that the used-clothing action violates two of Agoa’s eligibility criteria.

The 17-year-old programme requires participant countries to have achieved “elimination of barriers to US trade” or be making progress in that direction.

Agoa also stipulates that benefit-recipient countries should be moving toward a “market-based economy.”

‘Market forces’

Ms Hamilton asked at one point why the EAC countries don’t let “market forces” determine consumers’ clothing choices.

A Ugandan official replied that market forces should be determinants but should also be “guided” when necessary.

The EAC countries decided to adopt the used clothing import phase-out as a means of encouraging development of their own textile manufacturing sectors, said Uganda Trade Minister Amelia Kayambadde, who spoke in her capacity as chair of the EAC’s Council of Ministers.

“Industrialisation is a strategic pillar of EAC integration,” Ms Kayambadde said.

“The heads of state decided that textiles and footwear manufacturing is a priority.”

Growth of those sectors will likely create many more jobs in East Africa than will be lost through the shutdown of local businesses involved in the used-clothing trade, the EAC representatives argued.

Apparel manufacturing involves “a long value chain,” Ms Kayambadde noted.

She suggested that jobs would be produced all along it in the form of cotton growing, ginning, weaving, garment manufacturing, leather tanning, shoe making and retail businesses.

Asked by US panel members to provide studies showing such an outcome, EAC representatives said such analyses are being undertaken.

They meanwhile offered anecdotal responses.

‘New clothing’

A Ugandan official said “Kenya has found a big, big appetite for new clothing and goods produced within the region.”

Ms Kayambadde concurred that throughout the EAC “the demand is now for new clothing.”

East Africans, she said, “want a new life. People are able to afford to buy new things.”

Mr Bogard argued on Smart’s behalf that the ban on used clothing imports will be more likely to benefit Asian producers of low-cost garments than East African entrepreneurs seeking opportunities as textile manufacturers.

Loss of Agoa textile-export benefits would harm not only the EAC countries themselves but also US clothing manufacturers operating in East Africa, said Jeremy Lott, president of San Mar Corporation.

His firm based in the western US employs 4,000 Americans and hundreds of Tanzanians, Mr Lott told the panel.

San Mar manufactured more than 10 million shirts at its Tanzanian facilities last year that were subsequently exported to the US, he noted.

“An abrupt end of Agoa eligibility for Tanzania would force us to move production to China,” Mr Lott warned.

He said that members of San Mar’s mostly female workforce in Tanzania are paid at rates five times the national average income.

Related News

Uganda and the EAC should stand firm on the decision to progressively phase out second hand clothes

Civil society organizations under their umbrella “Working Group on Trade & Development” have requested the government of the republic of Uganda and the East African Community (EAC) in general to completely phase out the importation of second hand clothes into the region. The request was echoed through a press conference held at the SEATINI-Uganda offices in Bukooto on 13 July 2017.

They brought out facts that the heads of state on 20th February 2015 directed the council of ministers to study modalities for the promotion of textile and leather industries in the region. The decision arose out of the need for the EAC to advance a market driven towards integration by boosting manufacturing and industrialization.

It is on this note that Amb. Nathan Irumba, the executive director SEATINI Uganda, requested the government to seriously support both financially and policy wise the growth of the cotton textile and apparel sector.

Susan Nanduddu, the Executive director ACTADE believes that by phasing out these second hand clothes, the realization and achievement of the president’s vision of 2040 will come true. “I believe that the parliament of Uganda shall bring that bill back to table and push for a complete ban on second hand clothes said Nanduddu. Our administrators should consider the citizens dignity of not wearing under garments (underwear) which have already been worn by Americans”.

In addition she stated that women in Uganda play a big role in the agriculture and textile industry, i.e. knitting which comes as an added advantage and therefore a need to revive these sectors.

“It should be noted that a couple of years back in Uganda, citizens used to have “Jinja clothes” not because of the brand “Jinja” but as a result of being locally manufactured in Jinja,” said George Magimbi, a policy officer at Uganda Manufacturing Association.

He emphasized that government should support the cotton and textile industry since these sectors can greatly curb unemployment levels especially among the youths & women as well as producing sustainable and decent economic growth in the country. Therefore to achieve the vision 2040, there is need to promote local industries through the “Buy Uganda Build Uganda (BUBU)” campaign and therefore a need to ban second hand clothes.

AGOA should not be used as a dumping mode to Africa but rather a channel for development. With the increased purchase of second hands in Uganda, the question that needs to be addressed is whether Ugandans will afford the locally produced clothes. However if we are to move forward, we need to insist on standards.

Related News

The UK’s Repeal Bill: Exiting the EU with certainty

The Repeal Bill is designed to ensure that the UK exits the EU with maximum certainty, continuity and control.

The Government on 13 July 2017 took the next step in returning power from Brussels to the UK by introducing the European Union (Withdrawal) Bill.

Known as the Repeal Bill, it is designed to ensure that the UK exits the EU with maximum certainty, continuity and control. As far as possible, the same rules and laws will apply on the day after exit as on the day before.

This will allow the UK to leave the EU while ensuring that our future laws will be made in London, Edinburgh, Belfast and Cardiff.

For businesses, workers and consumers across the UK that means they can have confidence that they will not be subject to unexpected changes on the day we leave the EU. It also delivers on our promise to end the supremacy of EU law in the UK.

The Secretary of State for Exiting the European Union, David Davis, said:

“This Bill means that we will be able to exit the European Union with maximum certainty, continuity and control. That is what the British people voted for and it is exactly what we will do – ensure that the decisions that affect our lives are taken here in the UK.

“It is one of the most significant pieces of legislation that has ever passed through Parliament and is a major milestone in the process of our withdrawal from the European Union.

“By working together, in the national interest, we can ensure we have a fully functioning legal system on the day we leave the European Union.

“The eyes of the country are on us and I will work with anyone to achieve this goal and shape a new future for our country.”

The Repeal Bill is a mechanism to achieve three simple aims:

-

Repeal the European Communities Act, remove supremacy of EU law and return control to the UK.

-

Convert EU law into UK law where appropriate, giving businesses continuity to operate in the knowledge that nothing has changed overnight, and providing certainty that rights and obligations will not be subject to sudden change.

-

Create the necessary temporary powers to correct the laws that no longer operate appropriately so that our legal system continues to function outside the EU.

The Bill sets out how we will prepare our statute book for exit but will not make major changes to policy or legislation beyond what is necessary to ensure the law continues to work properly on day one.

As we exit the EU we want to ensure power sits closer to the people of the UKthan ever before. The Bill will ensure that nothing changes for Scotland, Wales and Northern Ireland – they will not lose any of their current decision-making powers.

The Government expects there will be a significant increase in the decision-making power of each devolved administration.

As powers are repatriated from the EU, the Government will ensure they are exercised within the UK in a way that ensures no new barriers to living and doing business within the UK are created. This will protect the UK internal market, ensuring we have the ability to strike the best trade deals around the world, protect our common resources, and fulfil our international obligations.

The Government has already made clear that as the Bill affects the powers of the devolved administrations and legislates in devolved areas, we will seek the consent of the devolved legislatures for the Bill. We would like all parts of the UK to come together in support of this legislation, which is crucial to delivering the outcome of the referendum.

The Bill will also provide the Government with a limited power to implement elements of the withdrawal agreement we expect to reach with the EU before we exit.

We are clear we want a smooth and orderly exit and the Bill is integral to that approach.

To ensure we are prepared for the process of withdrawal from the EU, the Government will also introduce a number of Bills over the course of the next two years including a Customs Bill and an Immigration Bill.

The Repeal Bill means we can make corrections to EU law so that it functions as UK law – this could involve changing a reference to a particular piece of EU law or transferring important functions from EU institutions to UK institutions, depending on the outcome of the negotiations. Allowing corrections to be made quickly will provide certainty for business.

Position papers published ahead of July negotiation

Position papers outlining how the UK will negotiate on important issues related to Brexit – and take steps towards fostering a new deep and special partnership with the EU after we leave – have been published.

Ahead of the second round of negotiations next week, the documents lay out the UK’s approach to issues related to our withdrawal from the EU on:

Each of the papers will be presented to the Commission for discussion next week.

Secretary of State for Exiting the European Union David Davis said:

“These position papers mark the fair and transparent way that the UK is approaching Brexit negotiations ahead of the second round of talks next week – and demonstrate how deciding the shape of our future partnership with the EU is inextricably linked with our withdrawal talks.

“While we’re leaving the EU we are not leaving Europe, and we want to continue cooperating with our friends and neighbours on issues of mutual importance including nuclear safeguards.

“By ending the jurisdiction of the Court of Justice of the European Union, UK courts will be supreme once more. Our sensible approach to pending cases means there would be a smooth and orderly transition to when the court no longer has jurisdiction in the UK.”

The papers can be viewed on our Article 50 and negotiations with the EU microsite here.

» Plan for the UK leaving the EU: Prime Minister’s letter to Donald Tusk triggering Article 50

Related News

Aid for Trade Global Review 2017: Sample case stories

Ahead of the Aid for Trade Global Review 2017, a monitoring and evaluation exercise was conducted to survey Aid-for-Trade results and priorities. The monitoring exercise invited the public and private sectors to submit case stories about Aid-for-Trade projects under the theme of “Promoting trade inclusiveness and connectivity for sustainable development”.

A total of 145 case stories were received before the cut-off date, which included capacity building programmes in trade facilitation, experiences in building trade-related infrastructure, and improving information and communications technologies (ICT) in developing countries. A sample of these case stories is provided below. The full collection of submitted case stories is available here.

While the WTO does not deliver the development assistance itself, the organization instead has a mandate to promote coherence between trade and development. As such, the WTO works to encourage additional flows of Aid for Trade, advocates for the integration of trade into national and regional development strategies, and monitors the impact of the financing of various donors on the ground.

Services Trade, Industrial Development and the African Continental Free Trade Area

Ministry for Foreign Affairs, Sweden

The Swedish Government has engaged with tralac – a capacity-building organisation developing trade-related capacity in Africa – since 2010 in order to promote, inter alia, regional economic integration. The African Continental Free Trade Area (CFTA) negotiations were launched in July 2015 and early on, tralac identified the need to engage proactively with the CFTA process to increase services trade capacity and to advance thinking about services trade for industrial development. Through numerous policy relevant studies and workshops, tralac have directed resources towards capacity development and thought leadership on trade in services. Key components have been the production of high-quality and timely research, interactions with many of the key stakeholders and presentation of the data in a non-technical manner. There has been a clear demand pull for further work and it is likely to contribute to an integration of CFTA provisions on services with strategies of investment generation, industrial development and regional integration.

Objective of tralac’s Work on CFTA, Services and Industrial Development

To increase services trade capacity and to advance thinking on the continent about services trade, since the launch of negotiations, the aim of tralac has been to direct further efforts and resources towards capacity development and thought leadership on trade in services. Combined with the centre’s existing work on industrial development and trade, this has enabled them to develop a strong base for several initiatives. A particular ambition of the analysis has been to present the data in a non-technical manner to be accessible to non-services experts.

Activities and Key Messages

tralac supports the concurrent negotiation of trade in goods and services, and have undertaken studies and communicated these through various fora in order to inform the development of several key messages for trade policy makers, negotiators and other trade policy stakeholders on the continent.

First of all, following the decision by the African Union Assembly in January 2012 to expeditiously establish a Continental Free Trade Area (CFTA), tralac contacted the African Union Commission (AUC) and organized a one-day open discussion on the implications of this decision. This workshop took place in Addis, Ethiopia in April 2014. Subsequently, a series of papers were produced on aspects of the CFTA for Africa; these were distributed directly to the AUC in addition to the tralac network of subscribers across African countries and further afield, as well as more than 1500 twitter followers. Members of the AUC have been invited to the tralac Annual Conference since 2014. Requests for 3 further analysis, focusing on legal and institutional matters, on options for trade in services negotiations modalities followed in 2015, as did requests for tralac staff to contribute to training programmes on services and legal issues. Since then tralac participated in the preparation of a draft CFTA Agreement through workshops in May and September 2016.

Outputs and Key Messages

Firstly, a very comprehensive study of trade in services for African countries was done (available here). Other efforts include:

-

Quantitative work on the economic impact of services trade restrictions

-

Analytical work on services negotiations modalities

-

Analytical work on specific services sectors including transport, tourism and financial services

-

Analytical work on movement of persons

In summary, the key messages have been:

-

New approaches, in line with current international practice, that are more cost-effective and efficient in terms of negotiating effort and more integration enhancing in terms of potential outcomes should be considered, in light of the appropriateness (or not) of approaches and modalities adopted by the WTO and the regional economic communities for the negotiation of trade in services agreements in this day and age on the continent.

-

Private sector interests associated with international production networks increasingly require a new approach to trade negotiations away from the traditional focus on market access to measures affecting production behind the border, with emphasis on regulatory issues.

-

Global value chains and digital connectivity mean that services cannot be considered alone – services must be considered with goods, and domestic regulation must be considered with services. Movement of people is also an essential consideration.

-

It is through effective implementation of the market integration agenda that regional industrial development can be promoted particularly through better functioning of regional value chains.

-

In the 21st century support services are an essential component of modern industrialisation; it is not possible to be competitive in manufacturing without competitive services inputs.

-

Industrialisation in the 21st century is about complex economic linkages and relationships that transcend traditional policy, industry/sectoral and geo-political boundaries. African industrial development is occurring in a globalised environment and the inputs into that development will not be found solely inside the borders of any one country or continent.

-

Africa’s infrastructure development programme (Programme for Industrial Development of Africa – PIDA) has to be complemented and supported by a trade in services agenda that emphasises regulatory reform/harmonisation/cooperation; after all it is the services associated with infrastructure such as road/rail/fibre networks that are inputs to production processes, to support industrial development and diversification.

tralac have engaged two expert volunteers on financial services and information communication and technology to deepen our capacity for both our training and our research. This has enabled tralac to refine our messages particularly on the importance of the regulation to trade and the development of core support services for industrial development.

For example, in the case of IT services, our observations and experiences indicate that Africa is facing significant challenges in providing ICT services and universal, affordable access. A unified approach towards a “digital single market” will not only assist in increased trade within Africa, but also strengthen Africa’s position in global trade. How have these messages been delivered?

tralac have built capacity and refined and shared the policy conclusions through the delivery of various workshops and presentations on services trade policy and industrialisation in the 21st century in the context of the CFTA.

tralac have presented to a wide range of public and private forums, including in discussions with:

-

Lesotho’s Departments of Trade and Finance

-

Namibia’s Departments of Trade, Finance and ICT

-

Regional economic communities including SADC and COMESA

-

African Union Commission, UNCTAD, UNECA

In other words, tralac has early on and throughout the CFTA process identified a both economically and politically relevant research agenda. This engagement will continue as negotiations intensify.

Outcomes and impact

tralac proactively got involved in the policy agenda and early on made sure to ensure have an impact on the CFTA negotiation process by engaging with key stakeholders and delivering messages in a timely as well as non-technical manner. It is clear that the demand for high-quality, policy-relevant and accessible research led to a continuous interest in tralac’s work, likely to contribute to well-formulated CFTA provisions on services that work with countries’ strategies of investment generation, industrial development and regional integration.

The data demonstrated the important forward and backward linkages of services in value chains, linking the debate to the fundamental challenges of Africa’s industrialisation.

Negotiations for the CFTA are ongoing, so one is not yet able to gauge how the messages have influenced the negotiating agenda. However, it is safe to say that tralac have generated debate, stimulated further engagement and given workshop participants the tools and knowledge to engage with a 21st century services trade and industrial policy agenda.

Busia One Stop Border Post (OSBP)

TradeMark East Africa

Busia is a busy border post connecting Eastern Uganda and Western Kenya, with a daily average of 210 trucks crossing to Uganda and 30 crossing to Kenya in 2013. This project aimed to reduce the time taken to cross the border by combining border clearance activities in a single location, simplifying clearance procedures, increasing coordination of controls and sharing data. A survey conducted in June 2016 showed that the average time it took to cross from Busia Uganda to Busia Kenya was reduced by 80% from 2011 while crossing in the reverse direction took 79% less time than in 2011. The World Bank’s East African Trade and Transport Facilitation Project supported the Government of Uganda and tapped the help of TradeMark East Africa. Funding was also provided by the United Kingdom, USAID and Canada according to the case story submission.

Efforts to stimulate intra-regional trade in Africa have traditionally focused on improvement of transportation infrastructure such as construction of roads, rails, ports, power and ICT. Of equal importance to complement these initiatives is the extent to which the flow of goods and movement of people along the regional trade routes is facilitated.

OSBPs enable the EAC region to improve cross border procedures leading to creation of new possibilities for economic growth and people mobility across borders. In East Africa, most border points, are a hall mark of mostly small buildings scattered across any given area, catalysed by long queues, lengthy and duplicate processes. This consequently leads to longer transit times at the borders by both people and cargo. OSBPs have made it possible to bring under one roof, various government agencies from neighbouring countries. OSBPs enable border agencies from neighbouring countries to perform joint controls that result in benefits to security, trade facilitation and human mobility. OSBPs facilitate mobility of persons and, by reducing time loss, can also reduce the cost of transport for shippers and goods to final markets accruing economic benefits across the national economic spectrum.

Uganda is keen on increasing the ease of inland transit of goods, people across borders as that is paramount to improving its competitiveness and increasing its trade to the region. World Bank’s East African Trade and Transport Facilitation Project, supported the Government of Uganda with UGX 18.5 million spread over a 4-year period, to implement the Busia OSBP. World Bank later transferred the project to TradeMark East Africa, which has overseen the completion and operationalisation of the Busia OSBP with a target of reducing the average border crossing time by 30%.

Results

Border Crossing Time Reduction: A TMEA Time and Traffic Survey, conducted in June 2016 shows significant results have been achieved due to operationalization of the Busia Uganda OSBP. The average time it takes to cross from Busia Uganda to Busia Kenya has reduced by 80% as a result of the operationalization (seventeen minutes for trucks, against a baseline of one hour, twenty six minutes in 2011) while the average time to cross from Busia Kenya to Busia Uganda has recorded a 79% reduction (two hours fifty seven minutes against a baseline of fourteen hours twenty minutes in 2011). Customs processing time for Busia Kenya reduced by 98% and for Busia Uganda by 69%.

Revenue inflows enhanced: The URA officer in charge of the Busia station, Mr. Ssozi Geoffrey indicated that since April 2016, there has been a UGShs 20Bn increase in revenue collected (from an average of UGShs 50Bn to UGShshs.70bn).Importers have benefited from faster clearance processes through taking advantage of increased round trips and increased storage space, among others.

Increased cooperation and coordination of controls: Border agencies are now more efficient as they are able to share resources such as office space and related equipment which has made them more efficient. The Ministry of Agriculture and Animal Industry had for instance never before had a computer in their offices at the border, which the TMEA support facilitated them with. Collaborating agencies as well as the business community like Uganda Clearing Industry and Forwarding Association (UCIFA) are all housed in one centre which has other amenities including restaurants that are leased out and generate income to run the facility in the future.